The session intends to facilitate constructive dialogue regarding the latest progress, challenges, and opportunities for achieving more sustainable and socially responsible apparel sourcing in the Post-COVID world. The session will offer a unique opportunity to hear directly from leading fashion brands and retailers regarding 1) fashion companies’ latest sourcing practices against the evolving business environment and their impacts on due diligence; 2) fashion companies’ new efforts and innovative projects to achieve more sustainable and socially responsible apparel sourcing; 3) opportunities and challenges to further improve sustainability and social responsibility in apparel sourcing in the post-COVID world. In addition, the session will be highly relevant and informative to all stakeholders in the fashion apparel business community, civil society, international organizations, academia, and policymakers.

The latest trade data shows that in the first four months of 2022, US apparel imports increased by 40.6% in value and 25.9% in quantity from a year ago. However, the seemingly robust import expansion is shadowed by the rising market uncertainties.

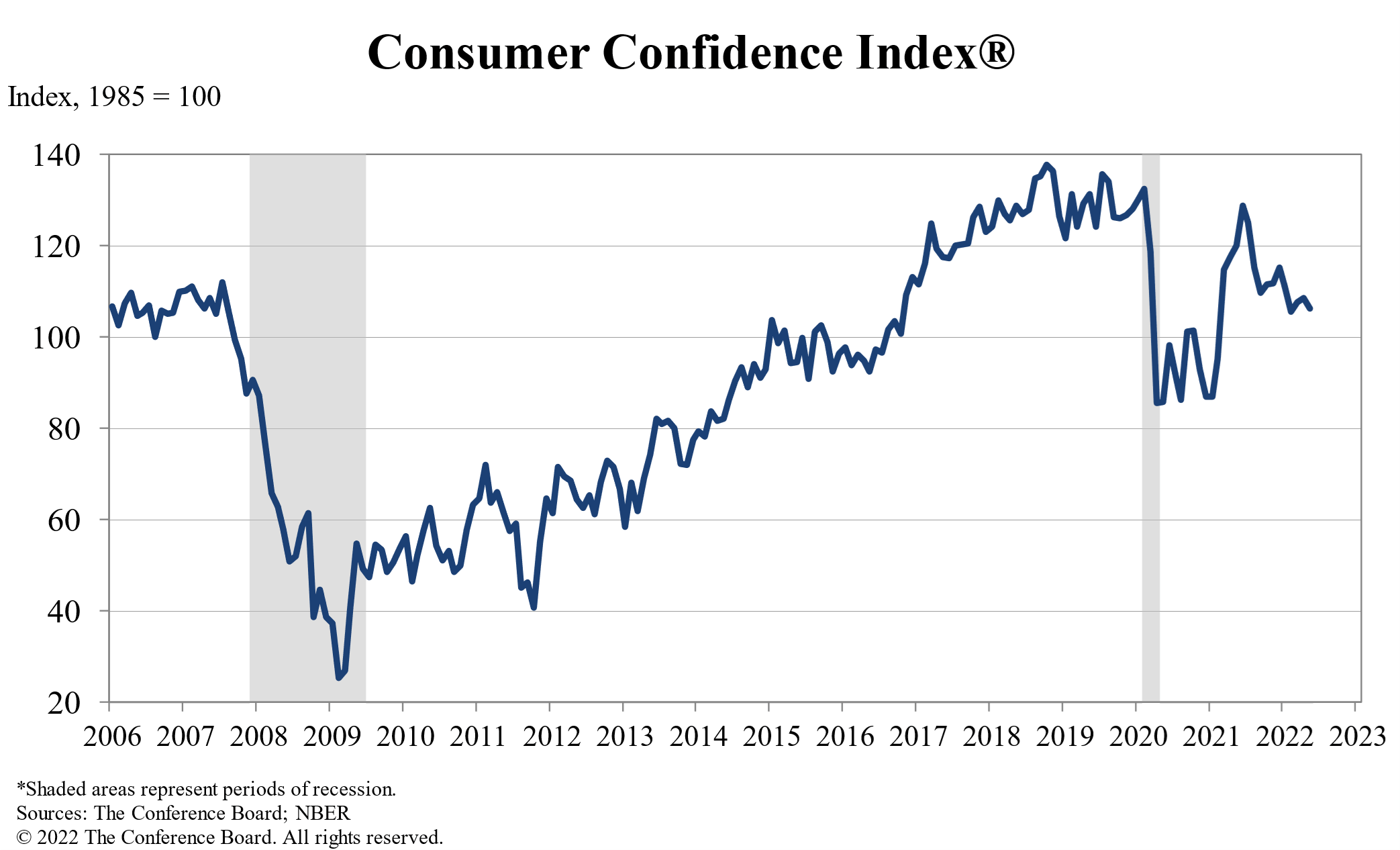

Uncertainty 1: US economy. As the US economic growth slows down, consumers have turned more cautious about discretionary spending on clothing to prioritize other necessities. Notably, in the first quarter of 2022, clothing accounted for only 3.9% of US consumers’ total expenditure, down from 4.3% in 2019 before the pandemic. Likewise, according to the Conference Board, US consumers’ confidence index (CCI) dropped to 106.4 (1985=100) in May 2022 from 113.8 in January 2022, confirming consumers’ increasing anxiety about their household’s financial outlook.

