This study aims to examine U.S. fashion companies’ evolving apparel sourcing and business practices in response to a shifting business environment, including ongoing hiking tariffs and geopolitical tensions. Based on data availability, transcripts of the latest earnings calls from about 30 leading publicly traded U.S. fashion companies were collected. These earnings calls were held between February and April 2026, reflecting company performance in the last quarter of 2025 or later. A thematic analysis of the transcripts was conducted using MAXQDA.

Key findings:

First, U.S. fashion companies identified shifting consumer demand, macroeconomic volatility, tariff hikes, and ongoing policy uncertainty as their main business concerns. The pressure on middle- to low-income consumers’ discretionary spending was emphasized as a structural issue that could persist in 2026. For example:

- Kohls: “consumer is behaving differently in this challenging macroeconomic environment. We know our core low to middle-income customers continue to face financial pressure, and they are seeking value…”

- Macy’s : “Our customers across nameplates skew more towards the middle and upper-income tiers. Performance remains stronger in these cohorts, while the lower tiers remain more choiceful. As we look ahead, there are many macroeconomic and geopolitical factors that could influence discretionary spend…”

- Carter’s: “It continues to be a challenging time to forecast the business. Consumer spending appears to have held up well, while other macro indicators, such as consumer confidence and overall inflation, are less positive. Tariffs continue to dominate the headlines… there continues to be a great deal of uncertainty about where all this will settle…”

- Oxford industries: “In an uncertain consumer environment, success comes from controlling what we can control and staying focused on execution…(we) have increased our flexibility and better positioned us to navigate continued uncertainty in the marketplace…”

Second, raising retail prices and focusing on full-price selling have become more common and systematic approaches among U.S. fashion companies to mitigate the impact of tariffs. Nonetheless, fashion companies remain selective–price increases have mostly occurred on fashion-forward, trend-driven, and premium items, while avoiding significant price increases for basic and core categories to shield most price-sensitive consumers. Companies also try to leverage new products and product innovation to justify the price increase. Additionally, many companies have reported that consumers have shown “no resistance” to price increases so far. For example:

- Columbia Sportswear: “For both Spring 2026 and Fall 2026, we increased U.S. pricing by a high-single digit percent. When combined with our other mitigation tactics, our goal in 2026 is to offset the dollar impact of higher tariffs…Retailers remain cautious as tariff-induced price increases are just now beginning to hit the marketplace.”

- Levi’s: “So tariffs, as I mentioned in my prepared remarks, impacts gross margins adversely by about 150 basis points, and we have an FX headwind of about 20. We’re fully offsetting this with higher pricing…We’re not seeing any initial demand reaction to it, so the elasticity is pretty good. More full price selling, which is, something that we’ve been focusing now for about 12-18 months, especially as a product, you know, and newness is resonating well with the consumer. And then lower product costs, which are a combination of lower, you know, better, and lower quarter, as well as the negotiation with the vendors as we rationalize SKUs…reduce unproductive…assortment…”

- Kontoor Brands: “Tariffs net of pricing represent a headwind to our gross margin rate in 2026. We’ve implemented price increases for Wrangler, Lee, and Helly Hansen as part of a holistic plan to mitigate the impact of the increases in tariffs. Our pricing strategies were thoughtful and developed in consideration of the fluid macro environment, the strength of our brands, our elasticity expectations in certain categories and channels, and the retail environment around the globe.”

- Oxford industries: “The price increases implied in our guidance range from 4%-8% and vary by brand. These increases reflect a more elevated assortment as well as higher pricing on new product with relatively limited like-for-like increases on existing product.”

- Victoria’s Secret: “Importantly, we pulled back on promotions, driving more regular price selling and double-digit AUR (average unit retail) expansion, which benefited margins across PINK’s portfolio, showing that the brand is regaining pricing power.”

