For FASH455 class: When writing your blog comment, consider addressing the following aspects:

#1 Based on the video, how do CAFTA-DR and USMCA help shape the Western Hemisphere textile and apparel supply chain?

#2 Based on the video, what do you see as the main opportunities for textile and apparel nearshoring or reshoring in the Western Hemisphere? How about the key bottlenecks (e.g., cost, infrastructure, labor, sustainability, or trade policy)?

#3 The speaker argues for a sectoral trade policy for textiles and apparel rather than broad “free trade.” What is your evaluation?

#4 How does the video help deepen your understanding of the complex economic and non-economic factors related to textile and apparel nearshoring and reshoring in the Western Hemisphere?

For FASH455 students: Please share your reflections on the video regarding the free trade debate. You can focus on analyzing 1-2 specific debates raised in the video (e.g., comparing the arguments from both sides) and then share your thoughts. Please do not simply state your “opinion,” but use examples, statistics, or trade theories we learned to support your viewpoint.

Below are selected comments by US Trade Representative Katharine Tai (Tai) and WTO (World Trade Organization) Director-General Dr. Ngozi Okonjo-Iweala (Ngozi).

What kind of global trade do we want today?

“For decades, the United States has been proud to champion the international rules-based order and the multilateral trading system…But the functioning and fairness of this order are now in question and that is why all of us need to adapt to a more challenging era marked by rapid technological change, increasing extreme climate events, vulnerable supply chains, intensifying geopolitical friction, widening inequality” (Tai)

“The United States is writing a new story on trade. We are pursuing fair competition, addressing the climate crisis, promoting our national security, and ensuring the rules-based system helps all economies, not just the biggest ones.” (Tai)

“how can we harness the effectiveness of our trade tools to be promoting not just efficiency and liberalization, but using those tools to promote what we consider certainly today to be higher goals. And those goals are resilience for our economy and the word economy, sustainability, again, for our economy in the world economy, and inclusivity… we started to see where the concentrations in supply and production started to impact this and spike this economic insecurity on a macro level and also for individuals” (Tai)

Trade and climate change

“trade is necessary to disseminate green technologies and through competition and scale efficiencies to drive down the cost of decarbonization. Another reason is that trade amplifies the impact of environmental policy action. Recent research at the WTO demonstrate that just as countries can reap economic gains by focusing on what they are relatively good at, the world can reap environmental gainsif countries focus on what they are relatively green at” (Ngozi)

Is trade diversification the future?

“A fragmented world economy would not just be bad for already-squeezed household budgets. Without trade, it would become harder, even impossible, to meet the big challenges of our time – resilience, socioeconomic inclusion, and climate change… The problems we encountered in the trading system were less about trade per se and more about excessive concentration for some products and supply relationships. The smart response is to deepen, diverse, and deconcentrate production so there are fewer potential bottlenecks” (Ngozi)

“we believe we can solve the problem by diversifying the supply chains not just to ourselves or to friends but to all over the world where the opportunity exists. Business should look at the possibility of not just doing China+1. It means China plus Vietnam or Indonesia. But they can do Bangladesh. They can do Laos. They can do Rwanda. They can do Senegal. They can do Nigeria. I’m just – Morocco” (Ngozi)

Debate the impact of trade

“Technology was generally a big culprit in job losses…U.S. manufacturing output, the volume of products produced here, is about as high as it has ever been. But the sector employs more machines and fewer people than it used to. Nevertheless, import competition was a significant factor and an easier focus, I think, for political anger.” (Ngozi)

“…between 1995 and 2011, while increased goods import from China did eliminate 2 million jobs in the United States, increased exports to China and elsewhere added 6.6 million jobs to the U.S. economy, 4 million of them from higher-services exports…These numbers illustrate the power of trade for job creation. But as we know, those new jobs were not created in the same places. Neither did they go to the same people. That a backlash would result from those left out was perhaps predictable, but it was not inevitable. There are countries that use domestic-policy levers to translate gains from trade into broadly shared growth by providing people security against income loss and support to seize new opportunities.” (Ngozi)

Renew or update the African Growth and Opportunity Act?

“The world is really different from when AGOA was first created…So I think copy-paste is to really lose an important opportunity…we should be practical. Also, we’re on a timeline…The AfCFTA, the African Continental Free Trade Area, that has been concluded, that has that has been brought into being by the countries on the continent. And those continental integration aspirations should absolutely be reflected in our offer to Africa, and something we should try to figure out how to incorporate” (Tai)

“African countries appreciate AGOA. They would like to see an agreement that is, you know, at least a decade out so that they have some predictability. What they’re hearing from investors is that with this up in the air, they can’t make up their minds whether to invest or not because they don’t know what will happen. So I think if we can reform and get it done, and people can have a predictable time horizon for AGOA, it would really help” (Ngozi)

How to reform the World Trade Organization?

“The United States wants a WTO where dispute settlement is fair and effective, and supports a healthy balance of sovereignty, democracy, and economic integration where all members embrace transparency, where we have better rules and tools to tackle non-market policies and practices, and to confront the climate crisis and other pressing issues.” (Tai)

“We must recognize the diversity of developing members. We should have flexibilities in the rules that reflect actual needs. But we cannot have economic and manufacturing powerhouses gaming the system by claiming the same development status and flexibilities intended for less-advantaged members.” (Tai)

“people ask me all the time, oh, are you worried because there are so many [Free trade agreement, FTA]? I’m not. Like I said, 75 percent of trade still goes on WTO terms [MFN tariff rates]. And we can learn from them.” (Ngozi)

“I don’t have enough time and money to waste resources in Geneva on a process that we don’t actually believe in…When President Biden talks about it from the floor of the United Nations General Assembly, if we still have trading partners who want to question our seriousness, then I think the problem is those partners and it’s not us” (Tai) [note: this comment was mentioned by Politico]

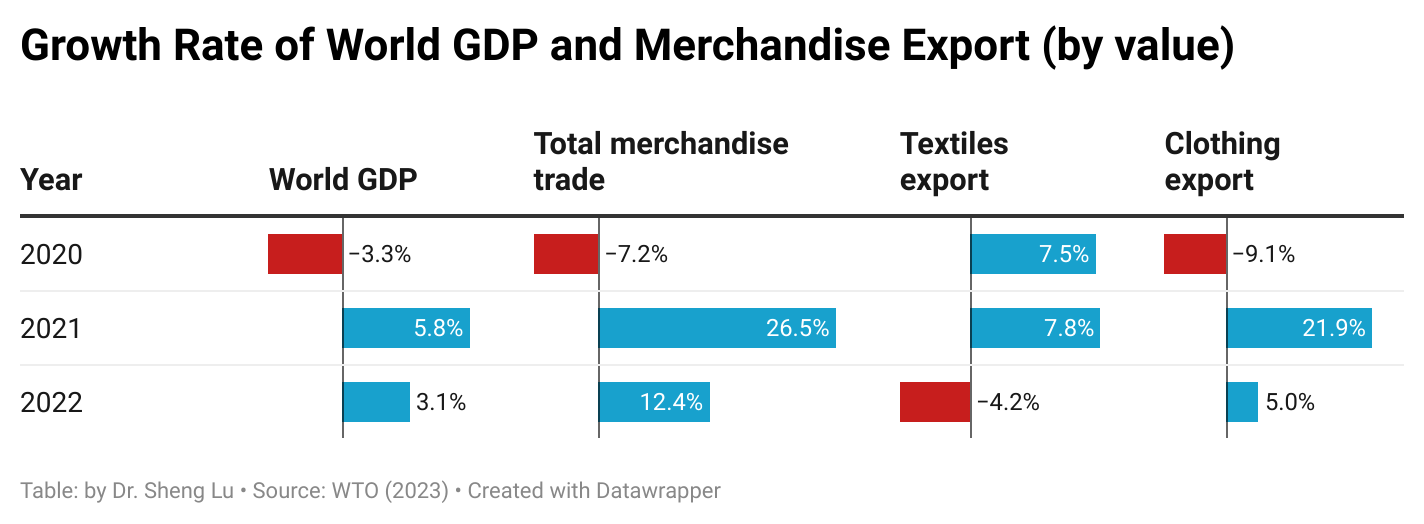

This article comprehensively reviewed the world textiles and clothing trade patterns in 2022 based on the newly released World Trade Organization Statistical Review 2023 and data from the United Nations (UNComtrade). Affected by the slowing world economy and fashion companies’ evolving sourcing strategies in response to the rising geopolitical tensions, mainly linked to China, the world’s textiles and clothing trade in 2022 displayed several notable patterns different from the past.

Pattern #1: The expansion of world clothing exports witnessed a notable deceleration in 2022, primarily attributed to the economic downturn. Meanwhile, the world’s textile exports decreased from the previous year, affected by the reduced demand for textile raw materials used to produce personal protective equipment (PPE) as the pandemic waned.

The world’sclothing exports totaled $576 billion in 2022, up 5 percent year over year, much slower than the remarkable 20 percent growth in 2021. The slowed economic growth plus the unprecedented high inflation in major apparel import markets, particularly the United States and Western European countries, adversely affected consumers’ available budget for discretionary expenditures, including clothing purchases.

The world’s textile exports fell by 4.2 percent in 2022, totaling $339 billion, lagging behind most industrial sectors. Such a pattern was understandable as the demand for PPE and related textile raw materials substantially decreased with the pandemic nearing its end.

