Key findings:

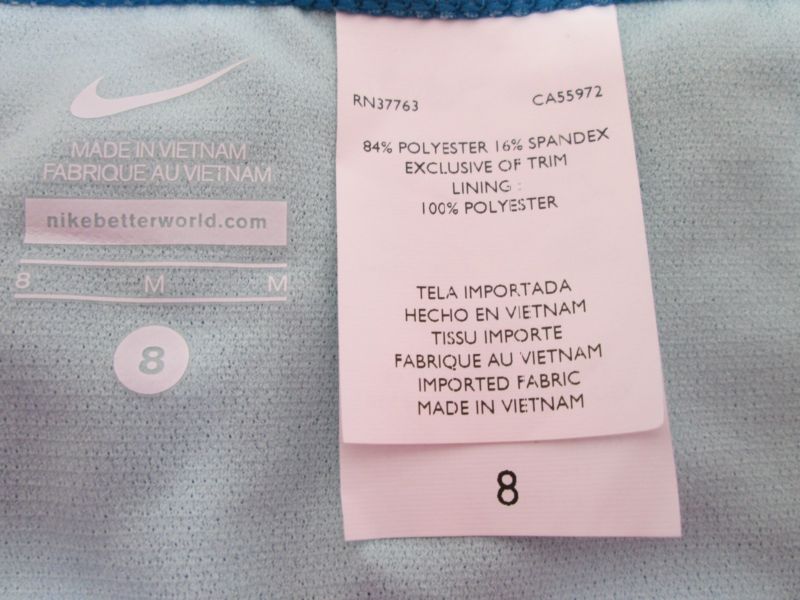

This study was based on a statistical analysis of 3,307 randomly selected clothing items made from recycled textile materials for sale in the U.S. retail market between January 2019 and August 2022 (see the sample picture above). The results show that:

First, U.S. retailers sourced clothing made from recycled textile materials from diverse countries.

Specifically, the sampled clothing items came from as many as 36 countries, including developed and developing economies in Asia, America, the EU, and Africa.

However, reflecting the unique supply chain composition of clothing made from recycled textile materials, U.S. retailers’ sourcing patterns for such products turned out to be quite different from regular new clothing. For example, whereas the vast majority (i.e., over 90%) of U.S. regular new clothing came from developing countries as of 2022 (UNComtrade, 2022), as many as 43% of the sampled clothing items made from recycled textile materials (n=1,408) were sourced from developed countries. Likewise, U.S. retailers seemed to be less dependent on Asia when sourcing clothing made from recycled materials (41.9%, n=1,387) and instead used near-sourcing from America (30.1%, n=994) more often, particularly domestic sourcing from the United States (14.8%, n=490).

Second, U.S. retailers appeared to set differentiated assortments for products imported from developed and developing countries when sourcing clothing made from recycled textile materials.

Among the sampled clothing items made from recycled textile materials, those imported from developing countries, on average, included a broader assortment than developed economies. Likewise, imports from developing countries also concentrated on products relatively more complex to make as opposed to developed countries. Developing countries’ more extensive clothing production capability, including the available production facilities and skilled labor force, than developed economies could have contributed to the pattern.

