According to forecast made by the Euromonitor, China will exceed the United States and become the world’s largest apparel market by 2019. Specifically, annual apparel sales in China will reach $333,312 million in 2019, an increase of 25% from $267,246 million in 2014. In comparison, apparel sales in the United States is estimated to reach $267,360 million in 2019, which is only 3% higher than $260,050 million in 2014.

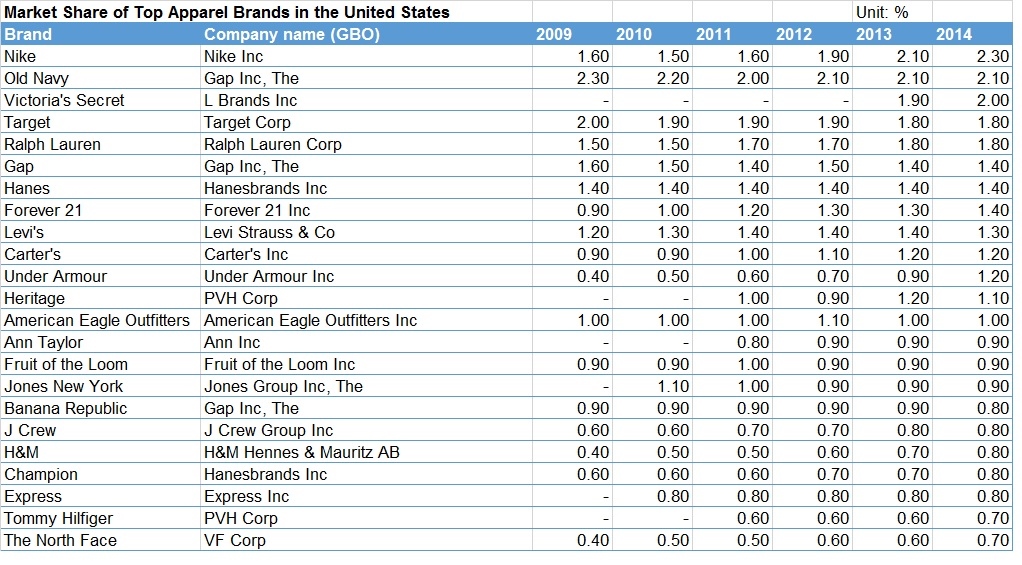

However, it shall be noted that China seems to be an even more competitive apparel market than the United States. For example, no apparel brand was able to achieve a market share more than 1% in 2014 in China, whereas in the United States, market shares of several leading apparel brands exceeded 2%. Moreover, domestic brands overall outperform international brands in the Chinese apparel market.

However, it shall be noted that China seems to be an even more competitive apparel market than the United States. For example, no apparel brand was able to achieve a market share more than 1% in 2014 in China, whereas in the United States, market shares of several leading apparel brands exceeded 2%. Moreover, domestic brands overall outperform international brands in the Chinese apparel market.

On the other hand, despite its overall market size, as a developing country, dollar spending on apparel per capita will remain much lower in China than many developed economies around the world. In 2014, each Chinese consumer on average spent $240 on apparel versus $815 in the United States, even though apparel spending accounted for a larger share in household income in China (around 10%) compared with the United States (less than 3%).

On the other hand, despite its overall market size, as a developing country, dollar spending on apparel per capita will remain much lower in China than many developed economies around the world. In 2014, each Chinese consumer on average spent $240 on apparel versus $815 in the United States, even though apparel spending accounted for a larger share in household income in China (around 10%) compared with the United States (less than 3%).

Several personal thoughts based on the data:

First, it is the time that U.S. apparel companies/fashion brands should start to seriously think about their sourcing strategy specifically for the Chinese market.

Second, for many Chinese apparel companies, serving the domestic market will help them more effectively achieve functional upgrading (i.e. shifting from low-value added manufacturing to higher-value added functions such as design, branding and distribution) than through exporting.

Third, controlling sourcing cost will be as important in China as in the United States. When China’s applied tariff rate is still as high as 9.63% for textiles and 16.05% for apparel (WTO, 2015), U.S. fashion companies/fashion brands may not have many options but to use “Made in China” to serve the Chinese consumers. In the long run, however, “Made in China” shall be gradually replaced by “Made in Asia”, especially when several free trade agreements (FTAs) involving China eventually take into effect (such as CEPA). However, China may strategically use rules of origin in these FTAs and encourage apparel manufacturers in the region to use Chinese made textile inputs (just like what U.S. did in NAFTA and CAFTA). Nevertheless, either for managing the apparel supply chain based on “Made in China” or “Made in Asia”, it doesn’t seem U.S. apparel companies/fashion brands will easily enjoy competitiveness over their Chinese competitors.

Data source: Euromonitor Passport(2015)