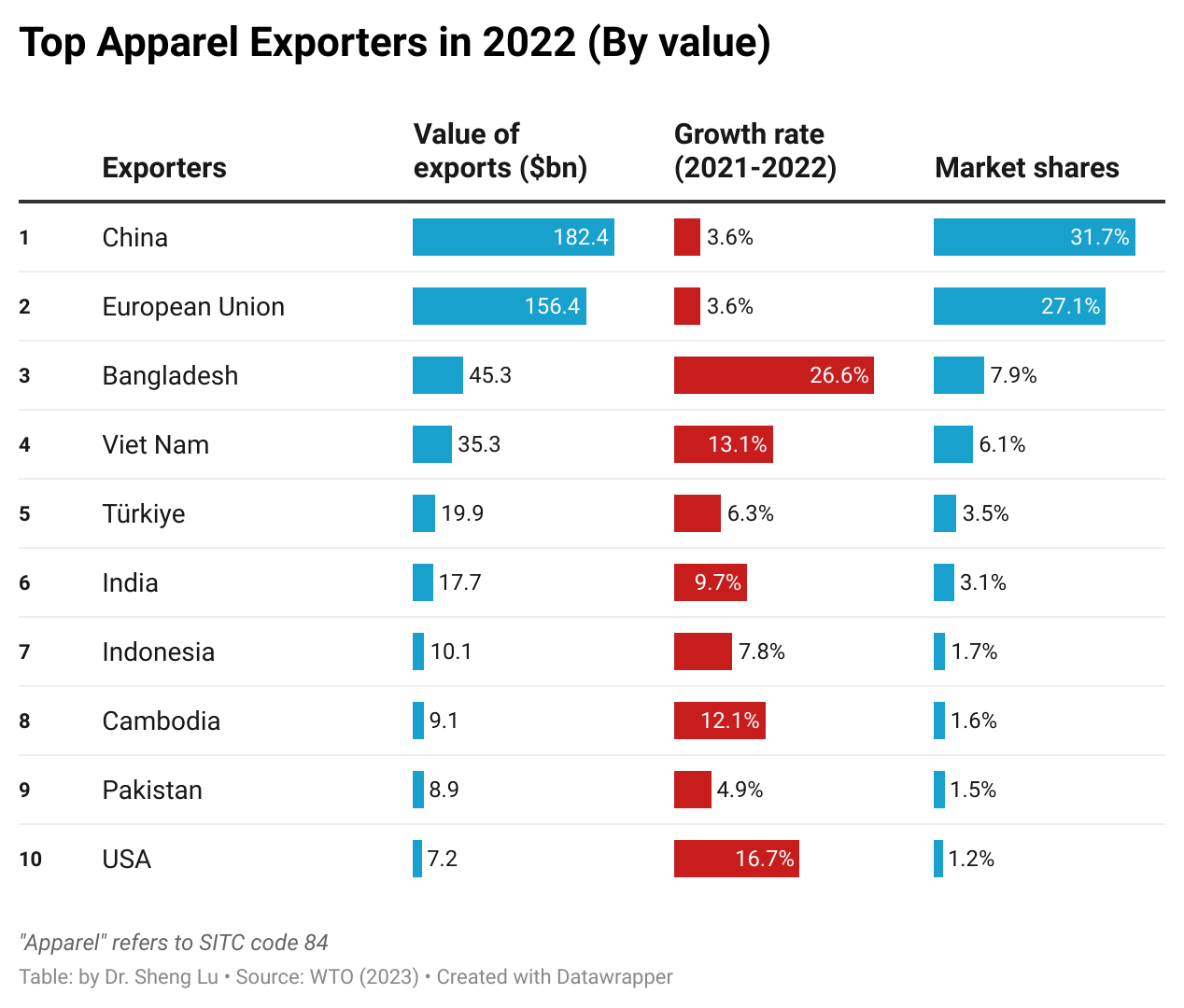

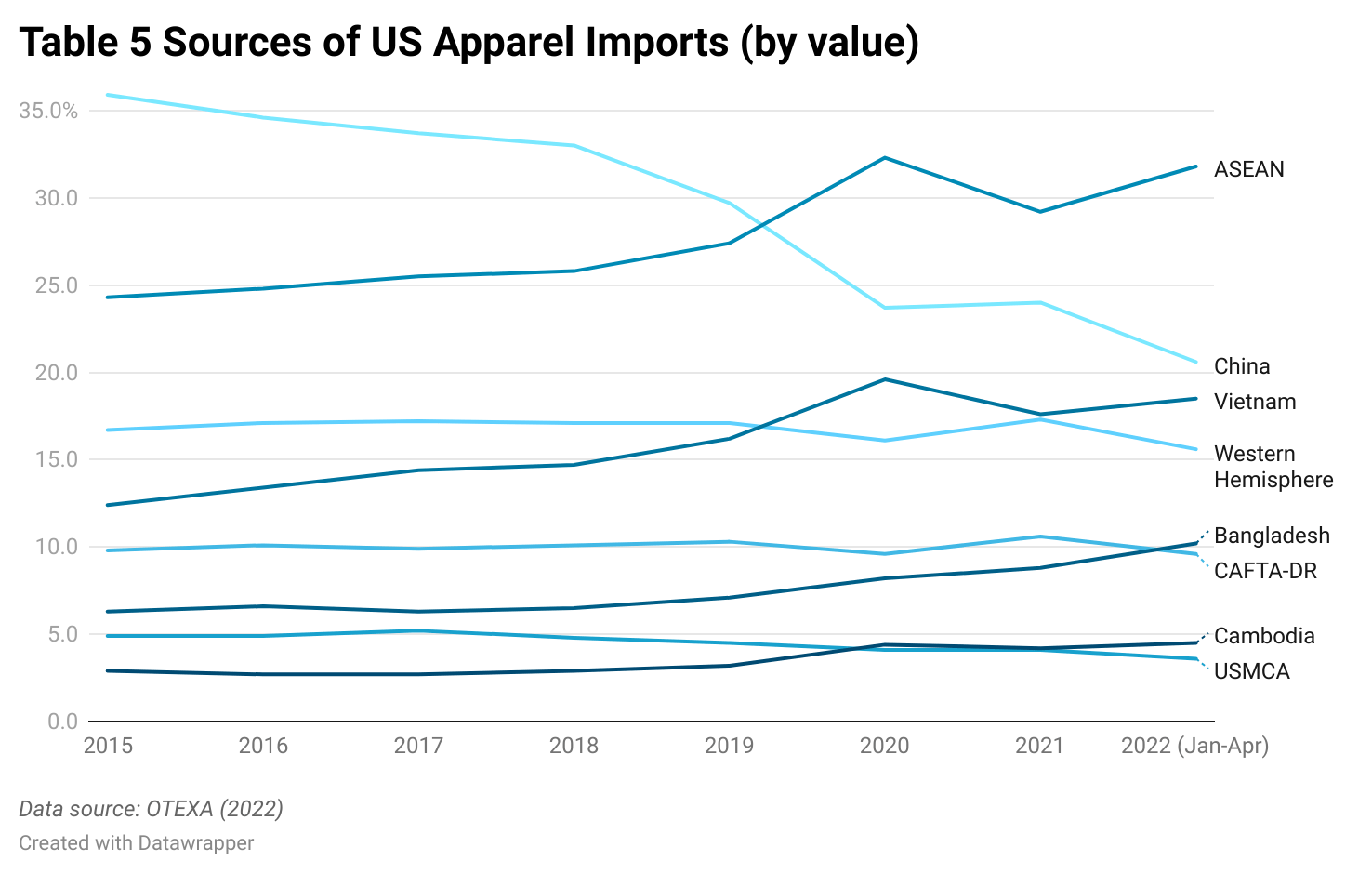

Pattern #2: China continued to lose market share in clothing exports, which benefited other leading apparel exporters in Asia. Notably, for the first time, Bangladesh surpassed Vietnam and ranked as the world’s second-largest apparel exporter in 2022.

In value, China remained the world’s largest apparel exporter in 2022. However, China’s clothing exports experienced a growth of 3.6 percent, below the global average of 5.0 percent, positioning China at the bottom of the top ten exporters.

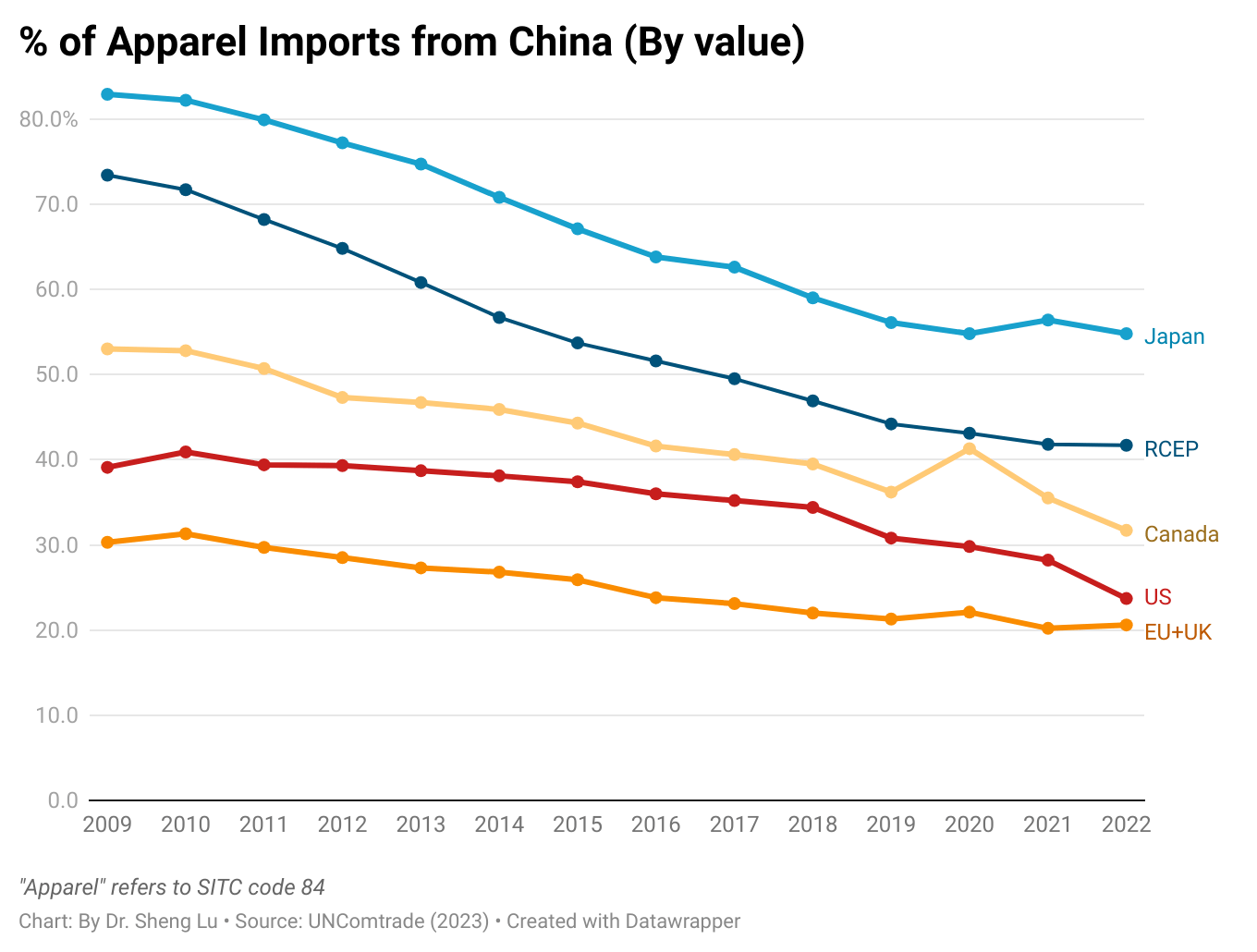

China’s global market share in clothing exports dropped to 31.7 percent in 2022, marking its lowest point since the pandemic and a significant decrease from the approximate 38 percent recorded from 2015 to 2018. In fact, China lost market share in almost all major clothing import markets, including the US, the EU, Canada, and Japan. The concerns about the risks of forced labor linked to sourcing from China and the deteriorating US-China relations were among the primary factors driving fashion companies’ eagerness to reduce their ‘China exposure” further.

China has been diversifying its clothing exports beyond the traditional Western markets in response to the challenging business environment. For example, from 2021 to 2022, Asian countries, especially members of the Regional Comprehensive Economic Partnership (RCEP), became relatively more important clothing export markets for China. Nevertheless, since RCEP members primarily consist of developing economies with ambitions to enhance their own clothing production, the long-term growth prospects for their import demand of ‘Made in China’ clothing remain uncertain.

Bangladesh achieved a new record high in its market share of world clothing exports, reaching 7.9 percent in 2022, which exceeded Vietnam’s 6.1 percent. Many fashion companies regard Bangladesh as a promising clothing-sourcing destination with growth potential because of its capability to make cotton garments as China’s alternatives, competitive price, and reduced social compliance risks.

Fashion companies’ efforts to “de-risking from China” also resulted in the robust growth of clothing exports from other large-scale Asian clothing producers in 2022, including Vietnam (up 13 percent), Cambodia (up 12 percent), and India (up 10 percent). In other words, despite the concerns about China, fashion companies still treat Asia as their primary sourcing destination.

Pattern #3: Developed countries stay critical textile exporters, and middle-income developing countries gradually build new textile production and export capability.

The European Union members and the United States stayed critical textile exporters, accounting for 25.1 percent of the world’s textile exports in 2022, up from 24.5 percent in 2021 and 23.2 percent in 2020. Thanks to the increasing demand from apparel producers in the Western Hemisphere, U.S. textile exports increased by 5 percent in 2022, the highest among the world’s top ten.

As a persistent long-term trend, middle-income developing countries have consistently been strengthening their textile production and export capability. For example, China, Vietnam, Turkey, and India’s market shares in the world’s textile exports have steadily risen. They collectively accounted for 56.8 percent of the world’s clothing exports in 2022, a notable increase from only 40 percent in 2010. Also, over time, these middle-income developing countries have achieved a more balanced textiles-to-clothing export ratio.

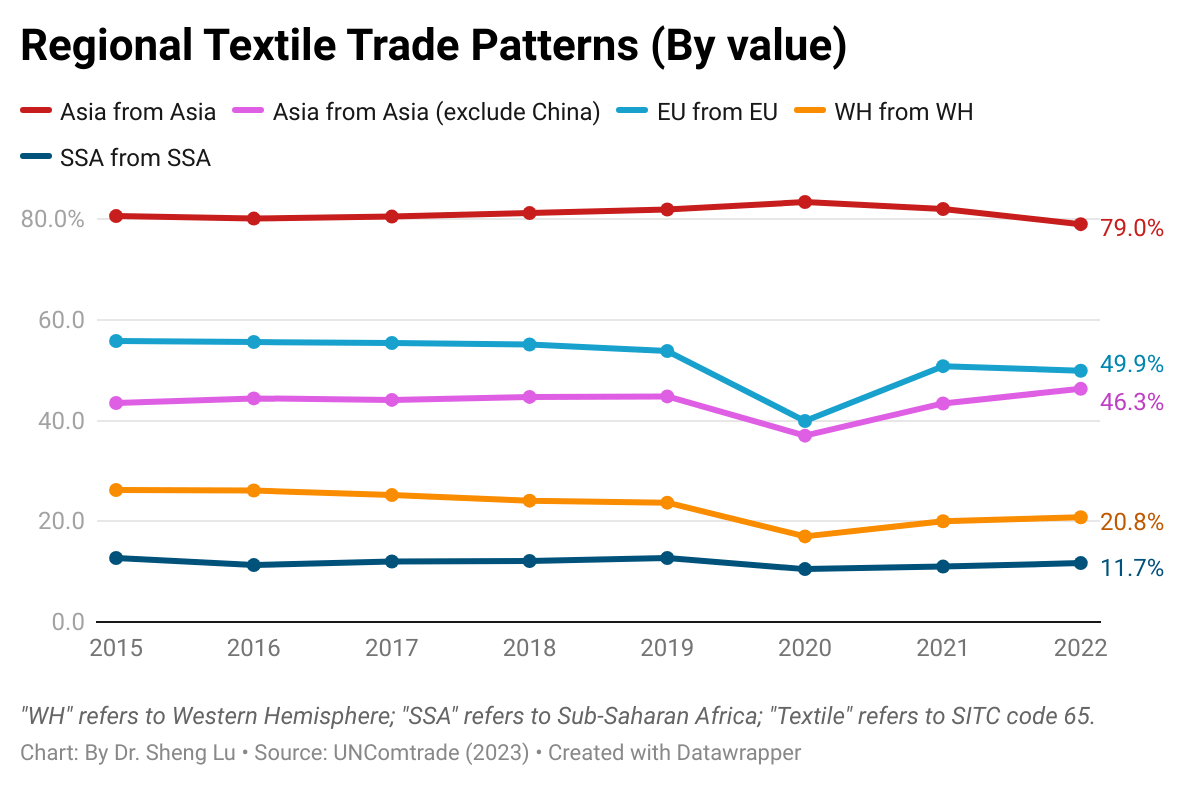

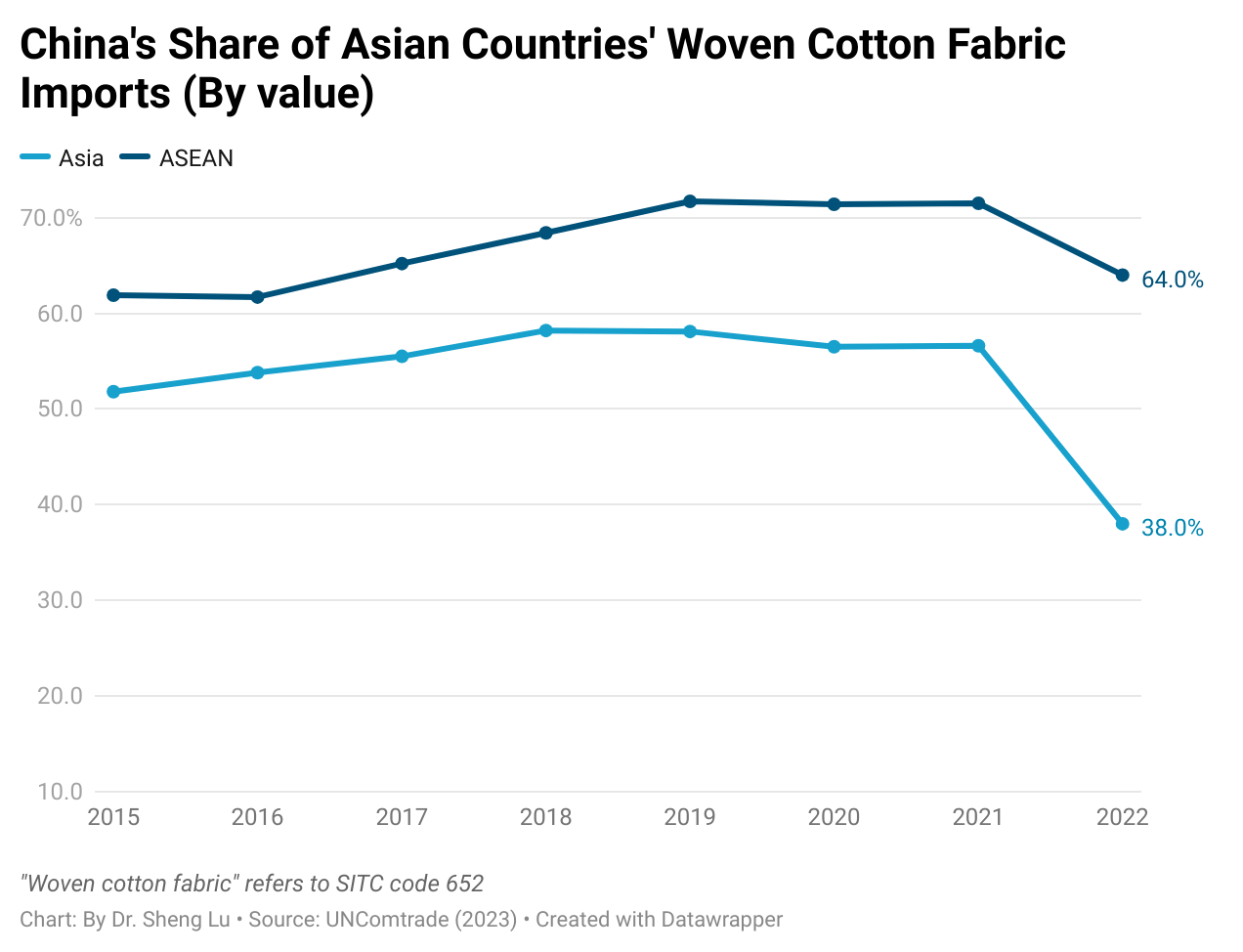

Pattern #4: Regional textile and apparel trade patterns strengthened further with the growing popularity of near-shoring, particularly in the Western Hemisphere. However, an early indication has emerged that Asian countries are diversifying their sources of textile raw materials away from China to mitigate growing risks.

