For FASH455: You must watch the video before commenting on the post. When writing your comment, you may consider addressing the following aspects.

Based on the video and the lessons from Reju, how would textile-to-textile recycling reshape the traditional global apparel supply chain? Which stages of the supply chain are most likely to relocate back to the U.S., and which will remain global?

Based on the video and the lessons from Reju, what are the biggest barriers to scaling textile-to-textile recycling? What risks may investors face when funding capital-intensive recycling plants in the US?

Will textile-to-textile recycling enable a meaningful revival of the U.S. textile and apparel industry and why?

Would “Made with recycled U.S. waste” be as valuable to consumers as “Made in USA”? Why?

Additional reading: 2026 Textile Recycling Expo USA Interview Series

For FASH455 class: When writing your blog comment, consider addressing the following aspects:

#1 Based on the video, how do CAFTA-DR and USMCA help shape the Western Hemisphere textile and apparel supply chain?

#2 Based on the video, what do you see as the main opportunities for textile and apparel nearshoring or reshoring in the Western Hemisphere? How about the key bottlenecks (e.g., cost, infrastructure, labor, sustainability, or trade policy)?

#3 The speaker argues for a sectoral trade policy for textiles and apparel rather than broad “free trade.” What is your evaluation?

#4 How does the video help deepen your understanding of the complex economic and non-economic factors related to textile and apparel nearshoring and reshoring in the Western Hemisphere?

Video 1: How an Oklahoma denim-maker supports creating American-made jeans

Video 2: President Trump’s Tariffs Backfire on US Textile Exporters

For FASH455 class: When writing your blog comment, consider addressing the following aspects:

Based on the videos, what is your evaluation of the opportunities and challenges of making textiles and apparel in the U.S.?

In what ways has international trade influenced the growth, decline, or transformation of U.S. textile and apparel production?

What do you think about the Round House Jeans owner’s strategy of selling imported jeans from Bangladesh at a higher profit margin to “subsidize” its low-margin U.S.-made jeans? Do you think this could be a sustainable business model in the long run?

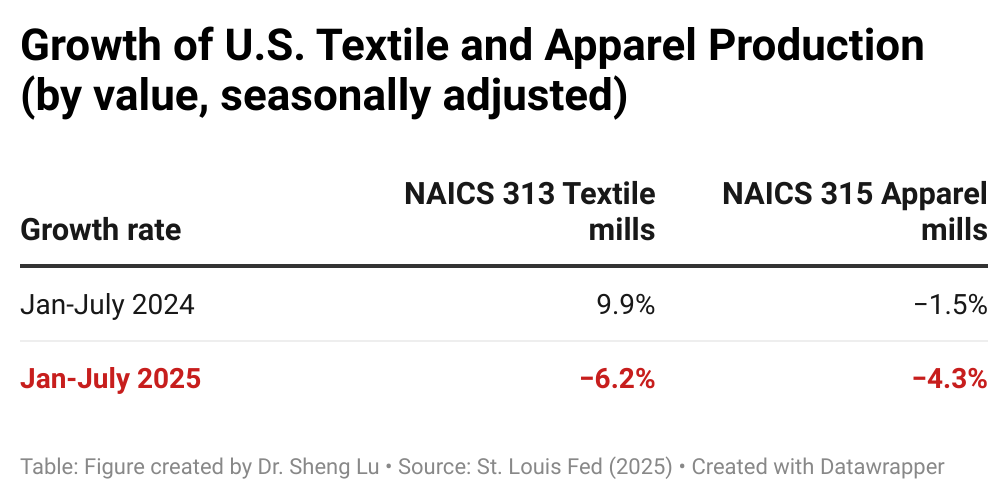

Based on the videos, why do you think U.S. textile and apparel production experienced even greater losses in the first half of 2025, despite higher tariffs on imports? [Detailed data HERE]

If you were invited to offer policy recommendations to boost U.S. domestic textile and apparel manufacturing, what would you propose, and why?

Video 1: Is U.S. Clothing Manufacturing at Risk? Tariffs and Competition Threaten Jobs (RT≠ Endorsement)

Video 2: Northern Virginia T-shirt brand faces challenges (RT≠ Endorsement)

Video 3: Tariffs could raise wedding dress prices for American brides (RT≠ Endorsement)

Video 4: Bangladeshi garment industry sweating on Trump tariffs (RT≠ Endorsement)

Video 5: Trump’s Tariff Twist: Can Pakistan’s Textiles Fill China’s Shoes? (RT≠ Endorsement)

Video 6: Tariffs: Europe’s textile sector holds its breath

For FASH455 class: When writing your blog comment, consider addressing the following aspects:

#1 Based on the videos, how do you expect the apparel sourcing strategy of US fashion companies to evolve in response to the tariff increase? For example, will companies continue to diversify sourcing, wait and see, or focus on expanding sourcing to countries or regions regarded as “safe havens”?

#2 Do you expect the higher tariffs on U.S. imports, including textiles and apparel, to benefit domestic “Made in the USA” production? Why or why not?

#3 As consumers, how do you perceive the impact of the tariffs on your shopping behavior and experiences? Have you noticed any changes, such as in price and product availability, while shopping for clothing recently? Feel free to share your observations.

#4 Are there any other notable impacts of the tariff increase on the global fashion apparel industry that we should be aware of? What additional questions do you have in mind about the tariff impacts?

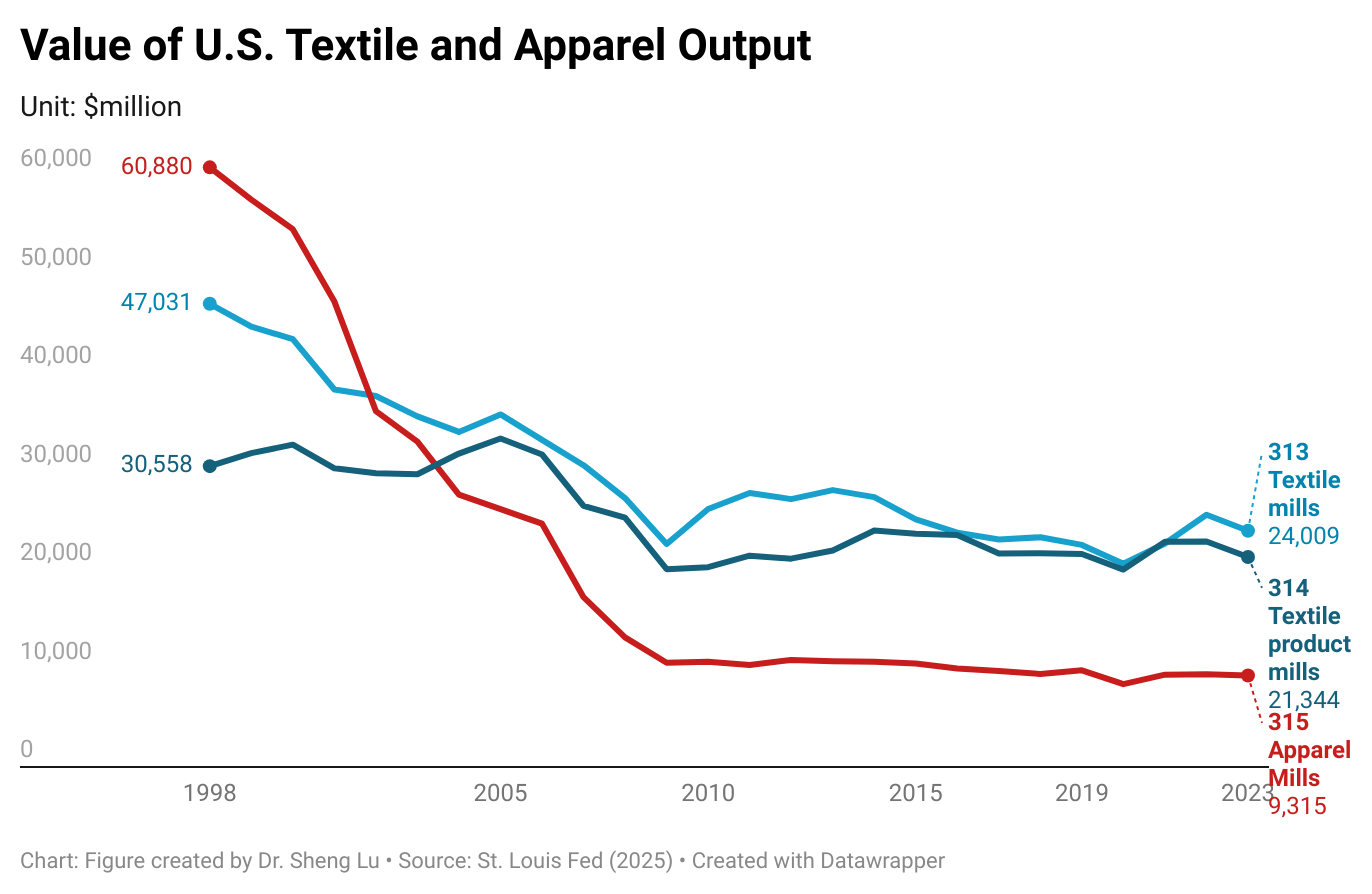

Textile and apparel manufacturing in the U.S. has significantly decreased over the past decades due to factors such as automation, import competition, and the changing U.S. comparative advantages for related products. However, thanks to companies’ ongoing restructuring strategies and their strategic use of globalization, the U.S. textile and apparel manufacturing sector has stayed relatively stable in recent years. For example, the value of U.S. yarns and fabrics manufacturing (NAICS 313) totaled $24 billion in 2023 (the latest data available), up from $23.3 billion in 2018 (or up 2.8%). Over the same period, U.S. made-up textiles (NAICS 314) and apparel production (NAICS 315) moderately declined by only 1.8% and 1.6%.

