This event is free and open to ALL UD students (undergraduate and graduate), faculty,and prospective students of the UD FASH program, but registration is required (please use .edu email address): https://www.wita.org/events/pathways-careers-behind-the-seams/

Note: Students in FASH455-010 (Tue and Thu) do not need to register for the event. We will attend the workshop and participate in the live Q&A session in the classroom.

Featured speakers (bios here) from JCPenney include:

Amanda Blackman, Director of Planning and Allocation

Michelle Erwin, Sourcing Manager

Hunter Green, Senior Manager of International Transportation

Angela Hofmann, VP, Government Affairs

Wayne Milano, SVP, Global Sourcing and Product Development

Aqsa Tasleem, Senior Manager of Fabric & Sustainability

Note: The revealed comparative advantage (RCA) index measures a country’s relative export performance of a particular product compared to the world average. It helps identify sectors in which a country holds a competitive edge in international trade. RCA =(Country’s exports of product X/Country’s total exports)/(World exports of product X/World total exports).

RCA > 1: A value greater than 1 indicates that the country has a revealed comparative advantage in the product, meaning the product has a higher export share in the country’s portfolio compared to the global average. This suggests the country is more competitive in exporting that product relative to the rest of the world.

RCA < 1: A value less than 1 means the country has a revealed comparative disadvantage in that product. It indicates that the country is less competitive in exporting that product compared to the global average.

Observe the sectors in which the U.S. enjoyed a revealed comparative advantage (i.e., RCA > 1) in 2023. How does this compare with Bangladesh? What is your explanation for the observed differences?

Argument: The U.S. textile manufacturing industry has been a winner of globalization

Comment #1: While it is true that many Americans lost their jobs due to the increase in trade, there are more benefits to both importing and exporting rather than the mercantilist view of trade. Increasing trade and globalization, especially during the Clinton administration, was an opportunity to develop strong relationships with other nations. The value of U.S. textile exports since 2000 has risen by 30% for yarn and 15% for fabric, after the establishment of agreements such as NAFTA. Additionally, one of the U.S. apparel manufacturers in the video used machinery for their production from Sweden. Without globalization and trade, they would not be able to use this high-tech equipment. All in all, U.S. textile manufacturing sector benefits from both importing and exporting goods.

Comment #2: Deeper down, the US textile sector seems to be winning in the long run. The squeeze that globalization has placed on them has allowed for innovation within the industry as they fight to stay relevant and compete with overseas goods. Operational slack such as high turnover jobs have been eliminated with automation, and US manufacturers gained a new branding niche that overseas companies do not: a US “personal touch.” Consumers may now be more willing to pay more for a garment just because it says it is made in the USA. USA-made clothing may now be perceived as higher quality and more scarce. The sentiment towards US-made goods and their quality could enact change to reduce overseas reliance, which is a win for US manufacturing in the long run. Additionally, globalization expands the export market for the US textile manufacturing sector.

Comment #3: As discussed in the video, there is a growing trend of reshoring and regionalization in some manufacturing sectors, including textiles. Some U.S. textile manufacturers have seized this opportunity to bring production back to the United States, capitalizing on the advantages of local supply chains, quality control, and speed to market. The video also shows how technology and automation can help streamline production processes and make manufacturing more competitive, even in higher-cost regions like the United States. US textile manufacturers have invested in innovation and automation, making them competitive in producing textiles with advanced features and properties in today’s global economy. It is globalization that is pushing the US textile industry to adopt these new technologies and continue improving its international competitiveness.”

Argument: the U.S. textile manufacturing industry has been a loser of globalization

Comment #4: One of the biggest arguments for globalization is the lower prices & affordability for the consumer. From this perspective, it seemed that the United States was a winner of globalization as a whole. However, when beginning to look at the consequences of moving production overseas, we not only see the textile manufacturing sector being affected, but we also see this impact disperse to the communities in America as well. When brands offshore and outsource production overseas for lower prices & labor, our very own US textile manufacturing industry is losing out on this business. It also forces this industry into a highly competitive environment that does not have equal “playing fields” and does not have insurance/protection in case environmental factors ruin crops. The US has clear labor laws and human rights policies (as well as increasing environmental policies), whereas their cotton-growing competitors, for instance, do not have to follow the same rules. This allows labor exploitation to decrease costs and makes US companies seem unappealing or less competitive.

Comment #5: Over the past few decades, the number of manufacturing jobs in the US textile industry has plummeted after companies began moving production overseas, specifically to countries like China, which have preferential treatment. These foreign facilities can produce things much faster and cheaper because the standards and regulations are completely different than those of the United States. Free trade does not consider these differences in labor and environmental laws, making it much less “free” than it claims. As countries overseas– specifically China and regions like Xinjiang– continue to not play by the rules, the US is forced to keep up by implementing things like the Toyota System…Americans want to be the best in manufacturing and globalization often gets in the way of this. With near-shoring, the US can reclaim high-quality, American-made garments while helping with job security and sustainability.

Comment #6: Overall, I believe that the U.S. textile manufacturing industry is a loser of globalization and international trade, mostly due to the competition from overseas. This competition includes more manufacturers from other countries, but also the competition of pricing since other oversea manufacturers are able to sell their cotton/textile materials at a lower price. Since the U.S. struggles to compete with these lower prices, they are forced to look for another way to have a competitive advantage in the textile manufacturing sector, such as lean manufacturing and technology improvements. At Carolina Cotton Works, Bryan Ashby shares how they have increased efficiency and use high-quality machines (note: imported) for their products. Although this sounds great, this also means that there are fewer workers.

Comment #7: Globalization creates a trade dependence on imports. It’s important we don’t depend on things for when things happen that we can’t predict like the pandemic where we can’t import anymore. Since there was a lack of local textile manufacturing and sourcing in the United States compared to what was being imported, there was less of a chance for technological advances and improvement in the United States textile manufacturing sector. Post Globalization, however, may be the chance for the United States to bring back the textile manufacturing sector momentum. I think this because the United States has seen the result of heavily relying on other countries for their cheap labor/sources, and this could add extra motivation for companies to want to figure out better alternatives in manufacturing in their own country.

Comment #8: I think currently the US is a loser to globalization only because brands want to get the product for cheap. I think brands think that would create more profit that way. However, I do believe we could get to a future where more things would be created in the US and wouldn’t have to pay that much in tariffs and other external prices. I think it would help boost people to work more. I think people are worried about making things in our country because of the relations we have with other countries.

Discussion questions:

Do you agree or disagree with any particular argument above? Any follow-up comments on the impact of globalization on the US textile manufacturing sector? What should government do with trade given the debates? Please feel free to share any additional thoughts.

#1 What are the examples of globalization in the above two videos about Temu?

#2 Based on the videos, who are the winners and losers of globalization and why?

#3 What role does international trade play in Temu’s business model?

#4 Some suggest ending the “de minimis rule.” Based on the videos, what is your view and recommendation for US policymakers?

#5 Anything you find interesting/surprising/intriguing in the video and why?

(Note: Anyone is welcome to join the discussion. For students in FASH455, please address at least two questions. Please mention the question number in your response, but there is no need to repeat the question).

Note: About “de minimis rule.”: Under US customs law, specifically the Trade Facilitation and Trade Enforcement Act of 2015, import duties are generally waived for goods valued at $800 or less per person per day. Therefore, Temu’s shipping from China to US consumers is likely to be eligible for the benefits.

This article provided a comprehensive review of the world textiles and clothing trade patterns in 2021 based on the newly released data from the World Trade Statistical Review 2022 and the United Nations (UNComtrade). Affected by the ongoing pandemic and companies’ evolving production and sourcing strategies in response to the shifting business environment, the world textiles and clothing trade patterns in 2021 included both continuities and new trends. Specifically:

Pattern #1: As the world economy recovered from COVID, the world clothing export boomed in 2021, while the world textile exports grew much slower due to a high trade volume the year before. Specifically, thanks to consumers’ strong demand, world clothing exports in 2021 fully bounced back to the pre-COVID level and exceeded $548.8bn, a substantial increase of 21.9% from 2020. The apparel sector is not alone. With economic activities mostly resumed, the world merchandise trade in 2021 also jumped 26.5% from a year ago, the fastest growth in decades.

In comparison, the value of world textiles exports grew slower at 7.8% in 2021 (i.e., reached $354.2bn), lagging behind most sectors. However, such a pattern was understandable as the textile trade maintained a high level in 2020, driven by high demand for personal protective equipment (PPE) during the pandemic.

Nevertheless, the world textiles and clothing trade could face strong headwinds down the road due to a slowing world economy and consumers’ weakened demand. Notably, amid hiking inflation, high energy costs, and retrenchment of global supply chains, leading international economic agencies, from the World Bank to the International Monetary Fund (IMF), unanimously predict a slowing economy worldwide. Likewise, the World Trade Organization (WTO) forecasts that the growth of world merchandise trade will be cut to 3.5% in 2022 and down further to only 1% in 2023. As a result, the world textiles and clothing trade will likely struggle with stagnant growth or a modest decline over the next two years.

Pattern #2: COVID did NOT fundamentally shift the competitive landscape of textile exports but affected the export product structure. Meanwhile, some long-term structural changes in world textile exports continued in 2021.

Specifically, China, the European Union (EU), and India remained the world’s three largest textile exporters in 2021, a pattern that has stayed stable for over a decade. Together, these top three accounted for 68% of the world’s textile exports in 2021, similar to 66.9% before the pandemic (2018-2019). Other textile exporters that made it to the top ten list in 2021 were also the same as a year ago and before the pandemic (2018-2019).

Meanwhile, the growth rate of the top ten textile exporters varied significantly in 2021, ranging from -5.5% (China) to 47.8% (India). The demand shift from PPE to apparel-related yarns and fabrics was a critical contributing factor behind the phenomenon. For example, China’s PPE-related textile exports decreased by more than $33bn (or down 43%) in 2021. In contrast, the world knit fabric exports (SITC code 655) surged by more than 30% in 2021, led by India (up 74%) and Pakistan (up 72%). Nevertheless, as consumers’ lifestyles almost reached a “new normal,” we could expect the textile export product structure to stabilize soon.