The regional textile and apparel supply chains were in good shape in Asia and Europe. For example, nearly 80 percent of Asian countries’ textile input and apparel imports came from within the region in 2022. Likewise, approximately half of EU countries’ textile imports were intra-region trade in 2022, and one-third were for apparel.

The Western Hemisphere (WH) textile and apparel supply chain became more integrated in 2022 thanks to the booming near-shoring trends. For example, 20.8 percent of WH countries’ textile imports came from within the region in 2022, up from 20.1 percent in the previous year. Likewise, about 15.1 percent of WH countries’ apparel imports came from within the region in 2022, higher than 14.7 percent in 2021 and 13.9 percent in 2022.

Compared with Asia and the EU, SSA clothing producers used much fewer locally-made textiles (i.e., stagnant at around 11% from 2011 to 2022), reflecting the region’s lack of textile manufacturing capability. A more comprehensive examination of strategies for bolstering the textile manufacturing sector in Sub-Saharan Africa, particularly in light of the recently enacted African Continental Free Trade Area (AfCFTA) agreement, might be warranted.

Additionally, data suggests that Asian countries began diversifying their textile imports away from China to mitigate supply chain risks. For example, with the official implementation of anti-forced labor legislation in the US and other primary apparel import markets directly targeting cotton made in China’s Xinjiang region, Asian countries significantly reduced their cotton fabric imports (SITC code 652) from China in 2022. Instead, Asian countries other than China accounted for 46.3 percent of the region’s textile supply in 2022, up from around 42-43 percent between 2019 and 2021.

It is critical to watch how willing, to what extent, and how quickly Asian countries can effectively reduce their dependency on textile supplies from China. The result is also an important reminder that Western fashion companies’ de-risking from China could exert significant and broad impacts across the entire supply chain beyond finished goods.

The full paper is HERE. Below are the key findings:

Over the past decade, U.S. fashion brands and retailers have seen Central America as a critical emerging apparel-sourcing destination. Especially since implementing the Dominican-Republic Central America Free Trade Agreement (CAFTA-DR) in 2006, a trade deal among the United States, El Salvador, Guatemala, Honduras, Nicaragua, the Dominican Republic (joined in 2007), and Costa Rica (joined in 2009), apparel sourcing from the region gained consistent interest among U.S. companies.

Nevertheless, U.S. apparel sourcing from CAFTA-DR members is NOT without significant challenges. For example, CAFTA-DR countries’ market shares in the U.S. apparel import market fell from 11.8% in 2005 before the trade agreement entered into force to only 10.6% in 2022, measured by value. Trade data also indicated that U.S. apparel sourcing from CAFTA-DR members concentrated on simple and low-value items, such as T-shirts, and lacked product diversification with no improvement over the years.

Given the high stakes of improving the status quo, this study quantitatively evaluated the impact of textile raw material access on CAFTA-DR’s apparel exports to the United States. Specifically, this study assumed that CAFTA-DR members cut their textile import tariff rates to improve garment producers’ textile raw material access (i.e., to reduce the cost of sourcing textiles from anywhere in the world and beyond the U.S. supply). The computable general equilibrium (CGE) model estimation based on the GTAP9 database shows mixed results:

On the one hand, cutting CAFTA-DR members’ textile import tariffs to improve their garment producers’ textile raw material access would significantly improve CAFTA-DR members’ price competitiveness of their apparel exports to the United States and increase the export volume.

However, cutting CAFTA-DR members’ textile import tariffs to improve their garment producers’ textile raw material access would significantly expand their textile imports from non-U.S. sources. This means that CAFTA-DR members’ dependence on the U.S. textile raw material supply may decline further.

Overall, the study’s findings remind us that the debate on expanding U.S. apparel sourcing from CAFTA-DR members should go beyond CAFTA-DR members’ garment production. Instead, more efforts could be made to enhance CAFTA-DR garment producers’ textile raw material access as an effective way to expand the region’s apparel exports to the United States.

Meanwhile, several leading CAFTA-DR apparel exporting countries, including Honduras and Nicaragua, have been engaged in negotiations for free trade agreements with China, Taiwan, and other Asian economies. As the study’s findings indicate, these new trade deals could incentivize CAFTA-DR apparel manufacturers to increase their textile sourcing from Asia. In other words, inaction on the U.S. side and maintaining the status quo still could have significant implications for the future stability of the Western Hemisphere textile and apparel supply chain.

USITC adopted two methods to estimate Section 301 tariffs’ economic impacts:

Econometric model estimates using monthly trade data (10-digit HS code) from January 2017 to December 2021.

A set of partial equilibrium models that linked section 301 tariffs to domestic prices and production at the four-digit NAICS code level. USITC used data from 2018 to 2021 as the base year.

USITC only considered Section 301 tariffs’ direct impacts, i.e., “how tariffs impacted prices, production, and trade for products subject to section 301 tariffs and domestic sectors that compete directly with those imports.”

Regarding the overall impact of Section 301 actions, USITC found that the tariffs imposed on Chinese goods resulted in a price rise paid by US importers, but the exporter prices received by Chinese firms were mostly unchanged. As a result, “imports from China decreased in quantity, leading to a substantial decline in their import value. These changes, in turn, caused an increase in production and prices in US domestic industries that were competing with Chinese imports.”

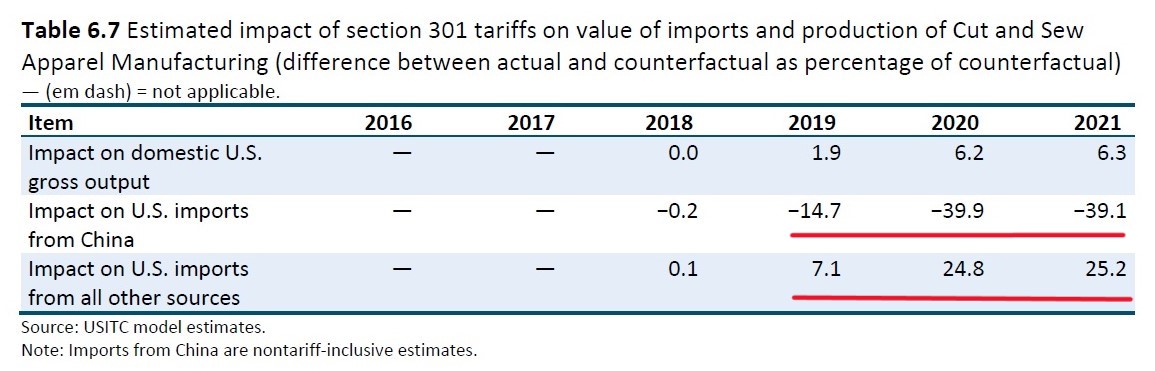

USITC also evaluated the specific impacts of Section 301 tariffs on the Cut and Sew apparel (NAICS 3152) sector. According to USITC:

“nontariff-inclusive value” refers to the change in the value of imports from China excluding the value of the section 301 duties themselves, which provide an indication of the change in import quantities because export prices are mostly unchanged.

First, Section 301 tariffs hurt US apparel imports from China. USITC estimated that US woven apparel (NAICS 3152) imports from China decreased by 14.7% in 2019 but fell nearly 40% in 2020 and 2021 due to Section 301 tariffs. However, USITC didn’t explain why imports from China suddenly worsened, nor if other factors, such as the Uyghur Forced Labor Prevention Act (UFLPA), played a role.

Second, Section 301 tariffs mostly replaced US woven apparel (NAICS3152) imports from China with other sources. However, the direct benefits of Section 301 tariffs to US domestic cut and sew manufacturing seemed limited. Specifically, USITC estimated that US woven apparel imports from sources other than China increased by 7.1% in 2019, 24.8% in 2020, and 25.2% in 2021 due to Section 301 tariffs. In comparison, Section 301 tariffs resulted in modest growth of US domestic woven apparel (NAICS3152) production (up to 6.3%) over the same period.

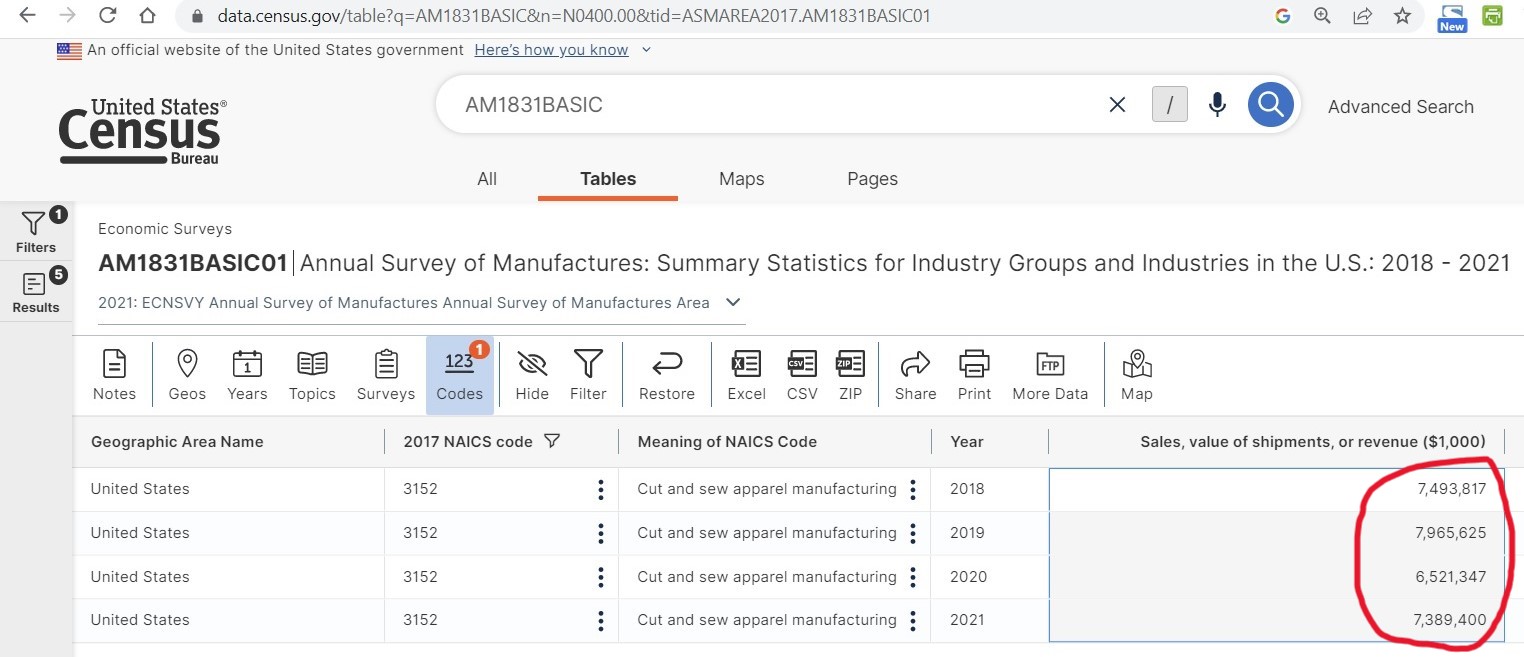

Actual trade and production data further showed that US woven apparel (NAICS 3152) imports from sources other than China increased from $55.3 billion in 2018 to $61.2 billion in 2021 (or up 10.7%). Over the same period, US domestic woven apparel (NAICS 3152) sales & value of shipments declined from $7.49 billion to $7.38 billion (or down 1.4%) (Data source: Census). In other words, no clear evidence suggests that Section 301 tariffs boosted US domestic woven apparel production.

Third, Section 301 tariffs made US woven apparel (NAICS 3152) imports from EVERYWHERE more expensive. On the one hand, USITC found that the price of US woven apparel (NAICS 3152) imports from China increased by 4.4% in 2019, 14.7% in 2020, and 14.5% in 2021 due to the Section 301 tariffs. However, similar to the case of trade volume, USITC didn’t explain why Section 301 tariffs’ price impact suddenly became more significant in 2020 and 2021. (Note: In fact, the Tranche 4A tariffs were 15% since September 1, 2019, but were reduced to 7.5% effective February 14, 2020, because of the US-China Phase One deal.)

Meanwhile, due to limited production capacity outside of China, the Section 301 tariffs caused an increase in the cost of US woven apparel imports from all other countries. Specifically, USITC found that the price of US woven apparel (NACIS 3152) imports from sources other than China increased by 3.2% from 2018 to 2021. (Note: given the hiking sourcing costs in 2022, the price increase could be more significant should USITC include updated 2022 trade data in the estimation.)

Additionally, USITC acknowledged that its estimation may “likely captures the most significant impacts of these tariffs in the short run.” However, some effects of section 301 tariffs would likely be delayed. For example, USITC said, “if importers and domestic producers anticipated the tariffs remaining in place long enough,” they may consider more costly changes, such as adjusting their supply chains and investing in domestic production.

Discussion questions:

Based on USITC’s assessment, should President Biden keep or remove the Section 301 tariffs on imports from China? Why or why not?

Regarding the impact of Section 301, any questions remain unanswered or can be studied further?

Any findings in the USITC report surprised you and why?

In December 2022, Just-Style consulted a panel of industry experts and scholars in its Outlook 2023–what’s next for apparel sourcing briefing. Below is my contribution to the report. All comments and suggestions are more than welcome!

2023 is likely another year full of challenges and opportunities for the global apparel industry.

First, the apparel industry may face a slowed world economy and weakened consumer demand in 2023. Apparel is a buyer-driven industry, meaning the sector’s volume of trade and production is highly sensitive to the macroeconomic environment. Amid hiking inflation, high energy costs, and retrenchment of global supply chains, leading international economic agencies, from the World Bank to the International Monetary Fund (IMF), unanimously predict a slowing economy worldwide in the new year. Likewise, the World Trade Organization (WTO) forecasts that the world merchandise trade will grow at around 1% in 2023, much lower than 3.5% in 2022. As estimated, the world apparel trade may marginally increase between 0.8% and 1.5% in the new year, the lowest since 2021. On the other hand, the falling demand may somewhat help reduce the rising sourcing cost pressure facing fashion companies in the new year.