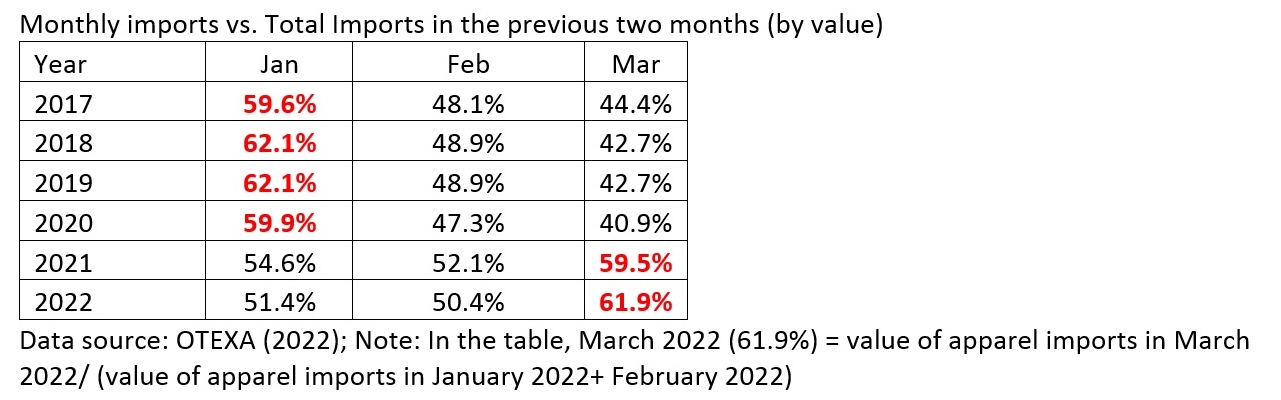

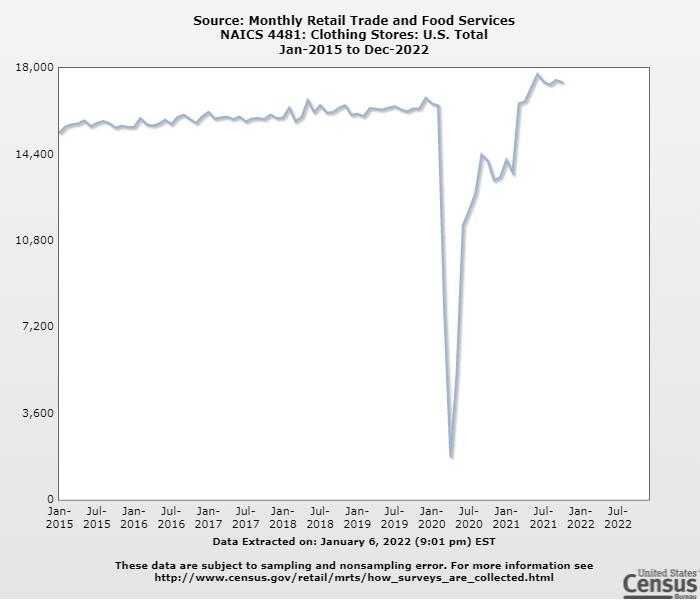

Removing the seasonal factor, US apparel imports in April 2022 went up 2.8% in quantity and 3.0% in value from March 2022, much lower than 9.3% and 11.9% a month ago (i.e., March 2022 vs. February 2022). The notable slowed import growth reflects the negative impact of inflation on US consumers’ clothing spending. According to the Census, the value of US clothing store sales marginally went up by 0.8% in April 2022 from a month ago, also the lowest so far in 2022.

Apparel import price index

Uncertainty 2: Worldwide inflation. Data from the Bureau of Economic Analysis shows that the price index of US apparel imports reached 103.1 in May 2022 (May 2020=100), up from 100.3 one year ago (i.e., a 2.8% price increase). At the product level (i.e., 6-digit HS Code, HS Chapters 61-62), over 60% of US apparel imports from leading sources such as China, Vietnam, Bangladesh, and CAFTA-DR experienced a price increase in the first quarter of 2022 compared with a year ago. The price surge of nearly 40% of products exceeded 10 percent. As almost everything, from shipping, textile raw materials, and labor to energy, continues to soar, the rising sourcing costs facing US fashion companies are not likely to ease anytime soon.

The deteriorating inflation also heats up the debate on whether to continue the US Section 301 tariff action against imports from China. Since implementing the punitive tariffs, US fashion companies have to pay around $1 billion in extra import duties every year, resulting in the average applied import tariff rate for dutiable apparel items reaching almost 19%. Although some e-commerce businesses took advantage of the so-called “de minimis” rule (i.e., imports valued at $800 or less by one person on a day are not required to pay tariffs), over 99.8% of dutiable US apparel imports still pay duties.

Uncertainty 3: “Made in China.” US apparel imports from China in April 2022 significantly dropped by 26.7% in quantity and 24.6% in value from March 2022 (seasonally adjusted). China’s market shares also fell to a new record low of 26.3% in quantity and 16.8% in value in April 2022. The zero-COVID policy and new lockdown undoubtedly was a critical factor contributing to the decline. Fashion companies’ concerns about the trajectory of the US-China relations and the upcoming implementation of the new Uyghur Forced Labor Prevention Act (UFLPA) are also relevant factors. For example, only 10.5% of US cotton apparel imports came from China in April 2022, a further decline from about 15% at the beginning of the year. Given the expected challenges of meeting the rebuttable presumption requirements in UFLPA and the high compliance costs, it is not unlikely that US fashion companies may continue to reduce their China exposure.

