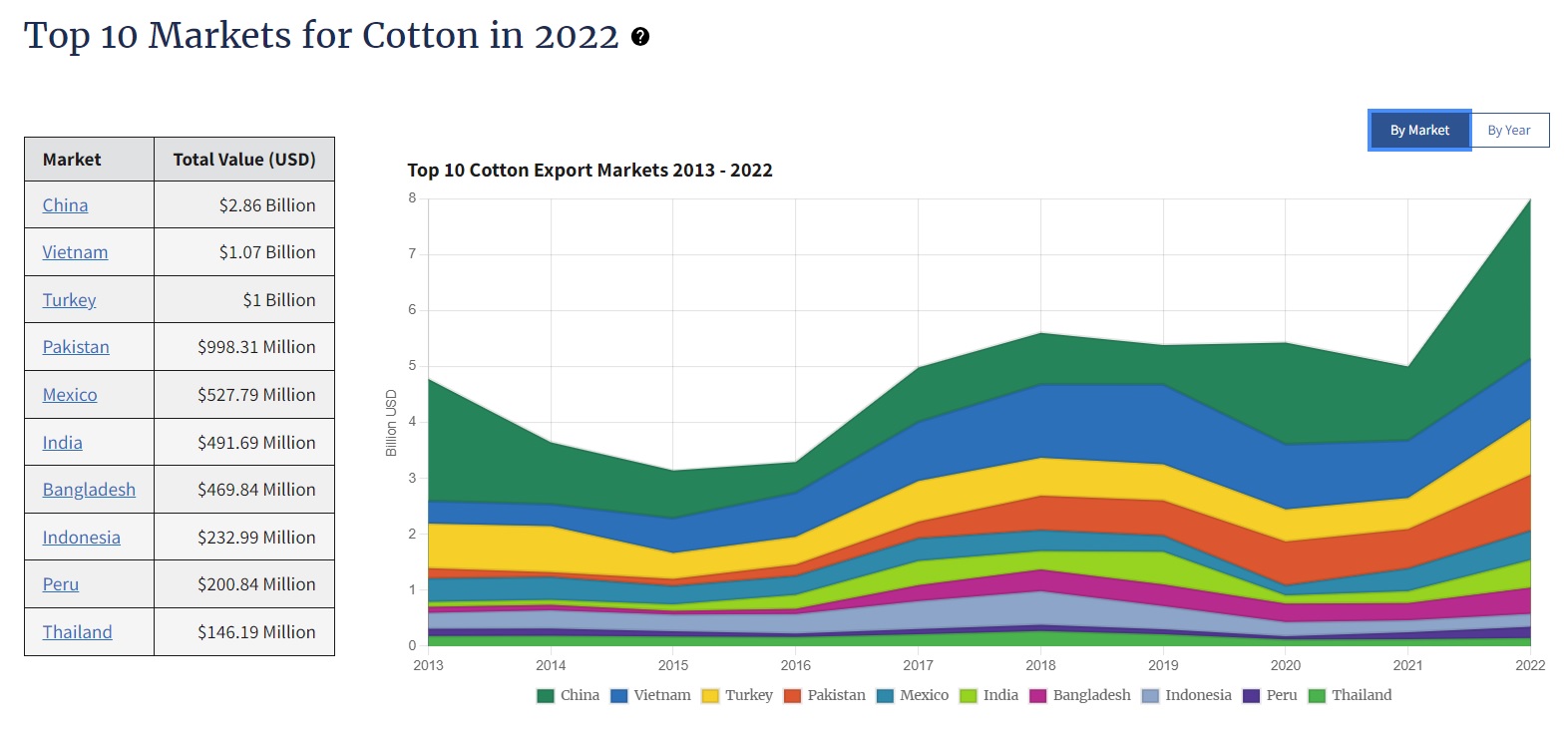

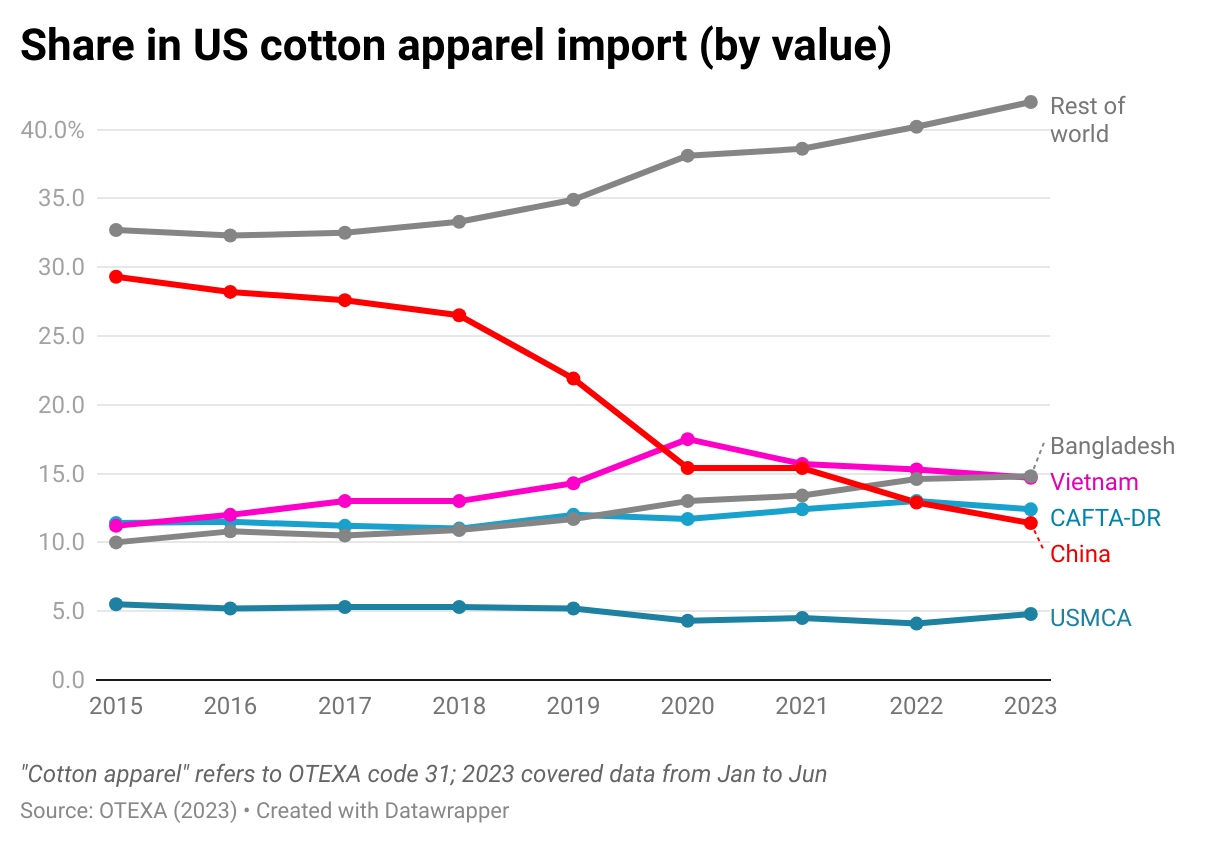

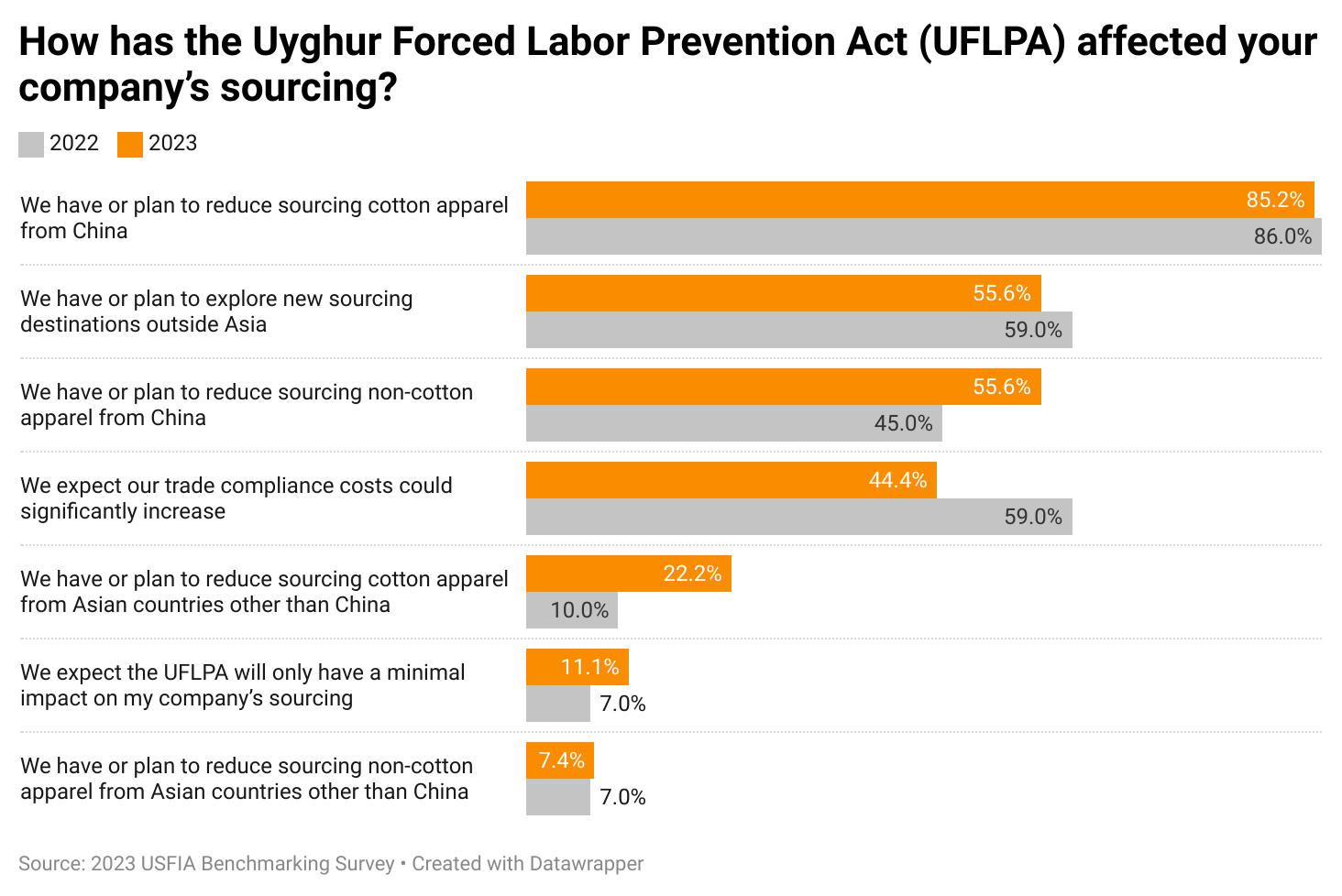

Discussion questions: What factors contribute to the complexity of eliminating banned Xinjiang cotton from the apparel supply chain? How can the current efforts be enhanced to better address the situation and by whom? Feel free to share any other reflections on the video and the graphs.

Hannah Laurits (second from the right) worked as a sourcing intern for Haddad Brands in New York City in the summer of 2023. In the picture, Hannah was visiting the company’s world class distribution center in New Jersey.

Hannah is passionate about adaptive clothing and making the fashion industry more inclusive and sustainable. She has participated in several related research projects, including working at UD’s Health and Innovation Lab and designing adaptive clothing for children with Down syndrome. Hannah’s master’s thesis explores U.S. retailers’ merchandising and business strategies for adaptive clothing. As a graduate instructor, Hannah teaches FASH133 (Foundations for Fashion Innovation), an important foundational course for FASH freshmen. Hannah is the recipient of the 2023 International Textiles and Apparel Association (ITAA) Sara Douglas Fellowship in recognition of her academic excellence and accomplishments.

During the summer of 2023, Hannah had the exceptional opportunity to work as a sourcing intern for Haddad Brandsin New York City. Below, she shared her reflections on this incredible internship experience.

Question: What does a typical day look like during your sourcing internship with Haddad?

Hannah: Each day, I would enter Haddad’s beautiful Manhattan office and make my way up to my desk on the 10th floor, which was home to the design and sourcing departments. I had the opportunity to sit next to my mentor and assist her in her day-to-day tasks as a Fabric and Trim Research &Development (R&D) Manager. This often consisted of maintaining fabric/trim development digital and physical libraries, creating new fabric swatch headers, entering fabric/trim data in PLM, partnering with Product Development to establish fabric and trim codes for PLM, and analyzing new fabric developments. I also assisted in collaborating and developing fabrications, finishes, and trims with our supply chain by communicating feedback via internal emails.

One thing that I really enjoyed was that each day consisted of working cross-functionally with the different teams. I helped prepare for and sit in on weekly fabric/trim development status meetings with the various Design teams where fabric/trim developments for the upcoming seasons were discussed and designers would make new fabric requests for their added styles. I also sat in on bi-weekly fabric/trim development status meetings with the Product Approval team to ensure the fabric samples from mills were up to standard for development. Here, I was able to help weigh in on fabrics and compare them to our standards to determine if they met our requirements or if they needed to be changed and how. Additionally, some days included meetings with various suppliers to discuss innovations in fiber, fabric, finish, and trim.

Being part of an internship that enabled me to perform meaningful work from day one, provided countless opportunities for personal growth, and exposed me to working with some of the most iconic global brands (e.g., Levi’s) was a truly fulfilling experience.

Question: Any major projects did you work on during your internship? What did you learn from the experiences?

Hannah:Each Haddad Legacy Intern was assigned and worked on a project for their department based upon a real business need. Based on my educational background and my passion for sustainability, my team outlined a project that would best fit. This involved researching innovative sustainable solutions and sourcing practices to further their sustainability efforts.

