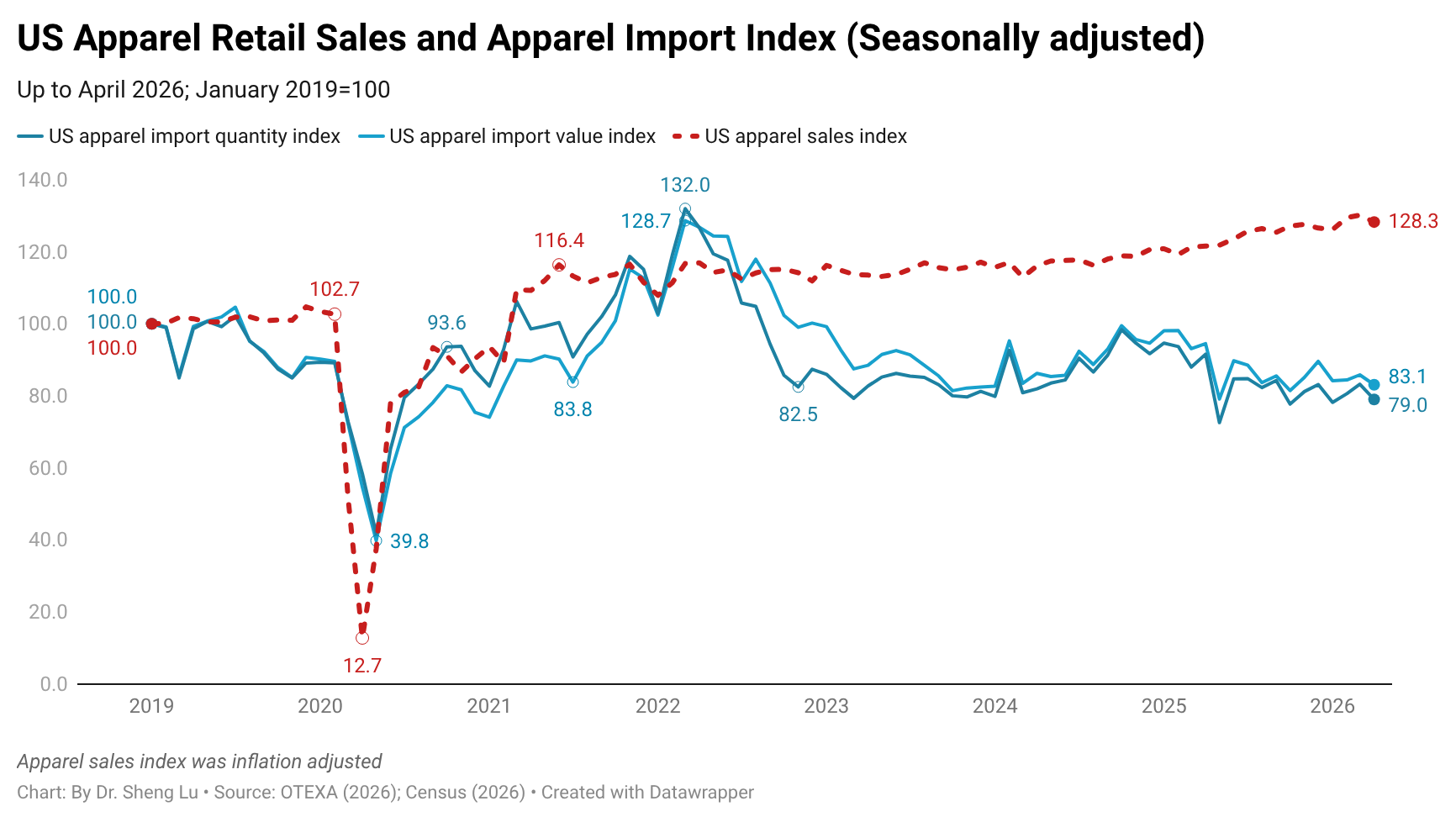

First, U.S. apparel imports continued to shrink in April 2026, reflecting consumers’ hesitation to spend on clothing amid worsening inflation and ongoing economic uncertainty. Specifically, U.S. apparel imports declined by 12.0% in value and 13.8% in April 2026 compared to the previous year, marking the fourth consecutive month of negative growth. Even after adjusting for seasonal factors, U.S. apparel imports in April 2026 were still 3.2% lower in value and 5.1% lower in quantity than in March 2026. As U.S. inflation rose to 4.2% in May 2026, U.S. apparel imports may not reverse the downward trend anytime soon. [see detailed monthly U.S. apparel import data here]

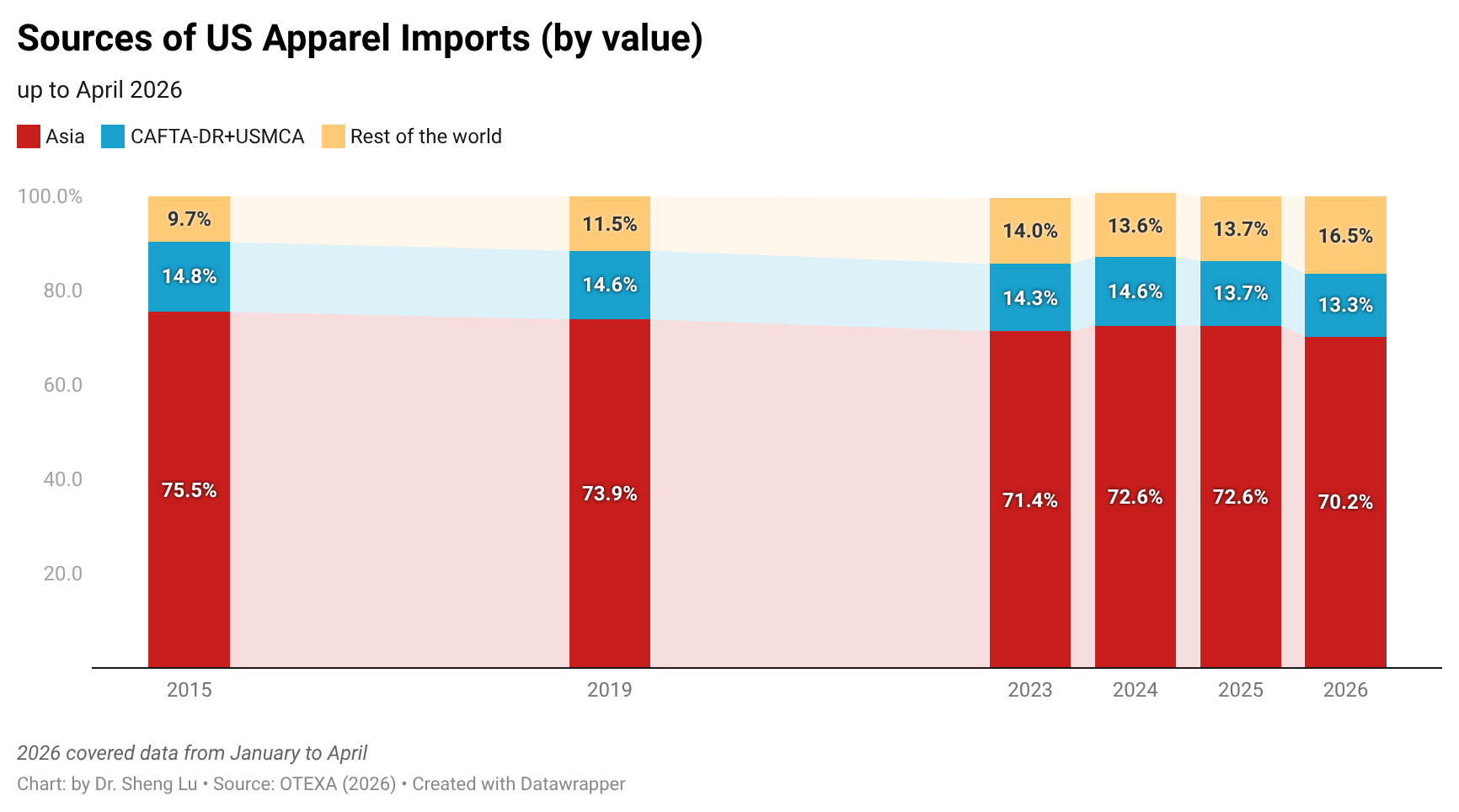

Second, although Asia still dominates, the U.S. apparel sourcing base is becoming increasingly diverse. By value, about 70.2% of U.S. apparel imports came from Asian countries in April 2026, down from 72.0% a year earlier. Notably, Asia’s declining market share was NOT captured by Western Hemisphere countries, whose share remained at 15.7% in April 2026 (including 13.7% for CAFTA-DR and USMCA members), even slightly lower than the 15.8% recorded in April 2025. Instead, U.S. apparel imports from countries outside Asia and the Western Hemisphere reached a new high of 14.1% in April 2026, up from 12.3% in April 2025 and well above the 7.4% recorded in 2015. This shift reflects U.S. fashion companies’ efforts in recent years to explore emerging sourcing destinations in regions such as Africa, the Middle East, and the EU to mitigate growing sourcing risks and other concerns.

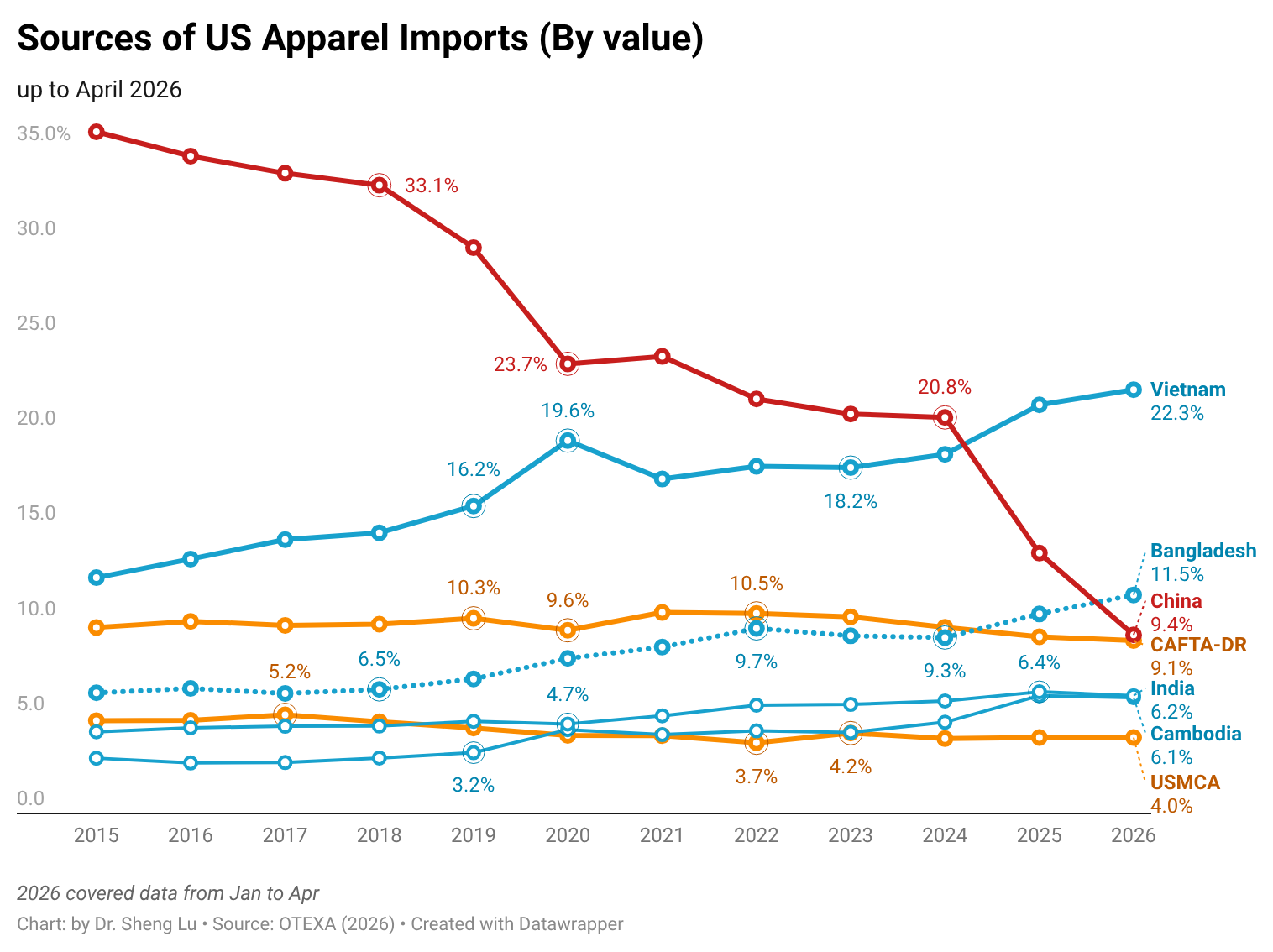

Third, at the country level, U.S. fashion companies have increased sourcing from several key Asian apparel-supplying countries beyond China, as well as from a few emerging sourcing destinations in other regions. Specifically, in the first four months of 2026, while the value of U.S. apparel imports decreased by 12%, imports from Vietnam (up 1.3%), Indonesia (up 2.3%), and Cambodia (up 14.2%) increased. Egypt (up 14.7%) and Turkey (up 6.4%) also became more popular sourcing destinations. In comparison, over the same period, U.S. apparel imports from China (down 50.2%), India (down 28.0%), and Bangladesh (down 11.2%) decreased substantially. Particularly for China and India, the much higher tariff rates imposed on their products were among the critical factors behind their loss of sourcing orders. Regarding Bangladesh, since it primarily produces low-volume items for U.S. fashion companies, it could be disproportionately affected as ordinary U.S. consumers purchase fewer clothing items amid economic stress. [See detailed country market share data here]

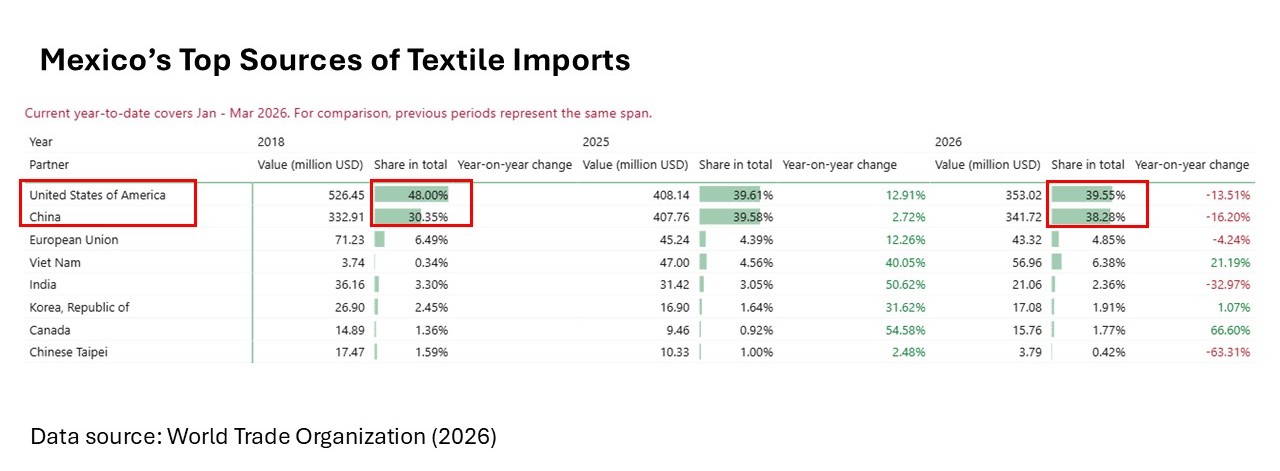

Fourth, with the upcoming US-Mexico-Canada Agreement (USMCA) joint review later this summer, the state of U.S. textile and apparel trade with Mexico and Canada has drawn increased attention. On the one hand, the OTEXA data show that the USMCA remained the single largest export market for U.S.-made yarns and fabrics as of 2026. In the first four months of 2026, about 48.4% of U.S. yarn and fabric exports went to USMCA members, including 33.9% destined for Mexico. This share has been highly consistent over the past decades, including when the USMCA replaced NAFTA in 2020. Meanwhile, according to the latest data from the World Trade Organization (WTO), in the first three months of 2026, the U.S. accounted for about 39.3% of Mexico’s textile imports. However, this percentage was noticeably lower than 48% in 2018. Over the same period, China has become an increasingly important textile supplier for Mexico, with its market share rising from 30.3% in 2018 to 38.3%.

