In June 2021, the U.S. International Trade Commission (USITC) released the 2021 Economic Impact of Trade Agreements Implemented under Trade Authorities Procedures report. By using both qualitative and quantitative methods, USITC assessed the impact of trade agreements on U.S. industries, including workers, since 2016. Below are the key findings related to the textile and apparel sector:

First, free trade agreements enacted in the U.S. have had a small but positive effect on the U.S. economy and trade. As of January 1, 2021, the United States has 14 free trade agreements (FTAs) with 20 countries in force. In the year 2017 (the base year), they led to an estimated increase in U.S. real Gross Domestic Product (GDP) of $88.8 billion (0.5 percent), and in aggregate U.S. employment of 485,000 full-time equivalent (FTE) jobs (0.3 percent). Real wages increased by 0.3 percent. Further, U.S. exports increased by $37.4 billion (1.6 percent), and imports increased by $95.2 billion (3.4 percent) because of these FTAs.

Second, USITC estimates that U.S.-free trade agreements have expanded the U.S. textile industry but hurt U.S. domestic apparel production. Thanks to the North American Free Trade Agreement (NAFTA, now the U.S.-Mexico-Canada Trade Agreement, USMCA) and the Dominican Republic-Central America Free Trade Agreement (CAFTA-DR), the Western Hemisphere has become the single largest export market for U.S. textile producers. However, U.S. apparel manufacturers have to face intensified import competition.

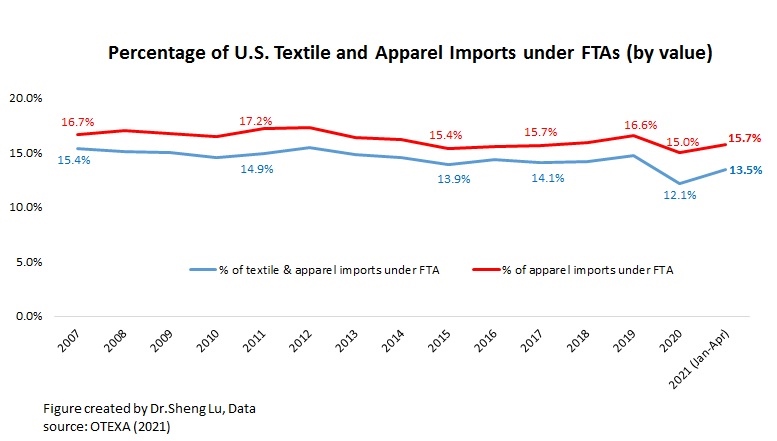

Third, the textile and apparel-specific rules in U.S. free trade agreements are complicated and often hinder the usage of the trade agreements. As noted by USITC, the U.S. duty on imported textile and, especially, apparel goods are among the highest of all product categories. Despite the duty-saving incentives, only 12.1% of U.S. textile and apparel imports came in under FTAs in 2020, even lower than 16.7% in 2007 when fewer FTAs were in force.

The complexity of the textile and apparel-specific rules of origins (ROOs) is a significant cause of the low FTA utilization rate. As USITC noted, “No two FTAs using the tariff shift model contain the same ROOs for apparel goods…for some importers, the strict preference rules of origins (ROOs), along with the record-keeping and documentation requirements the rules entail, make the cost of compliance too great to take full advantage of the duty-free opportunities.” According to the annual USFIA fashion industry benchmarking study, the surveyed U.S. fashion companies consistently expressed the same concerns about the too restrictive ROOs in U.S. FTAs.

Related, the USITC report noted, “some U.S. domestic textile industry representatives state that the existing FTA rules follow a simple template designed to benefit upstream manufacturers in the textile and apparel supply chain.” Having to use more expensive domestic-made fibers and yarns reduces the price competitiveness of U.S. fabrics and home textiles in the export market.

