The global textile and apparel industry is becoming increasingly complex, shaped not only by conventional economic factors like production costs but also by trade policy, geopolitical uncertainty, and rapidly evolving sustainability regulations. While much of our course has focused on the U.S. market and the perspective of U.S. brands and retailers, it is equally important to understand how these forces are unfolding in other regions of the world, particularly in Europe.

The EU plays a distinctive role in the global textile and apparel system. It is one of the world’s largest apparel consumer markets, home to many leading luxury fashion brands, and a global leader in setting sustainability and regulatory standards for textiles and apparel. Therefore, developments in the EU have far-reaching implications for textile and apparel production, sourcing, and trade patterns worldwide.

We are fortunate to have Dirk Vantyghem, Director General of the European Apparel and Textile Confederation (EURATEX), join us for this interview. Dirk shared valuable insights into how the EU textile and apparel industry is navigating this rapidly changing landscape, including:

The current state of the EU textile and apparel industry, its competitive strengths in innovation, sustainability, and high-end design, and the challenges posed by rising costs and shifting consumer demand

Key sourcing and supply chain trends among EU fashion brands, including diversification, increased transparency, and nearshoring to neighboring regions

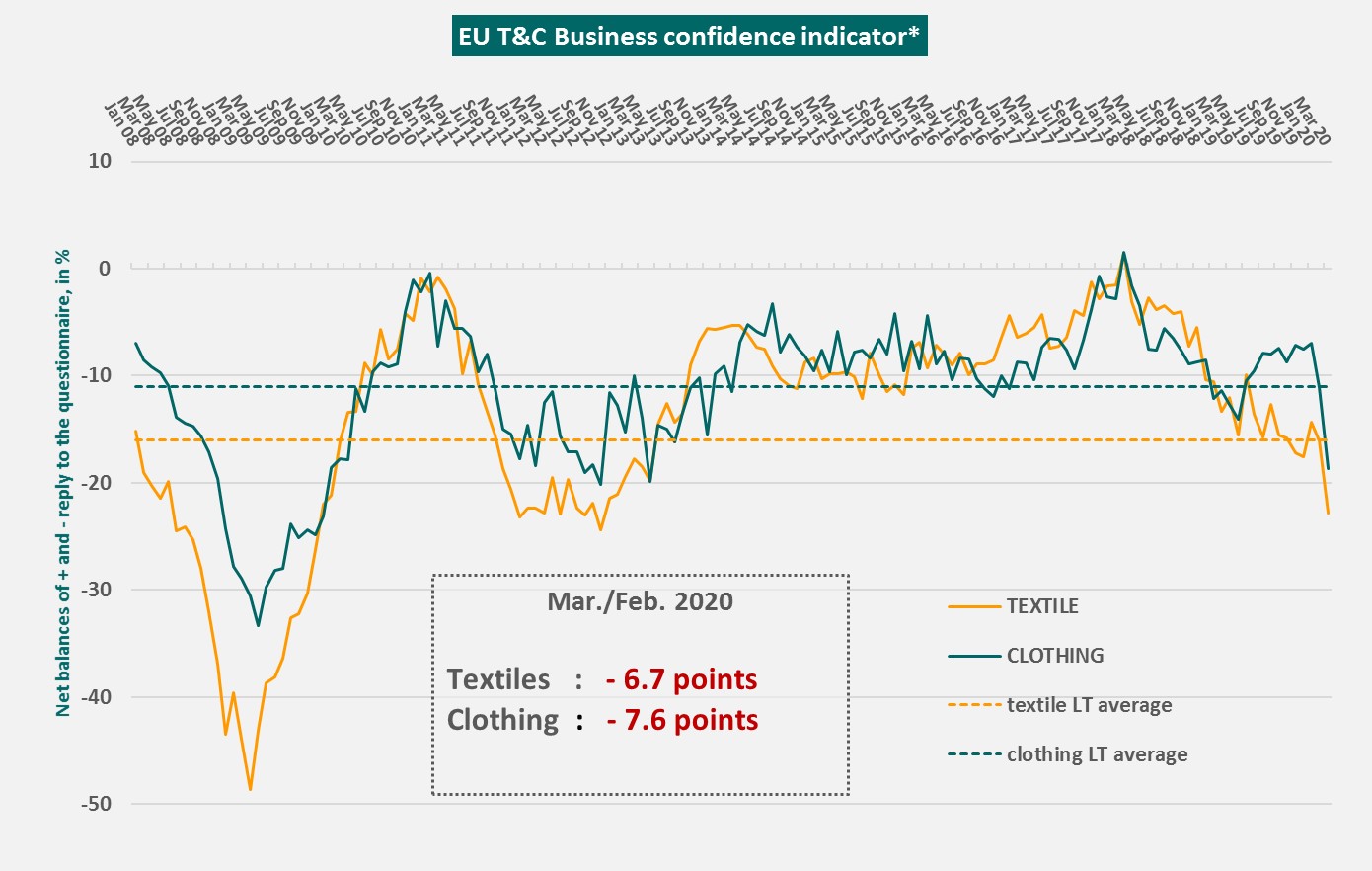

The impacts of rising trade tensions and geopolitical uncertainty on EU textile and apparel companies, and how these factors affect business strategies and consumer confidence

The EU textile and apparel industry’s approach to trade policy, balancing open markets with “fair trade” through stronger sustainability and compliance requirements, and expanding trade partnerships globally

The industry response and practical implications of the EU Strategy for Sustainable and Circular Textiles, launched in 2022, and the prospects and opportunities of textile-to-textile recycling in Europe

Potential areas for stronger U.S.-EU cooperation on textile and apparel trade, supply chains, and sustainability standards

About Dirk Vantyghem

Dirk Vantyghem is the Director General of the European Apparel and Textile Confederation (EURATEX), representing the interests of the European textile and apparel companies. Appointed in 2019, he leads the organization’s engagement with European institutions, focusing on promoting a competitive, innovative, and sustainable textile and apparel industry. Mr. Vantyghem brings over 20 years of experience in European business representation and policy advocacy, having previously served as a director at the European Chambers of Commerce and Industry (EUROCHAMBRES) in Brussels. He has extensive expertise in international trade, SME development, EU programs, and economic diplomacy, and holds a master’s degree in economics from the College of Europe.

AboutEmilie Delaye (moderator)

Emilie Delaye is a master’s student & graduate instructor in Fashion and Apparel Studies at the University of Delaware, with a specific interest in supply chain, global sourcing, and sustainability. Emilie is also a member of the Fair Labor Association (FLA) 2025-2026 Student Committee and the University of Delaware President’s Student Advisory Council.

First, the textile recycling rate remains low in the garment and footwear sector. As the OECD report noted, the market share of recycled fibers remained at approximately 7.6% in 2024 within total textile fiber production. Meanwhile, “of all recycled fibers, more than 90% was recycled polyester made from open-loop plastic bottles and less than 10% from actual post-consumer textiles.” For apparel sourcing, this means that using recycled input remains limited, fragmented, and often costly, challenging scalability for brands with large-volume sourcing models.

Second, the recycling supply chains are not immune to social responsibility and compliance risks. According to the OECD report, “Child laborin recycling processes is a key area of concern.” Meanwhile, a 2024 International Labor Organization (ILO) study cited in the report found that workers in waste management and recycling typically earn far less than in other sectors. Additionally, since “textile waste collection, aggregation and sorting are often performed manually, especially in contexts where automated systems are not common,” working conditions could be an issue. Informal workers could also be hired in the recycling supply chain. For example, the ILO estimates that about 80% of jobs in the recycling sector are informal, and in Dhaka alone, around 100,000 women and children work as informal waste pickers. Overall, for fashion brands and retailers that source clothing made with recycled textile materials, this means that due diligence must go beyond traditional Tier 1 or Tier 2 suppliers to include waste and recycling networks. Additionally, recycling activities could occur in regions different from those of garment manufacturing hubs.

Third, the large-scale export of used textiles has implications for recycling outcomes. The OECD report noted that textile waste often crosses borders for sorting or recycling. However, such textile waste trade could undermine domestic recycling capacity (e.g., in the Netherlands, half of the collected textiles are sorted abroad, and the local sorting capacity is used to sort textiles from Germany) and create environmental burdens on textile waste-importing countries. The debate over managing the used clothing trade could continue (e.g., how to avoid shifting environmental burdens from apparel-consuming countries to textile-waste-importing countries, especially those in the developing world).

Fourth, regulatory shifts are reshaping global trade related to textile recycling. The OECD report highlights the EU’s Ecodesign for Sustainable Products Regulation, the revision of the Waste Framework Directive, and the expansion of Extended Producer Responsibility (EPR) schemes. These measures, either already adopted or under development, mandate the separate collection of textiles from mixed household waste, require sorting prior to export to prevent misclassification of waste as reusable goods, and shift the financial responsibility for end-of-life management to producers. For fashion brands and retailers, these changes are likely to raise compliance costs and demand greater traceability throughout supply chains, including post-consumer waste. They also create stronger incentives to redesign products for durability, recyclability, and lower environmental impact, as regulatory fees and trade restrictions become directly tied to “product characteristics.”

Additionally, due diligence for fashion brands and retailers must be adapted to the era of circularity. The OECD report recommends that fashion companies prioritize:

scoping new high risk actors (waste pickers, sorters, informal workers),

identifying “choke points” in waste flows (e.g., large sorting hubs, major aggregators, or recycling facilities that process high volumes of textile waste and therefore have leverage over upstream practices)

evaluating how their own purchasing practices may contribute to downstream impacts (e.g., low pricing pressure or rejection of unsold goods can push waste handling into informal and unsafe channels).

meaningful engagement with workers and informal sector representatives, particularly in contexts where recycling activities occur in small workshops, open-air settings, or home-based units with limited regulatory oversight.

Summarized by Sheng Lu

For FASH455 class: When writing your blog comment, you may consider addressing the following aspects. Students are strongly encouraged to read the full report before leaving their comments.

Does global textile trade enable circularity or export waste burdens?

Should countries restrict used textile imports and exports?

Should brands prioritize textile-to-textile recyclability even if it increases costs or limits design flexibility? How might this shift sourcing geography or supplier selection?

To what extent should fashion brands and retailers be financially and legally responsible for post-production and post-consumer waste? Should waste costs be integrated into retail pricing?

