Q1. Since the pandemic, has the global fashion supply chain changed?

Key point: The pandemic taught fashion companies the importance of flexibility and agility in sourcing. Heavy reliance on China caused major disruptions during lockdowns, prompting companies to diversify their sourcing base and develop stronger supplier relationships to reduce various sourcing risks.

Q2. Is supply security now more important than price in sourcing decisions?

Key point: Security and sourcing are becoming more closely linked. Leading fashion companies understand that sourcing now requires balancing cost with other important factors such as flexibility, regulatory compliance, and risk management. New regulations related to sustainability demand increasingly detailed supply-chain documentation and transparency. Meanwhile, geopolitical tension between the U.S. and China further adds complexity to fashion companies’ sourcing decisions.

Q3. Are companies continuing to reduce the number of suppliers, and why?

Key point: Recent studies show that many fashion companies are diversifying sourcing beyond China, importing more from emerging supplying countries like Vietnam, Bangladesh, Indonesia, Cambodia, Pakistan, Egypt, and more. However, there are two divergent strategies: some brands expand their supplier base to spread risk and enhance capabilities in sustainable fibers, while others consolidate suppliers to strengthen partnerships with large vendors operating across multiple countries, many of which are still based in China.

Q4. Can the value chain function without China?

Key point: Not realistically. While China’s share of finished garment exports is declining, it still dominates in textiles raw materials. Even when apparel is made in other countries (like Vietnam and Cambodia), much of its fabric, investment, or ownership is Chinese. The newly released OECD data also show that about 30% of Southeast Asian apparel exports include Chinese content.

Q5. Which countries could take advantage of China’s declining role?

Key point: China’s dominance comes not only from its low costs but also from its capacity to produce almost any product category at large scale. To replicate this, companies need to use multiple sourcing locations — a “many-country model” instead of relying on just one. Therefore, diversification, rather than substitution, is the most practical approach. Firms seek to avoid over-dependence on any single country, especially given the volatility of tariffs and supply-chain disruptions.

Q6. Does “friendshoring” apply to fashion?

Key point: Politically appealing but impractical for apparel sourcing. The idea of friendshoring — trading only with “like-minded” nations — doesn’t fit with fashion’s global manufacturing system. Europe and the U.S. share values, but Europe lacks large-scale apparel production. Over 70% of U.S. apparel imports still come from Asia, where most countries are not formal U.S. allies. Therefore, political alignment cannot guide sourcing strategy in fashion; cost, capacity, and speed are more important.

Q7. Will geopolitics and the trade war reshape fashion sourcing in Europe or the U.S.?

Key point: Nearshoring remains a popular concept. European companies explore Eastern Europe and the Mediterranean; U.S. firms consider the Western Hemisphere and limited domestic production. Sustainability has emerged as the new opportunity for near-shoring. Fashion companies now aim to use more sustainable fibers in their clothing products. EU sustainability rules could also attract new investment to expand production in the EU. However, in general, small-sized firms need more resources and support to meet these high environmental standards, both to comply with the law and sustain their businesses.

Q8. Is de-globalizing production possible?

Key point: True de-globalization is unlikely. Instead, globalization is shifting toward greater transparency and accountability. Companies now need to track and report where products are made and how workers are treated, including the sourcing of raw materials. This encourages brands to work closely with their suppliers and promote stronger and strategic collaboration.

Q9. Are there enough incentives for production automation in fashion?

Key point: Yes — Automation provides a way to increase efficiency in high-wage countries like the U.S. With labor costs high and factories shrinking, machines and AI are being adopted to boost productivity and customization. Automation can also help cut down on overproduction — one of fashion’s major waste issues — by supporting made-to-order or small-batch manufacturing.

Q10. Why don’t we see full automation yet?

Key point: Cutting, sewing, and material handling today still require human labor, although factories increasingly use automated tools to boost productivity. Asian suppliers are upgrading equipment to handle smaller, faster orders. Automation is bringing back niche manufacturing (e.g., sock production in the U.S.) and supporting recycling efforts, such as sorting used garments. It helps lower minimum order quantities, matching production to uncertain consumer demand.

Q11. How can Europe maintain relevance amid the U.S.–China trade war?

Key point: Europe continues to be a key player in both textile and apparel manufacturing and consumption. Nearly half of the apparel in the EU is produced locally, often in high-wage countries like Italy, Germany, and France. Asian countries are looking for more market access to the EU because of higher tariffs imposed by the US (e.g., trade diversion). Europe also leads in sustainability and regulatory standards. Complying with EU rules often means meeting the highest global standards. Luxury branding (“Made in Italy/France”) remains highly influential, and the EU’s proactive trade agreements might even enable it to export textiles for processing in Asia, expanding supply chain integration.

Q12. Why hasn’t Africa become a viable textile hub yet?

Key point: Africa’s potential greatly relies on trade preferences like the African Growth and Opportunity Act (AGOA), which recently expired. Without duty-free U.S. access, U.S. companies are less likely to source there. However, the EU could help bridge the gap by forging partnerships for recycled textile materials and sustainable production. Regional collaboration could unlock Africa’s place in circular fashion supply chains.

For students in FASH455: Feel free to share your thoughts on any of the interview questions above. You may also challenge and debate any points raised in the interview and present your arguments.

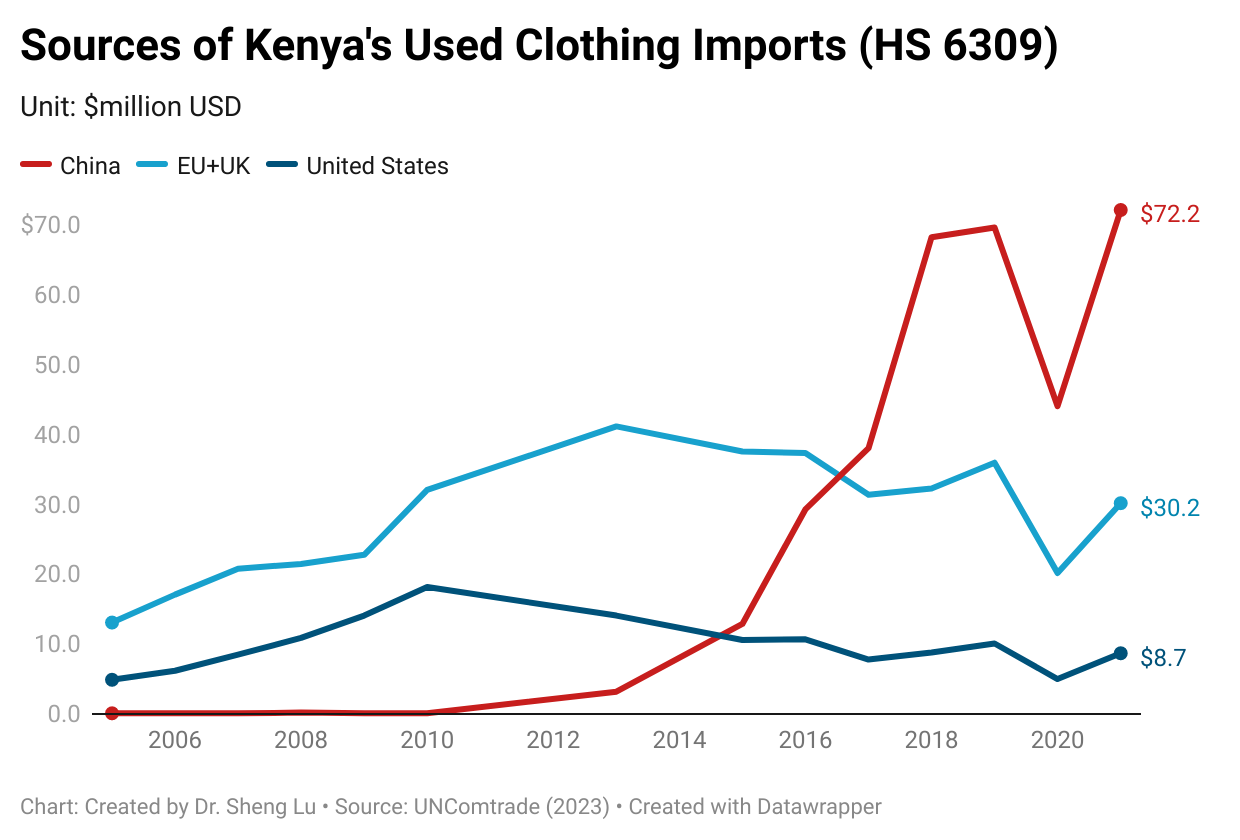

Concerns about the used clothing exports to Kenya (viewpoints from the Changing Markets Foundation)

Data from the United Nations (UNComtrade) shows that Kenya’s used clothing imports surged by over 500% from 2005 ($27 million) to 2021 ($172 million).

An overwhelming volume of used clothing shipped to Kenya is waste synthetic clothing, a toxic influx creating devastating consequences for the environment and communities. It is estimated that over 300 million items of damaged or unsellable clothing made of synthetic or plastic fibers are exported to Kenya each year, where they end up dumped, landfilled, or burned, exacerbating the plastic pollution crisis.

Interviews with used clothing traders in Kenya show that 20–50% of the used clothing in bales they purchased was unsellable due to being damaged, too small, unfit for the climate or local styles, and sometimes even with clothing that is covered in vomit, stains or otherwise damaged beyond repair.

European sorting companies often skimmed off high-quality used clothing for resale in the local EU market. They exported the lower-quality and lower-graded ones to developing countries like Kenya.

It remains challenging to recycle synthetic clothing as it often contains harmful additives or other materials that make the recycling process difficult or impossible. Additionally, the quality of the recycled synthetic fibers is typically lower than that of the original fabric (i.e., using virgin fiber).

Defend the used clothing exports to Kenya (viewpoints from the Textile Recycling Association, TRA)

Sorting, trading and selling used clothing “directly employs two million peoplein Kenya alone , with tens of millions employed globally and supporting many more employment positions in ancillary sectors.”

“Used clothing and textiles collected in the UK, should go through a detailed sorting process and can be sorted typically into 130 plus re-use and recycling grades and sometimes this can be more than 200 grades. In the sorting process each garment is picked up and individually assessed by highly trained experts*. The good quality re-useable products are segregated from the recycling grades.” [*According to Changing Markets Foundation’s report, about 36 million pieces of used clothing were exported from the UK to Kenya in 2021; All EU countries exported about 112 million pieces to Kenya]

“It is the buyers in these countries (note: countries like Kenya) that dictate the flows of (used clothing) textiles and which import the goods into their countries.”

“TRA members are required to ensure that only good quality re-usable clothing products are sold onto countries in Africa and other non-OECD countries. Recycling grades and other non-textile/clothing items have to be removed… However, the majority of countries are not subject to the same tight restrictions on trading as the UK.. This is to the extent that some countries allow unsorted used textiles containing a complete mix of re-usable items, recycling grades, and waste to be sold into African countries as a product.” “The qualities of (used clothing) items originating from different countries is likely to vary significantly.”

“Kenyan’s buy more than 10 times as much used clothing from China than they do from the UK.”

For FASH455: the blog comment assignment can address the following questions:

What is your stance on the used clothing trade? Should the government impose more export or import trade restrictions on used clothing?

As we learned in class, developing countries like Kenya are supposed to rely on making and exporting labor-intensive garments to develop their economies. Can importing used clothing lead to similar economic growth? Any evidence that can support the argument?

What are the ethical issues involved in the used clothing trade? Should government policies play a role in regulating these ethical concerns?

Could restricting the used clothing trade discourage fast fashion and reduce textile waste generation? Why or why not?

Should developed countries like the U.S. voluntarily restrict used clothing exports to lessen the economic and environmental pressures on developing countries like Kenya? What are the potential benefits and drawbacks of such a policy?

Based on the reading, what critical questions remain unanswered, and what further studies could be conducted to gather valuable information for informed decision-making on regulating the used clothing trade?