Second, fashion brands and retailers will likely continue leveraging sourcing diversification and strengthening relationships with key vendors in response to the turbulent market environment. According to the 2022 fashion industry benchmarking study I conducted in collaboration with the US Fashion Industry Association (USFIA), nearly 40 percent of surveyed US fashion companies plan to “source from more countries and work with more suppliers” through 2024. Notably, “improving flexibility and reducing resourcing risks,” “reducing sourcing from China,” and “exploring near-sourcing opportunities” were among the top driving forces of fashion companies’ sourcing diversification strategies. Meanwhile, it is not common to see fashion companies optimize their supplier base and work with “fewer vendors.” For example, fashion companies increasingly prefer working with the so-called “super-vendors,” i.e., those suppliers with multiple-country manufacturing capability or can make textiles and apparel vertically, to achieve sourcing flexibility and agility. Hopefully, we could also see a more balanced supplier-importer relationship in the new year as more fashion companies recognize the value of “putting suppliers at the core.”

Third, improving sourcing sustainability and sourcing apparel products using sustainable textile materials will gain momentum in the new year. On the one hand, with growing expectations from stakeholders and pushed by new regulations, fashion companies will make additional efforts to develop a more sustainable, socially responsible, and transparent apparel supply chain. For example, more and more fashion brands and retailers have voluntarily begun releasing their supplier information to the public, such as factory names, locations, production functions, and compliance records. Also, new traceability technologies and closer collaboration with vendors enable fashion companies to understand their raw material suppliers much better than in the past. Notably, the rich supplier data will be new opportunities for fashion companies to optimize their existing supply chains and improve operational efficiency.

On the other hand, with consumers’ increasing interest in fashion sustainability and reducing the environmental impact of textile waste, fashion companies increasingly carry clothing made from recycled textile materials. My latest studies show that sourcing clothing made from recycled textile materials may help fashion companies achieve business benefits beyond the positive environmental impacts. For example, given the unique supply chain composition and production requirements, China appeared to play a less dominant role as a supplier of clothing made from recycled textile materials. Instead, in the US retail market, a substantial portion of such products was “Made in the USA” or came from emerging sourcing destinations in America (e.g., El Salvador, Nicaragua) and Africa (e.g., Tunisia and Morocco). In other words, sourcing clothing made from recycled textile materials could help fashion companies with several goals they have been trying to achieve, such as reducing dependence on sourcing from China, expanding near sourcing, and diversifying their sourcing base. Related, we are likely to see more public dialogue regarding how trade policy tools, such as preferential tariffs, may support fashion companies’ efforts to source more clothing using recycled or other eco-friendly textile materials.

Additionally, the debates on fashion companies’ China sourcing strategy and how to meaningfully expand near-sourcing could intensify in 2023. Regarding China, fashion companies’ top concerns and related public policy debates next year may include:

What to do with Section 301 tariff actions against imports from China, including the tariff exclusion process?

How to reduce “China exposure” further in sourcing, especially regarding textile raw materials?

How should fashion companies respond and mitigate the business impacts of China’s shifting COVID policy and a new wave of COVID surge?

What contingency plan will be should the geopolitical tensions in the Asia-Pacific region directly affect shipping from the region?

Meanwhile, driven by various economic and non-economic factors, fashion companies will likely further explore ways to “bring the supply chain closer to home” in 2023. However, the near-shoring discussion will become ever more technical and detailed. For example, to expand near-shoring from the Western Hemisphere, more attention will be given to the impact of existing free trade agreements and their specific mechanisms (e.g., short supply in CAFTA-DR) on fashion companies’ sourcing practices. Even though we may not see many conventional free trade agreements newly launched, 2023 will be another busy year for textile and apparel trade policy deliberation, especially behind the scene and on exciting new topics.

By Sheng Lu

Discussion question: As we approach the middle of the year, why do you agree or disagree with any predictions in the outlook? Please share your thoughts.

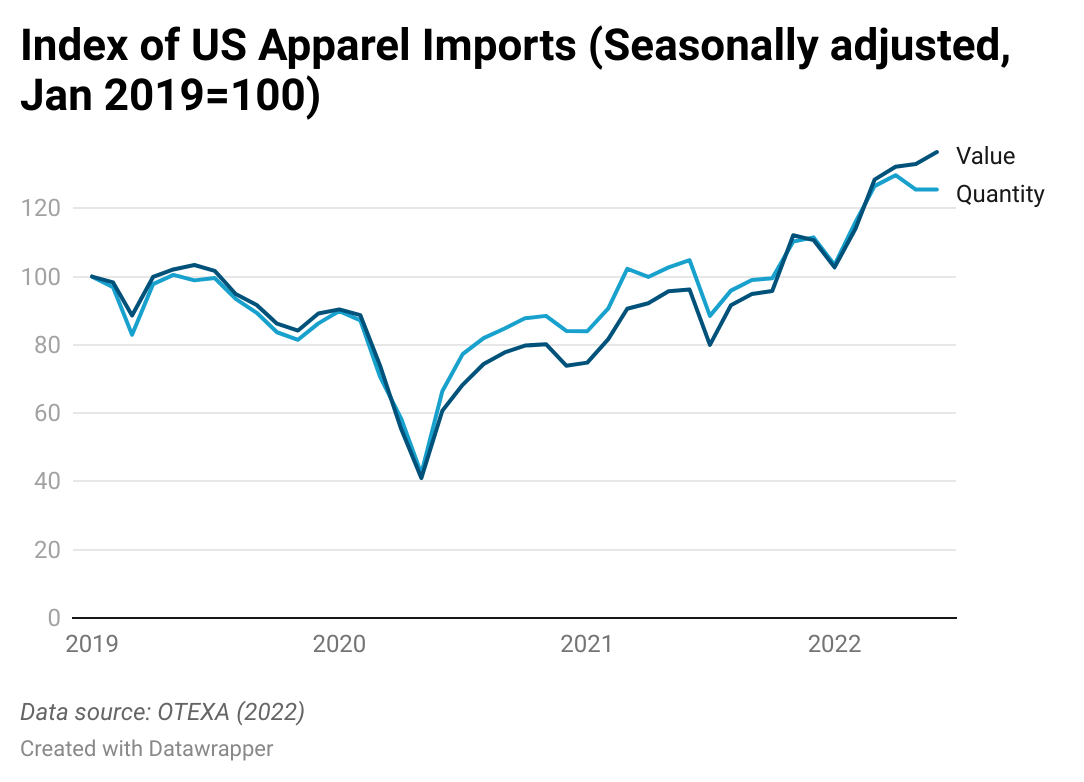

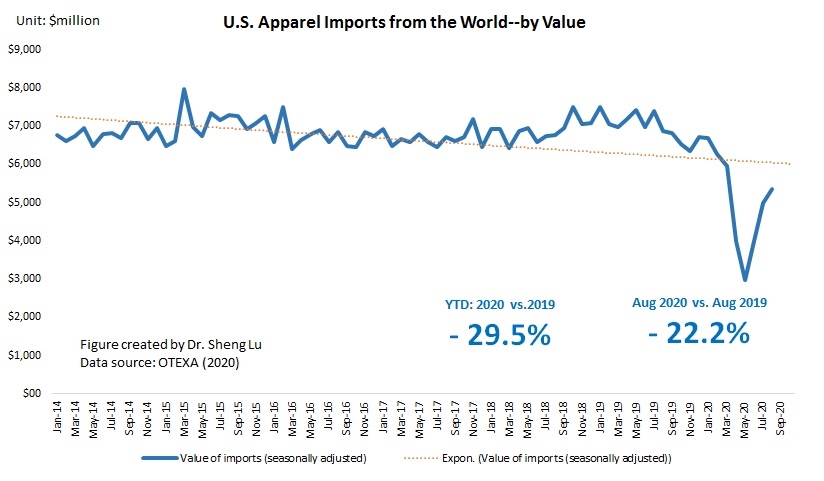

First, US apparel imports enjoyed a decent growth but started to face softening demand.

Thanks to consumers’ spending, in the first half of 2022, US apparel imports went up 40% in value and 24% in quantity from a year ago.

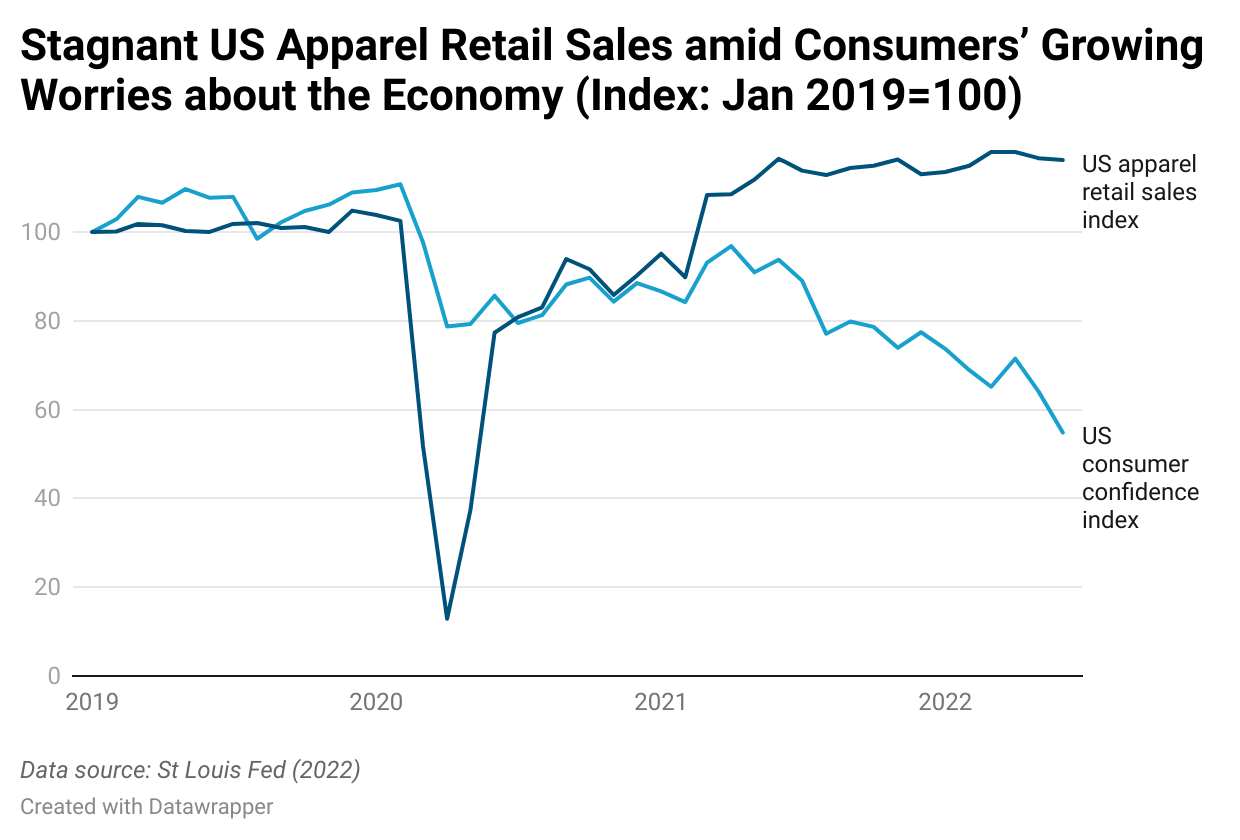

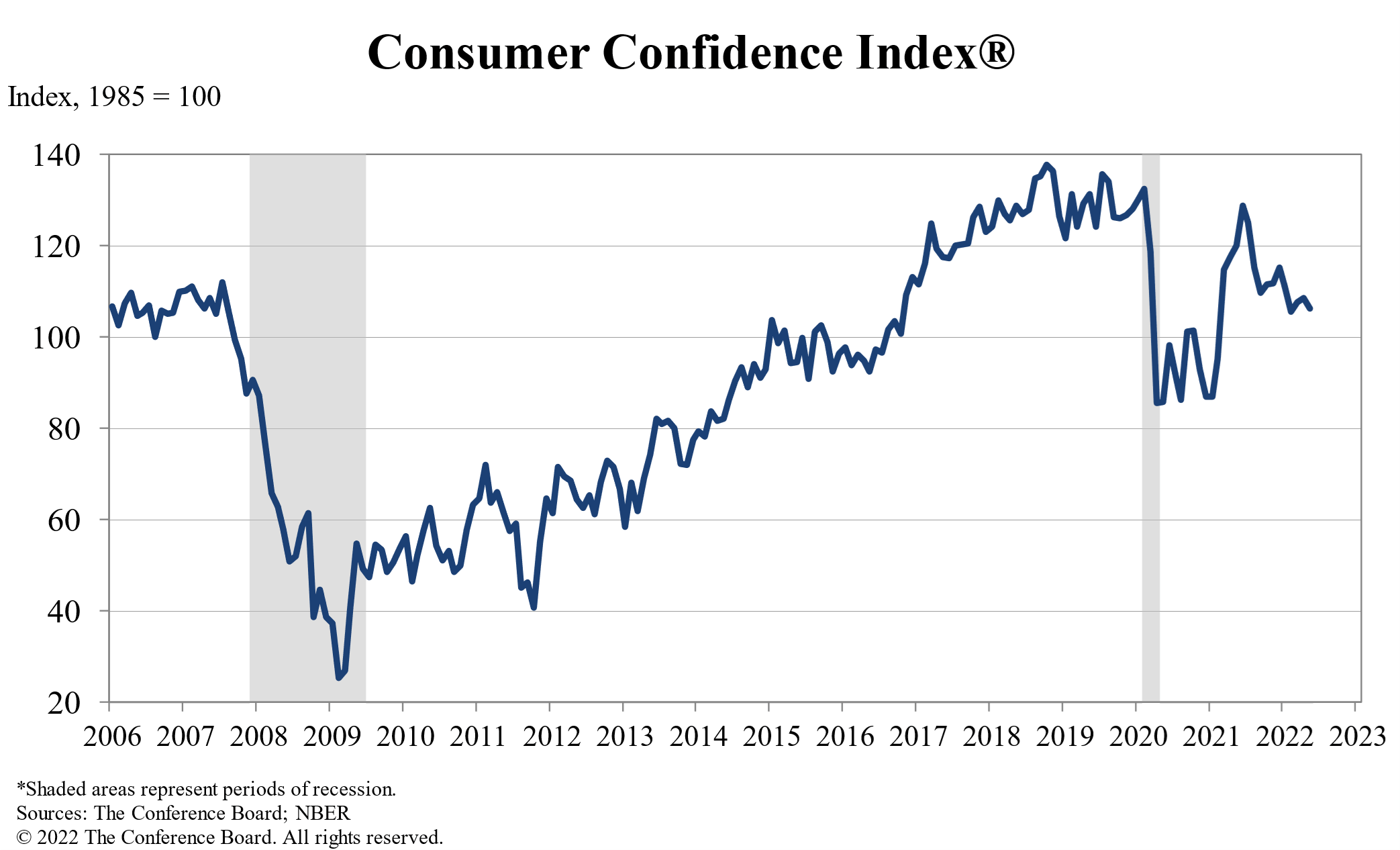

However, due to US consumers’ weakening demand amid the economic downturn, the speed of import expansion is slowing down quickly. As an alert, the US consumer confidence index (CCI) fell to 54.8 in June 2022 (January 2019=100), the lowest since the pandemic. This result suggests that US consumers were increasingly worried about their household’s financial outlook and would hold back their discretionary clothing spending.