On the other hand, as a trend already emerged before the pandemic, middle-income developing countries continued to play a more significant role in textile exports, whereas developed countries lost market shares. For example, the United States, Germany, and Italy led the world’s textile exports in the 2000s, accounting for more than 20% of the market shares. However, these three countries’ shares fell to 12.8% in 2019 and hit a new low of 11.3% in 2021. In comparison, middle-income developing countries like China, Vietnam, Turkey, and India have entered the development stage of expanding textile manufacturing. As a result, their market share in the world’s textile exports rose steadily. These countries also achieved a more balanced textiles/clothing export ratio over the years, meaning more textile raw materials like yarns and fabrics can be locally produced instead of relying on imports. For example, Vietnam, known for its competitive clothing products, achieved a new high of $11.5bn in textile exports in 2021 and ranked sixth globally. Vietnam’s textiles/clothing ratio also doubled from 0.15 in 2005 to 0.37 in 2021. It is not unlikely that Vietnam’s textile exports may surpass the United States over the next few years.

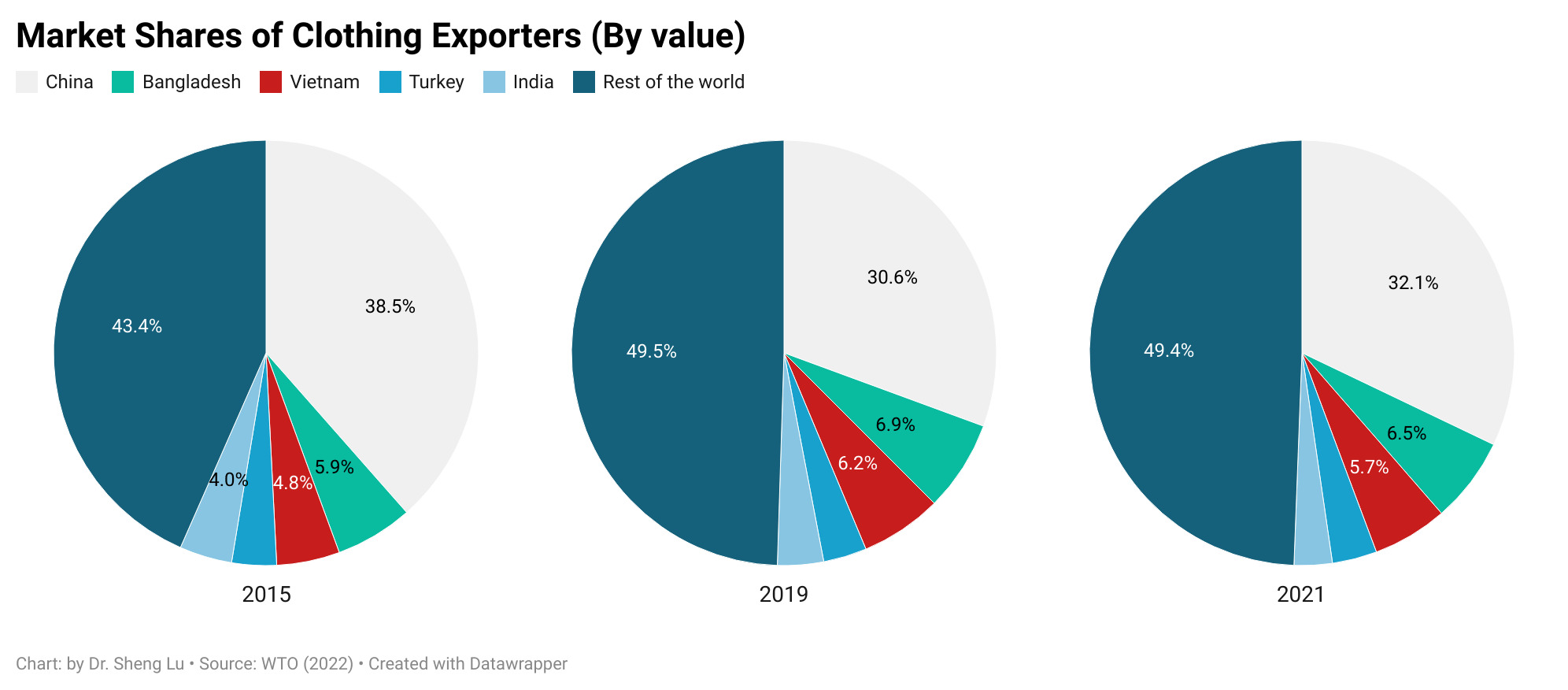

Pattern #3: Countries with large-scale production capacity stood out in world clothing exports in 2021. Meanwhile, clothing exporters compete to become China’s alternatives, but there seems to be no clear winner yet.

Consumers’ surging demand and COVID-related supply chain disruptions significantly impacted the world’s clothing export patterns in 2021. As fashion brands and retailers were eager to find sourcing capacity, countries with large-scale production capacity and relatively stable supply enjoyed the fastest growth in clothing exports. For example, except for Vietnam, which suffered several months of COVID lockdowns, all other top five clothing exporters enjoyed a more than 20% growth of their exports in 2021, such as China (up 24%), Bangladesh (up 30%), Turkey (up 22%), and India (up 24%).

As another critical trend, many international fashion brands and retailers have been trying to reduce their apparel sourcing from China, driven by various economic and non-economic factors, from cost considerations and trade tensions to geopolitics. Notably, despite its strong performance in 2021, China accounted for only 23.1% of US apparel imports in 2022 (January to September), much lower than 36.2% in 2015. Likewise, China’s market shares in the EU, Japanese, and Canadian clothing import markets also fell over the same period, suggesting this was a worldwide phenomenon.

With reduced apparel sourcing from China, fashion companies have actively sought alternative sourcing destinations, but the latest trade data suggests no clear winner yet. For example, Vietnam and Bangladesh, the two most popular candidates for “Next China,” accounted for 6.5% and 5.7% shares in the world’s clothing export in 2021, still far behind China (32.1%). Interestingly, from 2015 to 2021, the world’s top four largest clothing exporters next to China (i.e., Bangladesh, Vietnam, Turkey, and India) did not substantially gain new market shares. Instead, China’s lost market was filled by “the rest of the world.”

Additionally, recent studies show that many fashion companies have switched back to the sourcing diversification strategy in 2022 as managing risks and improving sourcing flexibility become more urgent priorities. In other words, the world’s clothing export market could turn more “crowded” and competitive in the coming years.

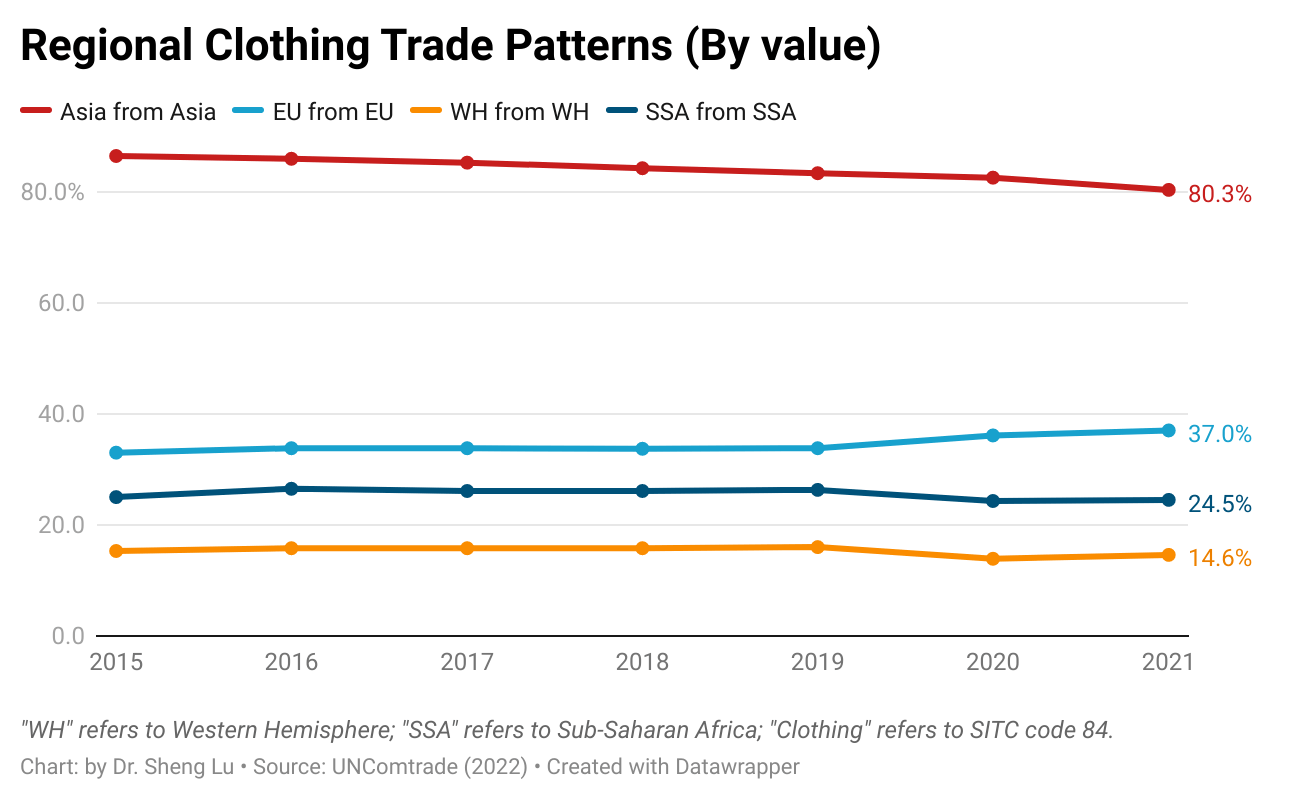

Pattern #4: Regional supply chains remain critical features of the world textiles and clothing trade. Several factors support and shape the regional textiles and clothing trade patterns. First, as clothing production often needs to be close to where textile materials are available, many developing clothing-producing countries rely heavily on imported textile materials, primarily from more advanced economies in the same region. Second, through lowered trade barriers, regional free trade agreements also financially encouraged garment producers, particularly in Asia, the EU, and Western Hemisphere (WH), to use locally or regionally made textile materials. Further, fashion companies’ interest in “near-shoring” supported the regional supply chain, and related textiles and clothing trade flows between neighboring countries.