- URBN: “We’re being highly strategic and thoughtful about taking price, these are definitely not across-the-board price increases. We’ve taken small price increases where we felt the price-value equation was appropriate, have seen really little to no price resistance where we did so. We also want to stress that we remain committed to maintaining our opening price points and our pricing architecture and protecting those items that our customers count on to have great price value. Next, we’re really planning very little incremental price increases over and above what we’ve already implemented this fall and holiday. We really don’t anticipate price resistance. Our focus remains on protecting the integrity and the value of our product while we manage our cost structure appropriately…”

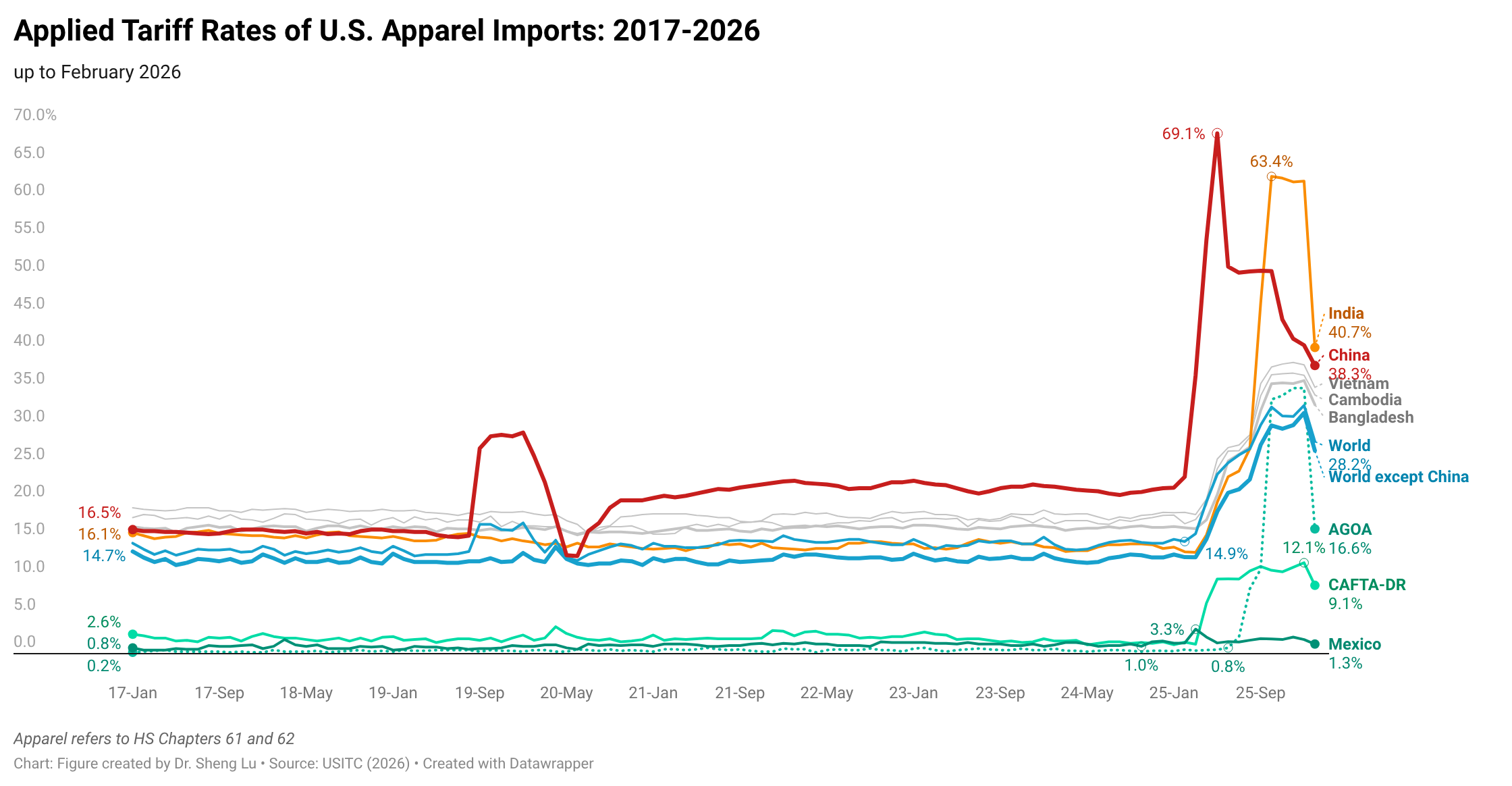

Third, regarding the apparel sourcing base, four strategies stand out: 1) continue sourcing diversification including reducing sourcing from China; 2) expand sourcing from other lower-cost manufacturing hubs in Asia, such as Bangladesh and Vietnam; 3) explore near-shoring opportunities in Mexico and Central America and take advantage of lower tariff benefits; 4) carefully monitor newly negotiated trade agreement with the US, especially those with textile and apparel-specific provisions, such as the one with Bangladesh. Meanwhile, many companies noted that full sourcing realignment takes 12–18 months or more. For example:

- Oxford industries: “Early in fiscal 2025, approximately 40% of our apparel and related products were expected to be sourced from producers located in China. Through the actions we took during the year, that figure declined to slightly less than 30% of our product purchases in fiscal 2025, and our annualized run rate entering fiscal 2026 has been reduced to approximately 15%.”

- Abercrombie & Fitch: “Obviously we’ve talked a lot about our sourcing footprint over the course of the last year or so. Really proud of that diversified network that we have in place, and it’s taken us years to build. We currently source from over 16 different countries. That’s been obviously a core enabler for us and our read and react model here. Approach isn’t changing…”

- Kontoor Brands: “Of particular interest to us is the trade agreement with Bangladesh, which we highlighted. That trade agreement reflected a potential reciprocal tariff ranging from 0% to 19%, depending on the U.S.-grown cotton content of products sourced from Bangladesh. More than 80% of the product we source from Bangladesh does include U.S.-grown cotton. Bangladesh is our largest country of origin from a sourcing perspective, so by nature, it’s also our largest source of tariff pressure.”

