Implemented in June 2022, the Uyghur Forced Labor Prevention Act (UFLPA) prohibits U.S. companies from importing apparel wholly or in part produced in China’s Xinjiang region. UFLPA could significantly alter U.S. apparel import patterns as fashion companies have begun or anticipate adjusting their sourcing base to comply with the law and mitigate the forced labor risks in the supply chain.

This study quantitatively evaluated the impacts of the UFLPA on U.S. apparel imports nearly two years after the law’s implementation. Unlike existing studies primarily focusing on UFLPA’s political or legal aspects, this study’s findings would enhance our understanding of the economic and trade implications of the new law.

A panel regression model was adopted to evaluate the quantitative impact of UFLPA on U.S. apparel imports based on data collected from OTEXA (2024) and USITC (2024), the most authentic government data source. Four countries in three categories were included in the study: 1) China; 2) Vietnam and Bangladesh representing top Asian apparel exporting countries other than China; 3) member countries of the Central America Free Trade Agreement (CAFTA-DR) representing near-shoring sourcing destinations. The annual trade activities of these four countries from 2010 to 2023 (the latest available) were used for the analysis.

The panel regression model suggests several interesting findings*:

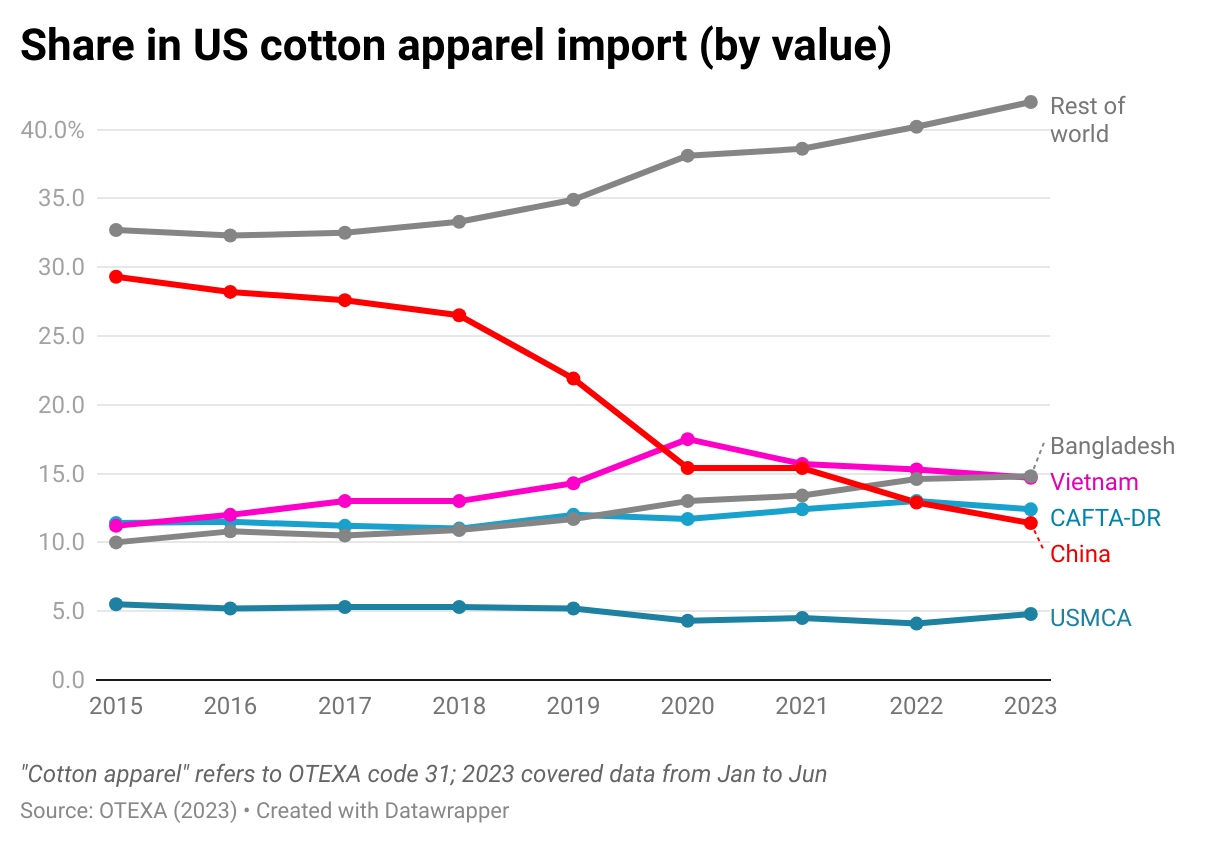

Firstly, the results showed that holding other factors constant, U.S. cotton apparel imports from China decreased significantly by approximately 350 million square meter equivalent (SME) annually following UFLPA’s implementation. In other words, the result confirmed that UFLPA had negatively affected U.S. cotton apparel imports from China. This result is far from surprising as Xinjiang accounted for nearly 90% of China’s cotton production, causing significant forced labor risks associated with importing cotton apparel from China.

Secondly, holding other factors constant, U.S. cotton apparel imports from Vietnam and Bangladesh and CAFTA-DR also respectively decreased by approximately 81 million SME, 51 million SME, and 20 million SME annually after UFLPA’s implementation in 2022. The results revealed U.S. fashion companies’ concerns about UFLPA compliance risks associated with sourcing from countries other than China, particularly Asia, due to their heavy reliance on cotton yarns and fabrics from China through a highly integrated regional supply chain.