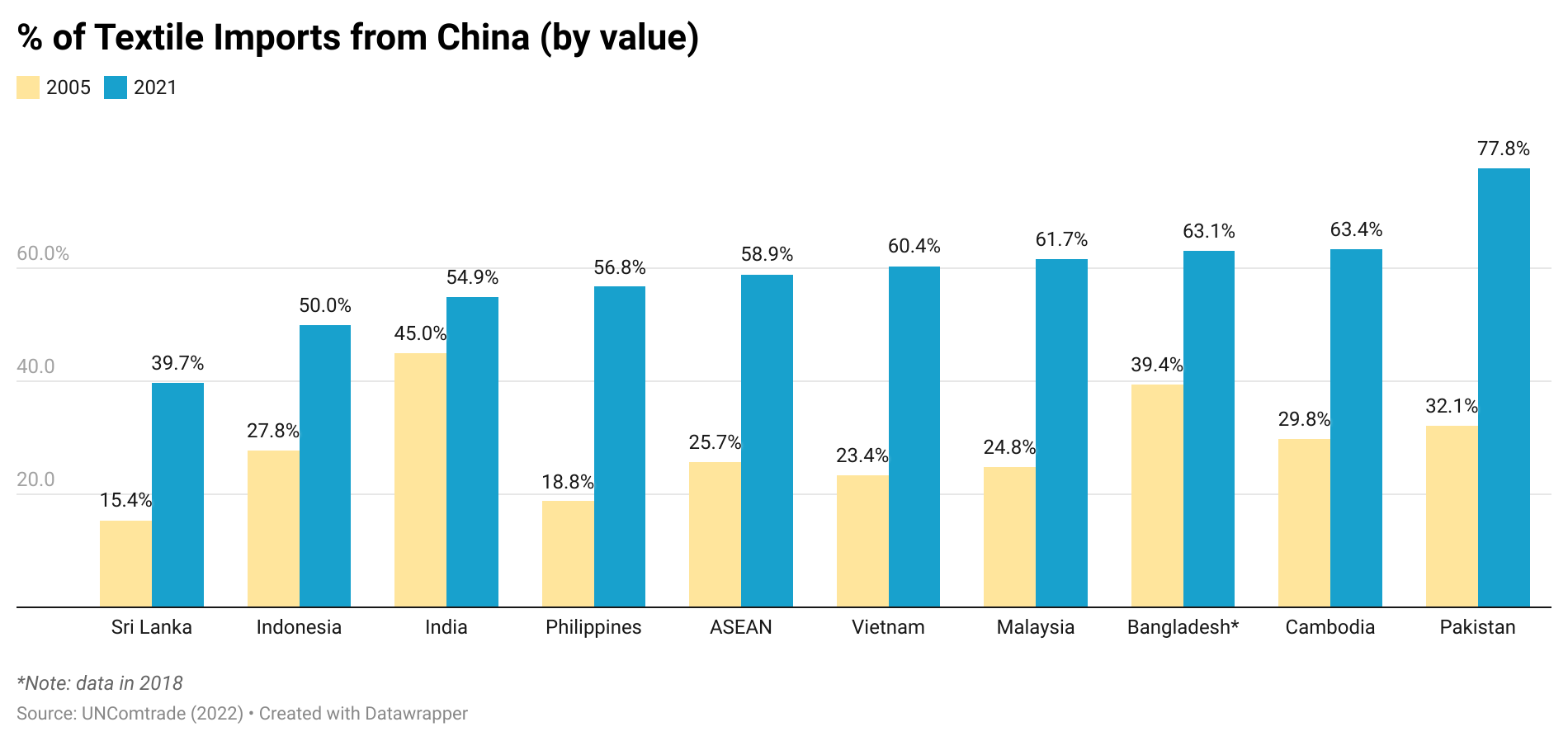

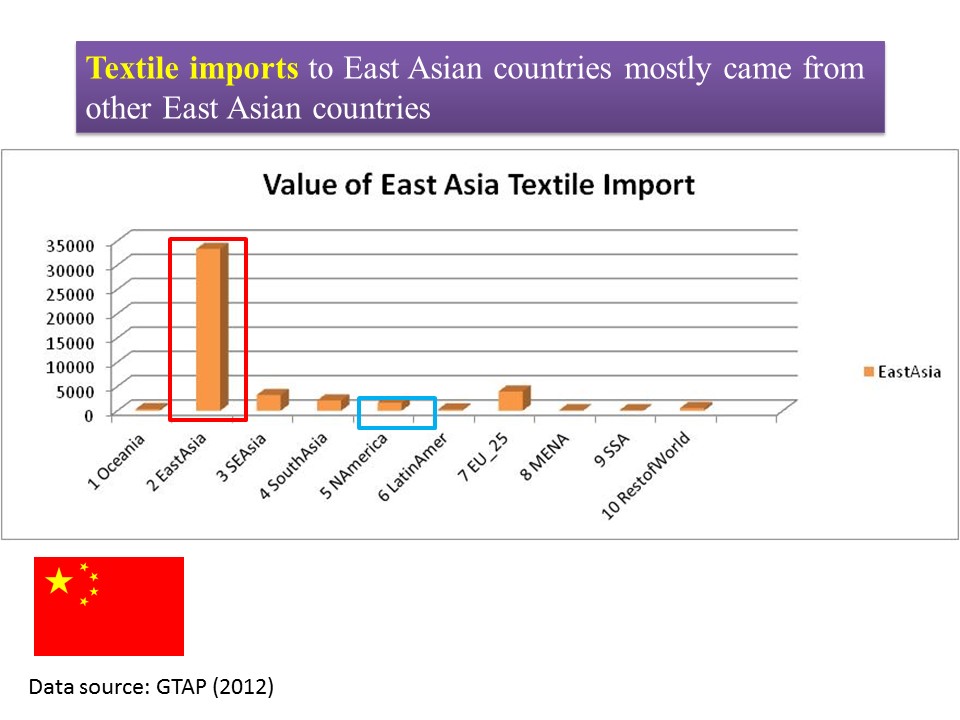

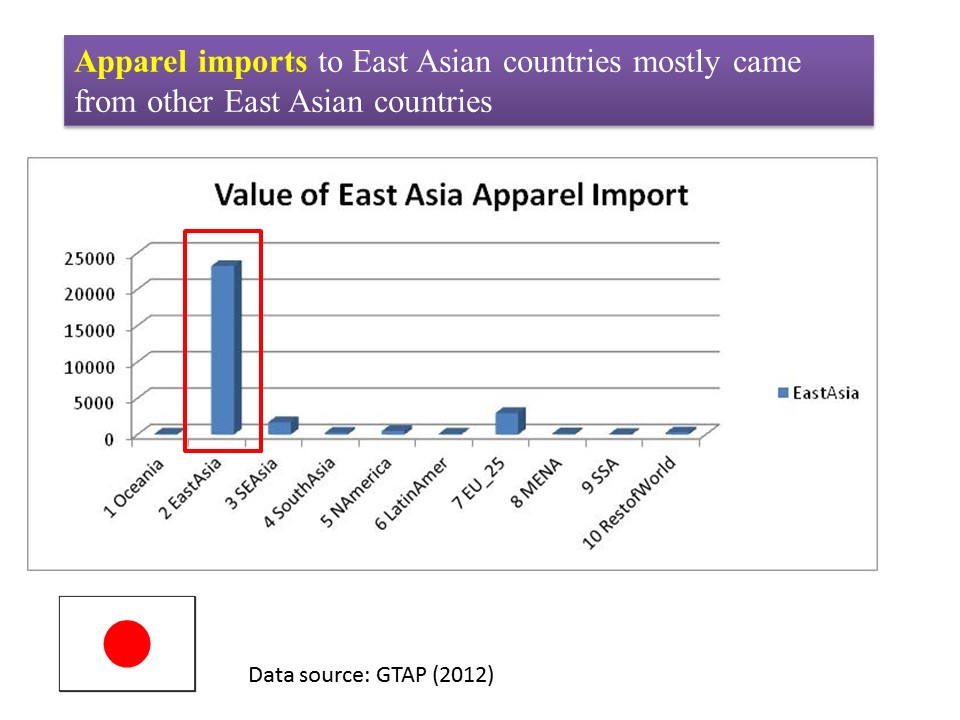

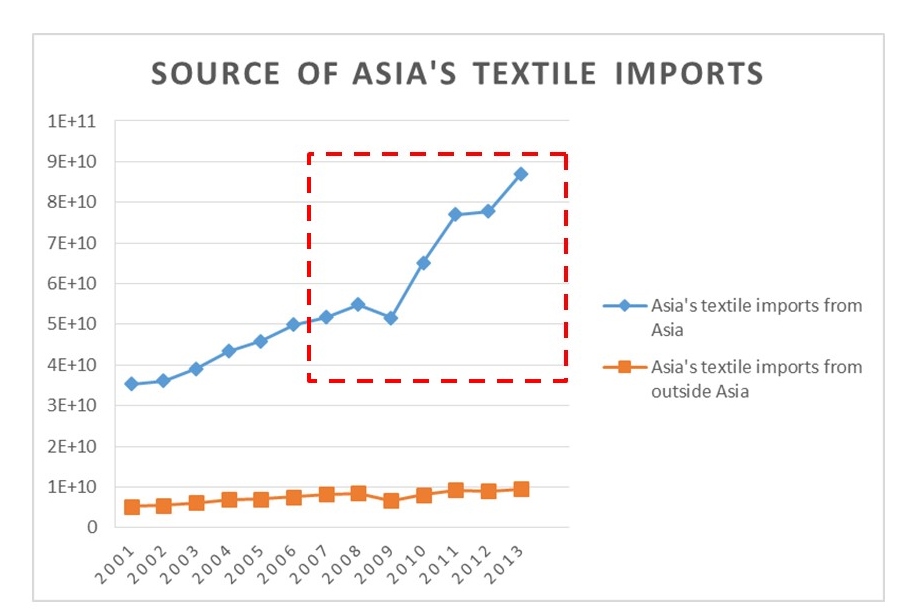

The latest trade data indicated that Asia’s regional textiles and clothing trade patterns strengthened further despite supply chain chaos during the pandemic. Specifically, in 2021, as many as 82% of Asian countries’ textile imports came from within Asia, up from 80% in 2015. China, in particular, has played a more prominent role as a leading textile supplier for other Asian clothing-exporting countries. For example, more than 60% of Vietnam’s textile imports came from China in 2021, a substantial increase from 23% in 2005. The same pattern applied to Pakistan, Cambodia, Bangladesh, and the Association of Southeast Asian Nations (ASEAN) members.

In January 2022, the Regional Comprehensive Economic Partnership (RCEP), a mega free trade agreement involving all major economies in Asia, entered into force. The tariff cut and very liberal rules of origin of the agreement will hopefully drive Asia’s booming regional textiles and clothing trade and further deepen its regional economic integration.

Besides Asia, the regional textiles and clothing trade pattern in the EU (or the so-called Intra-EU trade) was also in good shape. In 2021, 50.8% of EU countries’ textile imports and 37% of clothing imports came from other EU members. This pattern has changed little over the past decade, thanks to many EU countries’ commitment to maintaining local textiles and clothing production rather than outsourcing.