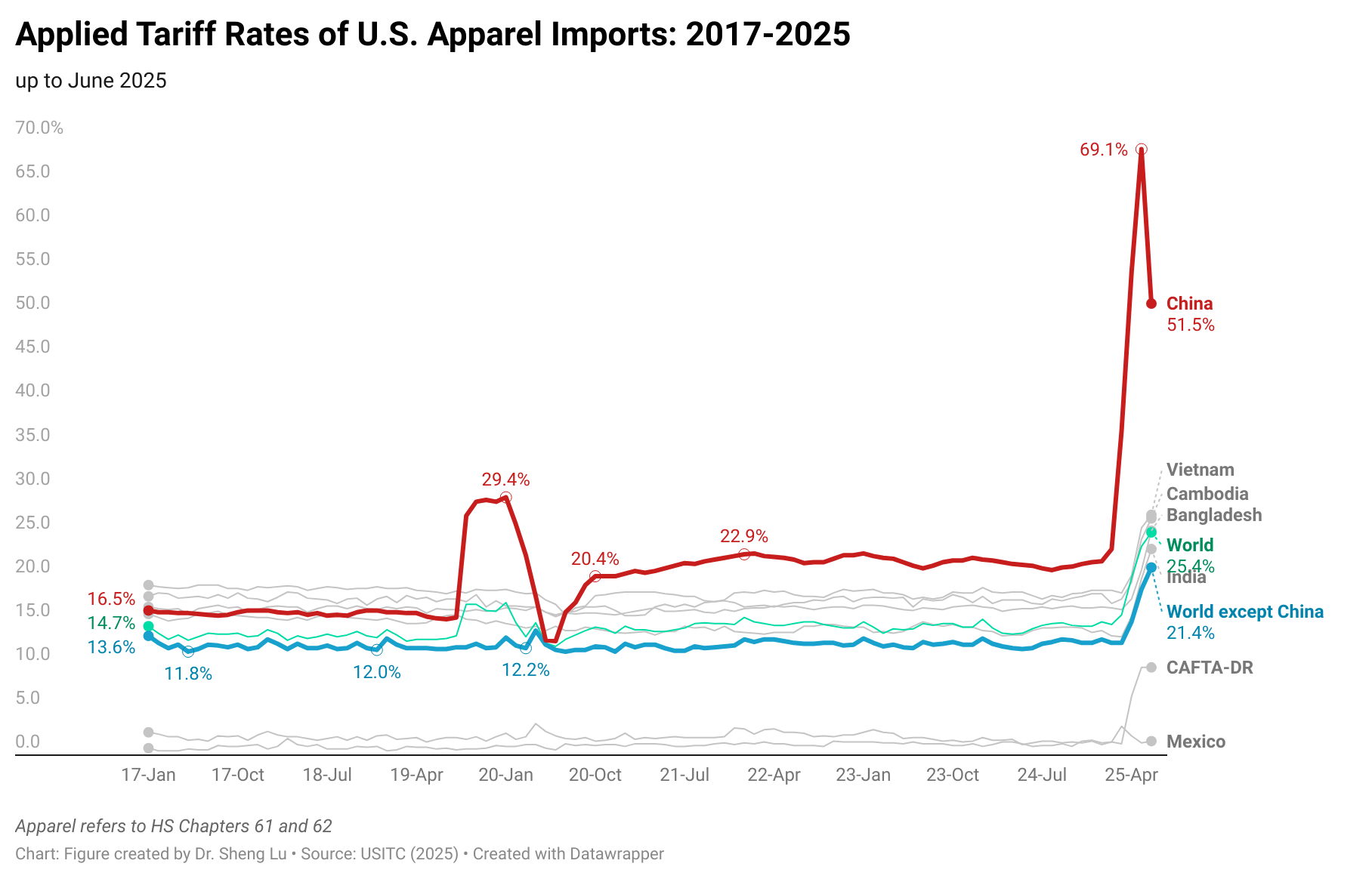

On the other hand, in value terms, USMCA accounted for 3.4% of U.S. apparel imports in the first four months of 2026 (including 2.8% from Mexico), slightly up from 3.2% over the same period in 2025. Despite the relatively low market share compared to Asian suppliers, it should be noted that in the first three months of 2026, nearly 98% of Mexico’s apparel exports went to the United States. Data from the U.S. International Trade Commission further show that almost 94% of those exports claimed duty-free benefits under the USMCA in the first three months of 2026, a significant jump from around 80%-83% in the past. USMCA-qualifying apparel has been among the very few products exempt from the tariff hikes since Trump’s second term.

Furthermore, in the first four months of 2026, about 55.3% of U.S. apparel imports from Mexico were cotton apparel, the lowest share since 2021 (around 57%). While the available data did not establish a direct causal relationship, the growing availability of textile inputs from Asia may have contributed to a broader diversification of Mexico’s apparel exports to the U.S. market beyond traditional products such as men’s and boys’ cotton trousers. This trend also underscores the high stakes of USMCA’s review. The agreement’s duty-free preferences and yarn-forward rules have long encouraged the use of U.S.-made textile inputs, especially those cotton-centered, in Mexican apparel production. Without these incentives, Mexican manufacturers could have greater flexibility in sourcing textile inputs from Asia, given the benefits of diversifying their export offerings. Such a shift could reduce demand for U.S. yarn and fabric exports and further weaken traditional Western Hemisphere textile and apparel supply chains.

Additionally, U.S. apparel imports from Sub-Saharan African (SSA) countries declined sharply, down 30.9% in value and 22.3% in quantity in April 2026. So far in the first four months of 2026, SSA countries together accounted for 1.9% of U.S. apparel imports, the same as in 2025. With the African Growth and Opportunity Act (AGOA) renewed for only one year and set to expire at the end of 2026, these results reinforce concerns that U.S. fashion companies are unwilling to expand apparel sourcing from AGOA without a clear long-term policy outlook.

For FASH455 class: When writing your blog comment, consider addressing the following aspects:

How do you see the importance of the garment industry to Lesotho—economically, socially, and politically?

Why and how could the 15% additional tariff have a significant impact on Lesotho’s garment industry?

What responsibilities do U.S. fashion brands and retailers have toward Lesotho in the situation described in the videos?

If you were a U.S. garment worker, would you support more favorable trade terms for Lesotho? Why or why not?

Background

According to the World Trade Organization (WTO), textiles and apparel accounted for 56.6% of Lesotho’s manufactured goods exports in 2023.

UNComtrade data shows that between 2023 and 2024, about half of Lesotho’s apparel exports went to the United States, its largest export market. Other countries in Sub-Saharan Africa (SSA) made up an additional 44% of Lesotho’s apparel exports.

Industry sources further indicate that between January 2024 and July 2025, about 60% of apparel labeled “Made in Lesotho” for sale in the U.S. retail market were tops, including 41% of T-shirts. All of these clothes targeted the mass and value market segments, and they were typically priced even lower than those “Made in Bangladesh.”

The African Growth and Opportunity Act (AGOA), a trade preference program enacted in 2000, has played a critical role in supporting Lesotho’s apparel export to the U.S. market.

Data from the Office of Textiles and Apparel (OTEXA) under the U.S. Department of Commerce shows that U.S. apparel imports from Lesotho totaled $151 million, or 0.19% of total U.S. apparel imports, in 2024. Notably, all of these imports claimed the AGOA duty-free benefits, and 96.8% were entered under the “third-country fabric” provision, which allows least developed countries (LDCs) like Lesotho to use textile raw materials sourced from third countries.

The latest Sourcing at MAGIC, one of the largest and most influential fashion apparel trade shows in North America, was held from August 18 to 20, 2025 in Las Vegas. Drawing thousands of apparel manufacturers, textile raw material suppliers, brands, and retail buyers from over 30 countries around the globe, the event provides a unique opportunity to observe the latest U.S. apparel sourcing trends and market sentiment.

Aligned with the results of the 2025 Fashion Industry Benchmarking Study released by the United States Fashion Industry Association (USFIA), the hiking tariffs imposed by the Trump administration and ongoing policy uncertainty were among the top concerns for MAGIC attendees. One major tariff impact often heard at the MAGIC show was the growing inflationary pressure. It was a prevailing view among vendors, brands, and retailers that a price increase had begun and would become even more noticeable to U.S. consumers in the upcoming months. Some also argue that “tariff is no longer a sourcing problem,” but how brands and retailers should handle their “profit margin, product assortment, and pricing.”

Meanwhile, apparel suppliers care significantly about the additional “reciprocaltariff” rates they face compared to their key competitors. For instance, a jeans supplier from Pakistan said they were relieved to see more order inquiries come in, as their Indian competitors faced significantly higher tariff rates threatened by the Trump administration.

Still, nearly 600 exhibitors from China attended MAGIC, making it the largest delegation from any country. Two interesting phenomena revealed how Chinese suppliers try to stay competitive in today’s challenging business environment. One is to offer various value-added sourcing services beyond physical products. For example, there was a dedicated session at this year’s MAGIC show that featured Chinese manufacturers that provide services such as drop shipping (i.e., when a customer places an order, the retail store never physically handles the product. Instead, the manufacturer is responsible for inventory, packing, and shipping), director to consumer (DTC) e-commerce and warehousing. Meanwhile, some Chinese vendors accept small orders (i.e., 6 pieces or less) or low minimum orders (i.e., 300 pieces) and promise a short lead time of 45 days. In comparison, the minimum order quantity (MOQ) required by suppliers in other Asian and Western Hemisphere countries typically exceeds thousands of pieces.

On the other hand, it is not uncommon to see that vendors from Bangladesh, Vietnam, Cambodia, or even Egypt and Ghana were actually owned by Chinese investors. Several Chinese factories purposefully highlight that they own factories across the world, from China and Southeast Asia to Africa. According to the USFIA benchmarking study, some U.S. fashion companies also prefer vendors with production capabilities in multiple countries to reduce sourcing risks.

As U.S. fashion companies continue to diversify their sourcing beyond the traditional top three—China, Vietnam, and Bangladesh—emerging destinations are increasingly optimistic about their U.S. export prospects. For instance, a supplier from Jordan noted that recent U.S. tariff hikes have boosted Jordan’s competitiveness, given the zero most-favored-nation (MFN) tariff under the U.S.-Jordan Free Trade Agreement and a 15% reciprocal tariff rate, which was lower than many Asian suppliers face.Jordanian suppliers speak highly of the capacity-building support from international organizations such as the International Trade Centre (ITC), particularly in areas like skills training and market intelligence.

Similar to Jordan, Egypt’s apparel exports can benefit from a zero most-favored-nation (MFN) tariff, provided they meet the rules of origin under the Qualifying Industrial Zones (QIZ) initiative. However, unlike Jordan, suppliers from Egypt tend to specialize in cotton and other natural-fiber–intensive apparel, leveraging their advantages in producing locally made, high-quality natural textile fibers.

Clothing made from preferred sustainable fibers, particularly those incorporating recycled textiles, has grown increasingly popular. Nearly every country represented at MAGIC, including developing nations in Asia and Africa, showcased such products.

It should be noted, however, that producing clothing with sustainable textile fibers requires suppliers to obtain certifications such as GOTS (Global Organic Textile Standard), Global Recycled Standard (GRS), and Better Cotton Initiative (BCI). Although these certifications add costs, most vendors view sustainability as an opportunity to enhance export competitiveness rather than a threat in the long term. Some also mentioned that buyers were often willing to pay a premium for products made with sustainable materials, providing a significant financial incentive.

On the other hand, achieving sustainable sourcing and production is becoming increasingly comprehensive, requiring continuous innovation in both technology and business models. For example, at the show, some vendors showcased apparel products that integrated multiple sustainability concepts, ranging from material development and eco-design to social responsibility and post-consumption solutions.

#1 This year, the top business challenges facing U.S. fashion companies center on the Trump Administration’s escalating tariff policy and its wide-ranging impacts on companies’ sourcing and business operations.

100 percent of respondents rated “Protectionist U.S. trade policies and related policy uncertainty, including the impact of the Trump tariffs” as one of their top business challenges in 2025. This included as much as 95 percent of respondents who ranked the issue among their top two concerns.

Respondents also expressed significant concerns about the wide-ranging effects of Trump’s tariff policy, including “Inflation and economic outlook in the U.S. economy” (80 percent), “Increasing production or sourcing cost” (nearly 50 percent), and “Protectionist trade policies and policy uncertainty in foreign countries, including retaliatory measures against the U.S.” (52 percent).

#2 Maintaining a geographically diverse sourcing base has been one of the most popular strategies adopted by U.S. fashion companies to mitigate the impact of rising tariffs and policy uncertainty.

This year, respondents reported sourcing apparel products from 46 countries, similar to the 48 countries reported in 2024 and an increase from 44 countries in 2023. At the firm level, approximately 60 percent of large companies with 1,000+ employees reported sourcing from ten or more countries in 2025, a notable increase from the 45–55 percent range reported in 2022 and 2023 surveys.

Amid escalating tariffs and rising policy uncertainty, Asia has become an ever more dominant apparel sourcing base for U.S. fashion companies in 2025.Respondents reported increased use of several Asia-based sourcing destinations other than China in 2025 compared to the previous year, including Vietnam (up from 90 percent to 100 percent), Cambodia (up from 75 percent to 94 percent), Bangladesh (up from 86 percent to 88 percent), Indonesia (up from 75 percent to 77 percent), and Sri Lanka (up from 39 percent to 53 percent).As part of their sourcing diversification strategy, U.S. fashion companies are also gradually increasing sourcing from emerging destinations in the Western Hemisphere and beyond, such as Jordan, Peru, and Colombia.

Most respondents intend to build a more geographically diverse sourcing base and broaden their vendor network over the next two years. Nearly 60 percent of respondents plan to source apparel from more countries, and another 40 percent plan to source from more suppliers or vendors. Reducing sourcing risk, especially to minimize the impact of rising tariffs and tariff uncertainty, is a key driver of companies’ sourcing diversification strategies

#3 U.S. fashion companies remain deeply concerned about the future of the U.S.-China relationship during Trump’s second term and intend to further “reduce China exposure” to mitigate sourcing risks.

While 100 percent of respondents reported sourcing from China this year, a record-high 60 percent of respondents reported sourcing fewer than 10% of their apparel products from China, up from 40 percent in 2024. Approximately 70 percent of respondents no longer used China as their top apparel supplier in 2025, representing a further increase from 60 percent in 2024 and significantly higher than the 25-30 percent range prior to the pandemic.

Despite the announcement of the reaching of a U.S.-China “trade deal” in May 2025, more than 80 percent of respondents plan to further reduce their apparel sourcing from China over the next two years through 2027, hitting a new record high. Many large-scale U.S. fashion companies are already limiting or plan to limit their apparel sourcing from China to a “low single-digit” percentage by 2026 or earlier, mainly due to concerns about the increasing geopolitical and trade policy risks associated with sourcing from the country.

Still, respondents rated China ashighly economically competitive as an apparel sourcing basecompared to many of its Asian competitors regarding vertical manufacturing capability, low minimum order quantity (MOQ) requirements, flexibility and agility, sourcing costs, and speed to market. However, non-economic factors, particularly the perceived extremely high risks of facing U.S. import restrictions, geopolitical tensions with the U.S., and concerns about forced labor, are driving U.S. fashion companies to continue their de-risking efforts.

#4 No evidence indicates that the Trump Administration’s tariff policy has successfully encouraged U.S. fashion companies to increase domestic sourcing of “Made in the USA” textile and apparel products or to expand sourcing from the Western Hemisphere.

Only about 44 percent of respondents explicitly say that they would expand sourcing from the Western Hemisphere, and even fewer respondents (17 percent) plan to source more textiles and apparel “Made in the USA” amid the tariff increase.

This year, fewer respondents reported sourcing apparel from Mexico and Canada (down from 60 percent in 2024 to 50 percent in 2025) and members of the Dominican Republic-Central America Free Trade Agreement, CAFTA-DR (down from 75 percent in 2024 to 64 percent in 2025).

About half of the respondents plan to expand apparel sourcing from Mexico and CAFTA-DR members over the next two years. Notably, nearly all of these companies also intend to increase sourcing from Asia, indicating that U.S. fashion companies view near-shoring from the Western Hemisphere as a complement, not a replacement, to their broader sourcing diversification strategy.

#5 Respondents overall remain highly committed to sustainability, social responsibility, and compliance issues in the sourcing process.

This year, the top sustainability and compliance areas where respondents plan to allocate more resources include “Investing in technology to enhance supply chain traceability or isotopic testing” (53 percent), “Providing sustainability and social compliance training for internal employees” (50 percent) and “Providing sustainability and social compliance training for suppliers” (50 percent).

Moreover, most respondents (over 70 percent) plan to increase their use of various “sustainable fibers” in clothing over the next three years. This trend is especially strong for recycled materials, with 80 percent of respondents indicating they intend to increase their use.

The top three positions with the highest demand among respondents from 2025 through 2030 are “Environmental sustainability-related specialists or managers,” “Trade compliance specialists,” and “Data scientists”—more than 40 percent of respondents plan to increase hiring. There is also strong demand for “Textile raw material specialists” and “Sourcing specialists.”