- Gildan: “we are pleased to announce that we are moving forward with phase two of our Bangladesh complex. Over the next 18 months, we will begin construction of our second large-scale textile facility, with initial production expected to come online in the later part of 2027. Expanding our Bangladesh footprint is central to reinforcing our cost leadership in ring spin and innerwear…we are increasing our internal capacity in Bangladesh and in Central America, obviously in anticipation to support the Hanes integration.”

- Land’s end: “our teams just got back from a sourcing trip in India with one of our major airline partners, and they couldn’t be happier about the breadth that we’re able to offer, and the opportunity that we’re creating for their employees.”

- Ralph Lauren: “You’ll start to see our broader mitigating actions take shape, country of origin shifts, optimization, merchandising actions. You’ll start to see those all come into play as we move through fiscal 2027”

Additionally, U.S. fashion companies closely monitor geopolitical tensions, including the ongoing conflict in the Middle East; however, the direct impact on sourcing remains limited, with greater concern centered on indirect disruptions to logistics and supply chain operations. For example:

- Nike: “This quarter, we also experienced traffic disruption from the Middle East, and we also are you know taking that into consideration as we’re thinking about where this business stands, and also as we look forward”

- Abercrombie & Fitch: “as it relates to some of the more near term news in the Middle East, you know, we do have some sourcing operations there in the region. Haven’t experienced any disruptions that would have any sort of meaningful impact to the receipt plans here that underpin our outlook. You know, we’ll keep monitoring that and we’ll keep agile with our sourcing base in total.”

- PVH: “It’s important to highlight that significant uncertainty remains around the conflict in the Middle East as well as evolving global trade policies, the broader macroeconomic environment and consumer spend in behavior. Our business in the Middle East, excluding Turkey, is about 1% of our total revenue and solely a wholesale business, so the profit impact is disproportionate at approximately 7%.”

- Victoria’s Secret: “in terms of Middle East, we’re obviously staying very close to the situation and monitoring the developments and how long this may last. There’s two areas right now that we’re paying close attention to. One is just shipments to North America. We are experiencing some delays, but not material that are gonna have a broader impact on the business that way. As you said, we’ve got franchise partners in the Middle East. There are a handful of store closures right now.”