More importantly, the U.S. textile and apparel manufacturing sector is evolving. Several important trends are worth watching:

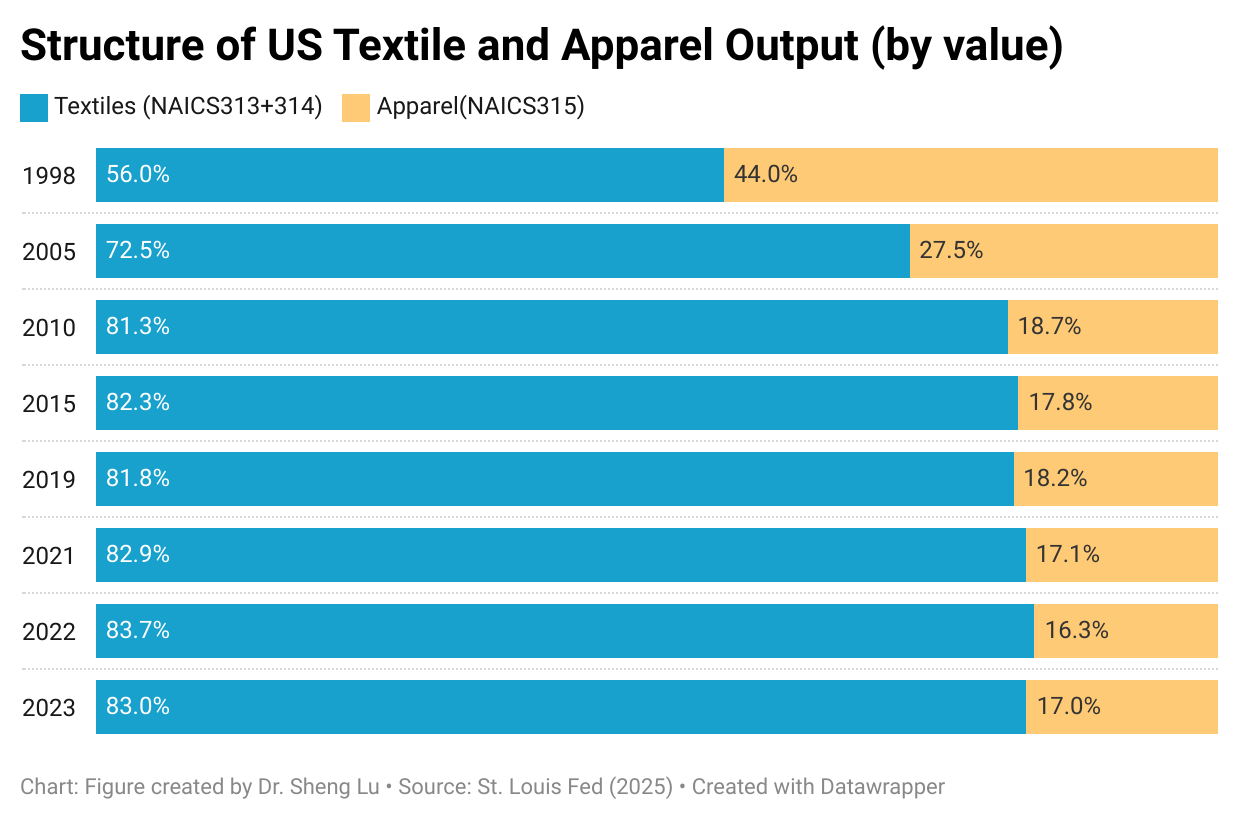

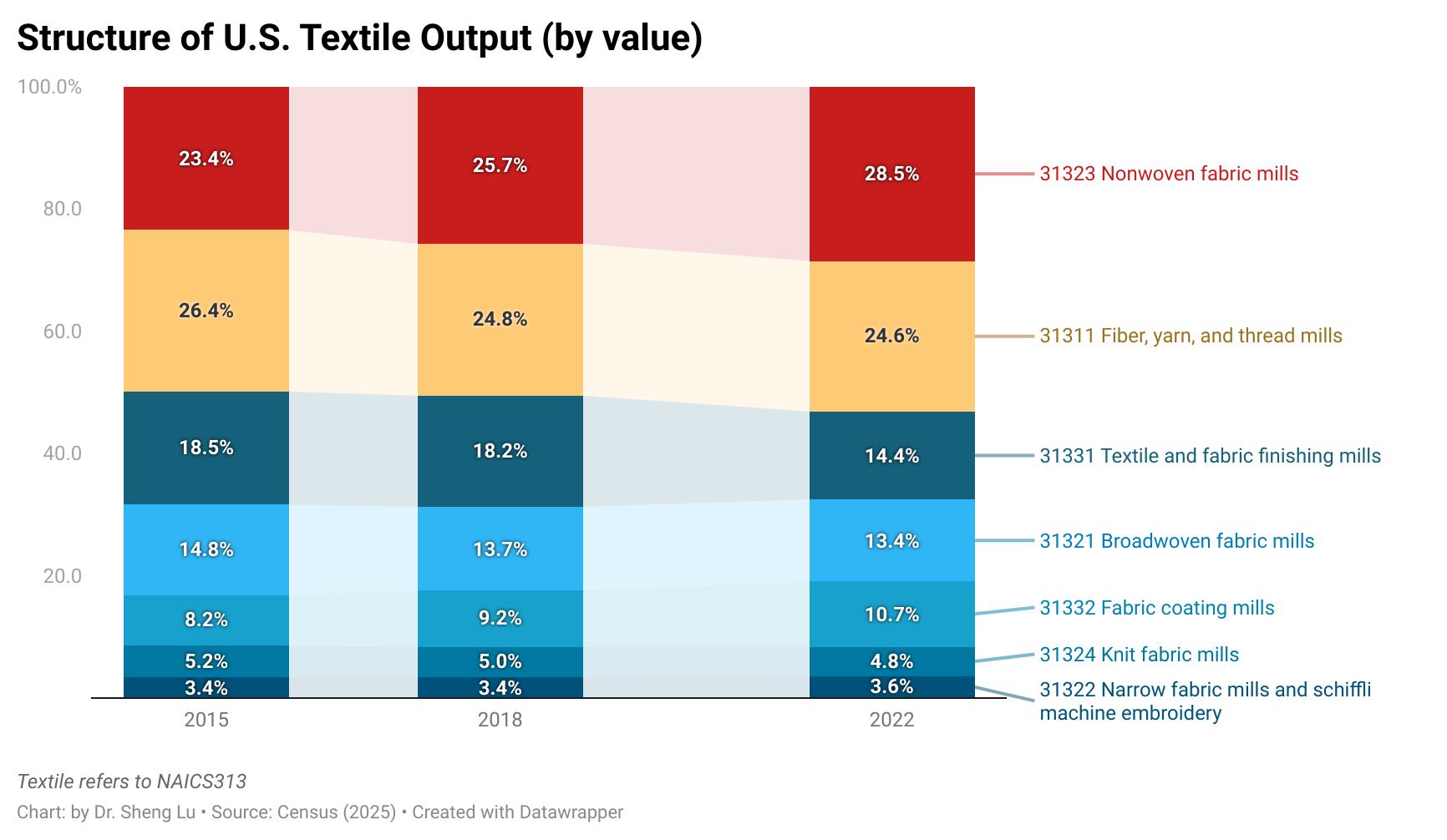

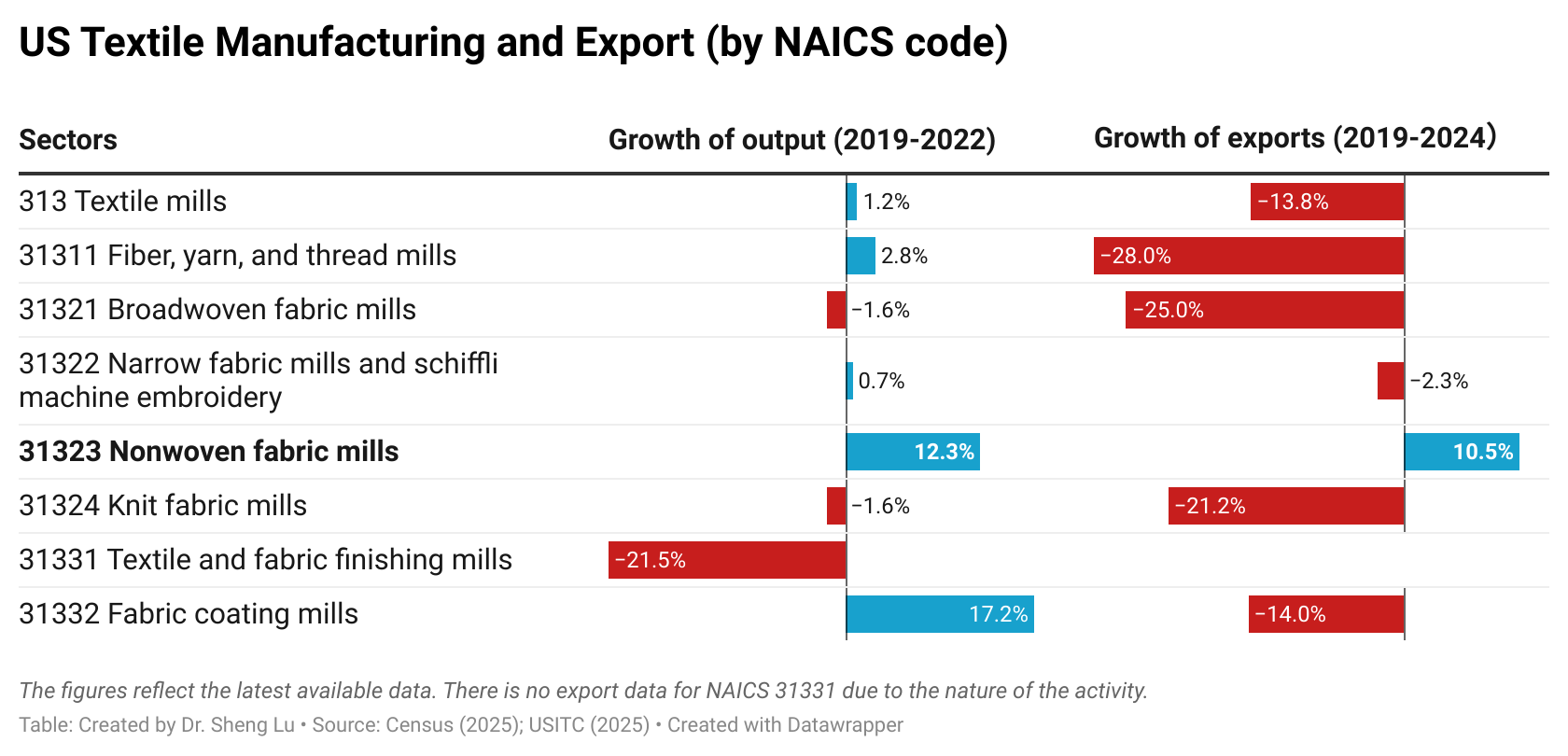

First, “Made in the USA” increasingly focuses on textile products, particularly high-tech industrial textiles that are not intended for apparel manufacturing purposes. Specifically, textile products (NAICS 313+314) accounted for over 83% of the total output of the U.S. textile and apparel industry as of 2023, much higher than only 56% in 1998 (U.S. Census, 2025). Textiles and apparel “Made in the USA” are growing particularly fast in some product categories that are high-tech driven, such as medical textiles, protective clothing, specialty and industrial fabrics, and non-woven. These products are also becoming the new growth engine of U.S. textile exports. Notably, between 2019 and 2022, the value of U.S. “nonwoven fabric” (NAICS 31323) production increased by 12.32%, much higher than the 1.15% average growth of the textile industry (NAICS 313). Similarly, while U.S. textile exports decreased by 13.75% between 2019 and 2024, “nonwoven fabric” exports surged by 10.48%--including nearly 40% that went to market outside the Western Hemisphere (U.S. International Trade Commission, 2025).