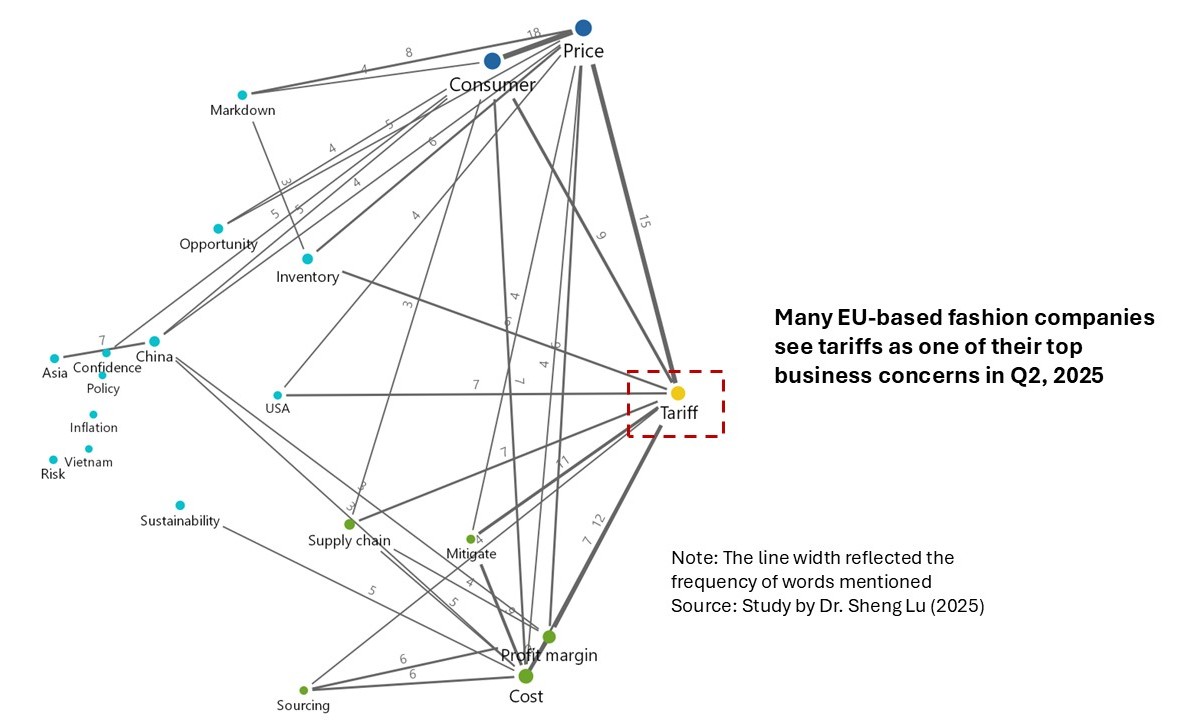

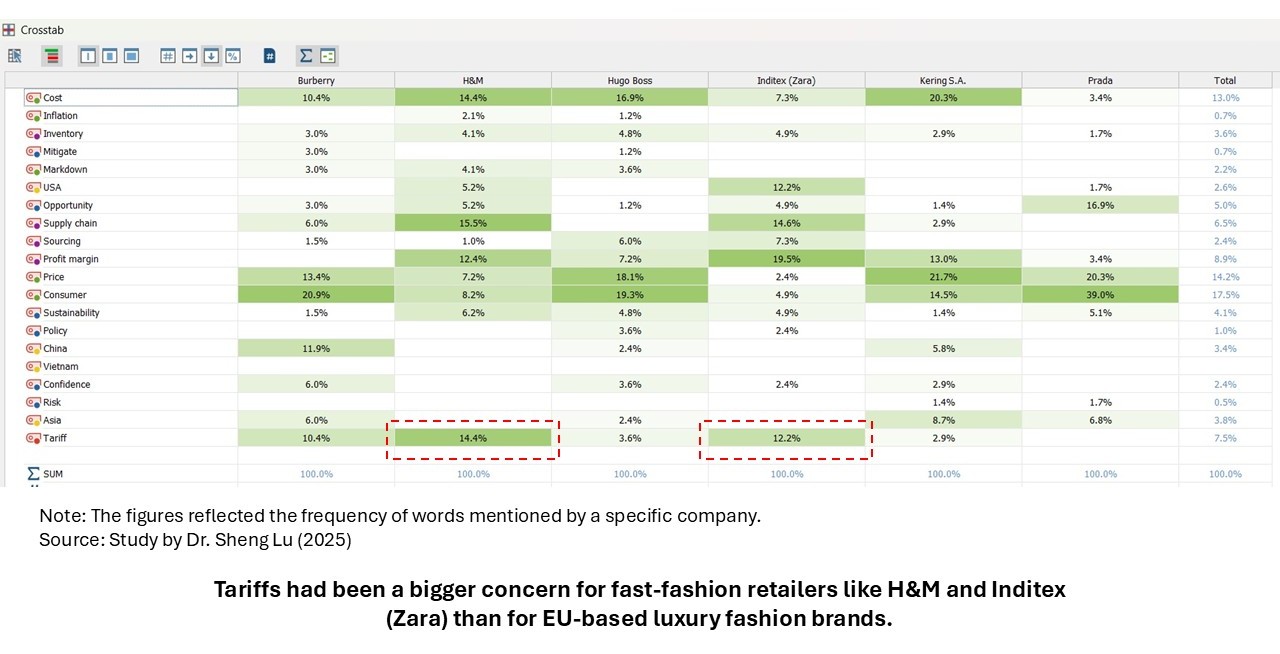

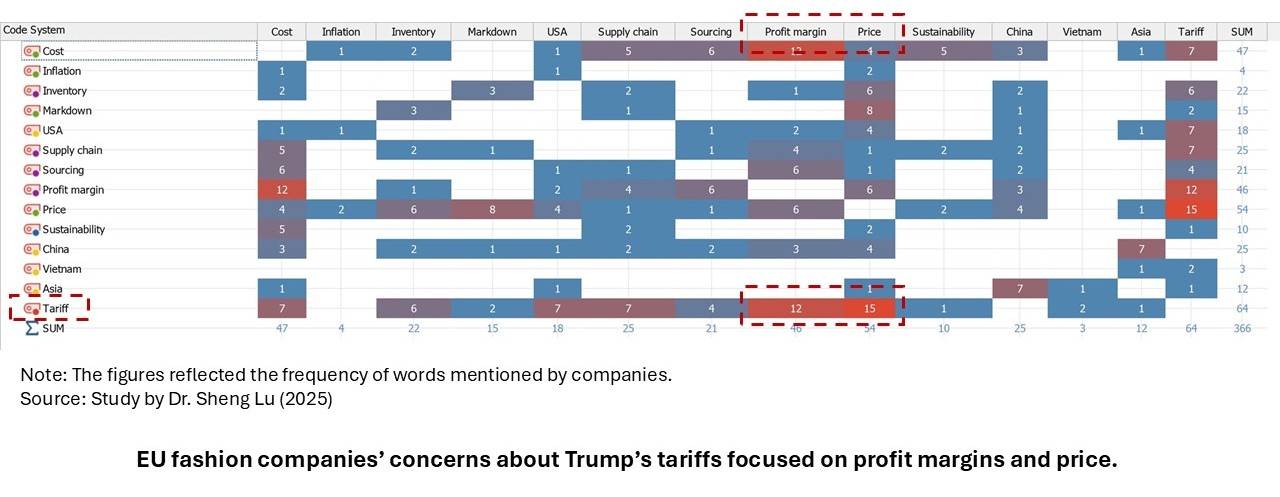

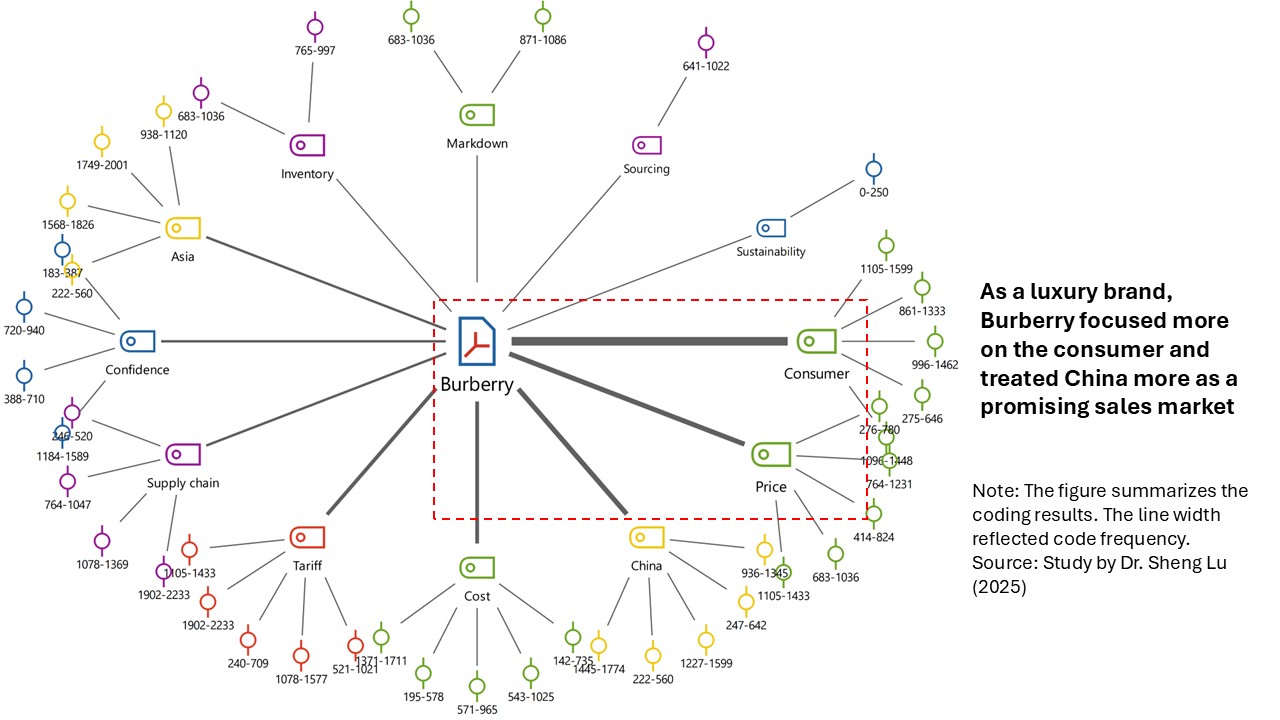

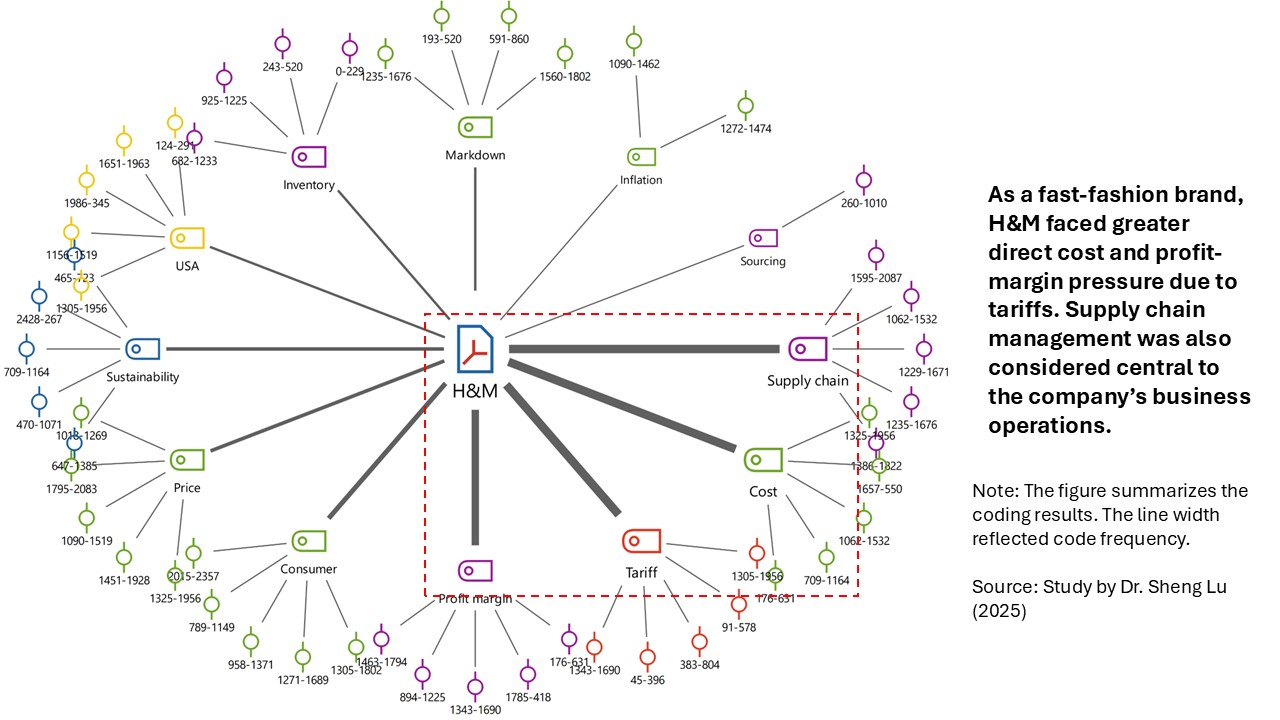

This study aims to examine the impacts of the Trump administration’s escalating tariffs on the apparel sourcing and business practices of EU-headquartered fashion companies. Based on data availability, transcripts of the latest earnings call from about 10 leading publicly traded EU fashion companies were collected. These earnings calls, held between August and November 2025, covered company performance in the second quarter of 2025 or later. A thematic analysis of the transcripts was conducted using MAXQDA.

First, reflecting the global nature of today’s fashion apparel industry, many EU-based fashion companies also see tariffs as one of their top business concerns in the second quarter of 2025. However, overall, luxury fashion companies reported less significant tariff effects than fast-fashion retailers and sportswear brands. The result reflected luxury fashion companies’ distinct cost structure, supply chain strategies, and competitive factors, making them less sensitive toward tariff-driven sourcing cost increases.

Second, EU-based fashion companies generally regarded the rising sourcing costs and the resulting pressure on profit margins as the most significant impacts of Trump’s tariffs. Companies also noted that the tariffs’ financial impacts would be more noticeable in the coming months as more newly launched products became subject to the higher import duties. For example:

Adidas: “We already had the double digit hit when it gets to cost of goods sold already in Q2 in the U. S…the impact of these duties, if they are the way we have calculated them here, an increase in cost of goods sold of about CHF 200,000,000 (about $250 million USD).”

H&M: “Against that, we have the impact of the tariffs that will then, based on the tariffs we pay during Q3, a lot of those garments will be sold during Q4, and that’s when they affect our profit and loss.”

Third, EU-based fashion companies commonly adopted a sourcing diversification strategy to mitigate the tariff impact. Companies also increasingly look for vendors that can deliver speed, flexibility, and agility. Furthermore, some EU companies have been strategically leveraging regional supply chains to meet the sourcing needs. For example:

Adidas: “We work with our suppliers who are mostly multi country…”

Hugo Boss: “Since our last update in early May, we have taken concrete steps to mitigate tariff-related impacts. Our well-diversified global sourcing footprint has a clear advantage in this regard. It enables us to swiftly adapt to changing conditions and optimize sourcing decisions.”

H&M: “We are working on how to increase the speed and reaction time in our supply chain. That’s a wide work that includes both, as we mentioned before, how we move production closer to the customer with what we call nearshoring or proximity sourcing, but it’s also working with a set of suppliers that can be much quicker and where they can support with a larger part of the product development process.”

C&A: “In the last quarter, we developed our logistics strategy to sustain C&A’s growth curve till 2030…This strategy was designed so as to bring greater speed and flexibility to our operational model through a more regionalized network, that is a network that is closer to the stores and major consumption centers, allowing us to have greater capacity to respond to the demands of each store.”

Fourth, like their U.S. counterparts, some EU fashion companies reduced their “China exposure” to lessen the impact of tariffs. Others establish a “China for China” supply chain due to perceived market opportunities there. For example:

Puma: “Our China exposure got reduced further for the Spring/Summer 2026 collection…The vast majority of our U. S. Imports originate from Asia, with Vietnam, Cambodia and Indonesia accounting for the majority…”

Adidas: “China is almost irrelevant for us because we have reduced the amount of China imports into the U. S. to only 2%…What we did is that we transferred the Chinese capacities to be mostly China for China…We have a more verticalized supply chain in China.”

Hugo Boss: “In particular, we have increased our inventory coverages in the U. S. And successfully rerouted product flows from China to other regions.”

Additionally, despite tariff-driven cost pressures, many EU-based fashion companies were cautious about raising prices, worried about losing customers in an overall weak market. Meanwhile, luxury fashion brands seem more comfortable raising prices than non-luxury brands. For example:

Adidas: “What kind of price increases could we take depending on the different duties, but there’s no decision on that…We are not the price leader, but we’d, of course, follow, a, what the market is doing, our competitor is doing and also, of course, look very closely what the consumer is accepting because in the end, it’s to keep the balance between all these factors.”

H&M: “That we do in the U.S., as we do in all other markets, and that leads to both price decreases and price increases to stay competitive. That’s an ongoing work. We are cautious about looking at the Q4 development in the U.S., given that we know we have already paid tariffs that will impact the gross margins as we look into the fourth quarter.”

Inditex (Zara): “With regards to the tariffs in the U.S. specifically, we have a stable pricing policy that we’re always talking about. Of course, all pricing activity, be it in the U.S. or any other geography, is primarily driven by commercial decisions, not financial ones. What we try to do in every market is maintain our relative position.”

Burberry: “19% of our revenues are from the US…We spent much of last year looking at the supply chain, looking at price elasticity…We took quite a surgical approach to price increases in the US, and…we really definitely understood where we had price elasticity there.”

Hugo Boss: “we will introduce moderate price adjustments globallywith the upcoming spring 2026 collections, which will begin delivery towards the 2025. These steps aim to safeguard our margin profile while remaining aligned with broader market dynamics.”

Q1. Since the pandemic, has the global fashion supply chain changed?

Key point: The pandemic taught fashion companies the importance of flexibility and agility in sourcing. Heavy reliance on China caused major disruptions during lockdowns, prompting companies to diversify their sourcing base and develop stronger supplier relationships to reduce various sourcing risks.

Q2. Is supply security now more important than price in sourcing decisions?

Key point: Security and sourcing are becoming more closely linked. Leading fashion companies understand that sourcing now requires balancing cost with other important factors such as flexibility, regulatory compliance, and risk management. New regulations related to sustainability demand increasingly detailed supply-chain documentation and transparency. Meanwhile, geopolitical tension between the U.S. and China further adds complexity to fashion companies’ sourcing decisions.

Q3. Are companies continuing to reduce the number of suppliers, and why?

Key point: Recent studies show that many fashion companies are diversifying sourcing beyond China, importing more from emerging supplying countries like Vietnam, Bangladesh, Indonesia, Cambodia, Pakistan, Egypt, and more. However, there are two divergent strategies: some brands expand their supplier base to spread risk and enhance capabilities in sustainable fibers, while others consolidate suppliers to strengthen partnerships with large vendors operating across multiple countries, many of which are still based in China.

Q4. Can the value chain function without China?

Key point: Not realistically. While China’s share of finished garment exports is declining, it still dominates in textiles raw materials. Even when apparel is made in other countries (like Vietnam and Cambodia), much of its fabric, investment, or ownership is Chinese. The newly released OECD data also show that about 30% of Southeast Asian apparel exports include Chinese content.

Q5. Which countries could take advantage of China’s declining role?

Key point: China’s dominance comes not only from its low costs but also from its capacity to produce almost any product category at large scale. To replicate this, companies need to use multiple sourcing locations — a “many-country model” instead of relying on just one. Therefore, diversification, rather than substitution, is the most practical approach. Firms seek to avoid over-dependence on any single country, especially given the volatility of tariffs and supply-chain disruptions.

Q6. Does “friendshoring” apply to fashion?

Key point: Politically appealing but impractical for apparel sourcing. The idea of friendshoring — trading only with “like-minded” nations — doesn’t fit with fashion’s global manufacturing system. Europe and the U.S. share values, but Europe lacks large-scale apparel production. Over 70% of U.S. apparel imports still come from Asia, where most countries are not formal U.S. allies. Therefore, political alignment cannot guide sourcing strategy in fashion; cost, capacity, and speed are more important.

Q7. Will geopolitics and the trade war reshape fashion sourcing in Europe or the U.S.?

Key point: Nearshoring remains a popular concept. European companies explore Eastern Europe and the Mediterranean; U.S. firms consider the Western Hemisphere and limited domestic production. Sustainability has emerged as the new opportunity for near-shoring. Fashion companies now aim to use more sustainable fibers in their clothing products. EU sustainability rules could also attract new investment to expand production in the EU. However, in general, small-sized firms need more resources and support to meet these high environmental standards, both to comply with the law and sustain their businesses.

Q8. Is de-globalizing production possible?

Key point: True de-globalization is unlikely. Instead, globalization is shifting toward greater transparency and accountability. Companies now need to track and report where products are made and how workers are treated, including the sourcing of raw materials. This encourages brands to work closely with their suppliers and promote stronger and strategic collaboration.

Q9. Are there enough incentives for production automation in fashion?

Key point: Yes — Automation provides a way to increase efficiency in high-wage countries like the U.S. With labor costs high and factories shrinking, machines and AI are being adopted to boost productivity and customization. Automation can also help cut down on overproduction — one of fashion’s major waste issues — by supporting made-to-order or small-batch manufacturing.

Q10. Why don’t we see full automation yet?

Key point: Cutting, sewing, and material handling today still require human labor, although factories increasingly use automated tools to boost productivity. Asian suppliers are upgrading equipment to handle smaller, faster orders. Automation is bringing back niche manufacturing (e.g., sock production in the U.S.) and supporting recycling efforts, such as sorting used garments. It helps lower minimum order quantities, matching production to uncertain consumer demand.

Q11. How can Europe maintain relevance amid the U.S.–China trade war?

