#1: Why did denim production shift from the United States to Asia? Was lower labor cost the primary driver, or were other structural factors equally or more important? Explain your reasoning.

#2: The video argues that U.S. denim mills are not competing against Pakistani fabric mills, but against “Pakistan’s entire vertically integrated apparel supply chain.” Do you agree? Why or why not? Should the United States rebuild a vertically integrated apparel supply chain, or should it focus on capital-intensive textile manufacturing while continuing to outsource labor-intensive apparel production? What are the benefits and challenges of each approach? Explain your thoughts.

#3: If you were the sourcing manager for Levi’s or American Eagle, under what circumstances would you choose to source denim apparel from the U.S. instead of Pakistan or Mexico? You may consider factors such as cost, lead time, product quality, sustainability, trade policy, and consumer demand.

#4: Would higher U.S. tariffs on imported apparel alone be enough to bring apparel manufacturing back to the United States? Use evidence from the video to support your argument.

Based on the article, do you think tariffs are an effective strategy for strengthening the U.S. textile industry and the Western Hemisphere textile and apparel supply chain today? Why or why not?

In your comment:

Clearly explain your viewpoint

Apply at least one key concept learned from our lectures in April/May

Use specific examples, data, or arguments from the article to support your viewpoint

You may also address any of the following aspects in your comment:

Why do some U.S. industry stakeholders, such as NCTO, prefer U.S. apparel sourcing from the Western Hemisphere over Asia?

How do trade agreements such as USMCA or CAFTA-DR support regional textile and apparel supply chains in the Western Hemisphere?

What are the advantages and limitations of producing textiles in the United States while assembling apparel in nearby countries in the Western Hemisphere?

Do you think tariffs encourage long-term investment in U.S. textiles, or do they mainly create short-term adjustments in sourcing strategies?

How could rising geopolitical tensions and supply chain disruptions increase the importance of Western Hemisphere sourcing?

My name is Martha Girard, and I am a proud Blue Hen alum. I can’t pinpoint exactly when my passion for fashion began. It has always simply been a part of who I am. Even when I was a toddler, I would wear princess ballgowns and heels to the grocery store (move over, Carrie Bradshaw). When it came time to choose a college, the University of Delaware’s highly regarded fashion program felt like a natural place to pursue that passion.

During my junior year, I had the opportunity to meet Dr. Sheng Lu, who recognized my drive and encouraged me to apply for the UD Summer Scholars research program. Soon after, the COVID-19 pandemic transformed the world as we knew it. While much of life came to a halt, I immersed myself in research, examining how retailers were approaching secondhand product assortment and pricing strategies (note: see the publication based on the summer scholar research). I developed a genuine passion for this work!

That passion for secondhand strategy and sustainable fashion led me to Nuuly, where I joined as a Merchandise Assistant after graduation. As part of a rapidly growing startup, I gained hands-on experience in buying, production, shipping, and planning. This was far more than I ever expected to learn early in my career. I later transitioned to Lilly Pulitzer as an Associate Merchandiser, where I managed women’s pants, shorts, and skirts.

In mid-2024, a personal move brought me to New York City, where I stepped into a new role as a Production Coordinator at Jay Franco. While this position differed from my previous experience—shifting from women’s fashion to licensed children’s home products—it presented an exciting challenge. I was drawn to the team (and my amazing boss, Emily) and trusted my instincts that it was the right opportunity.

Nearly two years later, I can confidently say that decision was the right one. I’ve developed a strong foundation in sourcing, supply chain, and production, and my background in buying and merchandising has strengthened my perspective. Together, these experiences continue to shape me as I grow in my career as a Production Manager.

Disclaimer: The views expressed in this interview are those of Martha Girard and do not reflect the views or positions of her employer or any affiliated organizations.

Sheng: What are your main responsibilities as a production manager? Can you walk us through your typical day? What aspects of the job do you find most interesting, or something you didn’t expect when you took the role?

Martha:My primary responsibility is to ensure that every order meets the buyer’s ship date. While that may sound straightforward, it requires close coordination from the moment a purchase order is issued to when the goods arrive at the warehouse. I serve as the primary point of contact between our factories and internal teams, ensuring all updates are clearly and consistently shared.

I typically start my day by reviewing and updating the status of all open orders. My direct report and I manage approximately 200–300 orders at any given time. These updates include pricing, ship dates, licensor approvals (as all products must be reviewed and approved by their respective licensors), and any factory-related developments. Communicating these updates to our cross-functional partners is critical to ensuring alignment and avoiding delays.

From there, I move on to processing new orders received that day, followed by reviewing shipping reports to confirm that all vessels are on schedule and progressing as expected.

What I find most exciting about my role is the constant variety. No two days are the same. With factors like tariffs and global shipping disruptions, there is always a new challenge to navigate. The role requires strong problem-solving skills and creative thinking to keep operations running smoothly and ensure our buyers’ expectations are consistently met.

Sheng: When deciding where to source home textile products, what are the most important factors you consider (e.g., cost, lead time, quality, supplier reliability)? How do you balance these trade-offs?

Martha:All of our products are custom-made for each buyer or retailer, so it is ultimately up to our customers to decide on the perfect balance of these trade-offs. The needs of a large department store may focus on classic home assortments, which differ significantly from those of a value-driven retailer like a dollar store. We are well-positioned to support both.

For example, a dollar store partner may collaborate with our product team to develop a cost-efficient item that can move from concept to shelf in as little as 120 days. In contrast, a large department store may work with us to design a premium throw blanket at a higher price point, with a longer development timeline of up to six months to ensure the final product meets their standards. This flexibility allows us to tailor our sourcing approach and deliver solutions that align with each customer’s unique strategy.

Sheng: How have recent tariffs and policy uncertainties affected home textile production and sourcing? What is your observation?

Martha: Unfortunately, the tariffs had a huge negative impact on U.S.-based fashion apparel companies. Many buyers canceled orders from China due to rising costs, prompting companies to explore sourcing options in countries with lower tariff exposure. This shift has been challenging, not only because companies have built strong, long-standing relationships with our manufacturing partners in China, but also because transitioning to new sourcing regions is both time-consuming and costly. It requires extensive research and development to evaluate whether alternative countries can meet our quality, pricing, and production standards.

Sheng: Sustainability is becoming increasingly important in the textile and apparel industry. How is this affecting the home textiles sector and your job? For example, are there changes in materials, sourcing practices, or supplier requirements?

Martha:We are finding that many of our licensors and customers are placing a strong emphasis on sustainability and eco-friendly materials. For example, one major customer (note: a well-known toy brand) only allows us to use 100% recycled polyester for their items and strives for eco-friendly packaging. As a company, we are happy to follow industry trends and advocate for more sustainable materials and practices, even if it could make sourcing and production more complex.

Sheng: Looking ahead, what industry trends will you be keeping a close eye on in the next 1-2 years, and why?

Martha: TikTok (which already seems like old news in 2026) has been one of the biggest game changers for our business. Our products frequently gain traction on the platform, making it an incredibly valuable tool for real-time customer feedback. It’s exciting to see what resonates with consumers to quickly adapt based on those insights. We’ve also introduced TikTok Live events, which have proven highly successful at driving engagement and visibility for our products.

Sheng: Reflecting on your time at UD and in FASH, what experiences helped prepare you for your career? What advice would you give to current students as they plan their career paths, especially in the sourcing field?

Martha: The most influential experiences I had at UD were my involvement with UDress, studying abroad in Paris, and participating in the Summer Scholars program. Each of these opportunities helped shape my perspective, build my confidence, and further define my career path.

My biggest advice is to put yourself out there and take advantage of every opportunity available to you. Try new things, trust your instincts, and don’t be afraid to step outside of your comfort zone. Most importantly, stay committed and work hard. You are all capable of achieving great things!

Registration is free for students and faculty – must use university email to register (click here). [Note: Registration is NOT required for students enrolled in FASH455 this spring semester. We will participate in the event from the classroom.]

Agenda:

Tuesday, March 10, 2026

2:30 – 2:35 PM – Welcome & Opening Remarks

Kenneth Levinson, Chief Executive Officer, WITA – The International Trade Membership Association

Diego Anez, WITA Academy Executive Director, WITA Managing Director, WITA – The International Trade Membership Association

2:35 – 2:55 PM – One-on-One Career Conversation

Stephen Lamar, President & CEO, American Apparel & Footwear Association

Moderator: Kenneth Levinson, Chief Executive Officer, WITA – The International Trade Membership Association

2:55 – 3:45 PM – Panel 1: How Trade Shapes the Fashion & Apparel Industry

Yusra Siddique, Attorney, ArentFox Schiff

Julia Hughes, President, United States Fashion Industry Association

Katherine Stubblefield, Acting Division Chief, Chemicals and Textiles, Office of Industries and Competitiveness Analysis, U.S. International Trade Commission

Moderator: Alyson Demirdjian, International Trade Specialist, International Trade Administration, Office of Textiles and Apparel, U.S. Department of Commerce (Note: M.S. in Fashion and Apparel Studies, University of Delaware)

3:45 – 3:55 PM – Break

3:55 – 4:15 PM – One-on-One Career Conversation

Ed Gresser, Vice President & Director for Trade & Global Markets, Progressive Policy Institute; author of the Trade Fact of the Week; former Assistant U.S. Trade Representative for Trade Policy and Economics

Moderator: Nicole Bivens Collinson, Managing Principal, Operating Committee, International Trade & Government Relations Practice Leader, Sandler, Travis & Rosenberg, P.A.

When studying global textile and apparel sourcing, our students often focus on fashion brands and retailers—but what happens on the manufacturing side is equally critical. From tariffs and trade policies to sustainability requirements, geopolitical tensions, and technological disruption, manufacturers face complex challenges that shape the global textile and apparel supply chain.

We are fortunate to have Dr. Christian Schindler, Director General of the International Textile Manufacturers Federation (ITMF), join us for this interview. He shared invaluable insights into how manufacturers are navigating today’s dynamic environment, including:

How rising tariffs and trade policy uncertainty are affecting textile and apparel manufacturers

China’s evolving role in the textile and apparel trade, and the implications for other critical textile and apparel supplying countries

The impact of geopolitical tensions on textile and apparel production, trade patterns, and manufacturers’ risk management strategies

Near-shoring: its prospects, limitations, and the factors influencing regional textile and apparel manufacturing shifts

Sustainability, recycling, and circularity: whether textile and apparel manufacturers see these trends as compliance, opportunity, or burden

How purchasing practices by fashion brands influence labor standards, compliance, and responsible sourcing at the factory level

The growing role of AI and digitalization in textile and apparel production, and the potential impacts on workers and supply chain efficiency

Dr. Christian P. Schindler serves as Director General of the International Textile Manufacturers Federation (ITMF), the global federation representing the full textile value chain from fibres to finished apparel and home textiles. He leads ITMF’s strategy, research publications, industry conferences, and global dialogues on trade, sustainability, and technological change in textiles.

AboutEmilie Delaye (moderator)

Emilie Delaye is a master’s student & graduate instructor in Fashion and Apparel Studies at the University of Delaware, with a specific interest in supply chain, global sourcing, and sustainability. Emilie is also a member of the Fair Labor Association (FLA) 2025-2026 Student Committee and the University of Delaware President’s Student Advisory Council.