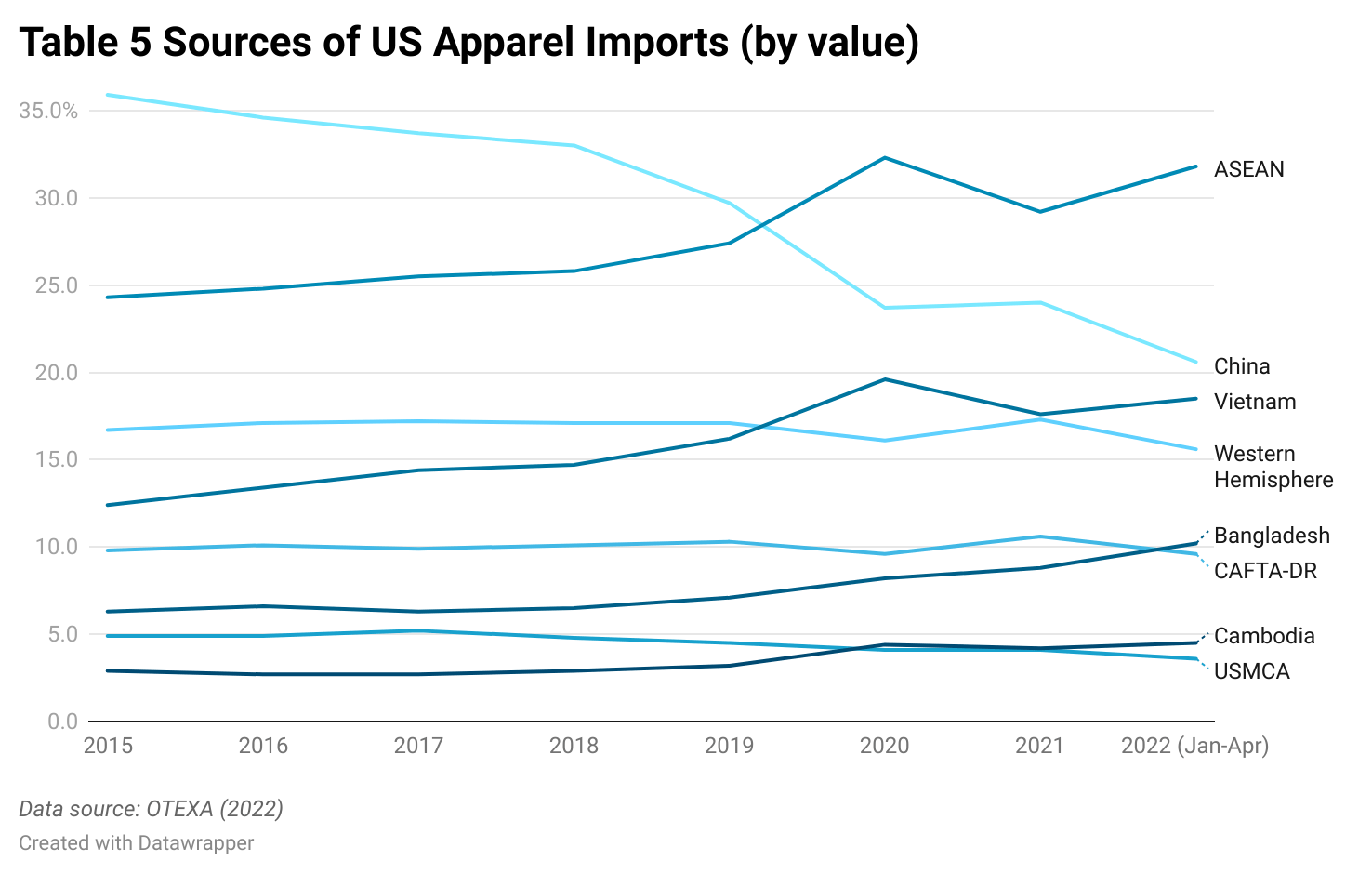

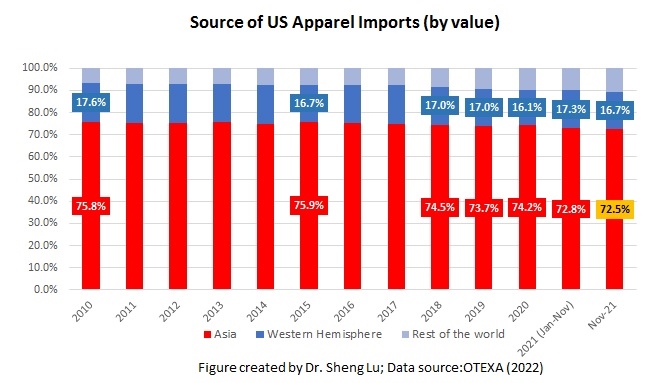

As US fashion companies source less from China, they primarily move their sourcing orders to China’s competitors in Asia. Measured in value, about 74.8% of US apparel imports came from Asia so far in 2022 (January-April), up from 72.8% a year ago. In comparison, there is no clear sign that more sourcing orders have been permanently moved to the Western Hemisphere. For example, in April 2022, CAFTA-DR members accounted for 9.3% of US apparel imports in quantity (was 10.8% in April 2021) and 10.2% in value (was 11.4% in April 2021).

Uncertainty 4: Shipping delays. Data suggests we are not out of the woods yet for shipping delays and supply chain disruptions. For example, as Table 2 shows, the seasonable pattern of US apparel imports in March 2022 is similar to January before the pandemic (2017-2020). In other words, many US fashion companies still face about 1.5-2 months of shipping delays. Additionally, several of China’s major ports were under strict COVID lockdowns starting in late March, including Shanghai, the world’s largest. Thus, the worsened supply chain disruptions could negatively affect the US apparel import volumes in the coming months.

Event summary by Mariel Abano (FASH455 student, Spring 2022)

COVID-19 and other external shocks such as the Ukraine-Russia war shifted the fashion supply chain from its conventional low-cost model. In response to the changes, brands and companies focus on flexibility, strengthening their relationships with suppliers, and sustainability.

Regarding the pandemic’s impacts on the apparel supply chain, fashion brands need to be more future-oriented to better prepare for unexpected market shocks that may come up in the fluctuating world. Flexibility within their merchandising teams allowed Neiman Marcus to pivot during the pandemic and market differently within the context of the pandemic. The company explored new ways to connect with its consumers via digital platforms as many physical stores closed. However, fashion companies need to be flexible enough to respond to the increasing demand from its growing e-commerce platform. This is not always easy to happen.