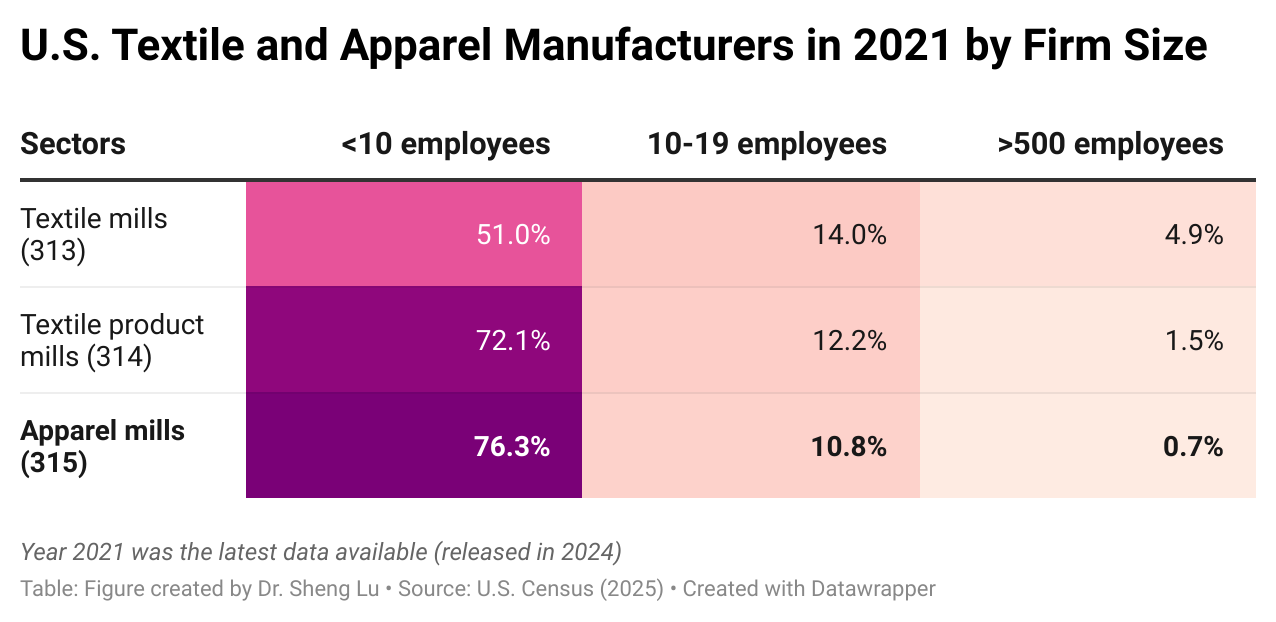

Second, U.S. apparel manufacturers today are primarily micro-factories, and they supplement but are not in a position to replace imports. As of 2021 (the latest data available), over 76% of U.S.-based apparel mills (NAICS 315) had fewer than 10 employees, while only 0.7% had more than 500 employees. In comparison, contracted garment factories of U.S. fashion companies in Asia, particularly in developing countries like Bangladesh, typically employ over 1,000 or even 5,000 workers.

Instead of making garments in large volumes, most U.S.-based apparel factories are used to produce samples or prototypes for brands and retailers. In other words, replacing global sourcing with domestic production is not a realistic option for U.S. fashion brands and retailers in the 21st-century global economy. Nor are U.S. fashion companies showing interest in shifting their business strategies from focusing on “designing + managing supply chain+ marketing” back to manufacturing.

Meanwhile, due to mergers and acquisitions (M&A) and to leverage economies of scale, approximately 5% of U.S. textile mills (NAICS313) had more than 500 employees as of 2021–this is a significant number, considering that textile manufacturing is a highly capital-intensive process.

