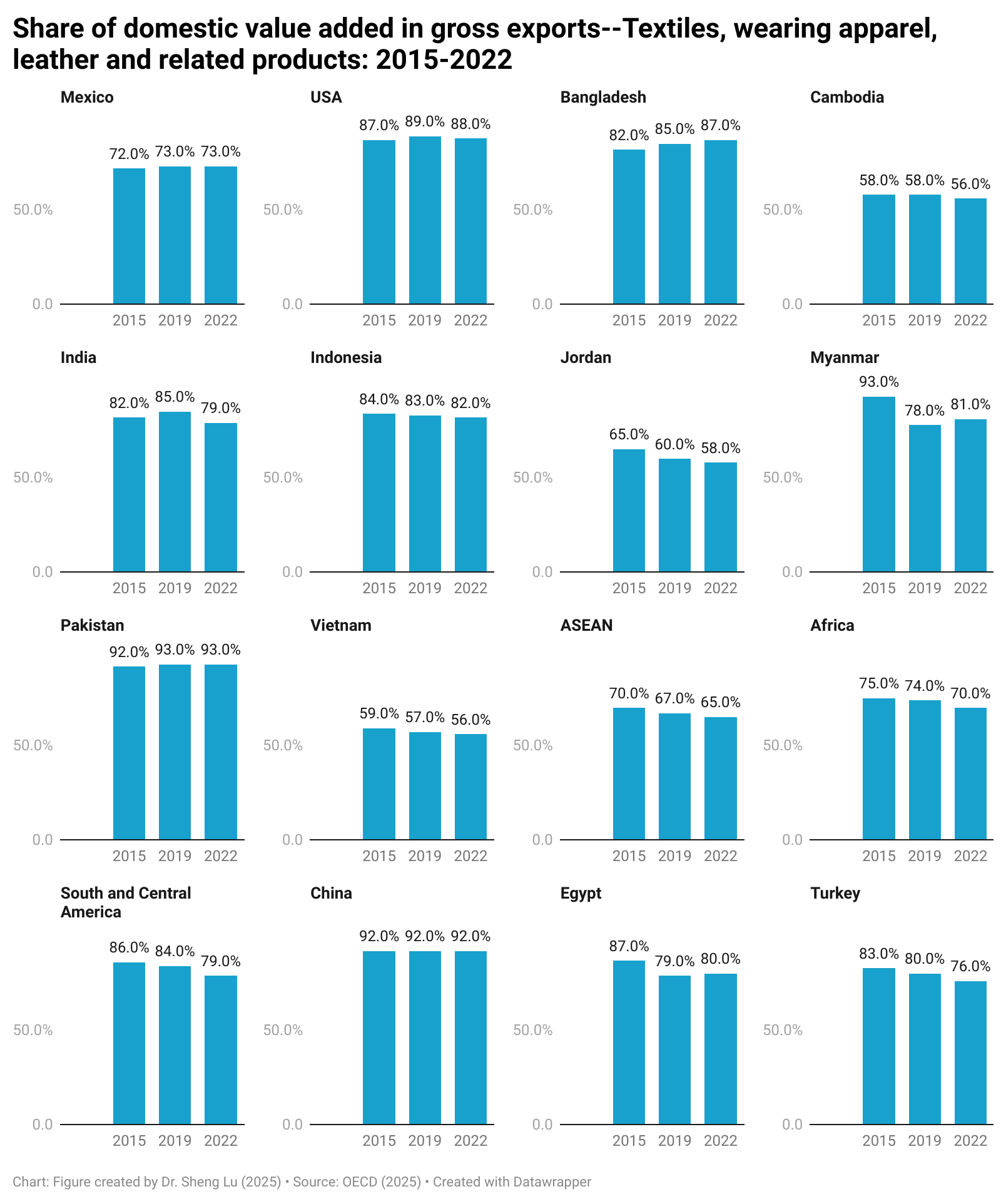

The study, newly published in the Journal of Chinese Economic and Foreign Trade Studies (peer-reviewed), examines the rapid growth of China’s apparel imports from Asian developing countries (ADCs), including Vietnam, Bangladesh, Cambodia, Indonesia, India, Sri Lanka, and Pakistan.