By Sheng Lu

Read the full paper: Lu, S. (2026). U.S. Fashion Companies’ Evolving Sourcing and Business Practices. Global Textile Academy, International Trade Centre (ITC). Geneva, Switzerland

In this blog post, it is noted that a main strategy for U.S. fashion companies is to increase their sourcing from lower-cost manufacturing hubs in Asia, such as Bangladesh and Vietnam, compared to sourcing from China. This shift is supported by the Flying Geese Model pattern that we discussed in class, where Asian countries with less advanced economies replace more advanced Asian countries in the more labor-intensive parts of production processes. This pattern helps to explain why U.S. companies are sourcing more from Bangladesh and Vietnam, because these countries are in the 4th tier (lowest tier) of Asia’s regional economies. China is in the 3rd tier and at a more advanced level, so it makes sense that sourcing from China will be more expensive for U.S. companies; with lesser developed economies, Bangladesh and Vietnam will be cheaper options. I’d like to further explore how much cheaper it actually is to source from a tier 4 Asian supplier versus a tier 3 one, and how much U.S. companies are actually saving by shifting their sourcing.

The course concept that relates to this blog post is the flying geese model because it is explaining how production can shift to different countries overtime to lower costs when things arise like tariffs and economic uncertainty. Therefore, when costs start to rise in countries like China, retailers will turn to lower cost countries for production like Bangladesh, and Vietnam because they have lower wages and are less developed than China. In addition, the blog discusses nearshoring to places like Mexico and Central America (which we discussed in class). This is important to note because it is showing that retailers not only care about the lowest possible production cost, but they also are looking into faster shipping channels as well. Changes like these can be a demonstration of the flying geese model. A takeaway that I took from this blog is that retailers and companies should try to be more flexible rather than put all their eggs in one basket with one country. This will help brands steer clear of potential tariffs and issues that are rising globally due to economic uncertainty in the world. If the brands are able to pivot quicker, then they can stay ahead in the fashion industry, and continue to move their production to benefit their company.

This blog post relates to the flying geese model that we heavily discussed in class. This model explains the level of development of different countries and how that order aligns with which countries produce what. When the most developed country, Japan, begins to have prices rise due to intense labor and other factors (tariffs), America tends to move to lesser developed countries where costs will be lower. These countries that are currently producing the cheapest garments are Bangladesh, Cambodia and Vietnam, while Japan is producing machinery. Another point I took from this blog was the comment about nearshoring from places like Mexico and Central America. This further proves how seriously America takes supply chain changes, and factors in other components such as quicker shipping and reliability. From discussing this topic in class and also reading this post, I think it’s very important for countries to factor in all of the different changes in the supply chain, and constantly be looking for the best strategies. Keeping strong relationships with all production countries will be helpful in times of unexpected change, and allow America to feel safe in having other options to fall back on.

One key concept from class that relates to this blog post is the flying geese model. In class we talked about why the flying geese model is important because it shows how textile and apparel production changes through Asian countries based on their economic development. More developed countries are more technologically advanced and less are more labor intensive. In this blog post, we see that the flying geese model is supported by the data because US fashion companies are reducing sourcing from China and expanding into low cost countries like Bangladesh and Vietnam. Oxford industries reduce its souring from China from 40% to 15% in early fiscal 2025 to 2026. This shows how the sourcing shifted. Going forward, I think fashion companies should add more flexible sourcing places instead of relying on one country.

A concept we have discussed both the advantages and challenges of in class is the “China+1” sourcing strategy, popular for companies seeking diversified supply chains. “China +1” as a name describes the strategy pretty succinctly, basing production in China while also incorpoarting another country to reduce risks associated with cost, tariffs, and production lead time. China is known for its advantage in labor as well as generally low costs, so exiting the country entirely (even amidst tarriff treats) would likely be an unwise decision for many brands who have history producing there. Rather than fully exiting China, they are reallocating supply chain processes in other countries. In this blog post, this strategy is shown clearly by firms who are diversifying into countries like Vietnam and Bangladesh, exploring nearshoring options in Mexico, while still maintaining much of their production in China. These shifts in business practice highlight that sourcing is not only based on costing logistics, but geopolitical tensions, comparative advantage, and risk aversion. A key takeaway that all brands should see in these examples is an overarching push to diversify sourcing countries and strategies, never relying too heavily on one or another, and having multi-country backup plans. This is a complex shift, involving changes in many logistics, but is alltogether necessary for the long term stability of production.

