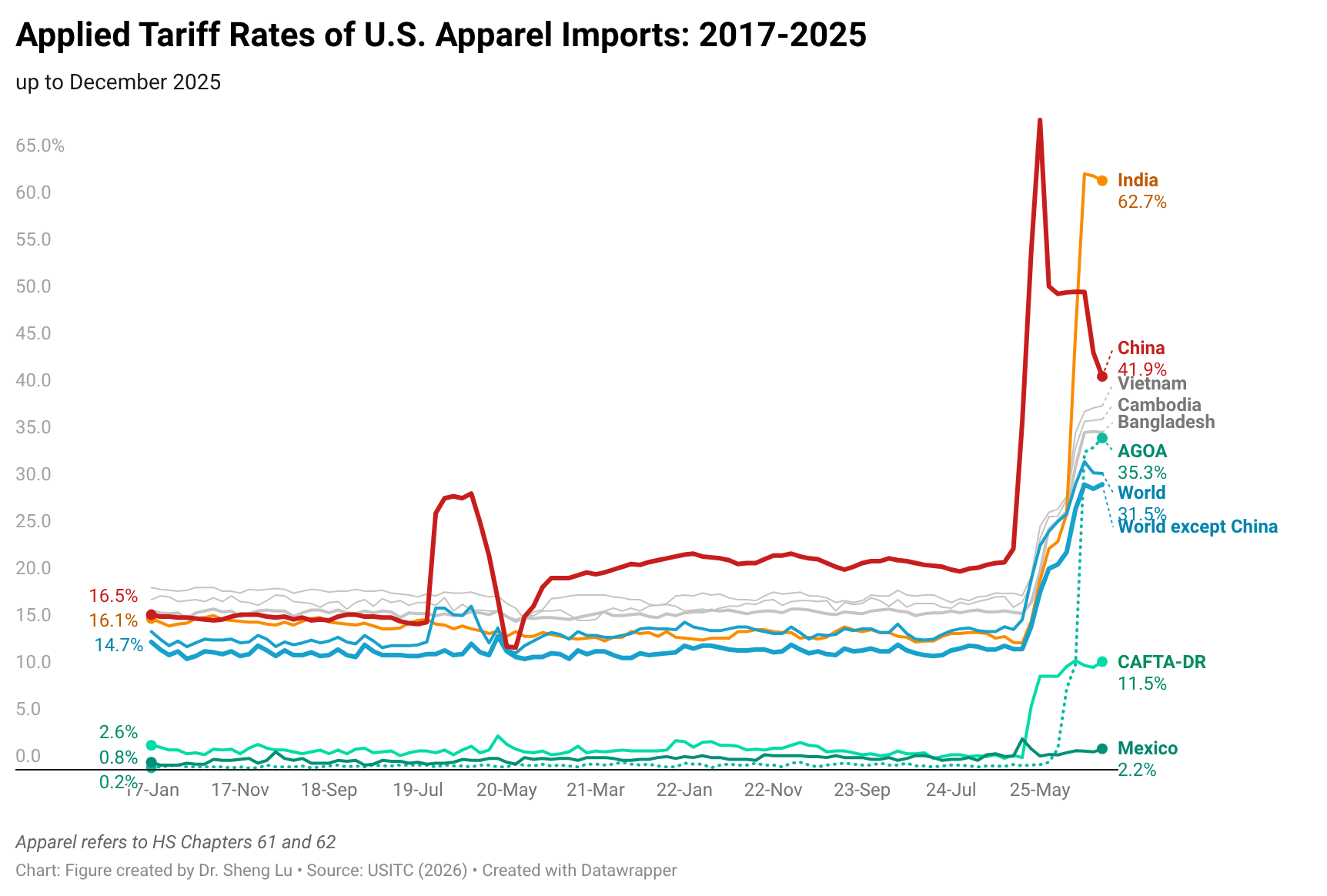

The average tariff rate for U.S. apparel imports (HS Chapters 61 and 62) reached 35.1% in December 2025, hitting a new high in decades and a sharp rise from 14.7% in January 2025, before President Trump’s second term. According to statistics from the Office of Textiles and Apparel (OTEXA), the U.S. International Trade Commission (USITC), and other government agencies, the hiking of tariffs and associated policy uncertainty has affected U.S. apparel sourcing and trade in multiple ways. [click here for detailed tariff data]