My research was not only conducted from outside sources but from internal ones as well. I felt an immense amount of support from all of the individuals who helped me accomplish this project and was excited to learn that they also are just as excited about sustainable practices as I am. At the end of the internship, each intern had the chance to present to senior management our individual projects. This experience taught me how to create a visually compelling presentation and relay large amounts of data concisely and effectively.

Question: What insights did you learn about the fashion apparel industry from the internship? For example, the key issues the industry cares about or the challenges it faces.

Hannah:From my internship experience, I was able to see firsthand key topics important to the fashion/apparel industry; specifically, two areas caught my attention.

First, sustainability and social responsibility. Consumers and investors are seeking more sustainable products and better practices from the brands they love. Considering this, sustainability-forward brands are focused on maintaining their high values regarding these areas and keeping their practices aligned with them.

Second, the fashion industry is constantly seeking innovative technology solutions, including in the sourcing and supply chain areas. Technology is evolving faster than ever, helping create efficient solutions to drive the fashion industry forward. Technologies such as 3D printing, AI, laser cutting, and more are being used to improve the industry in various ways such as trend forecasting, supply chain, and consumer experience, just to name a few. Even regarding sustainability, many fashion brands are investing in or actively exploring new technology solutions to help them develop a more sustainable and ethical supply chain and improve sourcing transparency, traceability, and accountability.

