According to Reuters, Shein has received the necessary approvals to proceed with its Hong Kong IPO, which could take place as early as this fall. As part of the IPO process, Shein has disclosed detailed information about its business operations. The following analysis focuses specifically on the company’s sourcing strategies and supply chain practices.

Overview of Shein’s market and financials

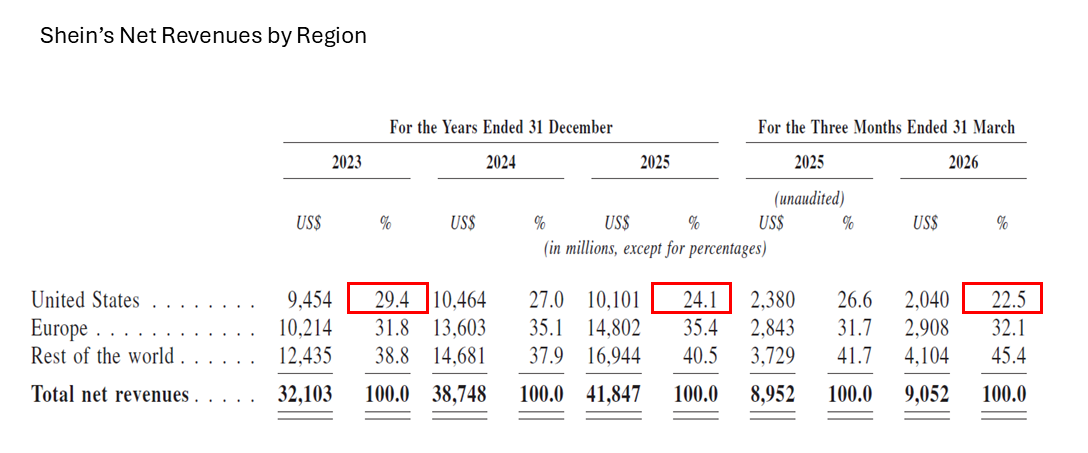

According to the IPO filing document, Shein serves “more than 273 million active consumers in approximately 160 markets across the world.” In the first quarter of 2026, about 22.5% of Shein’s net revenue came from the US, down from 24.1% in 2025, 27.0% in 2024, and 29.4% in 2023. Over the same period, the EU (about 32.1% in Q1 2026) and the rest of the world (about 45.4% in Q1 2026) accounted for a larger share of Shein’s revenue.

Shein’s gross margin increased from 60.6% in 2024 to 67.9% in 2025 and 70.4% in Q1 2026. This increase partly reflects Shein’s growing third-party marketplace business, in which Shein generally records only “service fees” from third-party merchants rather than the full value of merchandise sold, and does not incur merchandise cost of sales on those transactions. Thus, the increase in gross margin reflects, at least in part, a shift in business mix rather than a comparable improvement in the merchandise profit margin.

Meanwhile, Shein’s net profit margin declined from 8.7% in 2024 to 4.9% in 2025 and a negative 1.1% in Q1 2026. The pressure is particularly evident in fulfillment costs, which increased from around 42% of revenue between 2023 and 2024 to 45.6% in 2025 and 47.7% in the first quarter of 2026. Shein subsequently recorded a net loss of US$99 million in the first quarter of 2026.

What is Shein’s LATR Model?

Behind Shein’s “ultra fast fashion” is what it calls the “Large-scale Automated Test and Reorder (LATR) operating model.” Under this approach, new products are initially produced in batches of approximately 100–200 units, and demand is evaluated using real-time customer data. Products that perform well are replenished rapidly, often within five days. Shein believes this system enables it to simultaneously offer an extremely broad assortment, rapid product refreshment, and low inventory levels, the three objectives that traditional apparel retailers often struggle to achieve.

Warehouses play a critical role in Shein’s LATR model and supply chain. According to the company, it has approximately 6 million square meters of warehouse space across Asia, North America, Europe, the Middle East, and South America as of 30 June 2026. Once Shein’s supply chain partners produce a small batch of products, that batch is shipped to one of Shein’s warehouses. Upon receiving customer orders, Shein packages and ships products directly from its warehouses to customers around the world. Shein has also been increasing its efforts to establish new warehouses around the world to be closer to the markets it serves.

Where are Shein’s apparel products mostly made?

As of 2025, Shein works with 7,500 contract manufacturers as well as “large numbers of merchants, independent designers and other suppliers.” Most of Shein’s partners are small and medium-sized enterprises (SMEs). This suggests that instead of relying on a small number of vertically integrated factories, Shein leverages a large, fragmented, and flexible supplier network. The advantage of SMEs is that they can specialize in particular products or production processes and have unused capacity that can be activated when demand suddenly increases.

Shein also admits that its supply network is “built on a distributed footprint of supply chain and fulfillment locations anchored by a central logistics hub in China.” “In 2025, products stored in our central warehouses in the Chinese mainland represented over 90% of our net revenues.”