#6 With the upcoming expiration of the trade preference program this September, respondents again underscore the importance of immediate renewal of the African Growth and Opportunity Act (AGOA) and extending the agreement for at least another ten years.

Due to the upcoming expiration of AGOA and uncertainty about its future, this year, respondents sourced from only six SSA and AGOA members (i.e., Kenya, Ethiopia, Ghana, Madagascar, Mauritius, and Tanzania), fewer than the seven countries in 2024. And none of these countries were used by more than 20 percent of respondents.

Nearly 80 percent of respondents support “renewing AGOA for at least another ten years,” and no one opposes. This shows a consistent and wide base of support for AGOA among U.S. fashion companies.

More than 70 percent of respondents say that securing a long-term renewal of AGOA for at least ten years is essential for expanding apparel sourcing from the region. Similarly, another 60 percent of respondents believe that a long-term renewal of AGOA is necessary for U.S. fashion companies and their supply chain partners to commit to new investments in the region.

Authored by Dr. Sheng Lu in collaboration with the United States Fashion Industry Association (USFIA), this year’s benchmarking study was based on a survey of executives from 25 leading U.S. fashion companies from April to June 2025. The study incorporated a balanced mix of respondents representing various businesses in the U.S. fashion industry. Approximately 85 percent of respondents were self-identified retailers, 60 percent were self-identified brands, and about 50 percent were importers/wholesalers.

The survey respondents included large U.S. fashion corporations and medium-sized companies. Around 90 percent of respondents reported having over 1,000 employees; the rest (10 percent) represented medium-sized companies with 100-999 employees.

Apparel products are often subject to high tariffs for various reasons. In developed countries such as the United States, apparel has long been considered an “import-sensitive” sector, with relatively high tariff rates imposed primarily to “protect” specific domestic interest groups with political influences.

However, as importers, not exporters, pay the tariffs, heavy import duties have been a significant concern for US fashion companies for decades. According to data from the US International Trade Commission (USITC), in 2024, apparel (HS chapters 61 and 62) accounted for about 2.5 percent of total US imports but contributed approximately 15.6 percent of total tariff duties. Likewise, US fashion companies paid $11.9 billion in tariffs on apparel imports in 2024, an increase from $11.6 billion in 2023. The average applied tariff rate for apparel items reached 14.6% in 2024, a notable increase from 13.7% before the imposition of Section 301 tariffs on Chinese products. Additionally, due to retail markups, every $1 in tariffs could result in a $1.50 to $2 increase in the final retail price.

Meanwhile, developing countries, especially those least developed, also often impose high tariffs on apparel—either to protect their nascent domestic industries from import competition or to generate government revenues. For example, in Africa, the apparel import tariff rate commonly exceeds 35% as of 2023 (the latest data available).

In February 2025, President Trump announced the imposition of a so-called “reciprocal tariff,” aiming to “match” the tariff rates that other countries impose on US exports, thereby promoting “fairer trade practices.” However, the details of the “reciprocal tariff” idea remain highly uncertain.

In theory, if strict “tariff matching” is required on a product-by-product basis, US apparel imports from most leading sourcing destinations—particularly those in Asia without a free trade agreement with the US–would face a significant increase in tariffs. Similarly, beneficiary countries under the African Growth and Opportunity Act (AGOA) could face a similar issue, as AGOA is a trade preference program that does not provide duty-free market access for US products in Africa. If apparel exports from AGOA-member countries to the US were subjected to the same 35%+ tariff rates that US products currently face in their markets, it would be a devastating scenario.

By Sheng Lu

(note: this post is not open for comment/discussion)

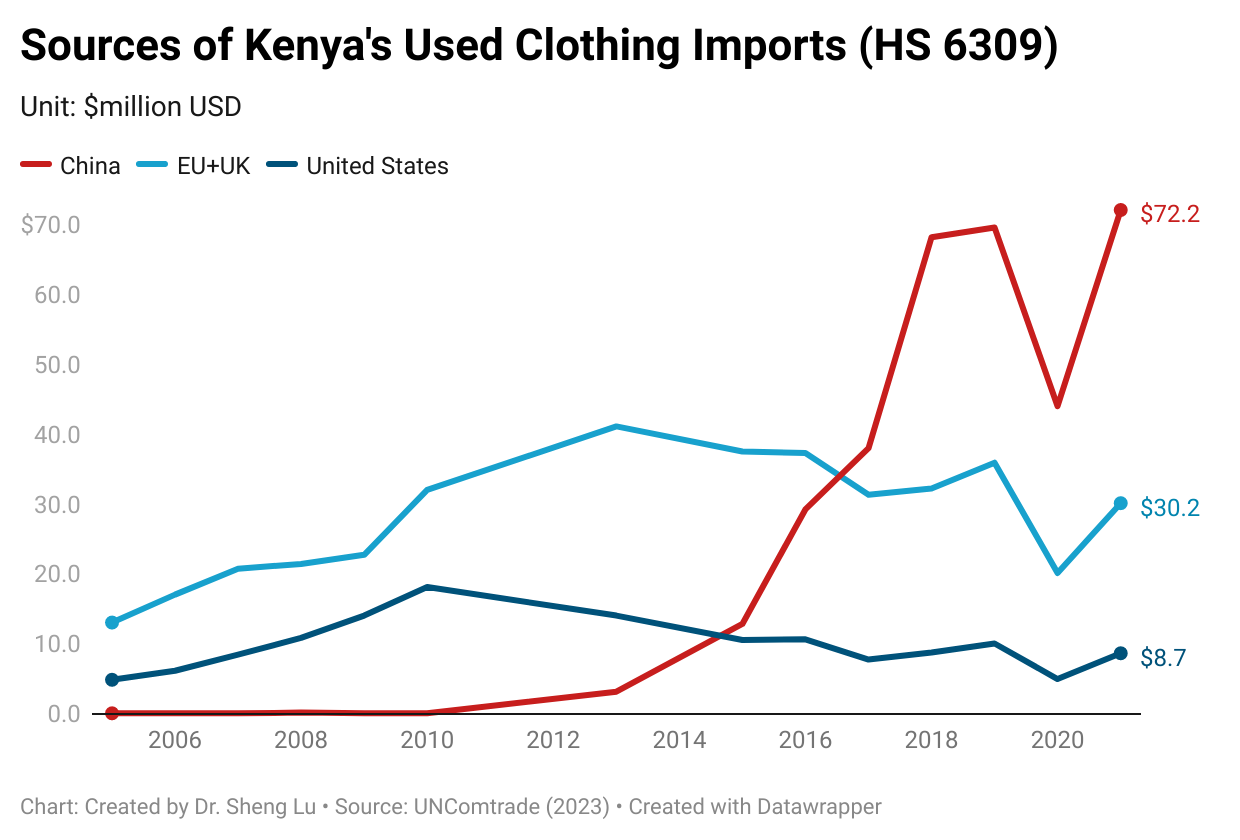

Concerns about the used clothing exports to Kenya (viewpoints from the Changing Markets Foundation)

Data from the United Nations (UNComtrade) shows that Kenya’s used clothing imports surged by over 500% from 2005 ($27 million) to 2021 ($172 million).

An overwhelming volume of used clothing shipped to Kenya is waste synthetic clothing, a toxic influx creating devastating consequences for the environment and communities. It is estimated that over 300 million items of damaged or unsellable clothing made of synthetic or plastic fibers are exported to Kenya each year, where they end up dumped, landfilled, or burned, exacerbating the plastic pollution crisis.

Interviews with used clothing traders in Kenya show that 20–50% of the used clothing in bales they purchased was unsellable due to being damaged, too small, unfit for the climate or local styles, and sometimes even with clothing that is covered in vomit, stains or otherwise damaged beyond repair.

European sorting companies often skimmed off high-quality used clothing for resale in the local EU market. They exported the lower-quality and lower-graded ones to developing countries like Kenya.

It remains challenging to recycle synthetic clothing as it often contains harmful additives or other materials that make the recycling process difficult or impossible. Additionally, the quality of the recycled synthetic fibers is typically lower than that of the original fabric (i.e., using virgin fiber).

Defend the used clothing exports to Kenya (viewpoints from the Textile Recycling Association, TRA)

Sorting, trading and selling used clothing “directly employs two million peoplein Kenya alone , with tens of millions employed globally and supporting many more employment positions in ancillary sectors.”

“Used clothing and textiles collected in the UK, should go through a detailed sorting process and can be sorted typically into 130 plus re-use and recycling grades and sometimes this can be more than 200 grades. In the sorting process each garment is picked up and individually assessed by highly trained experts*. The good quality re-useable products are segregated from the recycling grades.” [*According to Changing Markets Foundation’s report, about 36 million pieces of used clothing were exported from the UK to Kenya in 2021; All EU countries exported about 112 million pieces to Kenya]

“It is the buyers in these countries (note: countries like Kenya) that dictate the flows of (used clothing) textiles and which import the goods into their countries.”

“TRA members are required to ensure that only good quality re-usable clothing products are sold onto countries in Africa and other non-OECD countries. Recycling grades and other non-textile/clothing items have to be removed… However, the majority of countries are not subject to the same tight restrictions on trading as the UK.. This is to the extent that some countries allow unsorted used textiles containing a complete mix of re-usable items, recycling grades, and waste to be sold into African countries as a product.” “The qualities of (used clothing) items originating from different countries is likely to vary significantly.”

“Kenyan’s buy more than 10 times as much used clothing from China than they do from the UK.”

For FASH455: the blog comment assignment can address the following questions:

What is your stance on the used clothing trade? Should the government impose more export or import trade restrictions on used clothing?

As we learned in class, developing countries like Kenya are supposed to rely on making and exporting labor-intensive garments to develop their economies. Can importing used clothing lead to similar economic growth? Any evidence that can support the argument?

What are the ethical issues involved in the used clothing trade? Should government policies play a role in regulating these ethical concerns?

Could restricting the used clothing trade discourage fast fashion and reduce textile waste generation? Why or why not?

Should developed countries like the U.S. voluntarily restrict used clothing exports to lessen the economic and environmental pressures on developing countries like Kenya? What are the potential benefits and drawbacks of such a policy?

Based on the reading, what critical questions remain unanswered, and what further studies could be conducted to gather valuable information for informed decision-making on regulating the used clothing trade?

In December 2024, Just-Style consulted a panel of industry experts and scholars in its Shape of apparel sourcing in 2025 briefing. Below is my contribution to the report. Welcome any comments and suggestions!

What’s next for apparel sourcing

Although the world economy is predicted to grow at a similar pace in 2025 from 2024, the slowing US and Chinese economies could impose new challenges to apparel sourcing, from weakened demand to intensified price competition.

Regarding the macroeconomic environment in 2025, which “sets the tone” for apparel sourcing, the International Monetary Fund (IMF) and the World Bank estimated that the world economy would grow by approximately 2.7-3.2 percent in 2025, with almost no change from the previous year. Similarly, the World Trade Organization (WTO) projected that world merchandise trade would increase by 3.3 percent in 2025, slightly higher than 2.6 percent in 2024.

Despite this incremental improvement, the world’s two largest economies–the US (with 2.2 percent GDP growth in 2025, down from 2.8 in 2024 and 2.9 in 2023) and China (with 4.5 percent GDP growth in 2025, down from 4.8 in 2024 and 5.2 in 2023) are expected to experience slower economic growth in the new year ahead. This slowdown means that apparel producers around the world, particularly those developing countries making large-volume basic items, will likely continue to struggle with a shortage of souring orders in 2025 due to overall weak import demand.

Even more concerning, as China grapples with declining domestic sales, the world clothing market could see an additional influx of low-cost Chinese products, especially through new e-commerce channels. Notably, less than half of China’s clothing production is exported, indicating its significant untapped export capacity. Furthermore, while China’s wage levels are higher than those in many other Asian apparel-producing countries, the unit price of U.S. apparel imports from China measured in dollar per square meter equivalent ($/SME) dropped by more than 21% between 2018 and 2024 (up to October). In contrast, U.S. apparel import prices from the rest of the world increased by 7.8% over the same period. Related to this, what is often overlooked is that even Shein, the “ultra-fast fashion” retailer known for its exceptionally competitive pricing, deliberately opted out of the vast Chinese market due to concerns about the intense price competition there. In other words, disregarding the new Trump tariff, 2025 could see an escalation of trade tensions targeting Chinese products in the US market and beyond.

Meanwhile, due to concerns about rising geopolitical tensions worldwide and trade policy uncertainty during Trump’s second term, fashion companies will likely continue to leverage sourcing diversification to mitigate risks. However, the “reducing China exposure” and sourcing diversification movement has yet to substantially benefit near-shoring or emerging sourcing destinations such as the Western Hemisphere and Sub-Saharan Africa (SSA). This result was mainly because fashion companies utilized China to source a wide range of various products, whereas Western Hemisphere and SSA suppliers can only produce a few basic categories.

For example, my latest studies show that in the first nine months of 2024, even excluding major platforms like Shein, Amazon, and Temu, US fashion companies sourced more than 60K Stock Keeping Units (SKUs) of clothing items from China. In comparison, India and Vietnam each supplied approximately 15K SKUs, Cambodia and Bangladesh each contributed 3,000 SKUs, Mexico provided only 2K SKUs, and CAFTA-DR and AGOA member countries supplied around 200 SKUs each. Therefore, even if fashion companies report sourcing from more countries, they are likely to stay sourcing from more Asian countries with closer export capacity and structure to China. Meanwhile, the total value or volume of trade may not fully capture the whole picture of sourcing diversification. This trend may persist in 2025, even with new tariff escalations.

Apparel industry challenges and opportunities

Today’s fashion business is highly global and relies heavily on the frequent movement of goods and services across borders. Thus, the uncertain and protectionist nature of U.S. trade policy during Trump’s second term could present significant challenges to the fashion industry in 2025. Of particular concern is that Trump’s new tariff actions would raise fashion companies’ sourcing costs, create additional inflationary pressure, reduce US consumers’ purchasing power on clothing, and trigger retaliatory trade measures from U.S. trading partners, ultimately hurting the U.S. economy. Notably, when the 7.5% Section 301 tariff was imposed on selected Chinese clothing products in 2018, the U.S. Consumer Price Index (CPI) growth was relatively low at 1.9%. However, imposing a 20% global tariff, a 60% tariff on Chinese products, and the existing 15%-30% regular tariff on clothing when the CPI is historically high is like “adding fuel to the fire.”

Besides tariffs, in 2025, if not sooner, U.S. fashion companies and many e-commerce suppliers worldwide will closely watch how Congress and the new Trump administration reform the de minimis rule, which currently exempts small-value shipments under $800 from tariffs and most customs procedures. With Trump’s new tariffs looming, some argue that closing the de minimis “loophole” has become even more urgent, as it creates more financial incentives to use the rule to bypass the tariff increase. Meanwhile, proposals under consideration suggest removing textile and apparel products entirely from de minimis, a move that could be an “earthquake” for those fashion companies utilizing the rule heavily.

Trump’s approach and philosophy toward conventional trade agreements and trade preference programs in 2025 also deserve attention. During his first term, Trump launched a few bilateral trade negotiations, from the one with the United Kingdom and Japan to Kenya. Back then, Trump saw a bilateral agreement would give the U.S. more leverage for a better “deal.” Specifically related to apparel sourcing and trade, two flagship U.S. trade preference programs–the African Growth and Opportunity Act (AGOA) and the Haiti HOPE/HELP Act, will expire in September 2025. It remains uncertain whether the new Trump administration will support the early renewal of these two trade preference programs with minimal changes or prefer to renegotiate them and add new bilateral elements.

Additionally, even though the new Trump administration may not prioritize addressing climate change, it is an irreversible trend for fashion companies to allocate more resources to comply with upcoming or newly implemented sustainability and environmental-related legislation, whether from the EU or the US state level. Unlike in the past, when being more sustainable only meant adding operational costs or paying a “one-time fee,” today’s new generation of sustainability-focused regulations—such as Extended Producer Responsibility (EPR)—requires companies to shift their mindset and demonstrate continuous improvement. Interestingly, my recent study tracking apparel products’ sustainability claims shows that vague terms like “sustainable” and “eco-friendly” are gradually being replaced by more neutral, fact-based keywords such as “regenerative,” “textile waste,” and “low impact.”

Meanwhile, offering “sustainable” apparel products and those using “preferred sustainable fibers” could provide fashion companies new opportunities to diversify their sourcing base and expand their vendor networks. For example, studies show that in the U.S. market, China and many other Asian countries are not necessarily the top suppliers of clothing made with recycled materials. Instead, Europe and countries in the Western Hemisphere or even Africa present unique sourcing advantages and capacities due to the unique nature of such products. Therefore, in 2025, we can expect an ever-closer collaboration between design, product development, merchandising, sourcing, and legal teams within fashion companies, working together to meet the growing demand for sustainable apparel and ensure compliance with evolving regulations.