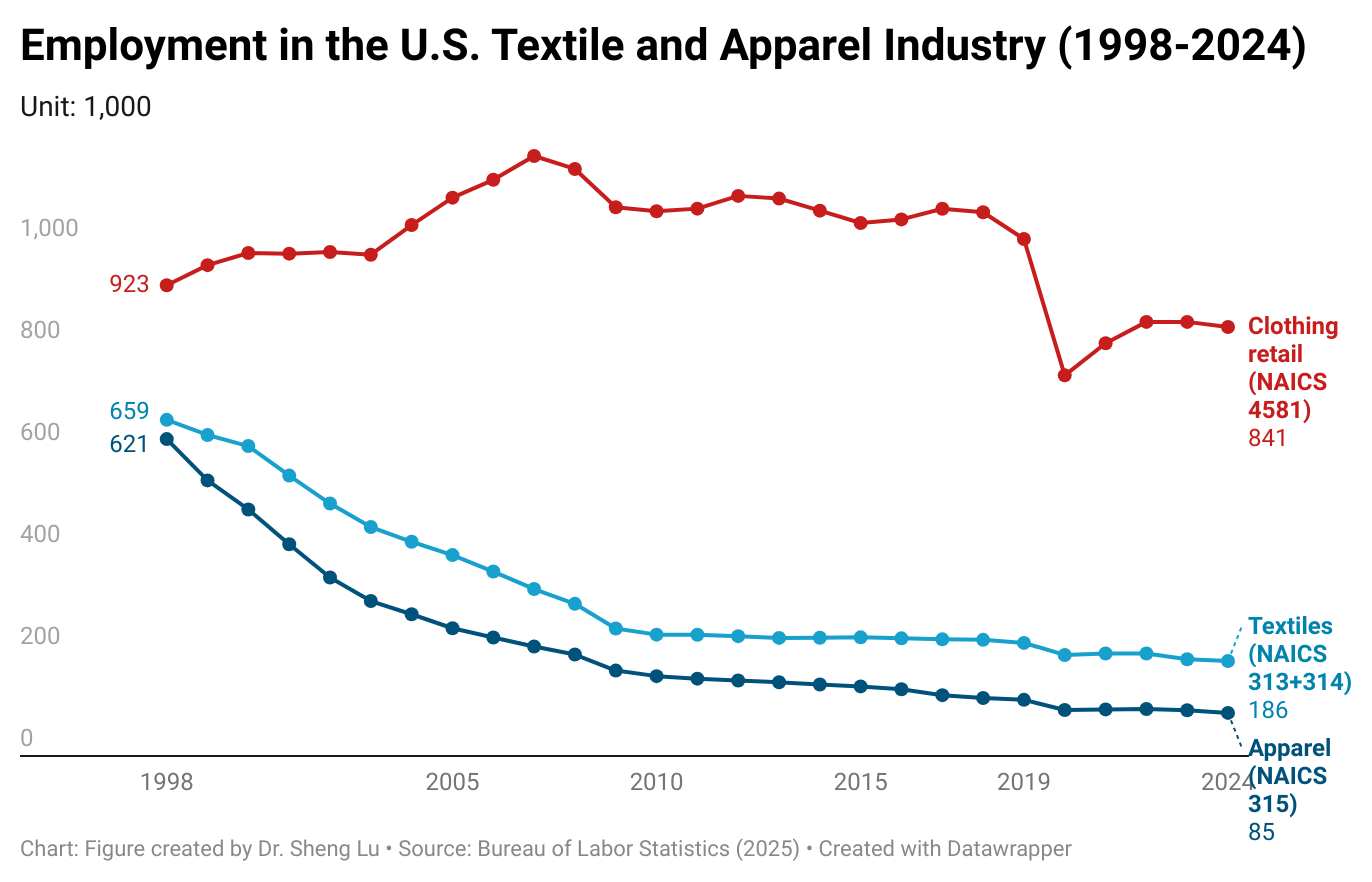

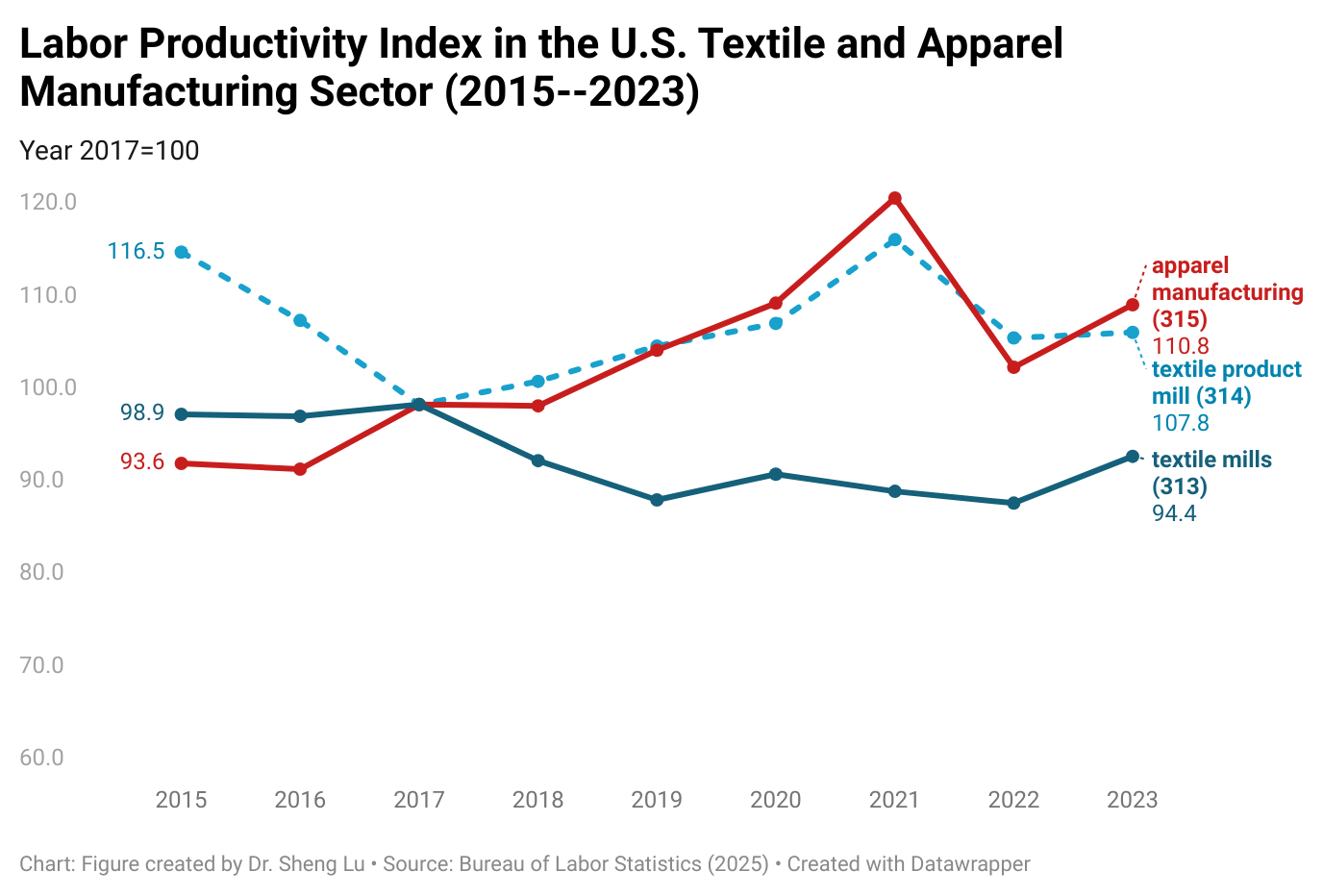

Third, employment in the U.S. textile and apparel manufacturing sector continued to decline, with improved productivity and technology being critical drivers. As of 2024, employment in the U.S. textile and apparel manufacturing sector (NAICS 313, 314, and 315) totaled 270,700, a decrease of 18.4% from 33,190 in 2019. Notably, U.S. textile and apparel workers had become more productive overall—the labor productivity index of U.S. textile mills (NAICS 313) increased from 89.7 in 2019 to 94.4 in 2023, and the index of U.S. apparel mills (NAICS 315) increased from 105.8 to 110.78 over the same period.

On the other hand, clothing retailers (NAICS 4481) accounted for over 75.7% of employment in the U.S. textile and apparel sector in 2024.