In class, we’ve been talking about how global supply chains shift across different countries based on costs and development levels. One idea we discussed in class that relates to this blog post is sourcing diversification. This basically means companies don’t rely on just one country for production, but instead spread it across different places to lower risk. This approach has become more important with rising tariffs and uncertainty in global trade.In the blog post, you can really see this happening because a lot of companies are starting to pull back from China and shift production to places like Vietnam and Bangladesh. What stood out to me was how Oxford Industries dropped its sourcing from China from around 40% to about 15%, which shows how big of a change this actually is. The post also mentions that these kinds of shifts can take over a year, which kind of shows how complicated it is to actually move production and adjust a supply chain.To me, this shows that companies aren’t really leaving Asia, but are instead shifting production within the region to find lower costs and more stability. It also suggests that sourcing strategies will keep evolving based on tariffs and labor costs. At the same time, it makes me question how long this strategy will last if production costs start rising in these newer countries too.

Sourcing diversification is not a key concept discussed in April/May lectures

Western Hemisphere supply chain sourcing, which stresses nearshoring production to places like Latin America to lower risk and enhance speed, is one important class concept that connects to this blog article. We covered in class how businesses prioritize this approach based on regulatory and economic considerations that influence sourcing decisions, such as tariffs and trade agreements like the USMCA, as well as cheaper shipping costs and quicker lead times. As businesses react to geopolitical unpredictability and growing expenses in Asia, this idea is particularly relevant today. The blog post makes it evident that American fashion brands are moving their sourcing from China to Western Hemisphere nations like Mexico and Central America. In addition to addressing legislative pressures like tariffs and trade disputes, this is in line with economic drivers like lowering inventory risk and shipping delays. The article emphasizes how businesses are putting an emphasis on adaptability and resilience, which nearshoring helps by reducing supply chains and enhancing response to shifts in demand.

In class, we discuss the competing wants of the US textile industry and US apparel industry. While the textile industry likes yarn-forward rules that force manufacturing into the states, the apparel industry prefers larger free trade agreements. We are reaching a breaking point for these industries in the current economic climate. Many brands’ key customers are mid to low-class buyers, and they are starting to feel the pressure on their discretionary spending. Due to macroeconomic volatility and uncertain geopolitics, discretionary income is going down, and people overall will become more guarded with spending. While the current tariffs are trying to push manufacturing into the states, they are failing and creating price hikes. The tariffs are a hidden tax on consumers. Given this, it is important to rethink certain economic policies. While some may be beneficial to the textile industry, overall, the current policy is becoming harmful to the consumer and the US economy.

One key concept from class that relates to this blog post is the Flying Geese Model. This model explains how industries start in more developed countries and then move to less developed countries when costs and wages get higher in the original country. In the blog, companies are dealing with weak demand, higher prices, and tariffs, which is making them rethink where they make products. This leads them to shift production to lower-cost and more flexible places such as Bangladesh and Vietnam.

The model also helps explain the changes in sourcing strategy. Companies are reducing their reliance on China while increasing near-shoring in Mexico and Central America to improve speed and deal with tariffs. These changes do not happen quickly, since companies say it can take 12–18 months or more to fully adjust.

A policy recommendation is to reduce uncertainty in trade rules so companies can plan better. The blog shows that changing tariffs and unpredictable policies are causing companies to adjust sourcing, including moving production away from China and increasing near-shoring in Mexico. However, because these changes take a long time, uncertain policies make it harder for companies to adjust smoothly. More predictable trade rules would help companies manage supply chains with less disruption.