Question: How do your learning experiences at FASH help with your internship? Any specific knowledge or skill sets do you find most critical?

Hannah:FASH had a great influence on my decision to pursue a sourcing internship with Haddad Brands. It was through the UD & FASH department’s Fashion Career Meetupthat I was able to connect with the amazing HR team at Haddad Brands and learn more about the company.

Specifically, it was FASH455 (Global Apparel Trade and Sourcing) that piqued my interest in the world of sourcing and provided foundational knowledge for my internship. Working in fabric research and development, on a daily basis, I referred back to key concepts from FASH215 (Fundamentals of Textiles I) and FASH220 (Fundamentals of Textiles II) on fiber, yarn, fabric, structures, color, and finish. Additionally, the FASH Social Responsibility and Sustainability certificate coursesplayed a unique role in my experience, helping me bring a sustainability forward perspective into my internship and providing a solid background to further build upon for my internship project.

Furthermore, the FASH department at UD excels at providing students with extensive foundational fashion industry knowledge. Not only is the course curriculum excellent, but so is the faculty who goes above and beyond to help foster student’s education and build critical professional skills.

Question: What’s your plan after graduation?

Hannah:I am currently working on wrapping up my master’s program and am on track to graduate in May 2024. I am seeking a full-time role that allows me to have a hand in developing products that have a positive impact on people and the planet. Potential roles include sustainability, social compliance, sourcing, product development, and product line management related to fashion apparel products. While I am originally from Delaware, I am hoping to relocate to a city on the East Coast such as NYC, Philadelphia, or Baltimore. However, I am open to considering job opportunities and locations beyond this scope. As my graduation approaches, I am eager to begin my career in the fashion apparel industry.

Meanwhile, I am actively seeking winter and spring internship opportunities in the greater Philadelphia area or remote positions to enhance my professional development.

#1 What are the examples of globalization in the above two videos about Temu?

#2 Based on the videos, who are the winners and losers of globalization and why?

#3 What role does international trade play in Temu’s business model?

#4 Some suggest ending the “de minimis rule.” Based on the videos, what is your view and recommendation for US policymakers?

#5 Anything you find interesting/surprising/intriguing in the video and why?

(Note: Anyone is welcome to join the discussion. For students in FASH455, please address at least two questions. Please mention the question number in your response, but there is no need to repeat the question).

Note: About “de minimis rule.”: Under US customs law, specifically the Trade Facilitation and Trade Enforcement Act of 2015, import duties are generally waived for goods valued at $800 or less per person per day. Therefore, Temu’s shipping from China to US consumers is likely to be eligible for the benefits.

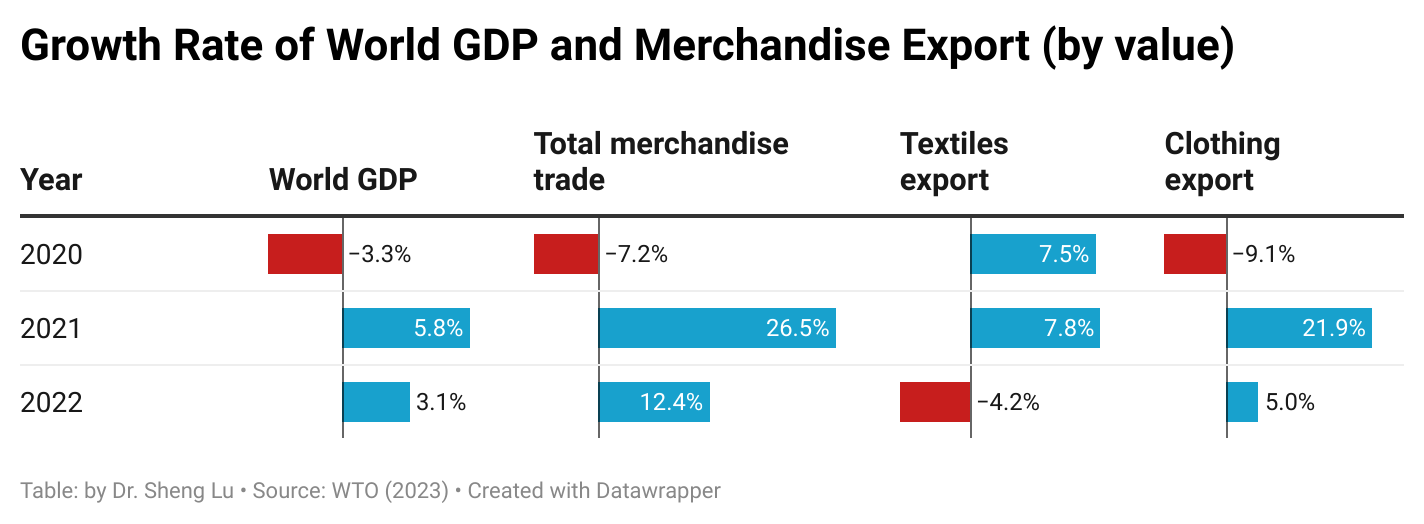

This article comprehensively reviewed the world textiles and clothing trade patterns in 2022 based on the newly released World Trade Organization Statistical Review 2023 and data from the United Nations (UNComtrade). Affected by the slowing world economy and fashion companies’ evolving sourcing strategies in response to the rising geopolitical tensions, mainly linked to China, the world’s textiles and clothing trade in 2022 displayed several notable patterns different from the past.