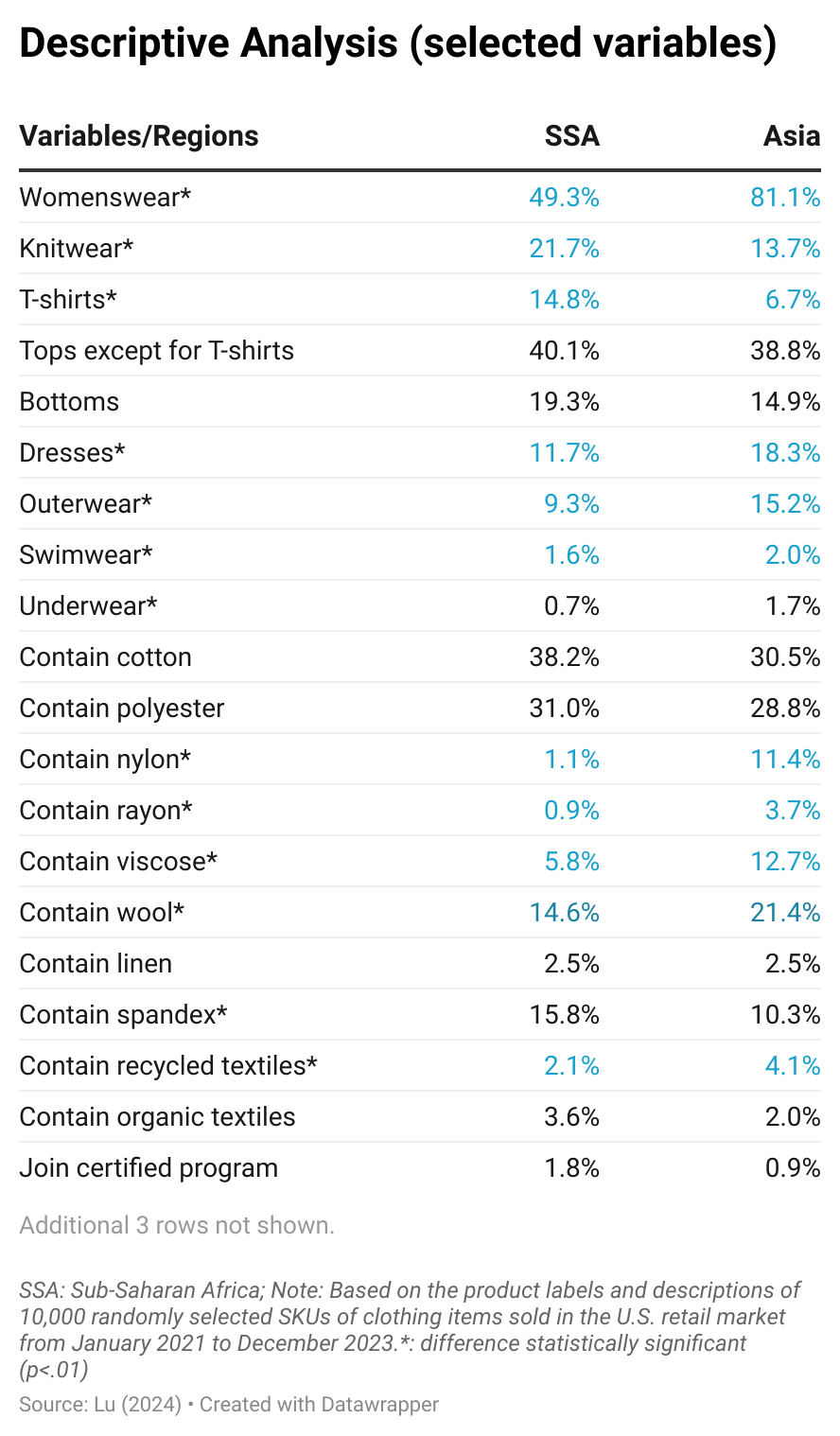

The prospect of Sub-Saharan Africa (SSA) as an apparel-sourcing base for U.S. fashion companies has been a growing heated debate. On the one hand, U.S. fashion companies, driven by increasing geopolitical concerns and other market factors, were eager to diversify apparel sourcing away from Asia. The SSA region was often regarded as one of the most popular alternative sourcing destinations thanks to its large population, relatively low labor costs, and shorter shipping distance to U.S. ports compared to most Asian. The African Growth and Opportunity Act (AGOA), a trade preference program enacted in 2000, in particular, allowed eligible apparel exports from SSA countries to enter the United States import duty-free, creating substantial financial incentives for U.S. fashion companies to source from the SSA region.

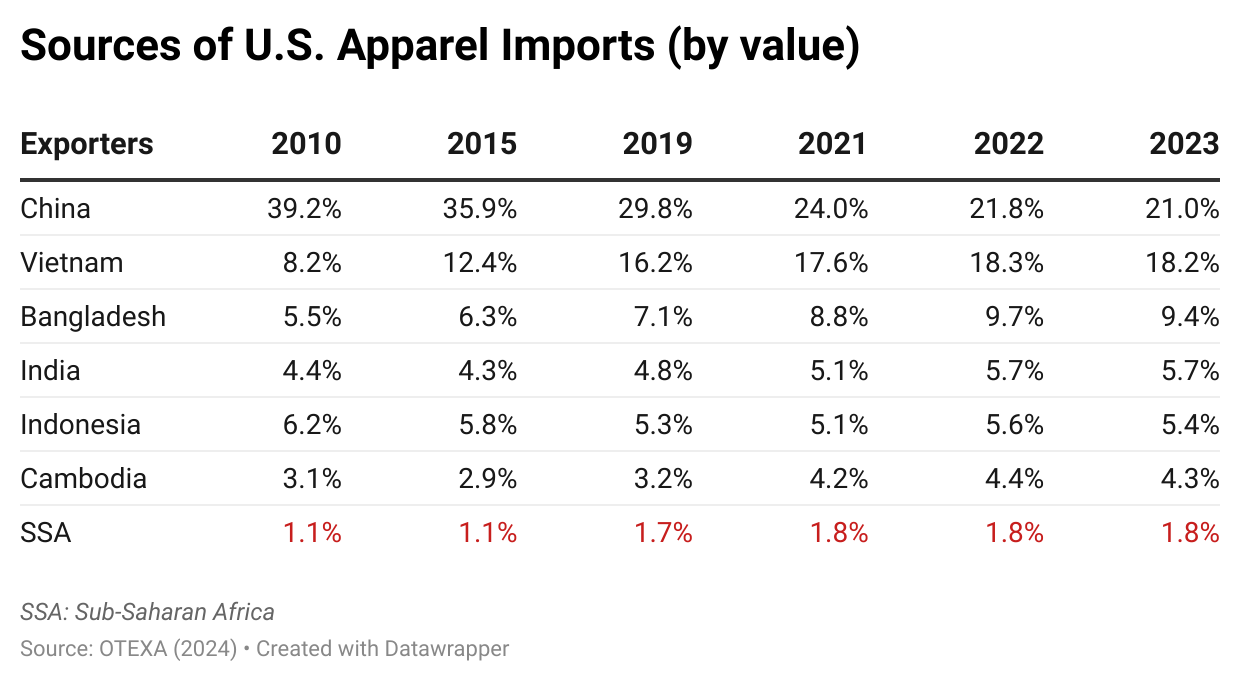

However, empirical trade data shows that U.S. apparel imports from SSA members have stagnated over the past decades without evident growth. Notably, with little change from 2010, SSA countries collectively accounted for only 1.8% of U.S. apparel imports in 2023, with no single SSA member achieving a market share of more than 1%. In contrast, over the same period, despite China’s declining market shares, the following five largest Asian suppliers—Vietnam, Bangladesh, India, Indonesia, and Cambodia—jointly accounted for 43.0% of U.S. apparel imports in 2023, a notable increase from 27.4% in 2010.

This study aims to evaluate SSA countries’ capacity to serve as an alternative apparel sourcing destination to Asian suppliers for US fashion companies. Specifically, the study examined the detailed product information of a total of 10,000 stock keeping units (SKUs) of clothing items sold in the U.S. retail market from January 2021 to December 2023. Half of these items were sourced from the six largest apparel-exporting countries in SSA: Lesotho, Kenya, Mauritius, Ethiopia, Madagascar, and Tanzania. Together, these countries accounted for over 96% of the value of U.S. apparel imports from the SSA region between 2021 and 2023. The remaining half came from China, Vietnam, Bangladesh, Cambodia, India, and Indonesia, the six largest Asian apparel exporters, which stably accounted for approximately 90% of U.S. apparel imports from Asia over the past decade.

Key findings:

First, the results revealed that U.S. fashion companies’ sourcing strategies for SSA countries appeared more subtle and complicated than simply treating the region as another low-cost sourcing destination, as suggested by previous studies. Instead, according to the results, U.S. fashion companies seemed to leverage SSA countries as suppliers of “niche products,” such as those relatively simple and basic apparel categories containing African cultural elements and targeting the luxury and premium market segment. Meanwhile, the demand for such products could be much smaller than regular apparel items sold in the value and mass market. This allows SSA countries to fulfill these smaller orders despite their limited production capacity, often family-owned or involving handmade processes.

Second, the study’s findings identified significant challenges for SSA countries serving as immediate alternatives to sourcing from Asia for U.S. fashion companies. While SSA countries could offer relatively low sourcing costs, the range of apparel products available for U.S. fashion companies to source from the SSA region remained significantly more limited than those from Asia. For example, results show that U.S. fashion companies preferred sourcing relatively basic and technologically simple categories like knitwear, T-shirts, and bottoms from SSA countries. However, imports from SSA countries offered more limited sizing and color choices and were less likely to include womenswear and relatively more sophisticated or specialized product categories such as outerwear and swimwear. As another example, U.S. apparel imports from SSA countries were primarily made of cotton and polyester, with less use of other fiber types, including nylon, rayon, viscose, wool, and those made from recycled textile materials (see table below).

Third, building on the previous point, the results call for new thinking on strengthening SSA countries’ genuine competitiveness as an apparel-sourcing destination. Over the past decades, trade preference programs such as AGOA have mainly focused on improving the price competitivenessof SSA countries’ apparel exports. However, as this study’s findings illustrate, AGOA and other trade preference programs seemed inadequate in assisting SSA countries in developing capacity beyond basic apparel categories and securing a sufficient variety of textile materials. As U.S. fashion companies have placed greater emphasis on factors beyond price in their sourcing decisions, such as flexibility, agility, sustainability, and vendors’ capability to make a wide variety of products, this could put SSA countries at even more significant disadvantages down the road to being considered alternatives to Asia for apparel sourcing.

The results also reminded us that AGOA’s liberal rules of origin, which allowed least-developed SSA countries to use textile materials from anywhere worldwide, cannot replace the crucial need to develop the local textile manufacturing capacity within the SSA region. Without a robust local textile manufacturing sector, SSA countries would encounter significant challenges in diversifying their product offerings to include more complex and versatile clothing categories, such as outerwear and women’s dresses. These categories typically require a wide variety of raw textile materials and accessories, making it highly impractical and inefficient to rely solely on imports for their supply.

On the other hand, the findings reveal the necessity of creating a stable and foreseeable business environment, such as the long-term renewal of AGOA, to attract more long-term investments in SSA. For example, investing in and strengthening SSA countries’ local supply of sustainable textile materials, such as recycled or organic fibers, could strategically enhance SSA countries’ competitiveness in meeting the increasing demand from U.S. fashion companies for sustainable apparel products.

The full article is available HERE and below is the summary:

With consumers’ growing demand for sustainable apparel products, fashion companies increasingly carry clothing made from recycled textile materials and seek additional supply bases. Recycled cotton has great potential for use in garments because of the wide availability of cotton-made secondhand clothing and the perceived positive environmental impacts of effectively recycling post-consumption cotton waste.

This study explores Egypt, Morocco, and Tunisia’s potential as sourcing bases for clothing made from recycled cotton. North African countries, including Egypt, Morocco, and Tunisia, have a long history of making and exporting cotton and cotton-made finished garments. The “developing country” status and membership in trade agreements or trade preference programs, such as the African Growth and Opportunity Act (AGOA) and the EU-Mediterranean Association Agreement, allow apparel products from these three countries to enjoy preferential duty benefits in the world’s top import markets. Therefore, there is great potential to capitalize on recycled cotton apparel and “green exports” to further promote economic development in the region.

About 13,000 Stock Keeping Units (SKUs) of clothing items made by these three countries newly launched to the world retail market between January 2022 and April 2024 were randomly captured from fashion brands and retailers’ websites. About half of the items were made of regular cotton, and the other half explicitly mentioned using “recycled cotton” in the product label or description. The results show that:

#1: Egypt, Morocco, and Tunisia have gradually expanded their clothing exports made from recycled cotton since 2022. For example, as estimated, about 1,300 SKUs of clothing using recycled cotton from these three countries were newly launched to the US and EU retail markets in 2023, a substantial increase from only 150 SKUs back in 2022 (or a sevenfold increase). Similarly, in the first four months of 2024, clothing using recycled cotton accounted for 10.2% of total cotton apparel from the three countries in the US and EU markets, a substantial increase from only 1.1% in 2022.