In comparison, the Western Hemisphere (WH) textile and apparel supply chain (e.g., clothing made in Mexico or Central America using US or regionally made textiles) seemed to struggle in recent years. As of 2021, only 20% of WH countries’ textile imports came from within WH, down from 26% in 2015. Likewise, WH countries (mainly the US and Canada) just imported 14.6% of clothing from WH in 2021, down from 15.3% in 2015 and much lower than their EU counterparts (37% in 2021). It will be interesting to see whether US and Canadian fashion companies’ expressed interest in expanding near-shoring may reverse the course.

Furthermore, the regional textiles and clothing trade patterns in Sub-Saharan Africa (SSA) are also worth watching. Compared with Asia and the EU, SSA clothing producers used much fewer locally-made textiles (i.e., stagnant at around 11% only from 2011 to 2021), reflecting the region’s lack of textile manufacturing capability. Most trade programs with SSA countries, such as the US-led African Growth and Opportunity Act (AGOA) and EU’s Everything But Arms (EBA) program, adopt liberal rules of origin for clothing products, allowing third-party textile input to be used. It can be studied whether such liberal rules of origin somehow disincentivize building SSA’s own textile manufacturing sector or are still essential given the reality of SSA’s limited textile production capacity.

Question: What does a typical day look like during your AAFA internship?

Ally: I would arrive at American Apparel and Footwear Association (AAFA)’s beautiful DC office, take the elevator up to the third floor, greet the two other interns, and make my way over to my desk. For the policy interns, our typical day consisted of working on individual projects and attending committee meetings, such as the weekly Social Responsibility Committee call with member companies, environmental and product safety meetings, trade policy meetings, and others. We also took notes on hearings and events and paid particular attention to topics related to the apparel sector. For example, I listened in and took notes on Hill hearings, workshops hosted by the World Trade Organization (WTO), and International Labour Organization (ILO) meetings. Some additional internship projects included updating country sourcing profiles for AAFA member companies to use in their factory selection process and analyzing trade data.

A very exciting and beneficial component of the AAFA internship experience was being able to attend special industry events such as the Washington International Trade Association (WITA) dinner and AAFA’s Annual Traceability and Sustainability Conference in Pittsburgh, PA. The WITA dinner is often referred to as “Trade Prom” and is packed with a ‘Who’s Who of trade policy professionals–over 500 attendees each year. Volunteering at this event with the other AAFA and WITA interns was incredible. The AAFA 2022 Traceability and Sustainability Conference in Pittsburgh, PA was another highlight of my internship experience. The conference took place at the American Eagle corporate headquarters, which was very exciting to tour. I spent three days in Pittsburgh with the AAFA team and heard presentations from top leaders in the fashion sustainability space, which was a dream! Member retailers spoke about what their companies are working on, what key challenges the industry faces, and how brands can collectively make a difference. It was a truly inspiring event and a phenomenal networking opportunity. This was an experience I will never forget!

Question: Any major projects did you work on during your internship? What did you learn from the experiences?

Ally:One of the main projects I worked on during my internship was updating AAFA’s Sourcing Profiles for their member companies. These country-specific sourcing profiles include essential information relevant to apparel companies’ sourcing decisions, such as a country’s political situation, minimum wage, membership in trade agreements, and economic outlook. Updating these sourcing profiles allowed me to understand why fashion brands and apparel retailers choose to source from particular countries over others. Having this solid background knowledge of leading apparel-sourcing destinations helps me tremendously, especially given that I am very interested in pursuing a career in sourcing. Some other projects I worked on include analyzing the latest US import patterns for travel goods and creating a “Corporate Social Responsibility Checklist” for AAFA members.

Question: What insights did you learn about the fashion apparel industry from the internship? For example, the key issues the industry cares about or the challenges it faces.

Ally: Through this highly valuable internship with AAFA, I saw the fashion industry through a unique policy and “DC” perspective. A key issue the industry cares about is sustainability. For example, fashion companies are increasingly implementing more and more environmentally and socially responsible business practices. Many leading US apparel brands shared their perspectives on building a more sustainable and transparent fashion supply chain at AAFA’s Traceability and Sustainability Conference. Fashion companies are also investing in innovative new technologies to work toward a closed-loop, circular economy.

Another challenge the fashion industry faces today is improving the supply chain’s transparency. For example, the alleged forced labor in China’s Xinjiang region is a huge concern to US apparel companies. With the recent implementation of the Uyghur Forced Labor Prevention Act (UFLPA) in June 2022, many US fashion brands and retailers are seeking advice on how to comply with this new law and minimize potential sourcing disruptions. Now, more than ever, apparel companies need to ensure they can map their supply chains all the way back to the very beginning, such as where they source their raw cotton.

There is also much interest among fashion companies in finding new sourcing destinations outside of China. For example, Sri Lanka sees this as an opportunity, as well as other developing countries such as Vietnam and Cambodia. We could see some notable shifts in US fashion companies’ sourcing patterns in the coming years.

Further, this Fall, I have been interning virtually at Worldwide Responsible Accredited Production (WRAP). WRAP is a non-profit organization headquartered in Arlington VA, with staff worldwide. WRAP certifies factories in the apparel, footwear, and sewn-products sector regarding their social responsibility performance. WRAP helps factories achieve this certification by conducting audits and working with factories directly to improve working conditions. AAFA and WRAP work closely with one another on numerous projects and industry events, and it has been wonderful to connect these two internship experiences. For example, I read and studied factory audit reports at WRAP. This allowed me to see fashion companies’ and auditors’ respective perspectives when examining a factory’s social compliance. Something that I took away from both internships is that garment factories could use auditing as an opportunity rather than a burden. By investing time and energy into improving factory working conditions and getting certified by a third-party organization, such as WRAP, a factory can attract more retailers, gain more business, and provide a better working environment for its workers.

Question: How do your learning experiences at FASH help with your internship? Any specific knowledge or skillsets do you find most critical?

Ally:My learning experiences in the UD’s FASH department were what influenced and inspired me to pursue the internship with AAFA and now with WRAP. FASH455 (Global apparel trade and sourcing), specifically, is what sparked my interest in apparel sourcing, supply chain, and trade. Before taking this class, I certainly had not thought about how free trade agreements affect the fashion industry. I found all the sourcing rules of origin such as “yarn-forward” and “fabric-forward” to be interesting and intriguing and I was eager to learn more. That is part of what led me to seek out these fashion opportunities in DC.

What I’ve learned through my time in the FASH department is that there are so many career directions a fashion merchandising degree can take you. Fashion is not all about runway shows and magazines- although those elements are very exciting. Many people often do not think about so many other aspects of the industry, like sourcing and trade. The fashion department at UD does a great job in providing students with a well-rounded education and improving students’ critical thinking skills, writing skills, data analytic skills, as well as other skills useful in preparing us for our future careers.

Being selected as a UD Summer Scholar during the Summer of 2021 was another fascinating and unique learning experience, which allowed me to begin researching an area of the fashion industry that I am most interested in–sustainability. Specifically, working with Dr. Lu, I researched US fashion retailers’ merchandising and marketing strategies for clothing made from recycled materials. I expanded the Summer Scholar’s research project into my master’s thesis which was recently published in the Journal of Fashion Design, Technology and Education. This is super exciting!

Choosing the University of Delaware and its fashion department for my education was the best choice I could have made. I have such positive memories such as my first business of fashion class with Professor Ciotti, my assortment planning and buying class with Professor Shaeffer, where we simulated working for a department store, and Dr. Cao’s sustainability and textile courses. Being Co-President of the Sustainable Fashion Club was also a highlight of my time in the FASH department. All of my coursework and experiences in the FASH department gave me the confidence needed to succeed in my internship and work experiences.

Question: What’s your plan after graduation?

Ally: I am currently nearing graduation from my Master’s program. I am on track to receive my Master’s degree in Spring 2023 (or earlier!). I am looking for full-time job opportunities in the realm of fashion sourcing, sustainability, and supply chain. I am hoping to live in either New York or DC after graduation, depending on what job opportunities become available. I am also keeping an open mind to other locations/job prospects. I am eager and excited to start my career in an industry that I am so passionate about, and I look forward to seeing where the future takes me!

Apparel is a $2.5 trillion global business, involving over 120 million workers worldwide and playing a uniquely critical role in the post-COVID economic recovery. The session intends to facilitate constructive dialogue regarding the progress, challenges, and opportunities of building a more resilient and sustainable fashion apparel supply chain in the Post-COVID world, which matters significantly to ALL stakeholders, from fashion brands, garment workers, and policymakers to ordinary consumers. The session will explore: 1) Why does building a more resilient and sustainable fashion apparel supply chain matter in the post-COVID world? What role can trade and trade policy play? 2) What significant progress has made the apparel supply chain more resilient and sustainable? What key challenges remain and why? 3) What needs to be done further to make the apparel supply chain more resilient and sustainable, particularly in the post-COVID world?

Panelists:

Dr. Arianna Rossi, Senior Research and Policy Specialist, International Labour Organization (ILO)

Ralph Kamphöner, Head of EU Office, Confederation of the German Textile and Fashion Industry

Dr. Sheng Lu, Associate Professor of Fashion and Apparel Studies, University of Delaware

Kekeli Ahiable, Advisor, Tony Blair Institute

Laura Husband, Just Style, Managing Editor (Moderator)

About the 2022 World Trade Organization (WTO) Public Forum

The 2022 WTO Public Forum, held from Sep 27 to 30, in Geneva, Switzerland) looked at how trade can contribute to post-pandemic economic recovery. The Forum examined, in particular, how trade rules can be strengthened, and government policies improved to create a more resilient, sustainable, and inclusive trading system. The Forum included three subthemes: Leveraging technology for an inclusive recovery, Delivering a trade agenda for a sustainable future, Framing the future of trade.

The virus is here to stay. What steps the companies must take to mitigate its impact?

Sheng: Earlier this year, I, together with the US Fashion Industry Association, surveyed about 30 leading US fashion brands and retailers to understand COVID-19’s impact on their sourcing practices. Respondents emphasized two major strategies they adopted in response to the current market environment. One is to strengthen the relationship with key vendors, and the other is to improve flexibility and agility in sourcing. These two strategies are also highly connected. As one respondent told us “We’re adjusting our sourcing model mix (direct vs. indirect) & establishing stronger strategic supplier relationships across entire matrix continue to build flexibility and dual sourcing options.” Many respondents, especially those large-scale fashion brands and retailers, also say they plan to reduce the number of vendors in the next few years to improve operational efficiency and obtain greater leverage in sourcing.

Which are the countries benefitting out of the US-China tariff war and why?

