This study aims to understand western fashion brands and retailers’ latest China apparel sourcing strategies against the evolving business environment. We conducted a content analysis of about 30 leading fashion companies’ public corporate filings (i.e., annual or quarterly financial reports and earnings call transcripts) submitted from June 1, 2022 to December 31, 2022.

The results suggest several themes:

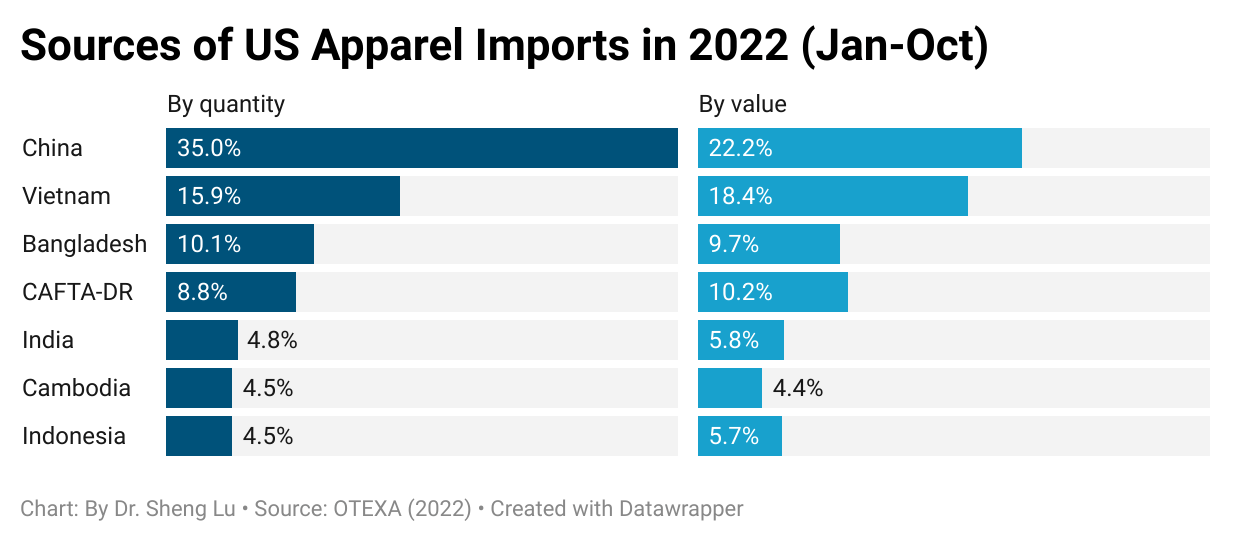

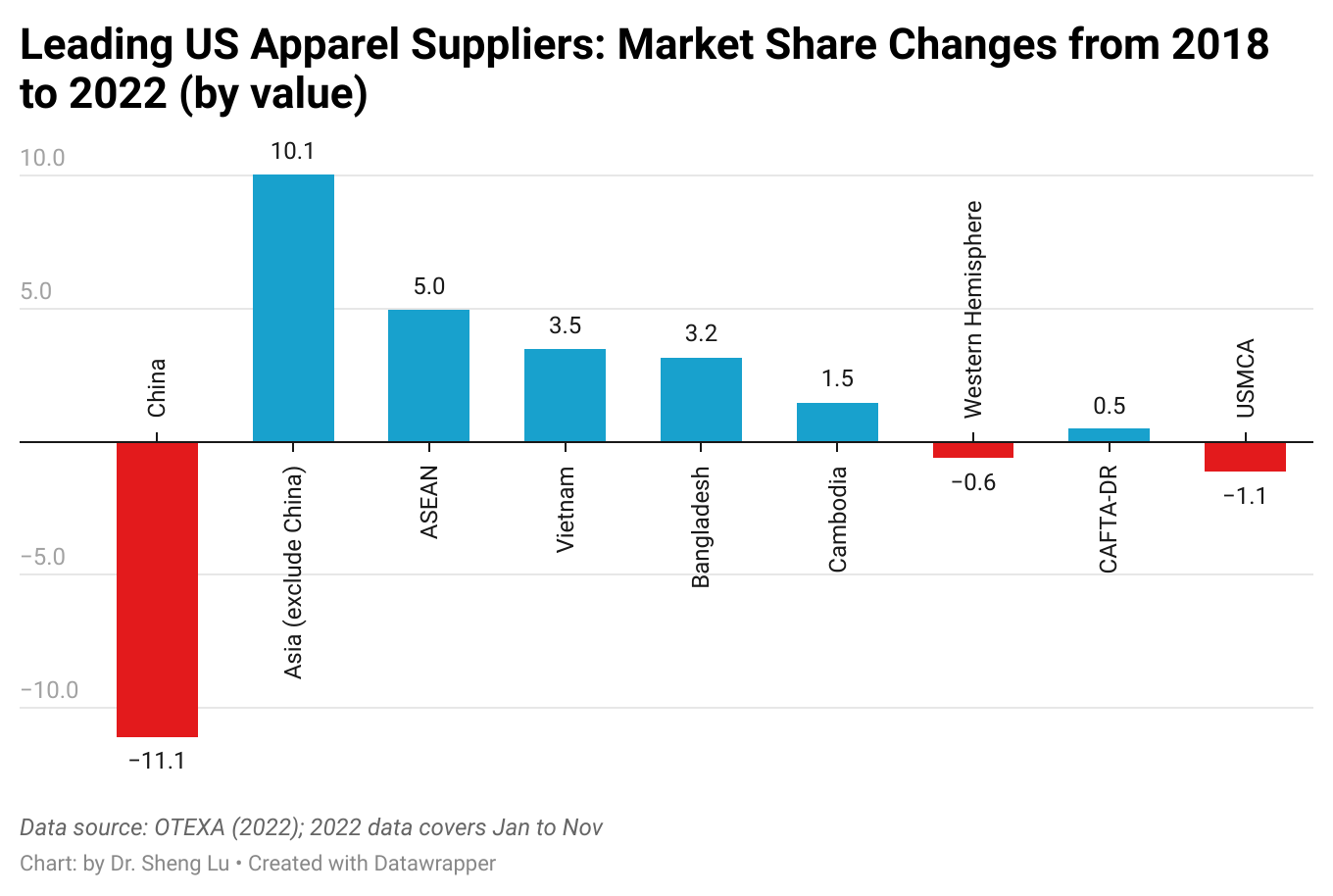

First, China remains one of the most frequently used apparel sourcing destinations. For example:

- Express says, “The top five countries from which we sourced our merchandise in 2021 were Vietnam, China, Indonesia, Bangladesh and the Philippines, based on total cost of merchandise purchased.”

- According to TJX, “a significant amount of merchandise we offer for sale is made in China.”

- Children’s Place says, “We source from a diversified network of vendors, purchasing primarily from Vietnam, Cambodia, Indonesia, Ethiopia, Bangladesh, and China.“

- Ralph Lauren adds, “In Fiscal 2022, approximately 97% of our products (by dollar value) were produced outside of the US, primarily in Asia, Europe, and Latin America, with approximately 19% of our products sourced from China and another 19% from Vietnam.

However, many fashion companies have significantly cut their apparel sourcing volume from China. More often, China is no longer the No.1 apparel sourcing destination, overtaken by China’s competitors in Asia, such as Vietnam.

- According to Lululemon, “During 2021, approximately 40% of our products were manufactured in Vietnam, 17% in Cambodia, 11% in Sri Lanka, 7% in China (PRC), including 2% in Taiwan, and the remainder in other regions… From a sourcing perspective, when looking at finished goods for the upcoming 2022 fall season, Mainland China represents only 4% to 6% of our total unit volume.”