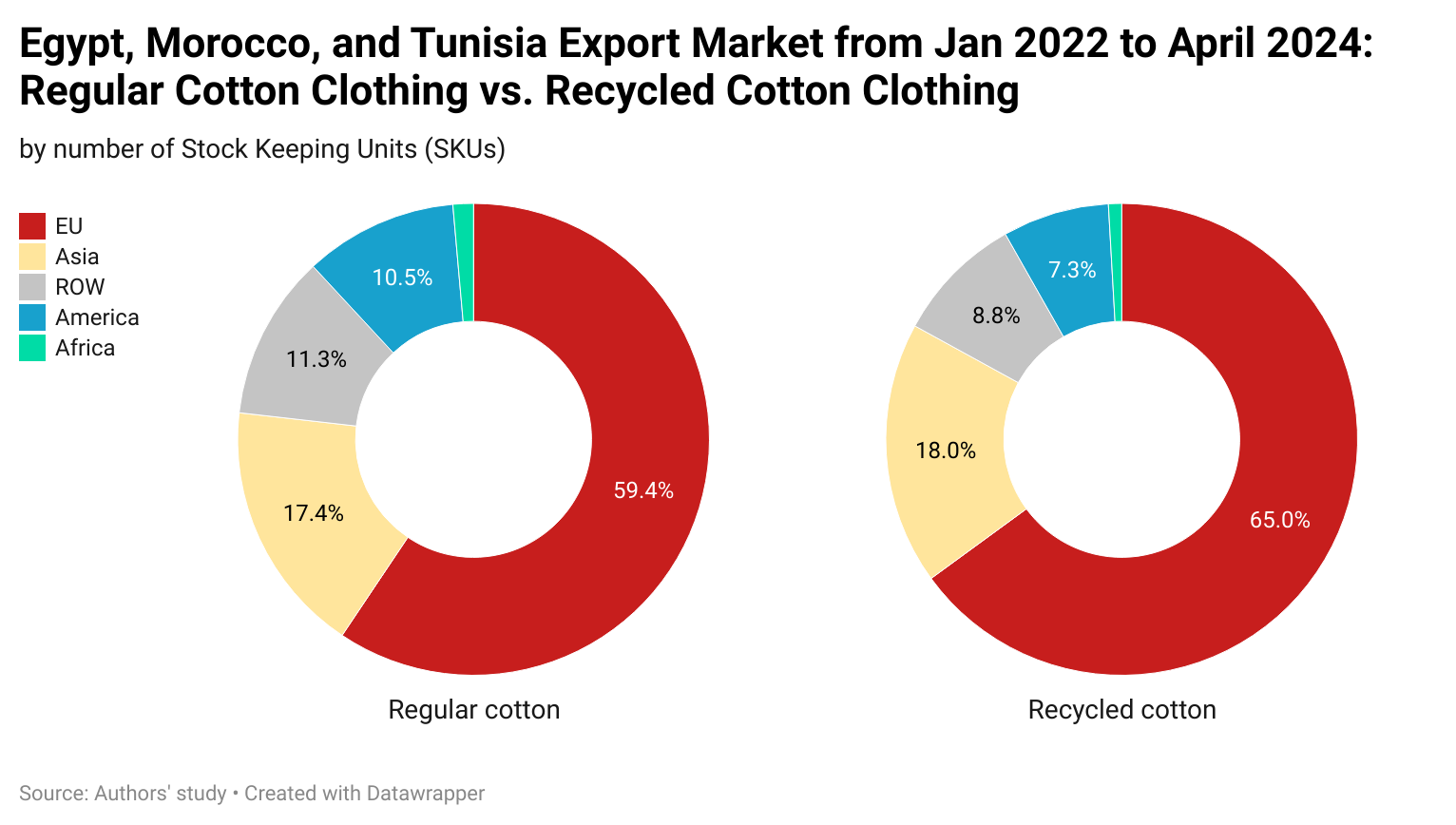

#2: Of the collected samples, apparel using recycled cotton from Egypt, Morocco, and Tunisia was destined for as many as 49 countries, reflecting the global demandfor such products. However, possibly restrained by the limited supply, the export market for clothing using recycled cotton remained less diverse than that for clothing made of regular cotton, which spanned 72 countries.

#3: Geographically, the European Union (EU) was the top clothing export market for Egypt, Morocco, and Tunisia, accounting for over 75% of these countries’ export value in 2022, according to UN trade statistics (UNComtrade). This was also the case for recycled cotton products. Specifically, the EU accounted for 65% of these three countries’ total recycled cotton clothing exports measured in SKUs in the collected samples, higher than 59.4% of regular cotton clothing products.

#4: Egypt, Morocco, and Tunisia focused on different product categories for clothing using recycled cotton than those made from regular cotton. Specifically, of the sampled items, clothing using recycled cotton had a notable concentration on bottoms (52.9%), followed by tops other than T-shirts (23.8%). Recycled cotton clothing also was more commonly used for outerwear (7.5%) than those using regular cotton (3.8%). In comparison, only about 7.9% of clothing using recycled cotton were T-shirts, much fewer than nearly 30% of those using regular cotton. Similarly, specific product categories, such as underwear and hosiery, rarely use recycled cotton. Likely, the concerns for quality and durability and the difficulty of absorbing higher production costs make using recycled cotton for these relatively simple categories more challenging.

#5: Even though cotton apparel made in Egypt, Morocco, and Tunisiaalready commonly mentioned their sustainability attributes (86%), phrases such as “sustainability” and “sustainable” appeared even more frequently in clothing using recycled cotton (94.6%). For example, some producers highlighted that they “worked with suppliers, workers, unions and international organizations” to ensure their recycled cotton clothing contributed to “the United Nations Sustainable Development Goals.” Likewise, some labels intentionally remind consumers about the positive environmental impact of using recycled cotton, “The use of recycled cotton helps to limit the consumption of raw materials.” Another added, “The production of recycled cotton recovered cotton, mainly from the production of other garments, thus reducing the production of virgin spring and water consumption, energy and natural resources.”

Meanwhile, compared to clothing using regular cotton, those made with recycled cotton in Egypt, Morocco, and Tunisia reported much higher participation incertification programs, such as the Recycled Claim Standard (RCS), which verifies the recycled content and tracks it from source to final product.

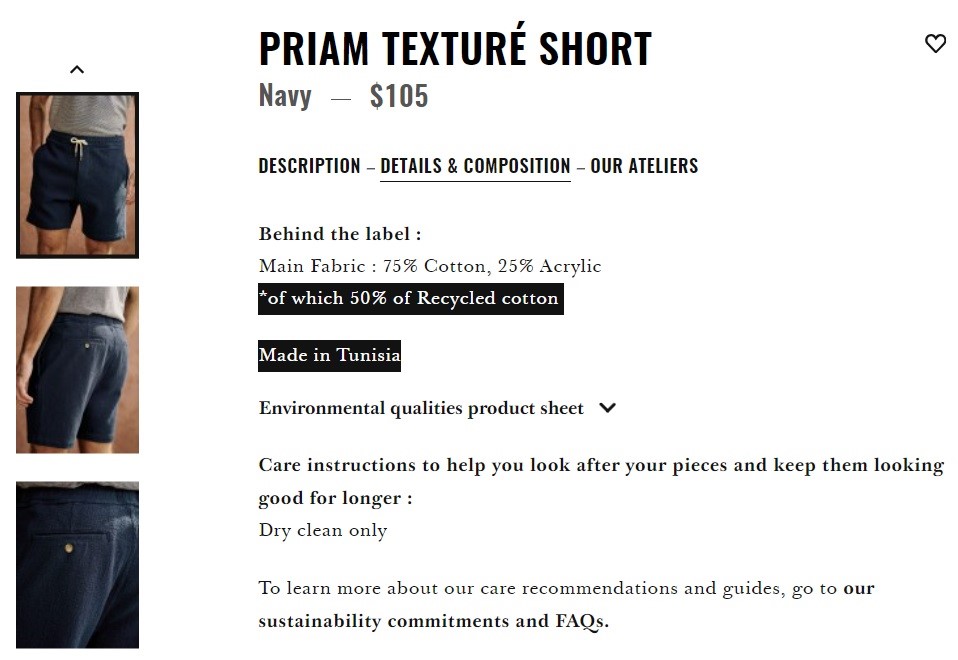

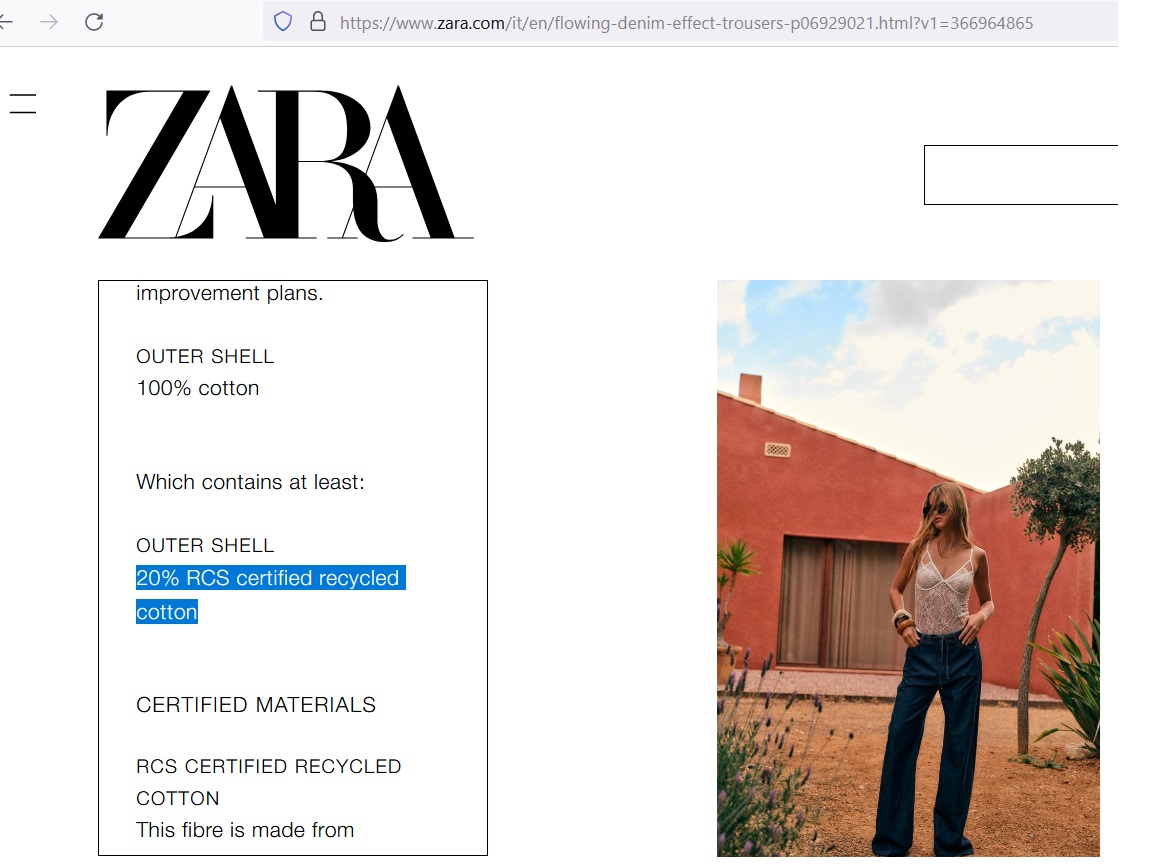

#6: Reflecting the technical limitations of the fiber property, it remains rare to have clothing that is 100% made from recycled cotton. According to industry experts, longer cotton fibers generally indicate higher quality. Since the recycling process shortens cotton fibers, regular virgin cotton or other fibers like polyester are typically used alongside recycled cotton to make fabrics smoother, stronger, and more durable. For example, common labels include descriptions such as “80% virgin cotton, 20% RCS certified recycled cotton” and “55% RCS certified recycled polyester, 45% RCS certified recycled cotton.”

#7: Except for T-shirts, in most cases, clothing made from recycled cotton in Egypt, Morocco, and Tunisia was priced lower than their equivalent using virgin fiber in the market. This is particularly the case for the premium and luxury market segments, where clothing using recycled fiber typically was 20-30% lower priced than regular clothing. The results echo the findings of numerous studies indicating that consumers are generally unwilling to pay higher prices for recycled fiber clothing as they perceive such products as lower quality and less “valuable.” Also, more needs to be done to create more financial incentives for producers in Egypt, Morocco, and Tunisia to expand the production scale and increase the use of recycled cotton in their products.

With consumers’ growing awareness of the environmental impacts of clothing production and consumption, retailers in Europe (EU) have expressed a heightened interest in selling clothing using recycled textile materials (referred to as “recycled clothing” in this study). For example, fast fashion giants like H&M and Zara and luxury brands such as Hugo Boss have started carrying recycled clothing, aiming to integrate circularity into their product designs and business models.

In the study, we examined retailers’ sourcing strategies for clothing made from recycled textile materials in five European countries, including the United Kingdom (UK), Italy, France, Germany, and Spain. These five countries represent the EU’s largest clothing retail markets, consistently accounting for over 60% of the region’s total apparel sales.

Through an industry source using web crawling techniques and manual verification, 5,000 Stock Keeping Units (SKUs) of clothing items made from recycled textile materials were randomly selected and analyzed. These items were sold by retailers in the UK, Germany, Italy, France, and Spain between January 2021 and May 2023.

The results show that Firist, EU retailers sourced clothing using recycled textile materials from diverse sources, including over 40 developing and developed countries across Asia, America, Europe, and Africa. Second, other than assortment diversity (i.e., the number of color or sizing options for a clothing item), no statistical evidence shows that developing countries had advantages over developed ones regarding product sophistication, replenishment frequency, and pricing for recycled clothing in the five EU markets. Third, a supplying country’s geographic location statistically affects the type of recycled clothing EU retailers import. For example, retailers in the five EU countries typically adopt the following sourcing portfolio by region:

Asia: relatively sophisticated clothing items (e.g., dresses and outerwear) targeting the mass and value market.

America (North, South, and Central): relatively simple clothing categories (e.g., T-shirts and socks) targeting the mass and value market.

Europe: sophisticated clothing categories primarily for the luxury or premium market

Africa: relatively simple clothing categories targeting the premium market

The findings offered new insights into the business aspects of recycled clothing, particularly regarding its intricate supply chains and leading suppliers. The study’s results have several additional important implications.