One concept from class that relates to the blog post is near-shoring. This occurs when companies move production closer to their customers to respond to demand faster, lower risk, and shipping time. This strategy has grown in popularity greatly recently due to the uncertainty of tariffs and their constantly changing rates. This idea connects to the article because the majority of U.S. fashion companies rely on only Asia and are left vulnerable to tariffs and shipping delays. Now they are exploring their options in Central America and Mexico which will also allow for shorter lead times while keeping costs competitive. From a managerial standpoint, fashion companies must find a balance between low costs, speed, and flexibility. Nearshoring is the answer for most of these companies since it allows for them to avoid delays and the unnecessary cost of tariffs.

This specifically relates to the Flying Geese Model we discussed in class. Fashion companies are shifting away from high cost countries like China to low cost countries like Bangladesh and parts of Central America. The model shows how companies move from more developed countries to less developed countries as wages and costs grow. Near-shoring and the Flying Geese Model demonstrate how companies change their sourcing to stay updated and remain efficient in this industry.

One key concept this blog post relates to is the flying geese model. In class, we discussed how the model explains the shifting of textile and apparel production within Asia based on each country’s level of economic development. More advanced countries move toward higher value and technology intensive production, while less developed countries take over more labor-intensive apparel manufacturing. This concept is clearly reflected in the blog post because many US fashion companies are reducing sourcing from China and expanding into lower-cost countries such as Bangladesh and Vietnam. The article also highlights how tariffs, geopolitical tensions, and rising costs are encouraging companies to shift production to countries with lower labor costs and growing manufacturing capacity. This directly supports the Flying Geese Model because production is moving regionally within Asia rather than leaving Asia completely. One important implication is that sourcing decisions today are no longer based only on cheap labor, but also on flexibility, trade policy, and long-term risk management.Going forward, I think fashion companies will continue diversifying production across several countries instead of relying too heavily on one sourcing hub.

A topic from class that strongly connects to this blog post is nearshoring, specifically the shift toward producing goods closer to key consumer markets. Many fashion companies are reconsidering long-distance sourcing strategies because relying heavily on Asian manufacturing has exposed them to things such as tariffs, delays, and sourcing uncertainty. As a result, brands are increasingly looking at countries like Mexico and Central America as alternative sourcing locations. The article reflects this trend by showing how U.S. apparel companies are trying to build more responsive and efficient supply chains. Producing closer to the American market can reduce transit times, improve inventory management, and help companies react more quickly to changing consumer demand. However, the cost of nearshoring can be a lot higher than manufacturing in Bangledesh or China, but from a business perspective, fashion brands today need to prioritize not only affordability, but also speed and adaptability of their manufacturers.

One key concept that relates to this blog post is the “China Plus One” decoupling that we discussed for the Opeka case study. The “China Plus One” is when a company moves only the final assembly step to a non-tariffed country like Vietnam or Indonesia. This would allow the company to regain access to the US market without the full effect of tariffs while maintaining relationships and production in China. The blog post suggests, “four strategies stand out: 1) continue sourcing diversification, including reducing sourcing from China” (Lu, 2026). US companies need to be able to source from different countries for different parts of the production process due to an increase in tariffs. One downside to the “China Plus One” is that factories in Vietnam or Indonesia may be over-capacitated and not able to mass-produce new products. In the blog, the solution for many of the brands is to source in Bangladesh, India, and China. While the brands explored many strategies, I think that the “China Plus One” can be the most effective for many of these well-established brands.

This article highlights how the US is shifting production to other countries such as Vietnam, Bangladesh and India due to China’s high tariffs. This relates to the concept of the flying geese model which indicates apparel production continues shifting toward lower-cost developing countries as global sourcing patterns evolve. The flying geese model explains that as countries become more advanced and wages rise, they move away from labor-intensive industries like apparel assembly and focus on higher-value activities. Therefore, the US is diversifying their sourcing to less developed countries that are more labor intensive. One implication from this is that countries need to diversify their supply chains rather than relying solely on one country. We noticed this issue in our most recent case study with Okepas sourcing from China with rising tariffs. Diversifying sourcing can help prevent tariff or geopolitical risks. The question at hand is with rising trade instability and geopolitical tensions will this accelerate long-term nearshoring in the Western Hemisphere, or will companies continue prioritizing the lowest-cost sourcing locations globally?