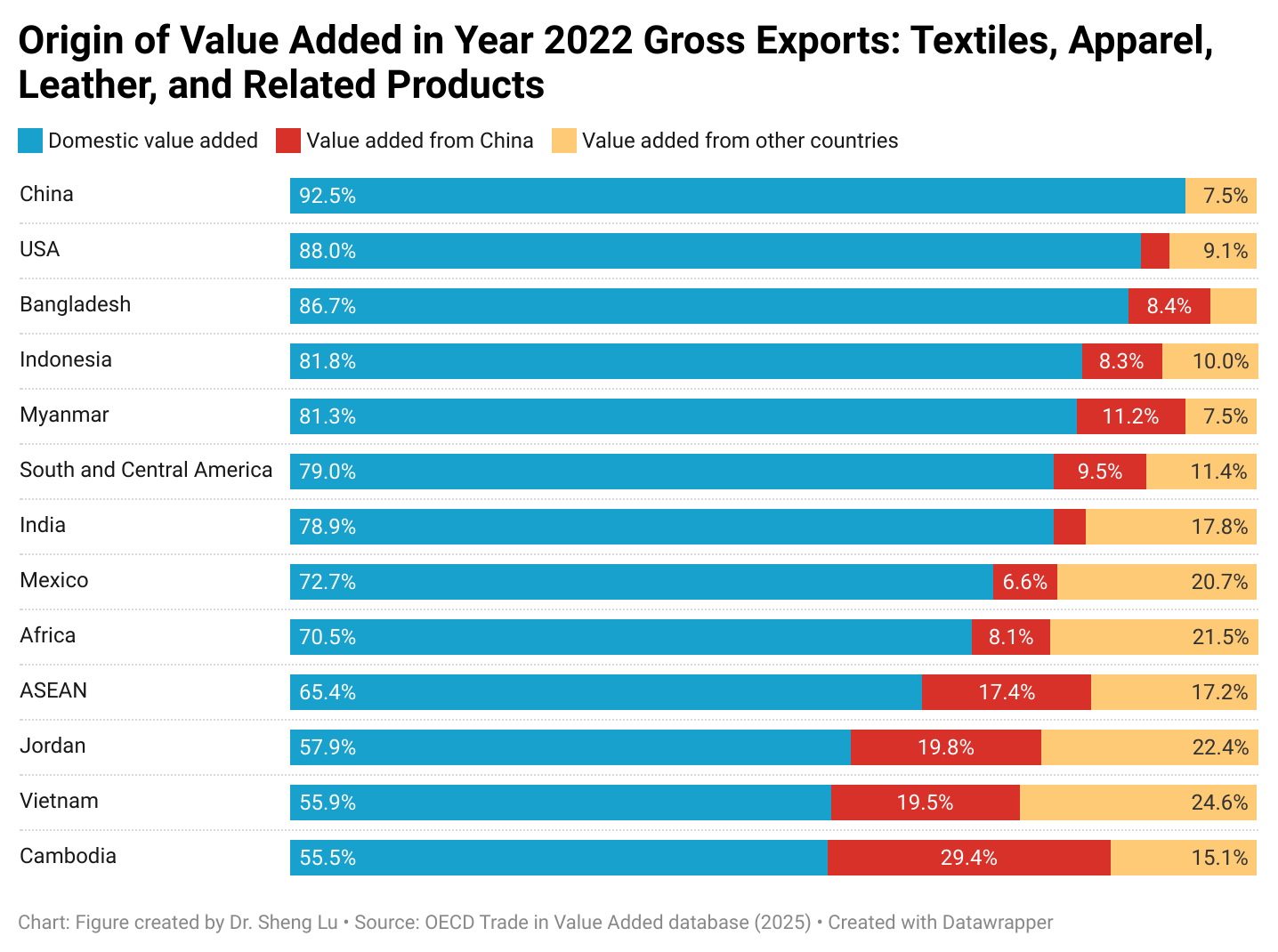

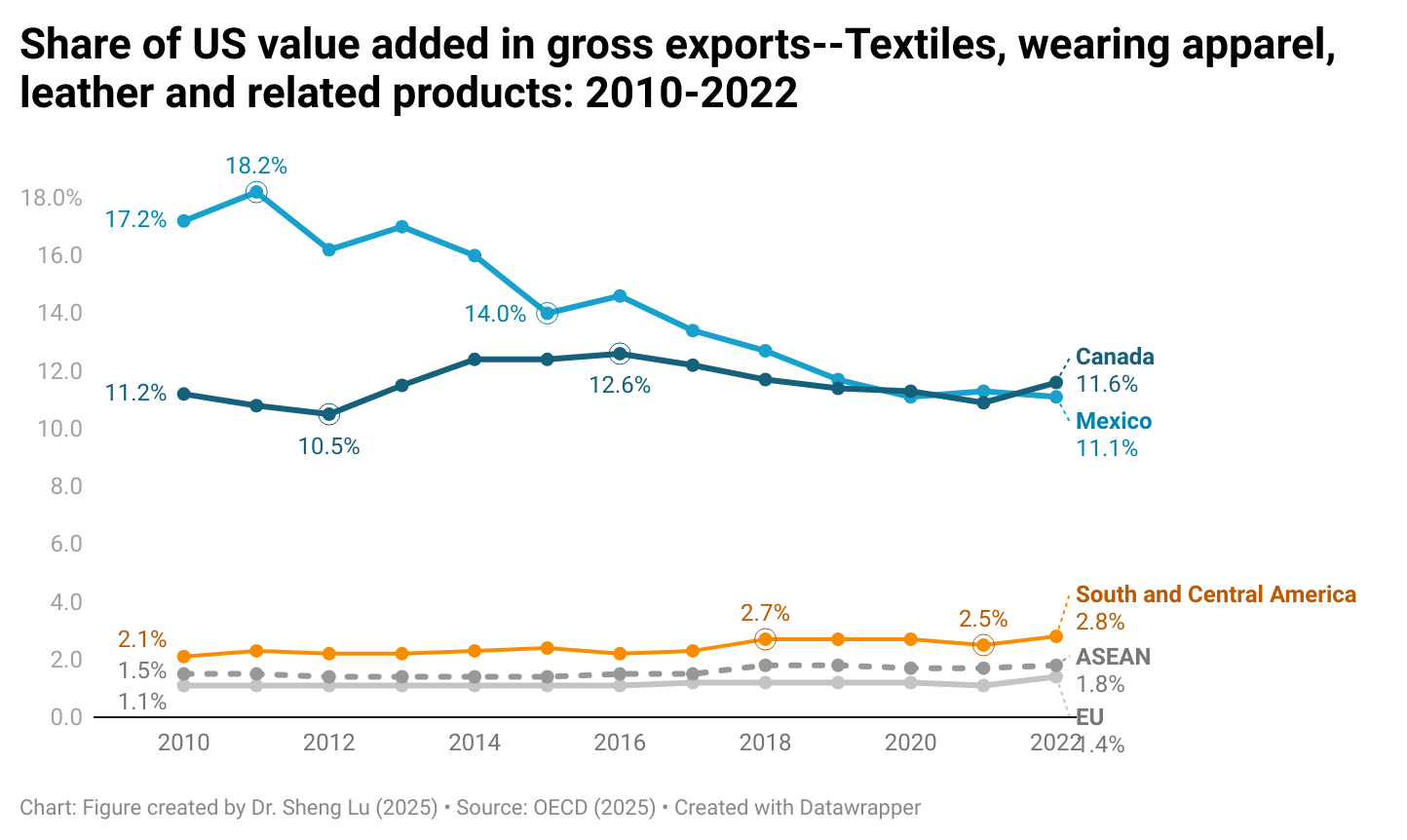

Textiles and apparel today are produced through a global supply chain. For clothing labeled as “Made in Vietnam,” it is likely that the textile raw materials, such as yarns, fabrics, and trims, are sourced from elsewhere.

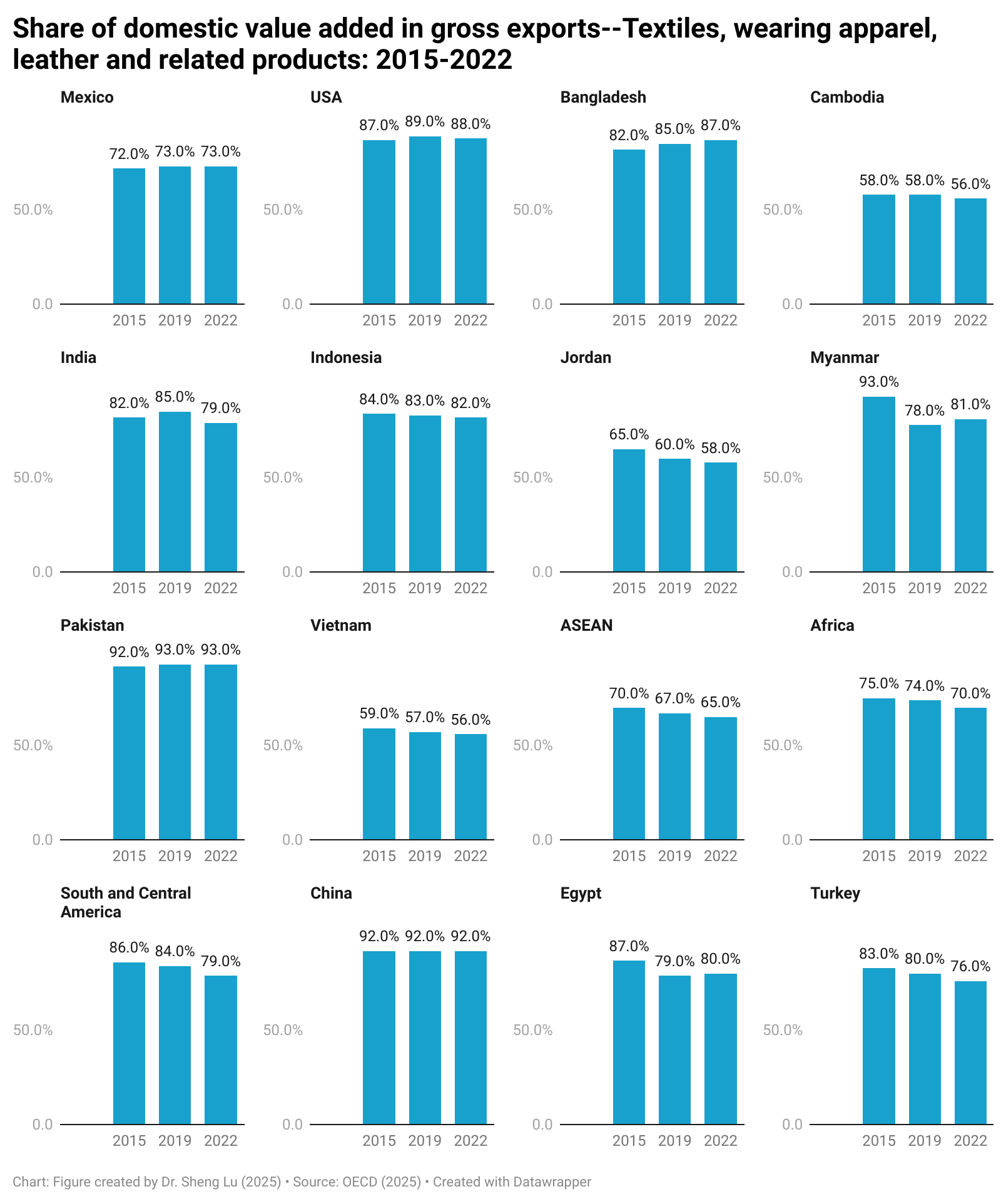

According to the newly released 2025 OECD trade in value added estimation, as of 2022, a country’s apparel exports commonly contain value added created in another country due to the use of imported textile materials and other inputs. This is the case for exports from leading apparel exporting countries in Asia, such as Vietnam (44% foreign value added), ASEAN members (35% foreign value added), Cambodia (45% foreign value added), India (21% foreign value added), and Jordan (42% foreign value added). Other emerging apparel sourcing destinations in North, South, and Central America, as well as the EU, also used substantial imported inputs for their apparel exports, such as Mexico (27.3% foreign value added), Türkiye (23.9% foreign value added), and Egypt (19.7% foreign value added). [See detailed data here]

Notably, among the sixteen countries and regions examined, they mostly increased the use of non-domestic value added in textile and apparel exports between 2015 and 2022 (note: paired T-test result was statistically significant at the 99% confidence level). This suggests that co-production through regional or global supply chains, rather than 100% domestic production, has become a more prominent phenomenon in the textiles and apparel industry. [See detailed data here]