First, while existing studies often suggest “local for local” textile recycling, the study’s findings revealed promising global sourcing opportunities for clothing using recycled textile materials. Particularly, leveraging a diverse sourcing base would allow EU retailers to take advantage of each supplying country’s unique production strength regarding product categories and assortment features and more efficiently balance various sourcing factors ranging from costs and flexibility to speed to market. Meanwhile, the study’s findings indicate that many countries worldwide have begun producing and exporting clothing using recycled textile materials, and the sourcing options and capacities will hopefully continue to grow.

Second, according to the study’s findings, unlike the patterns of making regular garments using virgin fiber, low-wage developing countries demonstrated no noticeable competitive edges over developed economies regarding producing and exporting clothing using recycled textile materials. Instead, developed economies, including many high-wage Western EU countries, emerged as top suppliers and leading sourcing destinations for recycled clothing. Thus, expanding clothing production using recycled textile materials presents an exciting economic opportunity with a promising future in developed countries, where many have plans to revitalize the domestic manufacturing sector and establish a sustainable circular economy.

Third, building on the previous point, the sustained commitment of fashion brands and retailers to carry more clothing made from recycled textile materials in their product assortment could hold significant implications for the future landscape of global apparel trade and sourcing patterns. For example, whereas apparel products are predominantly exported from developing to developed countries today, more trade flows could occur between developed economies in the future, attributed to their increasing production capacity and growing demand for clothing using recycled textile materials. Similarly, major apparel exporters in Asia, such as China and Bangladesh, might assume a less dominant role as a sourcing base for recycled clothing due to their insufficient infrastructure for efficiently sorting used clothing and generating high-quality recycled textile materials.

By Leah Marsh and Sheng Lu

Discussion questions proposed by FASH455:

#1 How might EU fashion companies’ sourcing strategies change as they increase carrying clothing made from recycled textile materials?

#2 Could the US emerge as a leading sourcing destination for clothing made from recycled textile materials? What are the potential advantages and disadvantages?

#3 Is expanding clothing made from recycled textile materials the right approach to achieve fashion sustainability? What is your thought?

On April 17, 2023, the US International Trade Commission (USITC) released a new report analyzing the trade and economic impact of the African Growth Opportunity Act (AGOA). The report fulfills the investigation request by the US House of Representatives Committee on Ways and Means in January 2022.

The full report is HERE. Below are the key findings regarding the apparel sector:

The African Growth and Opportunity Act (AGOA) matters significantly to Sub-Saharan African countries (SSA)’s apparel exports to the United States

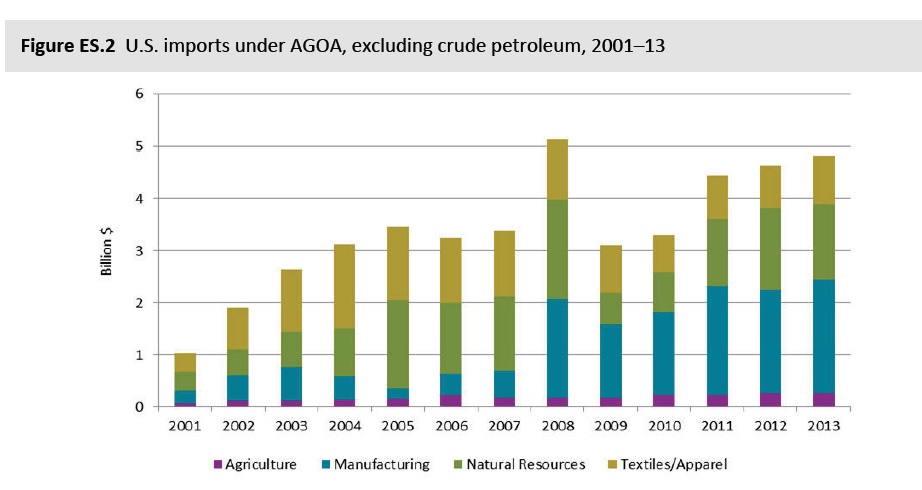

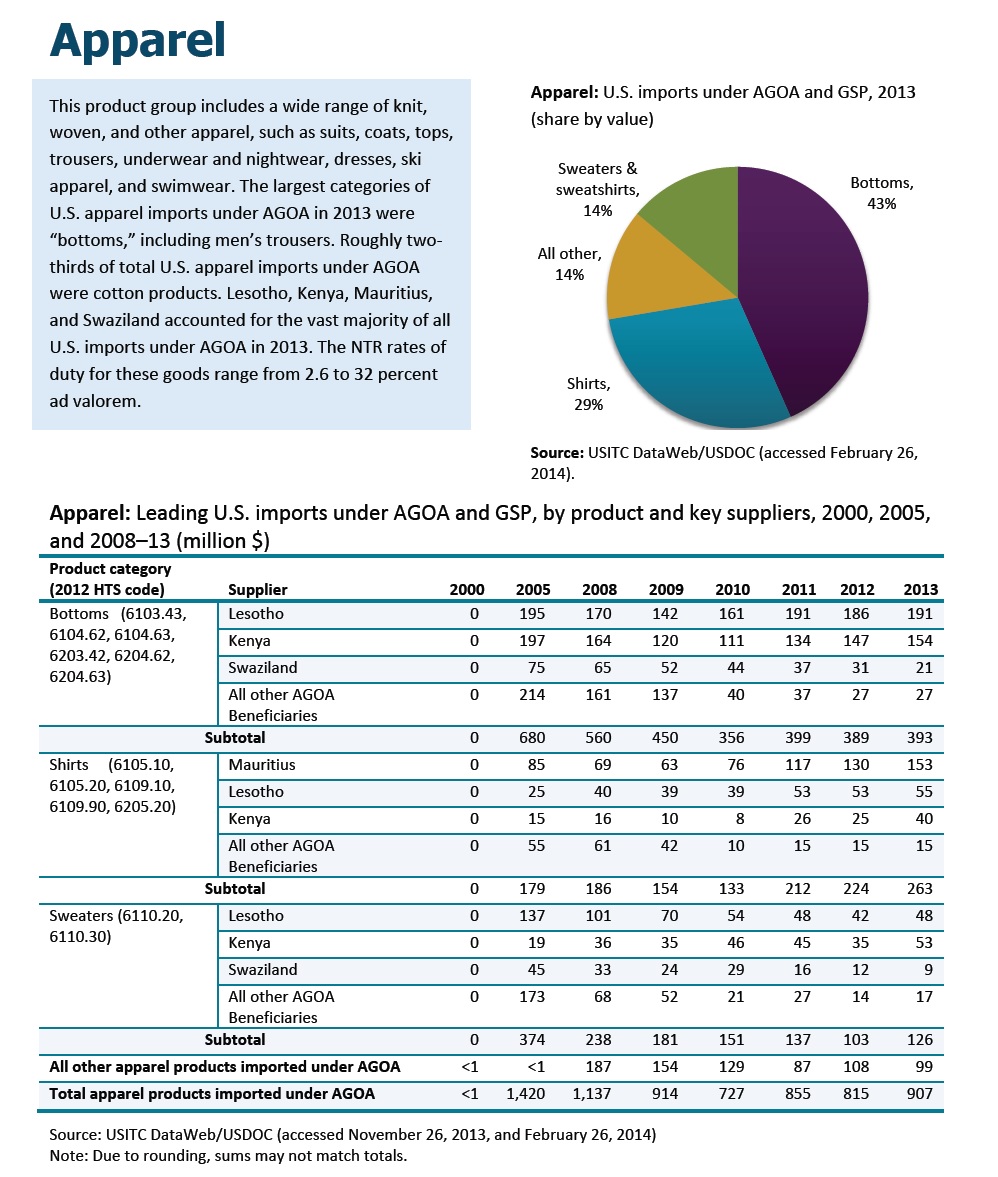

AGOA has been the primary competitive advantage for SSA’s apparel exports to the United States. For example, US apparel imports from AGOA beneficiaries have risen from $953 million in 2001 to $1.4 billion in 2021 (note: up to $1.76 billion in 2022). More than 96.4% of these imports claimed AGOA’s duty-free benefits, including 98.8% utilized the “third-country fabric” provision.

While twenty countries were eligible for AGOA’s apparel provision, over 90% of US apparel imports from AGOA members in 2021 originated in five SSA countries: Kenya (31.5%), Madagascar (19.9%), Lesotho (20.6%), Ethiopia (18.3%), and Mauritius (5.1%).

AGOA benefits appear essential for SSA countries to maintain their apparel exports to the United States. USITC noted that in every case when a country lost AGOA eligibility between 2000 and 2021, there was a noticeable decrease in US apparel imports from that country, such as Rwanda and Madagascar. (note: according to OTEXA’s latest trade data, US apparel imports from Ethiopia, which lost its AGOA eligibility in 2022, dropped by 42% in the first two months of 2023 from a year ago, far worse than a 5.8% decrease of AGOA members as a whole.)

SSA garment manufacturers often find supplying the US apparel market a better fit than Europe, primarily because US brands tend to place orders for higher volume bulk basics, which allows workers to focus on a narrower set of skills.

The impact of AGOA on SSA’s apparel production and exports varied at the country level

Some SSA countries (e.g., Kenya and Lesotho) already had well-established apparel industries when AGOA was implemented in 2000. In contrast, other SSA countries (e.g., Madagascar, Ethiopia, Tanzania, and Ghana) received substantial investments from foreign-owned firms after AGOA was enacted, which helped jumpstart their apparel sectors.

USITC also identified two “unsuccessful” AGOA cases. For example, Mauritius was the largest AGOA beneficiary apparel supplier to the United States in 2000 but has since fallen to the fifth-largest in 2021, largely due to increased labor costs. Likewise, South Africa’s apparel export to the US was negatively affected by its disqualification from the “third-country fabric” provision under AGOA.

AGOA has had a limited impact on building an integrated regional textile and apparel supply chain in SSA

Currently, SSA countries primarily participate in the cut-and-sew operations of apparel based on imported textile raw materials from outside the region (mostly from Asia).

The USITC identified several challenges in building the local textile industry in SSA. For example, building a textile mill typically requires much higher investments (e.g., $200–300 million) than a garment factory (i.e., $25 million). Also, most SSA manufacturers cannot make the various types of yarns and fabrics in demand from U.S. buyers.

The dilemma is not new: Access to textile inputs from sources outside SSA is essential for garment manufacturers in SSA to meet the specifications of US buyers. However, relying on imported textile inputs reduces the incentives for investing in new textile production capabilities in SSA.

The USITC report found Mauritius an exception as it has developed a relatively competitive capability in producing cotton fabrics, which are supplied to garment factories in Madagascar. There is also some collaboration between cotton producers in Tanzania and Uganda and Kenya’s textile manufacturers.

US fashion companies generally see SSA as a promising emerging sourcing destination

Apparel producers in SSA are less established in global apparel value chains than manufacturers in other parts of the world. Therefore, it is not uncommon that fashion brands and retailers “work more directly with SSA apparel manufacturers to ensure product quality, particularly for new or expanding product lines.”

Most SSA garment factories only have cut, make, and trim (CMT) capability and rely on imported textile materials arranged by fashion brands and retailers.

USITC found that US companies increasingly import man-made fiber (MMF) apparel from AGOA members to benefit from greater import duty savings. (note: US tariff rates for MMF apparel were typically higher than those made with natural fibers like cotton. On the other hand, however, it’s worth noting that SSA countries generally have more competitive advantages in producing cotton apparel products than in producing MMF apparel).

SSA countries also have advantages over their Asia competitors. For example, “a shipment takes about 15–18 days to travel from the port in Lomé to the East Coast of the United States. From China or Bangladesh, lead times range from 40–50 days.”

Many fashion brands “have expressed interest in sourcing from greenfield factories with fewer legacy challenges posed by compliance and environmental impacts.”

US fashion companies’ sourcing diversification strategy to avoid risk exposure also contributed to the expansion of their apparel imports from AGOA members.

Uncertainty of AGOA renewals hurt US apparel imports from SSA

Apparel companies typically make sourcing decisions 12–18 months in advance. This practice underscores the importance of renewing AGOA early rather than granting extensions only within two to nine months of expiration, as in the past.

The USITC report mentioned, “Without the assurance of the “third country fabric” provision, many US apparel companies sourced from AGOA beneficiaries reported holding back orders from the region.”

More can be done to leverage SSA’s cotton production better

Cotton growing is widespread across about thirty SSA countries. SSA accounts for about 7 percent of the world’s cotton production, the fifth-largest globally.

However, most SSA cotton is sold to international buyers and exported to Asian mills that process it into yarns and fabrics. In contrast, the consumption of domestic cotton in SSA is limited.

The SSA cotton industry produces high-quality, “sustainable” cotton that can be used in several high-value end products sold globally. However, because of a lack of mechanization, SSA cotton production struggles to increase supply to meet demand.

Also, cotton-growing regions in SSA tend to be poorer and less politically stable than other parts of the region.

Discussion questions:

Based on the blog post and class discussions, how competitive or attractive are AGOA members as apparel-sourcing destinations for US fashion companies, especially compared with suppliers from Asia and the Western Hemisphere?

Based on the blog post, what improvement can be made to make AGOA or any problems that need to be addressed?