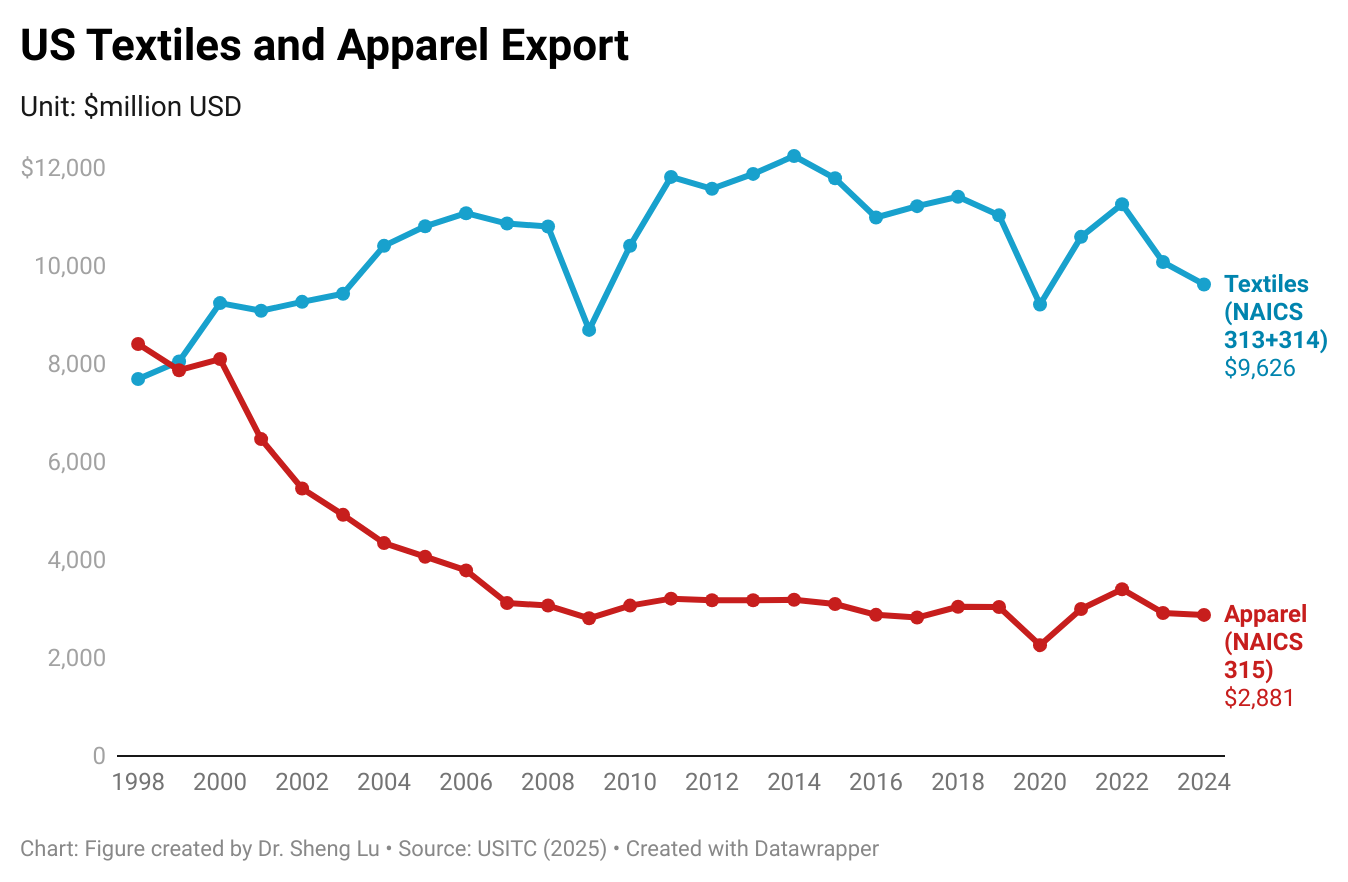

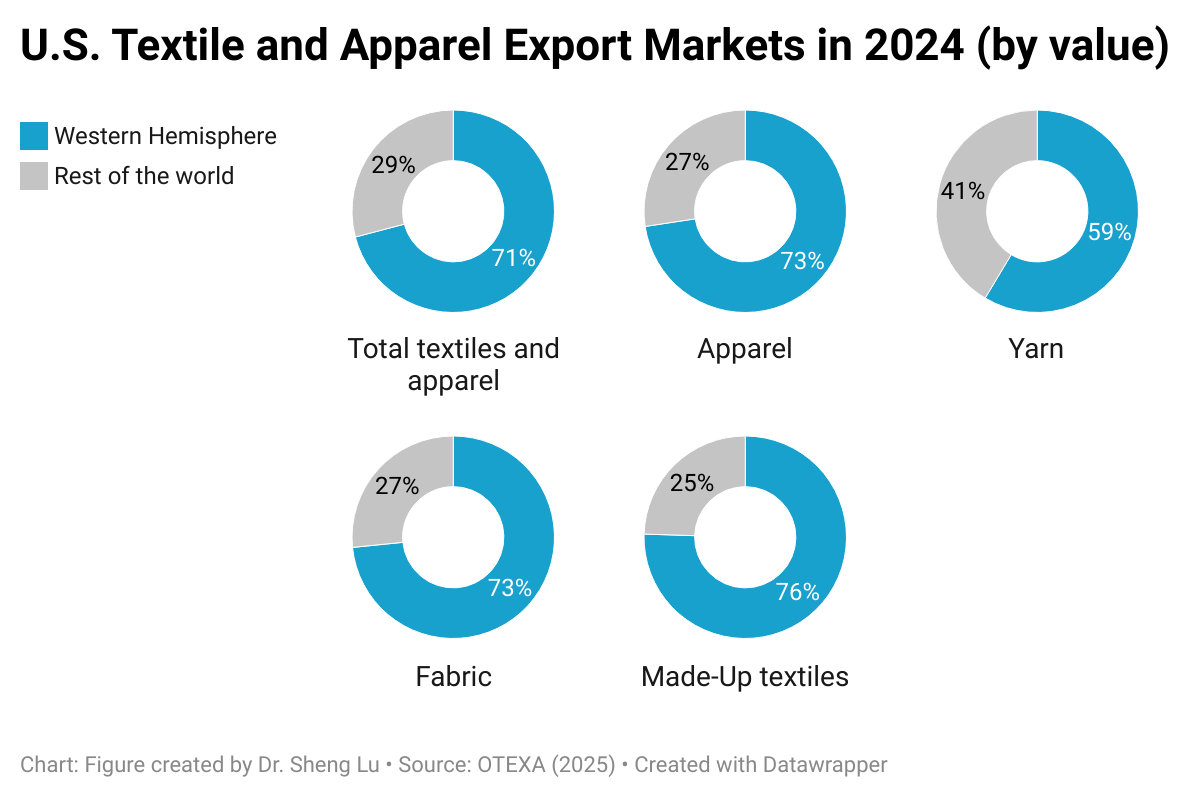

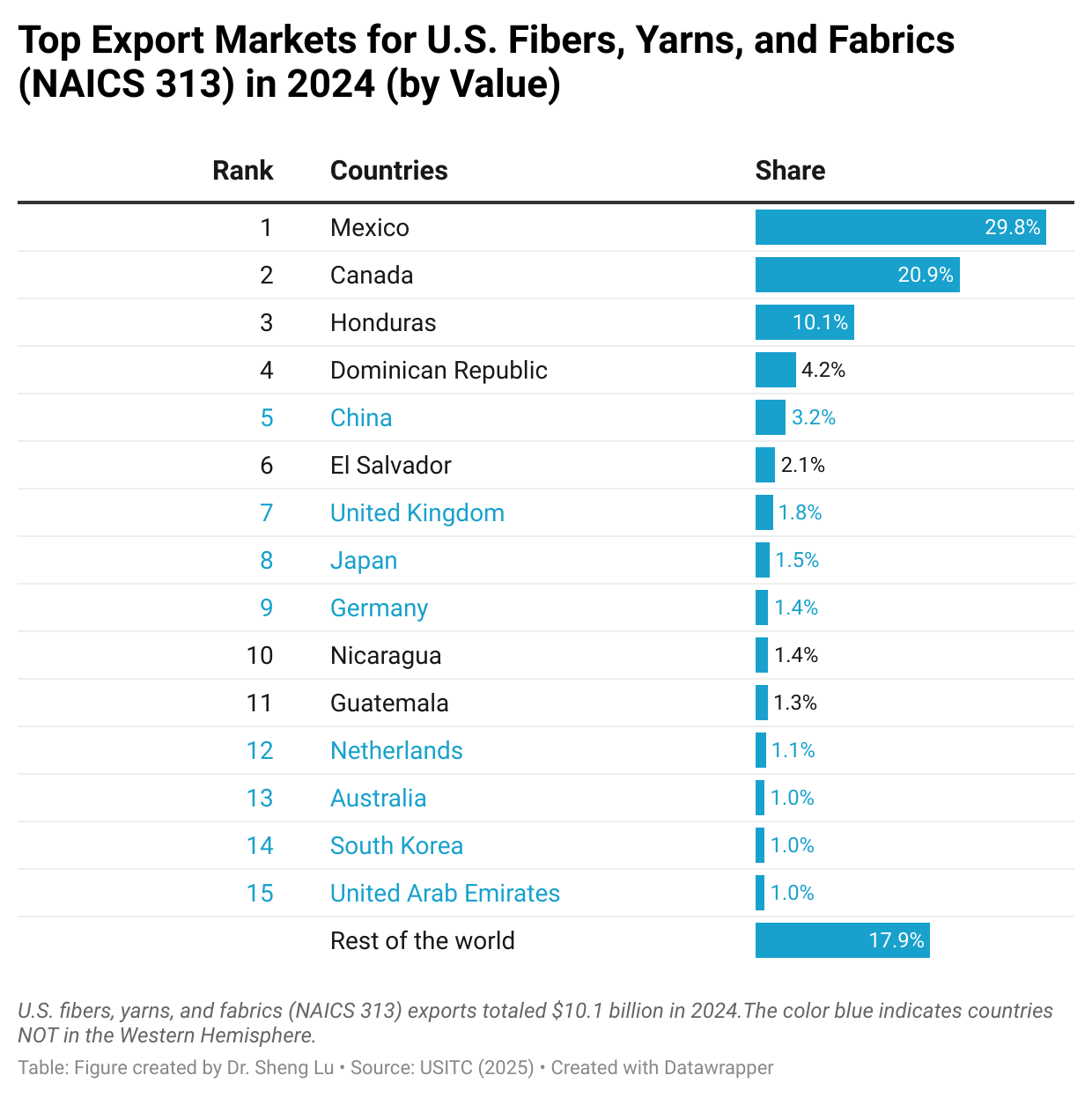

Fourth, international trade, BOTH import and export, supports textiles and apparel “Made in the USA.” On the one hand, U.S. textile and apparel exports exceeded $12.5 billion in 2024, accounting for more than 30% of domestic production as of 2023 (NAICS 313, 314 and 315). Thanks to regional free trade agreements, particularly the U.S.-Mexico-Canada Agreement (USMCA) and the Dominican Republic-Central America Free Trade Agreement (CAFTA-DR), the Western Hemisphere stably accounted for over 70% of U.S. textile and apparel exports over the past decades. However, for specific products such as industrial textiles, markets in the rest of the world, especially Asia and Europe, also become increasingly important. Thus, lowering trade barriers for U.S. products in strategically significant export markets serves the interest of the U.S. textile and apparel industry.