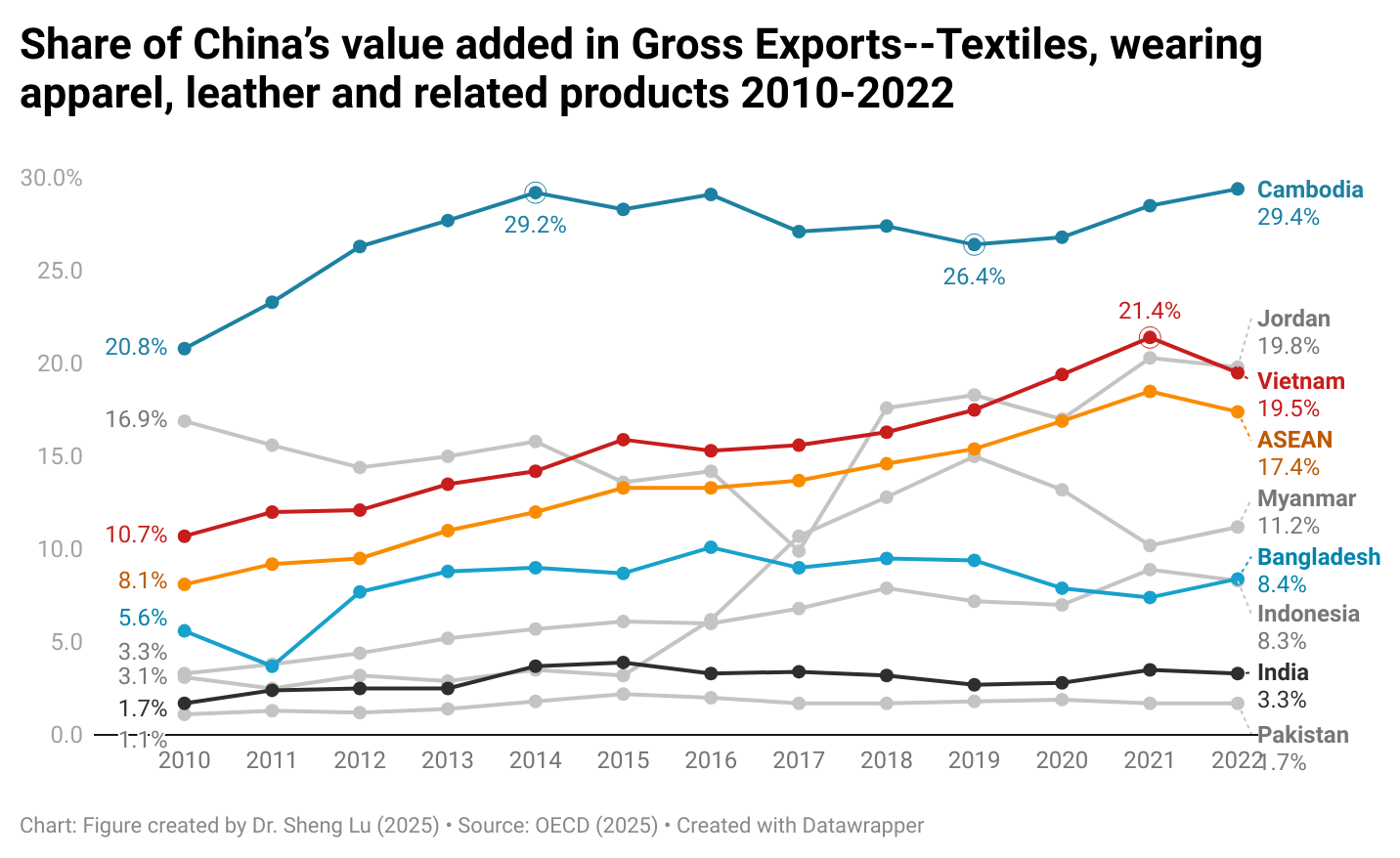

Furthermore, the value added from China appears to be increasing in the textile and apparel exports of many countries. Specifically, between 2015 and 2022, textile and apparel exports from several countries contained a higher percentage of value added from China, including not only Asian countries such as Vietnam (up 6 percentage points), ASEAN (up 4.1 percentage points) and Jordan (up 6.1 percentage points), but also those in other regions such as Egypt (up 3.3 percentage points), Mexico (up 1.7 percentage points), and South & Central America as a whole (up 4.7 percentage points). [See detailed data here] This result reflected China’s deliberate effort to expand its global economic presence through foreign direct investment, Belt and Road initiatives, and new trade agreements in recent years.

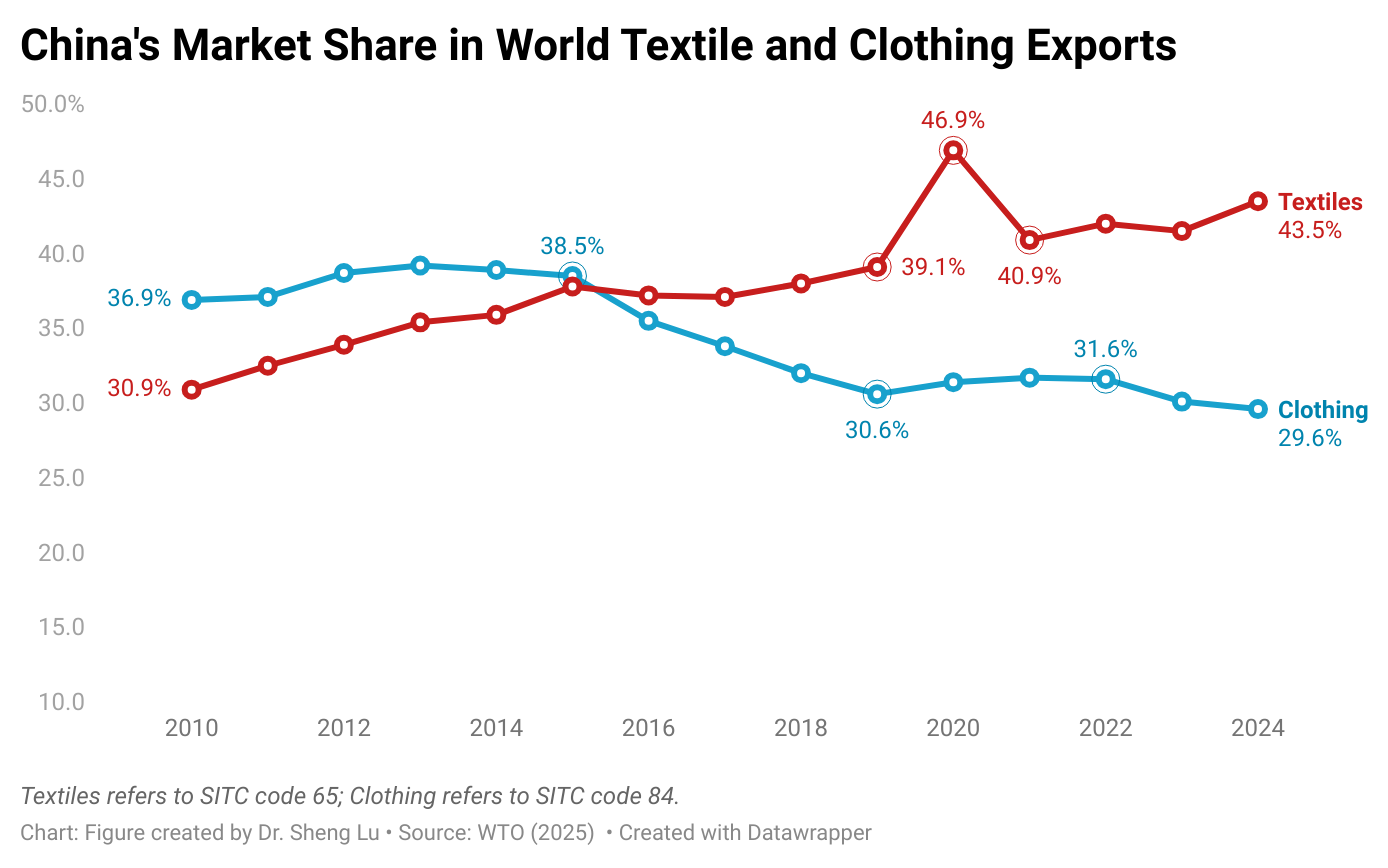

The latest data from the World Trade Organization (WTO) also shows that while China’s market share in the world clothing exports fell to 29.6% in 2024—the lowest level since 2010—China’s market share in textile exports increased to 43.3% in 2024, up from 41.5% a year earlier. In other words, consistent with the stage of development theory, China’s role as a major textile supplier to other apparel-exporting countries continues to grow, despite a decline in its finished garment exports. [See detailed data here]

In comparison, while the United States remained an important contributor to the value added of textile and apparel exports from Mexico and Canada, its contribution slightly declined between 2015 and 2022 (i.e., from about 12%-14% to 11%). As the USMCA undergoes its mandated six-year review, it is critical to strengthen, rather than weaken, this North American co-production supply chain, which has a significant impact on the economic interests of the U.S. textile and apparel industry. This is particularly important given that supply chain collaboration between the U.S. and Asian or EU countries for textile and apparel production has been limited, with little indication of growth: According to OECD data, the U.S. value added in Asian and EU countries’ textile and apparel exports remained only around 1.5% [See detailed data here].

by Sheng Lu

(This post is not open for discussion due to its technical nature)

About the interview: Fashion is possible because of international trade. Each year, the global fashion industry generates more than $4 trillion USD and provides families with affordable clothing options. However, as fast fashion continues to grow, so does awareness of pressing issues such as labor standards and environmental sustainability. How are the United States and China involved in the global fashion industry? How can they collaborate on the issues facing the global fast fashion industry, from production to consumption?

Sheng Lu joins the National Committee to discuss how fast fashion is a global phenomenon and how the United States and China can address common areas of concern.

Discussion questions [Please address at least two questions in your comment]

#1: Based on the video and our class discussion, what would be the advantages and disadvantages for Nike to make Converse shoes leveraging a global supply chain?

#2: Assume you are an experienced U.S. shoe worker. What arguments would you present to Nike’s sourcing executives to produce Converse in the United States?

#3: In your opinion, are protective tariffs worth the economic and foreign policy consequences? Why or why not?

#4: The “hidden costs” of global trade (e.g., emissions, labor conditions) are often obscured from consumers. How can brands like Converse address these “hidden costs” while maintaining market competitiveness? What specific policies or regulatory measures should governments implement to promote responsible sourcing and enhance supply chain transparency?

The event was hosted by the Washington International Trade Association on October 9, 2024

Panelists

Ralph Carter, Staff Vice President, Regulatory Affairs, FedEx

Kim Glas, President & CEO, National Council of Textile Organizations; Commissioner, U.S.-China Economic and Security Review Commission

Melissa Irmen, Director of Advocacy, NAFTZ-National Association of Foreign-Trade Zones

John Pickel, Senior Director, International Supply Chain Policy, National Foreign Trade Council

Felicia Pullam, Executive Director, Office of Trade Relations, U.S. Customs and Border Protection

Ana Swanson, Trade and International Economics Reporter, The New York Times (Moderator)

Event summary: Competing views about de minims and its reform

Arguments supporting De Minimis: Proponents like Ralph from FedEx argue that de minimis reduces trade friction, drives international supply chain efficiency, and allows U.S. companies to offer competitive pricing through free returns and streamlined customs processes. Meanwhile, they argue that the de minimis supports low-income U.S. consumers and enables small U.S. businesses to remain competitive.

Criticism of De Minimis: Critics, including Kim Glas from the National Council of Textile Organizations (NCTO), argue that it undercuts U.S. manufacturers, especially in industries like textiles, by allowing cheap imports from countries like China, often bypassing tariffs and safety regulations. They also say that de minimis was unfair to U.S. retailers that pay millions of dollars of tariff duties. Additionally, there are significant concerns about the safety risks posed by counterfeit goods and dangerous products (e.g., fentanyl) entering under de minimis exemptions.

Challenges of dealing with de Minimis: Felicia from the U.S. Customs and Border Protection (CBP) emphasizes the strain on the agency’s resources due to the sheer volume of de minimis shipments—it surged from about 2.8 million shipments per day in fiscal year 2023 to close to 4 million shipments per day in fiscal year 2024. She highlighted challenges such as the often unreliable information the de minimis imports submitted and the outdated authorities that hinder CBP’s enforcement.

Equal treatment for U.S. Foreign Trade Zones: U.S. Foreign Trade Zones (FTZs) are designated areas within the United States that are considered outside U.S. customs territory for import duties. They allow businesses to import, store, assemble, manufacture, or process goods with deferred or reduced customs duties, which are only paid when goods leave the FTZ and enter U.S. commerce. Currently, U.S. FTZs do not benefit from the de minimis exemption, meaning goods imported directly into the U.S. from overseas warehouses can qualify for de minimis, but goods entering through U.S. FTZs do not.

Melissa Irmen from NAFTZ-National Association of Foreign-Trade Zones advocates for U.S. foreign trade zones to be given the same de minimis privileges as foreign warehouses, arguing that this would ensure better oversight and security while maintaining trade efficiency. Critics, however, say that expanding de minimis in this way would exacerbate the problem rather than fix it.

Reforming the De minimis: There is a push for comprehensive reform of the De minimis system, with proposals ranging from raising duties on certain products to eliminating the exemption altogether for specific categories of goods (e.g., textiles, products subject to Section 301 tariffs).