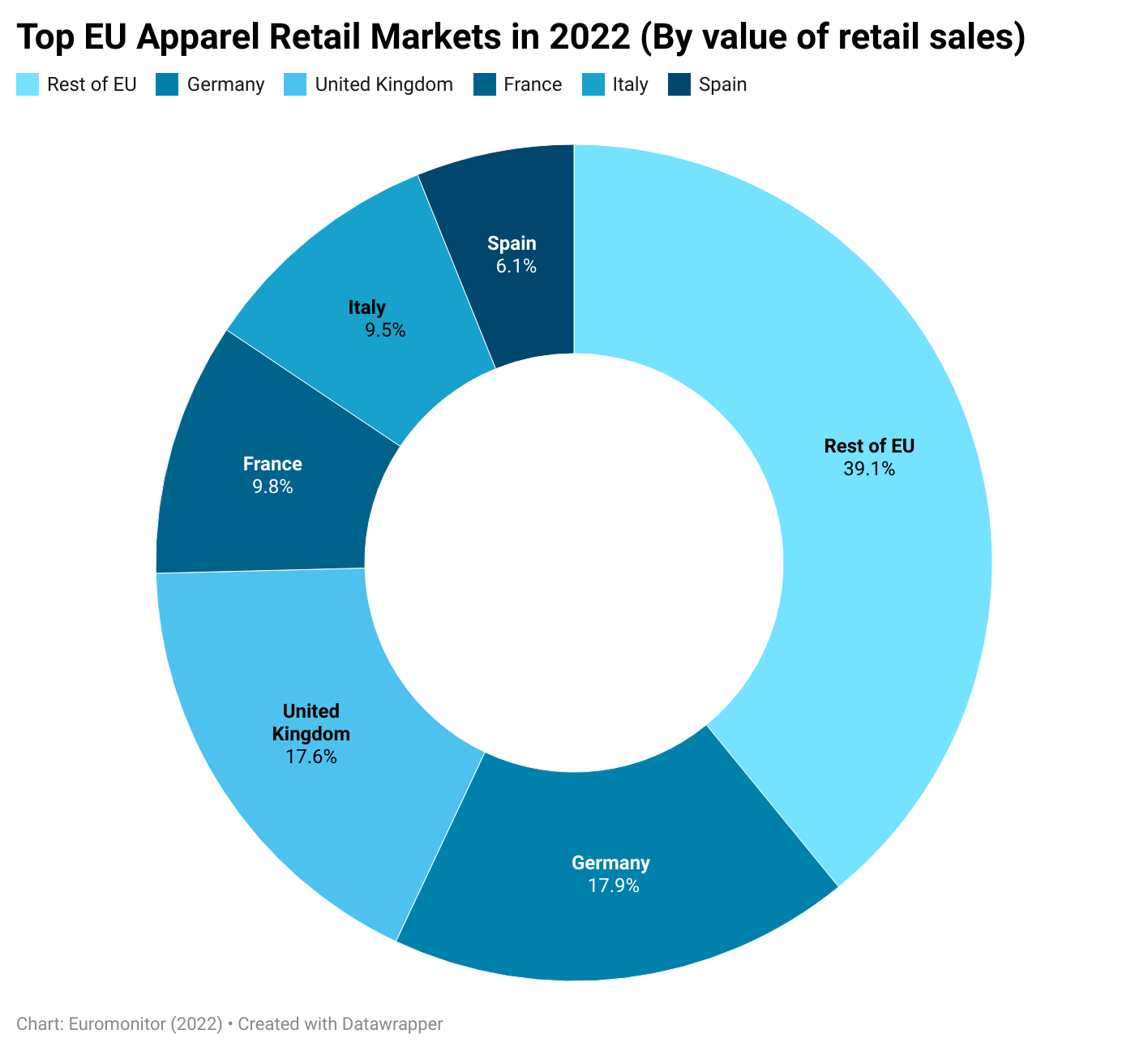

Key point: Europe continues to be a key player in both textile and apparel manufacturing and consumption. Nearly half of the apparel in the EU is produced locally, often in high-wage countries like Italy, Germany, and France. Asian countries are looking for more market access to the EU because of higher tariffs imposed by the US (e.g., trade diversion). Europe also leads in sustainability and regulatory standards. Complying with EU rules often means meeting the highest global standards. Luxury branding (“Made in Italy/France”) remains highly influential, and the EU’s proactive trade agreements might even enable it to export textiles for processing in Asia, expanding supply chain integration.

Q12. Why hasn’t Africa become a viable textile hub yet?

Key point: Africa’s potential greatly relies on trade preferences like the African Growth and Opportunity Act (AGOA), which recently expired. Without duty-free U.S. access, U.S. companies are less likely to source there. However, the EU could help bridge the gap by forging partnerships for recycled textile materials and sustainable production. Regional collaboration could unlock Africa’s place in circular fashion supply chains.

For students in FASH455: Feel free to share your thoughts on any of the interview questions above. You may also challenge and debate any points raised in the interview and present your arguments.

This study explored the survival strategies of apparel manufacturing in a high-wage developed economy using “Made in Ireland” as a case study. Based on a statistical analysis of 4,000 apparel items for sale in the retail market from January 2018 to December 2021, the study found that:

First, unlike the conventional views like the factor proportion trade theory and the global value chain theory, the study’s results showed that garment manufacturing did NOT disappear in Ireland as a high-wage developed country. Notably, garments “Made in Ireland” demonstrated many unique attributes, such as:

statistically more likely to target luxury and high-end markets than foreign-made apparel imported into Ireland;

statistically more likely to highlight their Irish cultural heritage and mention keywords such as “traditional,” “centuries-old,” “craftsmanship,” and “historical” in the product description;

statistically more likely to focus on manufacturing specific product categories with a world reputation, including jumpers and kilts;

statistically less likely to be seen in categories with an abundant supply from lower-cost imports, such as bottoms;

In other words, economic theories need to incorporate non-price competition factors and better explain the development patterns of a country’s garment sector, particularly in developed economies.

Second, the findings called for a rethink of the strategies supporting the garment-manufacturing sector in a high-wage developed country. Current industry practices and government policies aiming to promote garment manufacturing in a developed country primarily focus on implementing protectionist trade measures (i.e., restricting imports) or investing in modern technologies like automation. However, the study’s findings suggested new approaches. For example, using disaggregated product data at the Stock Keeping Unit (SKU) level, the study indicated that a substantial portion of garments “Made in Ireland” was sold overseas. Thus, promoting exports instead of curbing imports could be a more effective way of expanding garment production in a high-wage developed country.

On the other hand, the popularity of “Made in Ireland” jumpers and kilts in the world marketplace suggested that garment manufacturers in a high-wage developed country could survive their business by leveraging cultural heritage, history, and traditional craftsmanship instead of fancy new technologies. Likewise, to a certain extent, the value of maintaining garment manufacturing in a high-wage developed country in the 21st Century may not necessarily be about replacing imports, improving “speed to market,” or creating jobs but preserving a country’s unique cultural heritage and history.

Third, the study’s findings revealed the challenges facing garment manufacturers in a high-wage developed country like Ireland. For example, garments “Made in Ireland” were more likely to be sold with a discount, implying their price competition with foreign-made imports might not be entirely avoidable despite all the efforts from targeting the niche markets to differentiating product assortments.

On the other hand, garments “Made in Ireland” often targeted the high-end market, requiring the workforce to obtain demanding skills such as advanced sewing, craftsmanship, and a deep understanding of the Irish culture. However, the aging workforce and the shortage of skilled labor, a common problem facing developed countries, could also prevent the expansion of apparel manufacturing in Ireland in the long run. Thus, prompting the traditional Irish culture and apparel production craftsmanship, especially to attract the young generation to garment factories and be willing to pursue a career there, would be critical for sustaining the garment manufacturing sector in Ireland and other high-wage developed countries.

Background

Ireland has a long history of making garments, and specific categories of apparel “Made in Ireland” are famous worldwide, such as jumpers and kilts. As of 2020 (i.e., the latest data available), about 340 garment factories still operate in Ireland, a notable increase from 293 in 2010 (Eurostat, 2022). Meanwhile, the output of Ireland’s apparel manufacturing sector totaled $68 million in 2020 (measured in value-added), a substantial drop from $142 million ten years ago (Eurostat, 2022).

Meanwhile, export was critical in supporting apparel “Made in Ireland” today. Statistics show that Ireland’s apparel exports totaled $270 million in 2019 before the pandemic, down about 19% from 2005 (UNComtrade). However, over that period, Ireland’s apparel exports to most developed countries enjoyed positive growth, such as Spain (up 151%), the Netherlands (up 4.5%), Germany (up 14.5%), France (up 61.6%), and Japan (up 20.2%). Further, Ireland’s top four largest apparel export markets were all developed Western EU countries (UNComtrade, 2022). Geographic proximity and the specific product structure of Ireland’s apparel exports could be important factors behind these distinct export patterns.

by Miriam Keegan (FASH MS student, Fulbright-EPA scholar) and Sheng Lu

Full paper: Keegan, M. & Lu, S. (2023). Can garment production survive in a developed economy in the 21st century? A study of “Made in Ireland”. Research Journal of Textile and Apparel. (ahead of print) https://doi.org/10.1108/RJTA-09-2022-0113

Natalie Kaucic is a Merchandising professional currently in the role of Global Merchant for Dockers Men’s Tops at Levi Strauss & Co. She graduated from the University of Delaware in 2019 with a Fashion Merchandising Degree and Business Admin minor. During her studies, she was awarded the Fashion Scholarship Fund scholarship, studied at John Cabot in Rome, participated in the Disney College Program, and was a leader for the Delaware Diplomats. Natalie’s research on the global market for sustainable apparel was published in Just-style, a leading fashion industry trade publication. Post university, Natalie started as an assistant at Minted as a Merchandiser, where she worked in the Wedding category and faced the adverse challenges of the wedding industry during COVID-19. Levi’s was her next endeavor where she started as an assistant, and has since been promoted to run the Dockers Men’s Tops Category for the Globe.

Disclaimer: The comments and opinions expressed below are solely my own and do not reflect the views or opinions of any company.

Sheng: What are your primary job responsibilities as a global merchant? What does a typical day or week look like for you? Which part of the job do you find most exciting? Were there any aspects of the position that surprised you after you started?

Natalie: My primary responsibility is to create a brand-right and consumer-focused product assortment. Under the covers, this looks like a vast variety of tasks that I do on a seasonal basis. I regularly listen and work with regional merchandising to understand their regional specific needs, collaborate with design on new product ideas and fabrics, and meet with product development to work on new fabric innovations and product costing. Every week looks dramatically different for me in my work. Sometimes, I’m heads down in assortment strategy; other weeks, I work on creating templates and calendars for process improvement.

What I find most exciting is seeing the product in person. Most Dockers Tops are not sold domestically, so it’s really fun to see a product you worked on in the wild! I am also grateful to be able to manage an assistant. Seeing things click for her and watching her succeed is incredibly motivating.

What surprised me the most was the number of different teams I work with, including planning, regional merchants, product development, marketing, styling, design, garment/fit development, copy, IT, analytics, sales, business operations, and e-commerce. Learning what everyone does and who to go to was the most significant learning curve and the biggest shock coming into my role.

Sheng: Based on your observation and experience, how do the merchandising, product development, and sourcing teams collaborate in a fashion apparel company? Could you explain their respective responsibilities and how they support one another?

Natalie: In my role, I have more direct contact with our product development team than the sourcing team. I work very closely with product development as they are the team that helps produce our product. They manage fabric & garment development, costing negotiations, and innovation development/testing. They also work through some more micro-sourcing strategies, for example, moving the production from one factory to another to get better duty rates. As a hypothetical example, we sell a poplin shirt primarily in Europe. Pretend we produce the shirt in India at a cost of $10/each. However, shipping it to Europe incurs a 40% import duty, bringing the cost of goods sold (COGS) to $14. If we could produce the shirt in Mexico, where the duty rate to Europe is only 5%, even if the production cost is higher—say $12—the overall cost to Europe would still be lower. There are endless complexities to this that I’m sure you will learn more from FASH455—topics like free trade agreements, yarn forward rules of origin, etc.

Sheng: Fashion companies need to balance various factors such as cost, quality, speed to market, and compliance risks when deciding where to source their apparel products. Could you share your experiences and reflections on managing these challenges in the real world?

Natalie: Below is an example of natural fibers and the cost challenge with cotton-forward apparel products.

Currently, linen is in high demand, but there isn’t enough crop to meet industry needs—it’s a classic case of supply and demand. Not only does this drive up costs (COGS), but it also complicates the process of securing raw materials. It’s easy to overlook that the apparel industry is fundamentally tied to agriculture, making it vulnerable to factors like bad weather, natural disasters, and inaccurate demand forecasting. These challenges force us to make critical decisions. With rising garment costs, should the company absorb the expense to keep prices steady for consumers? Our product development team might ask if we need to pre-book fibers to lock in pricing—when is the right time to do that, and how much should we purchase?

This isn’t a new challenge. For example, cotton, our primary raw material for clothing, fluctuates in price like oil, making agility in sourcing essential!

Sheng: Studies show that consumers want to see more “sustainable apparel products” in stores. How are fashion companies responding to this demand? What opportunities and challenges does this trend present for fashion companies’ business operations, especially in merchandising, supply chain, and sourcing?

Natalie: This is such a complicated question. I think about this often as I am personally really passionate about this topic!

In my day-to-day work, I focus on sustainable fibers, as the fabric content of a garment is something I can directly influence. Working on a global scale, I collaborate with regions worldwide, each of which—along with their retailers—has different values regarding sustainable products. Europe, for instance, is relatively ahead of the US in sustainability and often requires a certain percentage of sustainable fibers (e.g., organic cotton, recycled cotton) in our products. In Europe, items using 100% organic cotton hold significant value and can command a higher price in stores such as Galeries Lafayette or Zalando. However, not all retailers and consumers globally share the same commitment to sustainability. In some cases, we may need to use synthetics for functional purposes, such as in activewear. In those instances, we prioritize using recycled polyester or nylon to meet our sustainability goals. Regardless of the consumer or price point, our goal is to integrate sustainability at every level and for every product.

One challenge I find particularly interesting is working with “recycled cotton.” As you may know, recycling cotton typically involves breaking down the fibers, which shortens and weakens them. Because of this, there’s usually a limit to how much recycled cotton can be used before fabric quality is affected. That’s why you often see recycled cotton blended with virgin cotton in the same garment. However, newer recycling methods that aim to preserve the staple length are emerging, offering hope for improvements as the technology becomes more mature and accessible.

Ultimately, heavy consumption, regardless of the fabric being recycled or organic, isn’t truly sustainable. The focus should be on choosing pieces you love and investing in items that are made to last.

Sheng: Are there any other major trends in the fashion industry that we should closely monitor in the next 1-3 years?

Natalie: In the next 1-3 years, I’m eager to see what AI-driven tools will be introduced to assist merchants in making smarter, data-backed decisions. In merchandising, we are constantly trying to predict the future. A lot of research and data analysis go into decision making, but also a big handful of going with your gut. Will AI be able to help us find trends in the past that can better help us make decisions for the future?

It’s not exactly a trend, but I’m really curious about the future of fast fashion giants over the next decade. With growing interest in sustainability and new regulations emerging from Europe, will we eventually see a decline in these dominant players, or will demand for fast, cheap apparel always persist?

Sheng: Last but not least, is there anything you learned from FASH455 or other FASH courses that you find particularly relevant and helpful in your career? What advice would you offer current students preparing for a career in the fashion apparel industry?

Natalie: I felt really prepared coming out of the FASH program for my corporate job. I picked this degree, as I’m sure many have because it combined the necessary key concepts of a business degree with the skills and knowledge to build a career in apparel. I think the classes I reference the most in my day-to-day life are product development classes, textile classes, and apparel buying. As a merchant, I need to be able to talk about fabric types with designers, cost engineering with product developers, and financial metrics with planners. FASH455 was one of my favorite classes because sourcing, trade, geopolitics, and policy constantly pull the strings behind the scenes in the apparel sector. FASH455 gives you insight into how these factors create ripples in the apparel sector.

When it comes to advice, it’s tried and true: network! Talk to teachers, reach out to alumni, sign up for the UD Job Shadow Program, and talk to the career center. There are so many services to take advantage of while at UD. Other than networking, I would highly recommend steering the subjects of your papers to companies and topics you are interested in. I worked on a few reports about Levi Strauss & Co., which confirmed it as a target company for me and helped me succeed in the interview process.

Lastly, be flexible! You might come in, as I did, thinking you want to be a buyer, only to realize it’s not the best fit. Or, you could start with greeting cards and stationery merchandising and pivot to apparel. Or even move out of apparel entirely! Nothing is set in stone, and that’s both the most stressful yet reassuring lesson I’ve learned since graduating.

The study is available HERE (published by the Government of the Netherlands). Key findings:

Size of used textiles trade:

In 2022, the Netherlands exported 248,000 tons of used textiles (or over €193 million), the highest in the past five years. This trend aligned with the EU’s broader used clothing exports, which reached 1.7 million tons in 2019. The average European price for used textiles was around €0.76 per kg in 2019.

In 2018, 84% of used textiles collected in the Netherlands were exported, with 53% being suitable for re-wearing, 33% recycled, and 14% being nonrecyclable and non-renewable.

Destinations of the used textile exports

Trade data analysis (HS6309 and HS6310 from 2017 to 2022) and interviews revealed several key export destinations for used clothing exports from the Netherlands:

Poland and Pakistanas Import-export hubs. The high volumes of HS 6309 (used textiles) exports from the Netherlands to Poland likely reflect the lower labor costs for labor-intensive manual sorting in Poland. For the last five years, Pakistan has also been a top-five destination for Dutch used textile exports (under HS6309). Four of the six Dutch collector-sorters interviewed confirmed that Pakistan is a primary export destination, noting that the lowest quality textiles were usually sent there. However, Pakistan is also the world’s sixth largest used clothing exporter, suggesting Pakistan is unlikely to be the final destination for the Dutch used textile exports but an import-export hub.

India is positioned as a significant recycling hub, particularly for HS 6310 (sorted and unsorted used rags and textile scraps) imported from the Netherlands. India also receives a substantial volume of HS 6310 textiles originating from the Netherlands via France. Notably, India enforces trade restrictions requiring textiles under HS 6309 (used textiles) to be imported only through the Kandla Special Economic Zone (KASEZ), with a mandate for at least 50% to be re-exported. Panipat in India is home to numerous spinning companies, ranging from large to small. These companies specialize in cleaning and sorting textile waste to produce recycled yarn, which is then supplied to weaving and manufacturing units in Panipat and beyond. Most of India’s used textiles re-exports went to African countries.

Ghana and Kenya were significant recipients of used textiles from the Netherlands, yet their export volumes for HS6309 (used textiles) and HS 6310 (sorted and unsorted used rags and textile scraps) were comparatively low. The high import-to-export ratios underscore these two countries’ role as the reuse and disposal destinations of used textiles from the Netherlands.