Impacts on apparel import price

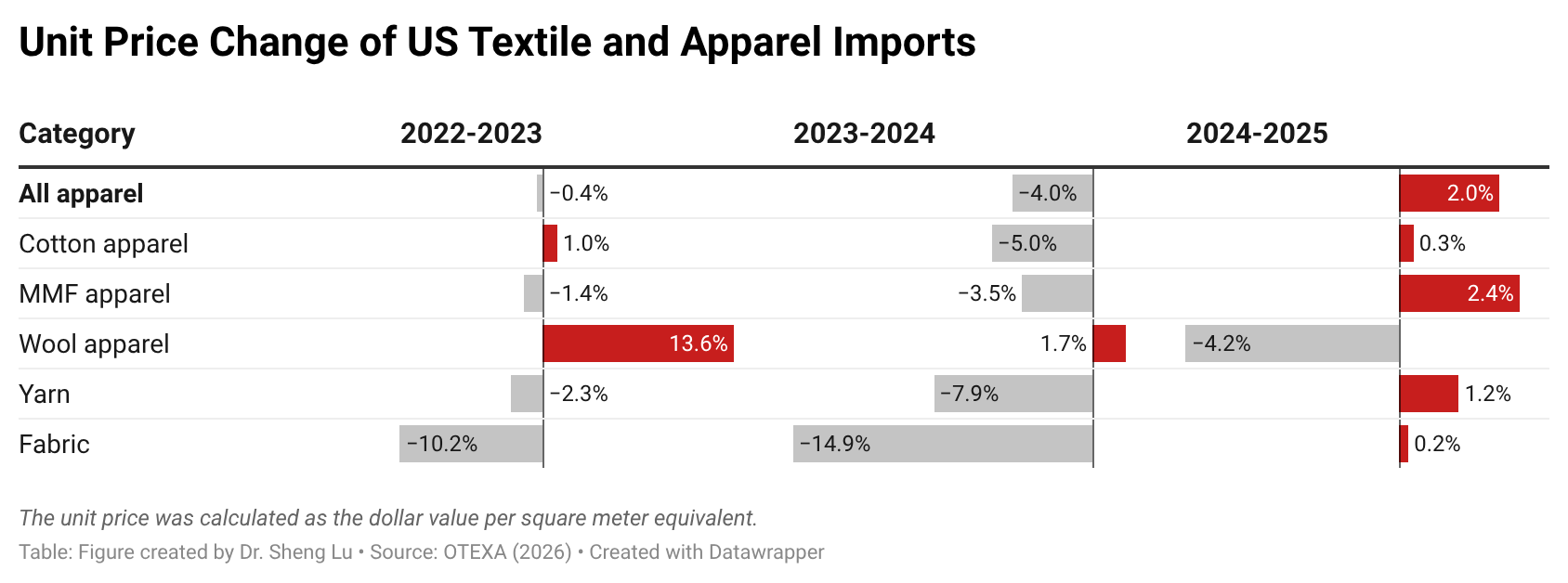

Apparel sourcing cost pressure increased in 2025, although price changes varied by fiber type. Data from OTEXA shows that, measured in dollars per square meter equivalent (SME), the unit price of US apparel imports increased from $3.08/SME in 2024 to $3.14/SME in 2025, a 2% year-over-year increase. Notably, due to an overall downward trend in world cotton prices, the unit price of US cotton apparel imports was almost flat in 2025, after a 5% decline in 2024.

In contrast, amid ongoing geopolitical tensions and rising oil prices, the unit price of US man-made fiber (MMF) apparel imports increased more noticeably by 2.4% in 2025. Still, in absolute terms, the unit price of US MMF apparel at $2.58/SME in 2025 was only about two-thirds of the price of cotton apparel at $3.59/SME.

Additionally, due to weaker demand for relatively more expensive clothing, the unit price of US wool apparel increased from $21.6/SME to only $20.68/SME, or down 4.2%.

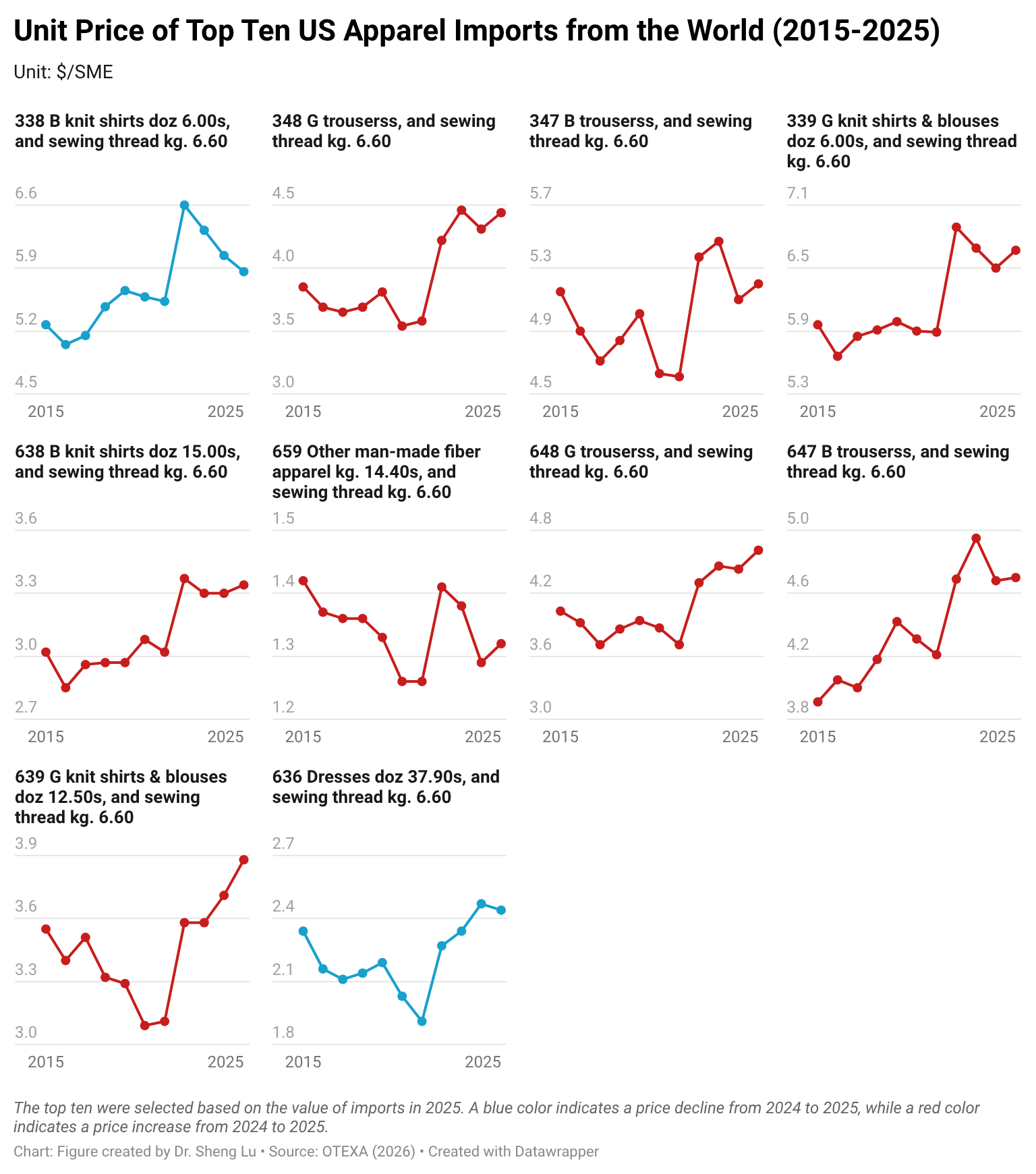

Amid higher tariffs, the unit import price for over half of the apparel import categories increased in 2025. Specifically, of the 106 apparel types categorized by OTEXA, 55 types (or 51.9%) saw a price increase between 2024 and 2025. This includes 22 categories (or 20.8%) with a price increase of more than 10 percent. Likewise, among the top ten largest apparel import categories by value in 2025, eight (80%) experienced price increases between 2024 and 2025, with an average increase of 2.5%. This result suggests that the upward price pressure was embedded in core, high-volume products rather than niche items. Particularly, as fashion companies navigate rising tariffs and policy uncertainty through more frequent adjustments to their original shipping schedules, it could increase their production and logistics costs more than usual. [Click here for detailed top ten U.S. apparel imports price data]