Likewise, Reformation tries its best to predict demand, build supply chain capacity, and manage lead time during COVID-19. Their manufacturing chains within the U.S. and vertical integration helped them respond quickly to supply chain disruptions. As a result, the company pivoted quickly to athleisure even though its brand is typically known for its event-wear dresses.

Meanwhile, when evaluating their supply chain, Amanda Martin explains that Neiman Marcusprioritizes labor, speed, and cost. With this, there is a balance between investment of capital and resources and mitigating costs like surging fuel prices.

The relationship with vendors also matters during the pandemic. For example, Neiman Marcus’s relationships with its vendors built over the years allowed the company to move more quickly from ocean to air shipping during the pandemic. In the discussion, Amanda Martin explained why the relationship between retailers/brands and manufacturers needs to help both sides grow and benefit. Likewise, Reformation also focuses on people and their relationships with their suppliers during the pandemic. Kathleen Talbot emphasizes that brand-supplier relationships are evolving. Fostering two-way conversations is key to moving away from the previous model that prioritized the needs and wants of the brand over the manufacturer.

Sustainability is NOT ignored during the pandemic. For example, fashion companies increasingly use technology and process management to take accountability for supply chains and improve traceability. In terms of environmental impact, there are more applications within sourcing emphasizing recycled and renewable materials. For example, Reformation recently launched a new circularity initiative that focuses on extending a product’s lifetime and then recycling that back into the system. When creating new styles, the company started from sustainable fibers. Further, they hope to shift transportation from air to other means to minimize their carbon footprint.

First, US apparel imports continue to rebound in November 2021 as companies build the inventory for the holiday season. Thanks to US consumers’ strong demand and the upcoming holidays, the value of US apparel imports went up by 15.7% in November 2021 from a month ago (seasonally adjusted) and increased by as much as 39.7% from 2020. However, before the pandemic, the value of US apparel imports always peaked in October and then gradually slipped in November and December. The unusual surge of imports in November 2021 could be the combined effects of price inflation and the late arrival of goods due to the shipping crisis.

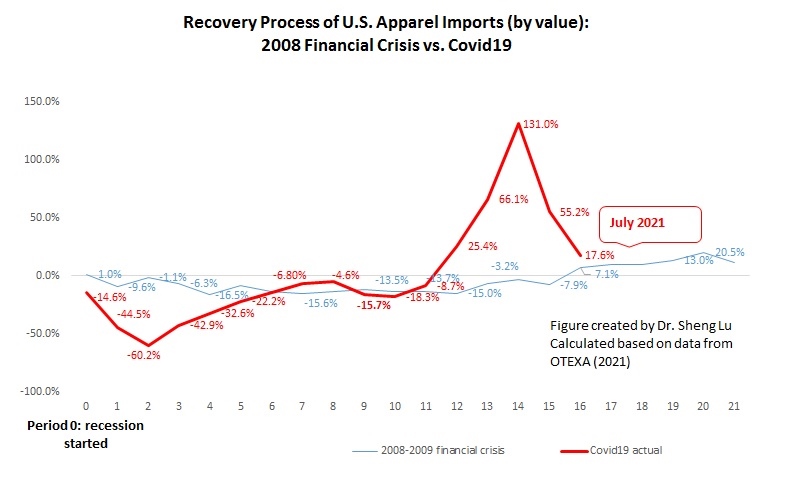

Meanwhile, US apparel imports so far in 2021 have been far more volatile than in the past few years because of uncertainties and disruptions caused by COVID-19 and the shipping crisis. For example, the year-over-year (YoY) growth rate ranged from 131% in May to 17.6% in July, causing fashion companies additional inventory planning and supply chain management challenges. Unfortunately, the new omicron variant could worsen the market uncertainty and volatility.

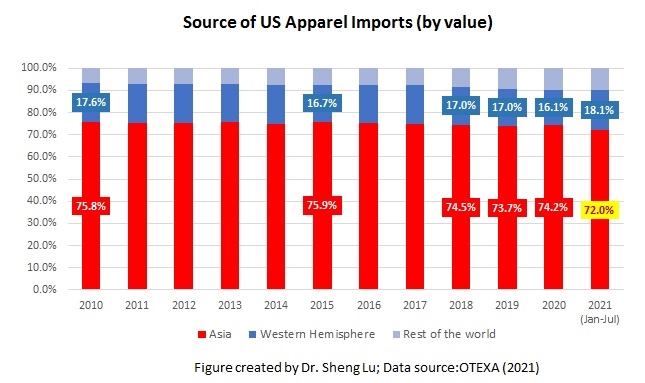

Second, Asian countries remain the dominant sourcing base for US fashion companies as the production capacity elsewhere is limited. Asian countries’ market shares fell from 74.2% in 2020 to 71.3% in July 2021, primarily because of the COVID lockdowns in Vietnam and Bangladesh. US apparel imports came from Asian countries rebounded to 74.8% and 72.5% in October and November 2021, respectively. This result suggests a lack of alternative sourcing destinations outside Asia, especially for large volume items. Meanwhile, the worsening shipping crisis affecting the route from Asia to North America could explain why Asian suppliers’ market shares in November were somewhat lower than a month ago.

Third, US companies continue to treat China as one of their essential sourcing bases in the current business environment. However, companies are NOT reversing their long-term strategy of reducing “China exposure.” China stays the largest supplier for the US market in November 2021, accounting for 41.5% of total US apparel imports in quantity and 25.8% in value. Due to the seasonal factor, China’s market shares typically peak from June to September and then drop from October until March-April.