#1 Respondents reported growing sourcing risks of various kinds in 2024, from navigating an uncertain U.S. economy, managing forced labor risks, and responding to shipping and supply chain disruptions to facing rising geopolitical tensions and trade protectionism.

Over half of the respondents ranked “Inflation and economic outlook in the U.S.” and “Managing the forced labor risks in the supply chain” as their top business challenges in 2024.

The issues of “Shipping delays and supply chain disruptions” and “Managing geopolitics and other political instability related to sourcing” have newly emerged among respondents’ top five concerns in 2024.

About 45 percent of respondents rated “Protectionist trade policy agenda in the United States” as a top five business challenge this year, a jump from only 15 percent in 2023.

#2 U.S. fashion companies leverage sourcing diversification to respond to the growing sourcing risks and market uncertainty in 2024.

Nearly 70 percent of large-sized companies with 1,000+ employees reported sourcing from ten or more countries, significantly higher than the 45-55 percent range in the past few years. It also has become more common for medium to small-sized companies with fewer than 1,000 employees to source apparel from six or more countries in 2024 than in the past.

Nearly 80 percent of respondentsplan to source from the same number of countries or even more countries through 2026, aiming to mitigate sourcing risks more effectively. However, their approaches differ at the firm level—some U.S. fashion companies plan to work with fewer vendors, while others intend to source from more.

#3 Managing the risk of forced labor in the supply chain continues to be a top priority for U.S. fashion companies in 2024.

U.S. fashion companies have adopted a comprehensive approach to comply with UFLPA and mitigate forced labor risks. On average, each surveyed company has implemented approximately six distinct practices across various aspects of their business operations this year, up from an average of five in 2023.

More than 90 percent of respondents say they are “Making more efforts to map and understand our supply chain, including the sources of fibers and yarns contained in finished products.” Notably, nearly 90 percent of respondents report mapping their entire apparel supply chains from Tier 1 to Tier 3 in 2024, a significant increase from about 40 percent in the past few years.

More than 80 percent of respondents say they “intentionally reduce sourcing from high-risk countries” in response to the UFLPA’s implementation. Another 75 percent of respondents explicitly state that their company has “banned the use of Chinese cotton in the apparel products” they carry.

About 45 percent of respondents have been actively “exploring sourcing destinations beyond Asia to mitigate forced labor risks.” However, this year, fewer respondents (i.e., under 10 percent) plan to cut apparel sourcing from Asian countries other than China directly, implying a more targeted and balanced approach to mitigating risks and meeting sourcing needs.

Based on field experience, respondents call for greater transparency in U.S. Customs and Border Protection (CBP)’s UFLPA enforcement, specifically in shipment detention and release decisions and in targeted entities and commodities information. Respondents also suggested that CBP reduce repeated detentions, focus on “bad actors” only, clarify enforcement on recycled cotton, and continue to partner with U.S. fashion companies on UFLPA enforcement.

#4 U.S. fashion companies remain deeply concerned about the deteriorating U.S.-China bilateral relationship and plan to further “reduce China exposure” to mitigate risks.

A record 43 percent of respondents sourced less than 10 percent of their apparel products from China this year, compared to only 18 percent in 2018. Likewise, nearly 60 percent of respondents no longer use China as their top apparel supplier in 2024, much higher than the 25-30 percent range before the pandemic.

Respondents rated China as economically competitive as an apparel sourcing base compared to many of its Asian competitors regarding vertical manufacturing capability, relatively low minimum order quantity (MOQ) requirements, flexibility and agility, sourcing costs, and speed to market. However, non-economic factors, particularly the perceived high risks of forced labor and geopolitical tensions, are driving U.S. fashion companies to move sourcing out of China. This trend applies to surveyed U.S. fashion companies selling products in China.

Nearly 80 percent of respondents plan to reduce their apparel sourcing from China further over the next two years through 2026. Consistent with last year’s results, large-size U.S. fashion companies with 1,000+ employees currently sourcing more than 10 percent of their apparel products from China are among the most eager to “de-risk.”

#5 U.S. fashion companies are actively exploring new sourcing opportunities, with a particular focus on emerging destinations in Asia and the Western Hemisphere.

This year, more respondents reported sourcing from India (89 percent utilization rate) than from Bangladesh (86 percent utilization rate) for the first time since we began the survey. Also, nearly 60 percent of respondents plan to expand apparel sourcing from India over the next two years, exceeding the planned expansion from any other Asian country.

For the second year in a row, three non-Asian countries made it to the top ten most utilized apparel sourcing destination list in 2024, including Guatemala (ranked 7th), Mexico (ranked 7th), and Egypt (ranked 10th). All three countries also witnessed an improved utilization rate in 2024 compared to last year’s survey results.

This year, a new record 52 percent of respondents plan to expand apparel sourcing from members of the Dominican Republic-Central American Free Trade Agreement (CAFTA-DR), over the next two years, up from 40 percent in 2023. However, most U.S. fashion companies consider expanding near-shoring from the Western Hemisphere as part of their overall sourcing diversification strategy. For example, nearly ALL companies that plan to increase sourcing from CAFTA-DR over the next two years also plan to increase sourcing from Asia.

75 percent of respondents identified the “lack of sufficient access to textile raw materials” as the main bottleneck preventing them from sourcing more apparel from CAFTA-DR members. Respondents say the local manufacturing capability for yarns and fabrics using fiber types other than cotton and polyester, such as spandex, nylon, viscose, rayon, and wool, was modest or low in the CAFTA-DR region, even when including the United States.

The U.S.-Mexico-Canada Trade Agreement (USMCA) entered into force on July 1, 2020, replacing the North American Free Trade Agreement (NAFTA). Within the context of expanding nearing-shoring from the Western Hemisphere, in 2024, about 65 percent of respondents reported sourcing from Mexico and Canada (or USMCA members), a noticeable increase from about 40 percent in 2019-2020. About 36 percent of respondents say their companies “expanded apparel sourcing from USMCA members because of the agreement.”

#6 Respondents underscore the importance of immediate renewal of AGOA before its expiration in September 2025 and extending the agreement for at least another ten years.

This year, respondents reported sourcing from seven AGOA members or countries in Sub-Saharan Africa (SSA), including Lesotho, Ethiopia (note: lost AGOA eligibility in 2022), Kenya, Madagascar, Mauritius, Tanzania, and Ghana, an increase from four countries in 2023, and six countries in 2022. Most respondents sourcing from AGOA in 2024 are typically large-scale U.S. fashion brands or retailers with 1,000+ employees. Generally, these companies treat AGOA as part of their extensive global sourcing network.

Over 86 percent of respondents support renewing AGOA for at least another ten years, and none object to the proposal. This reveals U.S. fashion companies’ strong support for the trade preference program and the non-controversial nature of continuing this agreement.

Over 70 percent of respondentssay another 10-year renewal of AGOA is essential for their company to expand sourcing from the region.

About 30 percent of respondents reported that they had already held back sourcing from AGOA members due to the pending renewal of the agreement and associated policy uncertainty. This figure could increase to half of the respondents if AGOA is not renewed by the end of 2024.

Another 30 percent of respondents indicate that keeping the flexible rules of origin in AGOA, such as the “third country fabric provision” for least-developed members, is essential for their company to source from the region.

Other topics the report covered include:

5-year outlook for the U.S. fashion industry, including companies’ hiring plan by key positions

The competitiveness of major apparel sourcing destinations in 2024 regarding sourcing cost, speed to market, flexibility & agility, minimum order quantity (MOQ), vertical integration and local textile manufacturing capability, social and environmental compliance risks and geopolitical risks (assessed by respondents)

Respondents’ detailed sourcing portfolio in 2024 for garments and textile materials (i.e., yarns, fabrics and accessories)

Respondents’ latest strategies to mitigate forced labor risks in the supply chain and fashion companies’ suggestions for CBP’s UFLPA enforcement based on field experience

U.S. fashion companies’ latest social responsibility and sustainability practices related to sourcing

U.S. fashion companies’ trade policy priorities in 2024

About the study

This year’s benchmarking study was based on a survey of executives from 30 leading U.S. fashion companies from April to June 2024. The study incorporated a balanced mix of respondents representing various businesses in the U.S. fashion industry. Approximately 80 percent of respondents were self-identified retailers, 60 percent were self-identified brands, 41 percent were importers/wholesalers, and 3 percent were manufacturers.

The survey respondents included large U.S. fashion corporations and medium-sized companies. Around 80 percent of respondents reported having over 1,000 employees; the rest (20 percent) represented medium-sized companies with 100-999 employees.

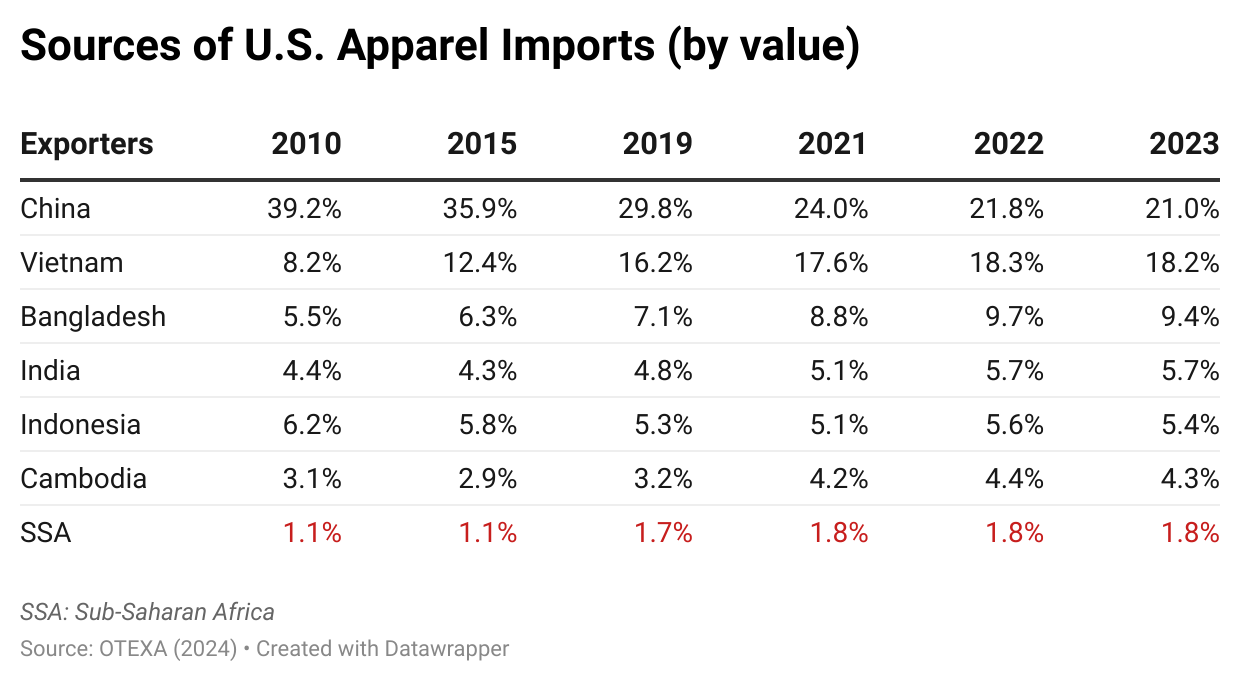

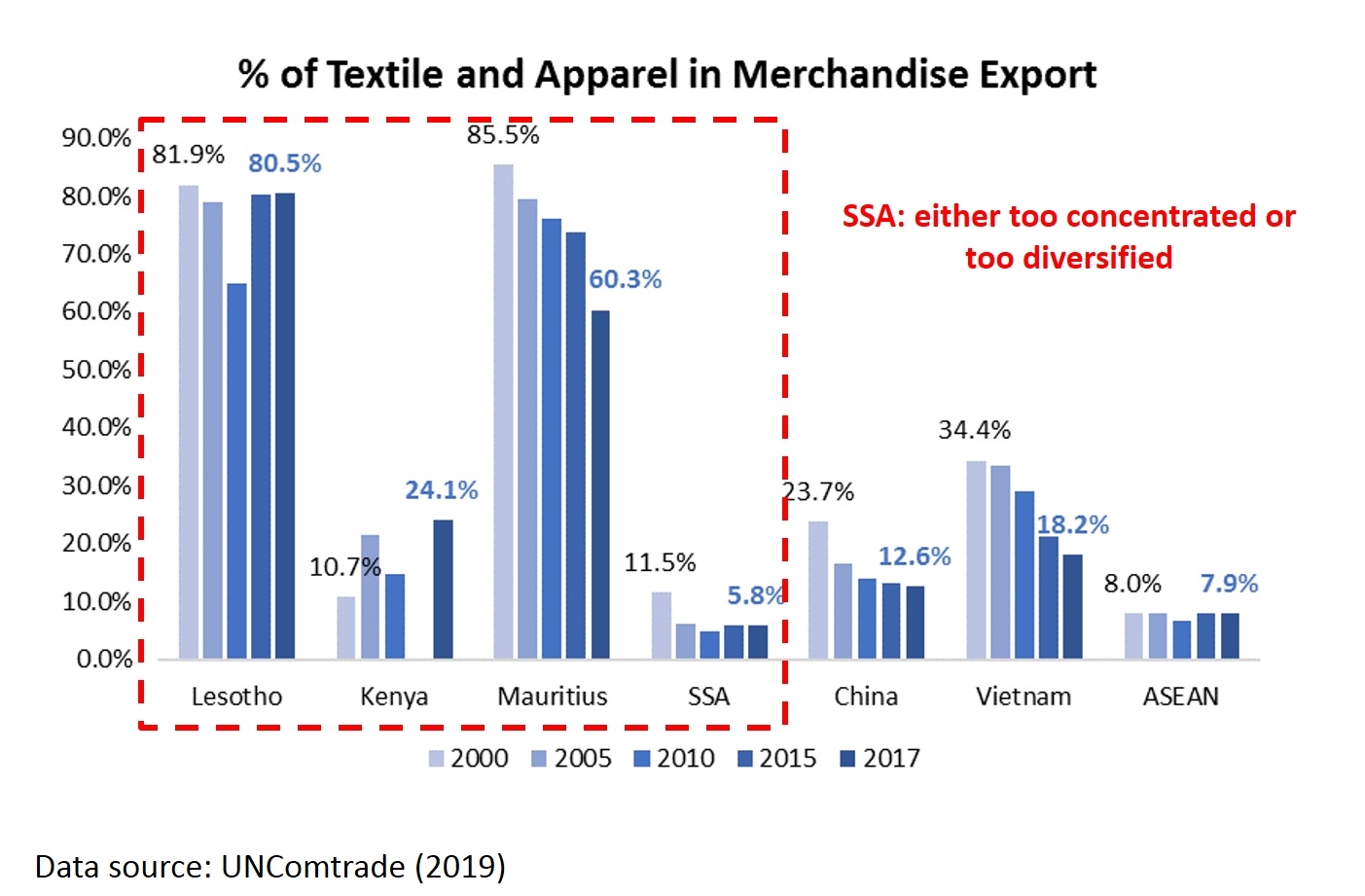

The prospect of Sub-Saharan Africa (SSA) as an apparel-sourcing base for U.S. fashion companies has been a growing heated debate. On the one hand, U.S. fashion companies, driven by increasing geopolitical concerns and other market factors, were eager to diversify apparel sourcing away from Asia. The SSA region was often regarded as one of the most popular alternative sourcing destinations thanks to its large population, relatively low labor costs, and shorter shipping distance to U.S. ports compared to most Asian. The African Growth and Opportunity Act (AGOA), a trade preference program enacted in 2000, in particular, allowed eligible apparel exports from SSA countries to enter the United States import duty-free, creating substantial financial incentives for U.S. fashion companies to source from the SSA region.