Impact on clothing retail price

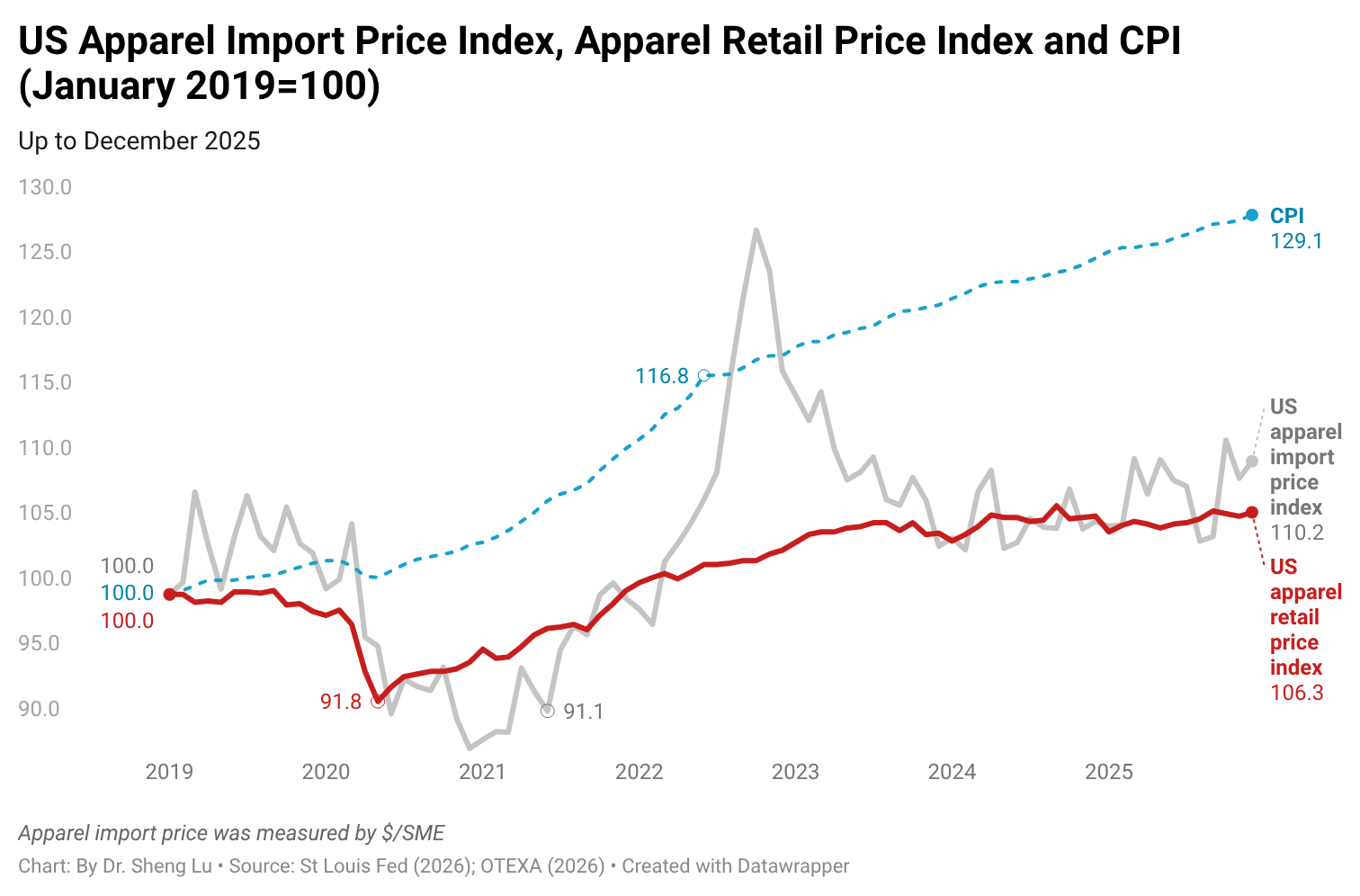

While the average U.S. apparel tariff rate rose from 14.7% in December 2024 to 31.5% in December 2025, the average U.S. clothing retail price increased only slightly by 0.3% during that time. This price rise was also much less than the 2.7% increase in the overall U.S. Consumer Price Index (CPI) during the same period. Since many apparel items are considered discretionary spending, higher inflation may lead consumers to reduce clothing purchases. [Click here for detailed U.S. apparel retail price index and CPI data]

Related, according to the Bureau of Economic Analysis (BEA), apparel accounted for 2.08% of U.S. consumers’ total personal spending in 2025, down from 2.10% in 2023 and 2.23% in 2021. As apparel retailers struggled to increase prices, younger generations, such as Gen Z, have turned to the secondhand clothing market.