Pattern #1: The expansion of world clothing exports witnessed a notable deceleration in 2022, primarily attributed to the economic downturn. Meanwhile, the world’s textile exports decreased from the previous year, affected by the reduced demand for textile raw materials used to produce personal protective equipment (PPE) as the pandemic waned.

The world’sclothing exports totaled $576 billion in 2022, up 5 percent year over year, much slower than the remarkable 20 percent growth in 2021. The slowed economic growth plus the unprecedented high inflation in major apparel import markets, particularly the United States and Western European countries, adversely affected consumers’ available budget for discretionary expenditures, including clothing purchases.

The world’s textile exports fell by 4.2 percent in 2022, totaling $339 billion, lagging behind most industrial sectors. Such a pattern was understandable as the demand for PPE and related textile raw materials substantially decreased with the pandemic nearing its end.

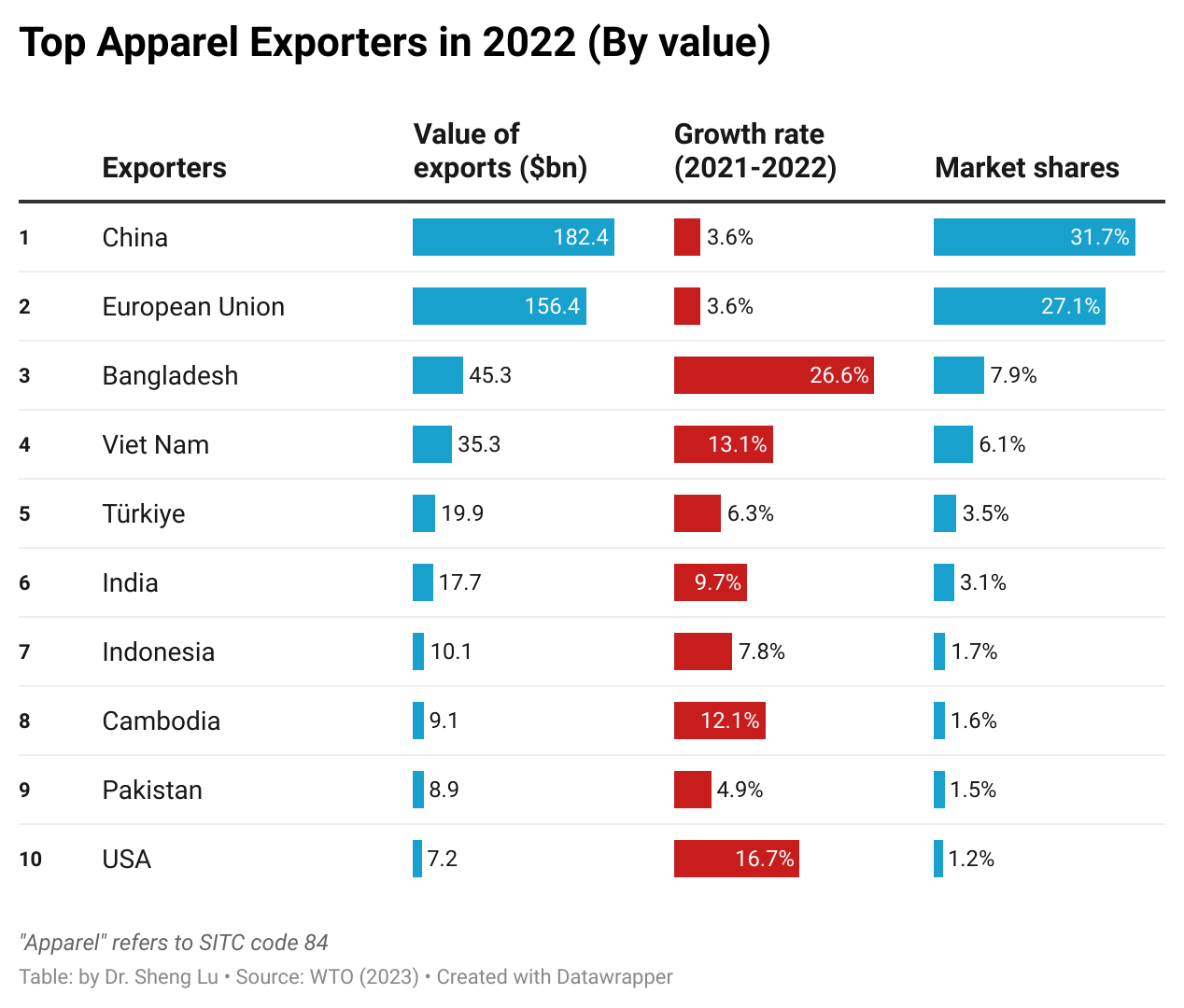

Pattern #2: China continued to lose market share in clothing exports, which benefited other leading apparel exporters in Asia. Notably, for the first time, Bangladesh surpassed Vietnam and ranked as the world’s second-largest apparel exporter in 2022.