Any other thoughts related to the patterns of apparel trade and sourcing based on the blog post?

Kekeli Ahiableis a private sector development Advisor with the Tony Blair Institute’s Industrialisation Practice. Working with industry leaders over the past 10 years, she has facilitated business and job creation opportunities in the trade infrastructure, supply chain, and manufacturing sectors across four continents.

In her current technical support role at TBI, she manages the Institute’s regional textile and apparel (T&A) project which aims to support the development of a best in class, sustainable, and circular cotton-to-apparel manufacturing hub across five West African countries.

She holds a Master of Public Policy (MPP) from the University of Oxford, with a focus on trade policy and economic development.

Interview Part:

Sheng: Thank you so much for speaking with us, Kekeli. First of all, would you please tell us a little about the Tony Blair Institute for Global Change (TBI) and your involvement with the textile and apparel (T&A) industry in West Africa?

Kekeli: Sure! The Tony Blair Institute for Global Change (TBI) is a not-for-profit organization that offers strategic advice and practical support to political leaders and governments so they can deliver reforms that raise standards and transform lives. Our work includes advising on a range of sectors including industrialization, energy, and technology. We currently work in 17 African countries.

Since 2019, we have been working with several governments in West Africa – specifically Cote d’Ivoire, Ghana, and Togo – to support the development of a best-in-class and sustainable textile and apparel sector that meets the needs of British, European, and North American retailers and consumers.

Our role has centered around supporting our partner governments to:

prepare for doing business; work with them to develop relevant sector strategy & review policy, etc.

design attractive investment incentives

attract interest in the region from relevant fashion trade actors

For instance, we facilitated a week-long investor roadshow to the three countries in 2019, with participation from three of the largest global apparel brands together with their mills and manufacturers (with a combined turnover of over US$ 70 billion). This was co-sponsored under the banner of Amcham Hongkong.

Covid-19 naturally impacted our physical scoping events and so we moved the conversations to virtual roundtable forums. Last December, eight of the UK’s biggest retailers, plus several European retailers, attended a session we organized, led by Rt Hon. Tony Blair. Representatives from the three main governments and other non-governmental groups involved in developing textiles and apparel in the region were also present to engage in discussion with the investors. We have also worked with the American Apparel and Footwear Association (AAFA) and the United States Fashion Industry Association (USFIA) to update US brands and retailers on West Africa’s potential as a nearshore sourcing destination for the North American market.

In summary, TBI is very much to help create top-of-mind awareness about West Africa’s suitability to grow a viable T&A sourcing hub and ultimately facilitate investment into the priority countries.

Sheng: What is the current state of the textile and apparel (T&A) industry in West Africa? What are the key development trends? How about the impact of COVID?

Kekeli: West Africa’s T&A market is rapidly expanding. Although considered nascent when compared to Asia’s more developed markets, its many greenfield opportunities also mean there are fewer legacy challenges to contend with. This offers a ripe opportunity for investors and manufacturers to start from an almost clean slate, which is crucial as the apparel industry makes strides toward a more environmentally sustainable footprint.

The region also has numerous natural and competitive advantages for textiles and apparel manufacturing and has seen increased interest from global actors, brands, manufacturers, infrastructure developers, development finance institutions, etc., over the last few years.

Key development trends

Recognizing shifting patterns in global T&A trade and the immense value in domestic processing of abundantly available raw materials, West African governments are demonstrating an ambition to harness their competitive advantages and expand their T&A sectors.

The governments of Cote d’Ivoire, Ghana, and Togo especially, are walking the talk. Togo’s agile government closed a ground-breaking €200 million investment deal with Arise IIP, in August 2020. The deal included building a 400-hectare eco-industrial park dedicated to textiles and apparel manufacturing. Apart from the park, the Arise group is investing into vertically integrated (fiber to fashion) knit apparel units which will start commercial operations in mid-2023.

Ghana has the most advanced industrial base of the three highlighted countries and hosts DTRT Apparel, which has been running its operation in Ghana for the past 7 years and is currently the largest apparel exporter from West Africa. As a further boost towards vertical integration, in March, they partnered on a co-creation deal with the International Finance Corporation (IFC) to jointly develop setting up a synthetic fabric mill in the region. Meanwhile, Northshore Apparel, another garment actor, recently began constructing a 10,000-worker garment factory in Ghana. To attract more foreign direct investment (FDI), the government is drafting a new T&A sector policy and incentive framework under the UK’s Foreign, Commonwealth & Development Office (FCDO) funded £16 million-pound JET Programme.

In a similar vein, Cote d’Ivoire, Africa’s second-largest cotton seed grower, is carrying out sector reforms and strategy development aimed at facilitating the domestic transformation of at least 50% of their annual cotton output.

Altogether, it is an exciting time to be developing the T&A sector in West Africa. We are excited to contribute towards this vision to create a best in class, vertical and sustainable manufacturing hub in the region, and help to create 500k direct and indirect jobs.

Impact of COVID

Most existing garment manufacturers pivoted to producing PPE for both domestic and international markets. For instance, DTRT is making this a permanent feature of their production, although orders have resumed from their traditional apparel buyers.

We have also witnessed a stronger resolve from governments to support their domestic T&A manufacturing sectors’ growth. The Togo deal, for instance, happened at the height of covid lockdowns. Some countries also offered waivers on value-add tax for their textile and apparel manufacturers and used the time to restructure their labor codes to meet international standards.

Sheng: How to understand West African countries’ competitiveness as an apparel-sourcing base for western fashion companies?

Kekeli: First, there is an immense opportunity to vertically integrate the T&A manufacturing value chain. The region produces around 1.5 million metric tons of cotton annually, which represents about 60% of Africa’s total output and 15% of global exports. The vast majority of this is exported unprocessed. Farming methods feature rain-fed irrigation with harvest done by handpicking, leading to 80% being labeled as preferred, sustainable cotton under Better Cotton Initiative (BCI) and Cotton made in Africa (CmiA) standards.

Secondly, its geographical location means it offers a natural nearshore market to Europe and US markets – literally less than two weeks away from Europe by sea.

Note: transit times are shorter depending on the shipping line. Transit references for the US are New York and Charleston, Antwerp and Hamburg for Europe, and Hangzhou for China/Asia. Source: Freightos, Bollore Africa Logistics interviews

Other benefits include an abundant trainable labor force, cost savings to manufacturers under favorable trade instruments like African Growth and Opportunity Act (AGOA), EU’s Economic Partnership Agreement (EPA)/Everything But Arms (EBA) program, etc., as well as consolidated political stability in all three countries. Moreover, there is strong potential for developing a circular textile economy facilitated by green manufacturing and initiatives like our West Africa Regeneration Zone (WARZ) initiative, on which TBI is collaborating with key brands and figures from the industry.

Apart from the main retail regions, there is a growing online retail market in Africa – estimated to increase to $75 billion by 2025 with projected $3.4 trillion aggregate GDP under African Continental Free Trade Area (AfCFTA). As we have seen with recent moves to the continent by Twitter, Google, and others, there is large scope for fashion retailers to use manufacturing in West Africa as a launchpad into this growing continental market, with free movement of goods and services under AfCFTA.

These are attractive propositions for buyers and manufacturers looking to diversify their supply chains and leave a greener carbon footprint in the process.

Sheng: It is of concern that used clothing exports from developed countries to Africa hurt the local textile and apparel industry. What is your assessment?

Kekeli: That is correct. The reality is that there is strong consumer demand for second-hand clothing, due to the cheap prices and readily available clothing for re-use. This is the main reason why the supply chains are routing the bales to other markets, including Africa. Most consumers in Africa rely heavily on the second-hand clothing markets. In this configuration, it is difficult for local players to compete and attract the same consumers’ appetites.

Moreover, this is quite complex, especially in an era of global value chains and [free] trade pacts that enjoin countries to offer some levels of reciprocity in their trade relations. Governments wishing to partake in international trade cannot simply ban imports of goods to protect their local industries. It is, therefore, crucial to explore practical win-win solutions.

For instance, there is a fast-growing global market for fabrics made from recycled materials as brands and manufacturers are taking steps to make their footprint greener. Receiver countries of second clothes could develop other business opportunities from the materials that arrive, with funding from relevant partners. Take Ghana as an example – its Kantamanto market, arguably the world’s largest reuse, repair, and upcycle market, process hundreds of tons of clothing each week. A large percentage of what comes to the market however ends up as landfilled waste due to various reasons.

One remedy is recycling, which ploughs back the many unsold and non-reusable clothes into the textile manufacturing economy. This not only reduces the need for virgin fibers but with the scale envisioned for the West Africa T&A manufacturing project, it increases the fabric feedstock available for domestic Cut, Make, Trim (CMT) manufacturers thus supporting to differentiate the region as a destination for circular apparel sourcing. Managed properly, we envision this would have positive spillover effects on the domestic market. At TBI, we published a piece on tackling Ghana’s textile waste which can be read here for a deeper dive into the subject.

Sheng: How does the textile and apparel industry in West Africa embrace sustainability?

Kekeli: The strongest aspect is from an environmental perspective. With rain-fed irrigation, around 80% of the region’s cotton is labeled as preferred cotton. Vertically integrating the cotton value chain by processing within one geographical area supports a lower carbon footprint of each final product.

West Africa’s geographical proximity to main buyer markets also increases its environmental sustainability credentials as a nearshore market.

Moreover, circularity is part of the culture in this part of the world – people reuse and pass on clothes to other family relations after use, with very little going to waste. We see an opportunity to scale this with the West Africa regeneration (WARZ) initiative. The WARZ initiative aims to support the development of a sustainable and circular textile and apparel supply base in West Africa where post-consumer textile waste is recycled at scale and becomes feedstock for making new apparel. This would be underpinned by disruptive recycling and traceability technology.

In our role as non-vested convenors and facilitators, we have convened a consortium of international and domestic stakeholders to develop a pilot project in Ghana, which is the world’s number two importer of second-hand clothing. Preliminary scoping puts the entire project size at over US$500 million with the potential to generate over 60K jobs along the value chain over the next 5-10 years. The following image depicts the initial concept for the regeneration zone project:

Relatedly, to demonstrate emerging support at the continental level, the African Development Bank recently approved the establishment of a €4 million Africa Circular Economy Facility to drive integration of the circular economy into African efforts to achieve nationally defined contribution targets.

Sheng: How important are trade preference programs like the African Growth and Opportunity Act (AGOA) to the development of the textile and apparel industry in West Africa? Do you think AGOA should be extended after 2025? Should the agreement keep the liberal “third-country fabric” rules of origin? Why or why not?

Kekeli: Trade preference programs are extremely important to facilitate the growth of Africa’s manufacturing and export capacity. As fundamentals like infrastructure tend to be less developed on the continent, preferential regimes like AGOA serve as a key enabler for manufacturing FDI. The T&A industries in countries like Kenya, Lesotho, and Madagascar have grown tremendously in the past few years thanks to AGOA’s tariff-free concessions. West Africa’s T&A industry is now in the beginning stages of development and needs an extension of AGOA to grow.

I believe in the short-medium term, maintaining third-country fabric rules is also crucial (note: Third-country fabric rules allow for apparel made with fabrics sourced from outside the AfCFTA/Sub-Saharan Africa region to qualify for duty-free access). The simple reason is that West Africa’s cotton value chain needs support to develop. While countries have ambitions for vertical integration by processing cotton within the region, these backward linkages will take time to develop.

A phase-out period may be negotiated to further incentivize accelerating the move towards domestic production of fibers that qualify to be used by CMT manufacturers in the [sub]-region.

Sheng: What does the African Continental Free Trade Area (AfCFTA) mean for the textile and apparel industry in West Africa?

Kekeli: The AfCFTA pact aims to form the world’s largest free trade area by connecting almost 1.3bn people across 54 African countries. The goal is to create a single market for goods and services to deepen the economic integration of Africa, with a combined GDP of around $3.4 trillion.

Historically, the most developed world regions have been those that have figured out and developed strong regional value chains. The EU, which is the world’s largest regional trade agreement (RTA) by value has over 64% of trade taking place within the regional block. Similar cases pertain in the US-Mexico-Canada (USMCA) and the Association of Southeast Asian Nations (ASEAN) free trade areas.

Intra-Africa trade on the contrary is currently under 20%, with strong potential for growth. Trade figures show that when African countries trade with each other, it is mostly intermediate or finished goods, which naturally have more value. The goal is to encourage more of this.

Textiles and apparel development in West Africa has strong potential to become a flagship example of what AfCFTA implementation could practically look like. In the next couple of years, I envision fabrics from Cote d’Ivoire, Benin, being exported to Ghana duty-free to feed apparel factories, designers from Cote d’Ivoire offering their expertise across the sub-region with no restrictions on their movement, textiles from Ghana being traded in Nigeria, etc. The possibilities are truly endless.

The virus is here to stay. What steps the companies must take to mitigate its impact?

Sheng: Earlier this year, I, together with the US Fashion Industry Association, surveyed about 30 leading US fashion brands and retailers to understand COVID-19’s impact on their sourcing practices. Respondents emphasized two major strategies they adopted in response to the current market environment. One is to strengthen the relationship with key vendors, and the other is to improve flexibility and agility in sourcing. These two strategies are also highly connected. As one respondent told us “We’re adjusting our sourcing model mix (direct vs. indirect) & establishing stronger strategic supplier relationships across entire matrix continue to build flexibility and dual sourcing options.” Many respondents, especially those large-scale fashion brands and retailers, also say they plan to reduce the number of vendors in the next few years to improve operational efficiency and obtain greater leverage in sourcing.

