The full interview, conducted by Modaes’ Editor-in-Chief, Iria P. Gestal, is available HERE (in Spanish). Below is an abridged translation.

Question: Fashion brands have reduced their exposure to China markedly in recent years. What has been the turning point?

Sheng: We could interpret fashion companies’ decisions in the context of their overall sourcing diversification strategy. Many companies want to diversify their sourcing base because of the ever-uncertain business environment, ranging from the continuation of the supply chain disruptions, and the Russia-Ukraine war, to the rising geopolitical tensions. As China is one of the largest sourcing bases for many fashion companies, reducing “China exposure” is unavoidable.

Question: Isn’t there a specific concern about sourcing from China?

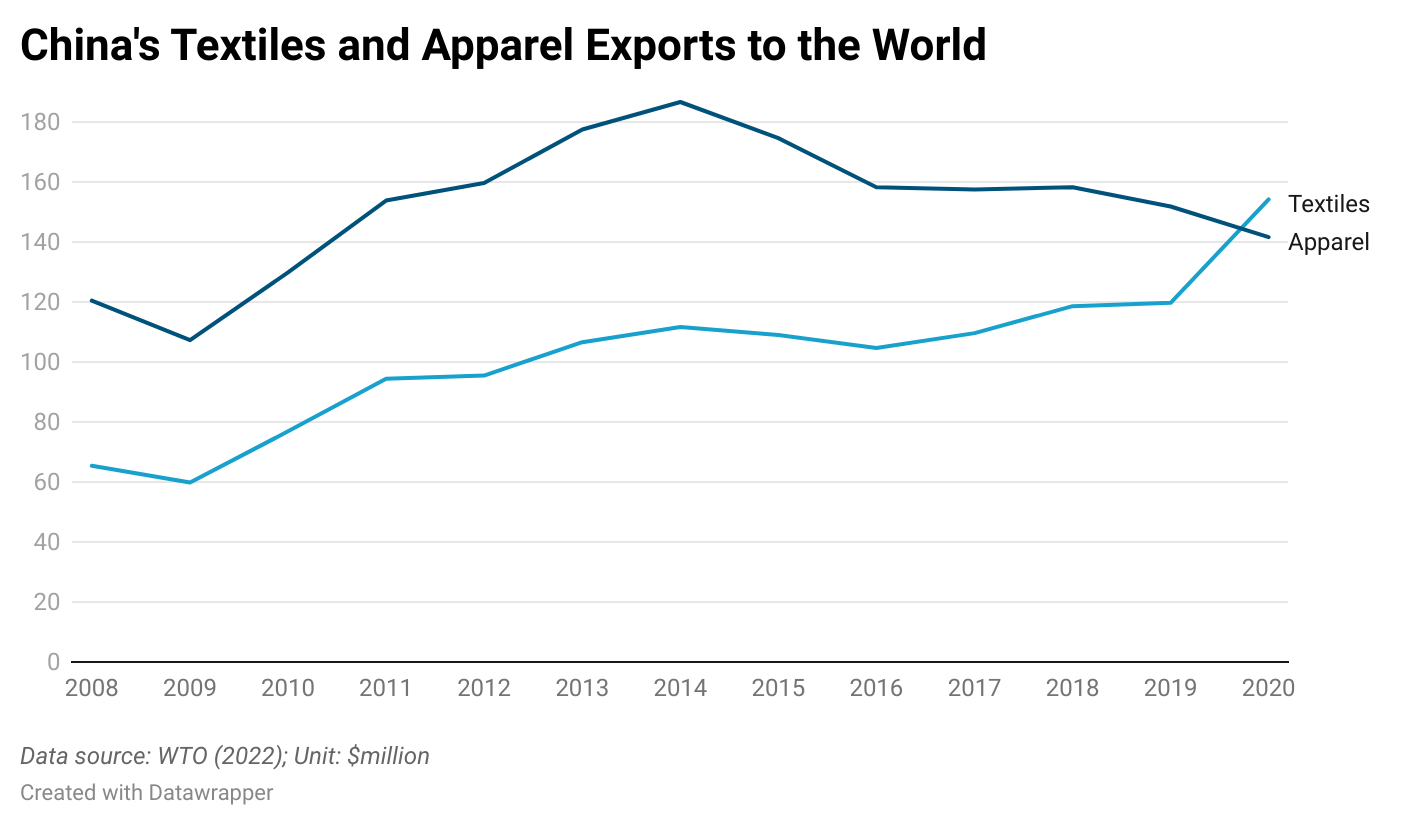

Sheng: Definitely! The Uyghur Forced Labor Prevention Act (UFLPA), officially implemented in the summer of 2022, is a big deal. For example, back in 2017, around 30% of US cotton apparel came from China. However, because of the new law and concerns about the risk of forced labor, China’s market shares fell to only 10% as of August 2022. One well-known US brand selling jean products cut their sourcing from China to just 1% of the total.

Question: Is it possible that the apparel sector as a whole reaches that point?

Sheng: Whether we like it or not, it is still unlikely to get rid of China from the supply chain entirely in the short to medium terms. Notably, China continues to play a significant role as a supplier of raw textile materials, particularly for leading apparel-exporting countries in Asia like Vietnam, Bangladesh, and Cambodia. Diversifying textile raw materials sourcing will be a longer and more complicated process.

Question: Is the “China Plus One” strategy no longer enough?

Sheng: The “China Plus One” strategy does not necessarily mean companies only source from “two” countries. Instead, the phrase refers to companies’ sourcing diversification strategy, trying to avoid “putting all eggs in one basket.” However, neither is the case that fashion companies blindly source from more countries today. Notably, many companies attempt to leverage a stronger relationship with key vendors to mitigate sourcing risks and achieve more sourcing flexibility and agility. For example, fashion companies increasingly tend to work with the so-called “super vendors,” i.e., those with multiple country presence and vertical manufacturing capabilities.