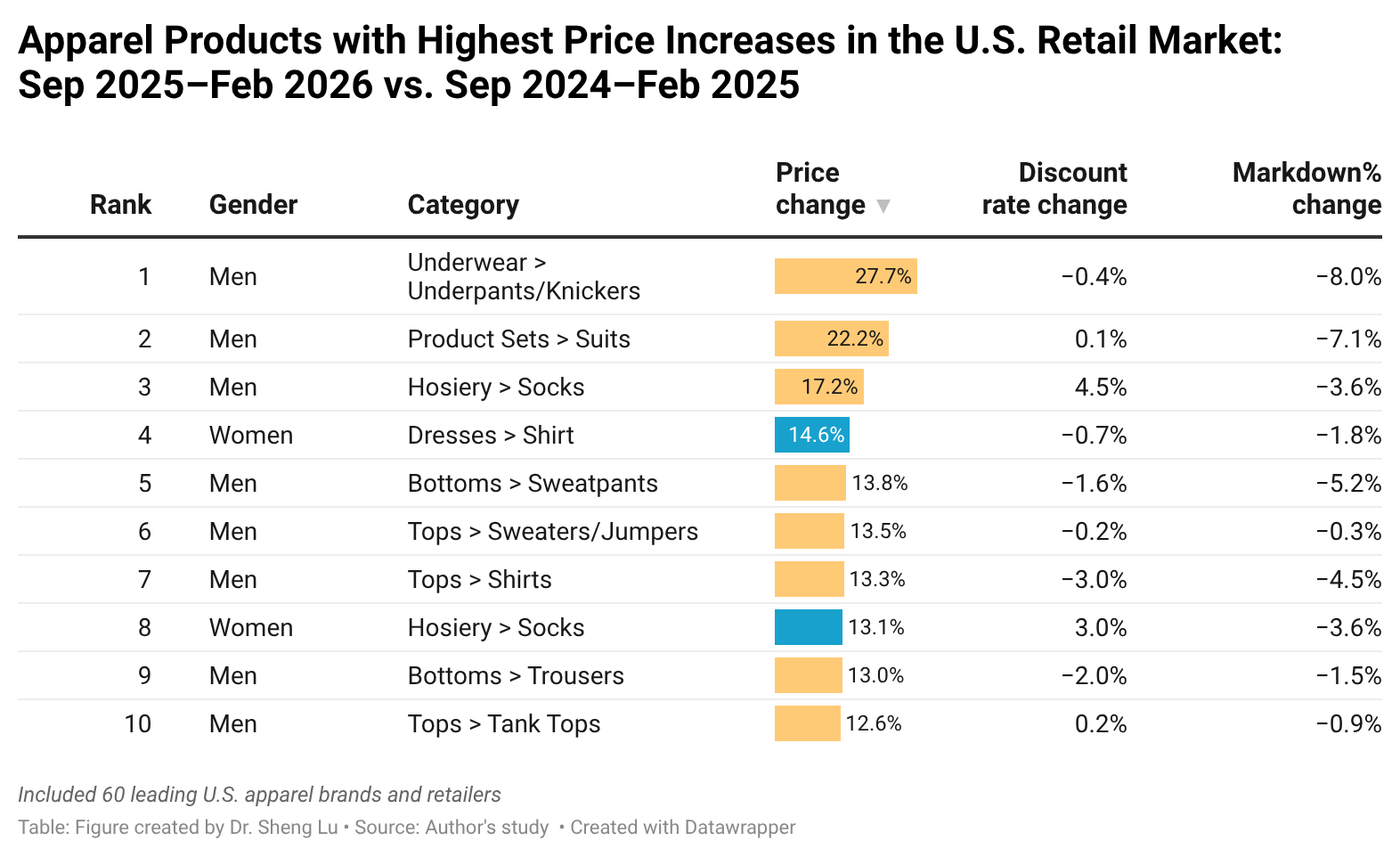

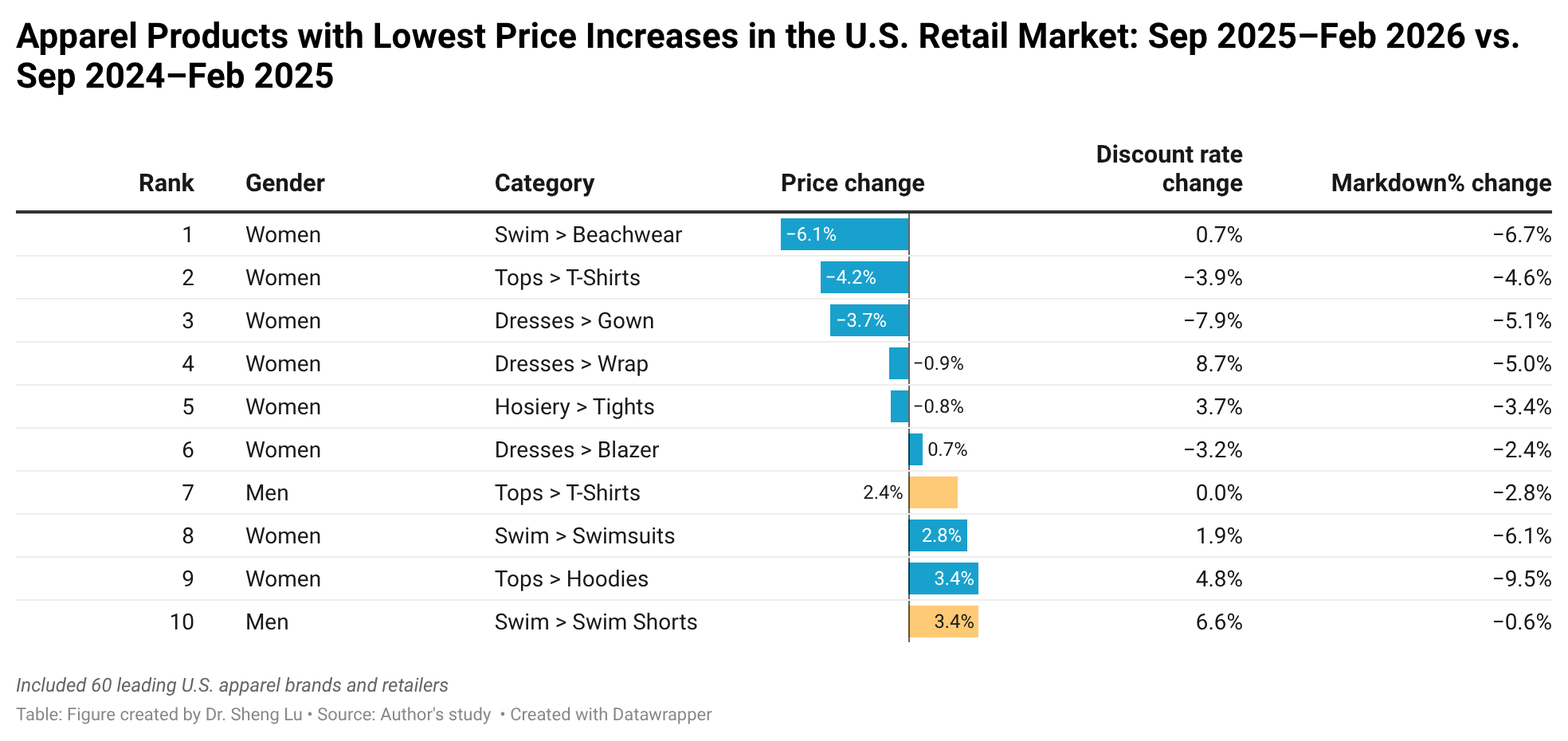

Additionally, data collected from industry sources show that the average retail price for necessities (e.g., men’s underwear) experienced the highest increase during September 2025 and February 2026 compared with the same period a year earlier (i.e., September 2024 and February 2025). In comparison, discretionary spending items such as women’s swimwear and dresses, as well as products with near-shoring opportunity (i.e., T-shirts), experienced the smallest increase over the same period.

Impact on fiber usage and sourcing base

The U.S. tariff rates not only vary by sourcing origin but also by fiber composition. Generally, apparel made with cotton fibers will face a lower tariff rate (i.e., around 8-16% Most-favored-Nation, MFN tariff rates) than apparel made only from man-made fibers (i.e., around 16-32% MFN tariff rates).