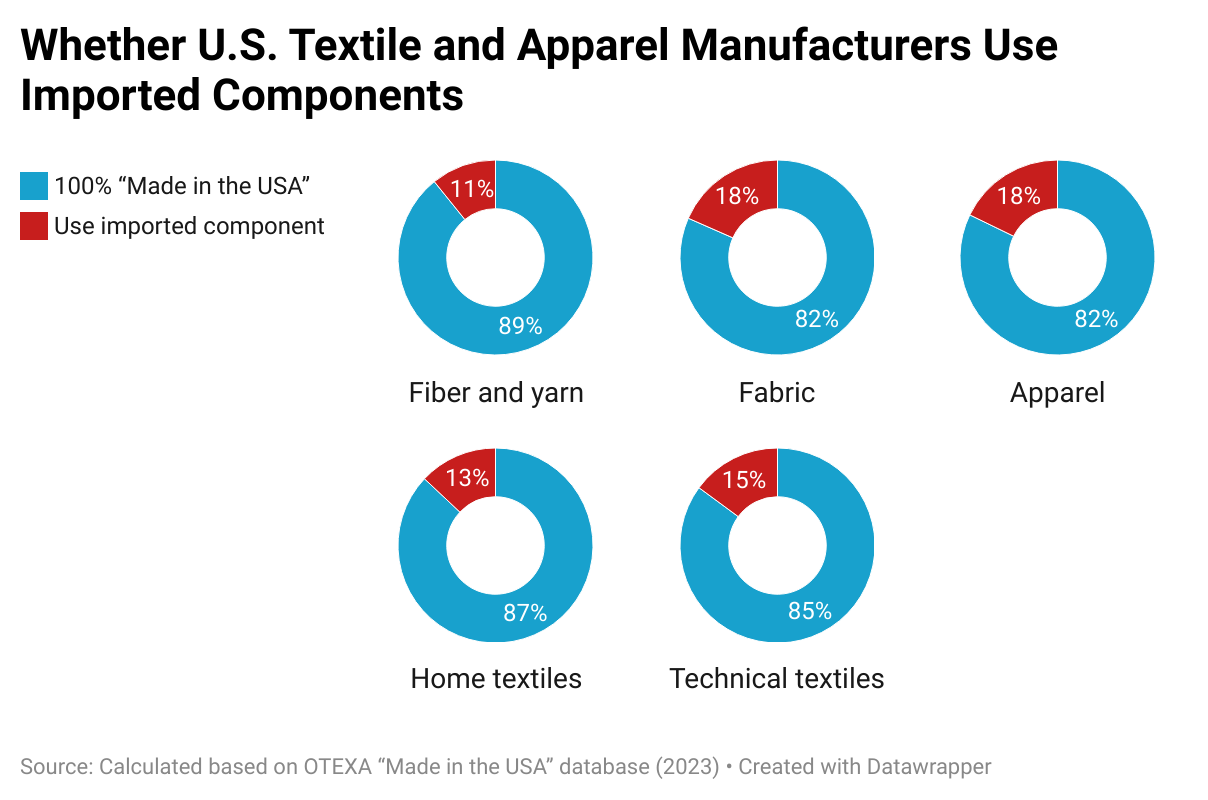

On the other hand, imports support textiles and apparel “Made in the USA” as well. A 2023 study found that among the manufacturers in the “Made in the USA” database managed by the U.S. Department of Commerce Office of Textile and Apparel, nearly 20% of apparel and fabric mills explicitly say they utilized imported components. Partially, smaller U.S. textile and apparel manufacturers appear to be more likely to use imported components–whereas 20% of manufacturers with less than 50 employees used imported input, only 10.2% of those with 50-499 employees and 7.7% with 500 or more employees did so. The results indicate the necessity of supporting small and medium-sized (SME) U.S. textile and apparel manufacturers to more easily access their needed textile materials by lowering trade barriers like tariffs.

Reflecting fashion companies’ interest in carrying more sustainable apparel products to meet consumers’ demand, there has been a notable increase in clothing using recycled cotton in the U.S. retail market since 2022. For example, based on information collected from US apparel retailers’ websites, only about 100 Stock Keeping Units (SKUs) of “Made in the USA” clothing explicitly indicated that they contained recycled cotton in 2022 and 2023, respectively. However, in the first nine months of 2024, this number had already doubled to around 200.

Despite the impressive growth, clothing containing recycled cotton remains a “niche” in the U.S. retail market. As of 2024, the total SKUs of “Made in the USA” clothing containing recycled cotton accounted for only about 0.1% of those made with regular virgin cotton.

Meanwhile, measured by SKU count, 70% of “Made in the USA” clothing containing recycled cotton was sold in the mass and value segments in the U.S. retail market from 2022 to 2024. In comparison, over the same period, “Made in the USA” clothing made with regular cotton catered to a more diverse consumer base, with a relatively balanced distribution across the mass and value segment (57%) and the luxury and premium segment (43%).

Product Features

There appears to be a notable distinction between the product categories of “Made in the USA” clothing using recycled cotton and those made with regular cotton. Specifically, from 2022 to 2024, by SKU count, “Made in the USA” clothing containing recycled cotton mainly focused on basics such as T-shirts (35.6%), jeans (20.1%), other bottoms (20.7%) and other tops (18.4%). Particularly, jeans appear more likely to contain recycled cotton than any other apparel category.

Using recycled cotton also appears to affect clothing’s design patterns. For example, from 2022 to 2024, nearly 85% of “Made in the USA” clothing containing recycled cotton chose plain design patterns compared to only 65% of those exclusively using regular cotton. These results echo findings from previous studies, suggesting that the shorter fiber length and lower quality of recycled cotton may limit the use of more intricate and complex design details.

Fiber Content

Reflecting the significant limitations of the quality and properties of the fiber, clothing labeled as using “100% recycled cotton” was rarely available in the U.S. retail market from 2022 to 2024, regardless of where the item was made. In most cases, recycled cotton accounted for no more than 30% of the total fiber content in a garment, with typical labels read like “49% cotton, 21% recycled cotton, 17% recycled polyester” (jeans), “Made from 70% cotton and 30% recycled cotton” (T-shirt), and “Made from 70% cotton, 29% recycled cotton, and 1% elastane” (skirt).

Results show that over 95% of “Made in the USA” clothing containing recycled cotton was blended with regular virgin cotton, and 92% of imported clothing did the same. According to textile scientists, this blend helps overcome the physical limitations of recycled cotton and enhances the fabric’s durability and softness. Approximately 14% of “Made in the USA clothing” containing recycled cotton was blended with polyester. This blend was commonly used for jeans and T-shirts to improve durability and flexibility and may also reduce production costs. However, compared with “Made in the USA” clothing made from regular cotton, it was uncommon to see recycled cotton blended with specific fiber types such as nylon, spandex, rayon, and linen. This result again revealed the physical limitations of recycled cotton and explained the narrow range of apparel products currently suited for its use.

Sustainability Claims

In practice, the sustainability claims of “Made in the USA” clothing containing recycled cotton in the U.S. retail market appear to be a “mixed bag.” On the one hand, as anticipated, “Made in the USA” clothing containing recycled cotton seems to be more likely to highlight its sustainability attributes than those using regular cotton only. From 2022 to 2024, by SKU count, more than 23.1% of “Made in the USA” items containing recycled cotton mentioned the word “sustainable” in the product description or label, and another 16.2% mentioned “eco-friendly.” In comparison, less than 2% of “Made in the USA” clothing made from regular cotton included these two terms. Similarly, a higher percentage of “Made in the USA” clothing using recycled cotton also featured other sustainability-related terms such as “impacts,” “waste,” and “certified,” compared to those made from regular cotton.

On the other hand, however, the sustainability claims of “Made in the USA” clothing containing recycled cotton are not without concerns. For example, in many cases, the product descriptions or labels provide no detailed and verifiable information about the actual “sustainability benefits” of producing and consuming clothing made from recycled cotton aside from vaguely saying the product was “sustainable,” “eco-friendly,” or “certified.”