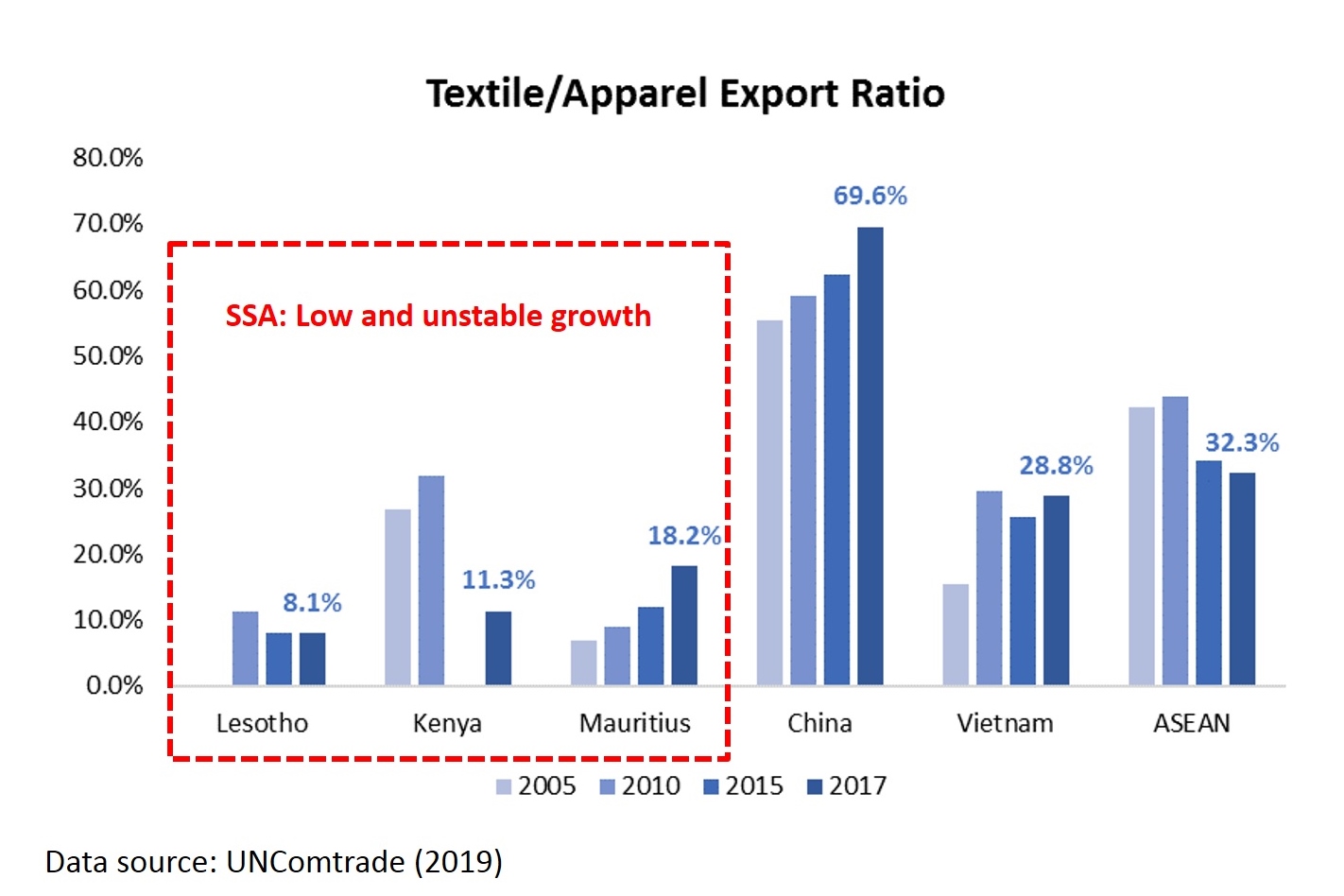

However, empirical trade data shows that U.S. apparel imports from SSA members have stagnated over the past decades without evident growth. Notably, with little change from 2010, SSA countries collectively accounted for only 1.8% of U.S. apparel imports in 2023, with no single SSA member achieving a market share of more than 1%. In contrast, over the same period, despite China’s declining market shares, the following five largest Asian suppliers—Vietnam, Bangladesh, India, Indonesia, and Cambodia—jointly accounted for 43.0% of U.S. apparel imports in 2023, a notable increase from 27.4% in 2010.

This study aims to evaluate SSA countries’ capacity to serve as an alternative apparel sourcing destination to Asian suppliers for US fashion companies. Specifically, the study examined the detailed product information of a total of 10,000 stock keeping units (SKUs) of clothing items sold in the U.S. retail market from January 2021 to December 2023. Half of these items were sourced from the six largest apparel-exporting countries in SSA: Lesotho, Kenya, Mauritius, Ethiopia, Madagascar, and Tanzania. Together, these countries accounted for over 96% of the value of U.S. apparel imports from the SSA region between 2021 and 2023. The remaining half came from China, Vietnam, Bangladesh, Cambodia, India, and Indonesia, the six largest Asian apparel exporters, which stably accounted for approximately 90% of U.S. apparel imports from Asia over the past decade.

Key findings:

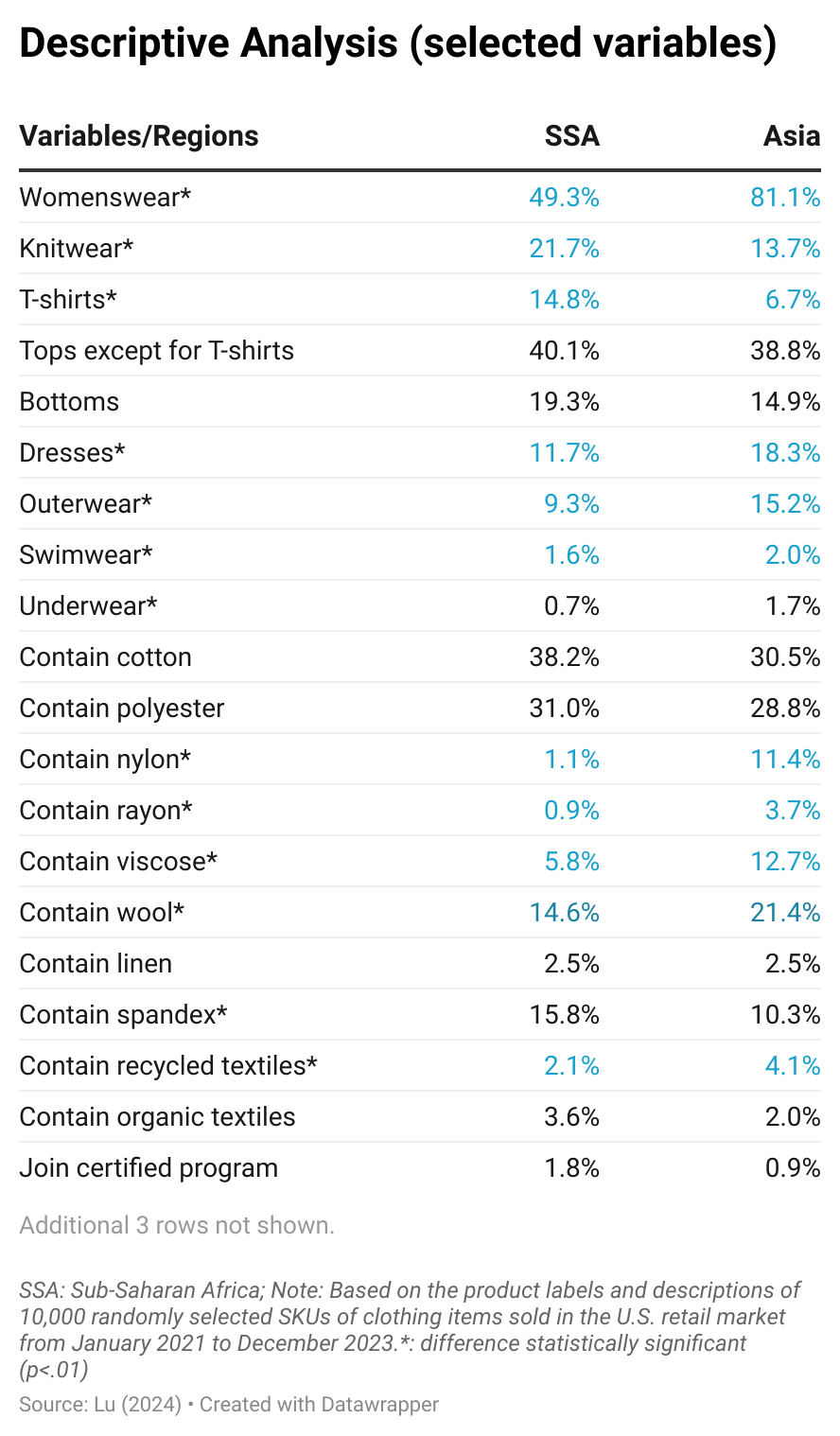

First, the results revealed that U.S. fashion companies’ sourcing strategies for SSA countries appeared more subtle and complicated than simply treating the region as another low-cost sourcing destination, as suggested by previous studies. Instead, according to the results, U.S. fashion companies seemed to leverage SSA countries as suppliers of “niche products,” such as those relatively simple and basic apparel categories containing African cultural elements and targeting the luxury and premium market segment. Meanwhile, the demand for such products could be much smaller than regular apparel items sold in the value and mass market. This allows SSA countries to fulfill these smaller orders despite their limited production capacity, often family-owned or involving handmade processes.

Second, the study’s findings identified significant challenges for SSA countries serving as immediate alternatives to sourcing from Asia for U.S. fashion companies. While SSA countries could offer relatively low sourcing costs, the range of apparel products available for U.S. fashion companies to source from the SSA region remained significantly more limited than those from Asia. For example, results show that U.S. fashion companies preferred sourcing relatively basic and technologically simple categories like knitwear, T-shirts, and bottoms from SSA countries. However, imports from SSA countries offered more limited sizing and color choices and were less likely to include womenswear and relatively more sophisticated or specialized product categories such as outerwear and swimwear. As another example, U.S. apparel imports from SSA countries were primarily made of cotton and polyester, with less use of other fiber types, including nylon, rayon, viscose, wool, and those made from recycled textile materials (see table below).

Third, building on the previous point, the results call for new thinking on strengthening SSA countries’ genuine competitiveness as an apparel-sourcing destination. Over the past decades, trade preference programs such as AGOA have mainly focused on improving the price competitivenessof SSA countries’ apparel exports. However, as this study’s findings illustrate, AGOA and other trade preference programs seemed inadequate in assisting SSA countries in developing capacity beyond basic apparel categories and securing a sufficient variety of textile materials. As U.S. fashion companies have placed greater emphasis on factors beyond price in their sourcing decisions, such as flexibility, agility, sustainability, and vendors’ capability to make a wide variety of products, this could put SSA countries at even more significant disadvantages down the road to being considered alternatives to Asia for apparel sourcing.

The results also reminded us that AGOA’s liberal rules of origin, which allowed least-developed SSA countries to use textile materials from anywhere worldwide, cannot replace the crucial need to develop the local textile manufacturing capacity within the SSA region. Without a robust local textile manufacturing sector, SSA countries would encounter significant challenges in diversifying their product offerings to include more complex and versatile clothing categories, such as outerwear and women’s dresses. These categories typically require a wide variety of raw textile materials and accessories, making it highly impractical and inefficient to rely solely on imports for their supply.

On the other hand, the findings reveal the necessity of creating a stable and foreseeable business environment, such as the long-term renewal of AGOA, to attract more long-term investments in SSA. For example, investing in and strengthening SSA countries’ local supply of sustainable textile materials, such as recycled or organic fibers, could strategically enhance SSA countries’ competitiveness in meeting the increasing demand from U.S. fashion companies for sustainable apparel products.

The full article is available HERE and below is the summary:

With consumers’ growing demand for sustainable apparel products, fashion companies increasingly carry clothing made from recycled textile materials and seek additional supply bases. Recycled cotton has great potential for use in garments because of the wide availability of cotton-made secondhand clothing and the perceived positive environmental impacts of effectively recycling post-consumption cotton waste.

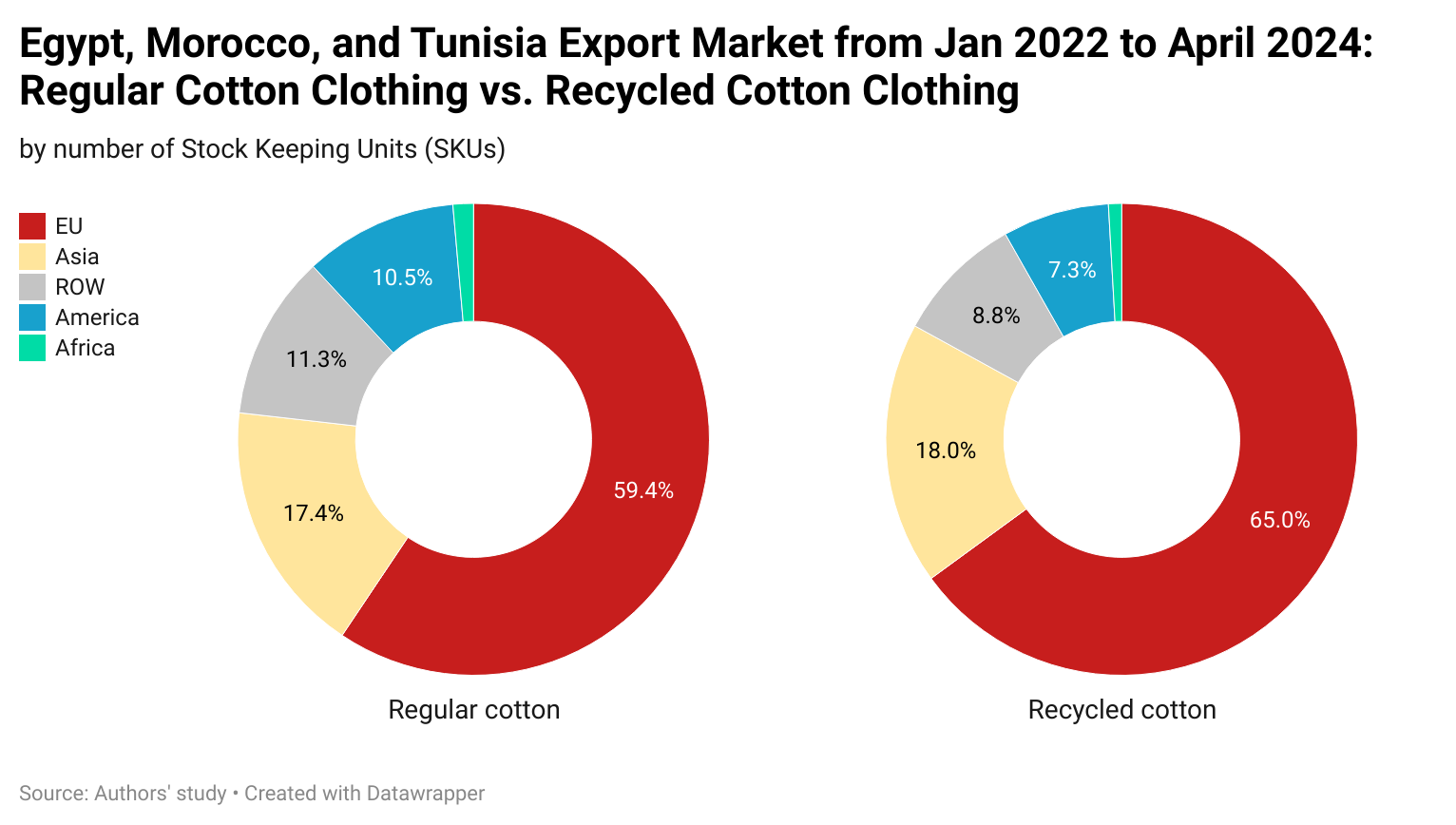

This study explores Egypt, Morocco, and Tunisia’s potential as sourcing bases for clothing made from recycled cotton. North African countries, including Egypt, Morocco, and Tunisia, have a long history of making and exporting cotton and cotton-made finished garments. The “developing country” status and membership in trade agreements or trade preference programs, such as the African Growth and Opportunity Act (AGOA) and the EU-Mediterranean Association Agreement, allow apparel products from these three countries to enjoy preferential duty benefits in the world’s top import markets. Therefore, there is great potential to capitalize on recycled cotton apparel and “green exports” to further promote economic development in the region.

About 13,000 Stock Keeping Units (SKUs) of clothing items made by these three countries newly launched to the world retail market between January 2022 and April 2024 were randomly captured from fashion brands and retailers’ websites. About half of the items were made of regular cotton, and the other half explicitly mentioned using “recycled cotton” in the product label or description. The results show that:

#1: Egypt, Morocco, and Tunisia have gradually expanded their clothing exports made from recycled cotton since 2022. For example, as estimated, about 1,300 SKUs of clothing using recycled cotton from these three countries were newly launched to the US and EU retail markets in 2023, a substantial increase from only 150 SKUs back in 2022 (or a sevenfold increase). Similarly, in the first four months of 2024, clothing using recycled cotton accounted for 10.2% of total cotton apparel from the three countries in the US and EU markets, a substantial increase from only 1.1% in 2022.

#2: Of the collected samples, apparel using recycled cotton from Egypt, Morocco, and Tunisia was destined for as many as 49 countries, reflecting the global demandfor such products. However, possibly restrained by the limited supply, the export market for clothing using recycled cotton remained less diverse than that for clothing made of regular cotton, which spanned 72 countries.