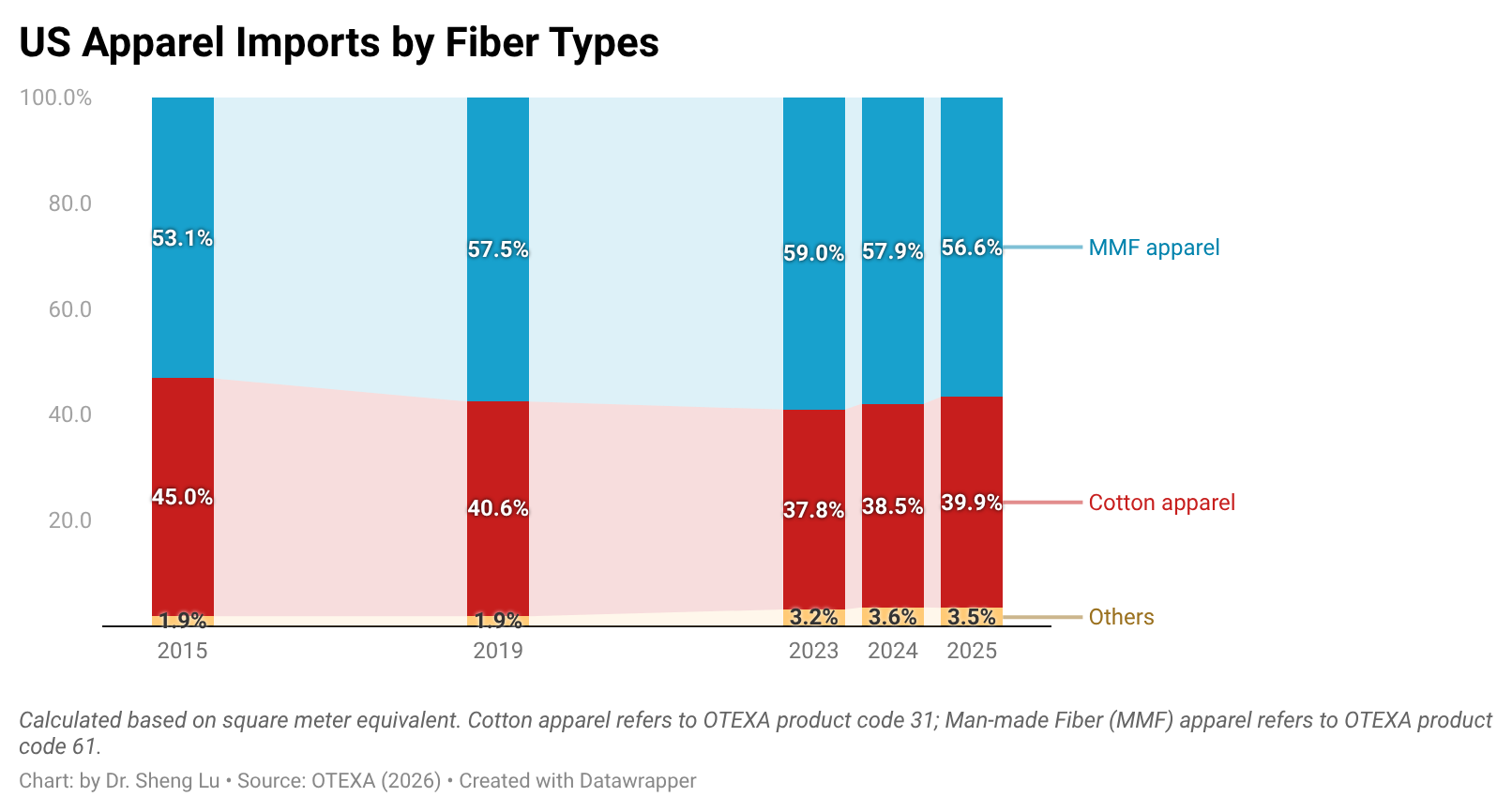

As U.S. fashion companies leverage “tariff engineering” to mitigate the import duty increase, U.S. apparel imports in 2025 included more cotton apparel and fewer of those made from man-made fiber (MMF). Specifically, measured by quantity, cotton apparel (OTEXA category 31) accounted for 39.9% of total US apparel imports in 2025, higher than 38.5% in 2024 and 37.8% in 2023. In comparison, man-made fiber (MMF) apparel accounted for 56.6% of total U.S. apparel imports in 2025, a noticeable decline from 57.9% in 2024 and 59% in 2023. [Click here for detailed U.S. apparel imports by fiber content data]