Sheng:The trade war benefits nobody, period. Today, textiles and apparel are produced through a highly integrated supply chain, meaning the US-China tariff war could increase everyone’s production and sourcing costs. Back in 2018, when the tariff war initially started, the unit price of US apparel imports from Vietnam, Bangladesh, and India all experienced a notable increase. Whereas companies tried to switch their sourcing orders, the production capacity was limited outside China. Meanwhile, China plays an increasingly significant role as a leading textile supplier for many apparel exporting countries in Asia. Despite the trade war, removing China from the textile and apparel supply chain is impossible and unrealistic.

How do you compare the African and Asian markets when it comes to sourcing and manufacturing? Which are the advantages both offer?

Sheng: Asia as a whole remains the world’s dominant textile and apparel sourcing base. According to statistics from the United Nations (i.e., UNComtrade), Asian countries as a whole contributed about 65% of the world’s total textile and apparel exports in 2020. In the same year, Asian countries altogether imported around 31% of the world’s textiles and 19% of apparel. Asian countries have also established a highly efficient and integrated regional supply chain by leveraging regional free trade agreements or arrangements. For example, as much as 85% of Asian countries’ textile imports came from other Asian countries in 2019, a substantial increase from only 70% in the 2000s. With the recent reaching of several mega free trade agreements among countries in the Asia-Pacific region, such as the Regional Comprehensive Economic Partnership (RCEP), the pattern of “Made in Asia for Asia” is likely to strengthen further.

In comparison, only about 1% of the world’s apparel imports come from Africa today. And this percentage has barely changed over the past decades. Many western fashion brands and retailers have expressed interest in expanding more apparel sourcing from Africa. However, the tricky part is that these fashion companies are hesitant to invest directly in Africa, without which it is highly challenging to expand African countries’ production and export capacity. Political instability is another primary concern that discourages more investment and sourcing from Africa. For example, because of the recent political turmoil, Ethiopia, one of Africa’s leading apparel sourcing bases, could be suspended for its eligibility for the African Growth and Opportunity Act (AGOA). Without AGOA’s critical support, Ethiopia’s apparel exports to the US market could see a detrimental decline. On the other hand, while these trade preference programs are crucial in supporting Africa’s apparel exports, they haven’t effectively solved the structural issues hindering the long-term development of the textile and apparel industry in the region. More work needs to be done to help African apparel producers improve their genuine export competitiveness.

Another issue is Brexit. Is that having any significant impact on the sourcing scenario of the world or is it just limited to the European nations?

Sheng: Despite Brexit, the trade and business ties between the UK and the rest of the EU for textile and apparel products continue to strengthen. Thanks to the regional supply chain, EU countries remain a critical source of apparel imports for UK fashion brands and apparel retailers. Nearly 35% of the UK’s apparel imports came from the EU region in 2019, a record high since 2010. Meanwhile, the EU region also is the single largest export market for UK fashion companies—about 79% of the UK’s apparel exports went to the EU region in 2019 before the pandemic.

However, trade statistics in the short run may not fully illustrate the impacts of Brexit. For example, some recent studies suggest that Brexit has increased fashion companies’ logistics costs, delayed customs clearance, and made talent-hiring more inconvenient. Meanwhile, Brexit provides more freedom and flexibility for the UK to reach trade deals based on its national interests. For example, the UK recently submitted its application to join the Comprehensive Progressive Agreement of the Trans-Pacific Partnership (CPTPP). The UK is also negotiating a bilateral trade agreement with the United States. The reaching of these new trade agreements, particularly with non-EU countries, could significantly promote the UK’s luxury apparel exports and help the UK diversity its source of imports.

How do you think the power shortages happening across Europe, China, and other nations, are going to impact the apparel supply chains?

Sheng: One of my primary concerns is that the new power shortage could exacerbate inflation further and result in a more severe price hike throughout the entire textile and apparel supply chain. When Chinese factories are forced to cease production because of power shortage, the impact could be far worse than recent COVID-related lockdowns in Vietnam and Bangladesh. As mentioned earlier, more than half of many leading Asian apparel exporting countries’ textile supplies come from China today. Also, no country can still compete with China in terms of the variety of apparel products to offer. In other words, for many western fashion brands and retailers, their stores and shelves could look more empty (i.e., having less variety of products to sell) because of China’s power shortage problem.

According to the World Trade Statistical Review 2021 report released by the World Trade Organization (WTO), the textiles and apparel trade patterns in 2020 include both continuities and new trends affected by the pandemic and companies’ evolving production and sourcing strategies in response to the shifting business environment.

Pattern #1: COVID-19 significantly affected the world textile and apparel trade volumes, resulting in substantial growth of textile exports and a declined demand for apparel.

Driven by increased personal protective equipment (PPE) production, global textile exports grew by 16.1% in 2020, reaching $353bn. In comparison, affected by lockdown measures, worsened economy, and consumers’ tighter budget for discretionary spending, global apparel export decreased by nearly 9% in 2020, totaling $448bn, the worst performance in decades. The apparel sector is not alone. The world merchandise trade in 2020 also suffered an unprecedented 8% drop from a year ago, with COVID-19 to blame.

Notably, as economic activities returned in the second half of 2020, the world clothing export quickly rebounded to around 95% of the pre-covid level by the end of 2020. That being said, the unexpected resurgence of COVID cases in summer 2021, especially the delta variant, caused new market uncertainties. Overall, the world textile and apparel trade recovery process from COVID-19 will differ from our experiences during the 2008 global financial crisis.

Pattern #2: COVID-19 did NOT shift the competitive landscape of the world textile exports; Meanwhile, textile exports from China and Vietnam gained new momentum during the pandemic.

China, the European Union (EU), and India remained the world’s three largest textile exporters in 2020. Together, these top three accounted for 65.8% of the world’s textile exports in 2020, similar to 66.9% before the pandemic (2018-2019).

Notably, China and Vietnam enjoyed a substantial increase in their textile exports in 2020, up 28.9% and 10.7% from a year ago, respectively. The complete textile and apparel supply chain and considerable production capability allow these two countries to switch clothing production to PPE manufacturing quickly. In particular, Vietnamexceeded South Korea and ranked the world’s sixth-largest textile exporter in 2020 ($10 bn of exports), the first time in history.

The United States dropped one place and ranked the world’s fifth-largest textile exporter in 2020 (was 4th from 2015 to 2019), accounting for 3.2% of the shares (was 4.4% in 2019). Production disruptions at the beginning of the pandemic and the shift toward PPE production for domestic consumption were the two primary contributing factors behind the decline in U.S. textile exports. Due to the regional trade patterns, around 67% of U.S. textile exports went to the Western Hemisphere in 2020, including 46% for members of the U.S.-Mexico-Canada Trade Agreement (USMCA) and another 17.2% for members of the Dominican Republic-Central America Free Trade Agreement (CAFTA-DR).

Pattern #3: Fashion companies’ efforts to diversify apparel sourcing from China somehow slowed during the pandemic.

China, the European Union, Vietnam, and Bangladesh unshakably remained the world’s four largest apparel exporters in 2020. Altogether, these top four accounted for 72.2% of the world market shares in 2020, higher than 71.4% in 2019.

Notably, while China steadily accounted for declining shares in the world’s total apparel exports since 2015, its market shares rebounded to 31.6% in 2020 from 30.7% in 2019. We can observe a similar pattern in Canada (up from 36.2% to 41.2%) and the EU (31.2% to 31.3%), two of the world’s leading apparel import markets. Even in the U.S. market, where Chinese goods face adverse impacts of the tariff war, the market shares of “Made in China” only marginally decreased from 30.8% in 2019 to 29.8% in 2020, compared with a more significant drop before the pandemic (i.e., fell from 34.4% 2018 to 30.8% in 2019).

Several factors could explain the resilience of China’s apparel exports: 1) fashion brands and retailers’ particular sourcing criteria match China’s competitiveness during the pandemic (e.g., flexibility, agility, and total landed sourcing cost). 2) China has one of the world’s most complete textile and apparel supply chains, allowing garment factories to access textile raw material and accessories locally. 3) Compared with many other apparel exporting countries, China suffered a shorter COVID lockdown period and resumed apparel production earlier and more quickly. Most Chinese textile and apparel factories started to reopen in April 2020, and they resumed an overall 90%-95% operational capacity rate by July 2020.

Nonetheless, fashion companies are NOT reversing their long-term strategies to reduce “China exposure” for apparel sourcing. On the contrary, non-economic factors, particularly the concerns about forced labor in China’s Xinjiang region, push most western fashion brands and retailers to develop apparel sourcing capacities beyond China. Meanwhile, no single country has yet and will likely become the “Next China” because of capacity limits. Instead, from 2015 to 2020, China’s lost market shares in the world apparel exports (around 7.8 percentage points) were picked up jointly by its competitors in Asia, including ASEAN members (up 4.4 percentage points), Bangladesh (up 1.3 percentage points), and Pakistan (up 0.3 percentage point). Such a trend is most likely to continue in the post-COVID world.

Pattern #4: Developed economies led textile PPE imports during the pandemic, whereas the developing countries imported fewer textiles as their apparel exports dropped.

On the one hand, the value of textile imports by developed economies, including EU members, the United States, Japan, and Canada, surged by more than 30 percent in 2020, driven mainly by their demand for PPE. The result also reveals the significant contribution of international trade in supporting the supply and distribution of textile PPE globally. On the other hand, the developing countries engaged in apparel production and export drove the import demand for textile raw materials like yarns and fabrics. However, most of these developing countries’ textile imports fell in 2020, corresponding to their decreased apparel exports during the pandemic.

Pattern #5: Despite COVID-19, the world apparel import market continues to diversify. The import demand increasingly comes from emerging economies with a booming middle class.

Affected by consumers’ purchasing power (often measured by GDP per capita) and the size of the population, the European Union, the United States, and Japan remained the world’s three largest apparel importers in 2020, a stable pattern that has lasted for decades. While these top three still absorbed 56.2% of the world’s apparel imports in 2020, it was a new record low in the past ten years (was 58.1% in 2019 and 61.5% in 2018), and much lower than 84% back in 2005.

Behind the numbers, it is not the case that consumers in the EU, the United States, and Japan necessarily purchase less clothing over the years. Instead, several emerging economies have become fast-growing apparel-consuming markets with robust import demand. For example, despite COVID-19, China’s apparel imports totaled $9.5bn in 2020, up 6.5% from 2019. From 2010 to 2020, China’s apparel imports enjoyed a nearly 15% annual growth, compared with only 0.56% of the traditional top three. Around 30% of China’s apparel imports today are luxury items made in the EU.