Characteristics of the used textile exports

The report highlights divergent perspectives on the quality and rewearability of textile exports to African countries. Dutch collectors and sorters assert that all exports from the Netherlands to Africa consist of good-quality rewearables. They distance themselves from the problem of textile waste exported to Africa, attributing it to the unregulated practices of certain parts of the used textiles trade that involve illegal contractors and exports.

According to the study, textiles deemed suitable for currently viable closed-loop recycling technologies include those made of pure cotton, pure wool, pure acrylic, and cotton-rich and wool-rich blends exceeding 80%. However, the study noted a concerning decline in the proportion of collected textiles suitable for rewear, coupled with a rise in textiles containing synthetic fibers. Most interviewees explicitly attribute the degradation in the quality of used textiles over time to the influence of “ultra-fast fashion.”

Environmental and social impacts of used textile exports

Interviews revealed a significant variation in the perceived environmental impacts of the used clothing trade. For example, participants from import-export hubs like Pakistan and recycling hubs like India emphasized minimal environmental harm, focusing on the positive contributions of used textile imports. In contrast, interviewees from reuse and disposal countries, such as Kenya and Ghana, discussed environmental harms and their localized impacts. Interviewees also expressed concerns that “certain sustainability solutions may be developed in such a way that generates additional problems further away” and benefit actors in Europe and the West only.

The study also found that 99% of fashion brands “do not disclose a commitment to ultimately reduce the number of new items they produce,” and only 12% of fashion companies have even disclosed the quantity of products produced annually in 2023, down from 15% in 2022.

The involved parties acknowledge the considerable difficulty in completely disassociating any participant in the reverse supply chain from the adverse impacts of textile exports. Despite efforts, achieving complete transparency beyond EU borders is deemed nearly impossible, as highlighted by one used textiles collector.

Job creation

The used textiles value chain unambiguously generates a huge amount of employment, particularly for women, in the sorting, recycling, selling, cleaning, repairing, re-styling, and distributing processes.

A 2023 International Labour Organization (ILO) study showed that new recycling and reprocessing activities could create over 10 million jobs in Latin America and the Caribbean and around 0.5 million jobs in Europe.

However, concerns related to job quality and social risks were also raised in interviews, particularly concerning reuse and disposal countries. Even where waste management systems for used textiles are formalized and managed, they often rely on the “labors of informal actors” for various functions such as distribution, resale, and disposal processes. Gender-based disadvantage may also be a concern. For example, the study found that whereas recycling and sorting enterprises are overwhelmingly owned and operated by men, women perform the majority of lower-wage, non-technical, and manual labor-intensive tasks.

Regulations

The Dutch government’s Circular Textiles Policy Programme for 2020–2025outlines a commitment to enhance the proportion of recycled materials in textiles and apparel products available in the Dutch market, including achieving a 10% reuse and 30% recycling rate of sold textiles and apparel by 2025.

The DutchExtended Producer Responsibility (EPR) for textileswas officially implemented on July 1, 2023. Onwards, producers are responsible for “recycling and reusing of textiles…including an appropriate collection system, recycling and reusing of clothing and household textiles and financing this entire system.”

The policy landscape for managing and exporting used textiles in Europe has evolved to align with environmental goals, with key milestones such as the EU Strategy for Sustainable and Circular Textiles in March 2022. While this strategy aims to create a greener and more resilient textiles sector, the report suggests a need for a bolder vision and more international orientation, emphasizing responsibility for socioenvironmental impacts beyond Europe.

The EU Waste Framework Directive (WFD) is another crucial instrument to tackle the environmental challenges of high textile consumption. The WFD regulates all aspects of textile waste management, including the specific obligations to ensure separate collection, treatment, and reporting requirements. The directive calls for all EU Member States to establish separate collection systems for used textiles by the beginning of 2025.

Supplementary video: Used clothing from Europe: Trash or treasure for Africa?

With consumers’ growing awareness of the environmental impacts of clothing production and consumption, retailers in Europe (EU) have expressed a heightened interest in selling clothing using recycled textile materials (referred to as “recycled clothing” in this study). For example, fast fashion giants like H&M and Zara and luxury brands such as Hugo Boss have started carrying recycled clothing, aiming to integrate circularity into their product designs and business models.

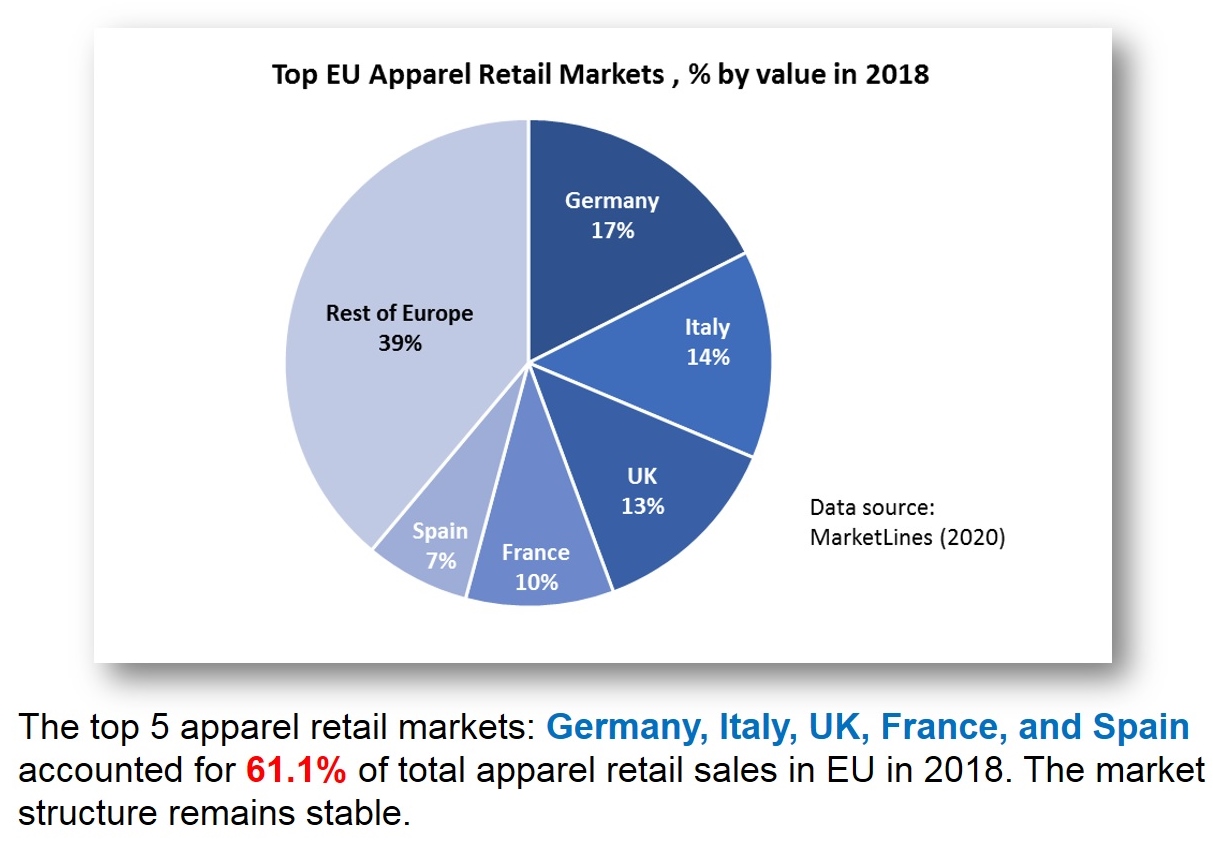

In the study, we examined retailers’ sourcing strategies for clothing made from recycled textile materials in five European countries, including the United Kingdom (UK), Italy, France, Germany, and Spain. These five countries represent the EU’s largest clothing retail markets, consistently accounting for over 60% of the region’s total apparel sales.

Through an industry source using web crawling techniques and manual verification, 5,000 Stock Keeping Units (SKUs) of clothing items made from recycled textile materials were randomly selected and analyzed. These items were sold by retailers in the UK, Germany, Italy, France, and Spain between January 2021 and May 2023.

The results show that Firist, EU retailers sourced clothing using recycled textile materials from diverse sources, including over 40 developing and developed countries across Asia, America, Europe, and Africa. Second, other than assortment diversity (i.e., the number of color or sizing options for a clothing item), no statistical evidence shows that developing countries had advantages over developed ones regarding product sophistication, replenishment frequency, and pricing for recycled clothing in the five EU markets. Third, a supplying country’s geographic location statistically affects the type of recycled clothing EU retailers import. For example, retailers in the five EU countries typically adopt the following sourcing portfolio by region:

Asia: relatively sophisticated clothing items (e.g., dresses and outerwear) targeting the mass and value market.

America (North, South, and Central): relatively simple clothing categories (e.g., T-shirts and socks) targeting the mass and value market.

Europe: sophisticated clothing categories primarily for the luxury or premium market

Africa: relatively simple clothing categories targeting the premium market

The findings offered new insights into the business aspects of recycled clothing, particularly regarding its intricate supply chains and leading suppliers. The study’s results have several additional important implications.

First, while existing studies often suggest “local for local” textile recycling, the study’s findings revealed promising global sourcing opportunities for clothing using recycled textile materials. Particularly, leveraging a diverse sourcing base would allow EU retailers to take advantage of each supplying country’s unique production strength regarding product categories and assortment features and more efficiently balance various sourcing factors ranging from costs and flexibility to speed to market. Meanwhile, the study’s findings indicate that many countries worldwide have begun producing and exporting clothing using recycled textile materials, and the sourcing options and capacities will hopefully continue to grow.

Second, according to the study’s findings, unlike the patterns of making regular garments using virgin fiber, low-wage developing countries demonstrated no noticeable competitive edges over developed economies regarding producing and exporting clothing using recycled textile materials. Instead, developed economies, including many high-wage Western EU countries, emerged as top suppliers and leading sourcing destinations for recycled clothing. Thus, expanding clothing production using recycled textile materials presents an exciting economic opportunity with a promising future in developed countries, where many have plans to revitalize the domestic manufacturing sector and establish a sustainable circular economy.

Third, building on the previous point, the sustained commitment of fashion brands and retailers to carry more clothing made from recycled textile materials in their product assortment could hold significant implications for the future landscape of global apparel trade and sourcing patterns. For example, whereas apparel products are predominantly exported from developing to developed countries today, more trade flows could occur between developed economies in the future, attributed to their increasing production capacity and growing demand for clothing using recycled textile materials. Similarly, major apparel exporters in Asia, such as China and Bangladesh, might assume a less dominant role as a sourcing base for recycled clothing due to their insufficient infrastructure for efficiently sorting used clothing and generating high-quality recycled textile materials.

By Leah Marsh and Sheng Lu

Discussion questions proposed by FASH455:

#1 How might EU fashion companies’ sourcing strategies change as they increase carrying clothing made from recycled textile materials?

#2 Could the US emerge as a leading sourcing destination for clothing made from recycled textile materials? What are the potential advantages and disadvantages?

#3 Is expanding clothing made from recycled textile materials the right approach to achieve fashion sustainability? What is your thought?

Impacts of the Red Sea Attacks on the Supply Chain

Impacts of the Red Sea attacks on the global textile and apparel trade: A summary from the media

US retailers/importers:1) “40 percent of shipments from Asia go to the U.S. through the Panama Canal” and “with access to the Suez Canal also now limited, vessels carrying goods to the East Coast of America will now take longer to deliver their shipments.” 2) “Companies that depend on inventory supplies from Asia will be impacted…These include things like sneakers, apparel and consumer electronics from countries such as China. Companies may be forced to pay more to get their inventory delivered, the costs of which could be passed on to consumers pushing up prices.”

EU retailers/importers: 1) “the rates for shipping goods from Asia to northern Europe have “more than doubled” since the start of December 2023.” 2) some EU fashion companies say “the crisis has delayed stock deliveries “by three to four weeks” and increased delivery costs by 20%” 3) some fashion retailers are “keen to avoid flying stock from Asia to Europe due to the significant amounts of carbon emissions caused by air freight.” 4) many EU fashion brands and manufacturers “expressed concern that they will have to shoulder the financial burden of the delays.”

China producers/exporters: 1) “Customers involved in China-European trade now face additional costs and a delay of seven to 10 days in such cases” 2) “Some Chinese exporters are shifting to China-Europe Railway Express services to ensure timely delivery of their goods and avoid staggering operational costs if they navigate around the Cape of Good Hope. However, “Some rail freight platform companies have proposed price increases for their railway services to Europe.”

India producers/exporters: 1) “Exports to the US west coast are intact, shipments to Europe, North Africa, and the Middle East have been affected. India exports goods worth $110 billion to the three regions.” 2) “The cost of freight and insurance has risen due to ships being compelled to avoid the region and take a longer route around the Cape of Good Hope. 3) Shipments are being held back by exporters, because they are feeling a pinch of additional freight cost. “Containers could face delays of 12-14 days in their turnaround time, although there is no shortage of containers.”

Bangladesh producers/exporters: 1) “over 70 percent of Bangladesh’s export-laden containers, which are destined for the EU, US East Coast and Canada, cross the Red Sea.” “Meanwhile, “8 to 10 percent of the country’s imports come through the route.” 2)Bangladeshi exporters and importers are having to pay higher freight charges to the US and Europe.” According to the Bangladesh Textile Mills Association (BTMA), the freight charge has already increased by $700 to $800 per container in case of import-laden vessels. The Bangladesh Garment Manufacturers and Exporters Association (BGMEA) expects Bangladesh’s domestic garment suppliers “will have to ultimately bear the freight cost.”

Pakistan producers and exporters: Textile and apparel shipments are facing stress. On the one hand, Pakistani textile and apparel producers are “highly reliant on timely raw materials and machinery imports. Any disturbances in shipping schedules could lead to production slowdowns and increased costs for manufacturers.” Meanwhile, “There have been “delays in fulfilling orders due to higher lead times and freight charges.” “Exporters have been incurring losses as they were honoring orders when they had assumed freight charges of $750.” However, as of mid-January, “shipping companies have jacked up freight charges to around $1,800, a massive 140% hike.”

(Note: This blog post will be updated as new information becomes available. Industry professionals are welcome to leave comments and share insights.)

According to Primark, it does not own any factories but sources all apparel products from contracted factories. Any contracted factory that manufactures products for Primark must meet internationally recognized standards before receiving the first sourcing order.

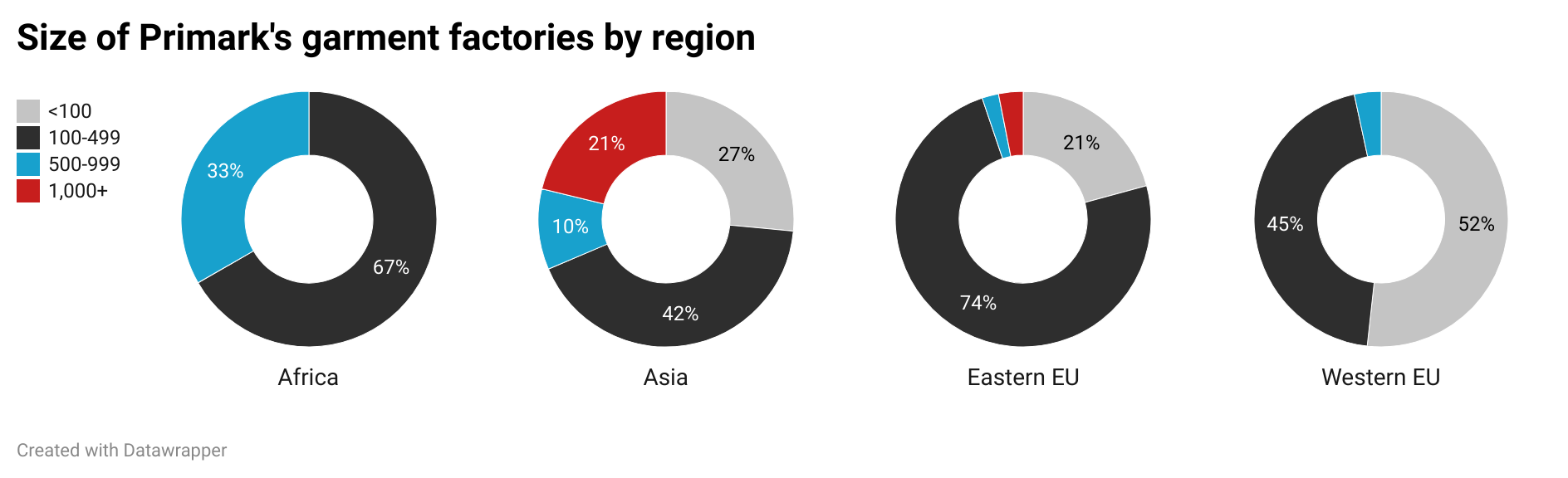

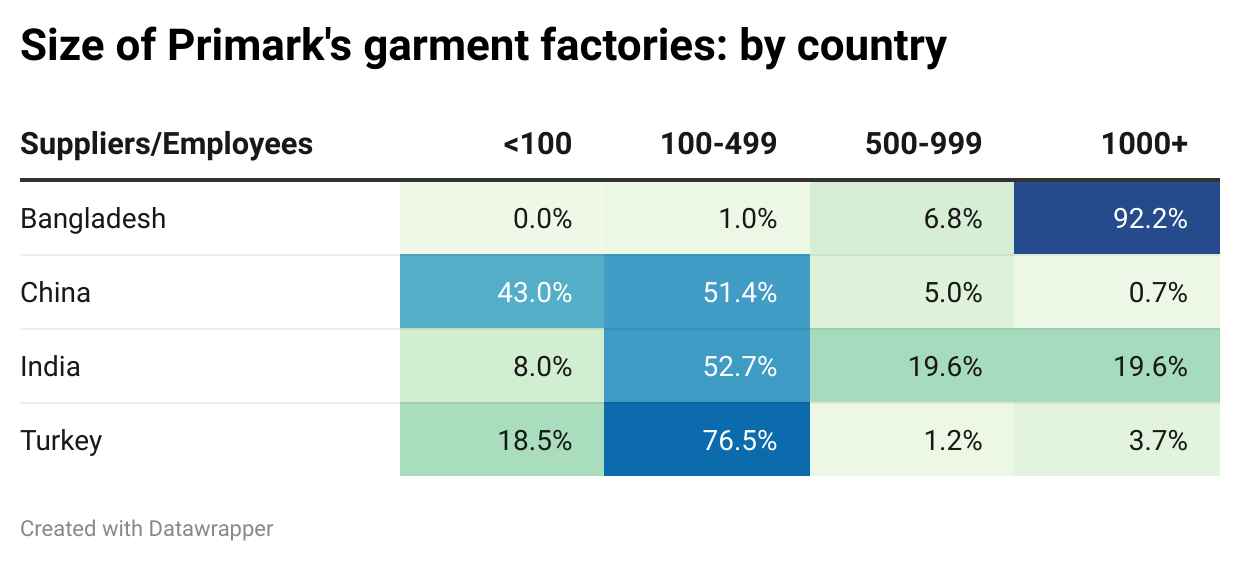

As of October 2022, Primark sourced from 883 contracted factories in 26 countries (note: it was a slight decline from 928 contracted factories in 28 countries as of May 2021). Of these factories, 85.5 percent were Asia-based because of the region’s massive production capacity and a balanced offer of various sourcing factors, from cost, speed to market, and flexibility to compliance risks.