To complicate the issue further, as clothing made from regular cotton increasingly emphasizes its sustainability benefits as a natural fiber, it somehow diminishes the exclusivity of recycled cotton as a sustainable option. For example, there is no clear evidence indicating that consumers generally perceive clothing using “recycled cotton” as more or less sustainable than those using “organic cotton” or cotton certified by reputable programs such as the “Better Cotton Initiative, BCI” and the “U.S. Cotton Trust Protocol.” In other words, “recycled cotton” faces intense competition as the preferred sustainable fiber among many choices available to fashion companies, including regular cotton.

Pricing Practices

Results show that “Made in the USA” clothing containing recycled cotton is not always “cheap” for U.S. consumers. For instance, for those targeting the mass market segment, between 2022 and 2024, adding recycled cotton increased the selling price of “Made in the USA” clothing by more than 10% compared to items made with virgin cotton, with jeans being the only exception (i.e., 12% lower).

Price data also show that “Made in the USA” recycled cotton items generally have higher price tags than comparable non-U.S.-made items across both mass and premium markets, particularly in popular categories like T-shirts and bottoms. This trend suggests that higher U.S. domestic production costs, particularly the higher wage level than Asian countries, could contribute to these elevated prices.

Reflections

As the findings highlighted, while visibility is increasing, promoting recycled cotton in clothing still encounters significant challenges. For instance, technical advancements in the quality of recycled cotton fiber are critical to enhancing its competitiveness among other “preferred sustainable fibers,” raising its perceived market value and enabling its use across a broader range of clothing categories beyond T-shirts and jeans.

Notably, due to slow progress in improving the physical properties of recycled cotton, some have seemingly “given up” on using it for clothing and suggest focusing more on repurposing recycled cotton for other categories, such as non-wovens, carpets, packaging, and home textiles. However, as sustainability legislation, such as the Extended Producer Responsibility (EPR) law, increasingly mandates fashion companies to recycle textile waste, not promoting recycled cotton could lead to greater reliance on recycled polyester or other man-made fibers in clothing, which may not serve the long-term business interests of the cotton industry.

by Katherine Yasik(Fashion Design and Product Innovation major & Sustainable apparel minor, Fashion and Apparel Studies, University of Delaware) and Sheng Lu

Textiles and apparel “Made in the USA” have gained growing attention in recent years amid the increasing supply chain disruptions during the pandemic, the rising geopolitical tensions worldwide, and consumers’ increasing interest in sustainable apparel and faster speed to market. Statistics from the U.S. Bureau of Economic Analysis showed that U.S. textile and apparel production totaled nearly $28 billion in 2022, a record high in the most recent five years. Meanwhile, unlike in the old days, a growing proportion of textiles and apparel “Made in the USA” are sold overseas today. For example, according to the Office of Textiles and Apparel (OTEXA) under the U.S. Department of Commerce, U.S. textiles and apparel exports exceeded $24.8 billion in 2022, up nearly 12% from ten years ago.

By leveraging U.S. Department of Commerce Office of Textiles and Apparel (OTEXA)’s “Made in U.S.A. Sourcing & Products Directory,” this study explored U.S. textiles and apparel manufacturers’ detailed production and export practices. Altogether, 432 manufacturers included in the directory as of October 1, 2023, were analyzed. These manufacturers explicitly mentioned making one of the following products: fiber, yarn, fabric, garment, home textiles, and technical textiles.

Key findings:

First, U.S. textile manufacturers exhibit a notable geographic concentration, whereas apparel manufacturers are dispersed throughout the country. Meanwhile, by the number of textile and apparel manufacturers, California and North Carolina are the only two states that rank in the top five across all product categories, showcasing the most comprehensive textile and apparel supply chain there.

Second, U.S. textile and apparel manufacturers have a high concentration of small and medium-sized enterprises (SMEs). Highly consistent with the macro statistics, few textile and apparel manufacturers in the OTEXA database reported having more than 500 employees. Particularly, over 74% of apparel and nearly 60% of home textile manufacturers are “micro-factories” with less than 50 employees.

Third, U.S. textile and apparel manufacturers have limited vertical manufacturing capability. A vertically integrated manufacturer generally makes products covering various production stages, from raw materials to finished products. Results show that only one-third of U.S. textile and apparel manufacturers in OTEXA’s database reported making more than one product type (e.g., yarn or fabric). Meanwhile, specific types of vertically integrated production models are relatively popular among U.S. textile and apparel manufacturers, such as:

Apparel + home textiles (5.8%)

Fabric + technical textiles (5.1%)

Yarn + fabric (3.9%)

However, the lack of fabric mills (N=38 out of 432) appears to be a critical bottleneck preventing the building of a more vertically integrated U.S. textile and apparel supply chain.

Fourth, it is not uncommon for U.S. textile and apparel manufacturers to use imported components. Specifically, among the manufacturers in the OTEXA database, nearly 20% of apparel and fabric mills explicitly say they utilized imported components. In comparison, given the product nature, fiber and yarn manufacturers had a lower percentage using imported components (11%). Furthermore, smaller U.S. textile and apparel manufacturers appear to be more likely to use imported components. For example, whereas 20% of manufacturers with less than 50 employees used imported input, only 10.2% of those with 50-499 employees and 7.7% with 500 or more employees did so. The results indicate the necessity of supporting SME U.S. textile and apparel manufacturers to access textile input through mechanisms such as the Miscellaneous Tariff Bill (MTB).

Fifth, many US textile and apparel manufacturers have already explored overseas markets. Specifically, factories making textile products reported a higher percentage of engagement in exports, including fiber and yarn manufacturers (68.4%), fabric mills (78.9%), and technical textiles producers (69.1%). In comparison, relatively fewer U.S. apparel and home textile producers reported selling overseas.

Sixth, U.S. textile and apparel manufacturers’ export markets are relatively concentrated. Specifically, as many as 72% of apparel mills and 57% of home textiles manufacturers in the OTEXA database reported selling their products in less than two markets. These manufacturers also have a high percentage of selling to the U.S. domestic market. Likewise, because of the reliance on the Western Hemisphere supply chain, more than half of U.S. fiber and yarn manufacturers reported only selling in two markets or less. In comparison, reflecting the global demand for their products, U.S. technical textile manufacturers had the most diverse markets, with nearly 40% exporting to more than ten countries.

Seventh, while the Western Hemisphere remains the top export market, many U.S. textile and apparel manufacturers also export to Asia, Europe, and the rest of the world. For example, nearly half of U.S. textile and apparel manufacturers in OTEXA’s database reported exporting to Asia, and over 60% of U.S. technical textile manufacturers sold their products to European customers.

Additionally, over half of U.S. textile and apparel mills engaged in exports leveraged U.S. free trade agreements (FTAs). U.S. textile mills, on average, reported a higher percentage of using FTAs than apparel and home textile manufacturers. As most U.S.-led FTAs adopt the yarn-forward rules of origin, the results suggest that while such a rule may favor the export of U.S. textile products, its effectiveness and relevance in supporting U.S. apparel exports could be revisited.

Moreover, in line with the macro trade statistics, U.S. textile and apparel manufacturers in the OTEXA database reported a relatively high usage of USMCA, given Mexico and Canada being the two most important export markets. In comparison, U.S. textile and apparel manufacturers’ use of CAFTA-DR was notably lower, even for fiber and yarn manufacturers (37%) and fabric mills (33.3%).

by Kendall Ludwig, Miranda Rack and Sheng Lu

Picture above: On December 13, 2023, Kendall Ludwig and Miranda Rack, FASH 4+1 graduate students and Dr. Sheng Lu, had the unique opportunity to present the study’s findings to senior U.S. trade officials from OTEXA and the Office of the U.S. Trade Representative (USTR) in Washington DC, including Jennifer Knight (Deputy Assistant Secretary for Textiles, Consumer Goods and Materials), Laurie-Ann Agama (Acting Assistant US Trade Representative for Textiles), Maria D’Andrea-Yothers (Director of OTEXA), Natalie Hanson (Deputy Assistant US Trade Representative for Textiles) and Richard Stetson (Deputy Director of OTEXA).

Check the Udaily article that features the research project and the presentation (February 2024).

Elizabeth Davelaar is a Co-Owner of Maker’s Way Fiber Mill in Brandon, SD, which opened in October 2021. The mill is a family-run business, with Elizabeth’s sister, Erin, and her mother, Kari, as other co-owners. Elizabeth began her career in the fashion industry at the University of Minnesota, where she graduated with a BS in Apparel Design from the College of Design. She then went to the University of Delaware, where she graduated with an MS in Fashion and Apparel Studies and a Graduate Certificate in Sustainable Apparel Business.

Elizabeth served as a project manager for a non-profit fashion brand in St. Louis and taught sewing to immigrant women in St. Louis and women in Ethiopia. She then moved to Vi Bella Jewelry in Sioux Center, IA, working her way from Shipping Manager to VP of Operations, Sustainability and Design. She then opened Maker’s Way Fiber Mill in 2021 with her family and has been working with local fiber producers to grow the yarn industry in South Dakota and surrounding areas.

Interview Part

Sheng: What inspired you to start your fiber mill business? What makes it special and exciting?