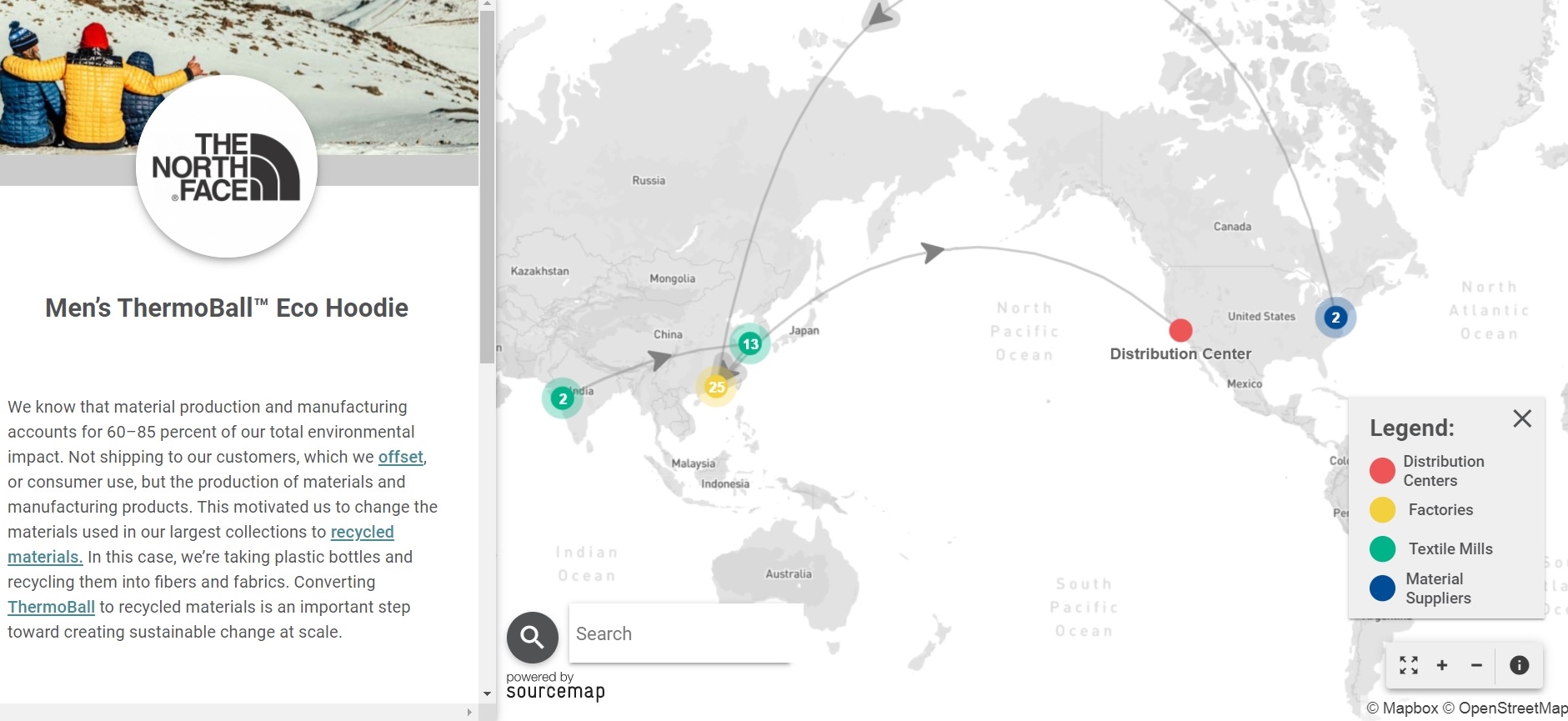

Sourcing map: North Face–Men’s Thermoball Eco Hoodie

#1 Why or why not do you think VF Corporation should de-globalize its supply chain—for example, bringing more sourcing and production back to the United States?

#2 Given such a globalized operation, should we still call VF Corporation an American company? Also, does the label “Made in ___” still matter today?

#3 Is the sole benefit of globalization helping us get cheaper products? How to convince US garment workers who lost their jobs because of increased import competition that they benefit from globalization also?

#4 How has COVID-19 changed your understanding of the benefits, costs, and debates on globalization? Do we still need globalization in a post-COVID world? Why?

#5 Throughout history, globalization has been viewed as a two-sided debate with social groups weighing its benefits and negative costs. With the emergence of COVID-19, how do you think certain social groups’ opinions towards globalization will change?

(Welcome to our online discussion. For students in FASH455, please address at least two questions and mention the question number (#) in your reply)

Minute 1’53s: What’s wrong with the view that trade is a zero-sum game.

Minute 4’50s: A review of the concept of comparative advantage by using the textile and apparel industry as an example.

Minute 7’30s: What is trade protectionism?

Minute 9’02s: Why did the United States brace the idea of free trade after WWII and push forward the establishment of the multilateral trading system GATT?

Minute 10’30s: what drives the U.S. trade deficit from the economic perspective?

Minute 15’57s: international trade and U.S. apparel manufacturing jobs

First, the volume of world textiles and apparel trade reduced in 2019 due to weakened demand and the negative impacts of trade tensions. According to the WTO, the value of the world textiles (SITC 65) and apparel (SITC 84) exports totaled $305bn and $492bn in 2019, respectively, decreased by 2.4% and 0.4% from a year ago. The world merchandise trade also fell by nearly 3% measured by value and 0.1% measured by volume 2018-2019, in contrast with a positive 2.8% growth 2017-2018. Put these numbers in context, the year 2019 was the first time that world merchandise trade fell since the 2008 global financial crisis, and the decline happened even before the pandemic. As noted by the WTO, the economic slowdown and the escalating trade tensions, particularly the tariff war between the United States and China, were among the major contributing factors for the contraction of trade flows.

Second, the pattern of world textile exports overall stays stable in 2019; Meanwhile, China and Vietnam continue to gain momentum. China, European Union (EU28), and India remained the world’s top three exporters of textiles in 2019. Altogether, these top three accounted for 66.9% of the value of world textile exports in 2019, almost no change from two years ago. Notably, despite the headwinds, China and Vietnam stilled enjoy the positive growth of their textile exports in 2019, up 0.9%, and 8.3%, respectively. In particular, Vietnam exceeded Taiwan and ranked the world’s seventh-largest textile exporter in 2019 ($8.8bn of exports, up 8.3% from a year earlier), the first time in history. The change also reflects Vietnam’s efforts to continuously upgrade its textile and apparel industry and strengthen the local textile production capacity are paying off.

Third, the pattern of world apparel exports reflects fashion companies’ shifting strategies to reduce sourcing from China. China, the European Union (EU28), Bangladesh, and Vietnam unshakably remained the world’s top four exporters of apparel in 2019. Altogether, these top four accounted for as much as 71.4% of world market shares in 2019, which, however, was lower than 74% from 2016 to 2018—primarily due to China’s reduced market shares.

China is exporting less apparel and more textiles to the world. Notably, China’s market shares in world apparel exports fell from its peak of 38.8% in 2014 to a record low of 30.8% in 2019 (was 31.3% in 2018). Meanwhile, China accounted for 39.2% of world textile exports in 2019, which was a new record high. It is important to recognize that China is playing an increasingly critical role as a textile supplier for many apparel-exporting countries in Asia.

On the other hand, even though apparel exports from Vietnam (up 7.7%) and Bangladesh (up 2.1%) enjoyed fast growth in absolute terms in 2019, their gains in market shares were quite limited (i.e., no change for Vietnam and marginally up 0.3 percentage point from 6.8% to 6.5% for Bangladesh). This result indicates that due to capacity limits, no single country has yet emerged to become the “Next China.” Instead, China’s lost market shares in apparel exports were fulfilled by a group of Asian countries altogether.

Fourth, associated with the shifting pattern of world apparel production, the world textile import is increasingly driven by apparel-exporting countries in the developing world. Notably, 2019 marks the first time that Vietnam emerged to become one of the world’s top three largest importers of textiles, primarily due to its expanded apparel production and heavy dependence on imported textile raw materials. In comparison, although the US and the EU remain the world’s top two largest textile importers, their total market shares had declined from nearly 40% in 2010 to only 31.2% in 2019, the lowest in the past ten years. Furthermore, both the US and the EU have been importing more finished textile products (such as home furnishings and carpets) as well as highly specialized technical textiles, rather than conventional yarns and fabrics for apparel production purposes. The weakening import demand for intermediary textile raw materials also suggests that reshoring (i.e., making apparel locally rather than sourcing from overseas) has NOT become a mainstream industry practice in the developed economies like the US and the EU.

Fifth, the world apparel import market is becoming ever more diversified as import demand is increasingly coming from emerging economies with a booming middle class. Affected by consumers’ purchasing power (often measured by GDP per capita) and size of the population, the European Union (EU28), US, and Japan remained the world’s top three importers of apparel in 2019. This pattern has lasted for decades. Altogether, these top three absorbed 58.1% of world apparel in 2019, which, however, was a new historic low (was 84% back in 2005). Behind the numbers, it is not the case that consumers in the EU, US, and Japan are necessarily purchasing less clothing. Instead, several emerging economies are becoming fast-growing apparel consumption markets and starting to import more. For example, China’s apparel imports totaled $8.9bn in 2019, up 8.1% from a year earlier. From 2010 to 2019, China’s apparel imports enjoyed a nearly 15% annual growth, compared with only 1.9% of the traditional top three.

The top challenge facing apparel sourcing and trade in the shadow of Covid-19 has quickly shifted from a lack of textile raw material to order cancellation. In major apparel consumption markets such as the EU and US, clothing stores are locked down, making retailers have no choice but to postpone or even cancel sourcing orders.

Based on the Global Trade Analysis Project Recursive Dynamic (GTAP-RD) Model and its latest database, we estimated the trade impact of Covid-19 in three possible scenarios, as summarized in the table below. All these three scenarios are pretty bad but likely situations we may have to face this year. (Note: Because China, US, and EU are the epic-centers of Covid-19, in the study, we assume these three countries/regions’ economies will be hit harder than the rest of the world.)

There are four preliminary findings:

First, the volume of the world apparel trade will be hit hard by Covid-19. As clothing stores are forced to shut down and consumers are losing jobs and struggling financially, the demand for apparel consumption in the EU and US, the world’s top two apparel consumption markets, is expected to drop sharply. As shown in the figures below, every 1% decline in the US and EU Gross Domestic Product (GDP) in 2020 could lead to at least a 2-3% drop in the value of their apparel imports. Notably, during the 2008 financial crisis, the value of world apparel imports also decreased by as much as 11.5% when the EU and US GDP suffered a 2.5-3% negative growth.