#3: Geographically, the European Union (EU) was the top clothing export market for Egypt, Morocco, and Tunisia, accounting for over 75% of these countries’ export value in 2022, according to UN trade statistics (UNComtrade). This was also the case for recycled cotton products. Specifically, the EU accounted for 65% of these three countries’ total recycled cotton clothing exports measured in SKUs in the collected samples, higher than 59.4% of regular cotton clothing products.

#4: Egypt, Morocco, and Tunisia focused on different product categories for clothing using recycled cotton than those made from regular cotton. Specifically, of the sampled items, clothing using recycled cotton had a notable concentration on bottoms (52.9%), followed by tops other than T-shirts (23.8%). Recycled cotton clothing also was more commonly used for outerwear (7.5%) than those using regular cotton (3.8%). In comparison, only about 7.9% of clothing using recycled cotton were T-shirts, much fewer than nearly 30% of those using regular cotton. Similarly, specific product categories, such as underwear and hosiery, rarely use recycled cotton. Likely, the concerns for quality and durability and the difficulty of absorbing higher production costs make using recycled cotton for these relatively simple categories more challenging.

#5: Even though cotton apparel made in Egypt, Morocco, and Tunisiaalready commonly mentioned their sustainability attributes (86%), phrases such as “sustainability” and “sustainable” appeared even more frequently in clothing using recycled cotton (94.6%). For example, some producers highlighted that they “worked with suppliers, workers, unions and international organizations” to ensure their recycled cotton clothing contributed to “the United Nations Sustainable Development Goals.” Likewise, some labels intentionally remind consumers about the positive environmental impact of using recycled cotton, “The use of recycled cotton helps to limit the consumption of raw materials.” Another added, “The production of recycled cotton recovered cotton, mainly from the production of other garments, thus reducing the production of virgin spring and water consumption, energy and natural resources.”

Meanwhile, compared to clothing using regular cotton, those made with recycled cotton in Egypt, Morocco, and Tunisia reported much higher participation incertification programs, such as the Recycled Claim Standard (RCS), which verifies the recycled content and tracks it from source to final product.

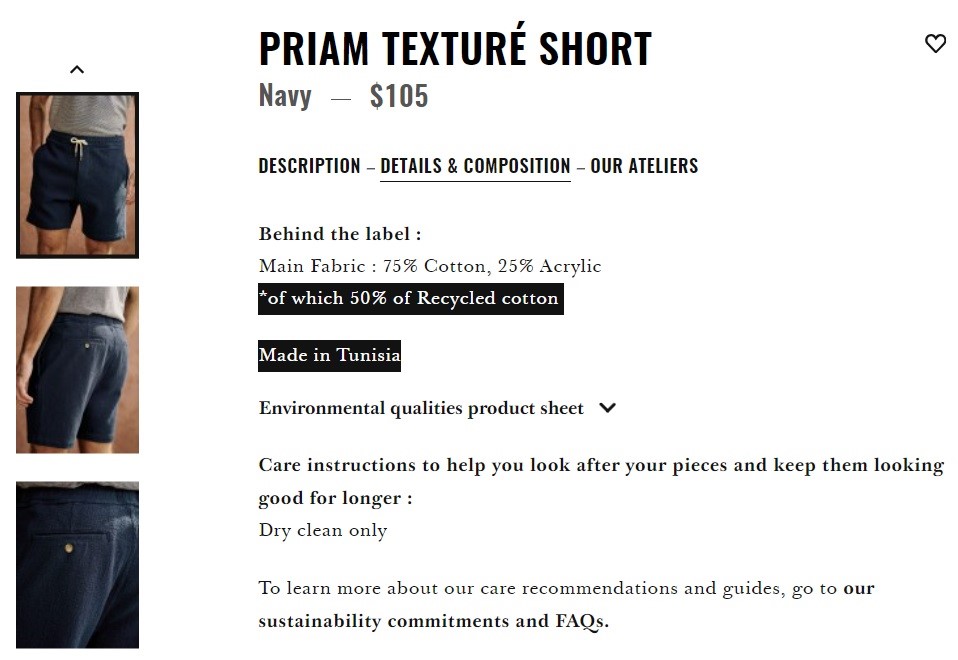

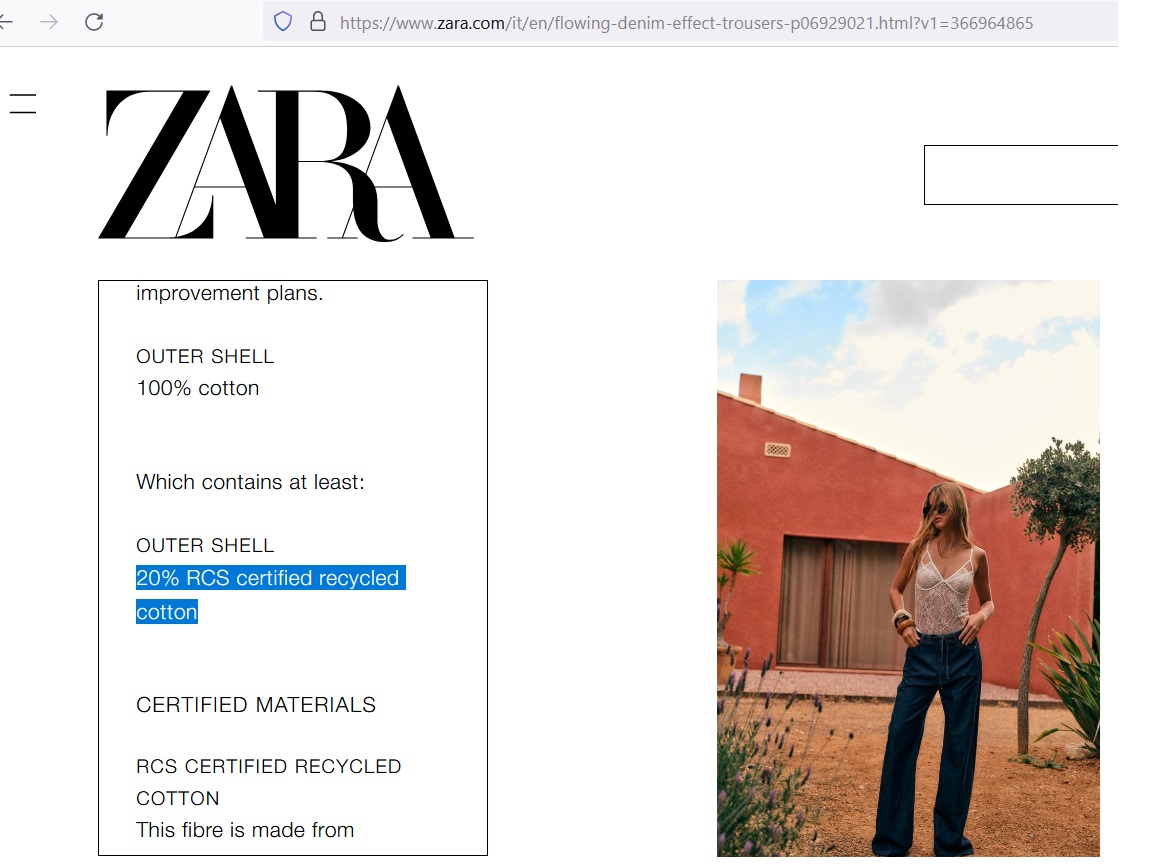

#6: Reflecting the technical limitations of the fiber property, it remains rare to have clothing that is 100% made from recycled cotton. According to industry experts, longer cotton fibers generally indicate higher quality. Since the recycling process shortens cotton fibers, regular virgin cotton or other fibers like polyester are typically used alongside recycled cotton to make fabrics smoother, stronger, and more durable. For example, common labels include descriptions such as “80% virgin cotton, 20% RCS certified recycled cotton” and “55% RCS certified recycled polyester, 45% RCS certified recycled cotton.”

#7: Except for T-shirts, in most cases, clothing made from recycled cotton in Egypt, Morocco, and Tunisia was priced lower than their equivalent using virgin fiber in the market. This is particularly the case for the premium and luxury market segments, where clothing using recycled fiber typically was 20-30% lower priced than regular clothing. The results echo the findings of numerous studies indicating that consumers are generally unwilling to pay higher prices for recycled fiber clothing as they perceive such products as lower quality and less “valuable.” Also, more needs to be done to create more financial incentives for producers in Egypt, Morocco, and Tunisia to expand the production scale and increase the use of recycled cotton in their products.

With consumers’ growing awareness of the environmental impacts of clothing production and consumption, retailers in Europe (EU) have expressed a heightened interest in selling clothing using recycled textile materials (referred to as “recycled clothing” in this study). For example, fast fashion giants like H&M and Zara and luxury brands such as Hugo Boss have started carrying recycled clothing, aiming to integrate circularity into their product designs and business models.

In the study, we examined retailers’ sourcing strategies for clothing made from recycled textile materials in five European countries, including the United Kingdom (UK), Italy, France, Germany, and Spain. These five countries represent the EU’s largest clothing retail markets, consistently accounting for over 60% of the region’s total apparel sales.

Through an industry source using web crawling techniques and manual verification, 5,000 Stock Keeping Units (SKUs) of clothing items made from recycled textile materials were randomly selected and analyzed. These items were sold by retailers in the UK, Germany, Italy, France, and Spain between January 2021 and May 2023.

The results show that Firist, EU retailers sourced clothing using recycled textile materials from diverse sources, including over 40 developing and developed countries across Asia, America, Europe, and Africa. Second, other than assortment diversity (i.e., the number of color or sizing options for a clothing item), no statistical evidence shows that developing countries had advantages over developed ones regarding product sophistication, replenishment frequency, and pricing for recycled clothing in the five EU markets. Third, a supplying country’s geographic location statistically affects the type of recycled clothing EU retailers import. For example, retailers in the five EU countries typically adopt the following sourcing portfolio by region:

Asia: relatively sophisticated clothing items (e.g., dresses and outerwear) targeting the mass and value market.

America (North, South, and Central): relatively simple clothing categories (e.g., T-shirts and socks) targeting the mass and value market.

Europe: sophisticated clothing categories primarily for the luxury or premium market

Africa: relatively simple clothing categories targeting the premium market

The findings offered new insights into the business aspects of recycled clothing, particularly regarding its intricate supply chains and leading suppliers. The study’s results have several additional important implications.

First, while existing studies often suggest “local for local” textile recycling, the study’s findings revealed promising global sourcing opportunities for clothing using recycled textile materials. Particularly, leveraging a diverse sourcing base would allow EU retailers to take advantage of each supplying country’s unique production strength regarding product categories and assortment features and more efficiently balance various sourcing factors ranging from costs and flexibility to speed to market. Meanwhile, the study’s findings indicate that many countries worldwide have begun producing and exporting clothing using recycled textile materials, and the sourcing options and capacities will hopefully continue to grow.

Second, according to the study’s findings, unlike the patterns of making regular garments using virgin fiber, low-wage developing countries demonstrated no noticeable competitive edges over developed economies regarding producing and exporting clothing using recycled textile materials. Instead, developed economies, including many high-wage Western EU countries, emerged as top suppliers and leading sourcing destinations for recycled clothing. Thus, expanding clothing production using recycled textile materials presents an exciting economic opportunity with a promising future in developed countries, where many have plans to revitalize the domestic manufacturing sector and establish a sustainable circular economy.

Third, building on the previous point, the sustained commitment of fashion brands and retailers to carry more clothing made from recycled textile materials in their product assortment could hold significant implications for the future landscape of global apparel trade and sourcing patterns. For example, whereas apparel products are predominantly exported from developing to developed countries today, more trade flows could occur between developed economies in the future, attributed to their increasing production capacity and growing demand for clothing using recycled textile materials. Similarly, major apparel exporters in Asia, such as China and Bangladesh, might assume a less dominant role as a sourcing base for recycled clothing due to their insufficient infrastructure for efficiently sorting used clothing and generating high-quality recycled textile materials.

By Leah Marsh and Sheng Lu

Discussion questions proposed by FASH455:

#1 How might EU fashion companies’ sourcing strategies change as they increase carrying clothing made from recycled textile materials?

#2 Could the US emerge as a leading sourcing destination for clothing made from recycled textile materials? What are the potential advantages and disadvantages?

#3 Is expanding clothing made from recycled textile materials the right approach to achieve fashion sustainability? What is your thought?

Below are selected comments by US Trade Representative Katharine Tai (Tai) and WTO (World Trade Organization) Director-General Dr. Ngozi Okonjo-Iweala (Ngozi).

What kind of global trade do we want today?

“For decades, the United States has been proud to champion the international rules-based order and the multilateral trading system…But the functioning and fairness of this order are now in question and that is why all of us need to adapt to a more challenging era marked by rapid technological change, increasing extreme climate events, vulnerable supply chains, intensifying geopolitical friction, widening inequality” (Tai)

“The United States is writing a new story on trade. We are pursuing fair competition, addressing the climate crisis, promoting our national security, and ensuring the rules-based system helps all economies, not just the biggest ones.” (Tai)

“how can we harness the effectiveness of our trade tools to be promoting not just efficiency and liberalization, but using those tools to promote what we consider certainly today to be higher goals. And those goals are resilience for our economy and the word economy, sustainability, again, for our economy in the world economy, and inclusivity… we started to see where the concentrations in supply and production started to impact this and spike this economic insecurity on a macro level and also for individuals” (Tai)

Trade and climate change

“trade is necessary to disseminate green technologies and through competition and scale efficiencies to drive down the cost of decarbonization. Another reason is that trade amplifies the impact of environmental policy action. Recent research at the WTO demonstrate that just as countries can reap economic gains by focusing on what they are relatively good at, the world can reap environmental gainsif countries focus on what they are relatively green at” (Ngozi)

Is trade diversification the future?

“A fragmented world economy would not just be bad for already-squeezed household budgets. Without trade, it would become harder, even impossible, to meet the big challenges of our time – resilience, socioeconomic inclusion, and climate change… The problems we encountered in the trading system were less about trade per se and more about excessive concentration for some products and supply relationships. The smart response is to deepen, diverse, and deconcentrate production so there are fewer potential bottlenecks” (Ngozi)

“we believe we can solve the problem by diversifying the supply chains not just to ourselves or to friends but to all over the world where the opportunity exists. Business should look at the possibility of not just doing China+1. It means China plus Vietnam or Indonesia. But they can do Bangladesh. They can do Laos. They can do Rwanda. They can do Senegal. They can do Nigeria. I’m just – Morocco” (Ngozi)

Debate the impact of trade

“Technology was generally a big culprit in job losses…U.S. manufacturing output, the volume of products produced here, is about as high as it has ever been. But the sector employs more machines and fewer people than it used to. Nevertheless, import competition was a significant factor and an easier focus, I think, for political anger.” (Ngozi)

“…between 1995 and 2011, while increased goods import from China did eliminate 2 million jobs in the United States, increased exports to China and elsewhere added 6.6 million jobs to the U.S. economy, 4 million of them from higher-services exports…These numbers illustrate the power of trade for job creation. But as we know, those new jobs were not created in the same places. Neither did they go to the same people. That a backlash would result from those left out was perhaps predictable, but it was not inevitable. There are countries that use domestic-policy levers to translate gains from trade into broadly shared growth by providing people security against income loss and support to seize new opportunities.” (Ngozi)

Renew or update the African Growth and Opportunity Act?

“The world is really different from when AGOA was first created…So I think copy-paste is to really lose an important opportunity…we should be practical. Also, we’re on a timeline…The AfCFTA, the African Continental Free Trade Area, that has been concluded, that has that has been brought into being by the countries on the continent. And those continental integration aspirations should absolutely be reflected in our offer to Africa, and something we should try to figure out how to incorporate” (Tai)

“African countries appreciate AGOA. They would like to see an agreement that is, you know, at least a decade out so that they have some predictability. What they’re hearing from investors is that with this up in the air, they can’t make up their minds whether to invest or not because they don’t know what will happen. So I think if we can reform and get it done, and people can have a predictable time horizon for AGOA, it would really help” (Ngozi)

How to reform the World Trade Organization?