Like many other EU-based fashion companies, near-shoring from within the EU was another critical feature of Primark’s sourcing strategies. About 14 percent of Primark’s contracted garment factories were EU-based (including Turkey).

Measured by the number of workers, Primark’s Asian factories were larger than their counterparts in other parts of the world. For example, while Primark’s factories in Pakistan and Bangladesh typically have more than 2,500+ workers, its factories in Western EU countries like the UK, Germany, Italy, and France, on average, only have 64-200 workers. This pattern suggests that Primark mainly uses Asian factories to fulfill volume sourcing orders, and its EU factories mainly produce replenishment or more time-sensitive fashionable items.

Meanwhile, similar to the case of other retailers like PVH, Primark’s contracted garment factories in China were smaller than their peers in the rest of Asia. For instance, while over 90% of Primark’s garment factories in Bangladesh employ more than 1,000 workers, around 43% of their contracted factories in China have fewer than 100 workers. This pattern suggests Primark could use China as an apparel sourcing base primarily for orders requiring greater flexibility and agility and those involving a wider variety of products but in smaller quantities.

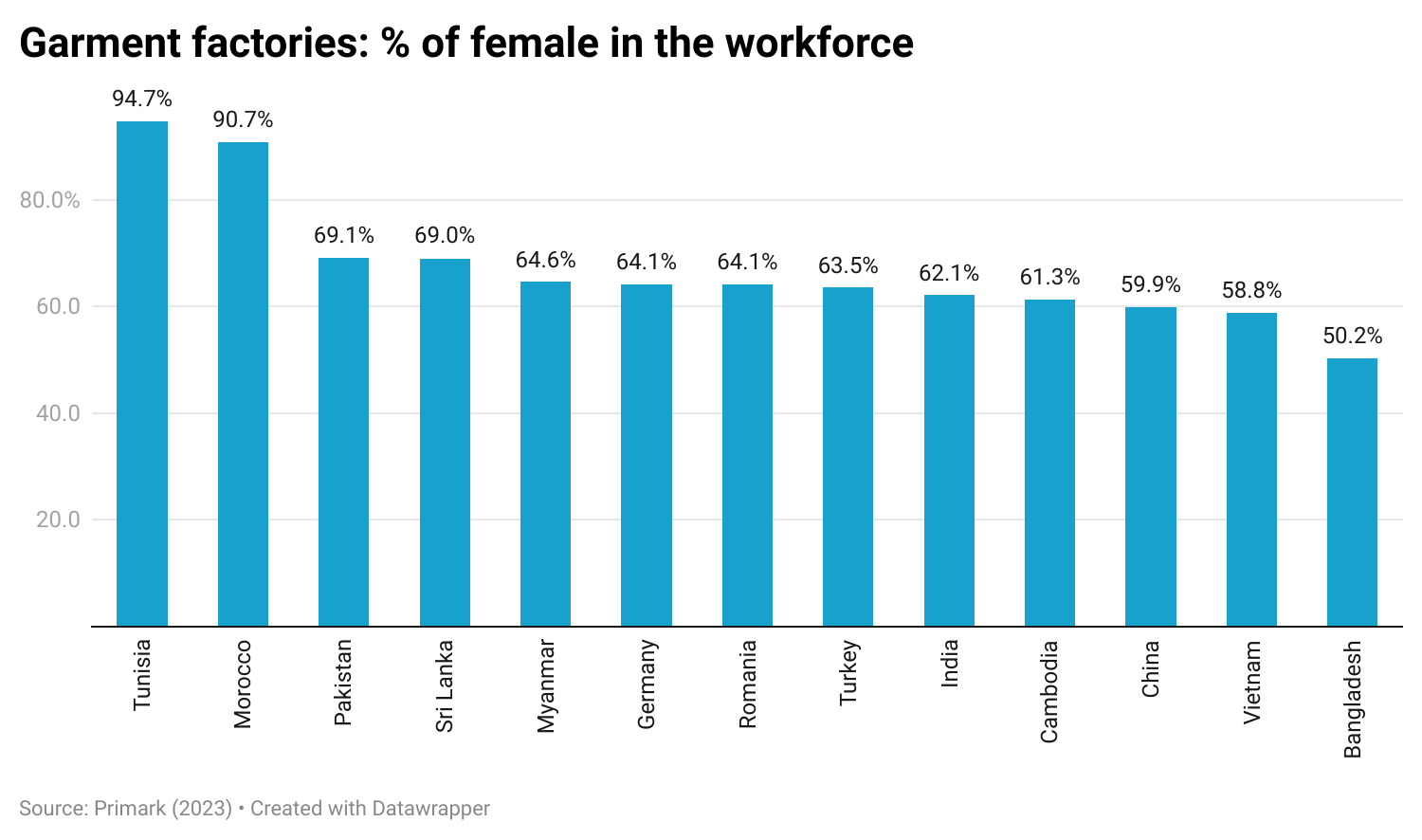

Further, reflecting the unique role of the garment industry in creating economic opportunities for women, females account for more than half of the workforce in most garment factories that make apparel for Primark. The percentage was exceptionally high in developing countries like Tunisia (94%), Morocco (91%), Pakistan (69%), Sri Lanka (69%), Myanmar (64%), India (62%), and Vietnam (59%).

According to Primark (as of September 2023), its Ethical Trade and Environmental Sustainability team comprises over 120 specialists based in key sourcing countries. The team conducts around 3,000 supplier audits a year to monitor compliance (i.e., fair pay, safety, and healthy working conditions.) Additionally, Primark says its factories were in line with the company’s environmental code of conduct, and the company “donated any unsold merchandise to the Newlife Foundation in Europe and KIDS/Fashion Delivers in the US.

by Sheng Lu

Discussion questions:

What are the unique aspects of Primark’s apparel sourcing strategies? What role does sourcing play in supporting Primark’s business success? Any questions or suggestions for Primark regarding its sourcing practices?

This article comprehensively reviewed the world textiles and clothing trade patterns in 2022 based on the newly released World Trade Organization Statistical Review 2023 and data from the United Nations (UNComtrade). Affected by the slowing world economy and fashion companies’ evolving sourcing strategies in response to the rising geopolitical tensions, mainly linked to China, the world’s textiles and clothing trade in 2022 displayed several notable patterns different from the past.

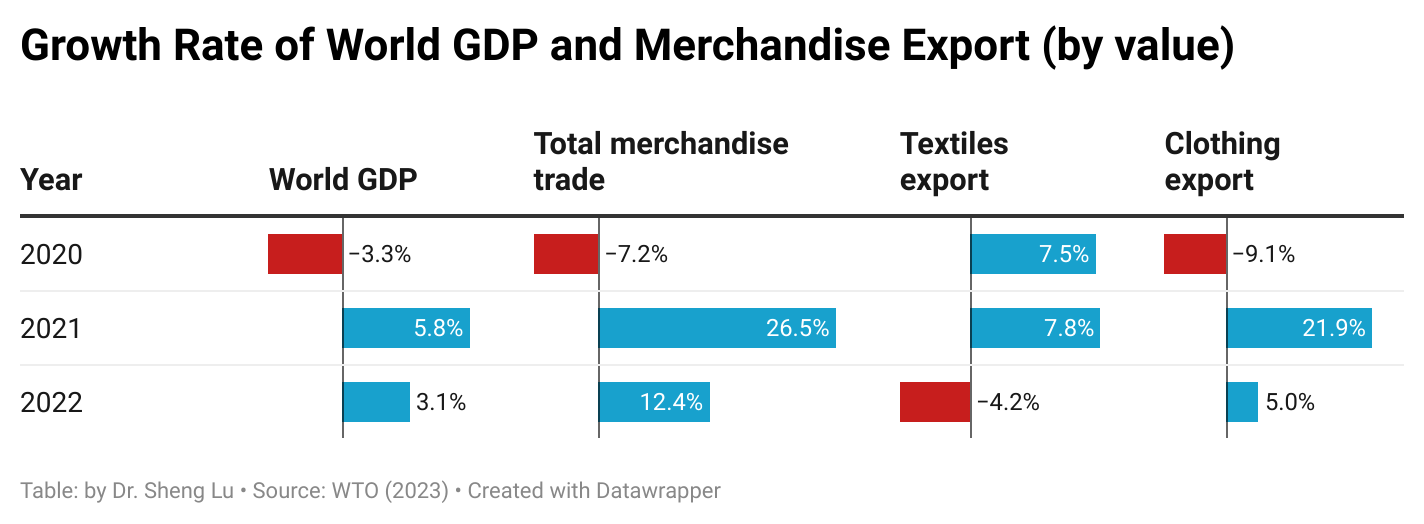

Pattern #1: The expansion of world clothing exports witnessed a notable deceleration in 2022, primarily attributed to the economic downturn. Meanwhile, the world’s textile exports decreased from the previous year, affected by the reduced demand for textile raw materials used to produce personal protective equipment (PPE) as the pandemic waned.

The world’sclothing exports totaled $576 billion in 2022, up 5 percent year over year, much slower than the remarkable 20 percent growth in 2021. The slowed economic growth plus the unprecedented high inflation in major apparel import markets, particularly the United States and Western European countries, adversely affected consumers’ available budget for discretionary expenditures, including clothing purchases.

The world’s textile exports fell by 4.2 percent in 2022, totaling $339 billion, lagging behind most industrial sectors. Such a pattern was understandable as the demand for PPE and related textile raw materials substantially decreased with the pandemic nearing its end.

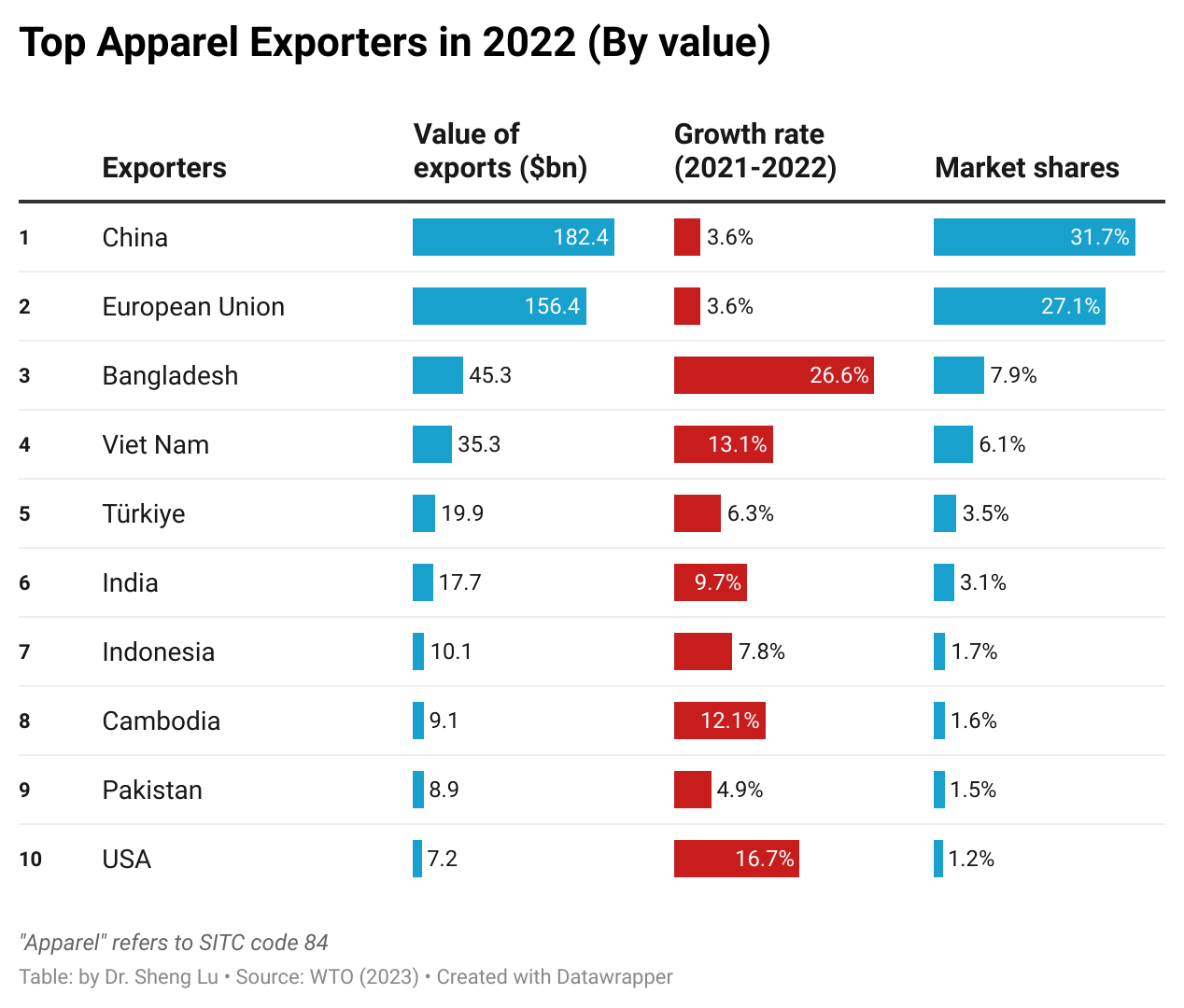

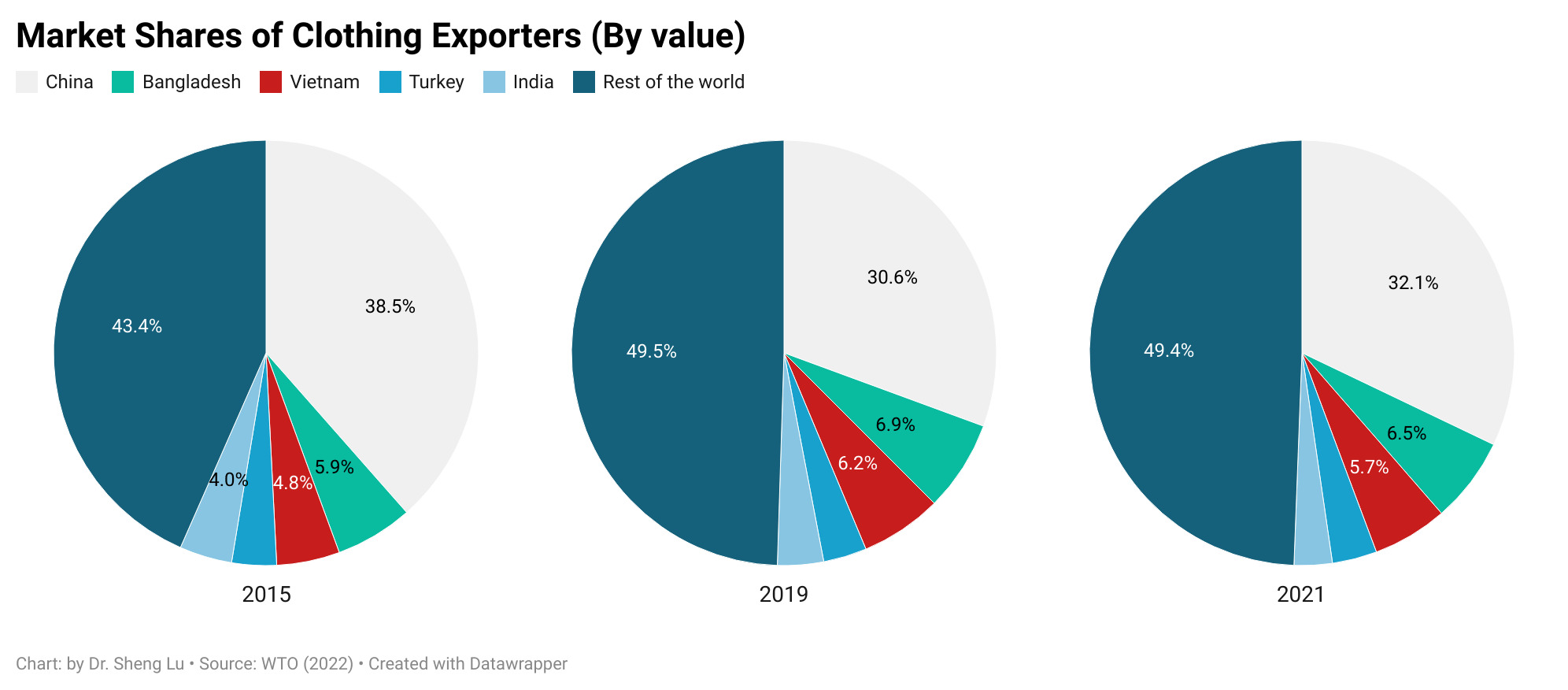

Pattern #2: China continued to lose market share in clothing exports, which benefited other leading apparel exporters in Asia. Notably, for the first time, Bangladesh surpassed Vietnam and ranked as the world’s second-largest apparel exporter in 2022.