Second, with a sharp decline in U.S. and EU apparel imports this year, China could be hit the hardest. In all the three scenarios we estimated, China will suffer the most significant drop in its apparel exports to the US and EU markets. The reasons are threefold: The first factor is the size effect—as the largest source of US and EU apparel imports and with its unparalleled production capacity, China is often used to fulfill large-volume sourcing orders. In the current situation, however, retailers are most likely to cancel these large-quantity orders, resulting in a disproportional loss of China’s apparel exports. Secondly, the US and EU apparel imports from China currently cover almost all major categories, which also makes China the most exposed to order cancellation. Furthermore, jointly affected by last year’s US-China trade war and the outbreak of Covid-19 in China earlier this year, many US and EU fashion brands and retailers have been shifting sourcing orders from China to other Asian countries, such as Bangladesh and Vietnam. To prioritize their limited resources, US and EU retailers are most likely to accelerate this process in the current difficult time.

Other than China, apparel factories in Bangladesh also could suffer severe export decline. Similar to the case of China, Bangladesh serves as a leading apparel supplier for BOTH the EU and US markets, making it more exposed to order cancellation than other countries. Notably, as a beneficiary of the EU Everything But Arms (EBA) program, around 60% of Bangladesh’s apparel currently go to the EU. In comparison, with a more diversified export market, apparel factories in Vietnam are in a better position and have more flexibility to mitigate the impact of a declined import demand from the EU and the US. In 2018, around 40% of Vietnam’s apparel exports went to other markets in the world.

Third, the decreased US and EU apparel imports will have a notable impact on employment in many apparel exporting countries.In history, a 10% change in the value of apparel exports typically results in a 4%-9% change in garment employment. This means, should the US and EU apparel imports drop by 10% in 2020, leading apparel exporting countries such as Bangladesh, Vietnam, Cambodia and India may have to cut 4%-9% of their jobs in the garment sector accordingly. Notably, in developing countries such as Bangladesh and Cambodia, the apparel sector remains the single largest job creator for the local economy, especially for women. The social and economic impact of job losses in the apparel sector due to Covid-19 is very concerning.

Fourth, the economic performance in the US, EU, and China will largely shape the pattern of apparel trade this year. The results in scenarios 1 and 2 overall are pretty close, suggesting the economic cloud of these three countries and regions altogether far exceed the rest of the world.

Last but not least, the global apparel supply chain could continue to face a turbulent time in the next 1-2 years, even if Covid-19 gradually gets under control in the second half of 2020. In history, affected by the 2008 global financial crisis, the value of world apparel exports dropped by 12.8% in 2009. However, the growth rate quickly rebounded to 11.5% the following year. Likewise, should the EU and US apparel imports were able to recover to its normal level in 2021, both importers and garment factories may have to deal with a new round of labor shortage, the price increase of raw material and a lack of production capacity.

In January 2018, Just-Style consulted a panel of industry leaders and scholars in its Outlook 2018–Apparel Industry Issues in the Year Ahead management briefing. Below is my contribution to the report. All suggestions and comments are most welcome!

1. What do you see as the biggest challenges – and opportunities – facing the apparel industry in 2018, and why?

One of the biggest opportunities facing the apparel industry in 2018 could be the faster growth of the world economy. According to the International Monetary Fund (IMF), the global growth forecast for 2018 is expected to reach 3.7 percent, about 0.1 percent points higher than 2017 and 0.6 percent points higher than 2016. Notably, the upward economic growth will be broad-based, including the United States, the Euro area, Japan, China, emerging Europe and Russia. Hopefully, the improved growth of the world economy will translate into increased consumer demand for clothing in 2018.

Nevertheless, from the macroeconomic perspective, oversupply will remain a significant challenge facing the apparel industry in 2018. Data from the World Bank and the World Trade Organization (WTO) shows that, while the world population increased by 21.6 percent between 2000 and 2016, the value of clothing exports (inflation-adjusted) surged by 123.5 percent over the same period. Similarly, between 2000 and 2016, the total U.S. population increased by 14.5 percent and the GDP per capita increased by 22.2 percent, but the supply of apparel to the U.S. retail market surged by over 67.8 percent during the same time frame. The problem of oversupply is the root of many challenges faced by apparel companies today, from the intense market competition, pressure of controlling production and sourcing cost, struggling with excessive inventory and deep discounts to balancing sustainability and business growth.

2: What’s happening with sourcing? How is the sourcing landscape likely to shift in 2018, and what can apparel firms and their suppliers do to stay ahead?

The 2017 US Fashion Industry Benchmarking Study, which I conducted in collaboration with the US Fashion Industry Association (USFIA) earlier this year, provides some interesting insights into companies’ latest sourcing strategies and trends. Based on a survey of 34 executives at the leading U.S. fashion companies, we find that:

First, most surveyed companies continue to maintain a relatively diversified sourcing base, with 57.6 percent currently sourcing from 10+ different countries or regions, up from 51.8 percent last year. Larger companies, in general, continue to have a more diversified sourcing base than smaller companies. Further, around 54 percent of respondents expect their sourcing base will become more diversified in the next two years, up from 44 percent in 2016; over 60 percent of those expecting to diversify currently source from more than 10 different countries or regions already. Given the uncertainties in the market and the regulatory environment (such as the Trump Administration’s trade policy agenda), companies may use diversification to mitigate potential market risks and supply chain disruptions due to protectionism.

Second, although U.S. fashion companies continue to seek alternatives to “Made in China” actively, China’s position as top sourcing destination remains unshakable. Many respondents attribute China’s competitiveness to its enormous manufacturing capacity and overall supply chain efficiency. Meanwhile, it is interesting to note that the most common sourcing model is shifting from “China Plus Many” to “China Plus Vietnam Plus Many” (i.e. China typically accounts for 30-50 percent of total sourcing value or volume, 11-30 percent for Vietnam and less than 10 percent for other sourcing destinations). I think this sourcing model will likely to continue in 2018.

Third, social responsibility and sustainability continue to grow in importance in sourcing decisions. In the study, we find that nearly 90 percent of respondents give more weight to sustainability when choosing where to source now than in the past. Around 90 percent of respondents also say they map their supply chains, i.e., keeping records of name, location, and function of suppliers. Notably, more than half of respondents track not only Tier 1 suppliers, suppliers they contract with directly, but also Tier 2 suppliers, i.e., supplier’s suppliers. However, the result also suggests that a more diversified sourcing base makes it more difficult to monitor supply chains closely. Making the apparel supply chain more socially responsible, sustainable and transparent will continue to be a hot topic in 2018.

3: What should apparel firms and their suppliers be doing now if they want to remain competitive further into the future? What will separate the winners from the losers?

I assume many experts will suggest what apparel firms should change to stay competitive into the future. However, the question in my mind is what should companies keep doing regardless of the external business environment? First, I think companies should always strive to understand and impress consumers and control their supply chains. Despite the growing popularity of e-commerce and the adoption of transformative new technologies, the fundamental nature of apparel as a buyer-driven business will remain the same. Second, companies should always leverage their resources and stay “unique,” no matter it means offering differentiated products or value-added services, maintaining exclusive distribution channels or keeping the leadership position in a particular niche market. Third, apparel firms should always follow the principle of “comparative advantage” and smartly define the scope of their core business functions instead of trying to do everything. Additionally, winners will always be those companies that can take advantage of the mega-development trends of the industry and be willing to make long-term and visionary investments, both physical and intangible (such as human talents).

4: What keeps you awake at night? Is there anything else you think the apparel industry should be keeping a close eye on in the year ahead? Do you expect 2018 to be better than 2017, and why?

I think the apparel industry should keep a close eye on the following issues in 2018:

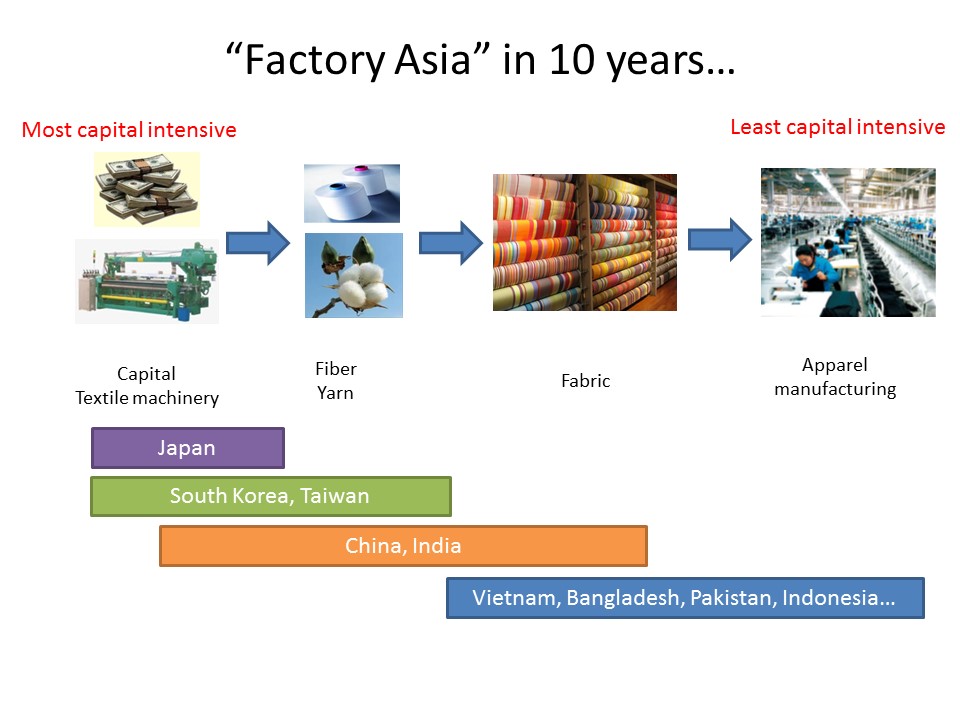

The possible reaching of the Regional Comprehensive Economic Partnership (RCEP): Even though RCEP is less well-known than the Trans-Pacific Partnership (TPP), we should not ignore the potential impact of the agreement on the future landscape of textile and apparel supply chain in the Asia-Pacific region. One recent study of mine shows that the RCEP will lead to a more integrated textile and apparel supply chain among its members but make it even harder for non-RCEP members to get involved in the regional T&A supply chain in the Asia-Pacific. This conclusion is backed by the latest data from the World Trade Organization (WTO): In 2016, around 91 percent of Asian countries’ textile imports came from other Asian countries, up from 86 percent in 2006. The more efficient regional supply chain as a result of RCEP will further help improve the price competitiveness of apparel made by “factory Asia” in the world marketplace. Particularly in the past few years, textile and apparel exports from Asia have already posted substantial pressures on the operation of the textile and apparel regional supply chain in the Western Hemisphere.