In class we talked a lot about the need and wants of the US textiles and apparel industries. The textile industry prefers yarn-forward rules to keep production in the states but for apparel larger free trade agreements are preferred. With the current economic climate that we are in we are seeing people struggling more and more to pay their bills, and put gas in the car, let alone purchase clothing. Most brands key customers are mid and low class buyers, but these buyers are having less and less free income to spend on things they want, like clothing. The current tariff situation is failing to move production to the US, and is in turn just making things more and more expensive for American consumers.

One key concept from our class that relates to this blog post is the “China Plus One” strategy that we discussed while we completing the Opeka case study. “China Plus One” is when companies keep some production activities connected to China, but move the final assembly or additional sourcing operations to non-tarriffed countries. This strategy helps companies reduce tariff costs and lower supply chain risks while still benefiting from China’s manufacturing capabilities. This concept is clearly reflected in the blog post as many US fashion companies are reducing their dependence on China while expanding sourcing in countries such as Bangladesh, Vietnam, India, and Central America. For example, Oxford Industries reduced sourcing from China from 40% to 15%, while companies such as Gildan are expanding production facilities in Bangladesh. These shifts show how companies are trying to avoid tariff pressure and improve sourcing flexibility without completely leaving Asia. A managerial implication is that fashion companies need flexible sourcing networks to respond to tariffs and geopolitical uncertainty. However, the article also shows that sourcing realignment can take over a year, making it difficult for smaller brands with fewer resources. Going forward, it will be interesting to see whether “China Plus One” strategies remain effective if tariffs continue expanding to more countries.

This blog post depicts elements of U.S trade policy as discussed in class lectures. Political uncertainty has amplified geopolitical tension and has forced retailers to restructure pricing, sourcing, and marketing efforts to mitigate the impact of tariffs. Tariffs, Trade Agreements and the U.S. withdrawnment, and Global Relations have changed the global landscape of retail. This has pressured retailers to rethink strategies in 1) staying within China but reducing the amount of production there with some relocation, 2) expand into other Asian countries such as Vietnam, 3) develop nearshoring relations with Mexico and Central America, or 4) move production into the U.S. to avoid tariffs altogether. The blog demonstrates these strategies by displaying first hand accounts from several different companies such as Oxford industries, Abercrombie & Fitch, Gildan, etc. and their short-term and long-term plans relating to the strategies above. As discussed in class, there are pros and cons to each of these strategies with high relocation costs, production capacities, available infrastructure, environmental stability, and efficiency of cost and speed being at the forefront of concerns. For example, many companies as discussed in the blog that switched production into Middle Eastern countries have faced geo-political issues in having to face rising tensions in those areas which could hinder production and cause disruptions in the supply chain. This has affected companies such as Victoria’s Secret, PVH, Nike, etc. This shows how relocation due to tariffs has made creating long-term strategy unpredictable for companies, in that they are now faced with tradeoffs to find the optimal location. This uncertainty poses difficulty for retail leaders and managers as they struggle to find sufficient strategies to replace their original supply chain practices. These short-term decisions to offset tariffs do not provide longevity in dependable and scalable aspects. As they may find a way around tariffs by relocating to other countries, increasing prices, or minimizing promotional efforts, these all create new problems of uncertain environments or customer price sensitivities.

This article connects to what we learned during class because it shows just how much political tensions and tariffs are reshaping the fashion industry worldwide. Many brands based in the United States are working to ensure products are still appealing to cost-conscious consumers as costs are rising. Sourcing shifts from China to countries such as Bangladesh and Mexico are important and illustrate how retailers are responding to tariff changes. Overall, this connects to the regional production trade agreements like USMCA and CAFTA-DR we discussed during class. Supply chains are becoming more flexible as they are dependent on consistently evolving tariffs and trade policy.