- Levi’s says, “The good thing about our supply chain is we’ve got truly a global footprint. We don’t manufacture a whole lot in China anymore. We’ve been slowly divesting manufacturing out of China, if you will, and kind of playing our chips elsewhere on the global map… Less than 1% of what we’re bringing into this country, into the US, less than 1% of it is coming from China.”

- Adidas says, “In 2021, we sourced 91% of the total apparel volume from Asia (2020: 93%). Cambodia is the largest sourcing country, representing 21% of the produced volume (2020: 22%), followed by China with 20% (2020: 20%) and Vietnam with 15% (2020: 21%).”

- Victoria’s Secret says, “On China, China is a single-digit percentage of our total inflow of merchandise. We’re not particularly dependent on China at all.”

- Nike: “As of May 31, 2022, we were supplied by 279 finished goods apparel contract factories located in 33 countries. For fiscal 2022, contract factories in Vietnam, China and Cambodia manufactured approximately 26%, 20% and 16% of total NIKE Brand apparel, respectively“

Meanwhile, fashion companies still heavily use China as a sourcing base for textile raw materials (such as fabrics). For example:

- Columbia Sportswear says it sources most of its finished products from Vietnam, but “a large portion of the raw materials used in our products is sourced by our contract manufacturers in China.”

- Likewise, Puma says, “90% of our recycled polyester comes from Vietnam, China, Taiwan (China) and Korea.”

- Guess says, “During fiscal 2022, we sourced most of our finished products with partners and suppliers outside the U.S. and we continued to design and purchase fabrics globally, with most coming from China.”

- Lulumemon says, “Approximately 48% of the fabric used in our products originated from Taiwan, 19% from China Mainland, 11% from Sri Lanka, and the remainder from other regions.”

Second, Western fashion companies unanimously ranked the COVID situation as one of their top concerns for China. Many companies reported significant sales revenue and profits loss due to China’s draconian “zero-COVID” policy and lockdown measures. For example,

- Tapestry says, “For Greater China, sales declined 11% due to lockdowns and business disruption… as a result, we have tempered our fiscal year 2023 outlook based on the expectation for a delayed recovery in China.”

- Adidas says, “With Great China… we continue to see several market-specific challenges that are affecting our entire industry. The strict zero COVID-19 policy with nationwide restrictions remains in place amid more than 2000 daily new COVID-19 cases in November. As a consequence, offline traffic is subdued due to the imminent risk of new lockdowns.

- Under Armour says, “Ongoing impacts of the COVID-19 pandemic and related preventative and protective actions in China…have negatively impacted consumer traffic and demand and may continue to negatively impact our financial results.”

- VF Corporation says, “The performance in Greater China…continues to be impacted by widespread rolling COVID lockdowns and restrictions as well as lower consumer spending.”

- Puma says, “COVID-19-related restrictions are still impacting business in Greater China, and higher freight rates and raw material prices continue to put pressure on margins.”

Notably, despite China’s most recent COVID policy U-turn, most fashion companies expect market uncertainties to stay in China, at least in the short run, given the surging COVID cases and policy unpredictability. For example:

- PVH says, “While we remain optimistic about our business in China, it continues to be a challenging environment as restrictions have once again intensified in the fourth quarter of 2022.”

- Nike says, “So we’ve taken a very cautious approach in our guidance to China, given the short-term uncertainties that are there.”

- Abercrombie & Fitch also listed China’s COVID situation as one of their top risk factors, “risks and uncertainty related to the ongoing COVID-19 pandemic, including lockdowns in China, and any other adverse public health developments.”

Third, fashion companies report the negative impacts of US-China trade tensions on their businesses. Also, as the US-China relationship sours, fashion bands and retailers have been actively watching the potential effect of geopolitics. For example,

- Express says, “recent geopolitical conditions, including impacts from the ongoing conflict between Russia and Ukraine and increased tensions between China and Taiwan, have all contributed to disruptions and rising costs to global supply chains.”