Thirdly, the results revealed a more significant positive relationship between U.S. cotton exports to China, Vietnam, Bangladesh, and CAFTA-DR countries and U.S. cotton apparel imports from these countries after UFLPA’s implementation. Related, trade data also showed a declining ratio of U.S. cotton apparel imports from China, Vietnam, Bangladesh, and CAFTA-DR countries relative to these countries’ cotton imports from the U.S. This pattern implies a closer alignment in the trade flow of raw cotton from the U.S. to these countries and the return of finished cotton apparel to the U.S. It could be the case that leading apparel exporting countries increasingly used US cotton after UFLPA to mitigate the forced labor risks.

Additionally, there was a negative relationship between U.S. cotton apparel imports from China, Vietnam, Bangladesh, and CAFTA-DR members and U.S. MMF apparel imports from these countries. In other words, cotton apparel and MMF apparel appear to compete within the total U.S. apparel import market. However, UFLPA’s implementation has not significantly impacted the relationship. Nonetheless, MMF apparel has accounted for a growing share of China’s total apparel exports to the United States after UFLPA’s implementation (down from 46% in 2010 to only 19% in 2023).

The study’s findings revealed a broad trade impact of UFLPA’s implementation that goes far beyond China. Notably, cotton apparel exporters from other Asian countries and those in the Western Hemisphere also appeared to be negatively affected by the new law. Also, unlike theoretical prediction, no clear evidence shows that UFLPA has significantly expanded the near-shoring of U.S. cotton apparel imports from the Western Hemisphere, such as CAFTA-DR members.

Meanwhile, the results call for further investigation of the net impact of UFLPA on U.S. cotton exports. While UFLPA may help U.S. cotton gain more shares in the global marketplace, the reduced U.S. import demand for cotton apparel due to forced labor risk concerns may also unexpectedly “shrink the pie size.”

*:The fixed effects (FE) model was selected for the study based on the likelihood ratio test results (p<.01). The result of the F-test suggests the FE model is statistically significant at the 99% confidence level (p<.01). The value of R2 exceeds 0.90, indicating an overall high goodness-of-fit of the panel regression. All the independent variables were statistically significant at the 99% confidence level (p<.01).

By Sheng Lu and Emilie Delaye

Note: The study will be presented at the 2024 International Textile and Apparel Association (ITAA) annual conference in November 2024.

[This blog post is not open for comment]