In value, China remained the world’s largest apparel exporter in 2022. However, China’s clothing exports experienced a growth of 3.6 percent, below the global average of 5.0 percent, positioning China at the bottom of the top ten exporters.

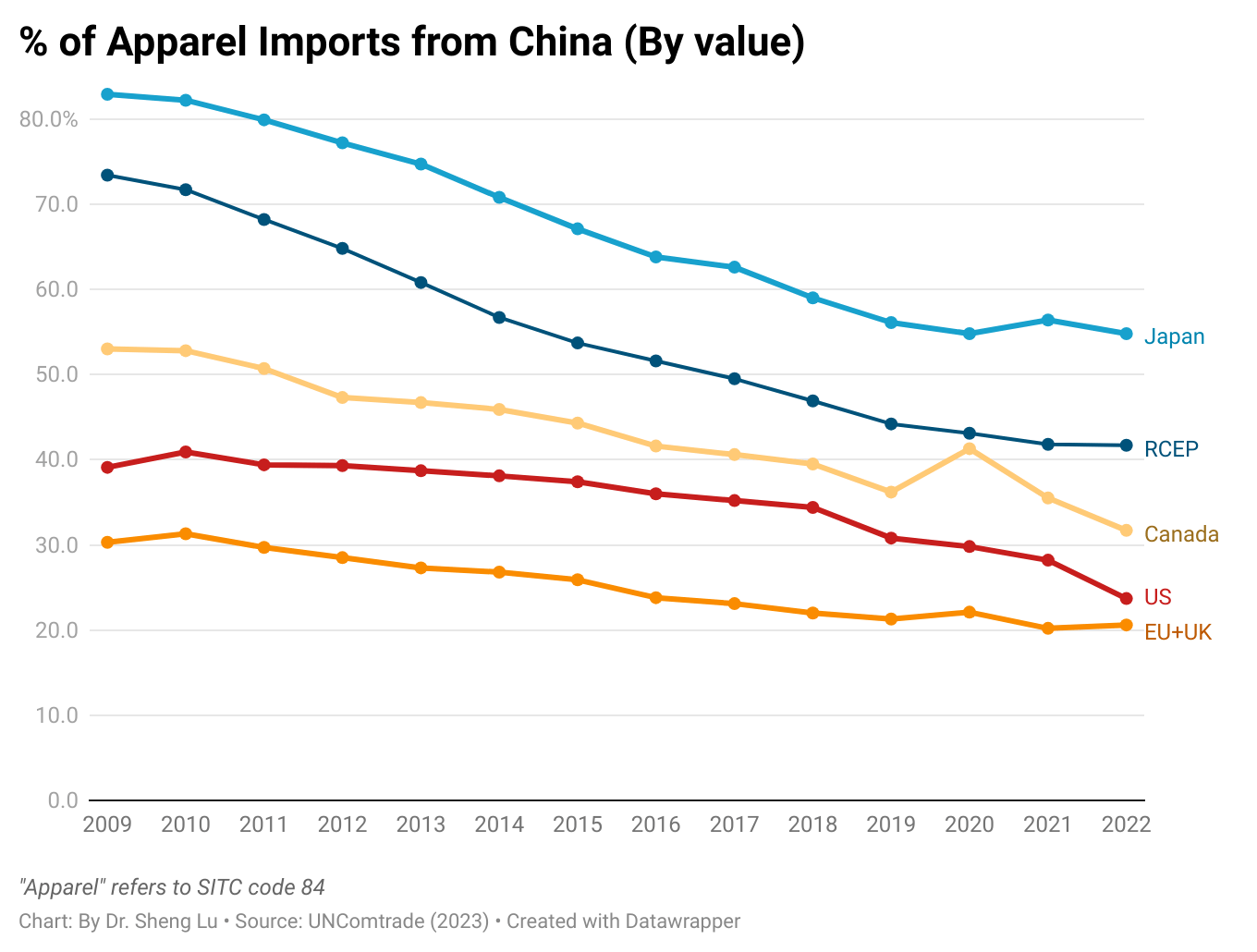

China’s global market share in clothing exports dropped to 31.7 percent in 2022, marking its lowest point since the pandemic and a significant decrease from the approximate 38 percent recorded from 2015 to 2018. In fact, China lost market share in almost all major clothing import markets, including the US, the EU, Canada, and Japan. The concerns about the risks of forced labor linked to sourcing from China and the deteriorating US-China relations were among the primary factors driving fashion companies’ eagerness to reduce their ‘China exposure” further.

China has been diversifying its clothing exports beyond the traditional Western markets in response to the challenging business environment. For example, from 2021 to 2022, Asian countries, especially members of the Regional Comprehensive Economic Partnership (RCEP), became relatively more important clothing export markets for China. Nevertheless, since RCEP members primarily consist of developing economies with ambitions to enhance their own clothing production, the long-term growth prospects for their import demand of ‘Made in China’ clothing remain uncertain.

Bangladesh achieved a new record high in its market share of world clothing exports, reaching 7.9 percent in 2022, which exceeded Vietnam’s 6.1 percent. Many fashion companies regard Bangladesh as a promising clothing-sourcing destination with growth potential because of its capability to make cotton garments as China’s alternatives, competitive price, and reduced social compliance risks.