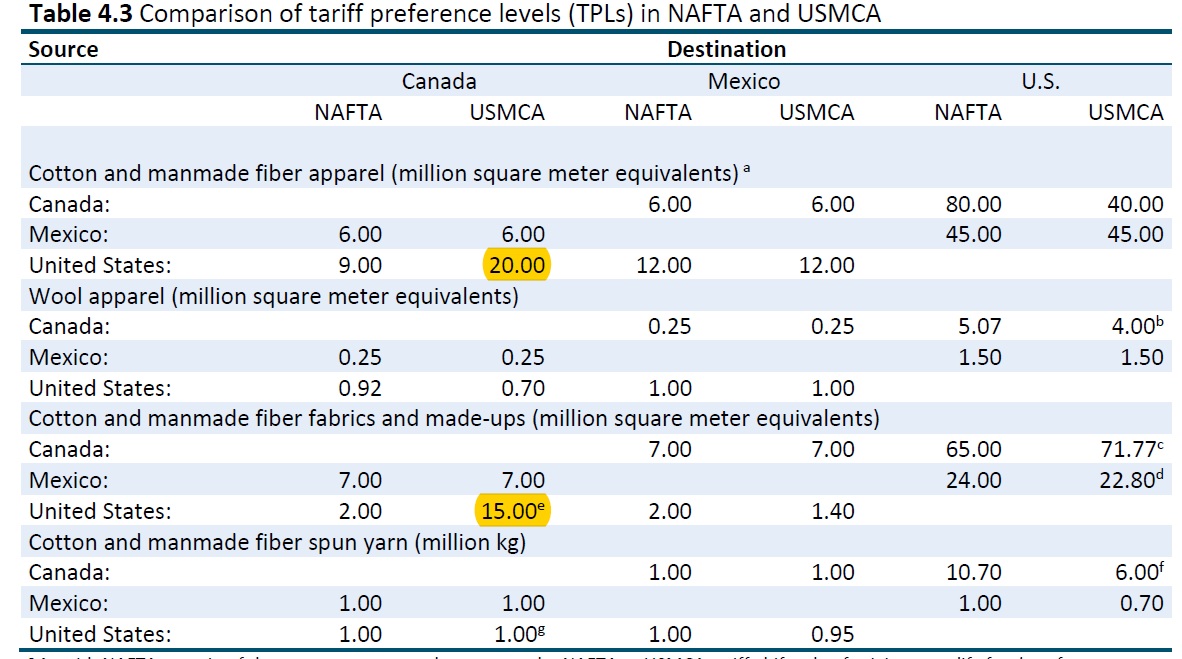

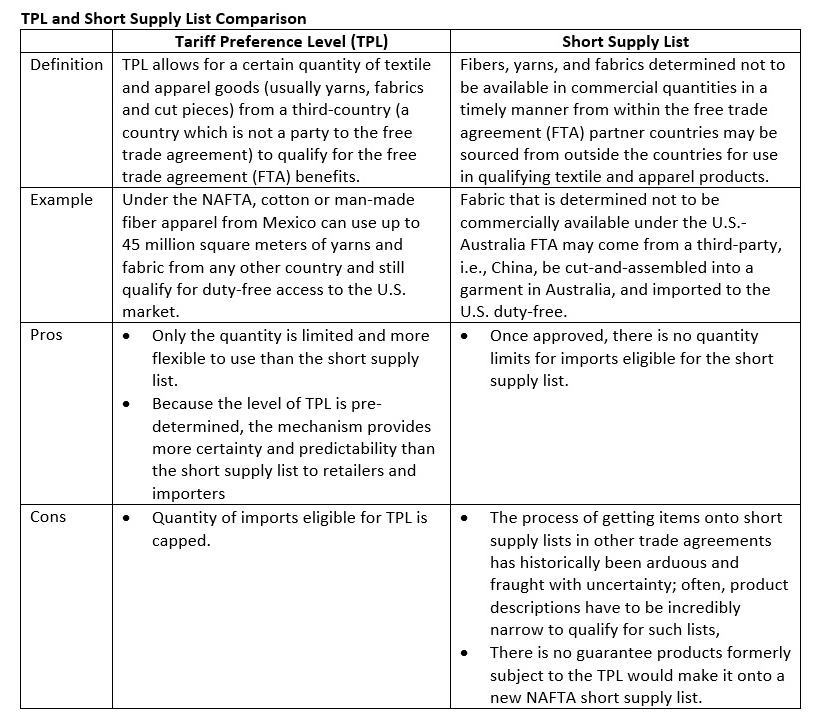

Further, the USITC report explains the history of the “Short supply” and “Tariff-preference level, TPL” mechanisms in U.S. free trade agreements. However, the report does not provide an assessment of their trade impacts.

Trade statistics show that these exceptions to the restrictive “yarn-forward” rules of origin are critical for U.S. apparel sourcing from certain FTA partners. For example, more than 60% of U.S. apparel imports from Canada claimed duty-free benefits by using the TPL mechanism rather than complying with the USMCA/NAFTA “yarn-forward” rules in 2020. Around 8% of U.S. apparel imports from Mexico did the same. Likewise, in 2020, approximately 4% of U.S. apparel imports from CAFTA-DR members used the “short supply” mechanism, and the other 4% used the “cumulation” mechanism.