In value, China remained the world’s largest apparel exporter in 2022. However, China’s clothing exports experienced a growth of 3.6 percent, below the global average of 5.0 percent, positioning China at the bottom of the top ten exporters.

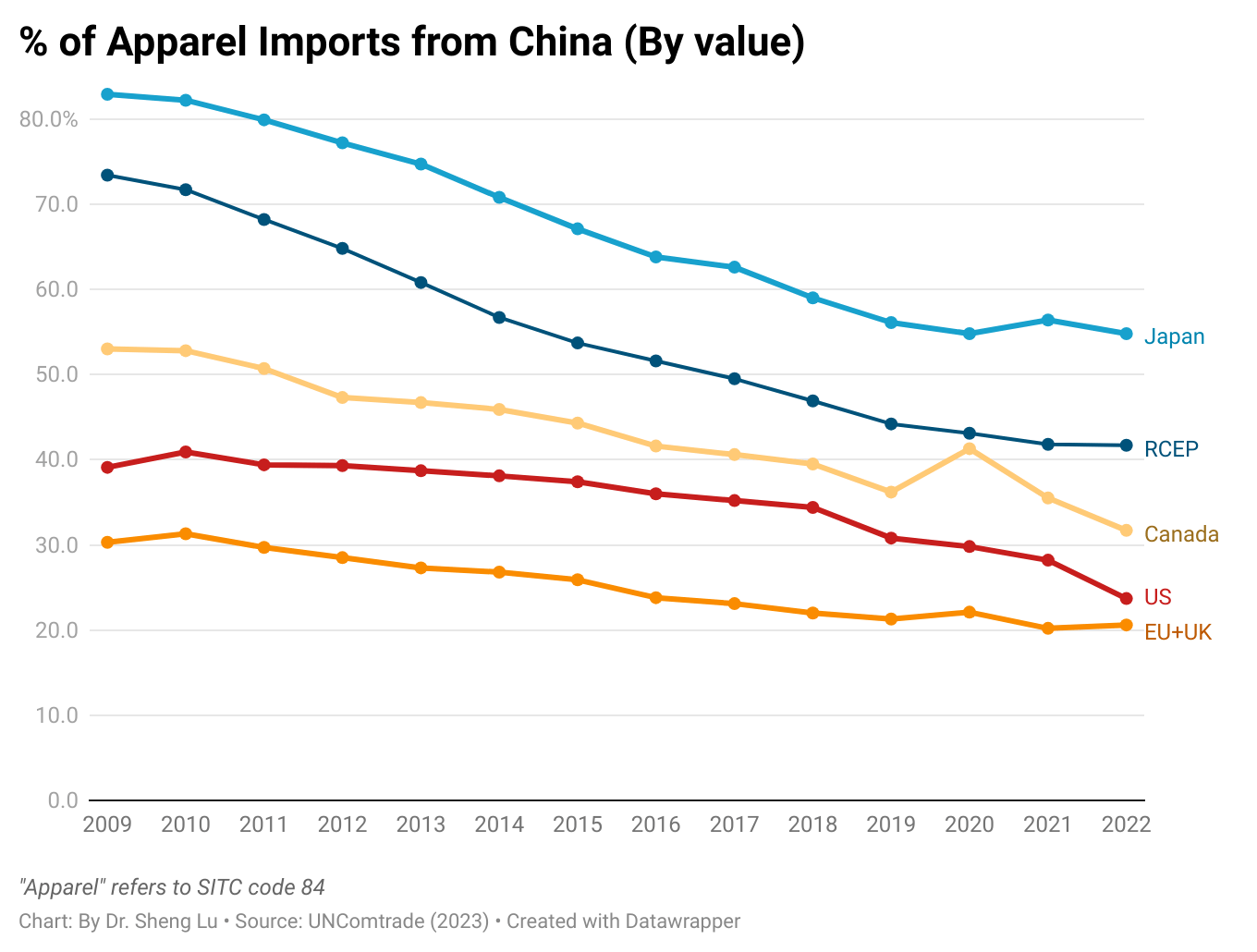

China’s global market share in clothing exports dropped to 31.7 percent in 2022, marking its lowest point since the pandemic and a significant decrease from the approximate 38 percent recorded from 2015 to 2018. In fact, China lost market share in almost all major clothing import markets, including the US, the EU, Canada, and Japan. The concerns about the risks of forced labor linked to sourcing from China and the deteriorating US-China relations were among the primary factors driving fashion companies’ eagerness to reduce their ‘China exposure” further.

China has been diversifying its clothing exports beyond the traditional Western markets in response to the challenging business environment. For example, from 2021 to 2022, Asian countries, especially members of the Regional Comprehensive Economic Partnership (RCEP), became relatively more important clothing export markets for China. Nevertheless, since RCEP members primarily consist of developing economies with ambitions to enhance their own clothing production, the long-term growth prospects for their import demand of ‘Made in China’ clothing remain uncertain.

Bangladesh achieved a new record high in its market share of world clothing exports, reaching 7.9 percent in 2022, which exceeded Vietnam’s 6.1 percent. Many fashion companies regard Bangladesh as a promising clothing-sourcing destination with growth potential because of its capability to make cotton garments as China’s alternatives, competitive price, and reduced social compliance risks.

Fashion companies’ efforts to “de-risking from China” also resulted in the robust growth of clothing exports from other large-scale Asian clothing producers in 2022, including Vietnam (up 13 percent), Cambodia (up 12 percent), and India (up 10 percent). In other words, despite the concerns about China, fashion companies still treat Asia as their primary sourcing destination.

Pattern #3: Developed countries stay critical textile exporters, and middle-income developing countries gradually build new textile production and export capability.

The European Union members and the United States stayed critical textile exporters, accounting for 25.1 percent of the world’s textile exports in 2022, up from 24.5 percent in 2021 and 23.2 percent in 2020. Thanks to the increasing demand from apparel producers in the Western Hemisphere, U.S. textile exports increased by 5 percent in 2022, the highest among the world’s top ten.

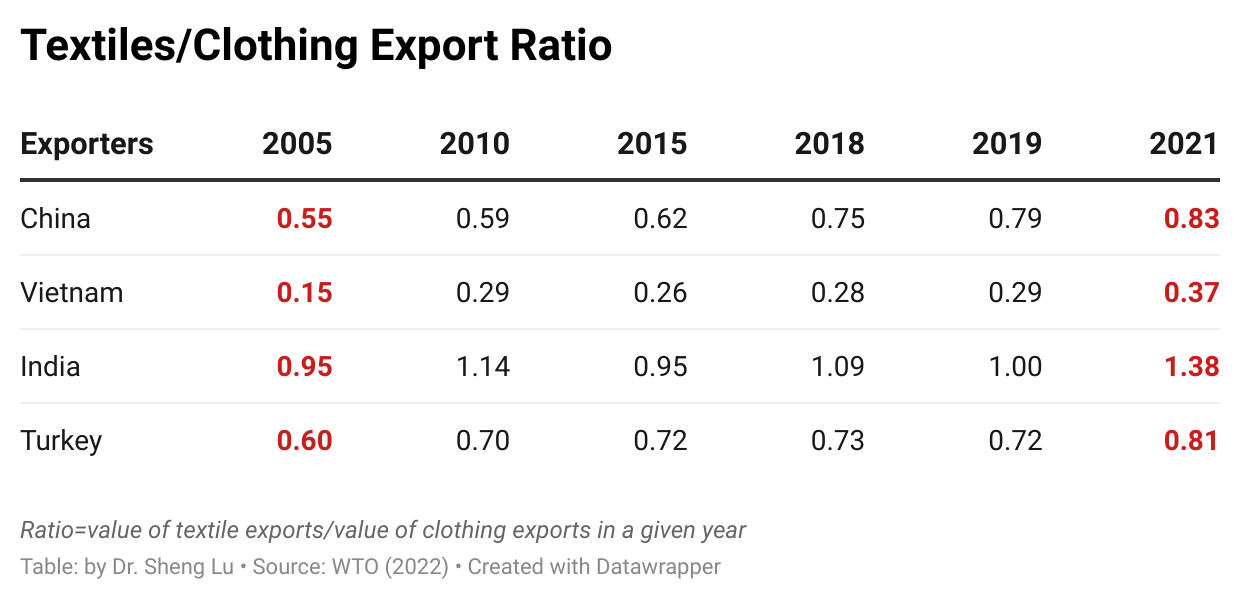

As a persistent long-term trend, middle-income developing countries have consistently been strengthening their textile production and export capability. For example, China, Vietnam, Turkey, and India’s market shares in the world’s textile exports have steadily risen. They collectively accounted for 56.8 percent of the world’s clothing exports in 2022, a notable increase from only 40 percent in 2010. Also, over time, these middle-income developing countries have achieved a more balanced textiles-to-clothing export ratio.

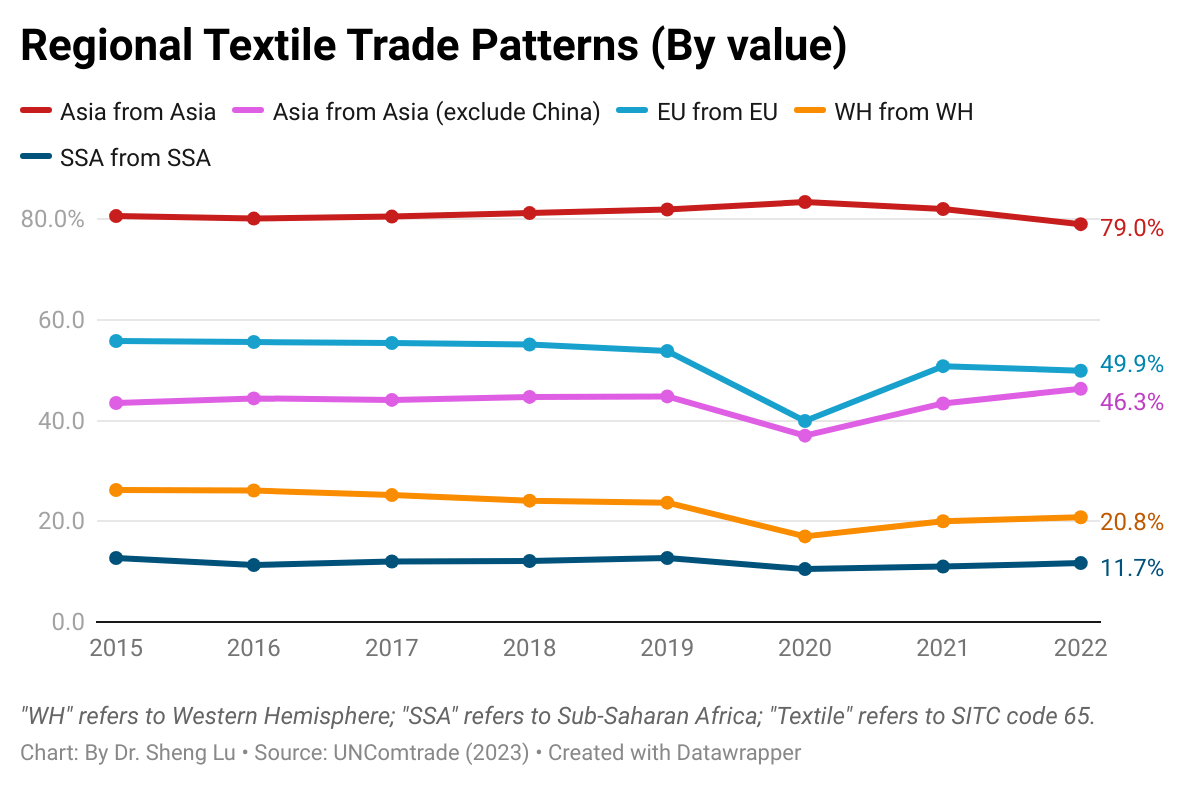

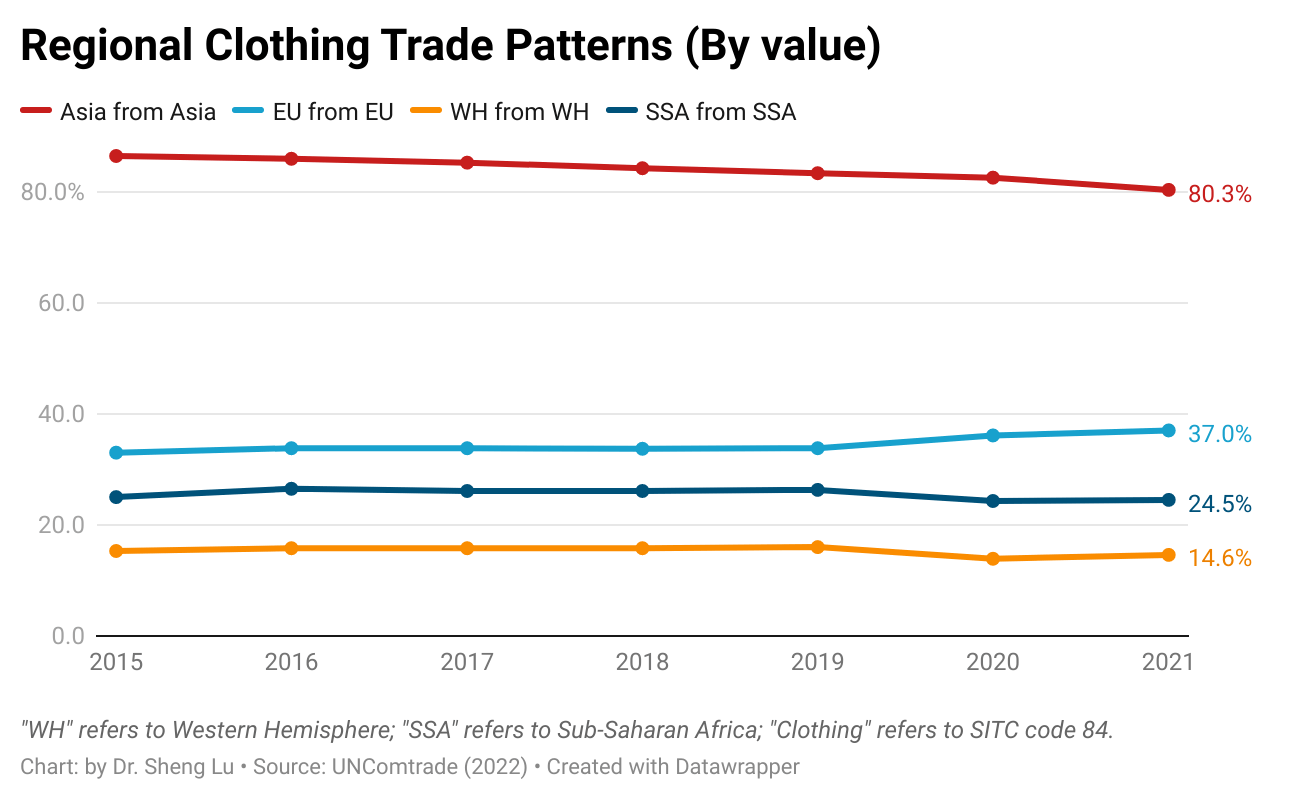

Pattern #4: Regional textile and apparel trade patterns strengthened further with the growing popularity of near-shoring, particularly in the Western Hemisphere. However, an early indication has emerged that Asian countries are diversifying their sources of textile raw materials away from China to mitigate growing risks.