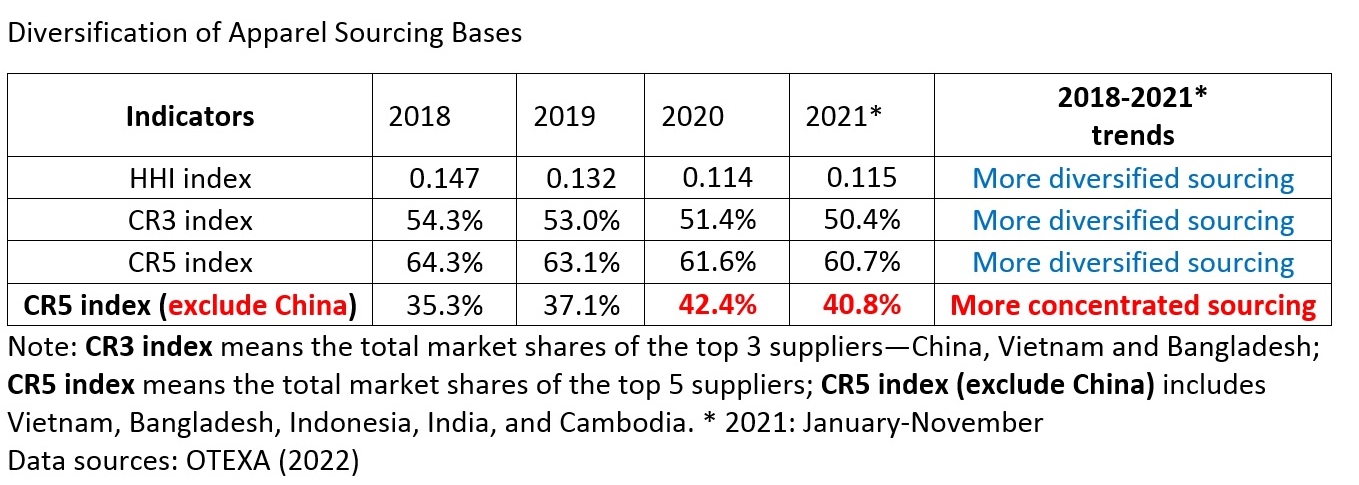

Both industry sources and the export product diversification index also consistently show that China supplied the most variety of products to the US market with no near competitors. In comparison, US apparel imports from Bangladesh, Mexico, and CAFTA-DR members concentrate more on specific product categories.

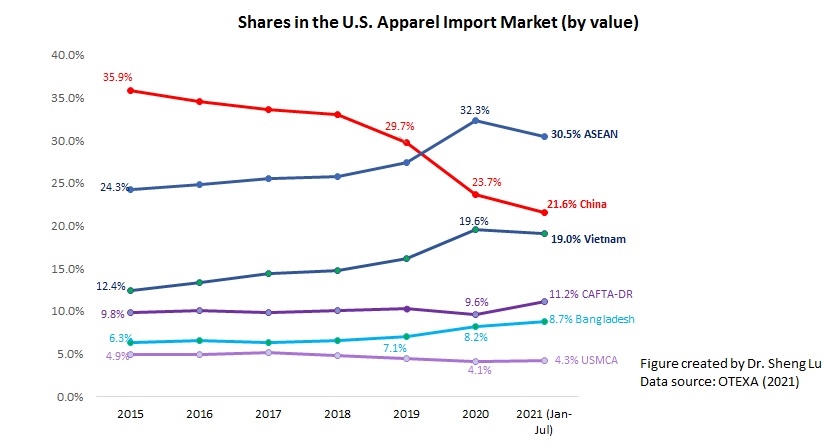

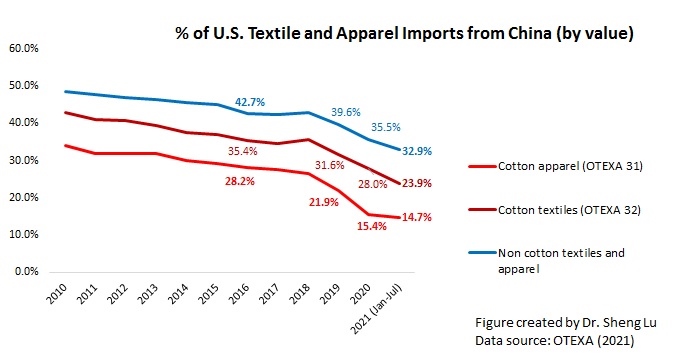

Nevertheless, the HHI index and market concentration ratios (CR3 and CR5) calculated based on the latest data suggest that US fashion companies continue to move their apparel sourcing orders from China to other Asian countries overall. For example, only around 15% of US cotton apparel comes from China, compared with about 27% in 2018. My latest studies also indicate that it has become ever more common to see a fashion company places only around 10% of its total sourcing value or volume from China compared to over 30% in the past. Furthermore, with the growing tensions of the US-China relations and the newly enacted Uyghur Forced Labor Prevention Act, fashion companies could take another look at their China sourcing strategy to avoid potential high-impact disruptions.