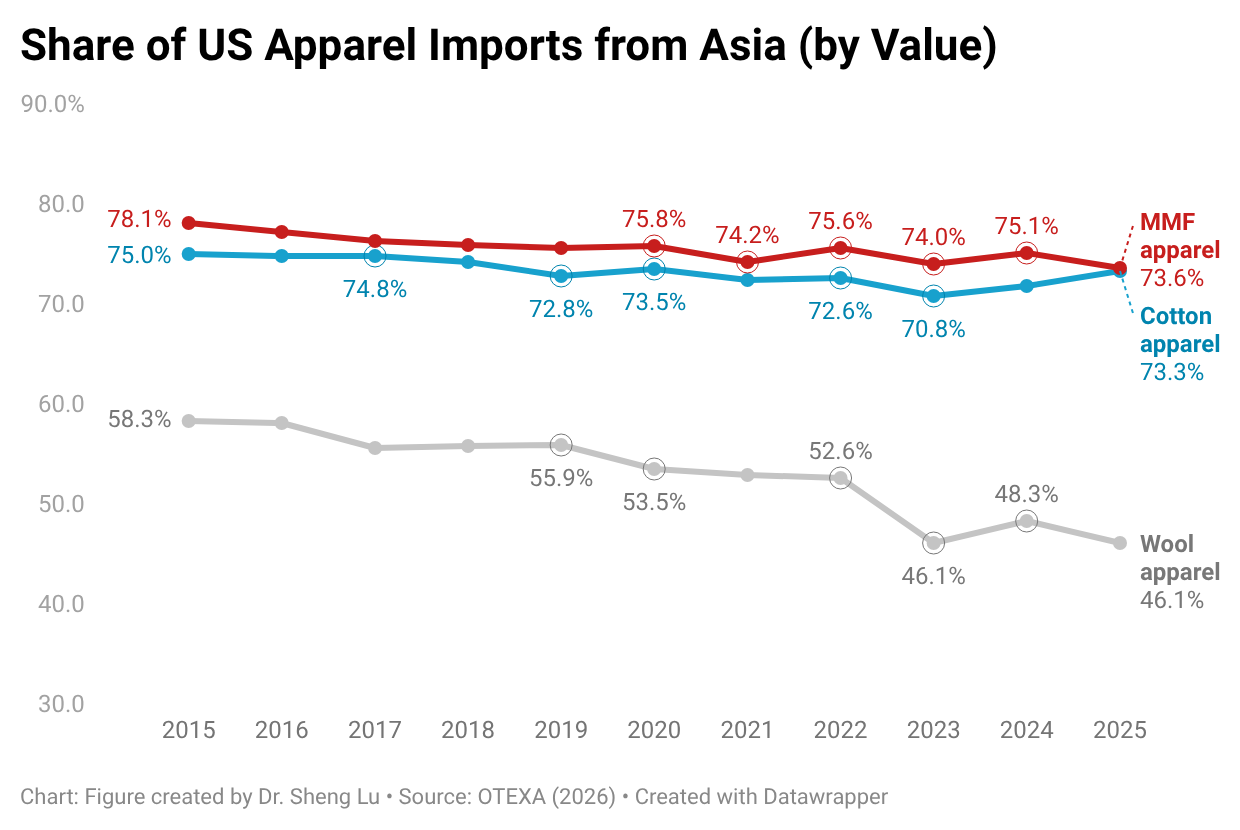

Furthermore, while Asian countries had demonstrated greater competitiveness in man-made fiber (MMF) clothing, higher tariffs on such products in 2025 led U.S. fashion companies to source fewer MMF clothing from Asia. Notably, in value terms, 73.6% of U.S. MMF clothing came from Asia in 2025, a noticeable decline from 75.1% a year earlier. In comparison, 73.1% of U.S. cotton apparel imports came from Asia in 2025, up from 71.8% in 2024. [Click here for Asia market share data]

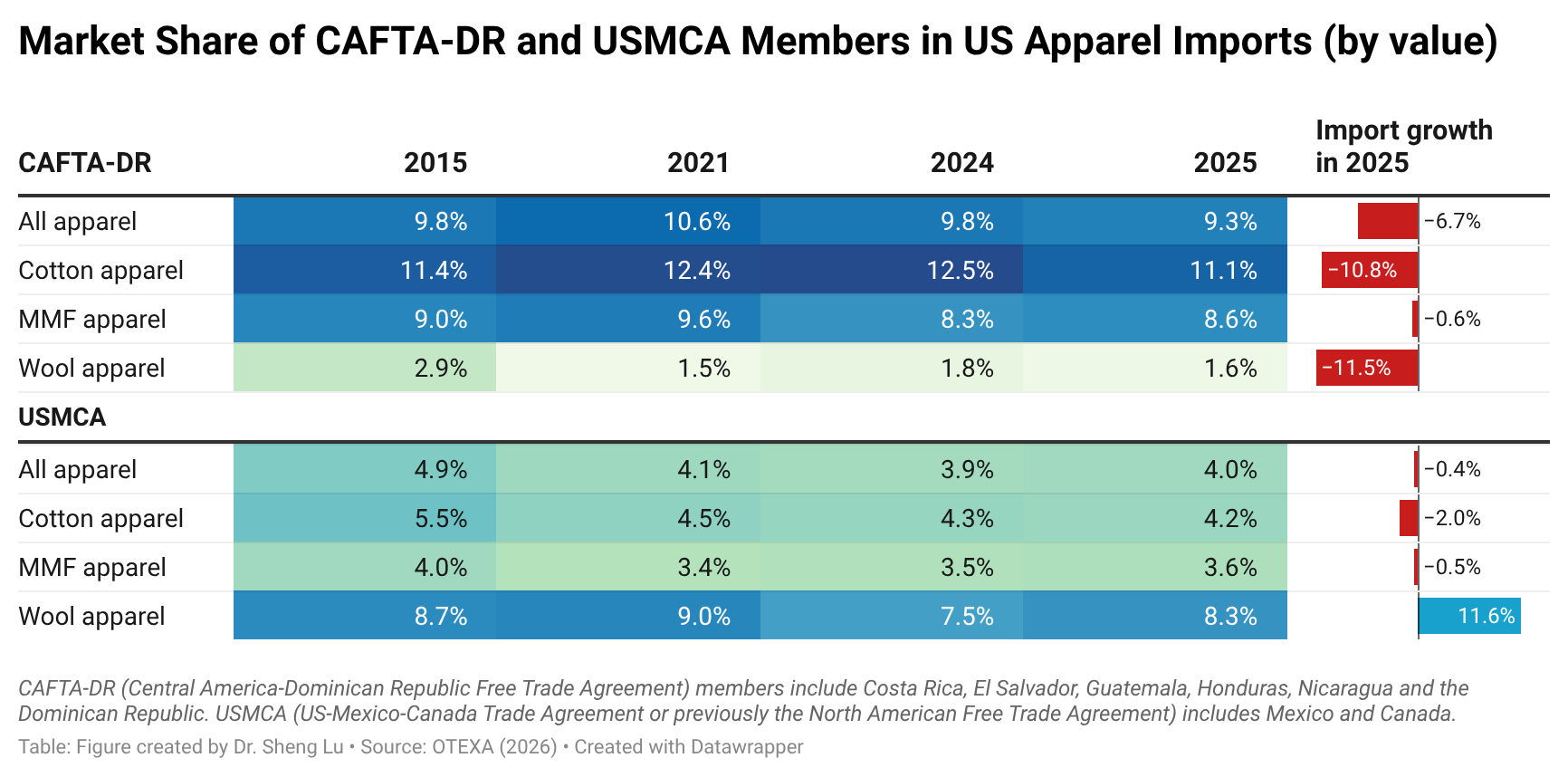

In comparison, it is interesting to note that while CAFTA-DR and USMCA members are perceived as more competitive in making and exporting cotton apparel products, due to tariff advantages, U.S. fashion companies import more man-made fiber (MMF) apparel from the regions in 2025. The same trend applied to wool apparel imports from the USMCA, which grew by 11.6%. These results suggest that if the tariff gap between U.S. apparel imports from CAFTA-DR and USMCA members and those from Asian countries continues in 2026, it may further incentivize U.S. fashion companies to explore additional MMF apparel sourcing opportunities in the Western Hemisphere. This incentive could be reinforced by the fact that, since February 2026, apparel imports from many Asian suppliers have been subject to the new Section 122 tariffs, while qualifying apparel products from CAFTA-DR and USMCA remain exempt. It may also represent a historic opportunity to expand investment in MMF textile manufacturing in CAFTA-DR and USMCA countries, thereby increasing regional production capacity and diversifying product offerings. [Click here for CAFTA-DR and USMCA market share data]