Particularly, in a face sheet released in September 2024, the Biden Administration announced it would address “the significant increased abuse of the de minimis exemption, in particular China-founded e-commerce platforms.” The announcement said the Biden Administration would issue a Notice of Proposed Rulemaking that would exclude from the de minimis exemption all shipments containing products covered by tariffs imposed under Sections 201 or 301 of the Trade Act of 1974, or Section 232 of the Trade Expansion Act of 1962. The announcement also called for Congress to pass new legislation to reform the de minimis rule comprehensively.

FASH455 Learning activity: After watching the two video above, please explore the following topics with the assistance of ChatGPT or other generative AI tools:

The significance and complexity of container shipping for U.S. fashion brands and retailers

Current issues related to container shipping for U.S. fashion brands and retailers

In your response, please include the following elements:

Questions: list at least three questions you asked ChatGPT or other AI tools that helped generate the most information and insights.

Summary and reflections: summarize the key points from the answers you received from the AI tool and share your reflections (e.g., were there any surprising insights? the outlook for the issues discussed)

Further Reading: Suggest 1-2 additional articles from national or international press that offer deeper insights into the topics. The readings need to be published after 2024. Please share the article link and briefly explain why you recommend them.

Speaker: Dr. Deborah Elms, Founder and Executive Director of the Asian Trade Centre and the President of the Asia Business Trade Association. The clip was part of the webinar “Asia’s Noodle Bowl Of Trade” (March 2023).

Background

The Asia-Pacific region includes several mega free trade agreements:

ASEAN (Association of Southeast Asian Nations) is a regional intergovernmental organization comprising ten countries in Southeast Asia (Brunei, Cambodia, Indonesia, Laos, Malaysia, Myanmar, the Philippines, Singapore, Thailand, and Vietnam). In 2022, ASEAN members have a combined nominal GDP of $3.6 trillion and a population of 671.6 million.

CPTPP (Comprehensive and Progressive Agreement for Trans-Pacific Partnership) is a free trade agreement signed by 11 countries in the Asia-Pacific region, including Japan, Malaysia, Vietnam, Australia, Singapore, Brunei, New Zealand, Canada, Mexico, Peru, and Chile. The CPTPP covers a market of 495 million people with a combined GDP of $13.5 trillion in 2021. The United States was originally a participant in the Trans-Pacific Partnership (TPP) negotiations, but in January 2017, former US President Trump withdrew the US from the agreement. The Biden administration has indicated no interest in rejoining CPTPP. Additionally, China is actively seeking to join CPTPP (as of March 2024).

RCEP (Regional Comprehensive Economic Partnership) is a free trade agreement signed by 15 countries in the Asia-Pacific region, including China, Japan, South Korea, Australia, New Zealand, Brunei, Cambodia, Indonesia, Laos, Malaysia, Myanmar, the Philippines, Singapore, Thailand, Vietnam. In 2021, RCEP members collectively represented a market of 2.3 billion people with a combined GDP of $26.3 trillion. India was an RCEP member but withdrew from the agreement due to concerns about import competition with China.

IPEF (Indo-Pacific Economic Framework for Prosperity) is a US-led economic cooperation framework that aims to “link major economies and emerging ones to tackle 21st-century challenges and promote fair and resilient trade for years to come.” IPEF is NOT a traditional free trade agreement, and it does not address market access issues like tariff cuts. Instead, IPEF includes four pillars: trade, supply chains, clean economy, and fair economy. IPEF members in the Asia-Pacific region include the United States, Japan, Australia, New Zealand, South Korea, India, Fiji, Brunei, Indonesia, Malaysia, the Philippines, Singapore, Thailand, and Vietnam. The IPEF is designed to be flexible, meaning that IPEF partners are not required to join all four pillars. For example, India chooses not to join the trade pillar of the framework. In 2021, IPEF countries collectively represented a market of 2.1 billion people with a combined GDP of $23.3 trillion. The potential economic impact of IPEF remains too early to tell.

Notably, ASEAN, CPTPP, RCEP, and IPEF members play significant roles in the world textile and apparel trade. Specifically:

ASEAN and RCEP members have established a highly integrated regional textile and apparel supply chain. For example, a substantial portion of ASEAN and RECP members’ textile imports came from within the region.

ASEAN and RCEP members’ supply chain connection with China has substantially strengthened over the past decade. In contrast, the US barely participated in Asia-based textile and apparel supply chains. For example, other than CPTPP, the US accounted for less than 2% of ASEAN, RCEP, and IPEF members’ textile imports in 2022.

ASEAN and RCEP members also hold significant market shares in the world textile and apparel exports (over 50%). Meanwhile, the US and EU are indispensable export markets for ASEAN and RCEP members.

Because of the inclusion of the United States, IPEF represented one of the world’s largest apparel import markets (i.e., 33.7% in 2021, measured in value). Similarly, in 2022, about 26% of US apparel imports came from current IPEF members. Should IPEF address market access issues, it could offer significant duty-saving opportunities for textile and apparel products.

Additionally, the UK’s membership in CPTPP may have a limited direct impact on the textile and apparel sector, at least in the short to medium terms. For example, current CPTPP members only accounted for about 6% of the UK’s apparel imports in 2022.

The new study released by Mckinsey & Co. was based on a survey of chief procurement officers (CPOs) from “apparel companies that collectively spend about $110 billion annually on sourcing” and follow-up in-depth interviews with 25 CPOs conducted in late 2023. Key findings:

#1 Fashion companies face increasingly challenging sourcing scenarios complicated by “ongoing supply disruptions caused by shifting demand, material price volatility, geopolitics, global trade issues, rising competition, and regulatory changes.” Compared to many other sectors, the apparel supply chain is particularly volatile, and disruptions can have amplified ripple effects throughout the supply chain. For example, an 11% decline in yarn exports could lead to a 30% drop in the production utilization rate of fabric mills.

#2 Fashion companies further prioritized “end-to-end” process efficiency in response to the shifting sourcing environment. For example, nearly 70 percent of respondents expect to “improve sourcing cost in the near term,” they plan to “improve efficiency across all facets of sourcing, including lower product costs, reduced sourcing expenses, and accelerated go-to-market processes.” Other practices to control sourcing costs include “using analytics to examine product cost breakdowns and identifying opportunities to improve fabric unit costs and material consumption,” “using digital platforms and data-driven insights to inform sourcing decisions and collaborating with suppliers to pinpoint cost savings opportunities.”

#3 Strengthening relationships with key suppliers remains critical. About 71 percent of surveyed brands consider “consolidating the supplier base” a medium to high priority for their strategy in the next five years. Surveyed fashion companies also indicate that deeper relationships, including “long-term volume commitments, shared strategic three- to five-year plans, and collaboration partnerships,” accounted for 43 percent of their total apparel supplier base in 2023, up from 26 percent in 2019. In comparison, suppliers based on “transactional relationships” only accounted for 3% of the total in 2023, a substantial decrease from 22% in 2019.

As the report noted, building strategic partnerships with core suppliers and “innovative niche suppliers” based on trust and transparency “resulted in a more robust, resilient, and agile supplier base” for fashion companies. More importantly, deeper importer-supplier partnerships extend beyond cost-saving measures but increasingly emphasize “sustained value creation.”

#4 Fashion companies continue to diversify their sourcingbasegeographically and pursue nearshoring to “improve speed, cost, and agility.” Specifically, between 2019 and 2023, respondents reduced their sourcing value from China (down from 30% to 22%) and sourced more from South Asia (up from 23% to 34%). At the country level, more than 40 percent of respondents plan to further increase sourcing from Bangladesh, India, and Vietnam. That being said, the report found that nearshoring remains “flat” in sourcing value in the US (about 17%) and in the EU (about 25%) from 2019 to 2023.

#5 To expand apparel nearshoring, several bottlenecks remain to be solved: 1) lower labor productivity in the region resulting in higher “total landed costs,” 2) challenges with yarn and fabric availability, and 3) the supplier bases in nearshoring countries can manufacture a more limited array of products.

The report also noted that “both local suppliers and Asian companies with a presence in Central America and Mexico have invested in improving their productivity and building local capacity for making yarns and fabrics,” which is helpful in addressing the challenges.

#6 Sustainability will continue to affect fashion companies’ sourcing decisions. For example, 80 percent of respondents said that “environmental, social, and governance certifications; transparency and traceability; and sustainable material usage have become prerequisitesin supplier selection.” Fashion companies commonly used scorecards (92 percent) and third-party audits (78 percent) to ensure suppliers’ compliance with sustainability requirements. There is also an increasing need for data transparency on sustainability. However, “data is important, but organizations must understand how to use it to create value.”

Further, 86 percent and 70 percent of respondents said they would use recycled polyester and recycled cotton in their apparel products over the next five years.

#7 Digital innovation will deepen further in the sourcing and product development area. Popular tools include 3D modeling and digital sampling, Fabric libraries, and Product Lifecycle Management (PLM) system. However, prioritizing process redesign, data quality enhancement, and the integration of systems are essential to enable efficient operations. For example, one company developed a single material ID library with more than 30,000 materials from approximately 300 suppliers, allowing the company to aggregate more than 6,000 cost sheets in less than a minute.

Megan Dawson-Elli graduated from the University of Delaware (UD) in 2016 with a degree in Fashion Merchandising. During her time at UD, she was the winner of the Fashion Scholarship Fund case study, a highly competitive national competition. Early in her academic career, she identified her interest in environmental sustainability within the fashion industry. This inspired Megan to study abroad in Hong Kong in 2014, where she was a Sourcing & Sustainability intern for Under Armour. After graduation, Megan worked in merchandising and sourcing before starting her career in environmental sustainability at PVH in 2018. Presently, Megan holds the position of Product Sustainability Manager at Tapestry, where she leads their work on product impact, environmentally preferred materials, and circularity.

In her free time, Megan enjoys reading, running, and traveling. She lives in NYC with her fiancé, also a UD graduate, and likes spending her weekends in Central Park.

Disclaimer: The views expressed in this interview are those of Megan Dawson-Elli and do not reflect the views or positions of her employer or any affiliated organizations.

Sheng: What does a Product Sustainability Manager do? Can you walk us through your typical day at Tapestry? Also, what makes you love your job?

Megan: As a Product Sustainability Manager, I work as an internal consultant to our brands to support their progress towards our Environmental, Social and Governance (ESG) goals and their desire to market and evaluate the environmentally preferred attributes of our products. Many initiatives fall under Product Sustainability, but I would bucket most of the work into several categories: marketing claims substantiation, environmentally preferred materials, product impact, circularity, and packaging. Every day can look different in this role, which keeps it exciting! One day I will be working with teams to craft a marketing claim about a product and the next I will be collecting data from suppliers for a life cycle assessment. My work is very dynamic, with some projects lasting days versus months. I love my job because I get to work with teams across the company that are passionate about sustainability, and even though I no longer work to create products, it’s still the focus of my work.

Sheng: Consumers today, especially our Gen Z students, want to see more “sustainable” fashion products in the market. What does “sustainable product” mean in practice? Can “sustainability” be objectively measured?

Megan: The term “sustainable” has become difficult to define as many initiatives can fit under it, like environmentally preferred materials, responsible sourcing, circularity, etc. It can also be seen as a yes/no question, while sustainability is a journey where progress should grow as new innovations become available. At a product level, the most visible sustainability initiatives that can be seen are environmentally preferred materials or social impact claims being made about the item. There are plenty of initiatives that companies are doing across their supply chain and their operations. Checking out a company’s annual Corporate Responsibility report will show a greater picture of its efforts, commitments, and progress.

Sheng: How can sourcing contribute to a fashion company’s sustainability efforts and make more sustainable products available to consumers?

Megan: At Tapestry, we follow an internal framework known as “Style, Performance and Impact.” This ensures all products meet our high standards of craftsmanship. The framework also guides our decision-making around environmentally preferred materials and material innovation investments.

Style: Does it meet design needs or the intended design function of the product?

Performance: Does it meet expectations of quality and cost?

Impact: Does the material or decision have a measurable reduction in environmental impact?

Additionally, suppliers play a critical role in helping companies realize their environmental and social ambitions. We consistently partner with stakeholders across our value chain to work toward more responsible practices that their businesses can incorporate, especially through increased implementation of environmentally preferred manufacturing practices and using preferred materials.

Sheng: Related to sustainability are the buzzwords “supply chain transparency” and “traceability.” What progress has been made, and what are the key steps for fashion companies in achieving greater transparency and traceability in their supply chains and sourcing?