“The United States wants a WTO where dispute settlement is fair and effective, and supports a healthy balance of sovereignty, democracy, and economic integration where all members embrace transparency, where we have better rules and tools to tackle non-market policies and practices, and to confront the climate crisis and other pressing issues.” (Tai)

“We must recognize the diversity of developing members. We should have flexibilities in the rules that reflect actual needs. But we cannot have economic and manufacturing powerhouses gaming the system by claiming the same development status and flexibilities intended for less-advantaged members.” (Tai)

“people ask me all the time, oh, are you worried because there are so many [Free trade agreement, FTA]? I’m not. Like I said, 75 percent of trade still goes on WTO terms [MFN tariff rates]. And we can learn from them.” (Ngozi)

“I don’t have enough time and money to waste resources in Geneva on a process that we don’t actually believe in…When President Biden talks about it from the floor of the United Nations General Assembly, if we still have trading partners who want to question our seriousness, then I think the problem is those partners and it’s not us” (Tai) [note: this comment was mentioned by Politico]

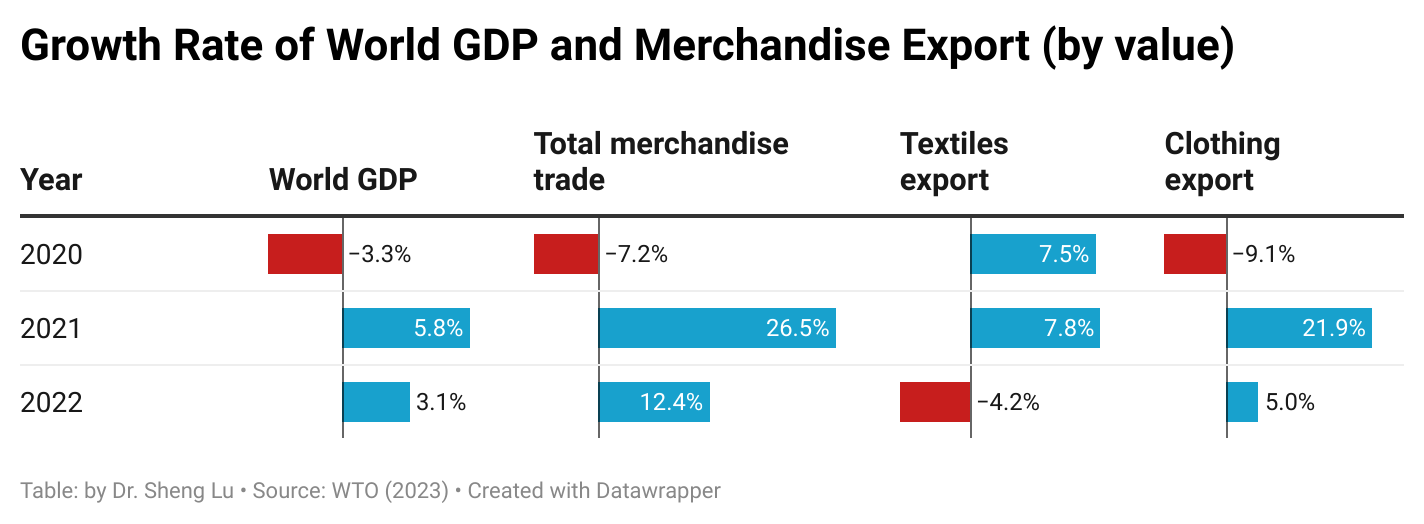

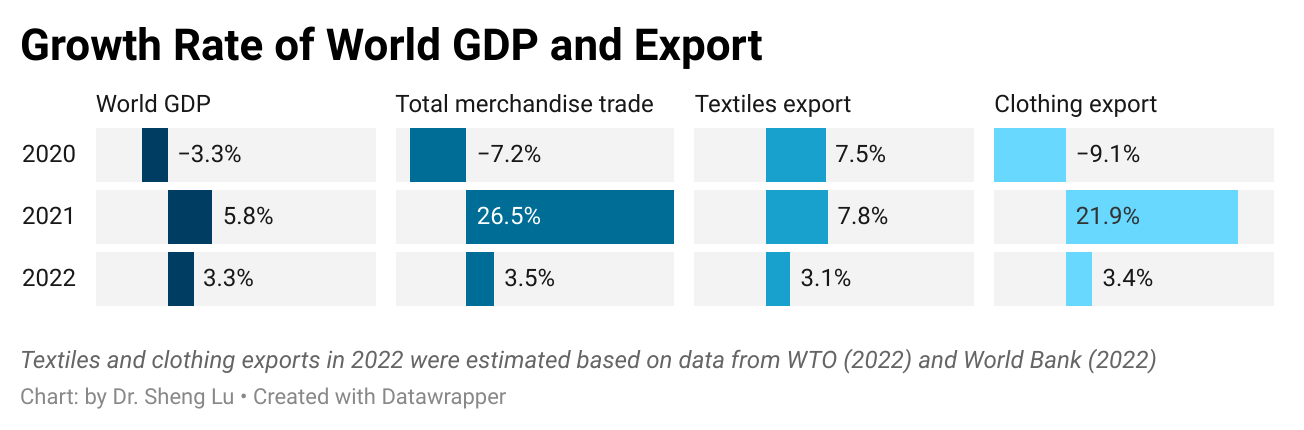

This article comprehensively reviewed the world textiles and clothing trade patterns in 2022 based on the newly released World Trade Organization Statistical Review 2023 and data from the United Nations (UNComtrade). Affected by the slowing world economy and fashion companies’ evolving sourcing strategies in response to the rising geopolitical tensions, mainly linked to China, the world’s textiles and clothing trade in 2022 displayed several notable patterns different from the past.

Pattern #1: The expansion of world clothing exports witnessed a notable deceleration in 2022, primarily attributed to the economic downturn. Meanwhile, the world’s textile exports decreased from the previous year, affected by the reduced demand for textile raw materials used to produce personal protective equipment (PPE) as the pandemic waned.

The world’sclothing exports totaled $576 billion in 2022, up 5 percent year over year, much slower than the remarkable 20 percent growth in 2021. The slowed economic growth plus the unprecedented high inflation in major apparel import markets, particularly the United States and Western European countries, adversely affected consumers’ available budget for discretionary expenditures, including clothing purchases.

The world’s textile exports fell by 4.2 percent in 2022, totaling $339 billion, lagging behind most industrial sectors. Such a pattern was understandable as the demand for PPE and related textile raw materials substantially decreased with the pandemic nearing its end.

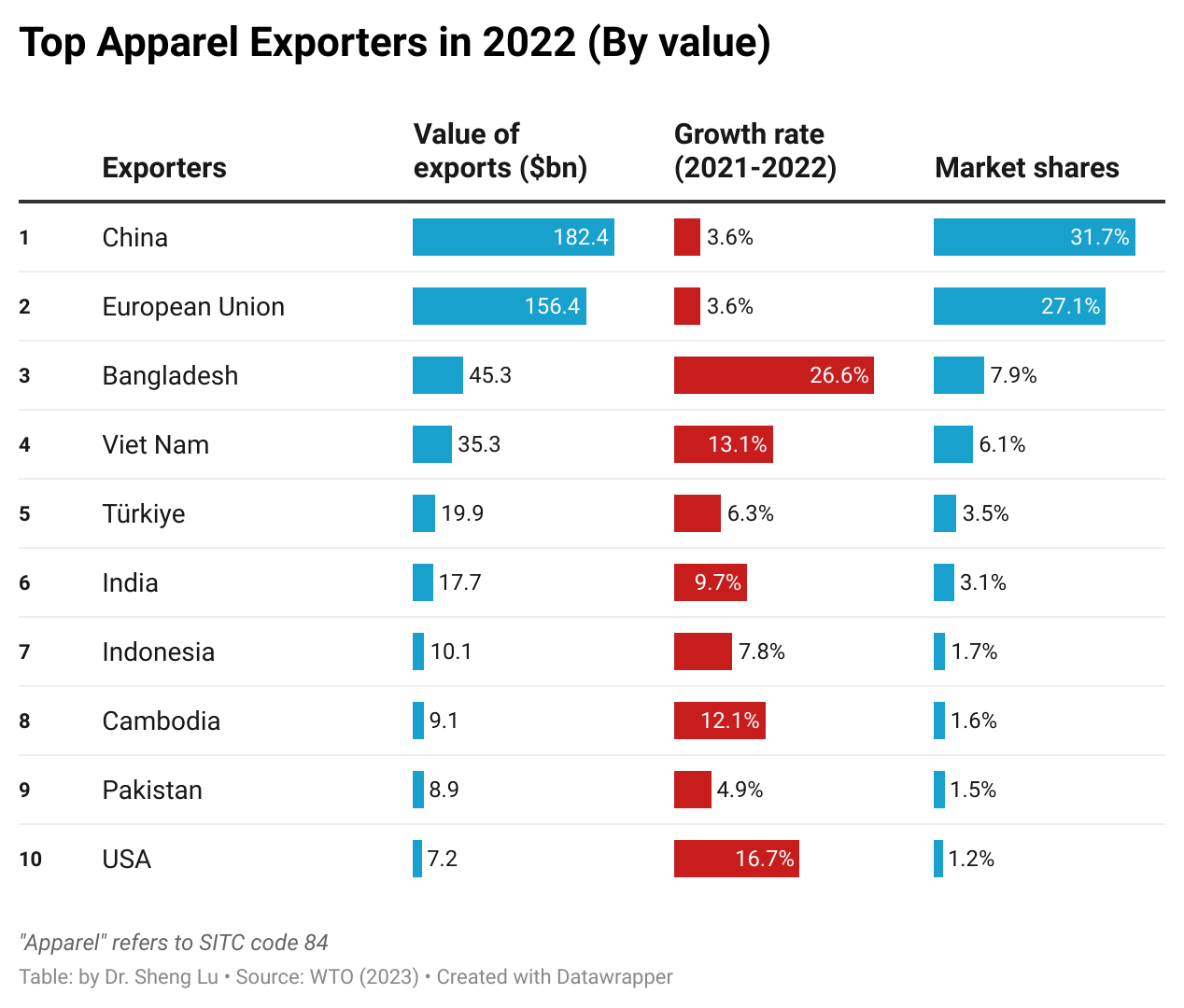

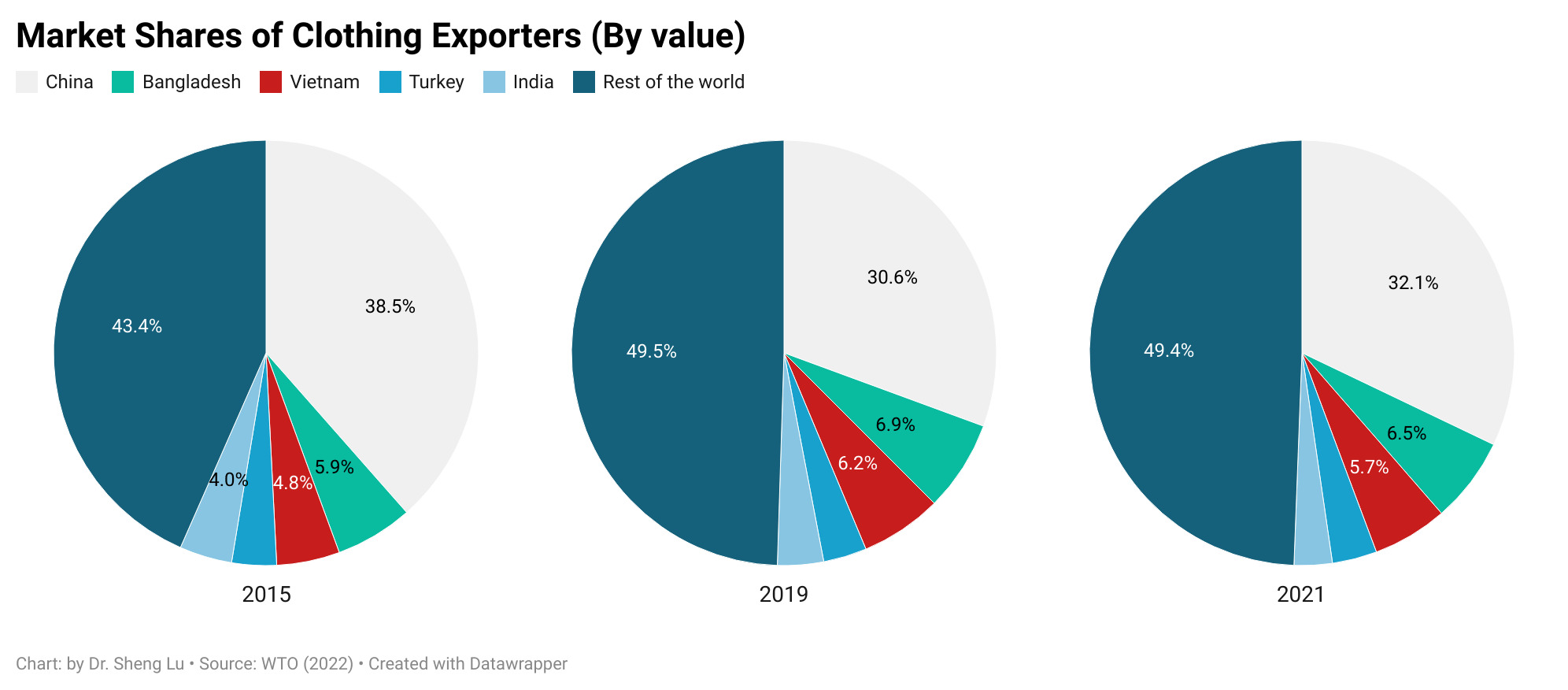

Pattern #2: China continued to lose market share in clothing exports, which benefited other leading apparel exporters in Asia. Notably, for the first time, Bangladesh surpassed Vietnam and ranked as the world’s second-largest apparel exporter in 2022.

In value, China remained the world’s largest apparel exporter in 2022. However, China’s clothing exports experienced a growth of 3.6 percent, below the global average of 5.0 percent, positioning China at the bottom of the top ten exporters.

China’s global market share in clothing exports dropped to 31.7 percent in 2022, marking its lowest point since the pandemic and a significant decrease from the approximate 38 percent recorded from 2015 to 2018. In fact, China lost market share in almost all major clothing import markets, including the US, the EU, Canada, and Japan. The concerns about the risks of forced labor linked to sourcing from China and the deteriorating US-China relations were among the primary factors driving fashion companies’ eagerness to reduce their ‘China exposure” further.

China has been diversifying its clothing exports beyond the traditional Western markets in response to the challenging business environment. For example, from 2021 to 2022, Asian countries, especially members of the Regional Comprehensive Economic Partnership (RCEP), became relatively more important clothing export markets for China. Nevertheless, since RCEP members primarily consist of developing economies with ambitions to enhance their own clothing production, the long-term growth prospects for their import demand of ‘Made in China’ clothing remain uncertain.

Bangladesh achieved a new record high in its market share of world clothing exports, reaching 7.9 percent in 2022, which exceeded Vietnam’s 6.1 percent. Many fashion companies regard Bangladesh as a promising clothing-sourcing destination with growth potential because of its capability to make cotton garments as China’s alternatives, competitive price, and reduced social compliance risks.

Fashion companies’ efforts to “de-risking from China” also resulted in the robust growth of clothing exports from other large-scale Asian clothing producers in 2022, including Vietnam (up 13 percent), Cambodia (up 12 percent), and India (up 10 percent). In other words, despite the concerns about China, fashion companies still treat Asia as their primary sourcing destination.

Pattern #3: Developed countries stay critical textile exporters, and middle-income developing countries gradually build new textile production and export capability.

The European Union members and the United States stayed critical textile exporters, accounting for 25.1 percent of the world’s textile exports in 2022, up from 24.5 percent in 2021 and 23.2 percent in 2020. Thanks to the increasing demand from apparel producers in the Western Hemisphere, U.S. textile exports increased by 5 percent in 2022, the highest among the world’s top ten.

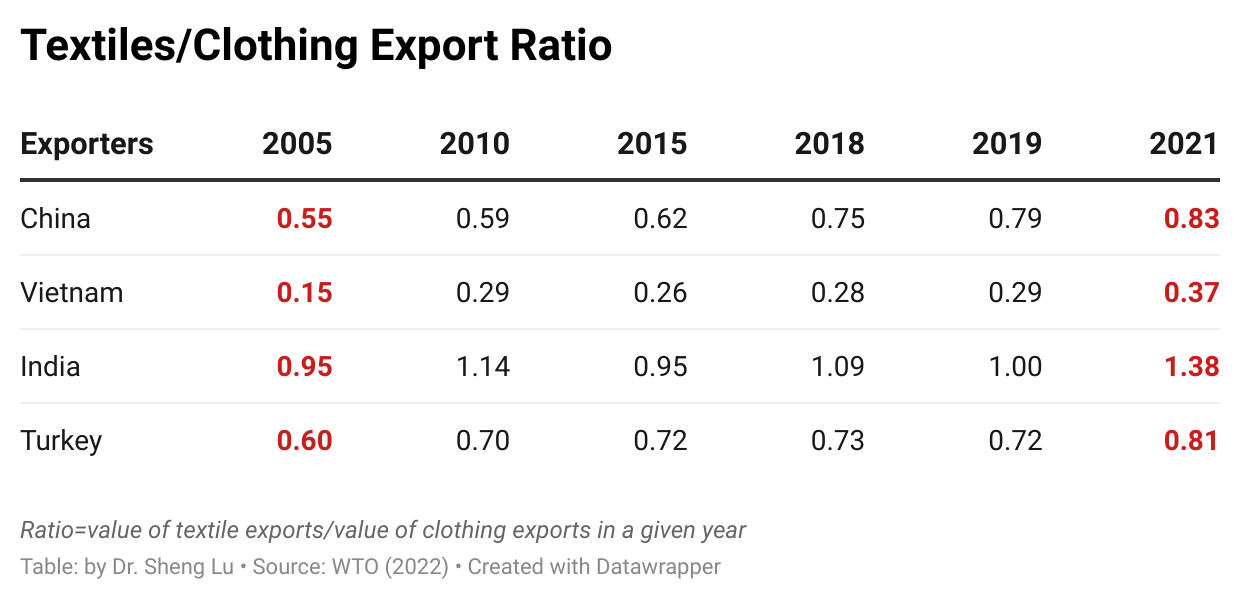

As a persistent long-term trend, middle-income developing countries have consistently been strengthening their textile production and export capability. For example, China, Vietnam, Turkey, and India’s market shares in the world’s textile exports have steadily risen. They collectively accounted for 56.8 percent of the world’s clothing exports in 2022, a notable increase from only 40 percent in 2010. Also, over time, these middle-income developing countries have achieved a more balanced textiles-to-clothing export ratio.