Automation of apparel manufacturing and its impact on the job market: Recall my observations at the MAGIC this August, several vendors showcased their latest technologies which have the potential to automate the cut and sew process entirely or substantially reduce the labor inputs in garment making. The impact of automation on the future of jobs is not a new topic, but the apparel industry presents a unique situation. Globally, over 120 million people remain directly employed in the textile and apparel industries today, a good proportion of whom are females living in poor rural areas. According to the World Trade Organization (WTO), for quite a few low-income and lower-middle income countries such as Bangladesh, Gambia, Pakistan, Madagascar, Sri Lanka, and Cambodia, as much as over 70 percent of their total merchandise exports were textile and apparel products in 2016. Should these labor-intensive garment sewing jobs in the developing countries were replaced by machines, the social and economic impacts will be consequential. I think it is the time to start thinking about the possible scenarios and the appropriate policy responses.

Dr. Marsha Dickson, Irma Ayers Professor, Department of Fashion and Apparel Studies at the University of Delaware discusses her co-founded Better Buying project(http://www.betterbuying.org), a meaningful effort to improve the social responsibility practices in the global apparel industry. The video is produced by Mallory Metzner, reporter of channel 49 of the University of Delaware.

During the talk, Gail made a few comments regarding trade policy in the Trump administration:

First, Gail believes that the existing U.S. free trade agreements (FTAs), trade preference programs (PTAs) and the U.S. commitments at the World Trade Organization (WTO) are unlikely to be undone by President Trump because retaliatory actions from other trading partners would be inevitable.

Second, regarding the North American Free Trade Agreement (NAFTA), Gail doesn’t think the proposed renegotiation would threaten the benefits presently enjoyed by the U.S. textile and apparel industry. Gail also thinks the Central America Free Trade Agreement (CAFTA-DR) is a lifeline for the U.S. domestic textile manufacturing sector. Notably, NAFTA and CAFTA-DR together account for almost 70% of U.S. yarn and fabric exports.

Third, as observed by Gail, Wilbur Ross, the Commerce Secretary, has been given an expanded role in trade in the Trump Administration. Gail believes Ross’s appointment is likely to bode well for NAFTA and CAFTA-DR on textiles because Ross until recently owned the International Textile Group (ITG), which has significant investments in Mexico and relies heavily on CAFTA-DR for its textile sales.

However, Gail doesn’t think concentrating on trade deficits to define trade policy is a very “good method” of navigating the trade world. Interesting enough, last time when the U.S. trade deficit significantly shrank was during the 2008 financial crisis.

Gail is also a strong advocator of sustainability in the textile and apparel sector. She believes that trade programs can play a vital role in encouraging sustainable development, improving labor practices and facilitating sustainable regional supply chains. According to Gail, powerful the labor provisions in trade programs can be if strong incentives are coupled with a credible threat of rapid enforcement – little evidence of effectiveness if only one (or fewer) of these conditions is met. However, comparing with enforcing labor provisions, Gail finds promoting and enforcing environmental sustainability standards through trade agreements is much more complex in the textile and apparel sector and will require creativity and strong participation from private sectors and consumers.

Before the public lecture, Gail visited FASH455 and had a special discussion session with students on topics ranging from the textile and apparel rules of origin in TPP, NAFTA renegotiation, AGOA renewal and state of the U.S. textile and apparel industry.

In January 2017, Just-Style consulted a panel of industry leaders and scholars in its Outlook 2017–Apparel Industry Issues in the Year Ahead management briefing. Below is my contribution to the report. Welcome for any suggestions and comments.

1: What do you see as the biggest challenges – and opportunities – facing the apparel industry in 2017, and why?

I see the uncertainty in the global economy will pose one of the biggest challenges facing the apparel industry in 2017. Apparel business is buyer-driven. A great number of studies have suggested that economic growth is by far the most effective and reliable predictive factor for apparel consumption. Unfortunately, it seems apparel companies have to deal with another year of economic volatility and weak demand in 2017. For example, according to the latest International Monetary Fund (IMF) forecast released in October 2016, global economic growth in 2017 is projected to only recover to 3.4 percent from 3.1 percent in 2016. There is no particular excitement among major apparel consumption markets either: outlook of the U.S. economy in 2017 is complicated by the strong U.S dollar, the Federal Reserve’s monetary policy as well as the uncertain trade and tax policy to be adopted by the new Trump administration; Economic growth in the EU region next year will continue to be hindered by the unknown fallout from UK’s referendum on leaving the EU, pervasive geopolitical uncertainties, high unemployment rates and the rising protectionist tendencies; Japan’s economic growth is projected to be as low as 1.0 percent in 2017 according to the Organization for Economic Co-operation and Development (OECD); And China’s economic growth in 2017 could slow again to 6.5 percent, which would be the slowest pace in more than 25 years. Reflecting the trend, we might see a stagnant growth or even a decline of global textile and apparel trade in 2017 as well.

Nevertheless, companies’ continuous investments on technology and innovation will create exciting new opportunities for the apparel industry. Particularly, growing areas in the apparel industry such as 3D printing, wearable technology, digital prototyping and e-commerce have made many “non-traditional” players now interested in fashion, including technology giants like Google and Apple. I think we can expect the apparel industry to become even more modern and high-tech driven in the years to come. The changing nature of the apparel industry will also increase demand for talents from an ever more diversified educational background, such as engineering, physical therapy and business analytics.

2: What’s happening with sourcing? How is the sourcing landscape likely to shift in 2017, and what strategies can help apparel firms and their suppliers to stay ahead?

One observation from me is that textile and apparel (T&A) supply chain is becoming more regional-based. For example, data from the World Trade Organization (WTO) shows that 91.4 percent of textiles imported by Asian countries in 2015 came from other Asian countries, up from 86.6 percent in 2008. This suggests that Asian countries togetherare building a more integrated T&A supply chain. Likewise, in 2015 close to 90 percent of apparel exported by North, South and Central American countries went to the United States and Canada and 81 percent of apparel exported by EU countries went to other EU countries too. To be noted, all of these three major T&A supply chains are facilitated by respective free trade agreements in the region such as the North American Free Trade Agreement (NAFTA), ASEAN–China Free Trade Area (ACFTA) and of course the common market enjoyed by the EU members. On the other hand, fashion brands and apparel retailers often use the Western-Hemisphere supply chain and EU-based supply chain as a supplement to the Asia-based supply chain for more fashion-oriented or time-sensitive items. I think such a dual-track sourcing strategy will continue in 2017.

Related, I think supply chain management will play a growing important role helping apparel companies control sourcing cost, improve speed to market and better meet consumers’ demand in 2017. An interesting phenomenon revealed by the 2016 U.S. Fashion Industry Benchmarking Study released by the U.S. Fashion Industry Association is that around 30 percent of respondents say they plan to consolidate rather than diversify their sourcing base in the next 2 years. As one respondent commented, “(Our) focus right now is really finding efficiencies and maximizing productivity in the supply chain. While we won’t necessarily move out of any countries, we are consolidating the base within regions.”

Last but not least, I think in 2017 apparel companies will continue to give more weight to sustainability and social responsibility in their sourcing decisions. Building a more transparent and sustainable supply chain is an irreversible trend in the apparel industry.

3: What should apparel firms be doing now if they want to remain competitive into the future? What will separate the winners from the losers?

To remain competitive into the future, apparel companies need to be prepared to change and be willing to try something new. Indeed, revolution is coming for the apparel industry, including the way products are made and sourced (example: 3D printing and various digital manufacturing tools), how consumers shop (example: the see-now-buy-now trend) and where and how to sell (example: the booming e-commerce and omni-channel retailing). In the past, small and medium sized companies (SME) were regarded more vulnerable than big players in the apparel industry for business survival. However, nowadays, without embracing the spirit of innovation and entrepreneurship, even large companies can quickly become “dinosaurs” and find their business struggling.

4: What keeps you awake at night? Is there anything else you think the apparel industry should be keeping a close eye on in the year ahead? Do you expect 2017 to be better than 2016, and why?

One thing that keeps me awake at night as a professor is what needs to be changed or updated in our curriculum to better prepare our students for the needs of the apparel industry. Fashion programs like us directly prepare future professionals for the fashion apparel industry. This also means we are not immune to the big shift in the industry either. For example, our course offerings currently include textile science, product development, merchandising, branding and sourcing and trade. But in addition to these conventional topics, what else should be added to the curriculum? What new skill setsor knowledge points will be highly expected by the apparel industry for our students in the future? Personally I think talent training is a critical area that the apparel industry and our fashion educational programs can and should form closer partnership. And the outcomes will be mutual beneficial too.

Trade policy is another area that keeps me awake at night. Trade policy matters for the apparel industry because it affects the quantity, price and availability of products in the market. Specifically, in 2017 I will be watching closely about the following trade agendas: 1) the WTO Trade Facilitation Agreement (TFA), which is nearing entering into force. TFA aims to make customs and border procedures easier, speed up the passage of goods between countries and lower cost of trade.

2) negotiation of the Regional Comprehensive Economic Partnership (RCEP). In 2015, the sixteen RCEP members altogether exported $369 billion worth of textile and apparel (50% of world share) and imported $124 billion (34% of world share). Since the Trans-Pacific Partnership (TPP) won’t be implemented anytime soon, RCEP has the potential to influence and reshape the T&A supply chain in the Asia-Pacific region.

3) a possible revision of the North American Free Trade Agreement (NAFTA). NAFTA is a critical factor facilitating and maintaining the Western-Hemisphere textile and apparel supply chain. A recent study of mine shows that ending the NAFTA would significantly hurt apparel manufacturing in Mexico and textile manufacturing in the United States, largely because apparel “Made in Mexico” today often contains yarns and fabrics “Made in USA”.

4) Trans-Pacific Partnership (TPP) and Trans-Atlantic Trade and Investment Partnership (T-TIP). Although many people think these two agreements are dead, I disagree. TPP and T-TIP are NOT conventional free trade agreements (FTAs) that deal with tariffs and non-tariff barriers only. Just like why we need traffic rules, TPP and T-TIP address our needs to update international trade regulations on 21st century trade agendas such as digital trade, state-owned enterprises, labor and environmental standards, small and medium sized enterprises and trade related investment. On the other hand, both TPP and T-TIP still have a solid and broad supporting base, which includes the fashion apparel industry. If trade politics is why TPP and T-TIP are in trouble, for the same reason, we should expect a reversal of the fate of these two agreements when time arrives. Plus, we should never underestimate the creativity and wisdom of trade policymakers.

The latest Just-Style State of Sourcing Survey conducted in December 2016 suggests a few trends of apparel sourcing in 2017: