Preliminary Findings:

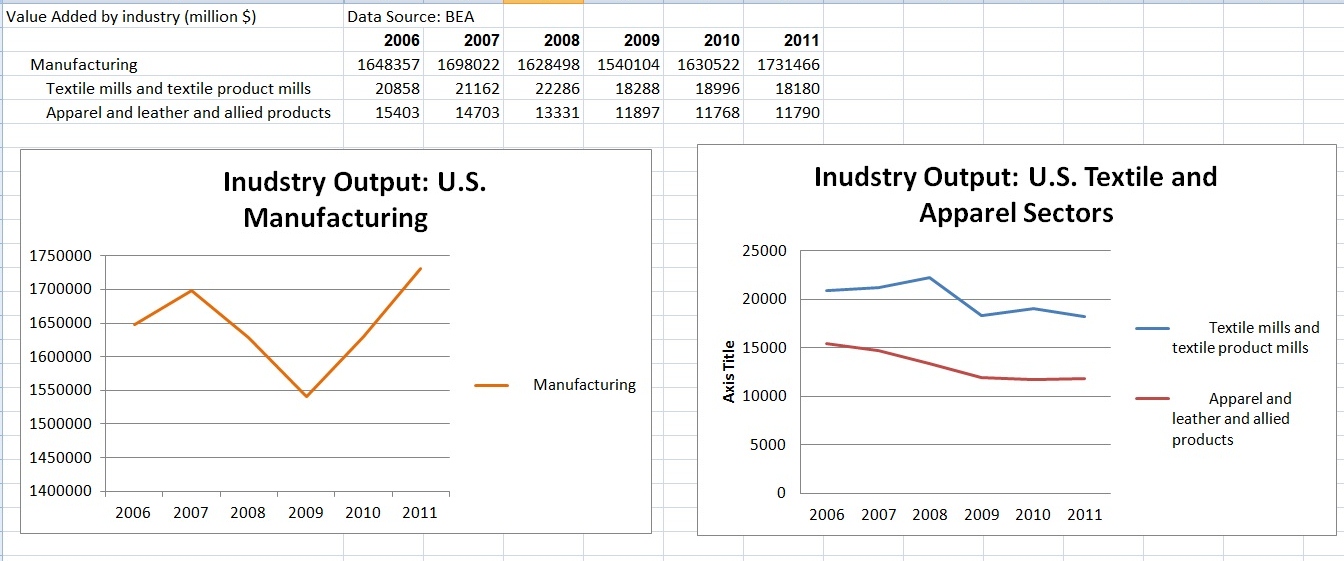

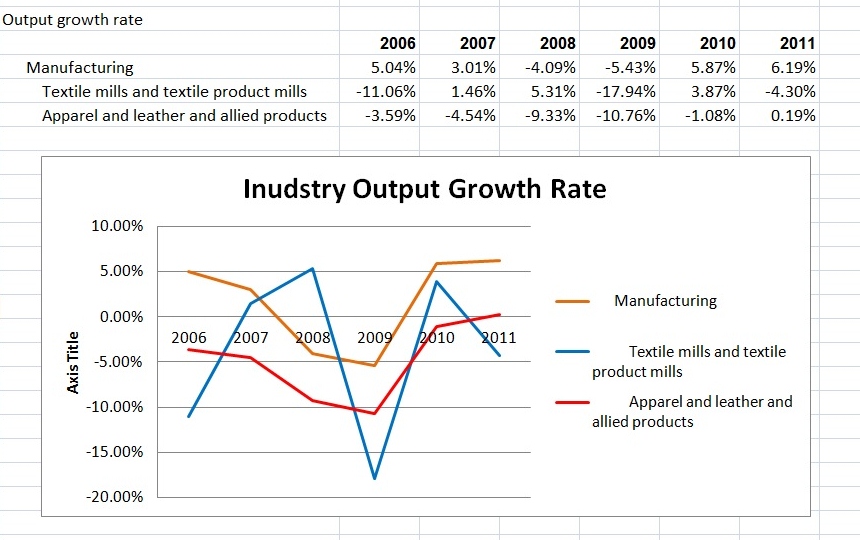

1. As suggested by numerous studies, the U.S. manufacturing sector as a whole demonstrated a robust V-shaped recovery from the 2008 financial crisis in terms of industry output. Growth rate of the industry output from 2010-2011 was also among the highest in the past 10 years.

2. There is no sign yet that textile and apparel (T&A) manufacturing is coming back to the U.S, despite suggested popularity of “insourcing” as result of rising labor cost in China. However, the decline rate of apparel manufacturing in the U.S. seemed to be slowing down.

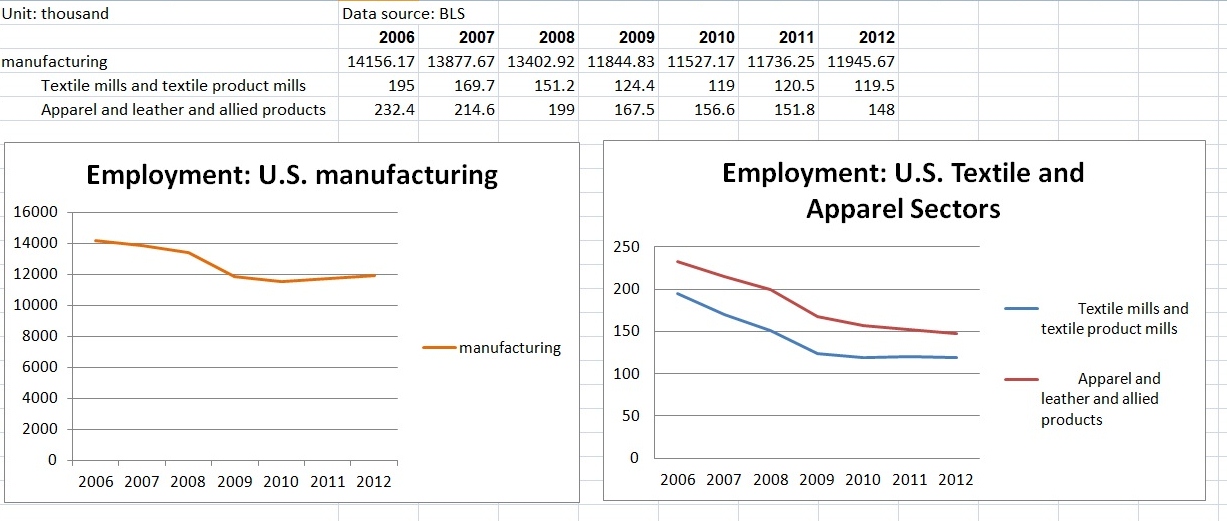

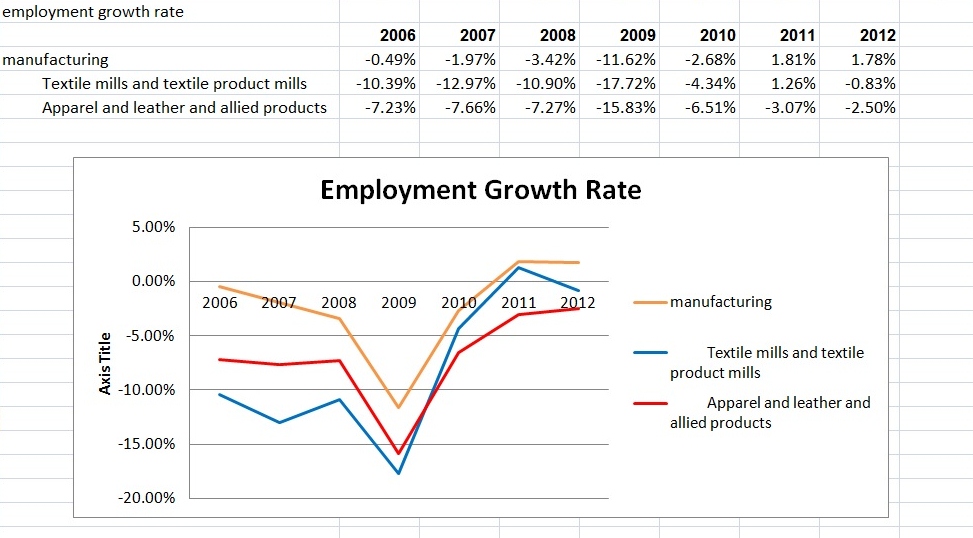

3. Jobless recovery happened both in the U.S. manufacturing sector as a whole and in the T&A manufacturing sectors. Particularly, the U.S. T&A industry respectively lost 21.0% and 25.6% of its manufacturing jobs from 2008-2012 compared with only 10.8% decline of employment in the manufacturing sector over the same period. Based on the current data, it can be concluded that a sizable return of manufacturing jobs in the U.S. T&A industry would hardly occur at least in the near future.

Sheng Lu