Fashion companies’ efforts to “de-risking from China” also resulted in the robust growth of clothing exports from other large-scale Asian clothing producers in 2022, including Vietnam (up 13 percent), Cambodia (up 12 percent), and India (up 10 percent). In other words, despite the concerns about China, fashion companies still treat Asia as their primary sourcing destination.

Pattern #3: Developed countries stay critical textile exporters, and middle-income developing countries gradually build new textile production and export capability.

The European Union members and the United States stayed critical textile exporters, accounting for 25.1 percent of the world’s textile exports in 2022, up from 24.5 percent in 2021 and 23.2 percent in 2020. Thanks to the increasing demand from apparel producers in the Western Hemisphere, U.S. textile exports increased by 5 percent in 2022, the highest among the world’s top ten.

As a persistent long-term trend, middle-income developing countries have consistently been strengthening their textile production and export capability. For example, China, Vietnam, Turkey, and India’s market shares in the world’s textile exports have steadily risen. They collectively accounted for 56.8 percent of the world’s clothing exports in 2022, a notable increase from only 40 percent in 2010. Also, over time, these middle-income developing countries have achieved a more balanced textiles-to-clothing export ratio.

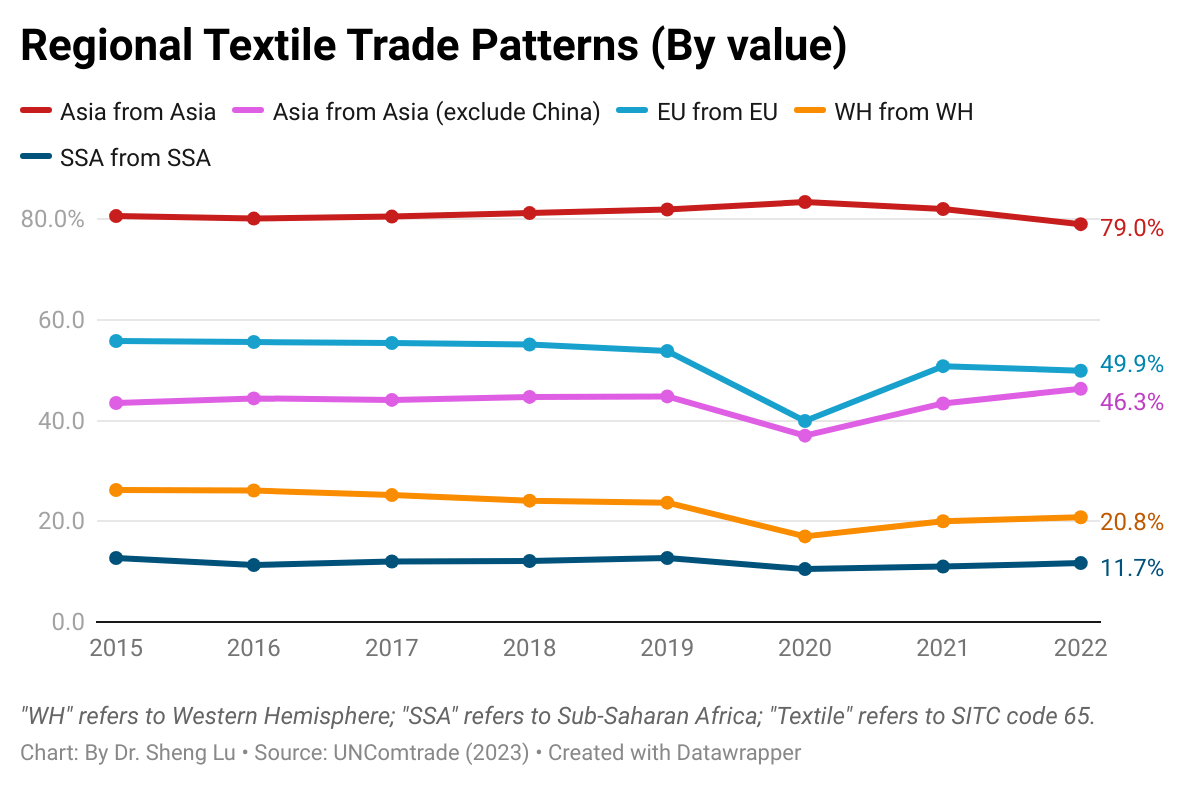

Pattern #4: Regional textile and apparel trade patterns strengthened further with the growing popularity of near-shoring, particularly in the Western Hemisphere. However, an early indication has emerged that Asian countries are diversifying their sources of textile raw materials away from China to mitigate growing risks.

The regional textile and apparel supply chains were in good shape in Asia and Europe. For example, nearly 80 percent of Asian countries’ textile input and apparel imports came from within the region in 2022. Likewise, approximately half of EU countries’ textile imports were intra-region trade in 2022, and one-third were for apparel.

The Western Hemisphere (WH) textile and apparel supply chain became more integrated in 2022 thanks to the booming near-shoring trends. For example, 20.8 percent of WH countries’ textile imports came from within the region in 2022, up from 20.1 percent in the previous year. Likewise, about 15.1 percent of WH countries’ apparel imports came from within the region in 2022, higher than 14.7 percent in 2021 and 13.9 percent in 2022.