The month-over-month growth of US apparel imports dropped to only 2.6% in value and nearly zero in quantity in June 2022 from over 10% at the beginning of the year.

As the trajectory of the US economy remains highly uncertain in the medium term, we could expect many US fashion companies to turn more conservative about placing new sourcing orders in the second half of 2022 to control inventory and avoid overstock.

Second, fashion companies struggled with hiking apparel sourcing costs driven by multiple factors.

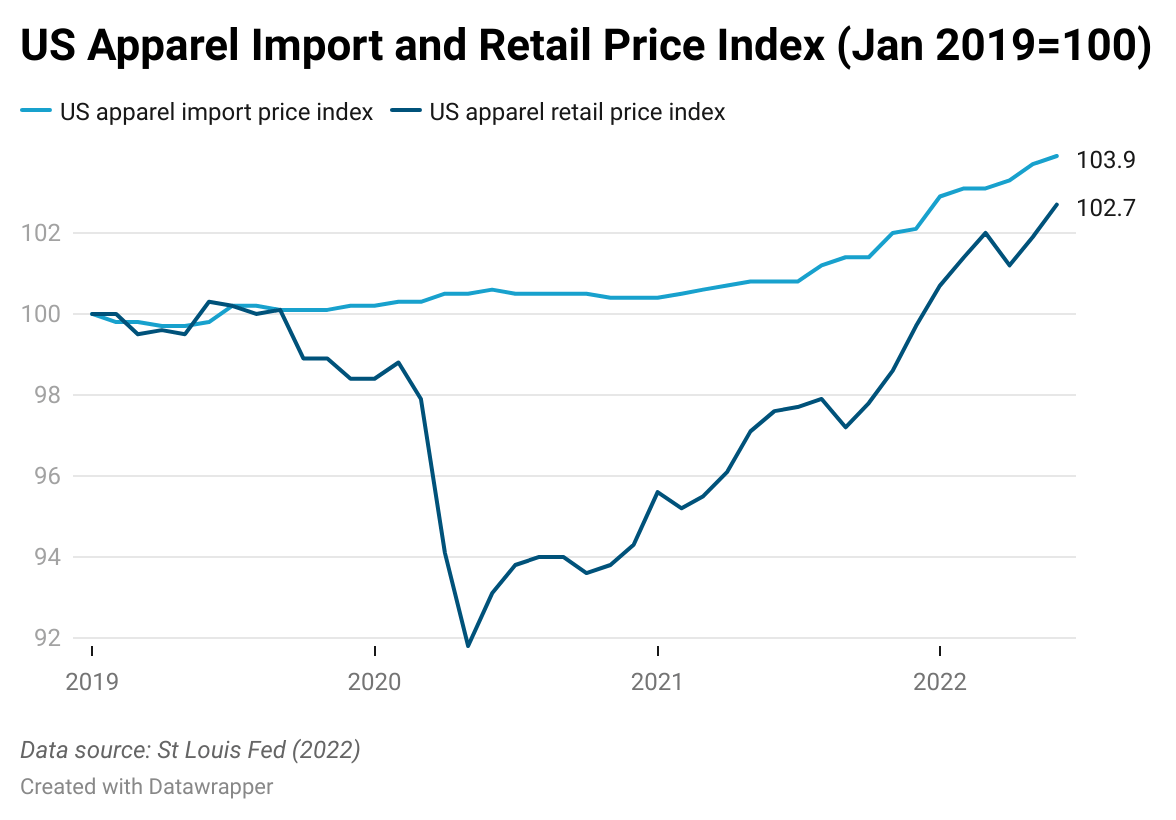

The price index of US apparel imports reached 103.9 in June 2022 (January 2019=100), a 3.1% increase from a year ago and the highest since 2019. USITC data further shows that, of the over 200 types of apparel items (HS Chapters 61 and 62) at the six-digit code level, nearly 70% had a price increase in the first half of 2022 from a year ago, including almost 40% experiencing a price increase exceeding 10 percent.

According to the 2022 Fashion Industry Benchmarking Study recently released by the US Fashion Industry Association (USFIA), 100 percent of respondents expect their sourcing costs to increase in 2022, including nearly 40 percent expecting a substantial cost increase from a year ago. Further, respondents say that almost everything has become more expensive this year, from textile raw materials, shipping, and labor to the costs associated with compliance with trade regulations.

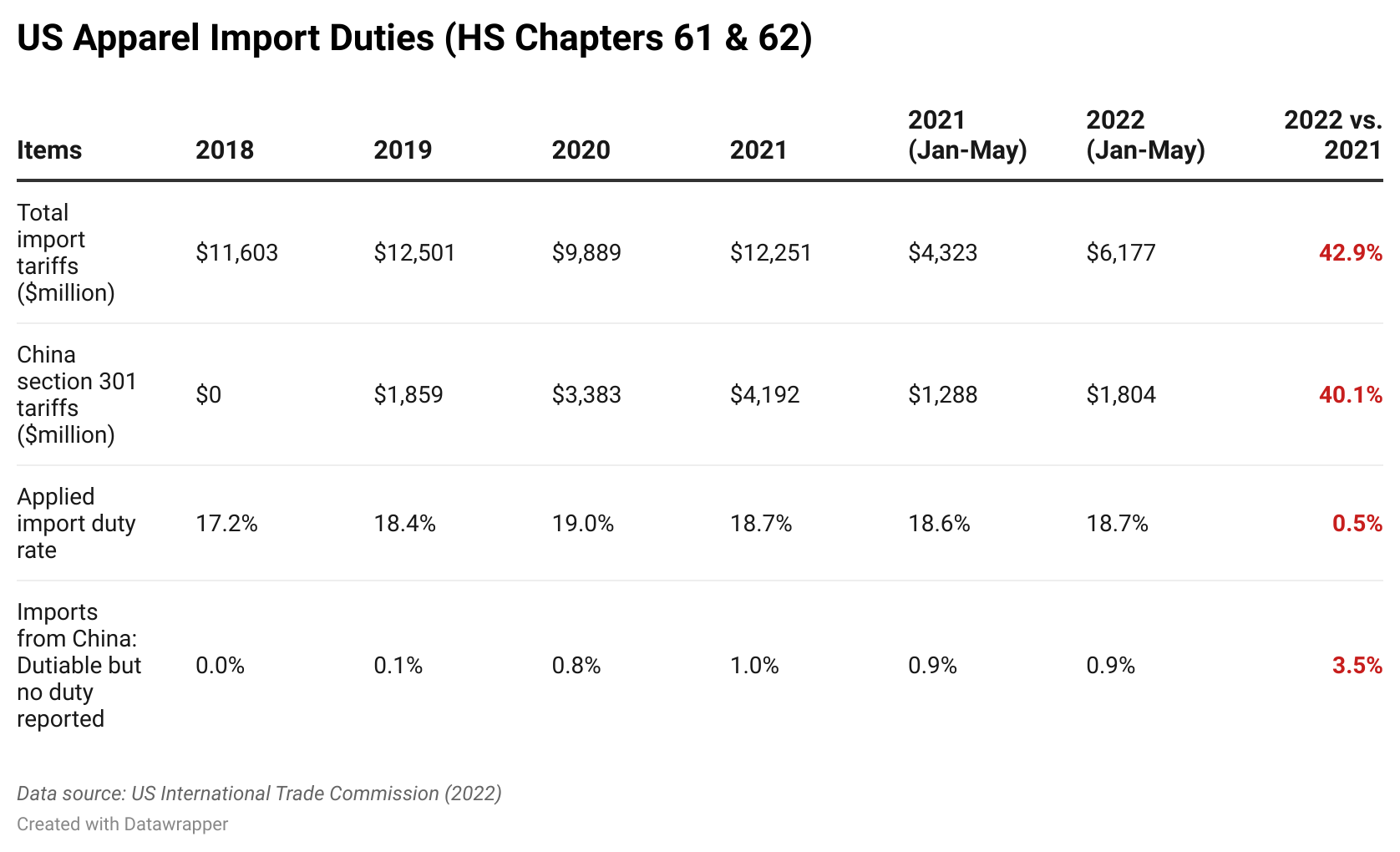

To make the situation even worse, the more expensive “cost of goods” resulted in heavier burdens of ad valorem import duties for US fashion companies. USITC data shows that in the first five months of 2022, US companies paid $6,117 million in tariffs for apparel imports (HS Chapters 61 and 62), a significant increase of 42.9% from a year ago. Of these import duties paid by US companies, about 30% (or $1,804 million) resulted from the controversial US Section 301 action against Chinese imports. Because of the Section 301 tariff action, the average applied US tariff rate for apparel imports also increased from 17.2% in 2018 to 18.7% in the first half of 2022.

Even though the US retail price index for clothing reached 102.7 in June 2022 (January 2019=100), the price increase was behind the import cost surge over the same period. In other words, given the intense market competition and weaker demand, US fashion companies couldn’t pass the sourcing cost increase to consumers entirely.

Third, US fashion companies continued to diversify their sourcing base in 2022, which benefited large-scale suppliers in Asia.

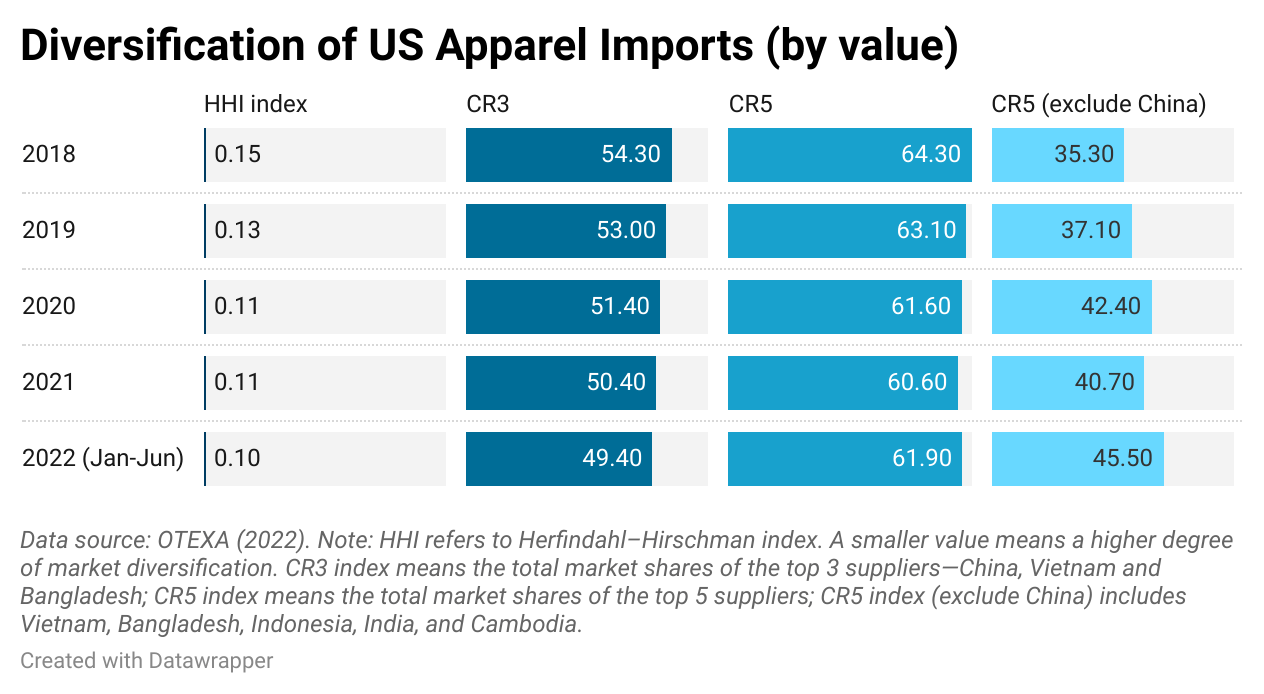

The Herfindahl–Hirschman index (HHI), a commonly-used measurement of market concentration, went down from 0.11 in 2021 to 0.10 in the first half of 2022, suggesting that US apparel imports came from even more diverse sources. Similarly, the CS3 index, measuring the total market shares of the top three suppliers (i.e., China, Vietnam, and Bangladesh), fell below 50% in the first half of 2022, the lowest since 2018.

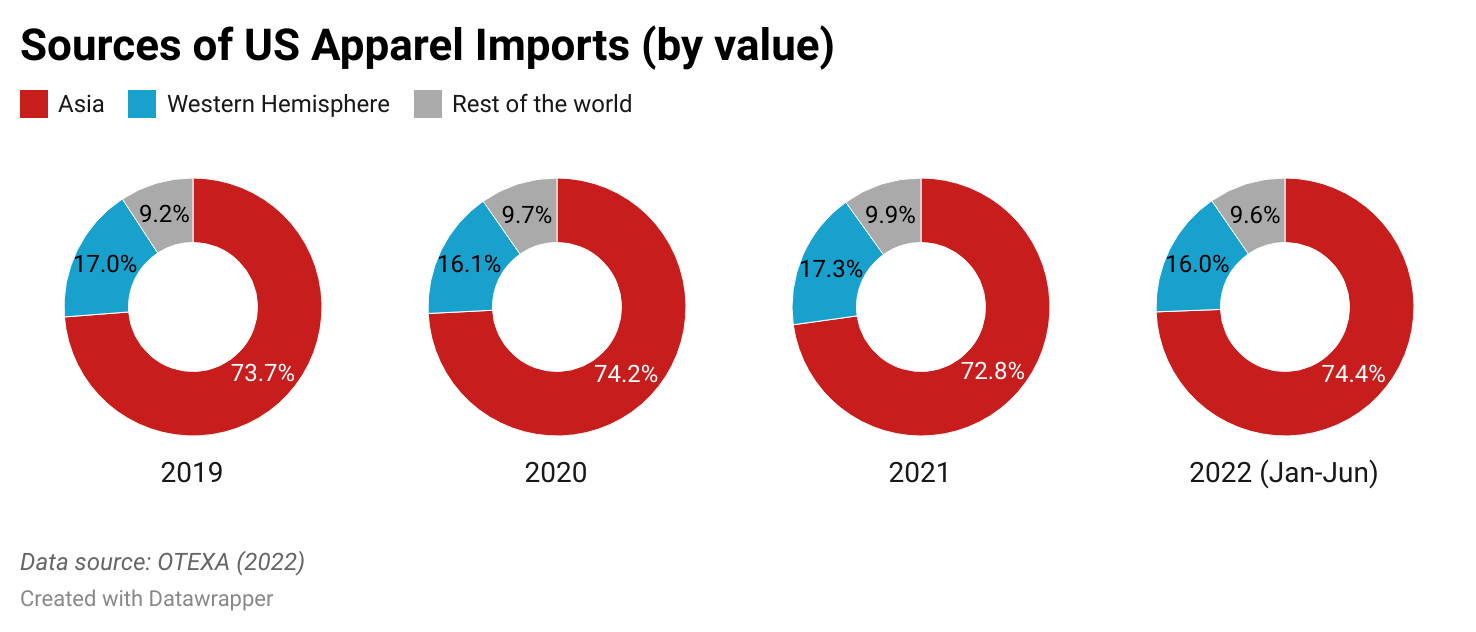

The Asia region remains the dominant source of apparel for US fashion companies: about 74.4% of US apparel imports came from Asian countries in the first half of 2022 (by value), which has stayed stable for over a decade.