Impact on Free Trade Agreement utilization

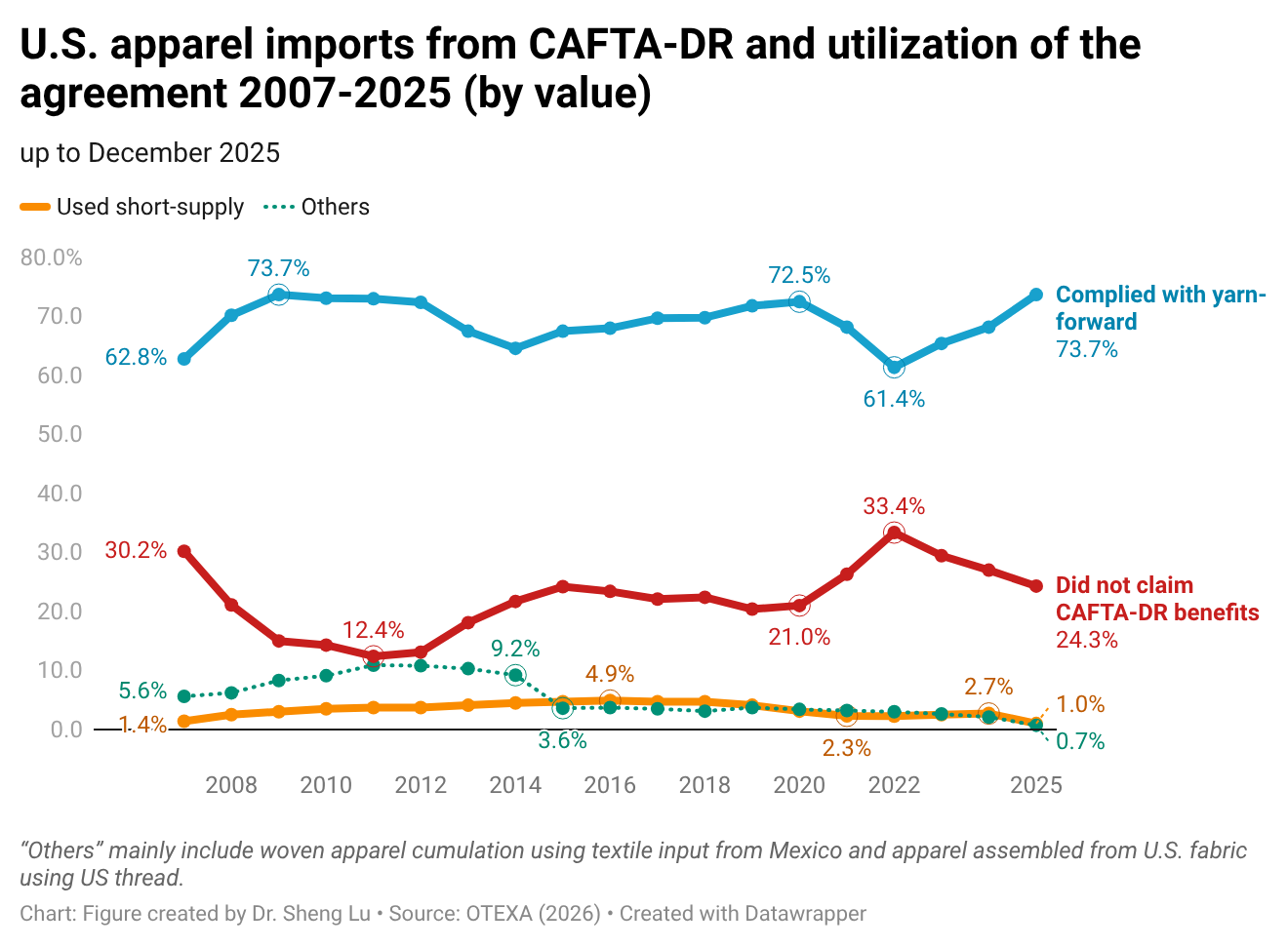

While there is no clear evidence from trade data showing that U.S. fashion companies expanded near-shoring from the Western Hemisphere in 2025, as a silver lining, the utilization of free trade agreements significantly improved. Specifically, measured in value, about 75.7% of U.S. apparel imports from members of the Dominican Republic-Central America Free Trade Agreement (CAFTA-DR) claimed duty-free benefits under the agreement, up from 73.0% in 2024 and 70.5% in 2023. Improved CAFTA-DR utilization in 2025 was driven by a higher volume of imports that met the yarn-forward rules of origin (i.e., up 1.5%). However, the utilization rate of the agreement’s short-supply mechanism decreased from 2.7% to 1.2%, despite more products being added to the list. [Click here for CAFTA-DR utilization data]