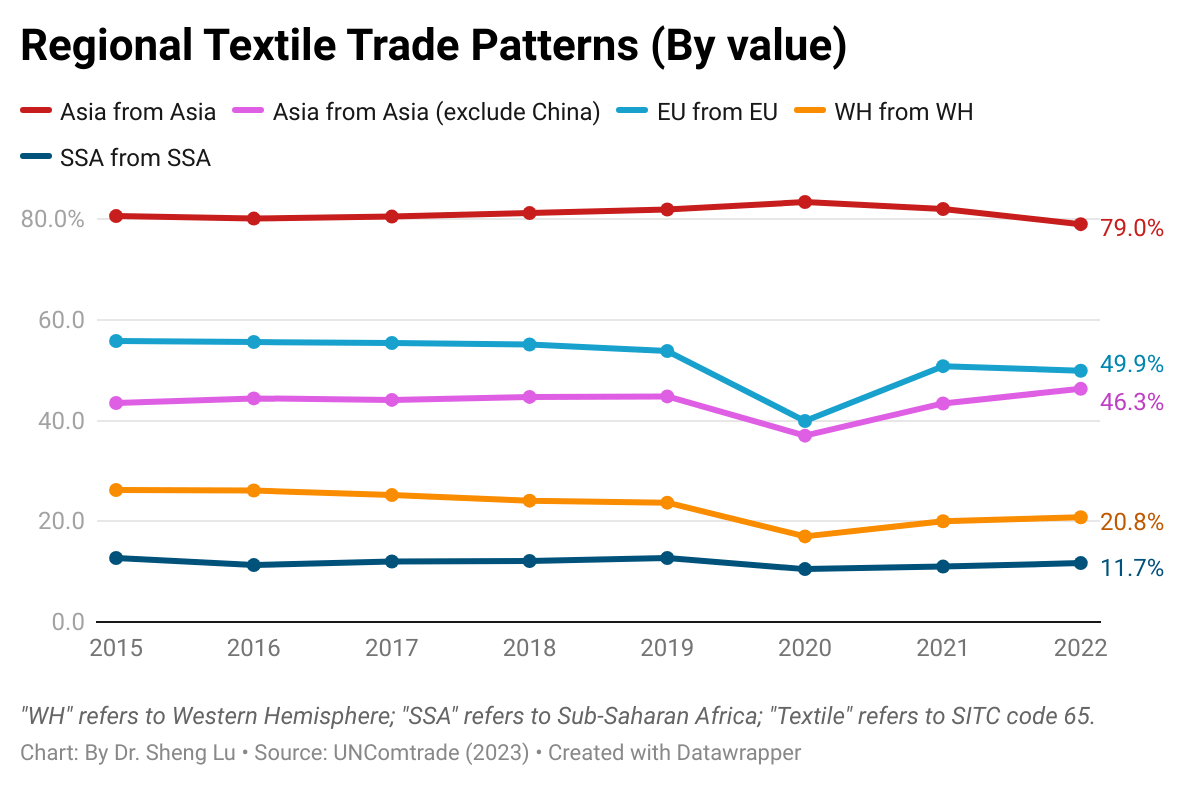

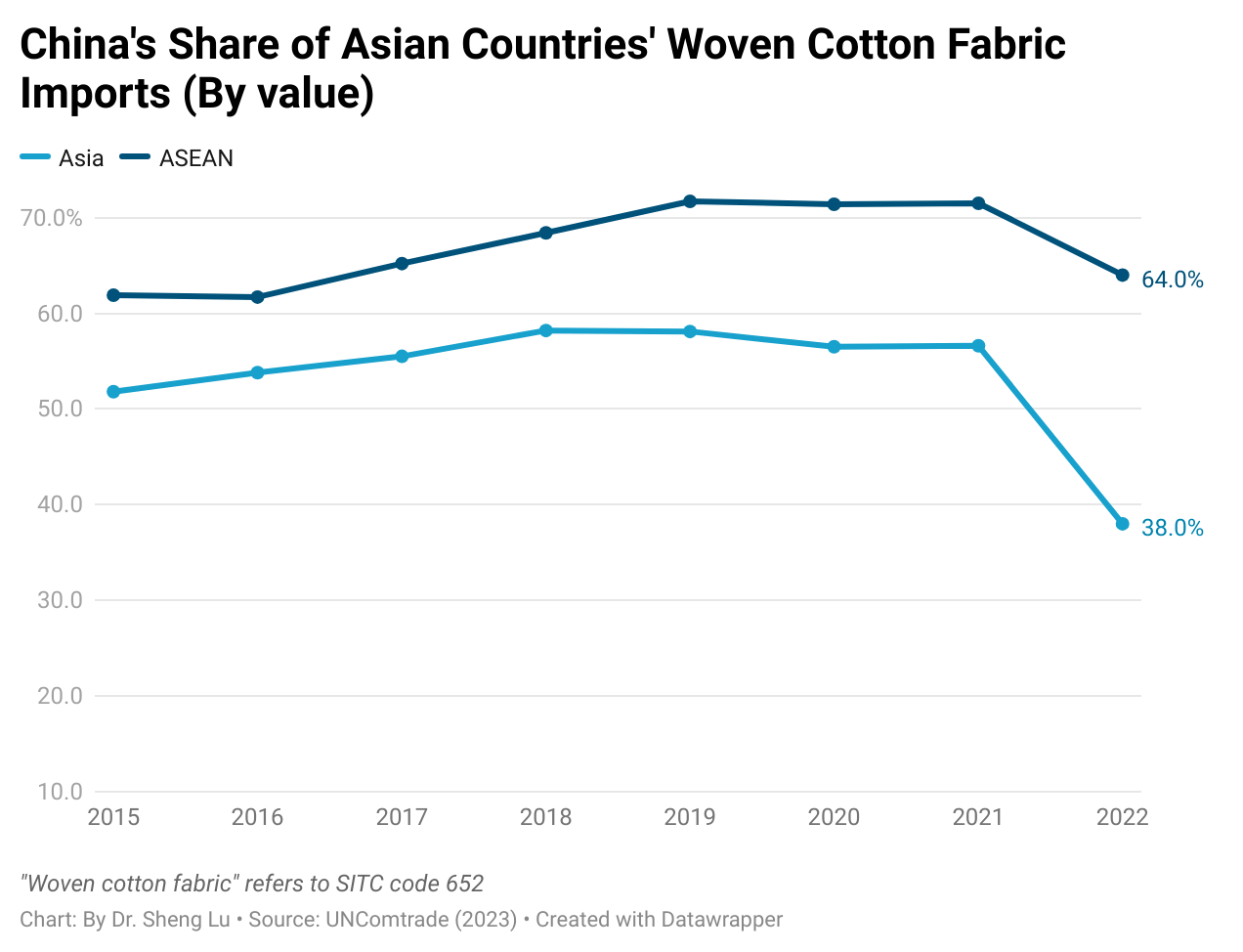

Pattern #4: Regional textile and apparel trade patterns strengthened further with the growing popularity of near-shoring, particularly in the Western Hemisphere. However, an early indication has emerged that Asian countries are diversifying their sources of textile raw materials away from China to mitigate growing risks.

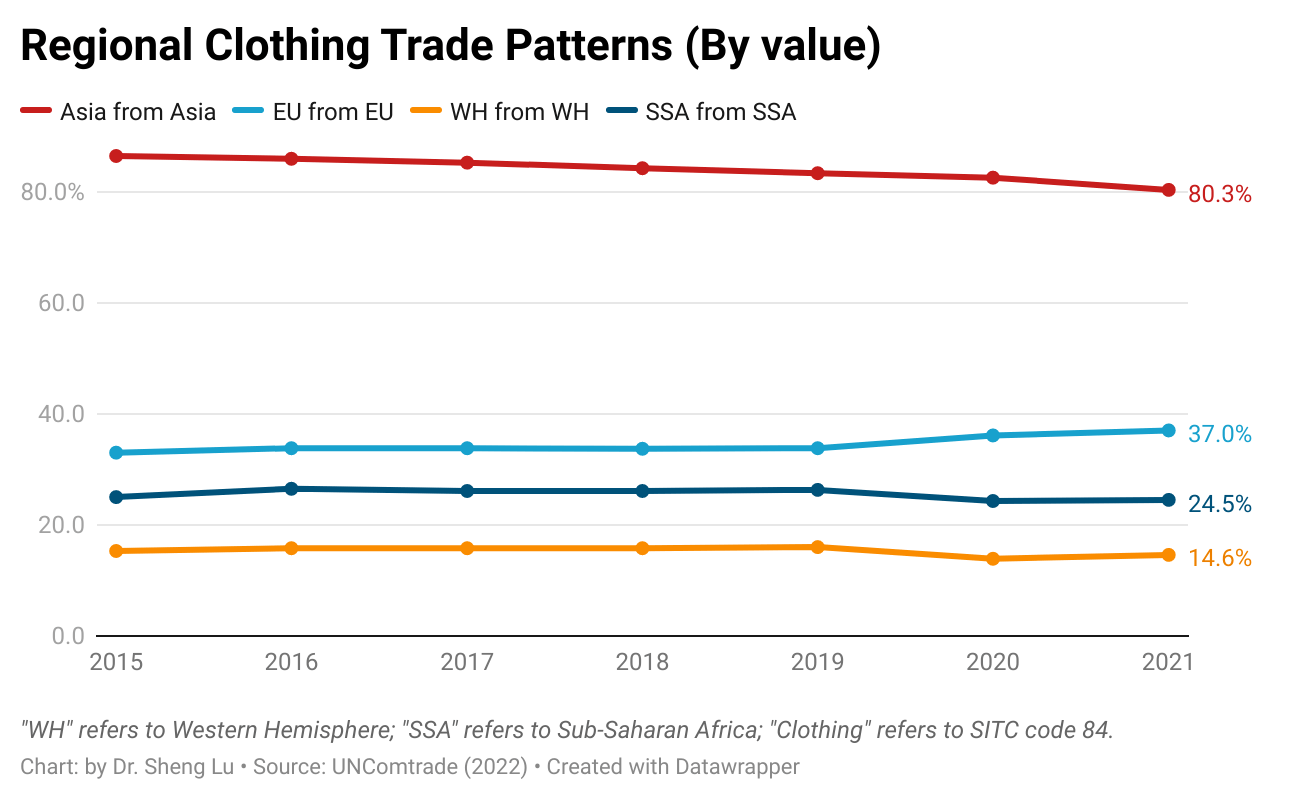

The regional textile and apparel supply chains were in good shape in Asia and Europe. For example, nearly 80 percent of Asian countries’ textile input and apparel imports came from within the region in 2022. Likewise, approximately half of EU countries’ textile imports were intra-region trade in 2022, and one-third were for apparel.

The Western Hemisphere (WH) textile and apparel supply chain became more integrated in 2022 thanks to the booming near-shoring trends. For example, 20.8 percent of WH countries’ textile imports came from within the region in 2022, up from 20.1 percent in the previous year. Likewise, about 15.1 percent of WH countries’ apparel imports came from within the region in 2022, higher than 14.7 percent in 2021 and 13.9 percent in 2022.

Compared with Asia and the EU, SSA clothing producers used much fewer locally-made textiles (i.e., stagnant at around 11% from 2011 to 2022), reflecting the region’s lack of textile manufacturing capability. A more comprehensive examination of strategies for bolstering the textile manufacturing sector in Sub-Saharan Africa, particularly in light of the recently enacted African Continental Free Trade Area (AfCFTA) agreement, might be warranted.

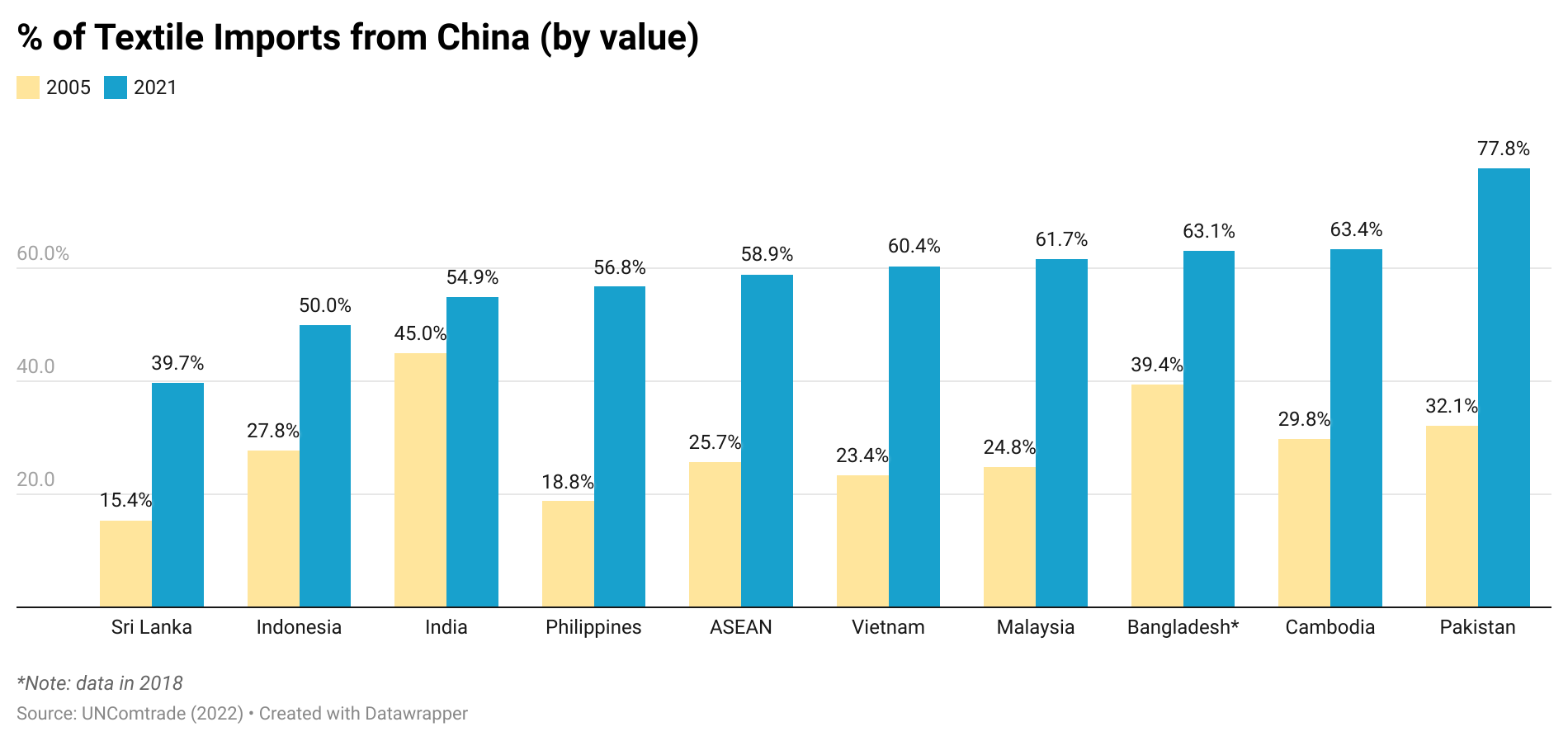

Additionally, data suggests that Asian countries began diversifying their textile imports away from China to mitigate supply chain risks. For example, with the official implementation of anti-forced labor legislation in the US and other primary apparel import markets directly targeting cotton made in China’s Xinjiang region, Asian countries significantly reduced their cotton fabric imports (SITC code 652) from China in 2022. Instead, Asian countries other than China accounted for 46.3 percent of the region’s textile supply in 2022, up from around 42-43 percent between 2019 and 2021.