Megan: To ensure a more responsible and transparent supply chain, it is critical to map supply chains and the relationships between suppliers. At Tapestry, we have begun the process of onboarding suppliers to join TrusTrace, a cloud-based web platform for sustainability, where we intend to conduct more upstream supply chain mapping and the collection of documentation to establish material and product traceability. We envision the platform will help us meet enterprise-wide sustainability commitments and goals, and help us align with upcoming regulatory requirements and industry best practices.

We have also improved downstream traceability by launching a digital product passport program, most notably through Coachtopia products. Customers can hold their smartphones against the cloud emblem on their Coachtopia product until the pop-up appears and then learn the total environmental impact of the product, along with all the potential avenues to extend its useful life under the sub-brand’s circular principles.

Sheng: As legislation related to fashion companies’ sustainability practices continues to be newly implemented or is on the horizon, are there any specific regulations you would recommend our students closely monitor?

Megan: There are many emerging ESG regulations, especially in Europe. Below are some that would be interesting to review.

Sheng: Any reflections on your experiences at UD and FASH? What advice would you offer to current students preparing for a career in fashion sustainability after graduation?

Megan: My “lightbulb moment” for wanting to pursue a career in sustainability happened while I was at UD, specifically from taking the ethics and sustainability in the fashion industry class. After identifying environmental sustainability as my focus and passion, I found ways to include it in every project, case study, and internship during school. The great thing about sustainability is that every department in a company can be part of the collective efforts, so even if you aren’t on an ESG (Environmental, Social, Governance) team, you can make an impact. If you are specifically interested in pursuing a role on an ESG team, I recommend networking with people in the industry that have those roles to learn more about what the job looks like and staying up to date on the latest news, innovations and regulations in the space. Also, there are plenty of college courses and industry certifications in sustainability that can be a great learning resource.

Students in FASH455 have proposed the following discussion questions based on the videos about the state of textile and apparel in Asia. Everyone is welcome to join the online discussion. For FASH455 students, please address at least two questions and mention the question number (#) in your reply.

#1 We have seen all the improvements and “upgrading” Vietnam has made toward the fashion industry. What can the garment industry in other countries take away from Vietnam’s experiences?

#2 Is Asia’s highly integrated apparel supply chain unique to the region? Can the Western Hemisphere “copy” Asia’s model?

#3 How can Asia’s textile and apparel industry balance the growing demand for sustainability and the need to remain cost-competitive? What innovative strategies can be adopted to achieve this balance?

#4 As Asian textiles and apparel factories continue to improve their efficiency and expand product offers, will it be beneficial for the US to reach a trade agreement with Asian countries? Or do you believe such an agreement might contradict the goals we try to achieve from CAFTA-DR?

#5 Will Vietnam eventually become the next China, or could its labor shortages be a significant barrier preventing its textile and apparel industry from advancing to the next level?

#6 Should textile and garment factories in Asia make more efforts to appeal to the younger generation (e.g., Gen Z)? Or is automation the solution?

#7 To what extent do you think Asian apparel exporting countries (e.g., Bangladesh, Vietnam and Cambodia) will reduce their dependence on textile raw materials supply from China due to the Uyghur Forced Labor Prevention Act (UFLPA)? Or, instead, do you think Asian apparel-exporting countries other than China benefit from UFLPA?

#8 The video shows that Asian countries have begun to invest heavily in new production capacities for textile recycling. Do you believe the region will continue to dominate textile and apparel production in the era of fashion circularity? Or will the emergence of textile recycling shift the world textile and apparel trade patterns in the long run?

Julia K. Hughes is President of the United States Fashion Industry Association (USFIA), which represents brands, retailers, importers, and wholesalers based in the United States and doing business globally. She represents the industry in front of the U.S. government as well as international governments and stakeholders, explaining how fashion companies create high quality jobs in the United States and economic opportunities around the world.

An expert on textile and apparel trade issues, Julie has testified before Congress and the Executive Branch. She frequently speaks at international conferences including the China & Asia Textile Forum, Fashion Institute of Technology (FIT), Harvard University’s Bangladesh Development Conference, MAGIC, Prime Source Forum, Vietnam Textile Summit, and others.

Julie served as the first President and is one of the founders of the Washington Chapter of Women in International Trade (WIIT) and is one of the founders of the WIIT Charitable Trust. She also was the first President of the Organization of Women in International Trade (OWIT). In 1992, she received the Outstanding Woman in International Trade award and in 2008, the WIIT Lifetime Achievement Award. She also is a member of the International Women’s Forum.

Julia has an M.A. in International Studies from the Johns Hopkins School of Advanced International Studies and a B.S. in Foreign Service from Georgetown University.

The interview was conducted by Leah Marsh, a graduate student in the Department of Fashion and Apparel Studies at the University of Delaware. Leah’s research focused on exploring EU retailers’ sourcing strategies for clothing made from recycled textile materials and fashion companies’ supply chain and sourcing strategies.

Discussion questions: What factors contribute to the complexity of eliminating banned Xinjiang cotton from the apparel supply chain? How can the current efforts be enhanced to better address the situation and by whom? Feel free to share any other reflections on the video and the graphs.

#1 What are the examples of globalization in the above two videos about Temu?

#2 Based on the videos, who are the winners and losers of globalization and why?

#3 What role does international trade play in Temu’s business model?

#4 Some suggest ending the “de minimis rule.” Based on the videos, what is your view and recommendation for US policymakers?

#5 Anything you find interesting/surprising/intriguing in the video and why?

(Note: Anyone is welcome to join the discussion. For students in FASH455, please address at least two questions. Please mention the question number in your response, but there is no need to repeat the question).

Note: About “de minimis rule.”: Under US customs law, specifically the Trade Facilitation and Trade Enforcement Act of 2015, import duties are generally waived for goods valued at $800 or less per person per day. Therefore, Temu’s shipping from China to US consumers is likely to be eligible for the benefits.

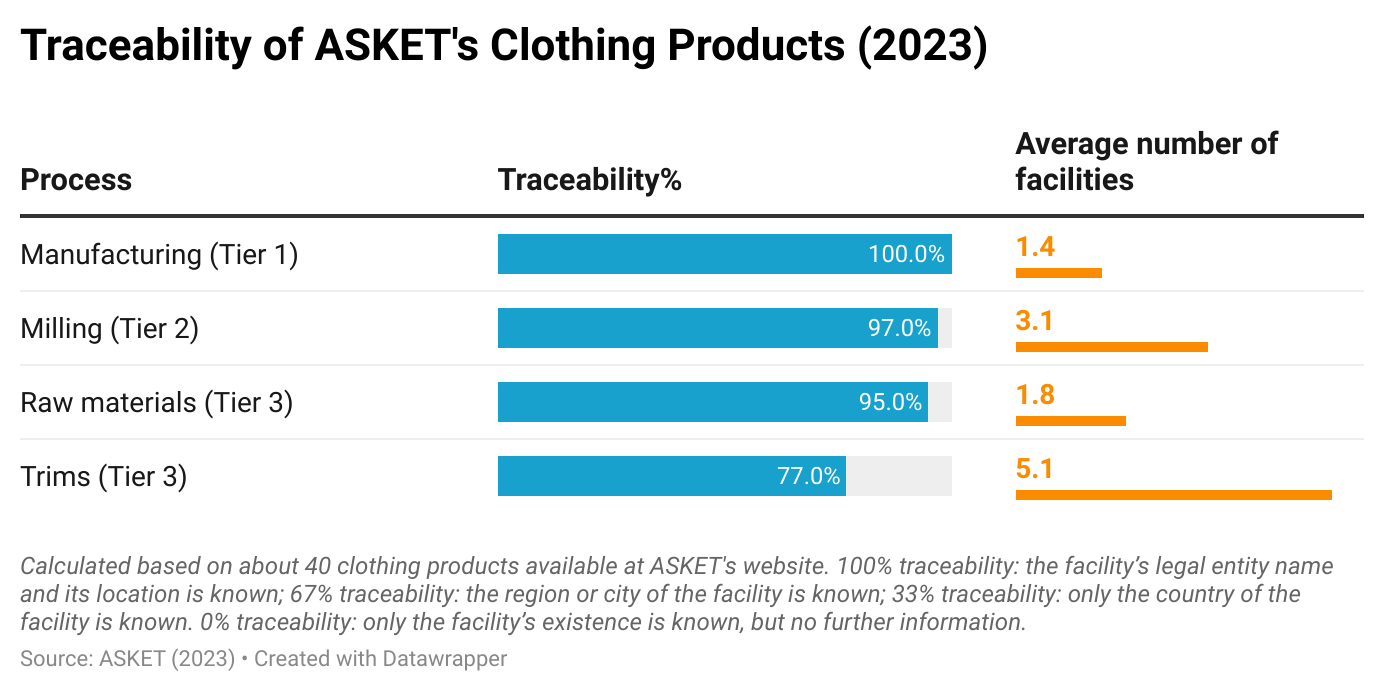

ASKET is a prominent online retailer based in Sweden that commits to complete supply chain transparency. Based on analyzing nearly 40 unique products and their detailed supply chain information posted on ASKET’s website as of May 2023, the article aims to shed light on the company’s supply chain traceability progress and the remaining challenges it faces.

First, while ASKET achieved full traceability for Tier 1 suppliers, tracking Tier 2 and Tier 3 suppliers was more difficult. For example, compared with its perfect traceability score for Tier 1 suppliers (i.e., garment factories), ASKET’s average traceability for Tier 2 Milling factories (i.e., yarn and fabric producers) was at around 97%, and the score fell to only 77% for trims suppliers in Tier 3.

As one critical contributing factor to the phenomenon, Tier 2 and Tier 3 suppliers had far more players than Tier 1, which presented a more significant challenge inobtaining detailed information about all the factories involved. For example, ASKET’s garment cutting and sewing operations predominantly occurred within a single facility. In contrast, making yarns, fabrics, and trims EACH usually involve multiple facilities in different parts of the world.

Second, a comprehensive understanding of the sub-supply chains associated with apparel components is pivotal in enhancing a fashion company’s overall traceability. Notably, the apparel supply chain is far more complicated than the commonly known four stages—fiber, yarn, fabric, and garment manufacturing. Rather, apparel components like yarns, fabrics, sewing threads, buttons, and zippers have complex and intricate sub-supply chains. For instance, for ASKET’s shirts or polo shirts:

Cotton was “farmed in New Mexico, Arizona, California and Texas, USA, ginned in Anqing, China.”

Yarn was “spun and twisted in Hyderabad, India,” and “dyed in Varese, Italy.”

Fabric was “woven in Letohrad, Czech Republic, dyed and finished in Prato, Italy.”

Sewing thread was “produced in Breisgau, Germany, wound and packed in St. Maria de Palautordera, Spain”

Button was produced in Saccolongon, Italy, with corozo farmed in Manabi, Ecuador.

Third, using recycled textile materials in apparel products could make it trickier to map the supply chain.

ASKET reported no problem tracking recycled textile materials derived from natural fibers, especially recycled wool products.

ASKET’s capability of tracing recycled man-made fiber textiles yielded mixed results. For example, ASKET was still investigating the Tier 3 raw material suppliers for one fabric made with “100% pre-consumer recycled nylon.” Likewise, for one body fabric derived from “plastic waste collected from Spanish Mediterranean and French Atlantic oceans and coastlines,” pinpointing the precise origin of the raw fiber posed a challenge.

Fourth, ASKET’s data shows that using recycled textiles in apparel products could incur higher transportation costs. For example, the average transportation cost for an ASKET garment using recycled textiles would reach $5 per unit (or 6.3% of the total production costs), much higher than regular clothing using non-recycled materials ($1 per unit or 3% of the total production). However, on average, making a garment using recycled textile materials could involve fewer facilities(e.g., 9 vs. 12). This result suggests that the higher transportation cost associated with clothing made from recycled textiles may not be attributed to a longer supply chain but rather to a more tedious and expensive recycled fiber collection process.

Additionally, ASKET’s data indicates a strong correlation between its retail price and sourcing costs. Specifically, ASKET’s applied a gross margin% ranging from 71%–81%. This implies that a $2 increase in sourcing costs could potentially lead to a retail price increase of $10-$20. Thus, controlling and managing sourcing costs will always be a priority for a fashion company.

Background: What sets Shein and Temu’s sourcing strategies apart from other US fashion brands?