Using product-level analysis of 8,000 apparel Stock keeping units (SKUs) sold in China’s retail market between 2023 and 2024, the research finds that:

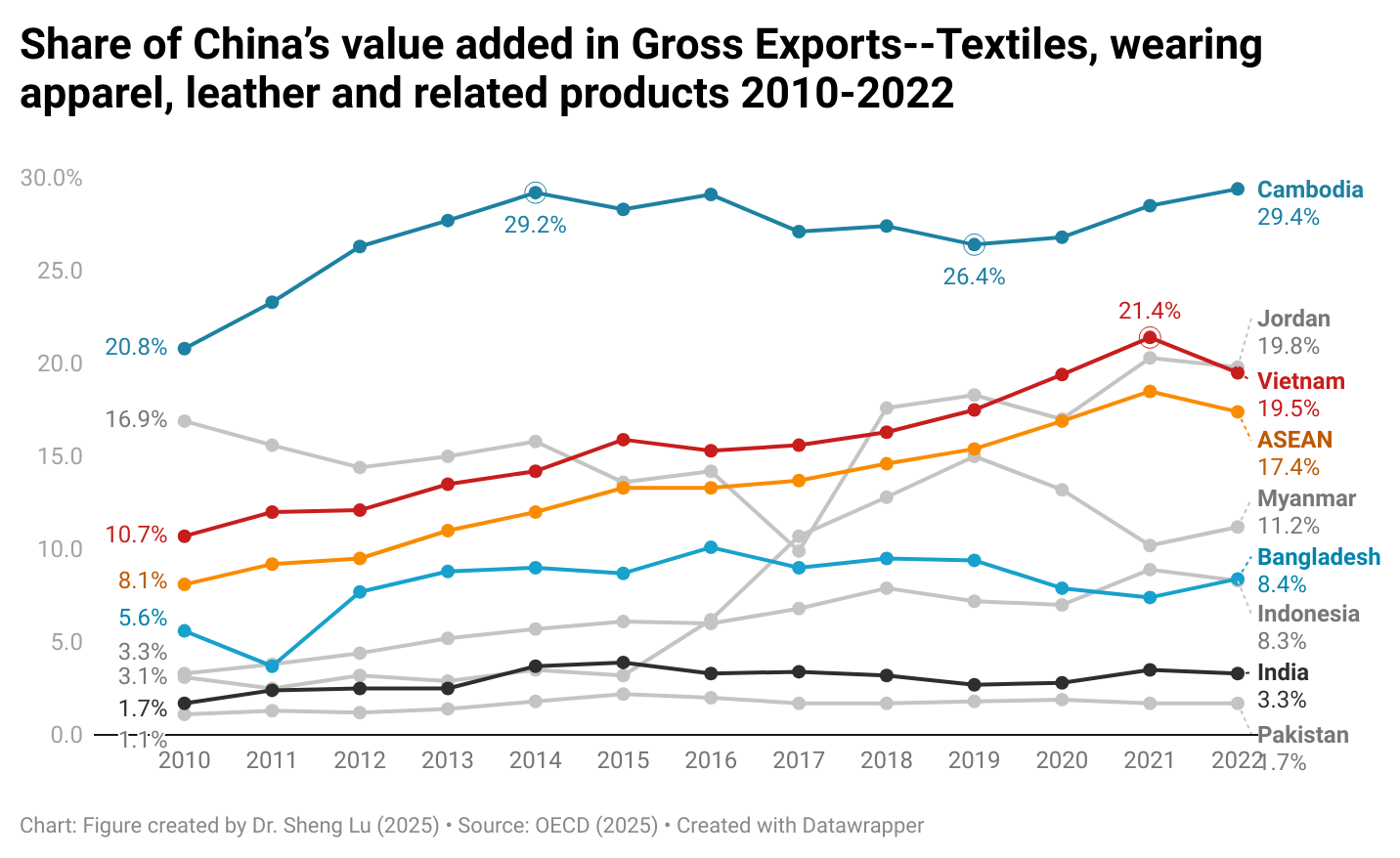

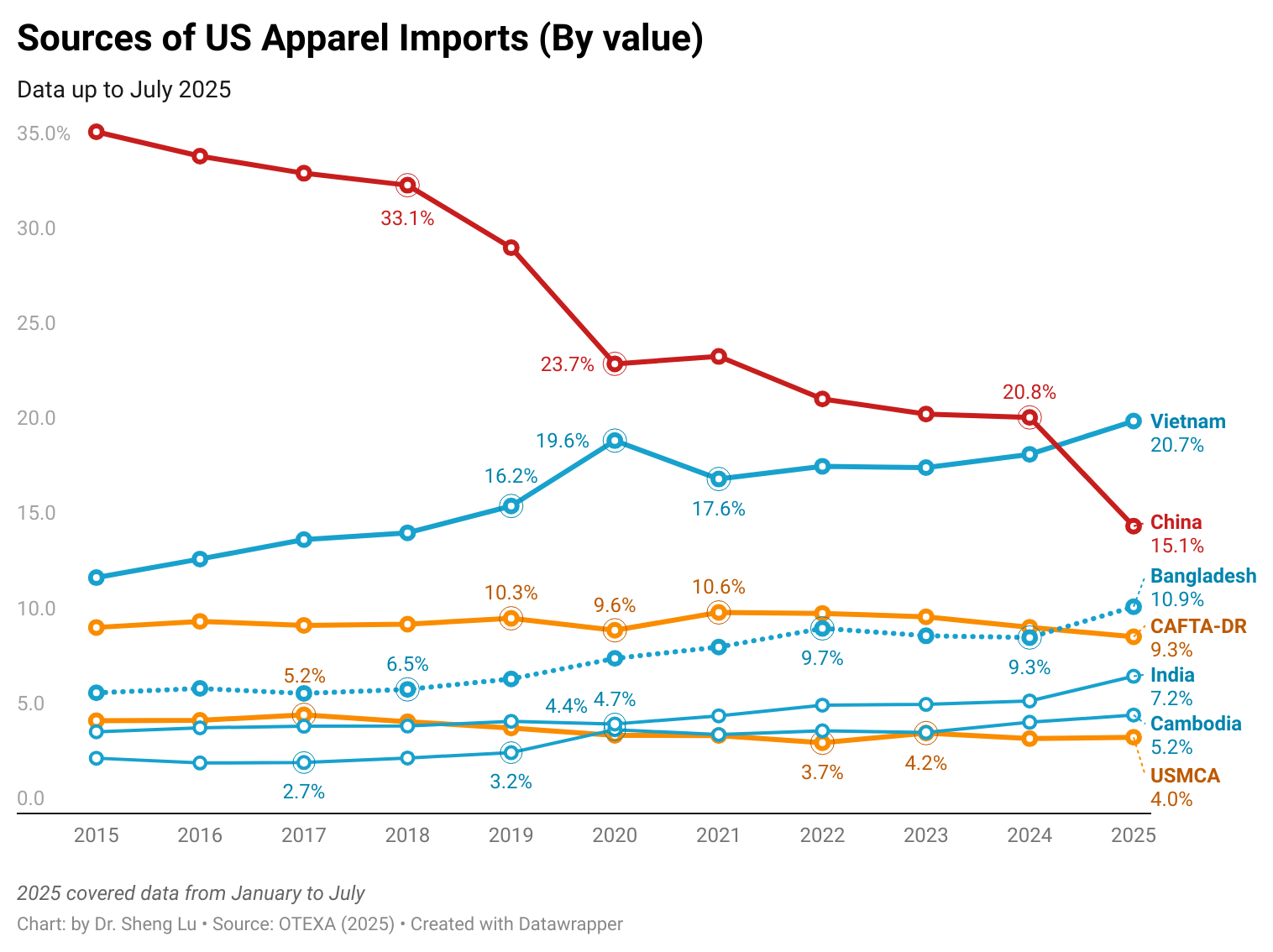

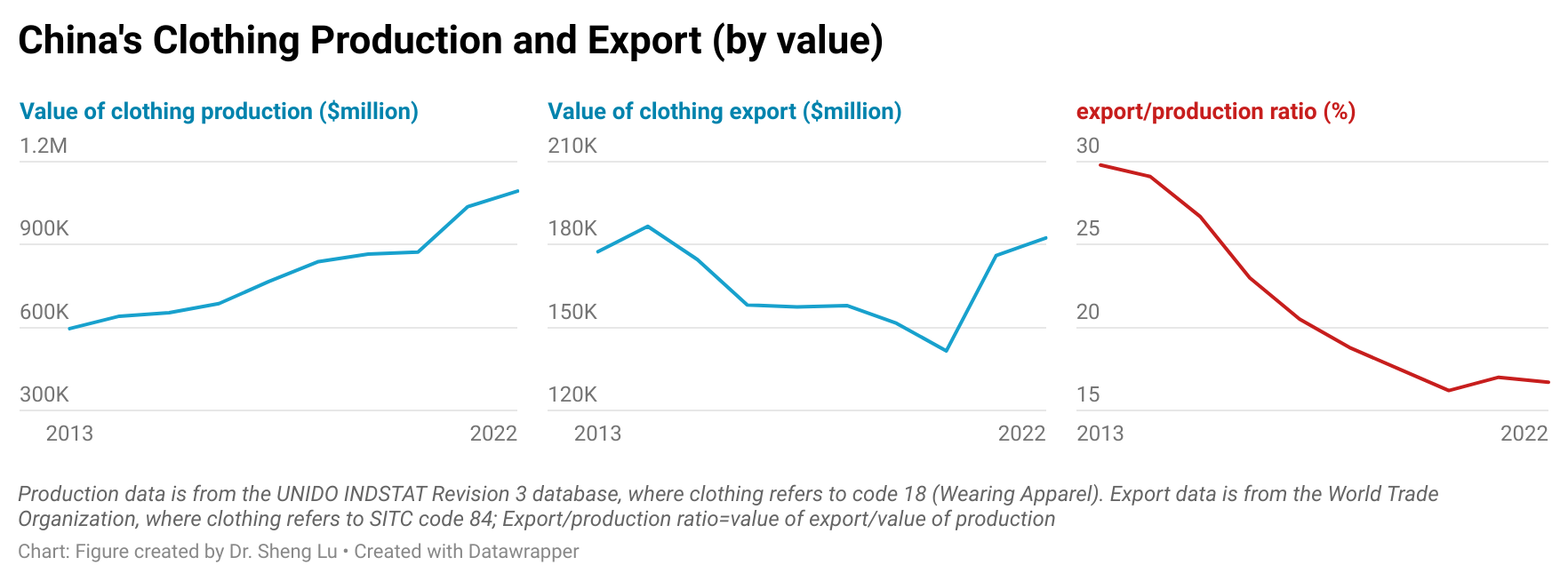

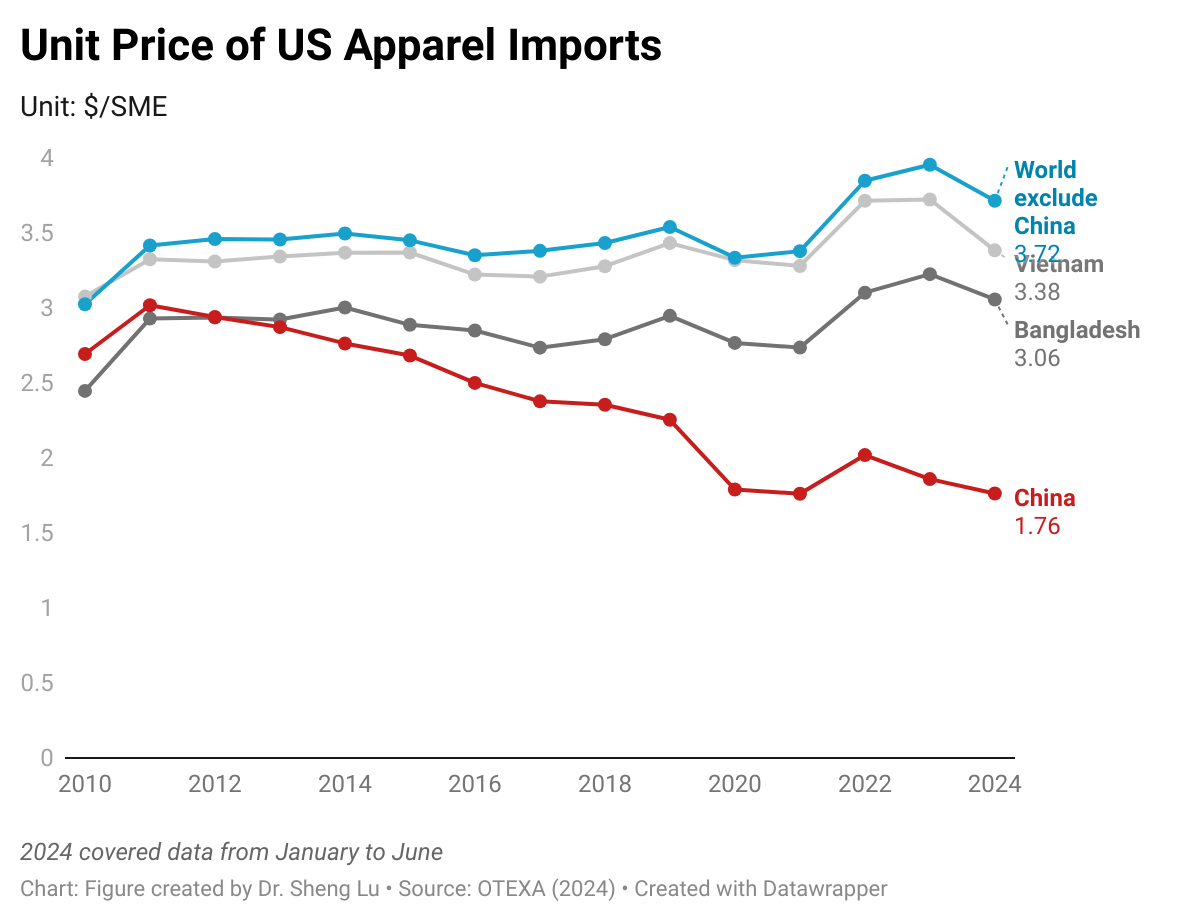

- China is becoming an increasingly important apparel export market for Asian suppliers, not just a competing manufacturing base. Trade statistics also showed that the value of apparel imports into China more than tripled from $2.1 billion in 2010 to more than $10 billion in 2024.

- China’s apparel imports from ADCs are no longer limited to basic low-end products today. Suppliers from these countries now offer a wide range of apparel categories comparable to domestically made Chinese products.

- China’s apparel imports from ADC countries are especially competitive in lower-priced staple items and replenishment-driven categories.