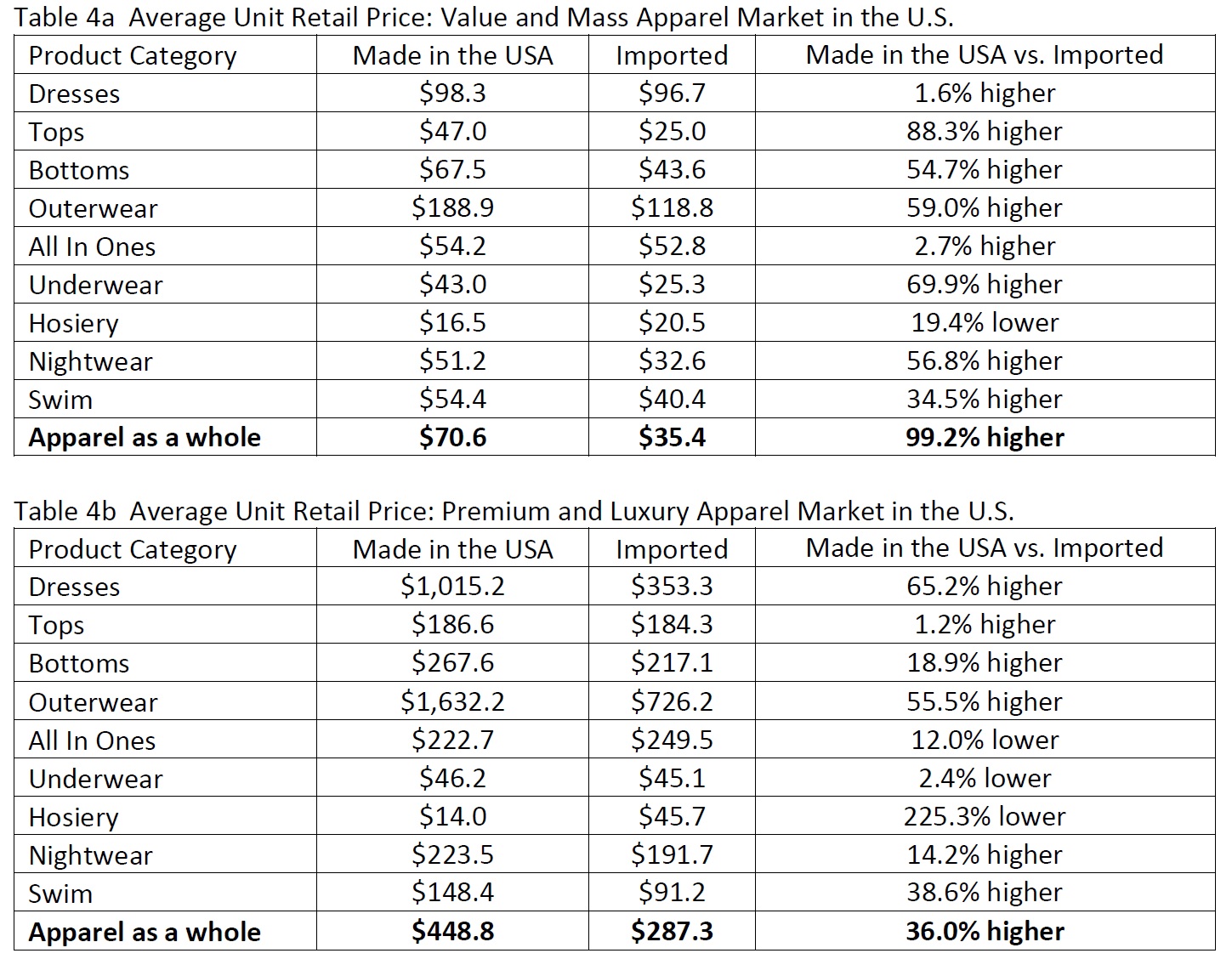

On the other hand, likely caused by developed countries’ overall higher production costs, the average retail price of sampled clothing items sourced from developed countries was notably higher than those from developing ones. However, NO clear evidence shows that U.S. retailers used developed countries primarily as the sourcing bases for luxury or premium items and used developing countries only for items targeting the mass or value market.

Third, an exporting country’s geographic location was another statistically significant factor affecting U.S. retailers’ sourcing pattern for clothing made from recycled textile materials. Specifically,

- Imports from Asia had the most diverse product assortment (e.g., sizing options) and focused on complex product categories (e.g., outwear) that targeted mass and value markets.

- Imports from America (North, South, and Central America) concentrated on simple product categories (e.g., T-shirts and hosiery) with moderate assortment diversity and mainly targeted the mass and value market.

- Imports from the EU were mainly higher-priced luxury items in medium-sophisticated or sophisticated product categories with diverse assortment.

- Imports from Africa concentrated on relatively higher-priced premium or luxury items in simple product categories (i.e., swim shorts) with a limited assortment diversity.

The study’s findings demystified the country of origin of clothing made from recycled textile materials hidden behind macro trade statistics. The findings also created critical new knowledge that contributed to our understanding of the supply chain of clothing made from recycled textile materials and U.S. retailers’ distinct sourcing patterns and affecting factors for such products. The findings have several other important implications:

First, the study’s findings revealed the broad supply base for clothing made from recycled textile materials and suggested promising sourcing opportunities for such products. Whereas existing studies illustrated consumers’ increasing interest in shopping for clothing made from recycled textile materials, the study’s results indicated that the “enthusiasm” also applied to the supply side, with many countries already engaged in making and exporting such products. Meanwhile, the results showed that U.S. retailers sourced clothing made from recycled textile materials in different product categories with a broad price range targeting various market segments to meet consumers’ varying demands. Moreover, as textile recycling techniques continue to advance, potentially enriching the product offer of clothing made from recycled textile materials, U.S. retailers’ sourcing needs and supply base for such products could expand further.

Second, the study’s findings suggest that sourcing clothing made from recycled textile materials may help U.S. retailers achieve business benefits beyond the positive environmental impacts. For example, given the unique supply chain composition and production requirements, China appeared to play a less dominant role as a supplier of clothing made from recycled textile materials for U.S. retailers. Instead, a substantial portion of such products was “Made in the USA” or came from emerging sourcing destinations in America (e.g., El Salvador, Nicaragua) and Africa (e.g., Tunisia and Morocco). In other words, sourcing clothing made from recycled textile materials could help U.S. retailers with several goals they have been trying to achieve, such as reducing dependence on sourcing from China, expanding near sourcing, and diversifying their sourcing base.

Additionally, the study’s findings call for strengthening U.S. domestic apparel manufacturing capability to better serve retailers’ sourcing needs for clothing made from recycled textile materials. On the one hand, the results demonstrated U.S. retailers’ strong interest in sourcing clothing made from recycled textile materials that were “Made in the USA.” Also, the United States may enjoy certain competitive advantages in making such products, ranging from the abundant supply of recycled textile waste and the affordability of expensive modern recycling machinery to the advanced research and product development capability. On the other hand, the results showed that U.S. retailers primarily sourced simple product categories (e.g., T-shirts and hosiery), targeting the value and mass markets from the U.S. and other American countries. This pattern somewhat mirrored the production and sourcing pattern for regular new clothing, for which apparel “Made in the USA” also lacked product variety and focused on basic fashion items compared with Asian and EU suppliers. Thus, strengthening the U.S. domestic apparel production capacity, especially for those complex product categories (e.g., outwear and suits), could encourage more sourcing of “Made in the USA” apparel using recycled textile materials and support production and job creation in the U.S. apparel manufacturing sector.

by Sheng Lu

Full paper: Lu, S. (2023). Explore U.S. retailers’ sourcing strategies for clothing made from recycled textile materials. Sustainability, 15(1), 38.