Question: Some politicians have said that the war in Russia has been the “geopolitical awakening” of Europe. Has the same thing happened in fashion?

Sheng: Indeed! We say fashion is a “global sector” because companies “produce anywhere in the world and SELL anywhere in the world.” However, many fashion brands and retailers have had to leave Russia due to the war and geopolitics. The same could apply to China—for example, China’s zero-COVID policy has posed a dilemma for western fashion companies operating there—whether to stay or leave the country, which used to be regarded as one of the fastest-growing emerging consumer markets. Likewise, more and more fashion companies have chosen to develop “dual supply chains” in response to the geopolitical tensions between China and the West—“made in China for China” and “made elsewhere for the rest of the world/Western market.” However, we must admit that this is not an ideal way to optimize the global supply chain.

Question: Has the apparel sector been “naïve” until now, ignoring these risks?

Sheng: I do not think so. In fact, most fashion companies and their leaders closely watch world affairs. As I recall, some visionary companies started evaluating geopolitics’ supply chain implications last year. Indeed, a peaceful world with few trade barriers is an ideal business environment for fashion companies. Unfortunately, there are too many “black swans” to worry about these days. As another example, “friend-shoring,” meaning only trading with allies or “like-minded” countries, becomes increasingly popular today. This phenomenon is also the result of geopolitics. With the looming of a new cold war (or the winter is already here), fashion companies may need to use imagination and prepare for the “worst scenarios” to come.

Question: Is a textile and apparel supply without China a more expensive one?

Sheng: It depends on how to look at it. The most challenging part of “reducing China exposure” is the textile raw materials. But we could think outside the box. For example, my recent studies show that China is NOT the top supplier of clothing made from recycled textile materials. Instead, fashion companies are more likely to source such products locally from the US or EU, or Africa—like Jordan, Tunisia, and Morocco, because of the unique supply chain composition. In other words, sourcing more clothing made from recycled textile materials may help fashion companies achieve several long-awaited goals, such as diversifying sourcing base, expanding nearshoring, and reducing sourcing costs.

–END–