One critical factor behind the apparent “contradictory” phenomenon is US fashion companies’ intention to reduce their “China exposure” further. Notably, considering all primary sourcing factors, from cost, speed to market, production flexibility, agility, and compliance risks, relatively large-scale Asian suppliers are the most likely alternatives to “Made in China.” Thus, the CR5 index excluding China (i.e., the market shares of Vietnam, Bangladesh, Indonesia, India, and Cambodia) increased from 40.7% in 2021 to 45.5% in the first half of 2022.

Fourth, US fashion companies’ evolving China sourcing strategy is far more subtle and complicated than simply “moving out of China.”

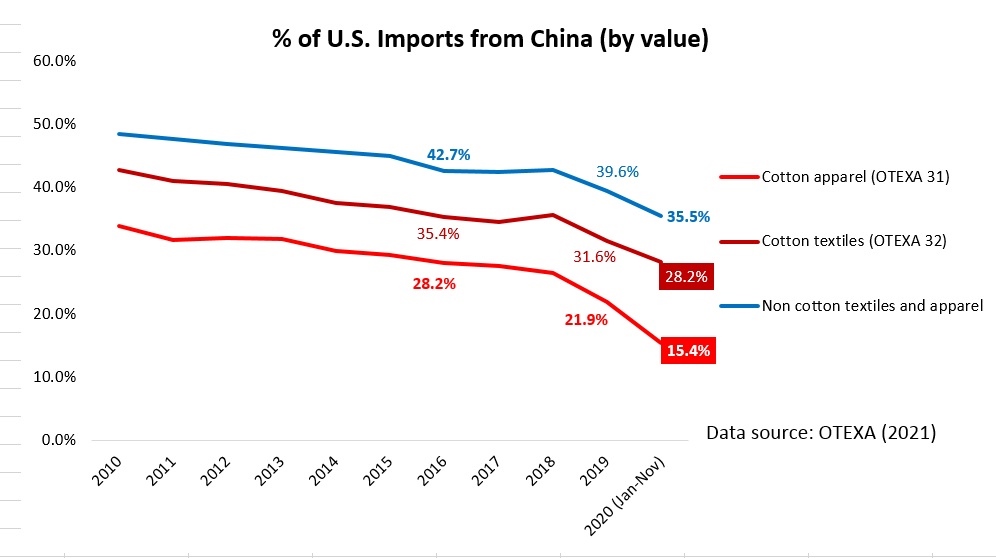

US fashion companies doubled their efforts to reduce sourcing from China in 2022, particularly in response to the newly implemented Uyghur Forced Labor Prevention Act (UFLPA) and the growing geopolitical risks. For example, measured in value, only 13.2% of US cotton apparel imports (OTEXA code 31) came from China in the first half of 2022, which fell from 14.4% a year ago and much lower than nearly 30% back in 2017.

Industry sources indicate that US fashion companies are “upgrading” what they source from China, possibly to offset the Section 301 punitive tariffs. The structural change includes importing less basic apparel items (e.g., tops and bottoms) and more sophisticated and higher-valued categories (e.g., dresses). Also, US fashion companies increasingly source from China for apparel items sold in the high-end market. For example, measured by the number of Stock Keeping Units (SKU), about 94% of apparel labeled “Made in China” sold in the US retail market targeted the value segment in 2018. However, of those apparel “Made in China” newly launched to the US retail market between January and July 2022, less than 2% were in the value segment. Instead, items targeting the higher-priced premium and mass market segments surged from 5% to 64%. Another 33% of “Made in China” were luxury apparel items. In other words, US fashion companies no longer see China as a sourcing base for cheap low-end products. Their sourcing decisions regarding China would give more consideration to non-price factors.

Fifth,US apparel imports from the free trade agreements and trade preference programs partners stayed relatively stable in 2022 but lacked growth.

Despite the growing enthusiasm among US fashion companies for expanding near sourcing from the Western Hemisphere, the trade volume stayed stagnant. For example, in the first half of 2022, members of the Dominican Republic-Central America Free Trade Agreement (CAFTA-DR) accounted for 8.8% of US apparel imports in quantity and 9.9% in value, lower than a year ago (i.e., 9.9% in quantity and 11.1% in value). Likewise, Mexico also reported lower market shares in the US apparel import market in 2022. The results remind us that encouraging more US apparel sourcing from free trade agreements and preference program partners should go beyond offering preferential duty treatment.

Product diversification is a critical area that needs improvement, particularly regarding Western Hemisphere sourcing. For example, results show that US apparel sourcing from CAFTA-DR and Mexico generally concentrated on basic items such as tops and bottoms. In comparison, Asian countries, such as China, Vietnam, and Bangladesh, could offer much more diverse categories of products. This explains why US fashion companies treat large-scale Asian countries as their preferred alternatives to “Made in China” rather than moving sourcing orders to CAFTA-DR or Mexico.

Even though the ultimate goal is to expand US apparel sourcing from the Western Hemisphere, we need to make more efforts to practically and creatively solve the bottleneck of textile raw material supply facing garment producers in the region.

This study offers valuable input and practical policy recommendations from U.S. apparel companies’ perspectives regarding expanding U.S. apparel sourcing from CAFTA-DR members. For the study, we consulted executives at 27 leading U.S.-based apparel companies (note: 85% report having annual revenues exceeding $500 million; over 95% have been sourcing apparel from the CAFTA-DR region for more than ten years).

The results confirm that expanding U.S. apparel sourcing from CAFTA-DR could be the best chance to effectively create more jobs in Central America and solve the root causes of migration there. To achieve this goal, we need to focus on four areas:

First, improve CAFTA-DR’s apparel production capacity and diversify its product offers.

As many as 92 percent of respondents report currently sourcing apparel from CAFTA-DR members.

Highly consistent with the macro trade statistics, the vast majority of respondents (i.e., 60 percent) place less than 10 percent of their company’s total sourcing orders with CAFTA-DR members.

Whereas respondents rate CAFTA-DR members overall competitive in terms of “speed to market,” they express concerns about CAFTA-DR countries’ limited production capacity in making various products. As a result, U.S. companies primarily source basic fashion items like T-shirts and sweaters from the region. These products also face growing price competition with many alternative sourcing destinations.

Improving CAFTA-DR’s production capacity and diversifying product offers would encourage U.S. apparel companies to move more sourcing orders from Asia to the region permanently.

Second, practically solve the bottleneck of limited textile raw material supply within CAFTA-DR and do NOT worsen the problem.

The limited textile raw material supply within CAFTA-DR is a primary contributing factor behind the region’s stagnated apparel export volume and a lack of product diversification.

Notably, respondents say for their apparel imports from CAFTA-DR members, only 42.9% of fabrics, 40.0% of sewing threads, and 23.8% of accessories (such as trims and labels) can be sourced from within the CAFTA-DR area (including the United States). CAFTA-DR’s textile raw material supply problem could worsen as the U.S. textile industry switches to making more technical textiles and less so for apparel-related fabrics and textile accessories.

Maintaining the status quo or simply calling for making the CAFTA-DR apparel supply chain more “vertical” will NOT automatically increase the sourcing volume. Instead, allowing CAFTA-DR garment producers to access needed textile raw materials at a competitive price will be essential to encourage more U.S. apparel sourcing from the region.

Third, encourage more utilization of CAFTA-DR for apparel sourcing.

CAFTA-DR plays a critical role in promoting U.S. apparel sourcing from the region. Nearly 90 percent of respondents say the duty-free benefits provided by CAFTA-DR encourage their apparel sourcing from the region.

The limited textile supply within CAFTA-DR, especially fabrics and textile accessories, often makes it impossible for U.S. companies to source apparel from the region while fully complying with the strict “yarn-forward” rules of origin. As a result, consistent with the official trade statistics, around 31 percent of respondents say they sometimes have to forgo the CAFTA-DR duty-free benefits when sourcing from the region.

Respondents say the exceptions to the “yarn-forward” rules of origin, including “short supply,” “cumulation,” and “cut and assemble” rules, provide necessary flexibilities supporting respondents’ apparel sourcing from CAFTA-DR members. Around one-third of respondents utilize at least one of these three exceptions when sourcing from CAFTA-DR members when the products are short of meeting the strict “yarn-forward” rules of origin. It is misleading to call these exceptions “loopholes.”

Fourth, leverage expanded apparel sourcing to incentivize more investments in the CAFTA-DR region’s production and infrastructure.

U.S. apparel companies are interested in investing in CAFTA-DR to strengthen the region’s sourcing and production capacity. Nearly half of respondents explicitly say they will make investments, including “building factories or expanding sourcing or manufacturing capacities” in the CAFTA-DR region through 2026.

CAFTA-DR will be better positioned to attract long-term investments in its textile and apparel industry with a sound and expanded apparel sourcing volume.

U.S. fashion companies report significant challenges coming from the macro-economy in 2022, particularly inflation and rising cost pressures. However, most respondents still feel optimistic about the next five years.

Respondents rated “increasing production or sourcing costs” and “inflation and outlook of the U.S. economy” as their 1st and 3rd top business challenges in 2022.

As a new record, 100 percent of respondents expect their sourcing costs to increase in 2022, including nearly 40 percent expecting a substantial cost increase from a year ago. Further, almost everything has become more expensive this year, from textile raw materials, shipping, and labor to the costs associated with compliance with trade regulations.

Over 90 percent of respondents expect their sourcing value or volume to grow in 2022, but more modest than last year.

Despite the short-term challenges, most respondents (77 percent) feel optimistic or somewhat optimistic about the next five years. Reflecting companies’ confidence in their businesses, nearly ALL respondents (97 percent) plan to increase hiring over the next five years.

U.S. fashion companies adopt a more diverse sourcing base in response to supply chain disruptions and the need to mitigate growing sourcing risks.

Asia remains the dominant sourcing base for U.S. fashion companies—eight of the top ten most utilized sourcing destinations are Asia-based, led by China, Vietnam, Bangladesh, and India.

More than half of respondents (53 percent) report sourcing apparel from over ten countries in 2022, compared with only 37 percent in 2021.

Reducing “China exposure” is one crucial driver of U.S. fashion companies’ sourcing diversification strategy. One-third of respondents report sourcing less than 10% of their apparel products from China this year. In addition, a new record of 50 percent of respondents sources MORE from Vietnam than China in 2022.

Nearly 40 percent of respondents plan to “source from more countries and work with more suppliers” over the next two years, up from only 17 percent last year.

Managing the risk of forced labor in the supply chain is a top priority for U.S. fashion companies in 2022, especially with the new implementation of the Uyghur Forced Labor Prevention Act (UFLPA).

Over 95 percent of respondents expect UFLPA’s implementation to affect their company’s sourcing. Notably, more than 85 percent of respondents plan to cut their cotton-apparel imports from China, and another 45 percent to further reduce non-cotton apparel imports from the country.

Most respondents (over 92 percent) do NOT plan to reduce apparel sourcing from Asian countries other than China. However, nearly 60 percent of respondents also would “explore new sourcing destinations outside Asia” in response to UFLPA.

Mapping and understanding the supply chain is a critical strategy adopted by U.S. fashion companies to address the forced labor risks in the supply chain. Almost all respondents currently track Tier 1 and 2 suppliers. With the help of new traceability technologies, 53 percent of respondents have started tracking Tier 3 suppliers this year (i.e., those manufacturing yarn, threads, and trimmings), a substantial increase from 25-36 percent in the past.

There is considerable new excitement about increasing apparel sourcing from members of the Dominican Republic-Central America Free Trade Agreement (CAFTA-DR). Respondents also call for more textile raw sourcing flexibility to encourage apparel sourcing from the CAFTA-DR region.

CAFTA-DR plays a more significant role as a sourcing base. About 20 percent of respondents place more than 10% of their sourcing orders from the region, doubling from 2021.

Over the next two years, more than 60 percent of respondents plan to increase apparel sourcing from CAFTA-DR members as part of their sourcing diversification strategy.

CAFTA-DR is critical in promoting U.S. apparel sourcing from the region. Around 80 percent of respondents took advantage of the agreement’s duty-free benefits when sourcing apparel from the region this year, up from 50—60 percent in the past.

Respondents say the exceptions to the “yarn-forward” rules of origin, such as the “short supply” and “cumulation” mechanisms, provide essential flexibility that encourages more apparel sourcing from CAFTA-DR members.

Respondents say improving textile raw material supply is critical to encouraging more U.S. apparel sourcing from CAFTA-DR members. Particularly, “allowing more flexibility in souring fabrics from outside CAFTA-DR” and “improving yarn production capacity and variety within CAFTA-DR” are the top two priorities.

U.S. fashion companies strongly support another ten-year renewal of the African Growth and Opportunity Act (AGOA). Meanwhile, Ethiopia’s loss of AGOA eligibility discourages U.S. apparel sourcing from the ENTIRE AGOA region.

As much as 75 percent of respondents say another ten-year AGOA renewal will encourage more apparel sourcing from the region and making investment commitments.

However, despite the tariff benefits and the liberal rules of origin, respondents express explicit concerns about the region’s lack of competitiveness in speed to market, political instability, and having an integrated regional supply chain.

Ethiopia’s loss of AGOA benefits had a notable negative impact on sourcing from the country AND the entire AGOA region. Notably, no respondent plans to move sourcing orders from Ethiopia to other AGOA beneficiaries.

The latest trade data shows that in the first four months of 2022, US apparel imports increased by 40.6% in value and 25.9% in quantity from a year ago. However, the seemingly robust import expansion is shadowed by the rising market uncertainties.