Leading US fashion companies have increasingly turned to sourcing diversification to reduce supply chain risks and market uncertainties. For example, industry surveys and firm-level analyses consistently found that prominent US fashion brands and retailers typically source from more than 10-20 countries. Notably, “reducing China exposure” is a growing trend among US fashion companies, given the concerns about the rising US-China trade tensions and geopolitics.

Instead, Temu and Shein are notable for their reliance on Chinese suppliers, with Temu primarily shipping products directly from China rather than US-based distribution centers. This business model may be explained by two factors.

One is to leverage China’s strengths in making apparel products with greater varieties and smaller quantities. In other words, while countries like Bangladesh and Cambodia may be better suited for sourcing large orders, “Made in China” can remain overall price competitive for a wide range of products requiring a smaller minimum order quantity. In this way, China can offer greater flexibility to Temu, which intends to manufacture various products while controlling costs.

Another possible reason is to take advantage of the “de minimis rule.” Under US customs law, specifically the Trade Facilitation and Trade Enforcement Act of 2015, import duties are generally waived for goods with a value of $800 or less per person per day. Therefore, Temu’s shipping from China to US consumers is likely to be eligible for the benefits.

Discussion question: What shall we do about Shein?

In March 2023, the Office of the United States Trade Representative (USTR) released its 2024 Fiscal Year Budget report, outlining six major goals and objectives for FY2024. USTR’s FY2024 goals and objectives for textile and apparel are similar to FY2023, but keywords such as “near-shoring” are newly emphasized.

Goal 1: Open Foreign Markets and Combat Unfair Trade

Provide policy guidance and support for international negotiations or initiatives affecting the textile and apparel sector to ensure that the interests of U.S. industry and workers are taken into account and, where possible, to provide new or enhanced export opportunities for U.S. industry. (Note: no change from FY2023)

Conduct reviews of commercial availability petitions regarding textile and apparel products and negotiate corresponding FTA rules of origin changes, where appropriate, in a manner that takes into account market conditions while preserving export opportunities for U.S. producers and employment opportunities for U.S. workers. (Note: no change from FY2023)

Engage relevant trade partners to address regulatory issues potentially affecting the U.S. textile and apparel industry’s market access opportunities. (Note: no change from FY2023)

Continue to engage with CAFTA-DR partner countries to address trade-related issues to optimize inclusive economic opportunities; strengthen trade rules and transparency and address non-tariff trade impediments; provide capacity building in areas such as textile and apparel trade-related regulation and practice on customs, border and market access issues, including agricultural and sanitary and phytosanitary regulations, to avoid barriers to trade. (note: newly mentioned “transparency”)

Continue to engage CAFTA-DR partners and stakeholders to identify and develop means to increase two-way trade in textiles and apparel and strengthen the North American supply chain and near-shoring to enhance formal job creation. (note: newly emphasized “Near-shoring”)

Provide policy guidance and support for international negotiations or initiatives affecting the textile and apparel sector to ensure that the interests of U.S. industry and workers are taken into account and, where possible, to provide new or enhanced export opportunities for U.S. industry. (Note: no change from FY2023)

Conduct reviews of commercial availability petitions regarding textile and apparel products and negotiate corresponding FTA rules of origin changes, where appropriate, in a manner that takes into account market conditions while preserving export opportunities for U.S. producers and employment opportunities for U.S. workers (note: no change from FY2023)

Engage relevant trade partners to address regulatory issues potentially affecting the U.S. textile and apparel industry’s market access opportunities. (note: no change from FY2023)

Goal 2: Fully Enforce U.S. Trade Laws, Monitor Compliance with Agreements, and Use All Available Tools to Hold Other Countries Accountable

Closely collaborate with industry and other offices and Departments to monitor trade actions taken by partner countries on textiles and apparel to ensure that such actions are consistent with trade agreement obligations and do not impede U.S. export opportunities. (note: no change from FY2023)

Research and monitor policy support measures for the textile sector, in particular in the PRC, India, and other large textile producing and exporting countries, to ensure compliance with international agreements. (note: no change from FY2023)

Continue to work with the U.S. textile and apparel industry to promote exports and other opportunities under our free trade agreements and preference programs, by actively engaging with stakeholders and industry associations and participating, as appropriate, in industry trade shows. (note: no change from FY2023)

Goal 4: Develop Equitable Trade Policy Through Inclusive Processes

Take the lead in providing policy advice and assistance in support of any Congressional initiatives to reform or re-examine preference programs that have an impact on the textile and apparel sector. (note: no change from FY2023)

Other Priorities for USTR in FY2024:

#1 “Advancing a Worker-Centered Trade Policy.” For example, given “communities of color and lower socio-economic backgrounds were more negatively affected by free trade policies that have reduced tariffs and distributed supply chains across the globe,” USTR will develop “a new strategic approach to trade relationships that is not built on traditional free trade agreements…USTR is embarking on trade engagements with allies and like-minded economies, like Taiwan and Kenya and [through] multinational economic frameworks that focus on clean energy and supply chains rather than tariffs.”

#2 Address forced labor. For example, USTR developed the first-ever focused trade strategy to combat forced labor. Paired with the implementation of the Uyghur Forced Labor Prevention Act, and the Memorandum of Cooperation (MOC) launching of a Task Force on the Promotion of Human Rights and International Labor Standards in Supply Chains under the U.S.-Japan Partnership on Trade. And USTR will “use every tool available to block the importation of goods made partially or entirely with forced labor.”

#3 Re-Aligning the U.S. – Beijing Trade Relationship. “USTR continues to keep the door open to conversations with the PRC, including on its Phase One commitments. However, USTR acknowledges the Agreement’s limitations. USTR’s strategy is expand beyond only pressing Beijing for change and includes vigorously defending our values and economic interests from the negative impacts of the PRC’s unfair economic policies and practices.”

#4 Strengthen enforcement of US trade policy. For example, USTR sees enforcement “a key component of our worker-centered trade policy.” USTR is “upholding the eligibility requirements in preference programs,” such as the African Growth and Opportunity Act (AGOA). As many enforcement tools were “were crafted decades ago,” USTR will be “reviewing our existing trade tools and working with Congress to develop new tools as needed.”

The session intends to facilitate constructive dialogue regarding the latest progress, challenges, and opportunities for achieving more sustainable and socially responsible apparel sourcing in the Post-COVID world. The session will offer a unique opportunity to hear directly from leading fashion brands and retailers regarding 1) fashion companies’ latest sourcing practices against the evolving business environment and their impacts on due diligence; 2) fashion companies’ new efforts and innovative projects to achieve more sustainable and socially responsible apparel sourcing; 3) opportunities and challenges to further improve sustainability and social responsibility in apparel sourcing in the post-COVID world. In addition, the session will be highly relevant and informative to all stakeholders in the fashion apparel business community, civil society, international organizations, academia, and policymakers.

This study aims to understand western fashion brands and retailers’ latest China apparel sourcing strategies against the evolving business environment. We conducted a content analysis of about 30 leading fashion companies’ public corporate filings (i.e., annual or quarterly financial reports and earnings call transcripts) submitted from June 1, 2022 to December 31, 2022.

The results suggest several themes:

First, China remains one of the most frequently used apparel sourcing destinations. For example:

Express says, “The top five countries from which we sourced our merchandise in 2021 were Vietnam, China, Indonesia, Bangladesh and the Philippines, based on total cost of merchandise purchased.”

According to TJX, “a significant amount of merchandise we offer for sale is made in China.”

Children’s Place says, “We source from a diversified network of vendors, purchasing primarily from Vietnam, Cambodia, Indonesia, Ethiopia, Bangladesh, and China.“

Ralph Lauren adds, “In Fiscal 2022, approximately 97% of our products (by dollar value) were produced outside of the US, primarily in Asia, Europe, and Latin America, with approximately 19% of our products sourced from China and another 19% from Vietnam.

However, many fashion companies have significantly cut their apparel sourcing volume from China. More often, China is no longer the No.1 apparel sourcing destination, overtaken by China’s competitors in Asia, such as Vietnam.

According to Lululemon, “During 2021, approximately 40% of our products were manufactured in Vietnam, 17% in Cambodia, 11% in Sri Lanka, 7% in China (PRC), including 2% in Taiwan, and the remainder in other regions… From a sourcing perspective, when looking at finished goods for the upcoming 2022 fall season, Mainland China represents only 4% to 6% of our total unit volume.”

Levi’s says, “The good thing about our supply chain is we’ve got truly a global footprint. We don’t manufacture a whole lot in China anymore. We’ve been slowly divesting manufacturing out of China, if you will, and kind of playing our chips elsewhere on the global map… Less than 1% of what we’re bringing into this country, into the US, less than 1% of it is coming from China.”

Adidas says, “In 2021, we sourced 91% of the total apparel volume from Asia (2020: 93%). Cambodia is the largest sourcing country, representing 21% of the produced volume (2020: 22%), followed by China with 20% (2020: 20%) and Vietnam with 15% (2020: 21%).”

Victoria’s Secret says, “On China, China is a single-digit percentage of our total inflow of merchandise. We’re not particularly dependent on China at all.”

Nike: “As of May 31, 2022, we were supplied by 279 finished goods apparel contract factories located in 33 countries. For fiscal 2022, contract factories in Vietnam, China and Cambodia manufactured approximately 26%, 20% and 16% of total NIKE Brand apparel, respectively“

Meanwhile, fashion companies still heavily use China as a sourcing base for textile raw materials (such as fabrics). For example:

Columbia Sportswear says it sources most of its finished products from Vietnam, but “a large portion of the raw materials used in our products is sourced by our contract manufacturers in China.”

Likewise, Puma says, “90% of our recycled polyester comes from Vietnam, China, Taiwan (China) and Korea.”

Guess says, “During fiscal 2022, we sourced most of our finished products with partners and suppliers outside the U.S. and we continued to design and purchase fabrics globally, with most coming from China.”

Lulumemon says, “Approximately 48% of the fabric used in our products originated from Taiwan, 19% from China Mainland, 11% from Sri Lanka, and the remainder from other regions.”

Second, Western fashion companies unanimously ranked the COVID situation as one of their top concerns for China. Many companies reported significant sales revenue and profits loss due to China’s draconian “zero-COVID” policy and lockdown measures. For example,

Tapestry says, “For Greater China, sales declined 11% due to lockdowns and business disruption… as a result, we have tempered our fiscal year 2023 outlook based on the expectation for a delayed recovery in China.”

Adidas says, “With Great China… we continue to see several market-specific challenges that are affecting our entire industry. The strict zero COVID-19 policy with nationwide restrictions remains in place amid more than 2000 daily new COVID-19 cases in November. As a consequence, offline traffic is subdued due to the imminent risk of new lockdowns.

Under Armour says, “Ongoing impacts of the COVID-19 pandemic and related preventative and protective actions in China…have negatively impacted consumer traffic and demand and may continue to negatively impact our financial results.”

VF Corporation says, “The performance in Greater China…continues to be impacted by widespread rolling COVID lockdowns and restrictions as well as lower consumer spending.”

Puma says, “COVID-19-related restrictions are still impacting business in Greater China, and higher freight rates and raw material prices continue to put pressure on margins.”

Notably, despite China’s most recent COVID policy U-turn, most fashion companies expect market uncertainties to stay in China, at least in the short run, given the surging COVID cases and policy unpredictability. For example:

PVH says, “While we remain optimistic about our business in China, it continues to be a challenging environment as restrictions have once again intensified in the fourth quarter of 2022.”

Nike says, “So we’ve taken a very cautious approach in our guidance to China, given the short-term uncertainties that are there.”

Abercrombie & Fitch also listed China’s COVID situation as one of their top risk factors, “risks and uncertainty related to the ongoing COVID-19 pandemic, including lockdowns in China, and any other adverse public health developments.”

Third, fashion companies report the negative impacts of US-China trade tensions on their businesses. Also, as the US-China relationship sours, fashion bands and retailers have been actively watching the potential effect of geopolitics. For example,

Express says, “recent geopolitical conditions, including impacts from the ongoing conflict between Russia and Ukraine and increased tensions between China and Taiwan, have all contributed to disruptions and rising costs to global supply chains.”

When assessing the market risk factors, Chico’s FAS says, “our reliance on sourcing from foreign suppliers and significant adverse economic, labor, political or other shifts (including adverse changes in tariffs, taxes or other import regulations, particularly with respect to China, or legislation prohibiting certain imports from China)”

Adidas holds the same view, “In addition, the challenging market environment in China had an adverse impact on the company’s business activities… Additional challenges included the geopolitical situation in China and extended lockdown measures.”