Which are the countries benefitting out of the US-China tariff war and why?

Sheng:The trade war benefits nobody, period. Today, textiles and apparel are produced through a highly integrated supply chain, meaning the US-China tariff war could increase everyone’s production and sourcing costs. Back in 2018, when the tariff war initially started, the unit price of US apparel imports from Vietnam, Bangladesh, and India all experienced a notable increase. Whereas companies tried to switch their sourcing orders, the production capacity was limited outside China. Meanwhile, China plays an increasingly significant role as a leading textile supplier for many apparel exporting countries in Asia. Despite the trade war, removing China from the textile and apparel supply chain is impossible and unrealistic.

How do you compare the African and Asian markets when it comes to sourcing and manufacturing? Which are the advantages both offer?

Sheng: Asia as a whole remains the world’s dominant textile and apparel sourcing base. According to statistics from the United Nations (i.e., UNComtrade), Asian countries as a whole contributed about 65% of the world’s total textile and apparel exports in 2020. In the same year, Asian countries altogether imported around 31% of the world’s textiles and 19% of apparel. Asian countries have also established a highly efficient and integrated regional supply chain by leveraging regional free trade agreements or arrangements. For example, as much as 85% of Asian countries’ textile imports came from other Asian countries in 2019, a substantial increase from only 70% in the 2000s. With the recent reaching of several mega free trade agreements among countries in the Asia-Pacific region, such as the Regional Comprehensive Economic Partnership (RCEP), the pattern of “Made in Asia for Asia” is likely to strengthen further.

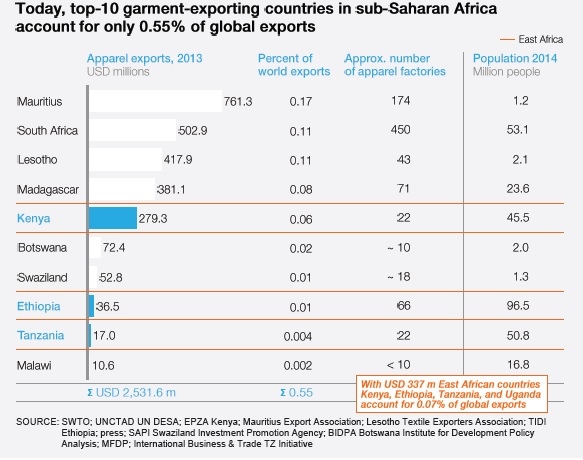

In comparison, only about 1% of the world’s apparel imports come from Africa today. And this percentage has barely changed over the past decades. Many western fashion brands and retailers have expressed interest in expanding more apparel sourcing from Africa. However, the tricky part is that these fashion companies are hesitant to invest directly in Africa, without which it is highly challenging to expand African countries’ production and export capacity. Political instability is another primary concern that discourages more investment and sourcing from Africa. For example, because of the recent political turmoil, Ethiopia, one of Africa’s leading apparel sourcing bases, could be suspended for its eligibility for the African Growth and Opportunity Act (AGOA). Without AGOA’s critical support, Ethiopia’s apparel exports to the US market could see a detrimental decline. On the other hand, while these trade preference programs are crucial in supporting Africa’s apparel exports, they haven’t effectively solved the structural issues hindering the long-term development of the textile and apparel industry in the region. More work needs to be done to help African apparel producers improve their genuine export competitiveness.

Another issue is Brexit. Is that having any significant impact on the sourcing scenario of the world or is it just limited to the European nations?

Sheng: Despite Brexit, the trade and business ties between the UK and the rest of the EU for textile and apparel products continue to strengthen. Thanks to the regional supply chain, EU countries remain a critical source of apparel imports for UK fashion brands and apparel retailers. Nearly 35% of the UK’s apparel imports came from the EU region in 2019, a record high since 2010. Meanwhile, the EU region also is the single largest export market for UK fashion companies—about 79% of the UK’s apparel exports went to the EU region in 2019 before the pandemic.

However, trade statistics in the short run may not fully illustrate the impacts of Brexit. For example, some recent studies suggest that Brexit has increased fashion companies’ logistics costs, delayed customs clearance, and made talent-hiring more inconvenient. Meanwhile, Brexit provides more freedom and flexibility for the UK to reach trade deals based on its national interests. For example, the UK recently submitted its application to join the Comprehensive Progressive Agreement of the Trans-Pacific Partnership (CPTPP). The UK is also negotiating a bilateral trade agreement with the United States. The reaching of these new trade agreements, particularly with non-EU countries, could significantly promote the UK’s luxury apparel exports and help the UK diversity its source of imports.

How do you think the power shortages happening across Europe, China, and other nations, are going to impact the apparel supply chains?

Sheng: One of my primary concerns is that the new power shortage could exacerbate inflation further and result in a more severe price hike throughout the entire textile and apparel supply chain. When Chinese factories are forced to cease production because of power shortage, the impact could be far worse than recent COVID-related lockdowns in Vietnam and Bangladesh. As mentioned earlier, more than half of many leading Asian apparel exporting countries’ textile supplies come from China today. Also, no country can still compete with China in terms of the variety of apparel products to offer. In other words, for many western fashion brands and retailers, their stores and shelves could look more empty (i.e., having less variety of products to sell) because of China’s power shortage problem.

#1 Based on the readings, why or why not do you think Africa is on the right track to become the next hub for apparel sourcing for western fashion brands?

#2 Based on the readings, do you think that any of the countries/regions discussed can become the “next China?” If so, what are the challenges faced by these exporters that have been gaining market shares (such as Vietnam and Bangladesh)?

#3 Why is Asian companies investing the most into the apparel industry in Sub Saharan Africa (SSA) rather than U.S. or EU investors? Notably, the African Growth and Opportunity Act (AGOA) is a trade preference program between the U.S. and SSA countries.

#4 If the punitive tariffs on Chinese goods are removed next year, why or why do you think U.S. retailers will increase apparel sourcing from China again?

#5 To which extent do you think the comparative advantage theory can explain the evolving world textile and apparel trade patterns?

#6 What policies or strategies could the US government use to convince companies to invest in the Sub-Saharan African region instead of countries like China and Vietnam?

Debate on used clothing trade

#7 Did you feel that the United States really explored every and any possible solution before deciding to suspend Rwanda’s eligibility under the AGOA? If not, what more could they have done or done differently?

#8 The US-EAC trade dispute on used clothing import ban is a very multilayered matter, which can be broken down with the help of trade preference programs. How can we improve the effectiveness of these trade preference programs and revolutionize them to become more significant in today’s economy?

#9 EAC countries are having a difficult time developing their local textile and apparel industry due to the large amounts of used clothing being imported and even proposed a high tariff to lower the amount of clothing being imported. Do you believe the ban on used clothing is the only option they have left for economic growth? If not, what are some ideas of ways they can grow their economy?

#10 The EAC countries have shown their unwillingness to used clothing trade. However, the US has presented that they are indifferent to regulate the used clothing trade as they are one of the biggest used clothing exporters. Are there any solutions to achieve the win-win situation on used clothing trade?

#11 The used clothing ban is put in place in order to develop the apparel and textile industry, but there needs to be more education for countries on sustainability. There is a big stigma about used clothing that needs to be abolished as well. An alternative to this ban is allowing used clothing, but also creating new clothing more sustainably so apparel and textile companies can profit. What are some other sustainable alternatives that benefit both sides?

#12 Given the debate on used clothing trade and its impact on East African nations, will you continue to donate used clothing? Why or why not?

[For FASH455: 1) Please mention the question number in your comments; 2) Please address at least TWO questions in your comments]

The original interview (in Spanish) is available HERE. Below is the translated version.

Question: Is there a reversal in the globalization of fashion?

Sheng Lu: The fashion industry is becoming more global AND regional — the making and selling of a garment “travel” through more and more countries. Just look at the label of a Gap sweatshirt: it is an American clothing brand, but the product is “Made in Vietnam,” and the label includes the size standards in six different countries. The business model of the fashion industry today is “making anywhere in the world and selling anywhere in the world.”

Q .: What do you mean the industry is becoming more “regional”?

Sheng Lu: The trade flows of textiles and apparel today are heavily influenced by regional free trade agreements (FTAs). For example, while China is known as the world’s largest apparel producer and exporter, nearly 50% of the clothing consumed by European consumers are still produced by EU countries themselves. Notably, consumers have different expectations for clothing: many are price-sensitive, but others prefer more trendy items, which requires “near sourcing”—this explains why fashion companies have to adopt a more balanced sourcing portfolio.

Q .: Is the price still the most important factor in fashion companies’ sourcing decisions?

Sheng Lu: Sourcing is far more than just about chasing for the lowest cost. Sourcing decisions today have to consider a mix of factors, ranging from flexibility, speed to market, sustainability, to compliance risks. In fact, few companies “put all eggs in one basket.” My recent studies show that both in the United States and the EU, fashion companies with more than 1,000 employees, typically sourced from more than twenty different countries—sometimes even exceed forty. Behind such a diversified sourcing practice is the necessity to strike a balance between so many different sourcing factors.

Q .: Is apparel sourcing becoming more diversified today than a decade ago?

Sheng Lu: From my observations, fashion companies are souring from more countries and regions than a decade ago, but not in terms of producers. Especially in the last two or three years, I see some large companies are consolidating their supplier base to build a closer relationship with key vendors. The reason is the same as mentioned earlier: a very competitive price is not enough for apparel sourcing today.

Q .: How has the tariff war between the United States and China affected apparel sourcing?

Sheng Lu: The trade war between the United States and China is having big impacts on apparel sourcing that go beyond the two countries. Notably, American fashion brands and retailers are moving sourcing orders from China to other Asian countries such as Vietnam and Bangladesh. However, finding China’s alternatives is anything but easy. Despite the tariff war, China remains a competitive player in apparel sourcing. The unparalleled production capacity that can fulfill orders nearly for any products in any quantity, and the ability to comply with complex sustainability and social responsibility regulations are among China’s unique competitive advantages. Understandably, companies are not giving up sourcing from China, as there are few other “balanced” sourcing destinations in the world. That being said, it is important to recognize that the big landscape of apparel sourcing is evolving. Even in Europe, which is not having a trade war with China, apparel “Made in China” is seeing a notable decline in its market share.

Q .: How is China adapting?

Sheng Lu: The textile and apparel industry in China is undergoing a structural change. Partially caused by the tariff war, apparel producers in China are increasingly moving their factories to nearby Asian countries (especially for big-volume and/or relatively low value-added product categories). Meanwhile, China itself is changing from an apparel producer to become a leading textile supplier for other apparel-exporting countries in Asia. This is NOT a temporary move, but a permanent transition, which has happened in many industrialized economies in history. Somehow, the tariff war has accelerated the adjustment process, however.

Q .: Will Africa be the next hub for apparel sourcing in the near future?

Sheng Lu: As textile and clothing trade is turning more regional-based, Africa is facing significant challenges to become an attractive tier-1 sourcing base for Western fashion brands and apparel retailers.

Q .: Why is that?

Sheng Lu: In general, there are three primary apparel import markets in the world: the United States, the European Union, and Japan—as of 2018, these three regions altogether still accounted for as many as 70% of the world apparel imports. Surely, Asian countries are important apparel suppliers for all these three regions. However, each of these three markets also has its respective regional suppliers—Mexico and Central & South American countries for the United States, China, and a few Southeast Asian countries for Japan and Eastern European countries for the EU market. Other than geographic proximity, often, these regional suppliers also enjoy preferential market access to the US, EU, and Japan provided by regional free trade agreements.

Africa, on the other hand, is not close to any of these three major apparel import markets geographically. Why would fashion companies in the United States, Japan, or the EU have to source from Africa when there are so many other options available?

Q .: For price?

Sheng Lu: Several trade preference programs currently offer apparel exporters in African countries preferential or duty-free market access to the United States, the EU, and Japan (such as the African Growth Opportunity Act and the EU and Japan Generalized System of Preferences programs). However, sourcing from Africa will entail other extra costs—for example, the raw material cost will be higher as yarns and fabrics have to be imported from Asia first, and the transportation bill could be costly due to the poor infrastructure. Further, not like their counterpart in Asia, the apparel industry is not regarded as a development priority in many African countries, which continue to rely heavily on the export of raw materials instead. Manufacturing for the local market is also complicated—apparel producers in Africa are struggling with both the cheap clothing imported from Asia and the mounting used clothing sent from the West.

Q .: It is said that fashion might be the most regulated sector in international trade other than agriculture. How to explain this?

Sheng Lu: I think we need some changes here. For example, in 2018, textiles and apparel accounted for only 5% of the total U.S. merchandise imports but contributed nearly 40% of the tariff revenue collected. This phenomenon, which makes no sense economically, is the result of the industry lobby—trying to protect domestic manufacturers from import competition.