Uncertainty 1: US economy. As the US economic growth slows down, consumers have turned more cautious about discretionary spending on clothing to prioritize other necessities. Notably, in the first quarter of 2022, clothing accounted for only 3.9% of US consumers’ total expenditure, down from 4.3% in 2019 before the pandemic. Likewise, according to the Conference Board, US consumers’ confidence index (CCI) dropped to 106.4 (1985=100) in May 2022 from 113.8 in January 2022, confirming consumers’ increasing anxiety about their household’s financial outlook.

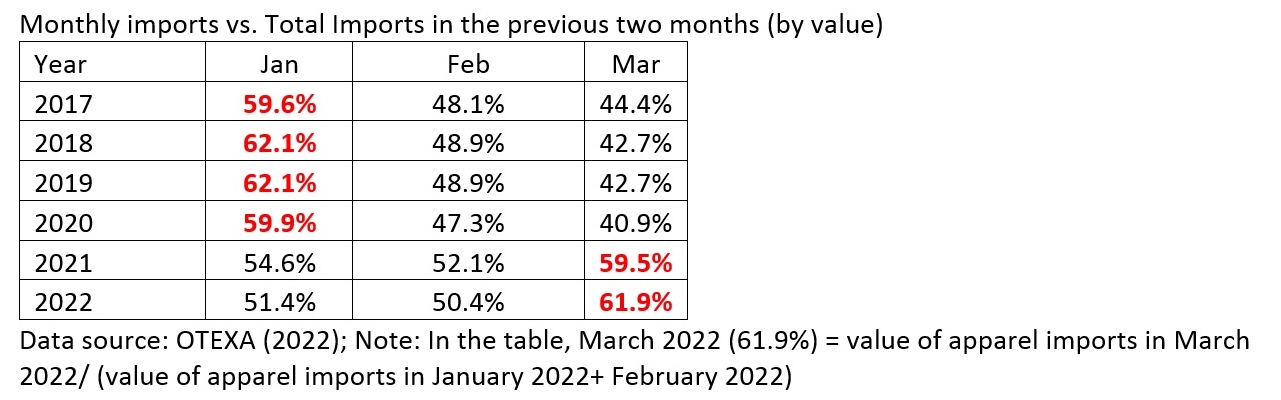

Removing the seasonal factor, US apparel imports in April 2022 went up 2.8% in quantity and 3.0% in value from March 2022, much lower than 9.3% and 11.9% a month ago (i.e., March 2022 vs. February 2022). The notable slowed import growth reflects the negative impact of inflation on US consumers’ clothing spending. According to the Census, the value of US clothing store sales marginally went up by 0.8% in April 2022 from a month ago, also the lowest so far in 2022.

Apparel import price index

Uncertainty 2: Worldwide inflation. Data from the Bureau of Economic Analysis shows that the price index of US apparel imports reached 103.1 in May 2022 (May 2020=100), up from 100.3 one year ago (i.e., a 2.8% price increase). At the product level (i.e., 6-digit HS Code, HS Chapters 61-62), over 60% of US apparel imports from leading sources such as China, Vietnam, Bangladesh, and CAFTA-DR experienced a price increase in the first quarter of 2022 compared with a year ago. The price surge of nearly 40% of products exceeded 10 percent. As almost everything, from shipping, textile raw materials, and labor to energy, continues to soar, the rising sourcing costs facing US fashion companies are not likely to ease anytime soon.

The deteriorating inflation also heats up the debate on whether to continue the US Section 301 tariff action against imports from China. Since implementing the punitive tariffs, US fashion companies have to pay around $1 billion in extra import duties every year, resulting in the average applied import tariff rate for dutiable apparel items reaching almost 19%. Although some e-commerce businesses took advantage of the so-called “de minimis” rule (i.e., imports valued at $800 or less by one person on a day are not required to pay tariffs), over 99.8% of dutiable US apparel imports still pay duties.

Uncertainty 3: “Made in China.” US apparel imports from China in April 2022 significantly dropped by 26.7% in quantity and 24.6% in value from March 2022 (seasonally adjusted). China’s market shares also fell to a new record low of 26.3% in quantity and 16.8% in value in April 2022. The zero-COVID policy and new lockdown undoubtedly was a critical factor contributing to the decline. Fashion companies’ concerns about the trajectory of the US-China relations and the upcoming implementation of the new Uyghur Forced Labor Prevention Act (UFLPA) are also relevant factors. For example, only 10.5% of US cotton apparel imports came from China in April 2022, a further decline from about 15% at the beginning of the year. Given the expected challenges of meeting the rebuttable presumption requirements in UFLPA and the high compliance costs, it is not unlikely that US fashion companies may continue to reduce their China exposure.

As US fashion companies source less from China, they primarily move their sourcing orders to China’s competitors in Asia. Measured in value, about 74.8% of US apparel imports came from Asia so far in 2022 (January-April), up from 72.8% a year ago. In comparison, there is no clear sign that more sourcing orders have been permanently moved to the Western Hemisphere. For example, in April 2022, CAFTA-DR members accounted for 9.3% of US apparel imports in quantity (was 10.8% in April 2021) and 10.2% in value (was 11.4% in April 2021).

Uncertainty 4: Shipping delays. Data suggests we are not out of the woods yet for shipping delays and supply chain disruptions. For example, as Table 2 shows, the seasonable pattern of US apparel imports in March 2022 is similar to January before the pandemic (2017-2020). In other words, many US fashion companies still face about 1.5-2 months of shipping delays. Additionally, several of China’s major ports were under strict COVID lockdowns starting in late March, including Shanghai, the world’s largest. Thus, the worsened supply chain disruptions could negatively affect the US apparel import volumes in the coming months.

In December 2021, Just-Style consulted a panel of industry leaders and scholars in its Outlook 2022–what’s next for apparel sourcing briefing. Below is my contribution to the report. All comments and suggestions are more than welcome!

What next for apparel sourcing?

As “COVID sets the agenda” and the trajectory of several critical market and non-market forces hard to predict (for example, global inflation, and geopolitics), fashion companies may still have to deal with a highly volatile and uncertain market environment in 2022. That being said, it is still hopeful that fashion companies’ toughest sourcing challenges in 2021 will start to gradually ease at some point in the new year, including the hiking shipping costs, COVID-related lockdowns, and supply chain disruptions.

In response to the “new normal,” fashion companies may find several sourcing strategies essential:

One is to maintain a relatively diverse apparel sourcing base. The latest trade data suggests that US, EU, and Japan-based fashion companies have been steadily sourcing from a more diverse group of countries since 2018, and such a trend continues during the pandemic. Echoing the pattern, in the latest annual benchmarking study I conducted in collaboration with the United States Fashion Industry Association (USFIA), we find that “China plus Vietnam plus many” remains the most popular sourcing model among respondents. This strategy means China and Vietnam combined now typically account for 20-40 percent of a fashion company’s total sourcing value or volume, a notable down from 40-60 percent in the past few years. Fashion companies diversify their sourcing away from “China plus Vietnam” to avoid placing “all eggs in one basket” and mitigate various sourcing risks. In addition, more than 85 percent of surveyed fashion companies say they will actively explore new sourcing opportunities through 2023, particularly those that could serve as alternatives to sourcing from China.

The second strategy is to strengthen the relationship with key vendors further. As apparel is a buyer-driven industry, fashion brands and retailers fully understand the importance of catering to consumers’ needs. However, the supply chain disruptions caused by COVID-19 remind fashion companies that building a close and partner-based relationship with capable suppliers also matters. For example, working with vendors that have a presence in multiple countries (or known as “super-vendors”) offers fashion companies a critical competitive edge to achieve more flexibility and agility in sourcing. Sourcing from vendors with a vertical manufacturing capability also allows fashion companies to be more resilient toward supply chain disruptions like the shortage of textile raw materials, a significant problem during the pandemic.

Further, we could see fashion companies pay even closer attention to textile raw material sourcing in the year ahead. On the one hand, given the growing concerns about various social and environmental compliance issues like forced labor, fashion brands and retailers are making more significant efforts to better understand their entire supply chain. For example, in addition to tracking who made the clothing or the fabrics (i.e., tier 1 & 2 suppliers), more companies have begun to release information about the sources of their fibers, yarns, threads, and trimmings (i.e., tier 3 & tier 4 suppliers). On the other hand, many fashion brands and retailers intend to diversify their textile material sourcing from Asia, particularly China, against the current business environment. Compared with cutting and sewing garments, much fewer countries can make textiles locally, and it takes time to build textile production capacity. Thus, fashion companies interested in taking more control of their textile raw material sourcing need to take concrete actions such as shifting their sourcing model and making long-term investments intentionally.

Apparel industry challenges and opportunities

One key issue we need to watch closely is the US-China relations. China currently remains the single largest source of apparel globally, with no near alternative. China also plays an increasingly significant role as a textile supplier for many leading apparel exporting countries in Asia. However, as the US-China relations become more concerning and confrontational, we could anticipate new trade restrictions targeting Chinese products and products from any sources that contain components made in China. Notably, with strong bipartisan support, President Biden signed into law the Uyghur Forced Labor Prevention Act on December 23, 2021. The new law is a game-changer! Depending on the detailed implementation guideline to be developed by the Customs and Border Protection (CBP), US fashion companies may find it not operationally viable to source many textiles and apparel products from China. In response, China may retaliate against well-known western fashion brands, disrupting their sales expansion in the growing Chinese consumer market. Further, as China faces many daunting domestic economic and political challenges, a legitimate question for fashion companies to think about is what an unstable China means for their sourcing from the Asia-Pacific region and what the contingency plan will be.

Another critical issue to watch is the regional textile and apparel supply chains and related free trade agreements. While apparel is a global sector, apparel trade remains largely regional-based, i.e., countries import and export products with partners in the same region. Data shows that from 2019 to 2020, around 80% of Asian countries’ textile and apparel imports came from within Asia and about 50% for EU countries. Over the same period, over 87% of Western Hemisphere (WH) countries’ textile and apparel exports went to other WH countries and about 75% for EU countries.

Notably, the reaching and implementation of new free trade agreements will continue to alter and shape new regional textile and apparel supply chains in 2022 and beyond. For example, the world’s largest free trade agreement, the Regional Comprehensive Economic Partnership (RCEP), officially entered into force on January 1, 2022. The tariff reduction and the very liberal rules of origin in the agreement could strengthen Japan, South Korea, and China as the primary textile suppliers for the Asia-based regional supply chain and enlarge the role of ASEAN as the leading apparel producer. RCEP could also accelerate other trade agreements in the Asia-Pacific region, such as the China-South Korea-Japan Free Trade Agreement currently under negotiation.

As one of RCEP’s ripple effects, we can highly anticipate the Biden administration to announce its new Indo-pacific economic framework soon to counterbalance China’s influences in the region. The Biden administration also intends to leverage trade programs such as the Dominican Republic-Central America Free Trade Agreement (CAFTA-DR) to boost textile and apparel production, trade, and investment in the Western Hemisphere and address the root causes of migration. These trade initiatives will be highly relevant to fashion companies that could use the opportunity to expand near sourcing, take advantage of import duty-saving benefits and explore new supply chains.

Additionally, fashion companies need to be more vigilant toward political instability in their major sourcing destinations. We have already seen quite a turmoil recently, from Myanmar’s military coup, Ethiopia’s loss of the African Growth and Opportunity Act (AGOA) benefits, concerns about Haiti and Nicaragua’s human rights, and the alleged forced labor in China’s Xinjiang region. Whereas fashion brands and retailers have limited or no impact on changing a country’s broader human rights situation, the reputational risks could be very high. Having a dedicated trade compliance team monitoring the geopolitical situation routinely and ensuring full compliance with various government regulations will become mainstream among fashion companies.

And indeed, sustainability, due diligence, recycling, digitalization, and data analytics will remain buzzwords for the apparel industry in the year ahead.

The virus is here to stay. What steps the companies must take to mitigate its impact?

Sheng: Earlier this year, I, together with the US Fashion Industry Association, surveyed about 30 leading US fashion brands and retailers to understand COVID-19’s impact on their sourcing practices. Respondents emphasized two major strategies they adopted in response to the current market environment. One is to strengthen the relationship with key vendors, and the other is to improve flexibility and agility in sourcing. These two strategies are also highly connected. As one respondent told us “We’re adjusting our sourcing model mix (direct vs. indirect) & establishing stronger strategic supplier relationships across entire matrix continue to build flexibility and dual sourcing options.” Many respondents, especially those large-scale fashion brands and retailers, also say they plan to reduce the number of vendors in the next few years to improve operational efficiency and obtain greater leverage in sourcing.

Which are the countries benefitting out of the US-China tariff war and why?

Sheng:The trade war benefits nobody, period. Today, textiles and apparel are produced through a highly integrated supply chain, meaning the US-China tariff war could increase everyone’s production and sourcing costs. Back in 2018, when the tariff war initially started, the unit price of US apparel imports from Vietnam, Bangladesh, and India all experienced a notable increase. Whereas companies tried to switch their sourcing orders, the production capacity was limited outside China. Meanwhile, China plays an increasingly significant role as a leading textile supplier for many apparel exporting countries in Asia. Despite the trade war, removing China from the textile and apparel supply chain is impossible and unrealistic.

How do you compare the African and Asian markets when it comes to sourcing and manufacturing? Which are the advantages both offer?

Sheng: Asia as a whole remains the world’s dominant textile and apparel sourcing base. According to statistics from the United Nations (i.e., UNComtrade), Asian countries as a whole contributed about 65% of the world’s total textile and apparel exports in 2020. In the same year, Asian countries altogether imported around 31% of the world’s textiles and 19% of apparel. Asian countries have also established a highly efficient and integrated regional supply chain by leveraging regional free trade agreements or arrangements. For example, as much as 85% of Asian countries’ textile imports came from other Asian countries in 2019, a substantial increase from only 70% in the 2000s. With the recent reaching of several mega free trade agreements among countries in the Asia-Pacific region, such as the Regional Comprehensive Economic Partnership (RCEP), the pattern of “Made in Asia for Asia” is likely to strengthen further.

In comparison, only about 1% of the world’s apparel imports come from Africa today. And this percentage has barely changed over the past decades. Many western fashion brands and retailers have expressed interest in expanding more apparel sourcing from Africa. However, the tricky part is that these fashion companies are hesitant to invest directly in Africa, without which it is highly challenging to expand African countries’ production and export capacity. Political instability is another primary concern that discourages more investment and sourcing from Africa. For example, because of the recent political turmoil, Ethiopia, one of Africa’s leading apparel sourcing bases, could be suspended for its eligibility for the African Growth and Opportunity Act (AGOA). Without AGOA’s critical support, Ethiopia’s apparel exports to the US market could see a detrimental decline. On the other hand, while these trade preference programs are crucial in supporting Africa’s apparel exports, they haven’t effectively solved the structural issues hindering the long-term development of the textile and apparel industry in the region. More work needs to be done to help African apparel producers improve their genuine export competitiveness.