- When assessing the market risk factors, Chico’s FAS says, “our reliance on sourcing from foreign suppliers and significant adverse economic, labor, political or other shifts (including adverse changes in tariffs, taxes or other import regulations, particularly with respect to China, or legislation prohibiting certain imports from China)”

- Adidas holds the same view, “In addition, the challenging market environment in China had an adverse impact on the company’s business activities… Additional challenges included the geopolitical situation in China and extended lockdown measures.”

- Macy’s adds, “At this time, it is unknown how long US tariffs on Chinese goods will remain in effect or whether additional tariffs will be imposed. Depending upon their duration and implementation, as well as our ability to mitigate their impact, these changes in foreign trade policy and any recently enacted, proposed and future tariffs on products imported by us from China could negatively impact our business, results of operations and liquidity if they seriously disrupt the movement of products through our supply chain or increase their cost.”

- Gap Inc. says, “Trade matters may disrupt our supply chain. For example, the current political landscape, including with respect to U.S.-China relations, and recent tariffs and bans imposed by the United States and other countries (such as the Uyghur Forced Labor Prevention Act) has introduced greater uncertainty with respect to future tax and trade regulations.”

- QVC says, “The imposition of any new US tariffs or other restrictions on Chinese imports or the taking of other actions against China in the future, and any responses by China, could impair our ability to meet customer demand and could result in lost sales or an increase in our cost of merchandise, which would have a material adverse impact on our business and results of operations.”

Additionally, NO evidence shows that fashion companies are decoupling with China. Instead, Western fashion companies, especially those with a global presence, still hold an optimistic view of China as a long-term business opportunity. For example:

- Inditex, which owns Zara, says, “we remain absolutely confident about our opportunities there (in China) in the medium to long term. Fashion demand continues to be strong in China. For sure it will remain a core market for us for Inditex.”

- Ralph Lauren says, “China provides not only the successful blueprint for our elevated ecosystem strategy globally, it also represents one of several geographic long-term opportunities for our brand…We continue to see near and long term brand opportunities in China.”

- Lululemon says, “On China, we remain very excited…we remain very, very excited about the potential and the role that will play in quadrupling our international business with Mainland China.”

- Nike says, “We have remained committed to investing in Greater China for the long term.”

- Adidas says, “On China, clearly, we believe in as a midterm opportunity in China… And then when the market opens up (from COVID), we believe, the western brand is well-positioned in China again, and we can start growing significant in China again.”

Meanwhile, Western fashion companies plan to make more efforts to localize their product offer and cater to the specific needs of Chinese consumers, especially the young generation. The “Made in China for China” strategy could become more popular among Western fashion companies. For example,

- PVH says, “So, I think in general, our production in China is heavily oriented to China for China production. I think for us generally speaking, the biggest impact of the shutdowns that we’ve seen across Shanghai and Beijing has really been focused on the impact to our China market.”

- Likewise, Levi’s says, “We’re manufacturing somewhere in the neighborhood of 5% of our global production is in China, and most of it staying in China.“

- Hanesbrands says, “we’re committed to opening new stores, and that’s continues to go well, despite, the challenges that are there. Looking specifically at Champion, we continued our expansion in China adding new stores in the quarter through our partners.”

- H&M says, “we still see China as an important market for us.”

- According to Hugo Boss, “Thanks to overall robust local demand, revenues in China in 2021 grew 24% as compared to 2019.”

- VF Corporation adds, “China is a significant opportunity…(We are) really pushing decision-making into the regions and providing more and more latitude for local-for-local decision-makings around product, around storytelling, certainly staying within the confines or the framework of the brand strategy, but really giving more freedom and more empowerment to the regions.”

by Sheng Lu

Further reading: Lu, S. (2023). Is China a business opportunity or liability for fashion companies in 2023? Just Style. https://www.just-style.com/features/is-china-a-business-opportunity-or-liability-for-fashion-companies/