Furthermore, unlike most Western fashion brands and retailers, which are pursuing a strategy of “reducing China exposure” and “sourcing diversification,” Shein’s IPO filing document does not indicate a large-scale shift of its production away from China.

What are Shein’s key supplier selection criteria?

Shein says its suppliers do not have to be exclusive. Instead, contract manufacturers are permitted to supply other companies. No individual supplier accounted for more than 10% of Shein’s total purchases, and the five largest suppliers together represented only 14.9%–16.4% of Shein’s purchases from 2023 to 2025.

Shein allocates sourcing orders in part based on each supplier’s expertise, not solely on price. According to Shein, “our cloud-based software solutions enable suppliers to be fully digitally integrated with our supply chain from end to end, giving us full-chain visibility. This allows us to automatically allocate orders to suppliers based on expertise, price, capacity and other factors, helping suppliers maximize capacity utilization.” Thus, Shein’s supplier network seems to be differentiated by production capabilities rather than treated as a pool of interchangeable factories.

Shein also expects its suppliers to be flexible and nimble, with the ability to produce small initial batches and rapidly scale up production when demand is demonstrated. According to the company, “because an initial production batch consists of approximately 100 to 200 items, we can quickly launch a large number of new products with minimal upfront commitment, inventory risk, and resource waste. If a product sells well, we can rapidly scale up its production to meet consumer demand. We can rapidly launch small initial batches, and restock products that are in demand in as few as five days.”

Overall, Shein’s business model means it needs a network of specialized factories with flexible capacity. Its technology essentially acts as the coordination mechanism connecting those factories to rapidly changing demand. Shein also says it connects with its suppliers closely and deeply through digital technologies. Shein argues that such integration helps its suppliers “enjoy more predictable order flow, improved asset utilization and higher returns on investment, even with small batch production.”