As another example, around 15%-17% of Mexico’s clothing exports to the United States do not claim the duty-free benefits provided by the North American Free Trade Agreement (NAFTA), as the NAFTA rules of origin strictly require the using of regional yarns and fabrics for qualified apparel items. In the end, companies prefer bigger savings on the raw material cost than claiming the NAFTA duty-saving benefits. We should think about how to modernize these trade rules and make them more supply-chain friendly in the 21st century.

Meanwhile, policymakers are developing new regulations to address some emerging areas in international trade, such as E-commerce, labor standards and environmental protection. Increasingly, trade policy is moving from “measures at the border” to “measures behind the borders.”

Sub-Saharan Africa (SSA) is widely regarded as a growing apparel-souring destination. Particularly, U.S. Congress established theAfrican Growth and Opportunity Act (AGOA), a non-reciprocal trade preference program, in 2000, to help developing SSA countries grow their economy through expanded exports to the United States. Because apparel production plays a dominant role in many SSA countries’ economic development, apparel has become one of the top exports for many SSA countries under AGOA. Notably, the “third-country fabric provision” under AGOA allows US apparel imports from certain SSA countries to be qualified for duty-free treatment even if the apparel items use yarns and fabrics produced by non-AGOA members, such as China, South Korea, and Taiwan. This special rule is deemed as critical as most SSA countries still have no capacity in producing capital and technology-intensive textile products.

That being said, to play a bigger role as an apparel sourcing base, SSA is not without significant challenges:

Challenge 1: limited industry upgrading and local textile production capacity

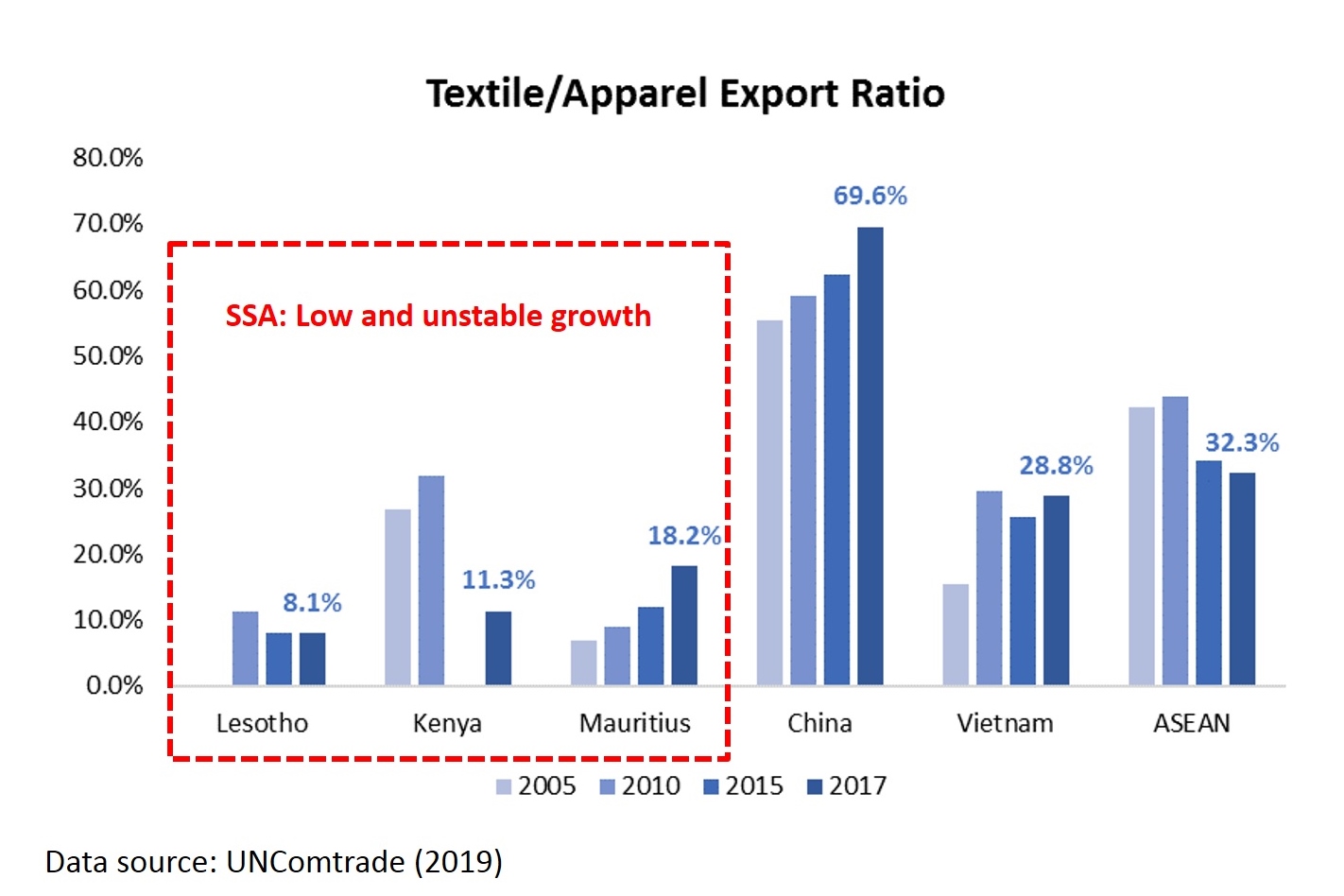

Theoretically, as a country’s economy advances, it should gradually be producing and exporting more capital and technology-intensive textiles versus labor-intensive apparel products. This is the notable trends in many Asian countries (such as China and Vietnam), where the textile/apparel export ratio has been rising steadily between 2005 and 2017. However, as a reflection of the stagnant industry upgrading, the textile/apparel export ratio remains fairly low in SSA, including in Lesotho, Kenya, and Mauritius, the top three largest apparel exporters in the SSA region.

Challenge 2: Slow and no progress in export diversification

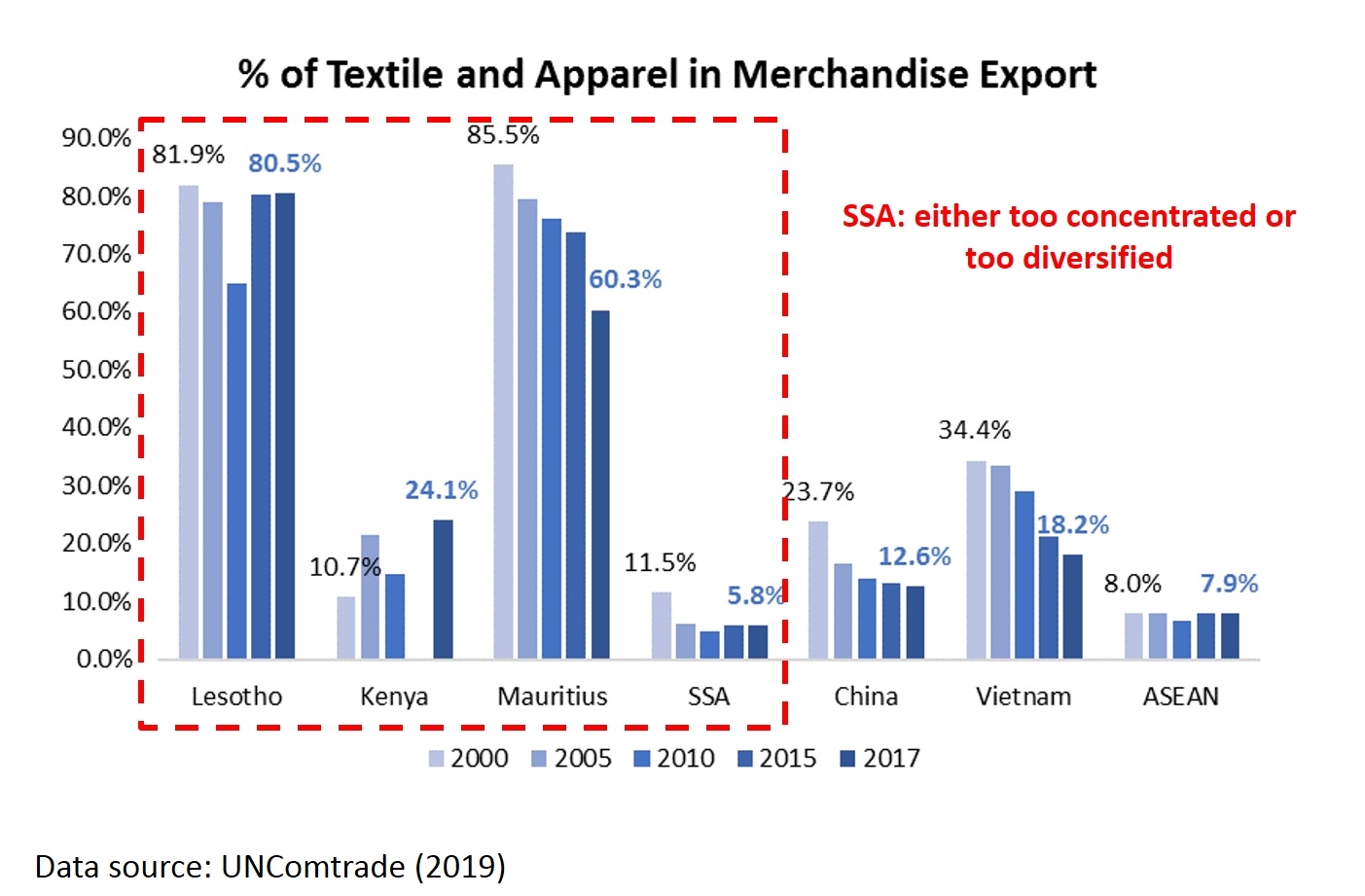

Ideally, as the economy becomes more sophisticated, textiles and apparel (T&A) should account for a declining share in a country’s total merchandise exports. Countries such as China, Vietnam, and ASEAN demonstrate perfect examples. However, in some SSA countries (e.g., Lesotho), T&A has stably accounted for over 80% of their total merchandise exports over the past 17 years, a sign of slow or no progress in export diversification. In other SSA countries, T&A accounted for less than 10% of their total merchandise exports, suggesting the sector is not a priority to the local economy.