Elizabeth: The mill was born out of the need to solve a problem. I became interested in natural dye at the University of Delaware under Professor Cobb. Once I moved back to the area where I grew up, COVID hit, and I was able to dive deeper into the natural dye and use local plants as a dye source. This also led to being curious about local natural fibers. South Dakota isn’t a state that grows cotton, and the hemp industry is currently small, but it has an abundance of sheep. According to statistics from the US Department of Agriculture, South Dakota has 235,000 sheep and is home to one of the nation’s largest wool co-ops. However, there are only 2 working fiber mills in the area that provide custom processing, which makes yarn made from local fiber very hard to find.

This led to the opening of Maker’s Way Fiber Mill. We are a full-service, custom fiber mill and make yarn, felt, roving, and home goods products from primarily wool and alpaca fiber. Approximately 90% of our time is spent processing for clients who own the animals and use the yarn themselves or sell it, with the other 10% processing yarn that we sell online via our website and in-person at events. The vast majority of our customers are local (within 4-5 hrs) and sell locally to crafters. We take pride in knowing where the fiber we use comes from, sourcing from local farms or using fiber from vintage or second-hand sources.

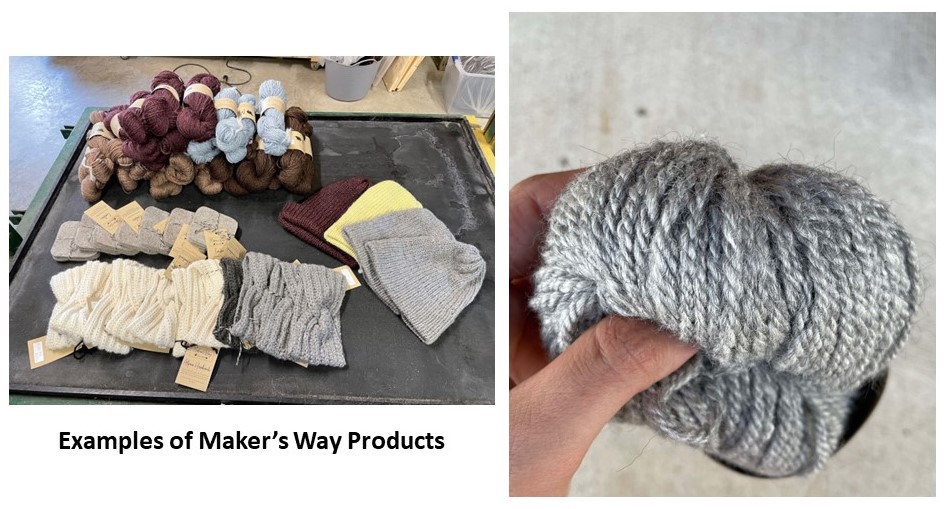

Hats made from 80% alpaca/20% Wool (both sourced from SD) with a small amount of recycled sari silk blended in. Photo courtesy of Elizabeth Davelaar

(Photo courtesy of Elizabeth Davelaar)

Photo courtesy of Elizabeth Davelaar

Sheng: According to Maker’s Way Fiber Mill’s website, sustainability is a critical feature of your products. Why is that, and how do you make your products sustainable?

Elizabeth: We believe that we are stewards of the earth and should be conscious of how the products we make are grown, created, and then how they can be disposed of. The fashion industry, from creating the product to end life, is a huge polluter. The current market for wool is not great for producers, and there isn’t a good avenue for alpaca producers. We work very hard to ensure that our products are sourced from people that we know and trust or are from vintage or second-hand sources. We also work to ensure our products are made from natural fibers, thus they are biodegradable.

We also work to limit the waste in our mill. Although we try our absolute best to reduce loss in the process, each step produces some loss in fiber. This fiber is swept up and either rewashed and added to our Millie line or added to our bird nest starters. The Millie line is yarn spun up from the scraps, and we end up running about four batches of this a year. Each batch is unique because of the different blends of fiber we run. The bird nest starters use fiber that either falls out of our carder or is swept off the floor. These are then put outside in the spring for birds to use for nesting. The fibers are short enough that the baby birds don’t get tangled in them as they would with yarn and because they are natural animal fibers, the nests will biodegrade, unlike acrylic yarns that are sometimes used.

Photo courtesy of Elizabeth Davelaar

Sheng: Maker’s Way Fiber Mill’s products are 100% locally made in South Dakota. From your perspective, what are the opportunities and challenges for manufacturing textiles in the US today?

Elizabeth: I see two big challenges in the natural animal fiber side of the U.S. textile industry: Lack of consumer knowledge of where clothing comes from and lack of infrastructure. But both also present big opportunities!

First, we have found with our mill that people don’t have a good understanding of how many steps there are in creating yarn in general, let alone clothing. We have people who question our pricing because they don’t understand what it means to make yarn in the United States. From start to finish, it takes eight different steps to get raw fiber from producers to yarn ready to sell. Our consultations for new clients tend to be very educational because even fiber producers don’t necessarily know all the steps. As we open the mill for tours and talk to people at events, they start to understand and respect how much work is behind the yarn we create, and that is when we see buy-in – when people start to see the whole process, as well as the people.

The second challenge I see is the overall lack of infrastructure. We are one of approximately 200 small-scale / artisan-style mills in the country (this number is approximate – there is not a good database) and do not run near the quantity compared to the larger manufacturers. As of 2018, there aren’t any small-scale fiber mill equipment manufacturers in the US, so all of the equipment available to us is either used or has to be imported from Canada or Italy. Wait time for most small producers to get their fiber made into yarn is approximately 8-12 months at many mills, some run up to 18 months out. Our mill currently runs about 6 months out and we have been open for just over a year.

For producers who want to sell their wool to larger manufacturers and not have it custom processed, as far as our research has shown, there is one large-scale scouring (wool washing) facility in the states and most of the large-scale spinners use fiber from this facility to spin into yarn and then send the fiber off to other finishing companies for knitting. Otherwise, all of the wool is shipped overseas, and producers are earning approximately $1.66/lb of wool (in 2020). We have heard of many producers that have stockpiles of wool because they are waiting for higher wool prices. Coops also won’t accept wool that isn’t white, so all dark colors of wool get thrown away as there isn’t a market for it.

We also see this as an opportunity. We have noticed the “buying local” trend extending past food also to include yarn. People also see value in making their own clothing and being intentional through knitting/crocheting. There is a growing market for it. We have also seen some demand for the addition of another large-scale scouring facility that could meet the needs for wool insulation and other home applications.

Sheng: Like other fashion programs in the US, most of our FASH students take job opportunities from fashion brands and retailers, not necessarily textile mills. How to raise the young generation’s interest in pursuing a career in textile and apparel factories? Do you have any suggestions?

Elizabeth: I definitely never intended to start a fiber mill when I was in school. I only took one textile class and am pretty sure only one of my design projects used wool. UD was really what fed the sustainability bug in me and I started to realize that sustainability starts at the very beginning of the lifecycle of clothing. Whether or not something can be biodegradable, recyclable, or repurposed starts with what fiber makes up the clothing. UD also showed me how global apparel is and how much carbon footprint it makes.

Working in a fiber mill is not an easy job. It is dirty, we tend to put in long days, and we are constantly learning new things. I am a very hands-on person, and I love being able to create things from nothing, so this job is a great fit for me. The part I loved most about being in design school was being able to create things, and my current job is that all day, every day. We split the mill into “zones” and between myself, Erin and our mom, we all specialized in a specific part of the process. I am in charge of skirting and cleaning fleeces, which means cleaning off all of the hay and visibly dirty areas (aka manure) and then washing the fiber in 140-180 degree water to get the dirt and lanolin out of the fleece. I then pick and card the fiber, which opens up and organizes the fiber into a long tube that is then drafted, spun, plied, and put into skeins. While most days tend to include the same things, each day is never the same as the last. Each animal fleece we run acts differently, so we are always learning new and better ways to run the equipment we have. It is challenging but also a labor of love. Because we work directly with producers, we know the names of most of the animals and love knowing that their fleeces are being used instead of being discarded! We also love connecting with local people who love purchasing from local producers and makers.

Photo courtesy of Elizabeth Davelaar

One of the biggest things I believe fashion programs can do to help open up students to different options in the fashion industry is to expose them to different opportunities and allow them to follow whatever passion they have and emphasize that there isn’t a “right” path in the industry. My classes opened me up to labor issues around the world and that then led me to Delaware. And the opportunities I was given at UD to follow my passions are a huge reason I am doing what I am doing now. One of the things I think UD does right is having many different professors with varying backgrounds in the FASH department and I think other universities would do well to implement that too.

Sheng: Any other key issues or industry trends you will watch in 2023?

Elizabeth: One of the key trends we are watching is the local craft movements and knowing where your clothing comes from. We saw a crafting resurgence happen during COVID and people are still pickup up their knitting needles and crochet hooks to create items to wear and love. We also see some carryover of the local food scene into the local fiber scene. We believe that this will continue to grow!