Macy’s adds, “At this time, it is unknown how long US tariffs on Chinese goods will remain in effect or whether additional tariffs will be imposed. Depending upon their duration and implementation, as well as our ability to mitigate their impact, these changes in foreign trade policy and any recently enacted, proposed and future tariffs on products imported by us from China could negatively impact our business, results of operations and liquidity if they seriously disrupt the movement of products through our supply chain or increase their cost.”

Gap Inc. says, “Trade matters may disrupt our supply chain. For example, the current political landscape, including with respect to U.S.-China relations, and recent tariffs and bans imposed by the United States and other countries (such as the Uyghur Forced Labor Prevention Act) has introduced greater uncertainty with respect to future tax and trade regulations.”

QVC says, “The imposition of any new US tariffs or other restrictions on Chinese imports or the taking of other actions against China in the future, and any responses by China, could impair our ability to meet customer demand and could result in lost sales or an increase in our cost of merchandise, which would have a material adverse impact on our business and results of operations.”

Additionally,NO evidence shows that fashion companies are decoupling with China. Instead, Western fashion companies, especially those with a global presence, still hold an optimistic view of China as a long-term business opportunity. For example:

Inditex, which owns Zara, says, “we remain absolutely confident about our opportunities there (in China) in the medium to long term. Fashion demand continues to be strong in China. For sure it will remain a core market for us for Inditex.”

Ralph Lauren says, “China provides not only the successful blueprint for our elevated ecosystem strategy globally, it also represents one of several geographic long-term opportunities for our brand…We continue to see near and long term brand opportunities in China.”

Lululemon says, “On China, we remain very excited…we remain very, very excited about the potential and the role that will play in quadrupling our international business with Mainland China.”

Nike says, “We have remained committed to investing in Greater China for the long term.”

Adidas says, “On China, clearly, we believe in as a midterm opportunity in China… And then when the market opens up (from COVID), we believe, the western brand is well-positioned in China again, and we can start growing significant in China again.”

Meanwhile, Western fashion companies plan to make more efforts to localize their product offer and cater to the specific needs of Chinese consumers, especially the young generation. The “Made in China for China” strategy could become more popular among Western fashion companies. For example,

PVH says, “So, I think in general, our production in China is heavily oriented to China for China production. I think for us generally speaking, the biggest impact of the shutdowns that we’ve seen across Shanghai and Beijing has really been focused on the impact to our China market.”

Likewise, Levi’s says, “We’re manufacturing somewhere in the neighborhood of 5% of our global production is in China, and most of it staying in China.“

Hanesbrands says, “we’re committed to opening new stores, and that’s continues to go well, despite, the challenges that are there. Looking specifically at Champion, we continued our expansion in China adding new stores in the quarter through our partners.”

H&M says, “we still see China as an important market for us.”

According to Hugo Boss, “Thanks to overall robust local demand, revenues in China in 2021 grew 24% as compared to 2019.”

VF Corporation adds, “China is a significant opportunity…(We are) really pushing decision-making into the regions and providing more and more latitude for local-for-local decision-makings around product, around storytelling, certainly staying within the confines or the framework of the brand strategy, but really giving more freedom and more empowerment to the regions.”

This article provided a comprehensive review of the world textiles and clothing trade patterns in 2021 based on the newly released data from the World Trade Statistical Review 2022 and the United Nations (UNComtrade). Affected by the ongoing pandemic and companies’ evolving production and sourcing strategies in response to the shifting business environment, the world textiles and clothing trade patterns in 2021 included both continuities and new trends. Specifically:

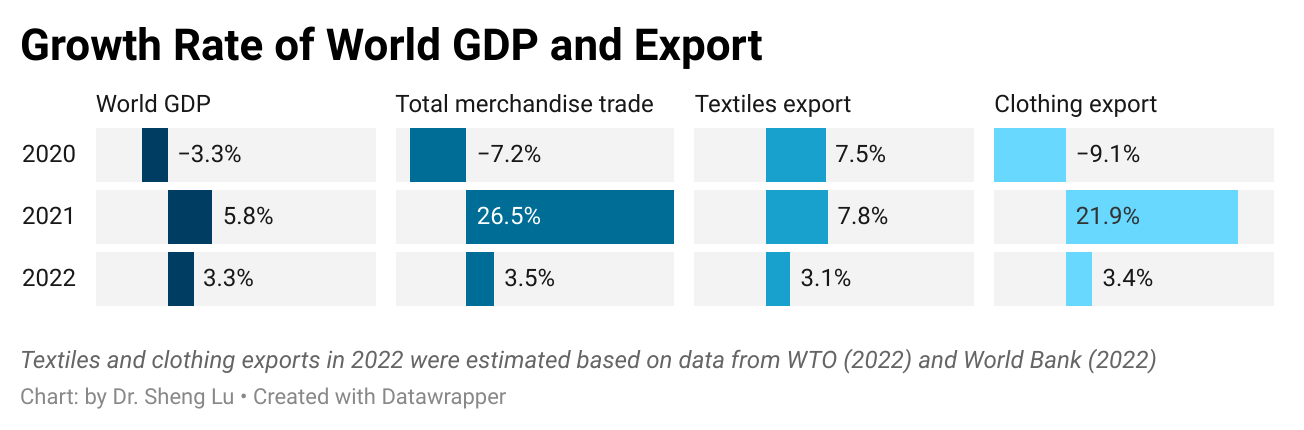

Pattern #1: As the world economy recovered from COVID, the world clothing export boomed in 2021, while the world textile exports grew much slower due to a high trade volume the year before. Specifically, thanks to consumers’ strong demand, world clothing exports in 2021 fully bounced back to the pre-COVID level and exceeded $548.8bn, a substantial increase of 21.9% from 2020. The apparel sector is not alone. With economic activities mostly resumed, the world merchandise trade in 2021 also jumped 26.5% from a year ago, the fastest growth in decades.

In comparison, the value of world textiles exports grew slower at 7.8% in 2021 (i.e., reached $354.2bn), lagging behind most sectors. However, such a pattern was understandable as the textile trade maintained a high level in 2020, driven by high demand for personal protective equipment (PPE) during the pandemic.

Nevertheless, the world textiles and clothing trade could face strong headwinds down the road due to a slowing world economy and consumers’ weakened demand. Notably, amid hiking inflation, high energy costs, and retrenchment of global supply chains, leading international economic agencies, from the World Bank to the International Monetary Fund (IMF), unanimously predict a slowing economy worldwide. Likewise, the World Trade Organization (WTO) forecasts that the growth of world merchandise trade will be cut to 3.5% in 2022 and down further to only 1% in 2023. As a result, the world textiles and clothing trade will likely struggle with stagnant growth or a modest decline over the next two years.

Pattern #2: COVID did NOT fundamentally shift the competitive landscape of textile exports but affected the export product structure. Meanwhile, some long-term structural changes in world textile exports continued in 2021.

Specifically, China, the European Union (EU), and India remained the world’s three largest textile exporters in 2021, a pattern that has stayed stable for over a decade. Together, these top three accounted for 68% of the world’s textile exports in 2021, similar to 66.9% before the pandemic (2018-2019). Other textile exporters that made it to the top ten list in 2021 were also the same as a year ago and before the pandemic (2018-2019).

Meanwhile, the growth rate of the top ten textile exporters varied significantly in 2021, ranging from -5.5% (China) to 47.8% (India). The demand shift from PPE to apparel-related yarns and fabrics was a critical contributing factor behind the phenomenon. For example, China’s PPE-related textile exports decreased by more than $33bn (or down 43%) in 2021. In contrast, the world knit fabric exports (SITC code 655) surged by more than 30% in 2021, led by India (up 74%) and Pakistan (up 72%). Nevertheless, as consumers’ lifestyles almost reached a “new normal,” we could expect the textile export product structure to stabilize soon.

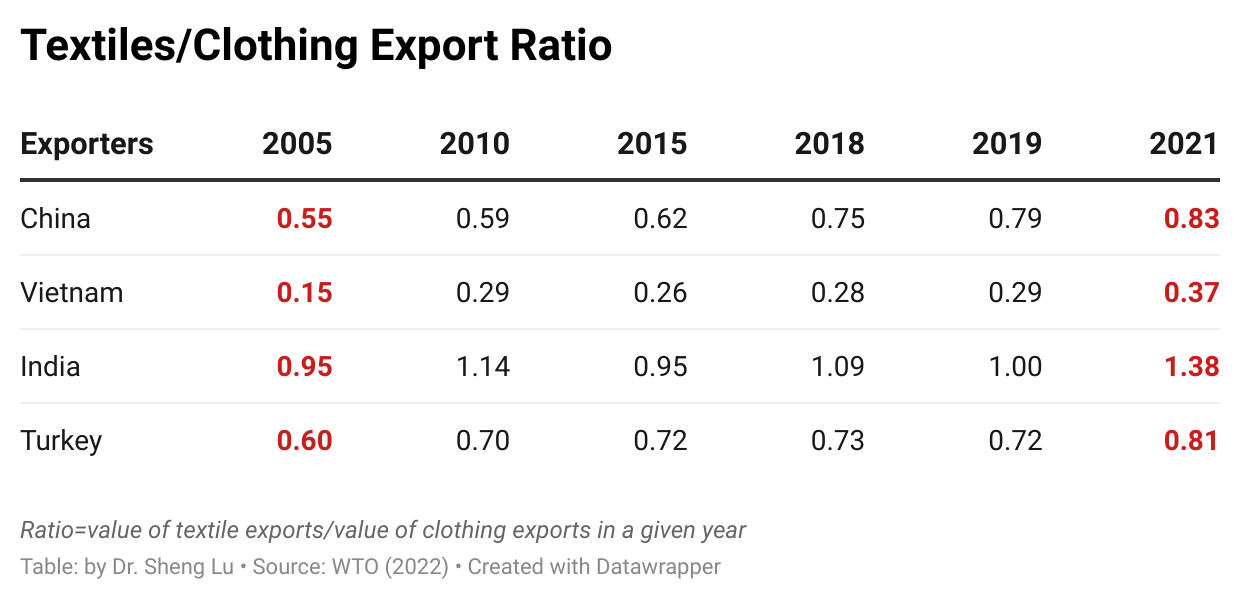

On the other hand, as a trend already emerged before the pandemic, middle-income developing countries continued to play a more significant role in textile exports, whereas developed countries lost market shares. For example, the United States, Germany, and Italy led the world’s textile exports in the 2000s, accounting for more than 20% of the market shares. However, these three countries’ shares fell to 12.8% in 2019 and hit a new low of 11.3% in 2021. In comparison, middle-income developing countries like China, Vietnam, Turkey, and India have entered the development stage of expanding textile manufacturing. As a result, their market share in the world’s textile exports rose steadily. These countries also achieved a more balanced textiles/clothing export ratio over the years, meaning more textile raw materials like yarns and fabrics can be locally produced instead of relying on imports. For example, Vietnam, known for its competitive clothing products, achieved a new high of $11.5bn in textile exports in 2021 and ranked sixth globally. Vietnam’s textiles/clothing ratio also doubled from 0.15 in 2005 to 0.37 in 2021. It is not unlikely that Vietnam’s textile exports may surpass the United States over the next few years.

Pattern #3: Countries with large-scale production capacity stood out in world clothing exports in 2021. Meanwhile, clothing exporters compete to become China’s alternatives, but there seems to be no clear winner yet.

