In January 2015, Mexico announced a set of new measures aimed at combating “unfair” trade practices in T&A imports and enhancing the competitiveness of domestic T&A sector in the face of increasing foreign competition.

The proposed measures will particularly target those imports considered to be “undervalued” by the Mexican government. According to Inside US Trade and Sourcing Journal Online, one of these measures is to establish a minimum reference price for imported T&A products. If shipments enter at below that price, they would be subject to an investigation by the Mexican government that could lead to the imposition of additional duties and taxes. To be noted, the proposed new measures will be taken separately from traditional trade remedy measures such as anti-dumping, countervailing duty and safeguard.

Other proposed measures intend to strengthen custom enforcement, including:

- Mexico will required a mandatory registry for T&A imports. A similar registry system has been required for footwear;

- Mexico will postpone the import duty reduction that was expected to be implemented at the beginning of 2016 on 73 apparel items and seven textile made-ups. Originally slated to enter into force on January. 1, 2013, the duty reduction from 25 percent to 20 percent has been twice postponed for one-year periods and will now be delayed until 2018;

- Importers will be required to provide advance notice of shipments to the Mexican Economy Secretariat in the future;

- Mexico will break down the current eight-digit tariff lines for textile and apparel products into 10 digits, which an industry source said would allow tariff rates to be more specific in light of the fact that apparel products have evolved to be more specialized;

Moreover, Mexico will implement a new financing mechanism with total available credit of 450 million pesos (around $30 million USD) over the next 12 months to help the domestic T&A industry (especially small- and medium-sized enterprises) upgrade their machinery and equipment, pursue innovative strategies and develop new products. The Mexican Service Agency for the Commercialization and Development of Agricultural Markets (Aserca) will further support the purchase of cotton from domestic growers by textile manufacturers.

According to WWD, the US T&A industry has three major concerns about Mexican’s proposed measures: one is the potential delay in custom clearance and more complicated documentation requirements; second is the additional tariff rate and increased cost of exporting from the United States or anywhere else in the world to Mexico; third is the lack of policy transparency adding to the potent business risks.

Industry Background

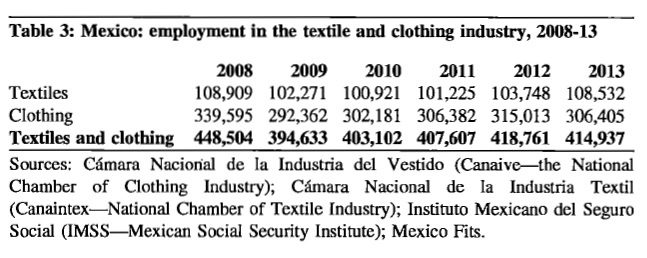

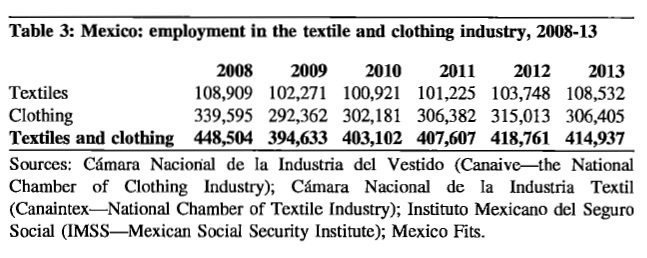

T&A industry accounted for 3.7 percent of Mexico’s GDP in 2013 (1.3 percent for textiles and 2.5 percent for apparel). About 415,000 workers directly employed in the sector in 2013, among which 74 percent worked for the apparel sector.

One important feature of Mexico’s T&A industry is the so called “Maquiladora” operation: simple sewing of garments made from imported fabrics and using cheap labor. The “Maquiladora” operation is largely coordinated by US-based apparel brands and retailers. Most of “Maquiladora” factories are located in the free trade zones, in which equipment and imported materials (such as fabrics) can be duty-free. Output of “Maquiladora” are exported, mostly to the United States.

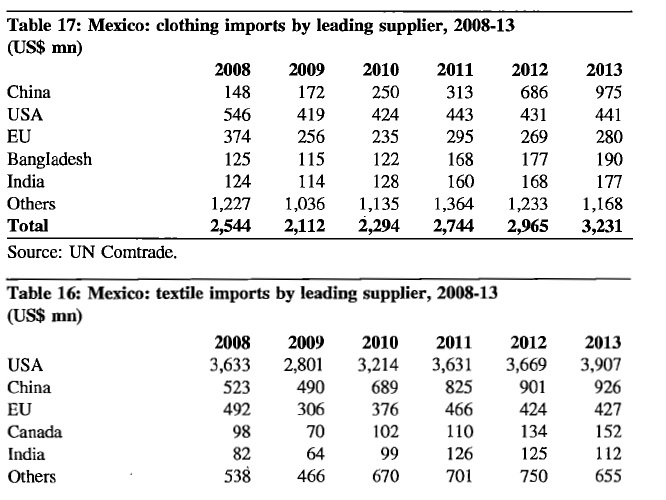

Mexico imported $8.6 billion T&A in 2013, among which $2.4 billion were fabrics, followed by made-up textiles ($0.55 billion) and yarns ($0.39 billion). This pattern reveals Mexico’s heavy reliance on imported textiles due to limited domestic textile manufacturing capacity.