- China’s apparel imports from ADCs were found more likely to feature recycled and organic textile materials than domestically produced apparel in China, suggesting growing competitiveness in sustainable apparel manufacturing.

The findings have several important implications:

First, the findings confirmed that ADCs have become a critical source of apparel for the Chinese retail market. This means that even though China may remain the world’s largest apparel producer and exporter in the foreseeable future, it is no longer the case that apparel sold in China is necessarily made domestically, as this study and trade statistics illustrate. Instead, China has become and could continue to expand its role as a growing export opportunity for many ADCs and support trade-led economic growth there. This is especially important and strategic in the medium to long term for hundreds of thousands of apparel producers from ADCs, as their exports to traditional markets, including the United States, face increasing tariff barriers and policy uncertainties since Trump’s second term began in early 2025.

Second, the study’s findings revealed that ADCs as a whole have developed a more competitive and enhanced apparel production capacity than previous studies suggested. Challenging the popular perception that ADCs were limited to producing cheap basic apparel items like T-shirts and bottoms, these countries can now manufacture a wide range of apparel products, almost comparable to those of Chinese companies, as this study found. This progress can be attributed to ongoing foreign investment and capacity-building support in ADCs, including from Chinese companies eager to expand their multi-country production capabilities, which has significantly boosted the scale and scope of apparel manufacturing in ADCs. Because of ADCs’ demonstrated ability to offer a wide range of apparel products, they can also be seen as preferred “alternatives” to sourcing from China, as Western fashion companies aim to build a more diversified apparel sourcing base and depend less on China.

Furthermore, the study’s findings suggested that expanding textile manufacturing capacity in ADCs could be a strategic move to further improve their apparel export competitiveness. It is important, though not surprising, that China’s apparel imports from ADCs were less diverse in fiber content than domestically produced apparel. This result echoed previous studies, which found that many ADCs still rely heavily on textile raw materials imported from China due to a lack of local manufacturing. Expanding textile production in ADCs would enable these countries to develop stronger vertical apparel manufacturing capabilities, broaden their apparel product offerings, and reduce vulnerability to supply chain disruptions in today’s turbulent trading environment. ADCs may particularly consider attracting more investment in strategic areas, such as products made with sustainable textile fibers, where their products appear even more prominent in the market than those made in China.

By Sheng Lu

Also read: China’s Apparel Imports From Other Asian Countries On the Rise (June 11, 2026, Sourcing Journal, by Kate Nishimura)

{kind=link}