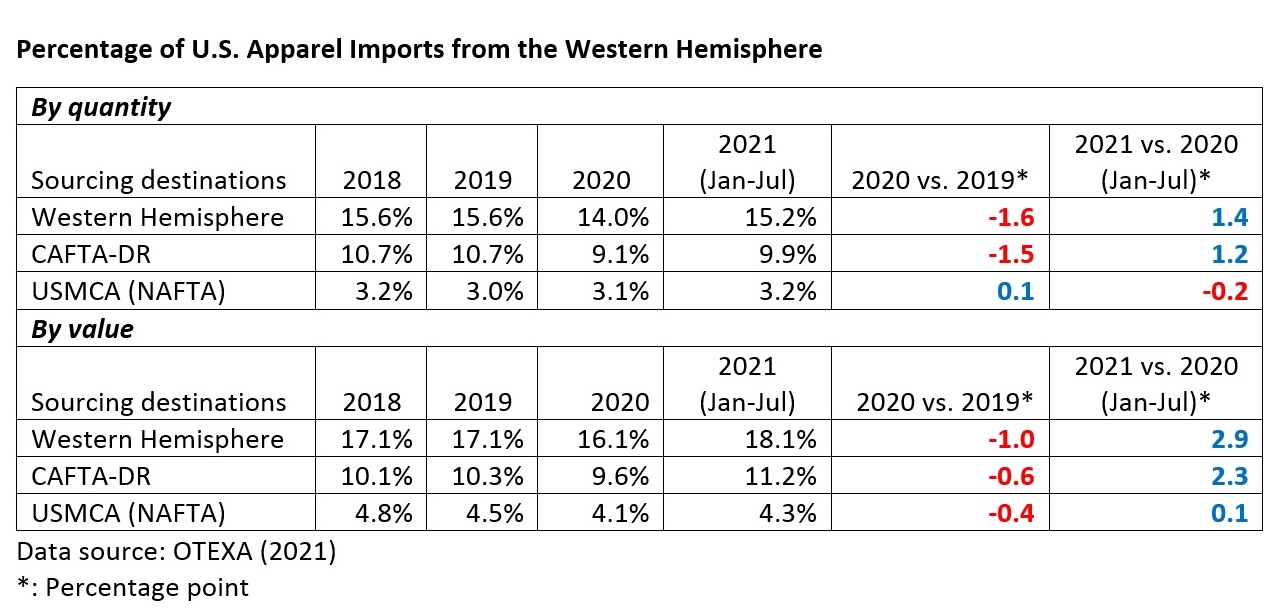

Fourth, near sourcing from the Western Hemisphere, especially CAFTA-DR members, continue to gain popularity. Specifically, 17.3% of US apparel imports came from the Western Hemisphere year-to-date (YTD) in 2021 (January-November), higher than 16.1% in 2020. Notably, CAFTA-DR members’ market shares increased to 10.6% in 2021 (January to November) from 9.6% in 2020. The value of US apparel imports from CAFTA-DR also enjoyed a 41.7% growth in 2021 (January—November) from a year ago, one of the highest among all sourcing destinations. The imports from El Salvador (up 42.6%), Honduras (up 47.1%), and Guatemala (36.6%) had grown particularly fast so far in 2021. However, the political instability in some Central American countries could make fashion companies feel hesitant to permanently switch their sourcing orders to the region or make long-term investments.

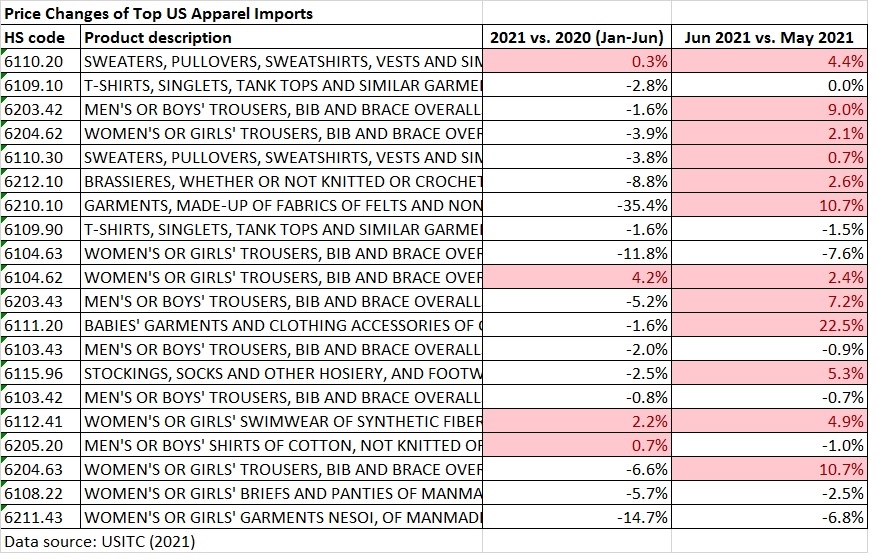

Additionally, the latest trade data suggests a notable increase in the price of US apparel imports. Notably, the unit price of US apparel imports from almost all leading sources went up by more than 10% from January 2021 to November 2021. As worldwide inflation continues, the rising sourcing cost pressure won’t ease anytime soon.

In December 2021, McKinsey & Co’ and Business of Fashion (BOF) released its annual State of Fashion report. Below are the key points in the report regarding the sourcing trends in the year ahead:

#1 The logistics challenges could intensify in 2022, with 87% of respondents expecting supply chain disruptions to continue to affect their profit margins in the year ahead negatively. The global surges in demand create additional and unpredictable pressures on freight services, ports, and terminals. As a result, fashion companies may need to “plan for a permanently more expensive logistical future.”

#2 It will be critical for fashion companies to keep sourcing flexible, build resilience into the supply chain, and work closely with vendors. As one respondent commented, “[crises like] pandemics do happen.”

#3 The interest in nearshoring and reshoring will continue in 2022. Over 70% of respondents plan to increase the share of nearshoring close to company headquarters, and about 25% intend to reshore sourcing to their headquarters’ country. Notably, some EU-based companies have been moving textile manufacturing from China to Turkey to minimize delays.

#4 One crucial free trade agreement to watch is the Regional Comprehensive Economic Partnership (RCEP), to take effect on January 1, 2022. It’s the largest free trade agreement in history, involving nearly 30% of the world’s population. RCEP “has the potential to be at the core of the reconstruction of the global supply chain. RCEP is possibly the only trading block with both production capacity and consumer demand,” meaning it could dramatically facilitate regional trade and investment within Asia.

#5 There is a “significant opportunities in creating a hyperdigital supply chain.” Some companies are leveraging technology to find“competitive advantages in a supply-chain context when it comes to speed, agility, cost efficiency, and price.” However, fashion companies admit, it will remain challenging to plan inventory flow with much precision, which won’t change any time soon.