Another issue is Brexit. Is that having any significant impact on the sourcing scenario of the world or is it just limited to the European nations?

Sheng: Despite Brexit, the trade and business ties between the UK and the rest of the EU for textile and apparel products continue to strengthen. Thanks to the regional supply chain, EU countries remain a critical source of apparel imports for UK fashion brands and apparel retailers. Nearly 35% of the UK’s apparel imports came from the EU region in 2019, a record high since 2010. Meanwhile, the EU region also is the single largest export market for UK fashion companies—about 79% of the UK’s apparel exports went to the EU region in 2019 before the pandemic.

However, trade statistics in the short run may not fully illustrate the impacts of Brexit. For example, some recent studies suggest that Brexit has increased fashion companies’ logistics costs, delayed customs clearance, and made talent-hiring more inconvenient. Meanwhile, Brexit provides more freedom and flexibility for the UK to reach trade deals based on its national interests. For example, the UK recently submitted its application to join the Comprehensive Progressive Agreement of the Trans-Pacific Partnership (CPTPP). The UK is also negotiating a bilateral trade agreement with the United States. The reaching of these new trade agreements, particularly with non-EU countries, could significantly promote the UK’s luxury apparel exports and help the UK diversity its source of imports.

How do you think the power shortages happening across Europe, China, and other nations, are going to impact the apparel supply chains?

Sheng: One of my primary concerns is that the new power shortage could exacerbate inflation further and result in a more severe price hike throughout the entire textile and apparel supply chain. When Chinese factories are forced to cease production because of power shortage, the impact could be far worse than recent COVID-related lockdowns in Vietnam and Bangladesh. As mentioned earlier, more than half of many leading Asian apparel exporting countries’ textile supplies come from China today. Also, no country can still compete with China in terms of the variety of apparel products to offer. In other words, for many western fashion brands and retailers, their stores and shelves could look more empty (i.e., having less variety of products to sell) because of China’s power shortage problem.

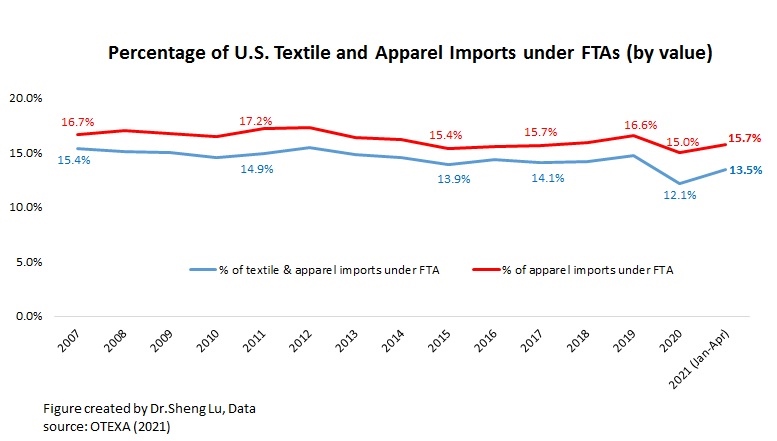

Data shows that 15.2% of US apparel imports came from USMCA and CAFTA-DR members YTD in 2021 (January-August), higher than 13.7% in 2020 and about 14.7% before the pandemic (2018-2019). Notably, CAFTA-DR members’ market shares increased to 11% in 2021 (January to Aug) from 9.6% in 2020. The value of US apparel imports from CAFTA-DR also enjoyed a 54% growth in 2021 (January—Aug) from a year ago, faster than 25% of the world’s average.

#2 Sourcing apparel from USCMA and CAFTA-DR members helps US fashion brands and retailers save around $1.6-1.7 billion tariff duties annually. (note: the estimation considers the value of US apparel imports from USMCA and CAFTA-DR members at the 6-digit HTS code level and the applied MFN tariff rates for these products; we didn’t consider the additional Section 301 tariffs US companies paid for imports from China). Official trade statistics also show that measured by value, about 73% of US apparel imports under free trade agreements came through USMCA (25%) and CAFTA-DR (48%) from 2019 to 2020.

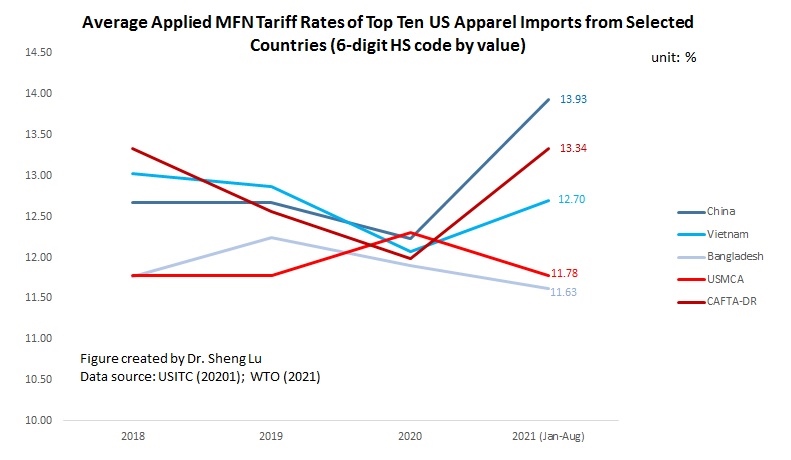

#3 US apparel imports from USMCA and CAFTA-DR members do NOT necessarily focus on items subject to a high tariff rate. Measured at the 6-digit HS code level, apparel items subject to a high tariff rate (i.e., applied MFN tariff rate >17%) only accounted for about 8-9% of US apparel imports from USMCA members and 7-8% imports from CAFTA-DR members. In comparison, even having to pay a significant amount of import duties, around 17% of US apparel imports from Vietnam and 10% of imports from China were subject to a high tariff rate (see table below).

The phenomenon suggests that USCMA and CAFTA-DR members still have limited production capacity for many man-made fibers(MMF) clothing categories (such as jackets, swimwear, dresses, and suits), typically facing a higher tariff rate. This result also implies that expanding production capacity and diversifying the export product structure could make USMCA and CAFTA-DR more attractive sourcing destinations.

#4 US apparel imports from USMCA and CAFTA-DR members tend to focus on large-volume items subject to a medium tariff rate. Specifically, from 2017 to 2021 (Jan-Aug), ten products (at the 6-digit HTS code level) typically contributed around half of the US tariff revenues collected from apparel items (HS chapters 61-62). However, the average applied MFN tariff rates for these items were only about 13%. Meanwhile, these top tariff-revenue-contributing apparel items accounted for about 50% of US apparel imports from USMCA members and nearly 64%-69% of imports from CAFTA-DR members.

Likewise, the top ten products (at the 6-digit HTS code level) typically accounted for 65%-68% of US apparel imports from USMCA members and nearly 73-75% of US apparel imports from CAFTA-DR members. These products also had a medium average applied MFN rate at 11-12% for USMCA and 12-13% in the case of CAFTA-DR.

Given the duty-saving incentives, expanding “near-sourcing” from USMCA and CAFTA-DR members could prioritize these large-volume apparel items with a medium tariff rate in short to medium terms. However, in the long run, a shortcoming of this strategy is that many such items are basic fashion clothing that primarily competes on price (such as T-shirts and trousers) and cannot leverage the unique competitive edge of near-sourcing (such as speed to market). When the US reaches new free trade agreements, particularly those involving leading apparel-producing countries in Asia, it could offset the tariff advantages enjoyed by USMCA and CAFTA-DR members and quickly result in trade diversion.

The textile and apparel industry plays a significant role in Myanmar’s economy, particularly the export sector. Data from UNComtrade shows that textile and apparel accounted for nearly 69% of Myanmar’s total exports of manufactured goods in 2020, a substantial increase from only 27% in 2011. Data from the International Labor Organization (ILO) also indicates that the textile and industry (ISIC 17 & 18) employed more than 1.1 million workers in Myanmar in 2019, up from 0.69 million in 2015. Most garment workers in Myanmar are women today (around 87%).

Since the United States lifted the import ban on Myanmar and the EU reinstated the Everything But Arms (EBA) trade preferences in 2013, Myanmar was one of the most popular emerging apparel sourcing bases among fashion companies. From 2020 to July 2021, some of the top fashion brands that carry “Made in Myanmar” apparel items include United Colors of Benetton, Next, Only, H&M, Guess, and Jack & Jones.

Thanks to foreign investment (note: nearly half of Myanmar’s garment factories are foreign-owned), Myanmar specializes in making relatively higher-quality functional/technical clothing (i.e., outwear like jackets and coats. Here is an example). This is different from many other apparel-exporting countries like Bangladesh, Vietnam, and Cambodia, mostly exporting low-cost tops and bottoms.

However, the latest trade data shows that Myanmar’s military coup that broke out in early 2021 had hurt the country’s apparel exports significantly. According to the US International Trade Commission (USITC), even though the total US apparel imports enjoyed a robust recovery in the first half of 2021 (up nearly 27%), the value of US apparel (HTS chapters 61 and 62) imports from Myanmar dropped by 0.4%. Almost ALL Myanmar’s top apparel exports to the US suffered a substantial decline or much slower growth in 2021 than the trend BEFORE the military coup (see the Table above). As US fashion companies switch sourcing orders from Myanmar to other suppliers, Myanmar’s market shares fell from 0.5% in 2020 to only 0.3% in the first half of 2021.

Highly consistent with the trade data, according to the 2021 Fashion Industry Benchmarking Study, many surveyed US fashion companies expressed concerns about the military coup in Myanmar and the rising labor and social compliance risks when sourcing from the country. Some respondents explicitly say they are leaving because of the current situation. “(We) have terminated sourcing from Myanmar due to instability.” says one respondent. Another adds, “We had orders in Myanmar that have already been moved to Cambodia. We are unlikely to place orders until the current situation is resolved.”

In another recent study, we find that apparel sourcing is not merely about “competing on price.” Instead, fashion companies give substantial weight to the factors of “political stability” and “financial stability” in their sourcing decisions today. In other words, the reputation risks matter for sourcing.

Unfortunately, the situation could get worse. The international community, including the US and the EU, is considering new sanctions against Myanmar, including suspending Myanmmar’s trade-preference program eligibility.

Designated as a “least developed country” (LDC) by the World Trade Organization, Myanmar’s apparel exports enjoy duty-free market access in the EU, Japan, and South Korea. These countries also, in general, offer very liberal “single transformation” (or commonly known as cut and sew) rules of origin for qualifying apparel made in Myanmar. This explains why Myanmar’s apparel exports mostly go to the EU (56%), Japan, and South Korea (around 30%).

The United States is another important export market for Myanmar, accounting for 7% of the country’s total apparel exports in 2020. As a beneficiary of the US Generalized System of Preferences (GSP) program, Myanmar’s luggage exports enjoy duty-free benefits in the US market. However, the US GSP program excludes textile and apparel products, meaning Myanmar’s apparel exports to the US still are subject to the regular Most-Favored-Nation (MFN) tariff rate at around 14.3% on average in 2020.

Further, given Myanmar’s highly concentrated apparel export markets and the pandemic, it will be challenging for Myanmar’s garment producers to find alternative apparel export markets in a relatively short period. For example, although China is recognized as one of the world’s largest and fastest-growing emerging import markets, only 1.4% of Myanmar’s apparel exports went to China in 2020.

According to the World Trade Statistical Review 2021 report released by the World Trade Organization (WTO), the textiles and apparel trade patterns in 2020 include both continuities and new trends affected by the pandemic and companies’ evolving production and sourcing strategies in response to the shifting business environment.

Pattern #1: COVID-19 significantly affected the world textile and apparel trade volumes, resulting in substantial growth of textile exports and a declined demand for apparel.

Driven by increased personal protective equipment (PPE) production, global textile exports grew by 16.1% in 2020, reaching $353bn. In comparison, affected by lockdown measures, worsened economy, and consumers’ tighter budget for discretionary spending, global apparel export decreased by nearly 9% in 2020, totaling $448bn, the worst performance in decades. The apparel sector is not alone. The world merchandise trade in 2020 also suffered an unprecedented 8% drop from a year ago, with COVID-19 to blame.

Notably, as economic activities returned in the second half of 2020, the world clothing export quickly rebounded to around 95% of the pre-covid level by the end of 2020. That being said, the unexpected resurgence of COVID cases in summer 2021, especially the delta variant, caused new market uncertainties. Overall, the world textile and apparel trade recovery process from COVID-19 will differ from our experiences during the 2008 global financial crisis.

Pattern #2: COVID-19 did NOT shift the competitive landscape of the world textile exports; Meanwhile, textile exports from China and Vietnam gained new momentum during the pandemic.

China, the European Union (EU), and India remained the world’s three largest textile exporters in 2020. Together, these top three accounted for 65.8% of the world’s textile exports in 2020, similar to 66.9% before the pandemic (2018-2019).

Notably, China and Vietnam enjoyed a substantial increase in their textile exports in 2020, up 28.9% and 10.7% from a year ago, respectively. The complete textile and apparel supply chain and considerable production capability allow these two countries to switch clothing production to PPE manufacturing quickly. In particular, Vietnamexceeded South Korea and ranked the world’s sixth-largest textile exporter in 2020 ($10 bn of exports), the first time in history.

The United States dropped one place and ranked the world’s fifth-largest textile exporter in 2020 (was 4th from 2015 to 2019), accounting for 3.2% of the shares (was 4.4% in 2019). Production disruptions at the beginning of the pandemic and the shift toward PPE production for domestic consumption were the two primary contributing factors behind the decline in U.S. textile exports. Due to the regional trade patterns, around 67% of U.S. textile exports went to the Western Hemisphere in 2020, including 46% for members of the U.S.-Mexico-Canada Trade Agreement (USMCA) and another 17.2% for members of the Dominican Republic-Central America Free Trade Agreement (CAFTA-DR).

Pattern #3: Fashion companies’ efforts to diversify apparel sourcing from China somehow slowed during the pandemic.

China, the European Union, Vietnam, and Bangladesh unshakably remained the world’s four largest apparel exporters in 2020. Altogether, these top four accounted for 72.2% of the world market shares in 2020, higher than 71.4% in 2019.

Notably, while China steadily accounted for declining shares in the world’s total apparel exports since 2015, its market shares rebounded to 31.6% in 2020 from 30.7% in 2019. We can observe a similar pattern in Canada (up from 36.2% to 41.2%) and the EU (31.2% to 31.3%), two of the world’s leading apparel import markets. Even in the U.S. market, where Chinese goods face adverse impacts of the tariff war, the market shares of “Made in China” only marginally decreased from 30.8% in 2019 to 29.8% in 2020, compared with a more significant drop before the pandemic (i.e., fell from 34.4% 2018 to 30.8% in 2019).