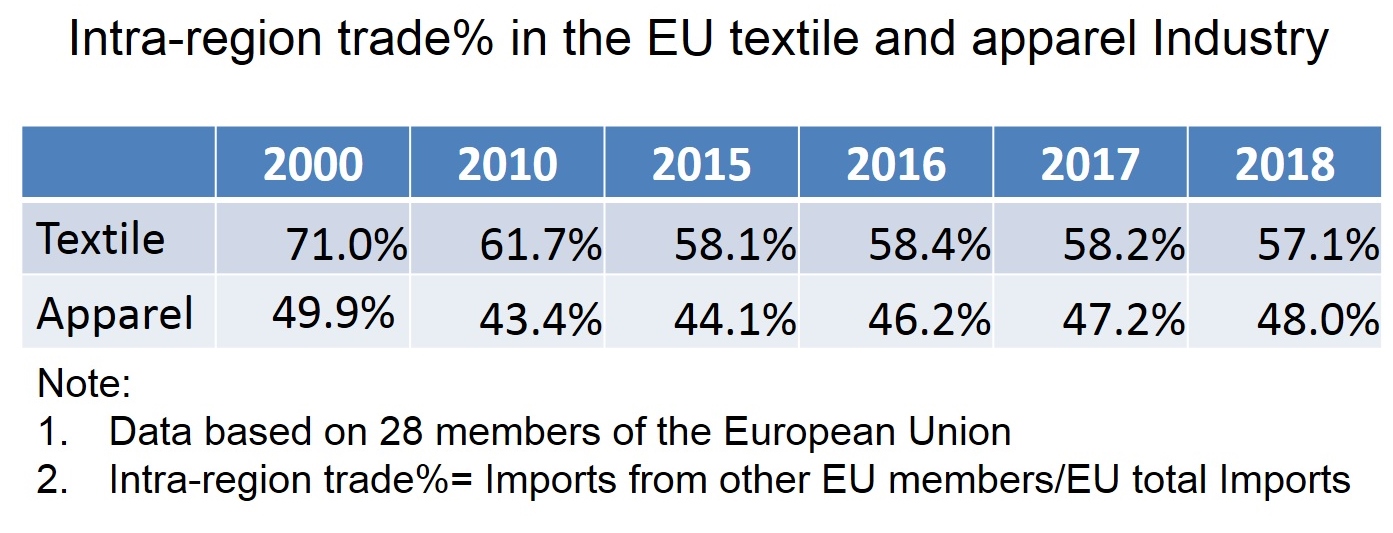

The regional textile and apparel supply chains were in good shape in Asia and Europe. For example, nearly 80 percent of Asian countries’ textile input and apparel imports came from within the region in 2022. Likewise, approximately half of EU countries’ textile imports were intra-region trade in 2022, and one-third were for apparel.

The Western Hemisphere (WH) textile and apparel supply chain became more integrated in 2022 thanks to the booming near-shoring trends. For example, 20.8 percent of WH countries’ textile imports came from within the region in 2022, up from 20.1 percent in the previous year. Likewise, about 15.1 percent of WH countries’ apparel imports came from within the region in 2022, higher than 14.7 percent in 2021 and 13.9 percent in 2022.

Compared with Asia and the EU, SSA clothing producers used much fewer locally-made textiles (i.e., stagnant at around 11% from 2011 to 2022), reflecting the region’s lack of textile manufacturing capability. A more comprehensive examination of strategies for bolstering the textile manufacturing sector in Sub-Saharan Africa, particularly in light of the recently enacted African Continental Free Trade Area (AfCFTA) agreement, might be warranted.

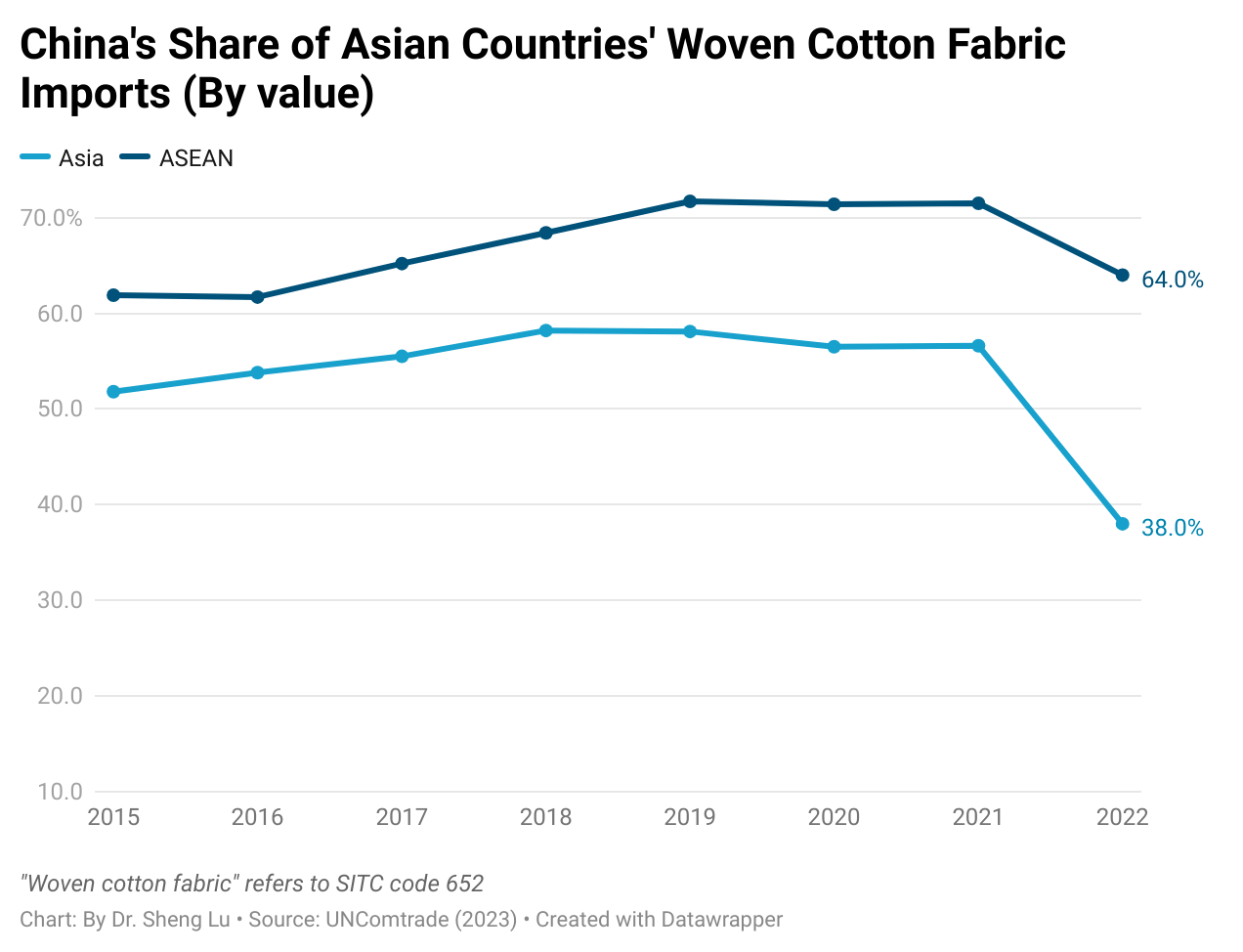

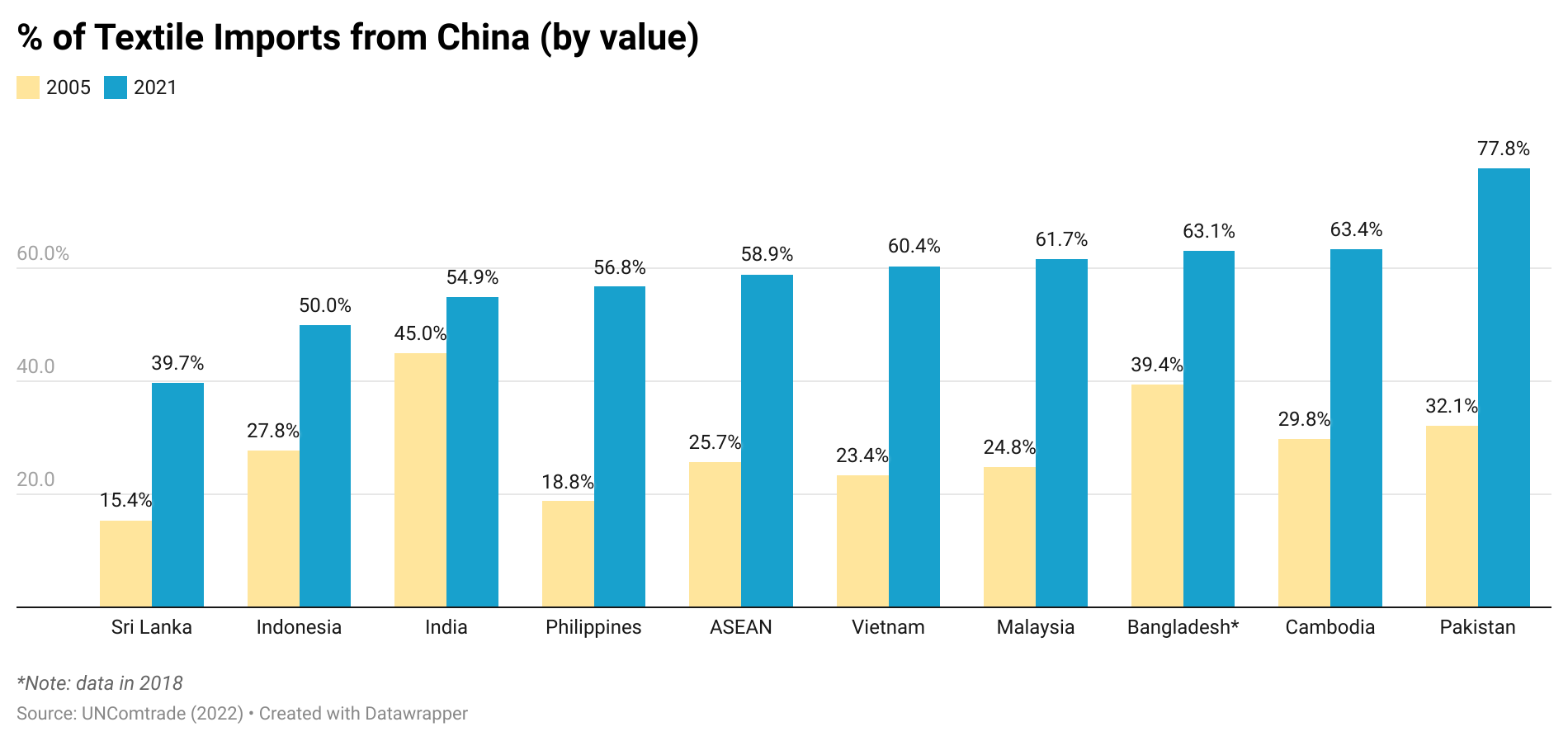

Additionally, data suggests that Asian countries began diversifying their textile imports away from China to mitigate supply chain risks. For example, with the official implementation of anti-forced labor legislation in the US and other primary apparel import markets directly targeting cotton made in China’s Xinjiang region, Asian countries significantly reduced their cotton fabric imports (SITC code 652) from China in 2022. Instead, Asian countries other than China accounted for 46.3 percent of the region’s textile supply in 2022, up from around 42-43 percent between 2019 and 2021.

It is critical to watch how willing, to what extent, and how quickly Asian countries can effectively reduce their dependency on textile supplies from China. The result is also an important reminder that Western fashion companies’ de-risking from China could exert significant and broad impacts across the entire supply chain beyond finished goods.

On July 6, 2023, the European Commission proposed a new rule, which aims to reduce textile waste and bolster used textile markets across the European Union (EU). EU says the new initiative will “accelerate the development of the separate collection, sorting, reuse and recycling sector for textiles in the EU, in line with the EU Strategy for Sustainable and Circular Textiles (released in March 2022).

What are your thoughts on the latest update on the new proposed rules?

The new EU rule goes far beyond existing regulations on sustainable textile and apparel production. For example:

While circular fashion is mostly voluntary efforts by companies, the new rule will impose a mandatory “eco-modulation fee” that is used to collect, sort, and recycle used textiles.

The proposal also aims to address “the issue of illegal exports of textile waste to countries ill-equipped to manage.” Notably, despite the controversies surrounding the negative impacts of the used clothing trade on the developing world, few countries impose export restrictions on used clothing.

Additionally, there are few specific rules or regulations that explicitly mention stopping “fast fashion.” The new EU rule will be the first of its kind. It will be interesting to see how EU-based fast fashion giants like Zara and H&M respond to the proposal.

How do you think it will affect global apparel production, sourcing and trade?

While we are still waiting for the proposal’s details, the new rule is expected to substantially promote more use of recycled textile fibers in clothing with profound implications for the future of global apparel production, sourcing, and trade patterns.

For example, one of my recent studies found that given the many ways of recycling textile waste (e.g., mechanical and chemical), the supply chain of clothing made from recycled materials is versatile, potentially allowing countries of all kinds to get involved. Also, sourcing clothing made from recycled textile materials may offer many exciting business benefits beyond sustainability, such as reducing “China exposure,” expanding near-shoring, and diversifying the sourcing base.

What are the opportunities for the global apparel industry given these new proposed rules?

One opportunity is on the supply side–the new proposed rule could drive significant new investments in textile recycling, from exploring new textile recycling methods and improving the efficiency of collecting and sorting used clothing to expanding the production capacity in making garments using recycled textiles. In the future, clothing made from recycled textile materials may no longer be a “niche product” but a mainstream offering.

The new rule may also raise public awareness of the environmental and social aspects of clothing. For example, consumers may continue to push brands and retailers to make the apparel supply chain more transparent and inform them about the product’s detailed environmental, climate, and social impact.

What are the challenges for the global apparel industry given these new proposed rules?

It is unsure whether the “eco-modulation fee” will apply to EU-based textile and apparel producers only or will affect any producers that sell products in the EU markets. Given the long and fragmented nature of the textile and apparel supply chain, who will be subject to the “eco-modulation fee” needs clarification.

Fashion brands and retailers may also face higher sourcing costs and more limited product choices when sourcing clothing using recycled textiles. Like it or not, achieving “cost neutral” remains a critical principle for most fashion companies.

On the other hand, reflecting the unique supply chain of clothing made from recycled textiles, fashion companies must strengthen the monitoring efforts beyond the garment factories (i.e., tier 1 suppliers) to include tier 2 and 3 suppliers that handle the initial stages of recycled textile production.

Antonio de Sousa Maia, Legal Officer, European Commission;

Cecilia Nilsson-Bottka, Policy Officer, European Commission;

Enrico Venturini, Senior Researcher, NEXT TECHNOLOGY TECNOTESSILE;

Dirk Vantyghem, Director General, EURATEX;

Clara Mallart, Senior Specialist for Sustainability, MODACC.

Summary of remarks by Dirk Vantyghem (Director General of the European Apparel and Textile Confederation, EURATEX)

EU textile and apparel companies are still struggling with an adverse business environment, from high energy bills and hiking inflation to an economic slowdown. Many companies are in trouble. New “green measures” must be careful about their impacts on companies’ business operations.

Textile and apparel is one of the most globalized sectors in the EU. Government sustainability policy must consider the global dimension of their implications on EU companies, such as the impact on fair competition and investments across borders.

Consumers’ demand for sustainable textile and apparel products, especially their willingness to pay a premium, remains a question mark.

If new sustainability regulations are implemented, it is imperative for the government to assist companies going through the transition. Small and medium-sized enterprises (SMEs) form the backbones of the textile and apparel industry. These SMEs must survive as they provide critical products and services to large-scale fashion brands.

Many green legislations impacting the EU textile and apparel industry are coming (e.g., new labeling requirements on sustainable materials). Close collaboration and dialogue between the industry and legislators are essential.

Mango is a fashion company based in Barcelona, Spain that was founded in 1984 by brothers Isak Andic and Nahman Andic. The company has grown significantly since its inception and now has over 2,700 stores in 109 countries worldwide. Mango is known for its trendy and high-quality clothing, which is targeted toward young women.

One of the critical factors in Mango’s success has been its ability to stay current and relevant in the fast-paced fashion world. The company regularly collaborates with top designers and influencers to create unique and fashionable collections that appeal to its target audience. Mango also closely monitors emerging trends and adapts its collections accordingly.

Besides clothing, Mango also offers accessories, such as bags, shoes, jewelry, and a home collection. The company has a solid online presence, with an e-commerce website that allows customers to shop from anywhere in the world.

In December 2022, Mango announced the Sustainable 2030 strategy, which “aims to move towards the full traceability and transparency of its value chain, in order to continue with the process of auditing its suppliers and ensuring that appropriate working conditions are being fulfilled for the workers in the factories the company works with around the world.” As part of the strategy, Mango will “focus its efforts on moving towards a more sustainable collection, prioritizing materials with a lower environmental impact and incorporating circular design criteria, so that by 2030 these will predominate in the design of its products and all its fibers will be of sustainable origin or recycled.”