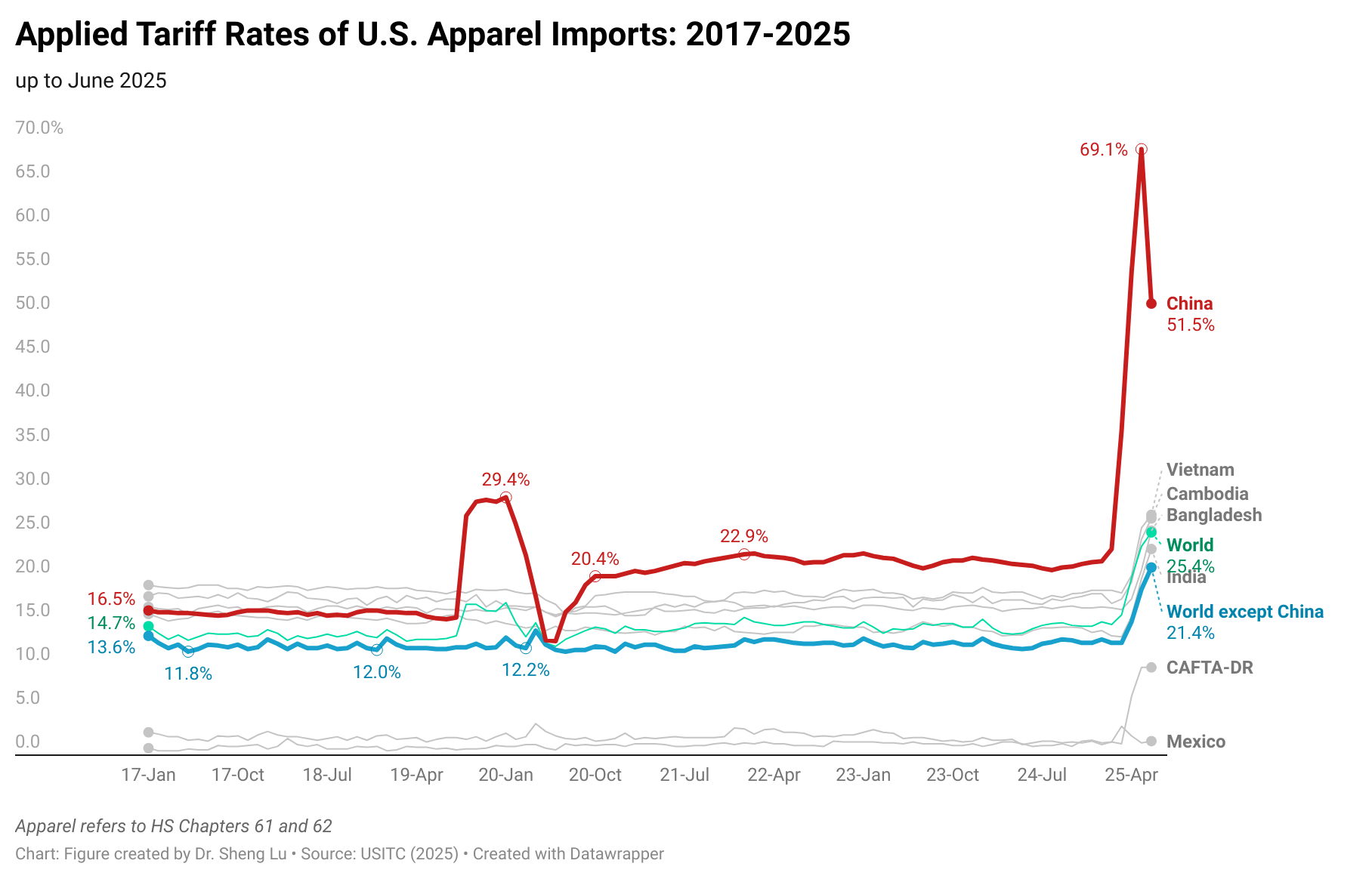

How have de minimis removal and tariffs affected Shein?

Shein acknowledged that the removal of the U.S. de minimis exemption has already reduced its U.S. sales, slowed company-wide revenue growth, and increased fulfillment expenses. Shein says it is also aware of the EU de minimis rule changes.

In response to the removal of de minimis, Shein says it “for products previously eligible for the de minimis exemption, we have transitioned from a simple customs entry process for de minimis packages to a customs clearance process that requires more extensive documentation and procedures. Amongst other things, we have adopted necessary protocols for the formal entry process to ensure compliance with the more stringent documentation and other procedural requirements”

Regarding tariffs, Shein says “As a result of the recent developments, our China-origin products have become subject to tax rates ranging from 10% to 87.5% (increased from 0-62.5% during the Track Record Period prior to the removal of the de minimis exemption and the Trump Administration’s recent imposition of additional tariffs).

To mitigate the tariff impacts, Shein has been “pursuing a wide range of options, including increasing our prices in the U.S. market to offset a portion of the increased.”

How does Shein see the impacts of environmental regulations? How does sustainability fit its business model?

Shein argues that its demand-driven production system reduces overproduction by producing only small initial batches and replenishing products only after actual consumer demand has been observed. According to the company, this approach minimizes excess inventory, lowers waste, and improves profitability simultaneously. In other words, sustainability is portrayed as aligned with operational efficiency rather than being a cost imposed by regulation.

However, reducing unsold inventory is distinct from addressing the broader environmental impacts associated with the high-volume apparel overconsumption problem.

In the IPO filing document, Shein also introduces the company’s evoluSHEIN sustainability roadmap, which includes responsible design, material sourcing, circularity initiatives, and decarbonization efforts across the value chain. Shein intends to integrate sustainability into product development, manufacturing, and logistics while continuing to emphasize affordability and efficiency.

Supplier auditing

According to Shein, under its Responsible Sourcing (“SRS”) program, suppliers are audited by both in-house teams and internationally renowned third-party auditors, including Bureau Veritas, Intertek, Openview, SGS, TÜV Rheinland, and QIMA, all members of the Association of Professional Social Compliance Auditors. Shein ran roughly 4,200, 4,550, and 5,150 SRS on-site audits in 2023, 2024, and 2025, respectively, covering contract manufacturers representing about 95% of company-branded procurement value each year. In 2025, over 99% of Shein’s on-site SRS audits were conducted by third-party auditors.

Additionally, Shein discloses that 5, 12, and 5 suppliers were terminated in 2023, 2024, and 2025, respectively, for SRS policy violations. The supplier code of conduct is said to align with the International Labor Organization (ILO) core conventions and the UN Universal Declaration of Human Rights.

However, in the IPO filing document, Shein didn’t mention anything related to forced labor risk, Xinjiang cotton, or UFLPA-related compliance.

What important business issues does Shein see over the next few years?

According to the IPO filing document, Shein sees its future success as depending on the company’s ability to continue expanding internationally while adapting to increasingly complex trade and regulatory environments. Shein regards investments in technology, artificial intelligence, supply chain resilience, fulfillment infrastructure, and marketplace expansion as central strategic priorities.

Importantly, Shein acknowledges that “we have grown rapidly since our inception, and there is no assurance that our growth will continue. In particular, we recorded a net loss of US$99 million for the three months ended 31 March 2026, and there is no assurance that we will achieve or maintain profitability in the future.”

Shein also noted that international tensions are expected to “escalate at an accelerated pace,” potentially creating additional barriers to trade. Its China-based sourcing model therefore represents a strategic vulnerability, even if maintaining production in China remains economically advantageous. As Shein acknowledged, “We sell products to a large number of countries and regions around the world, including the United States and Europe. Currently, the substantial majority of the products sold by us or on our marketplace originate from the Chinese mainland. Tariffs and other trade restrictions imposed by any country where we sell products, particularly on products shipped from China, could significantly hinder our ability to sell products to that country.”

by Sheng Lu

{kind=link}