Compared with Asia and the EU, SSA clothing producers used much fewer locally-made textiles (i.e., stagnant at around 11% from 2011 to 2022), reflecting the region’s lack of textile manufacturing capability. A more comprehensive examination of strategies for bolstering the textile manufacturing sector in Sub-Saharan Africa, particularly in light of the recently enacted African Continental Free Trade Area (AfCFTA) agreement, might be warranted.

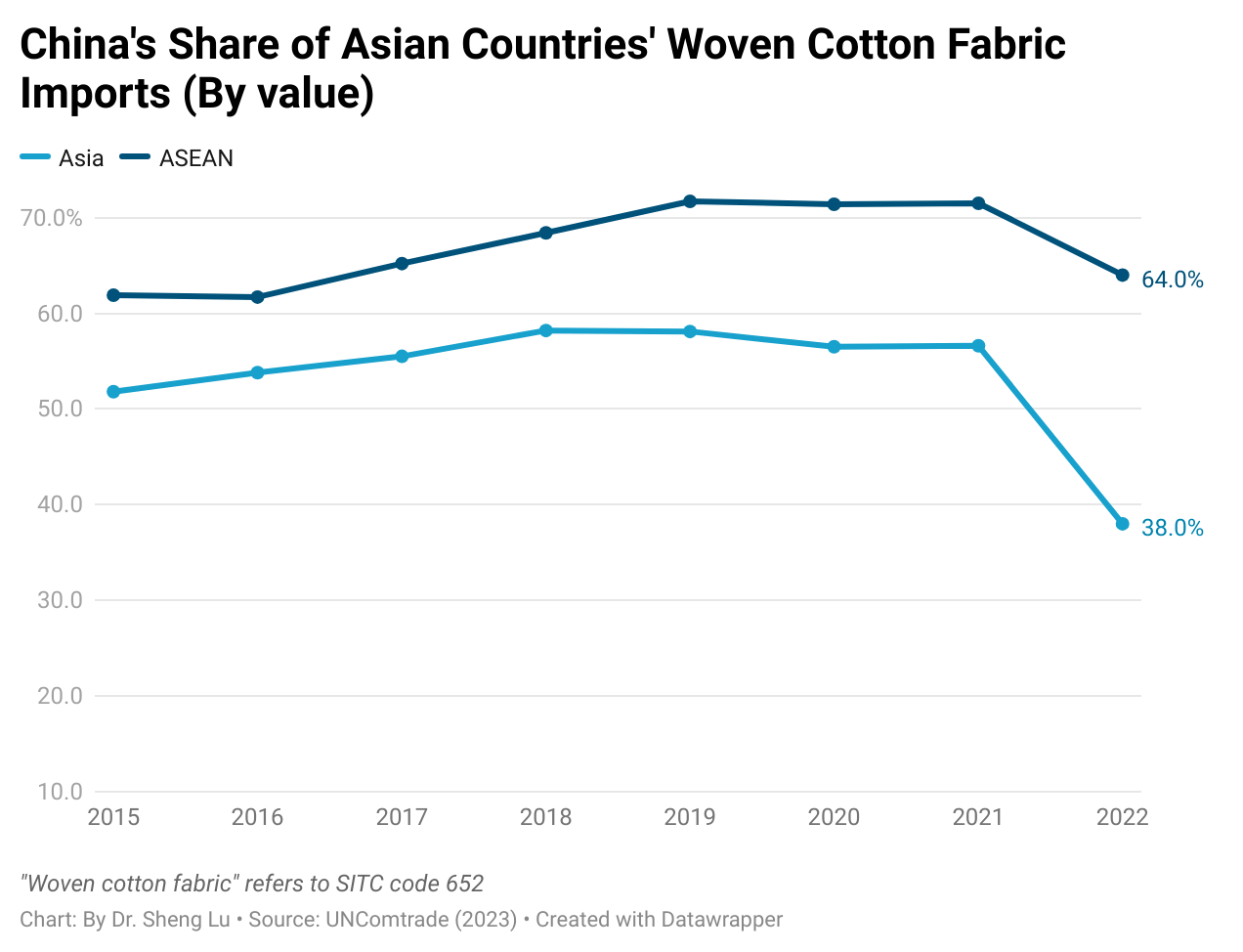

Additionally, data suggests that Asian countries began diversifying their textile imports away from China to mitigate supply chain risks. For example, with the official implementation of anti-forced labor legislation in the US and other primary apparel import markets directly targeting cotton made in China’s Xinjiang region, Asian countries significantly reduced their cotton fabric imports (SITC code 652) from China in 2022. Instead, Asian countries other than China accounted for 46.3 percent of the region’s textile supply in 2022, up from around 42-43 percent between 2019 and 2021.

It is critical to watch how willing, to what extent, and how quickly Asian countries can effectively reduce their dependency on textile supplies from China. The result is also an important reminder that Western fashion companies’ de-risking from China could exert significant and broad impacts across the entire supply chain beyond finished goods.