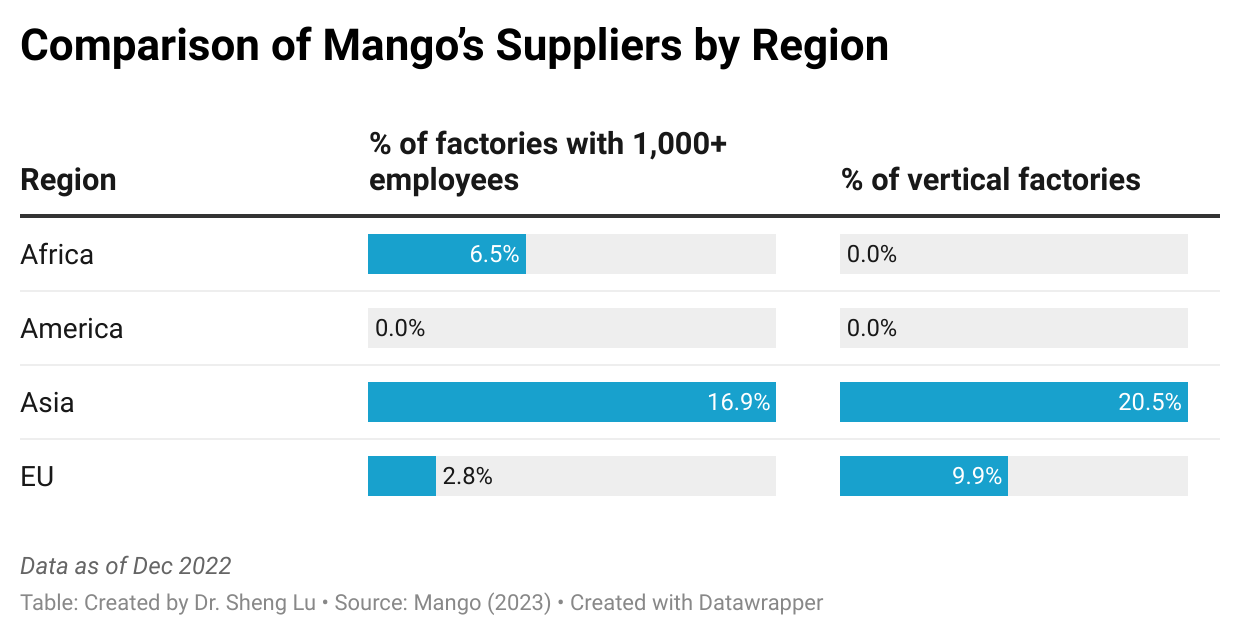

Mango’s Apparel Sourcing Strategies (as of December 2022)

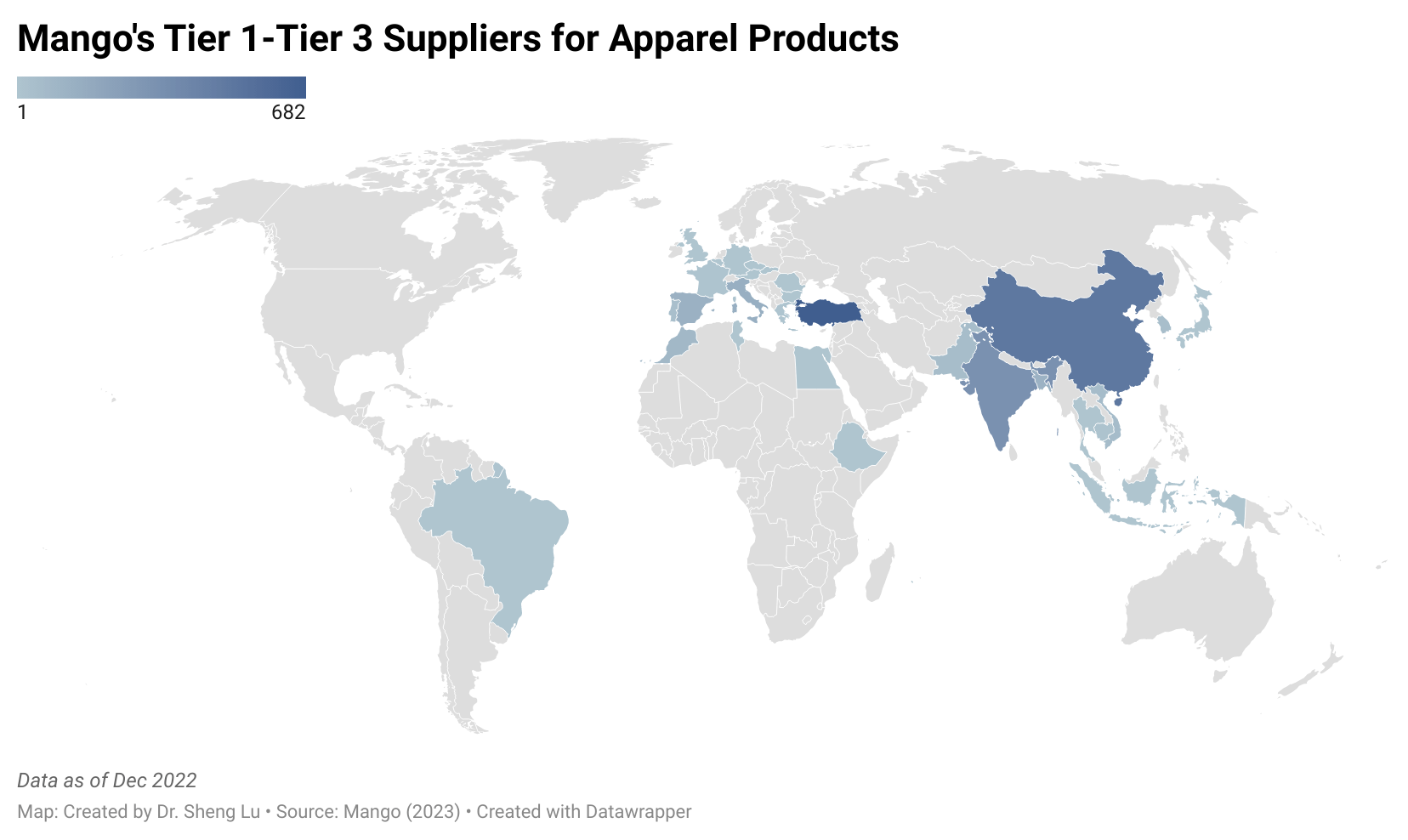

First, Mango adopted a sophisticated global sourcing network for its apparel products. Specifically, Mango’s apparel supply chain involves 1,878 Tier 1, Tier 2, and Tier 3 factories in 29 countries worldwide. About 31% of these factories produce garments (Tier 1), 19% supply fabrics (Tier 2), and 49% provide textile raw materials like yarns and accessories (Tier 3). Further, about 407 factories (or 21%) have vertical production capability (e.g., making both finished garments and textile inputs).

Second, like many EU fashion companies, near-shoring from the EU and Turkey is a critical feature of Mango’s apparel sourcing strategy. For example, about 44.8% of Mango’s Tier 1 garment suppliers were EU based (including Turkey), whereas Asia suppliers only accounted for 54%. Likewise, about 34% of Mango’s Tier 2 fabric suppliers and nearly half of its Tier 3 yarn and accessories suppliers were also EU based. The result reflects the EU’s intra-region textile and apparel trade patterns, supported by the region’s relatively complete textile and apparel supply chain. In comparison, US fashion companies typically source more than 80% of finished garments from Asia, and most of these garments also use Asia-based textile raw materials.

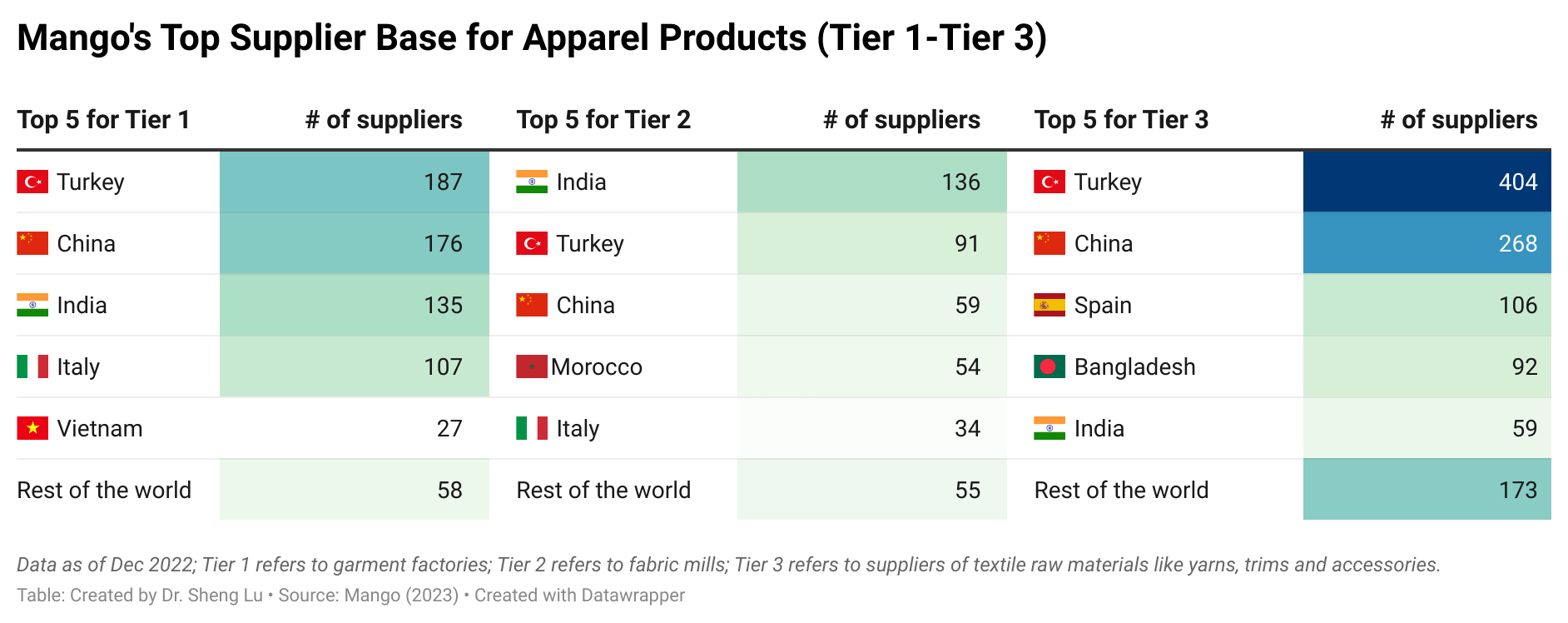

Third, measured by the number of suppliers, Mango’s top Tier 1 apparel production bases include Turkey (187 factories), China (176 factories), India (135 factories), and Italy (107 factories). Industry sources further indicated that between 2021 and 2022, Mango primarily sourced from Turkey and India for Tops (69% and 78%, respectively). Mango’s imports from China and Italy were more diverse in product categories (e.g., dresses, outwear, bottoms, and swimwear). On the other hand, Mango’s apparel imports from Italy were much higher priced ($107 retail price on average) than those from the other three countries ($38-41 retail price on average).

Fourth, the factory size and vertical production capabilities of Mango’s suppliers seem to vary by region. Notably, Mango’s Asia-based suppliers are more likely to be large-sized (with 1,000+ employees) and offer vertical production (e.g., making both finished garments and textile input). Mango’s Africa and America-based suppliers were relatively small-sized or lacked vertical integration.

This article provided a comprehensive review of the world textiles and clothing trade patterns in 2021 based on the newly released data from the World Trade Statistical Review 2022 and the United Nations (UNComtrade). Affected by the ongoing pandemic and companies’ evolving production and sourcing strategies in response to the shifting business environment, the world textiles and clothing trade patterns in 2021 included both continuities and new trends. Specifically:

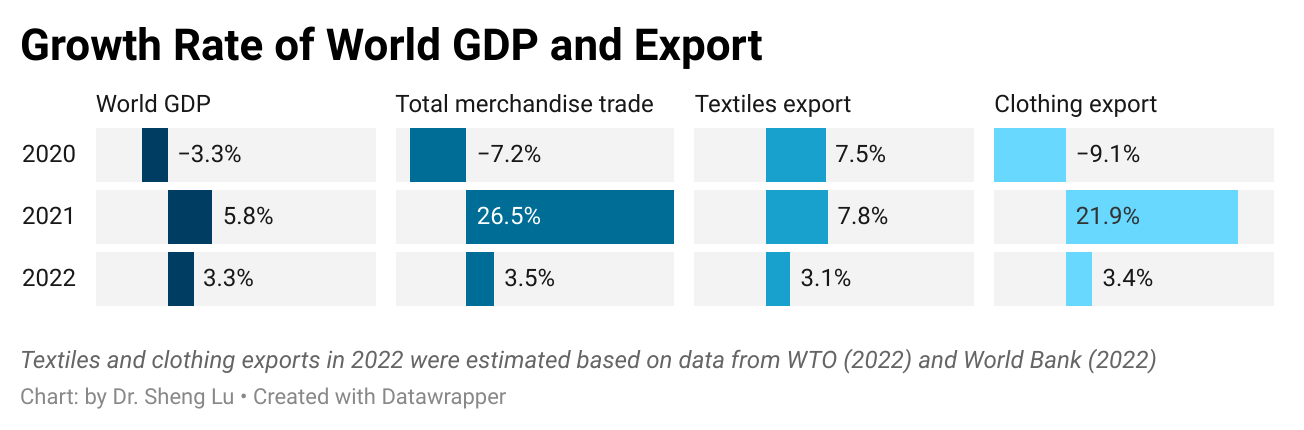

Pattern #1: As the world economy recovered from COVID, the world clothing export boomed in 2021, while the world textile exports grew much slower due to a high trade volume the year before. Specifically, thanks to consumers’ strong demand, world clothing exports in 2021 fully bounced back to the pre-COVID level and exceeded $548.8bn, a substantial increase of 21.9% from 2020. The apparel sector is not alone. With economic activities mostly resumed, the world merchandise trade in 2021 also jumped 26.5% from a year ago, the fastest growth in decades.

In comparison, the value of world textiles exports grew slower at 7.8% in 2021 (i.e., reached $354.2bn), lagging behind most sectors. However, such a pattern was understandable as the textile trade maintained a high level in 2020, driven by high demand for personal protective equipment (PPE) during the pandemic.

Nevertheless, the world textiles and clothing trade could face strong headwinds down the road due to a slowing world economy and consumers’ weakened demand. Notably, amid hiking inflation, high energy costs, and retrenchment of global supply chains, leading international economic agencies, from the World Bank to the International Monetary Fund (IMF), unanimously predict a slowing economy worldwide. Likewise, the World Trade Organization (WTO) forecasts that the growth of world merchandise trade will be cut to 3.5% in 2022 and down further to only 1% in 2023. As a result, the world textiles and clothing trade will likely struggle with stagnant growth or a modest decline over the next two years.

Pattern #2: COVID did NOT fundamentally shift the competitive landscape of textile exports but affected the export product structure. Meanwhile, some long-term structural changes in world textile exports continued in 2021.

Specifically, China, the European Union (EU), and India remained the world’s three largest textile exporters in 2021, a pattern that has stayed stable for over a decade. Together, these top three accounted for 68% of the world’s textile exports in 2021, similar to 66.9% before the pandemic (2018-2019). Other textile exporters that made it to the top ten list in 2021 were also the same as a year ago and before the pandemic (2018-2019).

Meanwhile, the growth rate of the top ten textile exporters varied significantly in 2021, ranging from -5.5% (China) to 47.8% (India). The demand shift from PPE to apparel-related yarns and fabrics was a critical contributing factor behind the phenomenon. For example, China’s PPE-related textile exports decreased by more than $33bn (or down 43%) in 2021. In contrast, the world knit fabric exports (SITC code 655) surged by more than 30% in 2021, led by India (up 74%) and Pakistan (up 72%). Nevertheless, as consumers’ lifestyles almost reached a “new normal,” we could expect the textile export product structure to stabilize soon.

On the other hand, as a trend already emerged before the pandemic, middle-income developing countries continued to play a more significant role in textile exports, whereas developed countries lost market shares. For example, the United States, Germany, and Italy led the world’s textile exports in the 2000s, accounting for more than 20% of the market shares. However, these three countries’ shares fell to 12.8% in 2019 and hit a new low of 11.3% in 2021. In comparison, middle-income developing countries like China, Vietnam, Turkey, and India have entered the development stage of expanding textile manufacturing. As a result, their market share in the world’s textile exports rose steadily. These countries also achieved a more balanced textiles/clothing export ratio over the years, meaning more textile raw materials like yarns and fabrics can be locally produced instead of relying on imports. For example, Vietnam, known for its competitive clothing products, achieved a new high of $11.5bn in textile exports in 2021 and ranked sixth globally. Vietnam’s textiles/clothing ratio also doubled from 0.15 in 2005 to 0.37 in 2021. It is not unlikely that Vietnam’s textile exports may surpass the United States over the next few years.

Pattern #3: Countries with large-scale production capacity stood out in world clothing exports in 2021. Meanwhile, clothing exporters compete to become China’s alternatives, but there seems to be no clear winner yet.