Challenge 3: Intense competition both in key export markets and domestic market

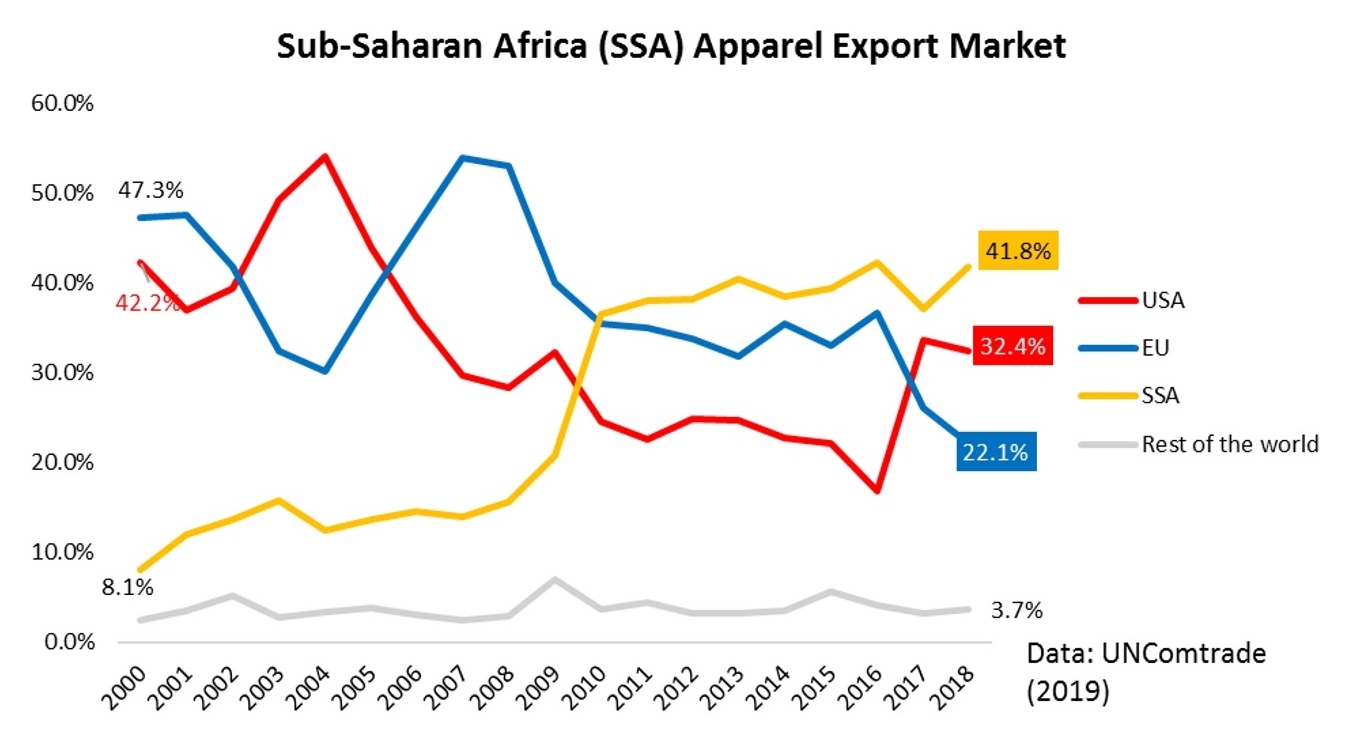

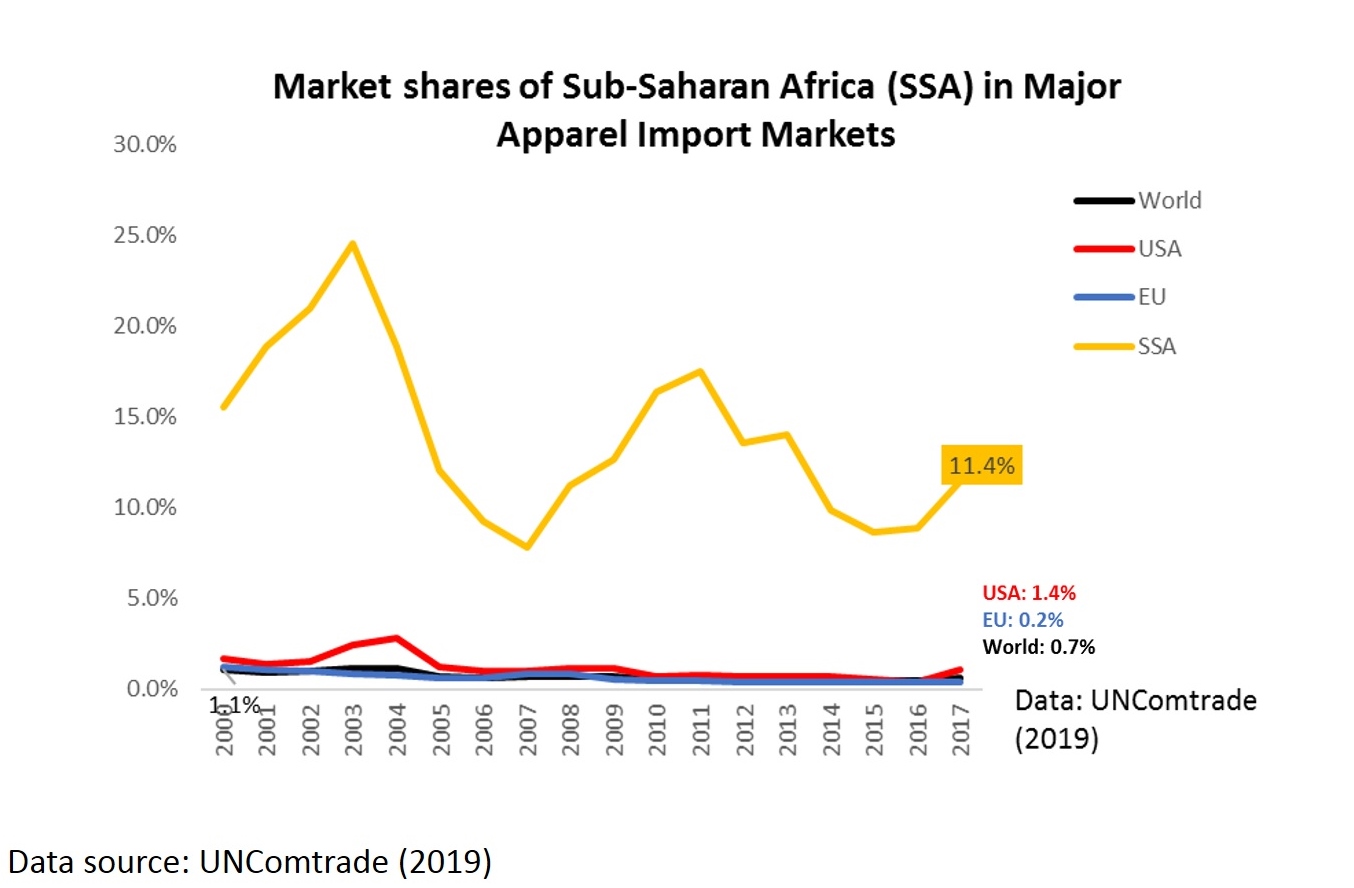

As of 2017, over 96% of SSA countries’ T&A exports went to three markets: the United States, the EU, and other SSA members. However, because of the intense competition, except for the regional SSA market, SSA countries account for merely 1.4% and 0.2% of total U.S. and EU textile and apparel imports in 2017 respectively.

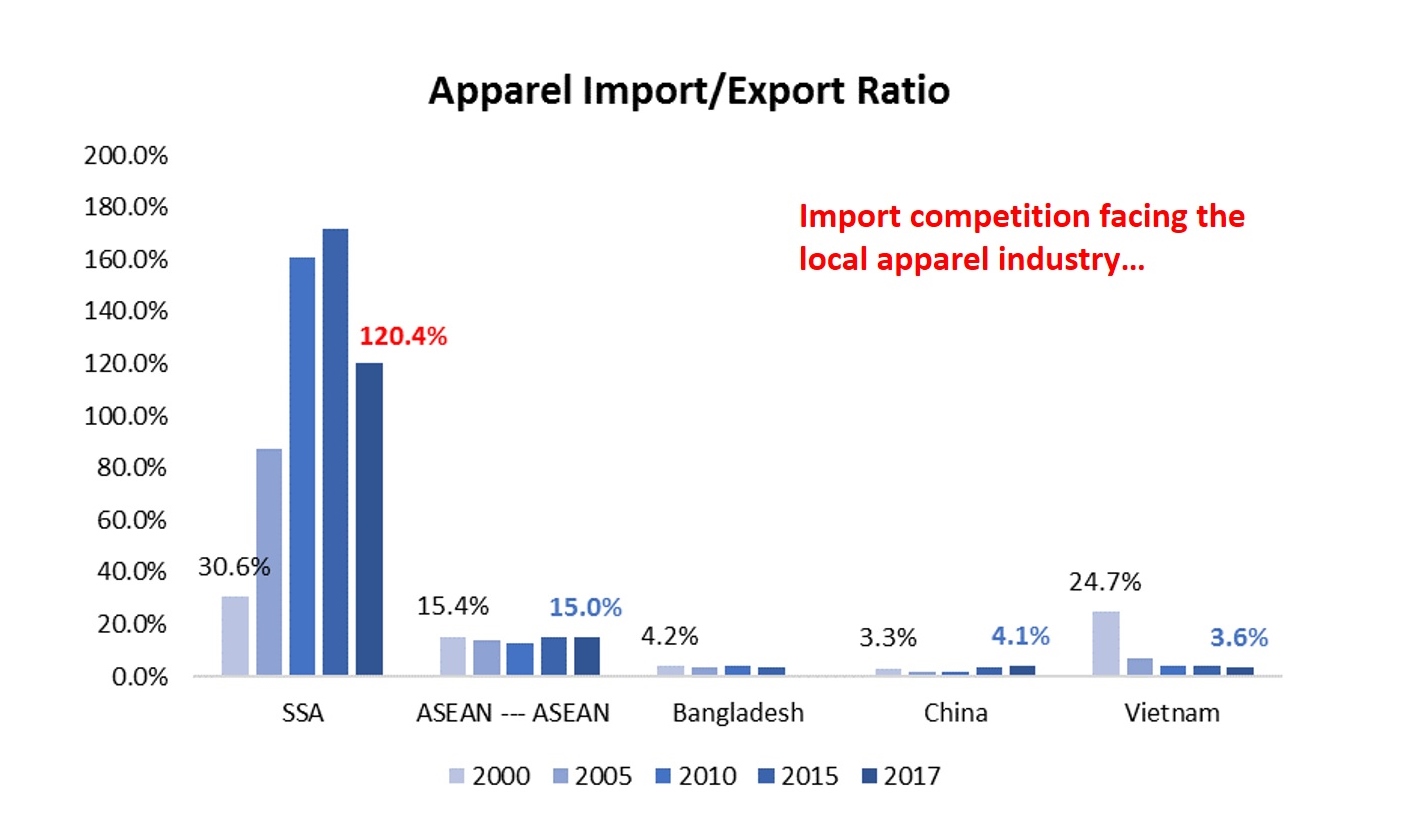

Even more concerning, the T&A industry in SSA countries is facing growing competition in the domestic market with cheap imports, mostly from Asia. Notably, SSA countries import MORE apparel than they export, a phenomenon rarely seen among developing countries in a similar stage of economic development.

Challenge 4: U.S. companies remain low interest in investing in the region directly

According to several recent studies, leading U.S. fashion brands and retailers remain low interest in investing in the SSA region directly, even though companies admit more investments in areas such as infrastructure are critical to the success of SSA countries serving as competitive apparel sourcing bases. Some argue that the “temporary” nature of AGOA make companies hesitant to build factories in SSA. However, should AGOA become a permanent free trade agreement, which follows the principle of reciprocity, SSA countries would have to lower their trade barriers to U.S. products, including eliminating the tariffs and non-tariff barriers, in exchange for the reciprocal market access benefits from the United States. It doesn’t seem most AGOA members are ready for that stage yet.

(In the video: Gail Strickler, former Assistant US Trade Representative for Textiles, highlights the immense opportunities created by the renewal of AGOA for duty-free access to the massive US market for African textile and apparel producers.)

The African Growth and Opportunity Act (AGOA) is a non-reciprocal trade agreement enacted in 2000 that provides duty-free treatment to U.S. imports of certain products from eligible sub-Saharan African (SSA) countries. AGOA intends to promote market-led economic growth and development in SSA and deepen U.S. trade and investment ties with the region. (note: non-reciprocal means SSA countries do not need to offer equivalent benefits to imports from the United States.)

Because apparel production plays a dominant role in many SSA countries’ economic development, apparel has become one of the top exports for many SSA countries under AGOA. Like many trade agreements and trade preference programs, AGOA also set unique rules of origin for textile and apparel (T&A):

First, to enjoy the duty-free and quota-free treatment in the US market, eligible T&A products made in qualifying AGOA countries need to be one of the following categories:

Apparel made with US yarns and fabrics;

Apparel made with Sub-Saharan African (SSA) regional yarns and fabrics, subject to a cap;

Apparel made with yarns and fabrics not produced in commercial quantities in the United States;

Certain cashmere and merino wool sweaters; and

Eligible hand-loomed, handmade or folklore articles and ethnic printed fabrics.

Second, under a special rule called “third-country fabric” provision, AGOA countries with lesser-developed countries (LDBC) status can further enjoy duty-free access in the US market for apparel made from yarns and fabric originating anywhere in the world (such as China, South Korea, and Taiwan). This special rule is deemed as critical because most SSA countries still have no capacity in producing capital and technology-intensive textile products. [Note: Although the US imports of apparel made with third-country fabric are subject to a cap, the cap has never been reached].

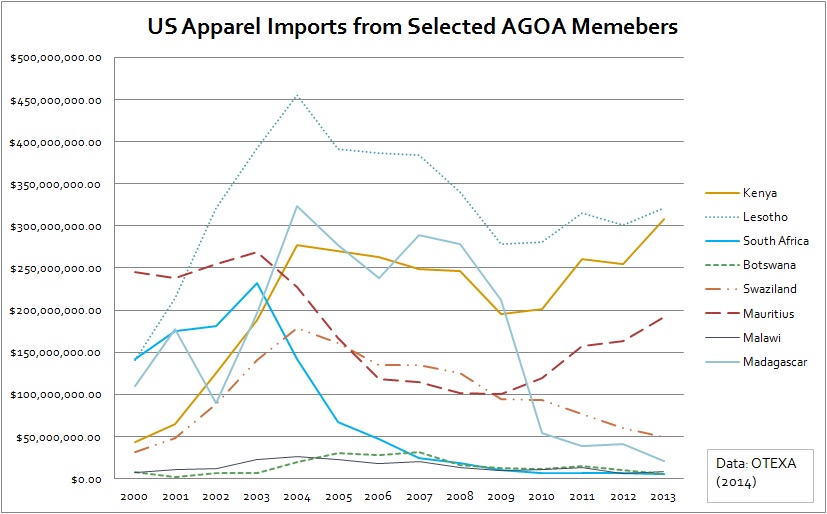

1) Increase exports of apparel. This can be evidenced by the fact that most US apparel imports under AGOA came from those countries that are eligible for the “third-country fabric” provision, such as Lesotho, Kenya, Mauritius, and Swaziland. In comparison, because South Africa is not eligible for the “third-country fabric” provision, its apparel exports to the United States had significantly dropped since 2003 and only accounted for 0.6% among AGOA countries in 2013.

2) Encourage foreign investment. From 2003 to 2013, a total 21 T&A FDI projects were made in SSA, among which 18 projects (or 85.7%) were greenfield FDI. The third-country fabric provision is the main driver for these FDI projects. For example, many Chinese and Taiwanese investors had opened apparel factories in Ghana, Kenya, Lesotho, Madagascar, Malawi, Mauritius, Namibia, Nigeria and Tanzania as a source of exports to the United States and the EU.

3) Enhance trade diversification. Theoretically, relaxing rules of origin (RoO) such as the third-fabric provision can free up companies’ resources and allow them to expand export product lines. As observed by a few empirical studies, AGOA’s third-country fabric provision helped related countries increase the varieties of apparel exports between 39 and 61 percent.