Other interesting comments from the report:

“One mega trend…in the sector is the importance of breaking down the traditional boundaries of what’s in the company and [what is done externally]; what can be accomplished together as a network — whether it’s creativity, sustainability, and supply chain, or technology.”

“As fashion brands look to pursue closed-loop recycling solutions, it is increasingly important to engage with suppliers who can help them move toward sourcingcircular materials.” “Cost is certainly a factor; recycled fibres are typically more expensive than their virgin counterparts.”

“In the longer term, fashion brands will need to balance the desire to enhance speed to market with the need to alleviate supply chain pressure…That may mean streamlining production, logistics planning, and booking capabilities, as well as putting in place contingency plans and alternative suppliers while remaining as agile and flexible as possible.”

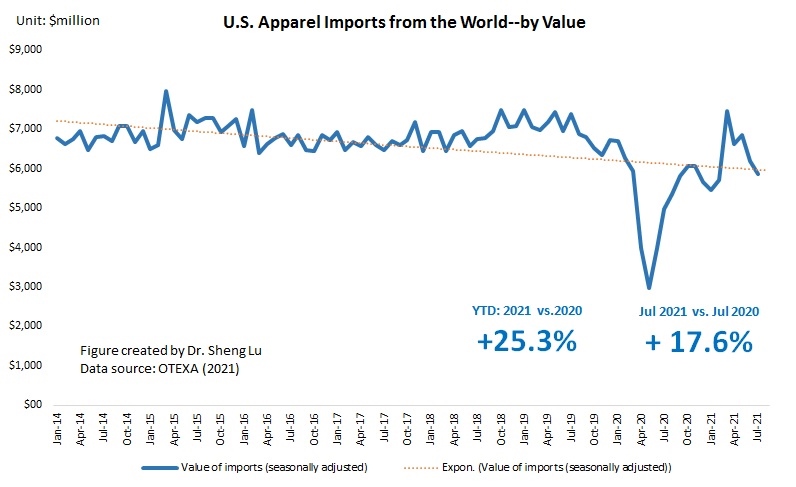

First, the shipping crisis and new wave of COVID cases start to affect US apparel imports negatively. While US consumers’ demand for clothing overall remains strong, for the second month in a row, the value of US apparel imports (seasonally adjusted) in July 2021 decreased by 5.5% from a month ago and down 9.7% from May to June. The absolute value of US apparel imports year to date (YTD) in 2021 (January—July) was 25.3% higher than in 2020 and around 87% of the pre-COVID level (benchmark: January-July, 2019). However, the year-over-year growth in July 2021 was only 15.4%, compared with 60.0% in May 2021 and 29.1% in June 2021. Overall, the results remind us that the market environment is far from stable yet as the COVID situation in the US and other parts of the world continues to evolve.

Second, Asian countries lost market shares as some leading apparel supplying countries, including Vietnam and Bangladesh, struggled with new COVID lockdowns. While Asia as a whole remains the single largest apparel sourcing base for US companies, Asian countries’ market shares fell from 74.2% in 2020 to 71.3% in July 2021, the lowest since 2010. The new COVID lockdowns in Vietnam and Bangladesh, the No. 2 and No. 3 top suppliers for the US market, post significant challenges to US fashion companies trying to build inventory for the upcoming holiday season. Notably, US companies source many high-volume products from these two countries, and there is a lack of alternative sourcing destinations in the short run.

Third, US companies continue to treat China as an essential sourcing base during the current challenging time. However, there is no clear sign that companies are reversing their long-term strategy of reducing “China exposure.” China stays the largest supplier for the US market in July 2021, accounting for 41.3% of total US apparel imports in quantity and 26.0% in value. The export product diversification index also suggests that China supplied the most variety of products to the US market. US apparel imports from Bangladesh, Mexico, and CAFTA-DR members are more concentrated on specific product categories. In other words, should China were under lockdowns, the negative impacts on US companies’ inventory management could be even worse.

Nevertheless, the HHI index and market concentration ratios (CR3 and CR5) calculated based on the latest data suggest that US fashion companies continue to move their apparel sourcing orders from China to other Asian countries overall. For example, only 14.7% of US cotton apparel imports came from China in 2021 (January—July), a new record low in the past ten years. Further, as US apparel imports from China typically peak from June to September because of seasonal factors, China’s market shares are likely to drop in the next few months. Additionally, the fundamental concerns about sourcing from China are NOT gone. On the contrary, new US actions against alleged forced labor in Xinjiang are likely in the coming months and affect imports from China beyond cotton products.

Fourth, US apparel sourcing from the Western Hemisphere, especially CAFTA-DR members, gains new momentum. Specifically, 18.1% of US apparel imports came from the Western Hemisphere YTD in 2021 (January-July), higher than 16.1% in 2020 and 17.1% before the pandemic. Notably, CAFTA-DR members’ market shares increased to 11.2% in 2021 (January to July) from 9.6% in 2020. The value of US apparel imports from CAFTA-DR also enjoyed a 58.4% growth in 2021 (January—July) from a year ago, one of the highest among all sourcing destinations. The imports from El Salvador (up 75.2%), Honduras (up 74.6%), Dominican Republic (45.1%), and Guatemala (40.6%) had grown particularly fast so far in 2021.

Meanwhile, US apparel imports from USMCA members stayed stable (i.e., no significant change in market shares). CAFTA-DR and USMCA members currently account for around 60% and 25% of US apparel imports from the Western Hemisphere. They are also the single largest export market for US textile products (about 70%).

Fifth, US apparel imports start to see a notable price increase. While an across-the-board price increase was not a big concern at the beginning of 2021, the increase has become more noticeable since June 2021. For example, of the top 20 US apparel imports (HS chapters 61-62) at the 6-digit HS code level based on import value, the price of thirteen products increased from May to June 2021. The price increase at the country level is even more significant. From May to July 2021, the average unit price of US apparel imports from leading sources all went up substantially, including China (7%), Vietnam (13%), Bangladesh (13.9%), and India (15.6%).