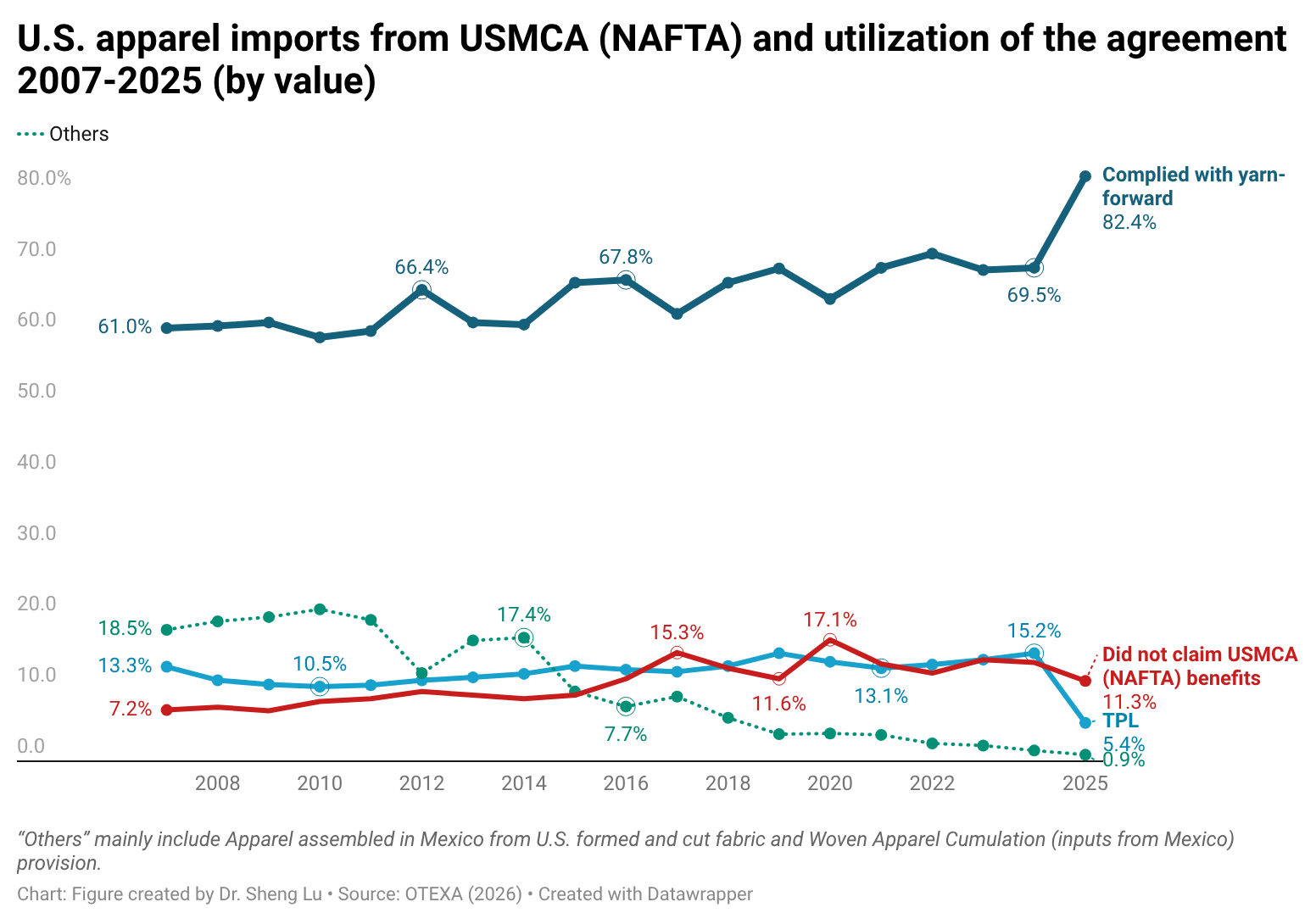

Similarly, in value, about 88.7% of U.S. apparel imports from Mexico and Canada claimed duty-free benefits under the U.S.-Mexico-Canada Agreement (USMCA), up from 86.1% in 2024 and 85.7% in 2023. Notably, in the past, only around 20% of U.S. apparel imports from Canada met the yarn-forward rules of origin; however, this percentage increased dramatically to 69.9% in 2025. Since March 2025, USMCA-qualifying products have been exempt from the “reciprocal tariffs” imposed by the Trump administration, which likely encouraged more U.S. apparel imports from Canada to take advantage of the rules. [Click here for USMCA utilization data]

By Sheng Lu

Read the full paper: Lu, Sheng (2026). US Apparel Import and Sourcing Patterns in 2025. Global Textile Academy, International Trade Centre (ITC). Geneva, Switzerland

An important concept we learned about in class was the lasting effect of tariffs and how they play into the overall global supply chains that apparel companies utilize. Increasing tariffs can negatively impact sourcing decisions, and oftentimes companies must regroup and source from other regions when this occurs. This is what the blog post touches on, as companies have chosen to adjust their sourcing regions rather than their retail prices when high tariffs were implemented. Sourcing in different regions can be beneficial, such as CAFTA-DR and USMCA, because it saves apparel brands money in production and does not require them to increase their retail prices to a point where their consumers are unhappy. This has increased the use of free trade agreements as well. Personally, I think diversifying where companies source is a good strategy. Although it may come with disadvantages such as higher costs and the potential of ethical issues, relying on one area to source from can be quite risky. Companies that were sourcing only from Asia when the high tariffs were imposed were more negatively impacted than others and likely struggled to adjust quickly. This shows that flexibility within supply chains is becoming important in a way similar to cost, as companies need to be able to adapt at a fast turnaround and stay competitive in a rapidly changing market.

A key concept related to this that we discuss frequently in class is how tariffs themselves do not necessarily lead to more localized production. This is due to another concept we learned, factor proportion theory, the idea that countries have different advantages based on their individual situations. For example, the US has advantage in capital but not labor., which is why production stays mainly in lower cost countries that have advantage in labor, like Bangladesh. Tariffs as a means to localize production seems counterintuitive when you understand this theory, as they increase costs but do not change the existing limitations that countries face. Trade is more driven by availability of resources and country advantages rather than changes in policy, which is why tariffs alone cannot shift apparel production back to the US.

One key concept from class that relates to this is factor proportion theory, which explains that countries specialize in production based on their advantages in labor and capital. For example, the U.S. has more of an advantage in capital, while countries like Bangladesh have cheaper labor, which is why a lot of apparel production still happens there. Because of this, even when tariffs increase, production does not simply move back to the U.S. since those underlying advantages do not really change. Another idea from class is how tariffs affect global supply chains. When tariffs increase, companies do not always raise prices, but instead look for other places to source from. This is what we see in the blog, where companies shift sourcing to regions like CAFTA-DR and USMCA to avoid higher costs and take advantage of trade agreements. This allows them to keep prices more stable for consumers instead of passing on all the extra costs. I think this also shows why diversifying sourcing is important. If companies rely too much on one region, like Asia, they are more affected when tariffs or policies change. At the same time, switching sourcing locations can create other issues, like higher costs or ethical concerns. Because of this, companies need to balance cost with flexibility so they can adjust quickly and stay competitive.

Two key concepts related to this article are supply chain management and overseas markets. This article specifically talks about the current high tariffs that the U.S. has put in place and how they are impacting the exports specifically in the fashion industry. This has disrupted the supply chain as there are significant taxes being added to the clothing being brought into the U.S. The article states that the tariff rate has risen from 14.7% to 31.5% in a year, but the average U.S. garment retail price has only increased by 0.3%. I found it interesting that there were higher tariffs on man made fibers in 2025 causing U.S. fashion companies to source less man made fiber clothing from Asia. I’m wondering why there has been less of an increase in retail price when there is such a high tariff increase. In the article it says that there has been less of a demand for higher priced clothing and all clothing is rising in price because of these new policies and the constant changing. Is it because companies know consumers won’t buy these higher priced items? If so, what are companies doing to make their money back with the loss of profit from the tariffs?