At the same time, Mexico’s apparel imports increased from $2.4 billion in 2008 to $2.9 billion in 2013. Particularly, Mexico’s apparel imports from China surged by 558.8 percent between 2008 and 2013. In 2013 alone, apparel imports from China went up by 42.1% to $0.97 billion. It is said that China is the main target of Mexico’s proposed new import measures.

[Comment for the post is closed]

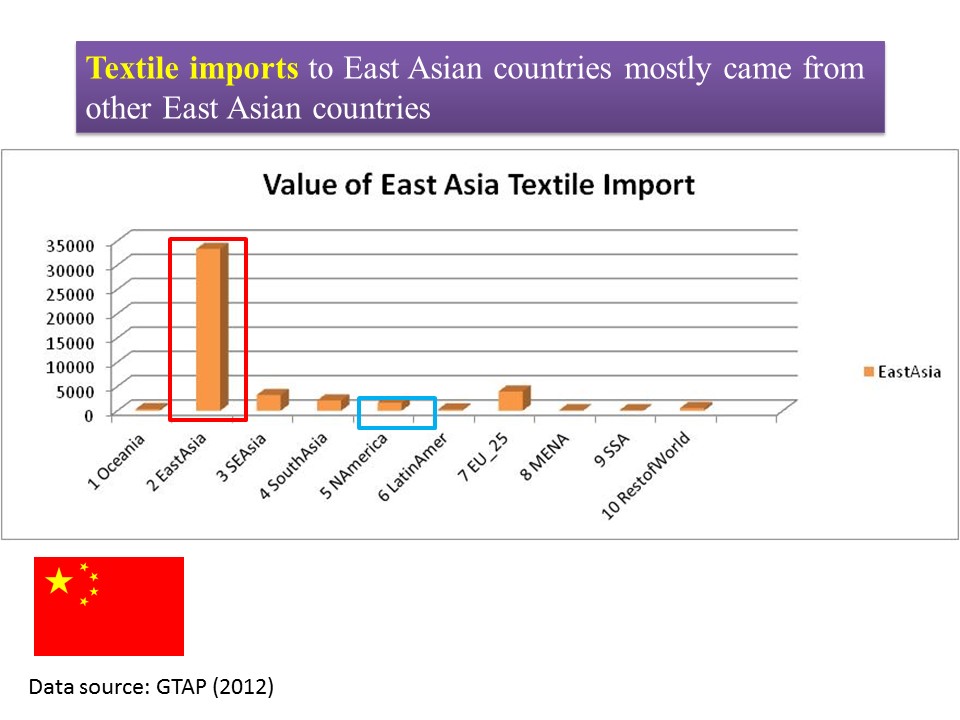

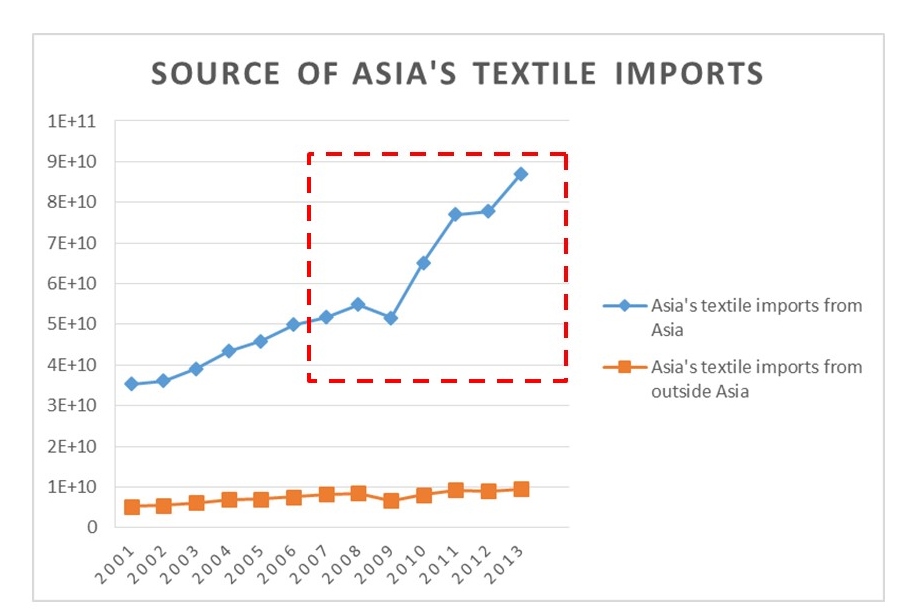

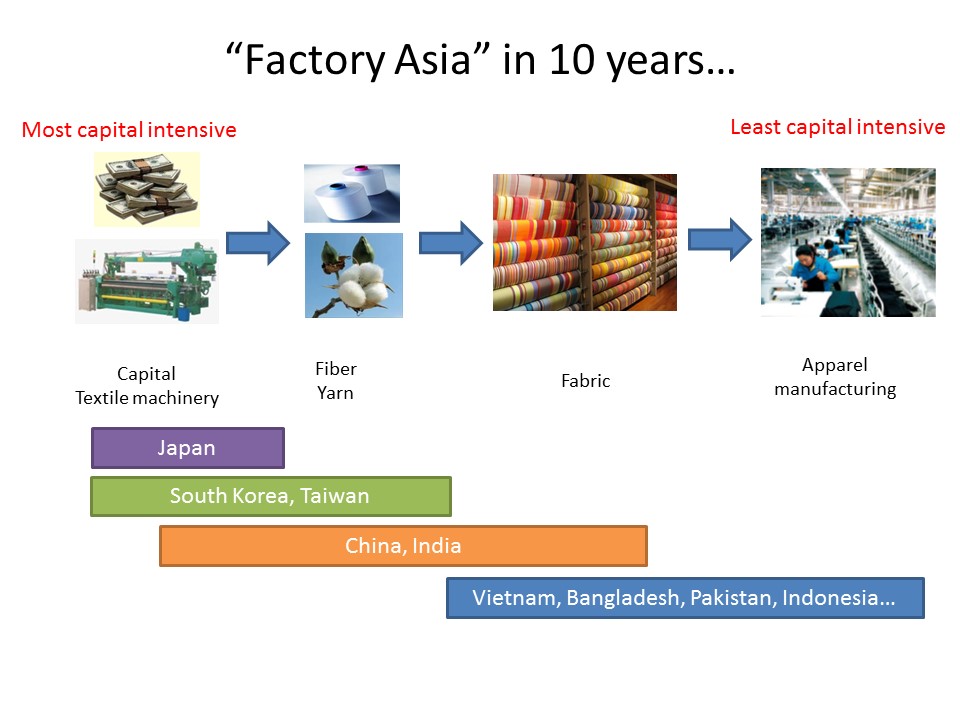

As we discussed in class, following the “flying geese pattern”, countries in Asia form a dynamic division of labor in textile and apparel (T&A) manufacturing. Although China may gradually lose its comparative