As almost everything is becoming more expensive, from raw material, shipping to labor, the August and September trade data (to be released in October and November) could suggest an even more significant price increase.

Discussion question: How has the container shipping crisis affected the fashion apparel industry? While shopping for clothing, do you observe any market trends related to the shipping crisis (e.g., retail price and product availability)? Why or why not do you think the container shipping crisis will go away anytime soon?

#1 COVID-19 continues to substantially affect U.S. fashion companies’ sourcing and business operations in 2021

Recovery is happening: Most respondents expect their business to grow in 2021. Around 76 percent foresee their sourcing value or volume to increase from 2020. Around 60 percent of respondents expect a full recovery of their sourcing value or volume to the pre-COVID level by 2022.

Uncertainties remain: Still, 27 percent find it hard to tell when a full recovery will happen. About 20 percent of respondents still expect 2021 to be a very challenging year financially.

U.S. fashion companies’ worries about COVID still concentrate on the supply side, including driving up production and sourcing costs and causing shipping delays and supply chain disruptions. U.S. fashion companies’ COVID response strategies include strengthening relationships with key vendors, emphasizing sourcing agility and flexibility, and leveraging digital technologies. In comparison, few respondents canceled sourcing orders this year.

#2 The surging sourcing costs are a significant concern to U.S. fashion companies in 2021.

As many as 97 percent of respondents anticipate the sourcing cost to increase further this year, including 37 percent expect a “substantial increase” from 2020.

Respondents say almost EVERYTHING becomes more expensive in 2021. Notably, more than 70 percent of respondents expect the “shipping and logistics cost,” “cost of textile raw material (e.g., yarns and fabrics),” “cost of sourcing as a result of currency value and exchange rate changes,” and “labor cost” to go up.

#3 U.S. fashion companies’ sourcing strategies continue to envovle in response to the shifting business environment.

Asia’s position as the dominant apparel sourcing base for U.S. fashion companies remains unshakeable.

“China plus Vietnam plus Many” remains the most popular sourcing model among respondents. However, the two countries combined now typically account for 20-40 percent of a U.S. fashion company’s total sourcing value or volume, down from 40-60 percent in the past few years.

Asia is U.S. fashion companies’ dominant sourcing base for textile intermediaries. “China plus at least 1-2 additional Asian countries” is the most popular textile raw material sourcing practice among respondents.

As U.S. fashion companies prioritize strengthening their relationship with key vendors during the pandemic, respondents report an overall less diversified sourcing base than in the past few years.

#4 U.S. fashion companies continue to reduce their China exposure. However, the debate on China’s future as a textile and apparel sourcing base heats up.

Most U.S. fashion companies still plan to source from China in short to medium terms. While 63 percent of respondents plan to decrease sourcing from China further over the next two years, it is a notable decrease from 70 percent in 2020 and 83 percent in 2019.

Most respondents still see China as a competitive and balanced sourcing base from a business perspective. Few other sourcing countries can match China’s flexibility and agility, production capacity, speed to market, and sourcing cost. As China’s role in the textile and apparel supply chain goes far beyond garment production and continues to expand, it becomes ever more challenging to find China’s alternatives.

Non-economic factors, particularly the allegations of forced labor in China’s Xinjiang Uygur Autonomous Region (XUAR), significantly hurt China’s long-term prospect as a preferred sourcing base by U.S. fashion companies. China also suffered the most significant drop in its labor and compliance rating this year.

#5 With an improved industry look and the continued interest in reducing “China exposure,” U.S. fashion companies actively explore new sourcing opportunities.

Vietnam remains a hot sourcing destination. However, respondents turn more conservative this year about Vietnam’s growth potential due to rising cost concerns and trade uncertainties caused by the Section 301 investigation.

U.S. fashion companies are interested in sourcing more from Bangladesh over the next two years. Respondents say apparel “Made in Bangladesh” enjoys a prominent price advantage over many other Asian suppliers. However, the competition among Bangladeshi suppliers could intensify as U.S. fashion companies plan to “work with fewer vendors in the country.”

Respondents are also interested in sourcing more from Sub-Saharan Africa by leveraging the African Growth and Opportunity Act (AGOA). Respondents also demonstrate a growing interest in investing more in AGOA members directly. “Replace AGOA with a permanent free trade agreement that requires reciprocal tariff cuts and continues to allow the “third-country fabric provision” is respondents’ most preferred policy option after AGOA expires in 2025.

#6 Sourcing from the Western Hemisphere is gaining new momentum

Overall, U.S. fashion companies’ growing interest in the Western Hemisphere is more about diversifying sourcing away from China and Asia than moving the production back to the region (i.e., reshoring or near-shoring).

Respondents say CAFTA-DR’s “short supply” and “cumulation” mechanisms provide critical flexibility that allow U.S. fashion companies to continue to source from its members. However, despite the “yarn-forward” rules of origin, only 15 percent of respondents sourcing apparel from CAFTA-DR members say they “purposefully use U.S.-made fabrics” to enjoy the agreement’s duty-free benefits.

Respondents suggest that encouraging more apparel sourcing from the Western Hemisphere requires three significant improvements: 1) make the products more price competitive; 2) strengthen the region’s fabric and textile raw material production capacity; 3) make rules of origin less restrictive in relevant U.S. trade agreements.

This year’s benchmarking study was based on a survey of executives at 31 leading U.S. fashion companies from April to June 2021. The study incorporates a balanced mix of respondents representing various types of businesses in the U.S. fashion industry. Approximately 54 percent of respondents are self-identified retailers, 46 percent self-identified brands, 69 percent self-identified importers/wholesalers. Around 65 percent of respondents report having more than 1,000 employees. Another 27 percent of respondents represent medium-sized companies with 101-999 employees.