One key concept from class that the article strongly reflects is the Flying Geese Model through U.S. fashion companies’ ongoing sourcing diversification away from China. Brands including Oxford Industries and Abercrombie & Fitch discussed expanding sourcing in Bangladesh, Vietnam, India, and Central America to reduce tariff exposure and labor costs. For example, Oxford Industries reduced sourcing from China from 40% to about 15%, while Gildan is expanding manufacturing facilities in Bangladesh. These shifts demonstrate the classic “flying geese” pattern where production migrates to lower-cost economies as geopolitical tensions and tariffs make older sourcing hubs less attractive. The article also shows how trade agreements and tariff policies accelerate this movement. One important implication is that fashion companies must build flexible and diversified sourcing networks rather than relying heavily on one country. The article suggests that firms with established multi-country sourcing strategies are better prepared to manage tariffs and geopolitical uncertainty.

One key concept from our class that relates to the article “U.S. Fashion Companies’ Evolving Sourcing Practices amid Tariffs and Geopolitical Tensions” is sourcing diversification. In class we discussed how fashion companies reduce risk by spreading production across multiple countries instead of relying heavily on one sourcing location. This article shows how many U.S. fashion companies are diversifying their sourcing networks because of rising geopolitical uncertainties, increased tariffs, and economic challenges. Some examples include Oxford Industries and Abercrombie & Fitch, which have minimized sourcing from China but increased production from Bangladesh, Vietnam, Mexico, and Central America.It was mentioned in the article how companies were offsetting increased costs by increasing prices strategically and prioritizing full-price sales over promotional efforts. It was interesting to know that a lot of brands were avoiding increasing the price of staple products to save low-income customers while increasing prices for trendy and luxury goods. Overall, the article made me realize how connected globalization, sourcing, and pricing tactics are in the fashion industry. I wonder if companies would shift their production from China in the coming years or if the sourcing trends would settle down due to reduced tariffs and decreased geopolitical conflicts.

A key concept from our class that can easily be related to this blog post is the Flying Geese Model. We briefly discussed how the flying geese model is represented through the movement of labor intensive jobs in Asia migrating from areas becoming higher in capital, to parts of the country abundant with labour as costs rise over time.

In this blog, the concept is supported by the sourcing shifts that many U.S. fashion companies are making away from China and toward countries like Bangladesh and Vietnam. As China becomes more developed and wages increase (increase in capital), companies are now seeking lower cost suppliers where labor costs remain cheaper. Additionally, the article shows how tariffs and geopolitical tensions are accelerating this transition, pushing brands to diversify sourcing and avoid dependence on one country. The discussion of nearshoring to Mexico and Central America demonstrates that companies are balancing low production costs with faster shipping and reliability.

Going forward, I think fashion companies will continue to seek out the cheapest form of sourcing; yet keep sourcing spread out among multiple networks in order to stay flexible during uncertain economic conditions.

One key concept from class that clearly connects to this article is sourcing diversification and how it reflects the broader Flying Geese Model. The article shows that U.S. fashion companies are actively shifting production away from China due to rising tariffs and geopolitical uncertainty. For instance, Oxford Industries reduced its China sourcing from 40% to about 15%, and Gildan is expanding its Bangladesh manufacturing footprint, noting that this move is “central to reinforcing our cost leadership” (from the document). These examples illustrate production migrating to lower‑cost regions as conditions in China become less favorable. What stood out to me is how companies are not only diversifying geographically but also adjusting pricing strategies to manage tariff pressure. Many brands reported taking selective price increases, especially on trend‑driven items, while protecting core basics for more price‑sensitive consumers. Levi’s even noted “no initial demand reaction” to higher prices, which shows how pricing power and product innovation can offset cost shocks. Overall, the article reinforces how intertwined global sourcing, trade policy, and pricing strategy have become. It also makes me think about whether these sourcing shifts will continue long‑term or stabilize if tariffs ease and geopolitical tensions cool. Companies with flexible, multi‑country networks seem best positioned to adapt either way.