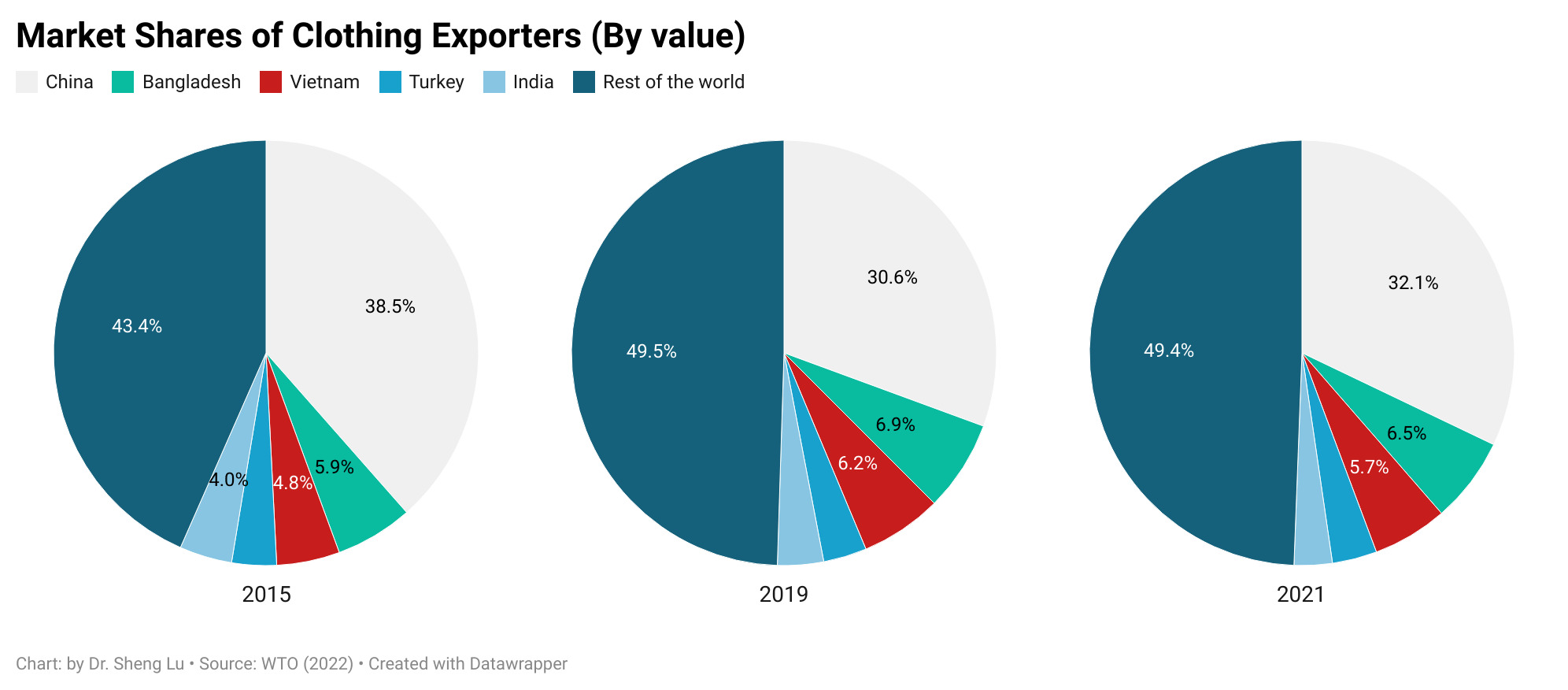

Consumers’ surging demand and COVID-related supply chain disruptions significantly impacted the world’s clothing export patterns in 2021. As fashion brands and retailers were eager to find sourcing capacity, countries with large-scale production capacity and relatively stable supply enjoyed the fastest growth in clothing exports. For example, except for Vietnam, which suffered several months of COVID lockdowns, all other top five clothing exporters enjoyed a more than 20% growth of their exports in 2021, such as China (up 24%), Bangladesh (up 30%), Turkey (up 22%), and India (up 24%).

As another critical trend, many international fashion brands and retailers have been trying to reduce their apparel sourcing from China, driven by various economic and non-economic factors, from cost considerations and trade tensions to geopolitics. Notably, despite its strong performance in 2021, China accounted for only 23.1% of US apparel imports in 2022 (January to September), much lower than 36.2% in 2015. Likewise, China’s market shares in the EU, Japanese, and Canadian clothing import markets also fell over the same period, suggesting this was a worldwide phenomenon.

With reduced apparel sourcing from China, fashion companies have actively sought alternative sourcing destinations, but the latest trade data suggests no clear winner yet. For example, Vietnam and Bangladesh, the two most popular candidates for “Next China,” accounted for 6.5% and 5.7% shares in the world’s clothing export in 2021, still far behind China (32.1%). Interestingly, from 2015 to 2021, the world’s top four largest clothing exporters next to China (i.e., Bangladesh, Vietnam, Turkey, and India) did not substantially gain new market shares. Instead, China’s lost market was filled by “the rest of the world.”

Additionally, recent studies show that many fashion companies have switched back to the sourcing diversification strategy in 2022 as managing risks and improving sourcing flexibility become more urgent priorities. In other words, the world’s clothing export market could turn more “crowded” and competitive in the coming years.

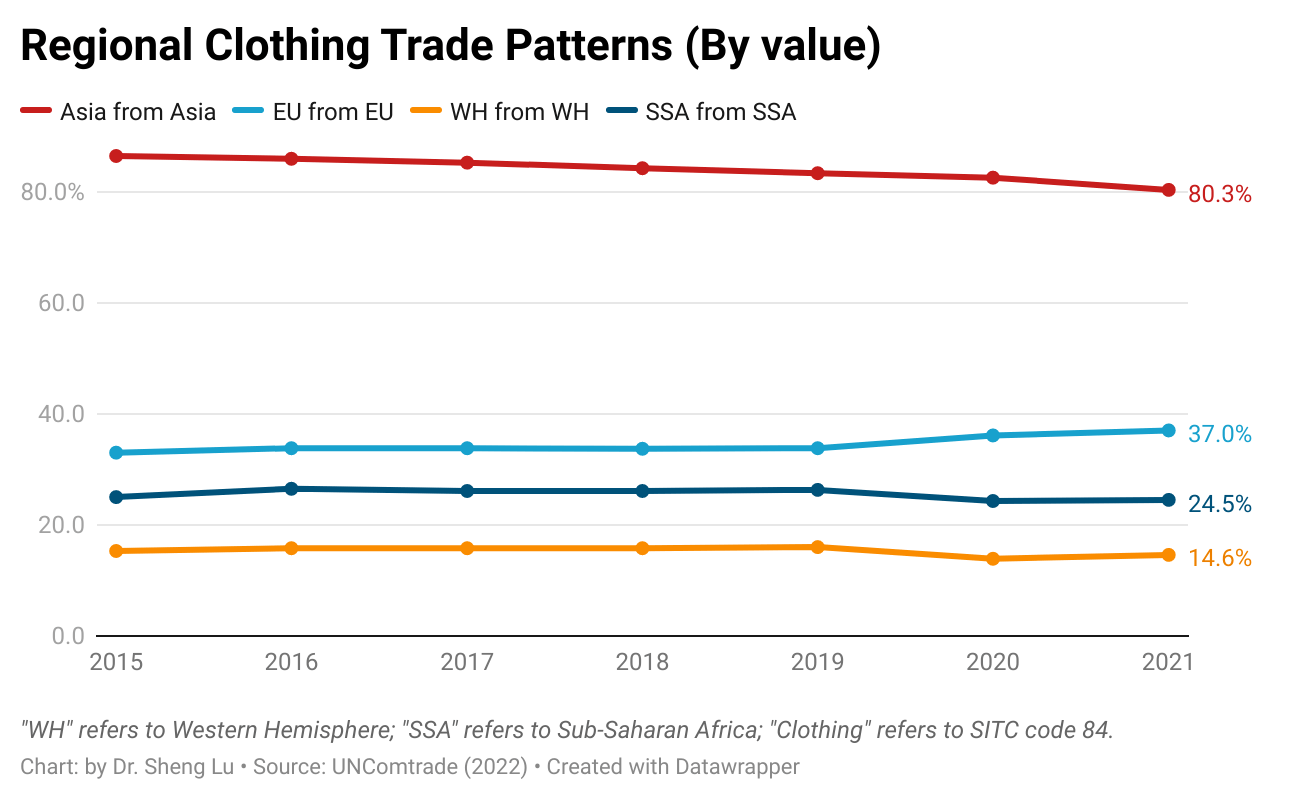

Pattern #4: Regional supply chains remain critical features of the world textiles and clothing trade. Several factors support and shape the regional textiles and clothing trade patterns. First, as clothing production often needs to be close to where textile materials are available, many developing clothing-producing countries rely heavily on imported textile materials, primarily from more advanced economies in the same region. Second, through lowered trade barriers, regional free trade agreements also financially encouraged garment producers, particularly in Asia, the EU, and Western Hemisphere (WH), to use locally or regionally made textile materials. Further, fashion companies’ interest in “near-shoring” supported the regional supply chain, and related textiles and clothing trade flows between neighboring countries.

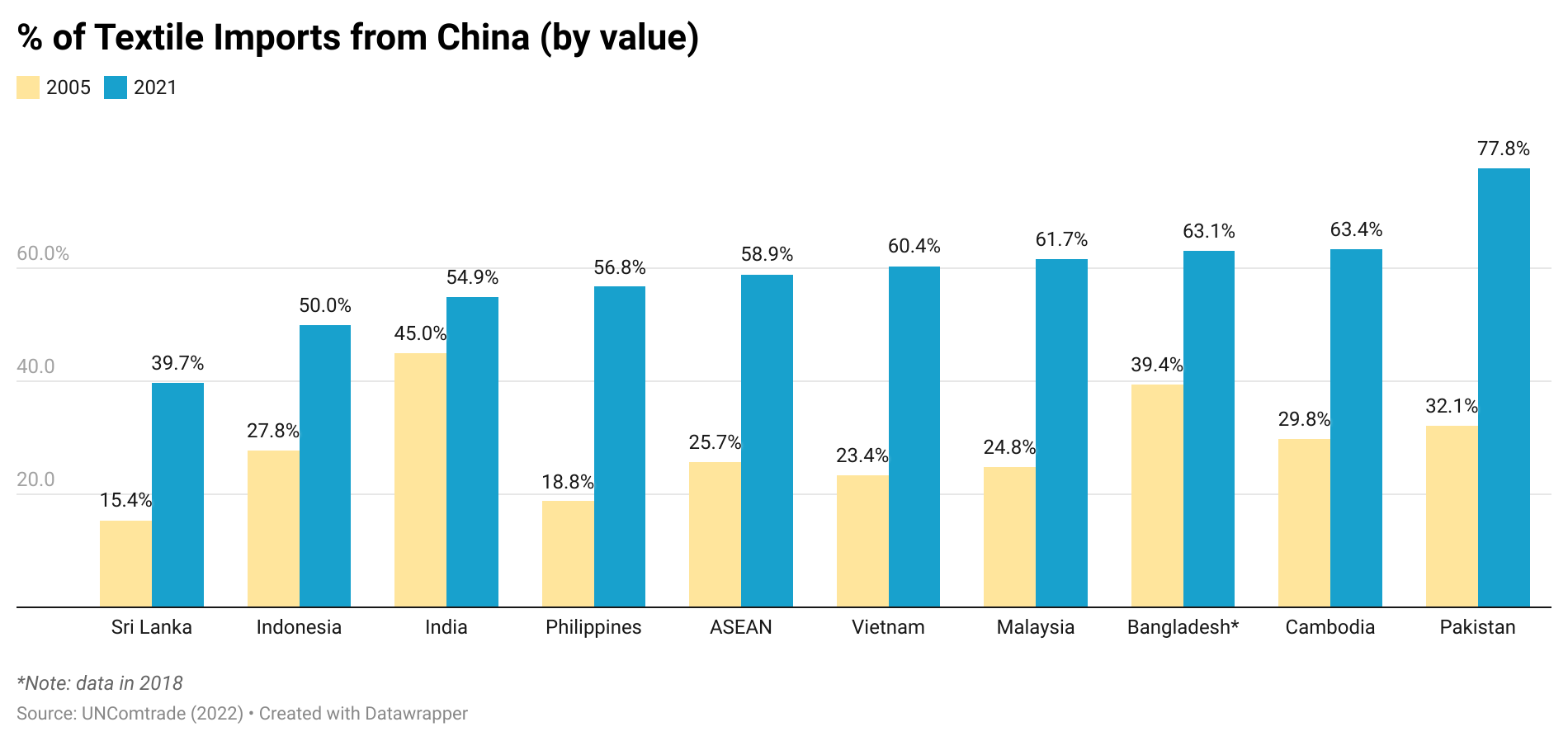

The latest trade data indicated that Asia’s regional textiles and clothing trade patterns strengthened further despite supply chain chaos during the pandemic. Specifically, in 2021, as many as 82% of Asian countries’ textile imports came from within Asia, up from 80% in 2015. China, in particular, has played a more prominent role as a leading textile supplier for other Asian clothing-exporting countries. For example, more than 60% of Vietnam’s textile imports came from China in 2021, a substantial increase from 23% in 2005. The same pattern applied to Pakistan, Cambodia, Bangladesh, and the Association of Southeast Asian Nations (ASEAN) members.