advantage in labor-intensive apparel manufacturing, it will continue playing a critical role in “Factory Asia” (i.e. Asia-based T&A supply chain). As results, Asia will remain a giant player in T&A production and export in the years to come.

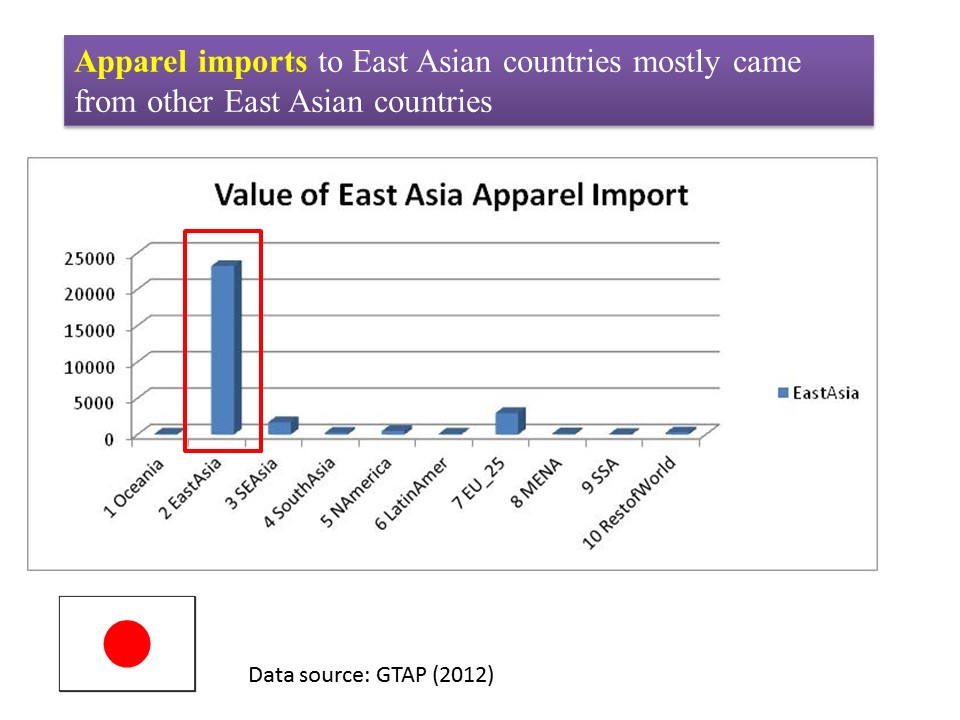

As we discussed in class, following the “flying geese pattern”, countries in Asia form a dynamic division of labor in textile and apparel (T&A) manufacturing. Although China may gradually lose its comparative advantage in labor-intensive apparel manufacturing, it will continue playing a critical role in “Factory Asia” (i.e. Asia-based T&A supply chain). As results, Asia will remain a giant player in T&A production and export in the years to come.