How to deal with China as a sourcing destination remains a tough and controversial issue facing U.S. apparel retailers and fashion brands in 2016. Although companies are of grave concerns about China’s continuous rising production cost (especially labor cost), few other lower-wage countries can beat China in terms of industry integration, supply chain efficiency, and reliability.This blog post intends to add to the discussion by taking a look at the supply side, i.e. what is happening in the China textile and apparel (T&A) industry.

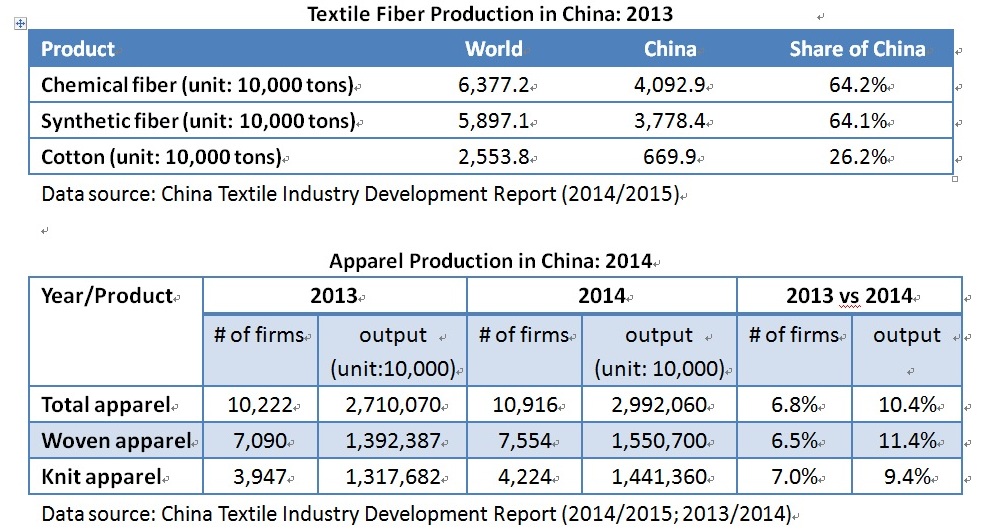

First, China’s production capacity remains unparalleled in the world. In 2014, the latest statistics available, textile fiber production in China exceeded 50 million tons, accounting for 54.36 percent of world share. By 2013, as much as 64.2 percent of the world’s chemical fibers, 64.1 percent of synthetic fibers and 26.2 percent of cotton were produced in China (see the table blew). On the other hand, apparel production in China reached 29.9 billion units in 2014, up 10.4 percent from 2013. Given China’s vast production capacity, very likely it will remain the top apparel sourcing destination for most EU and US fashion apparel companies for many years to come. For example, Vietnam’s apparel production in 2015 totaled 2.85 billion units, which was only around 10 percentage of China’s production scale in 2014.

Second, China’s T&A industry is growing slower. Specifically, output of China’s T&A industry (measured by value added) grew only 7.0 percent between 2013-2014, a significant drop from 10.3 percent between 2009-2010. Other major economic indicators in the industry, from sales revenue, net profit to investment, followed a similar pattern (see the figure below). Additionally, for the first time since the 2008 financial crisis, China’s T&A exports suffered a 3.9 percent decline in 2015 (-1.3% for textiles and -5.4% for apparel). Given the downward pressure on China’s economy and uncertainties in the world marketplace, such a slow-growth pattern is likely to continue in the years ahead.

Third, China’s T&A industry is undergoing important structural adjustment. Within the total industry output, the ratio of apparel, home textiles and industrial textiles has turned from 51:29:20 in 2010 to 46.8: 28.6: 24.6 in 2014, reflecting China’s efforts to move towards making more value-added and technology-intensive textile products. This ratio is expected to become 40:27:33 by the end of 2020 (i.e. the end of China’s 13th five-year plan). In order to overcome the pressure of rising labor and production cost, China’s T&A manufacturing base is gradually moving from the east coast to the western and central part of the country (accounting for 22.5 percent of China’s T&A production in 2014, up from 16.8 percent in 2010; this share may further increase to 28 percent by 2020). Additionally, T&A companies in China are encouraged to increase spending on research and development (R&D), which on average had accounted for 0.47 percent of T&A companies’ sales revenue in 2013, up from 0.43 percent in 2011.

Fourth, T&A companies in China are actively seeking business opportunities in the domestic retail market. Apparel retail sales in China reached 893.6 billion yuan in 2014 (around $137.5 billion), among which 30.77 percent were sold online (up from 14.54 percent in 2011). Apparel retail price on average rose 2.6 percent between 2013-2014, compared with 2.0 percent increase of China’s overall CPI over that period. However, it shall be noted that apparel retail sales in China’s tier 1 and tier 2 cities achieved almost zero growth in 2014, partially reflecting the negative impact of retail price increase on consumers’ demand. In comparison, apparel retail sales in China’s tier 3 & 4 cities as well as rural areas remain robust and strong. Additionally, financial performance of T&A companies in China is becoming more polarized. Companies that follow the traditional business model of manufacturing and exporting are facing their most difficult time since the 2008 financial crisis. However, there are also many success stories of apparel companies that focus on function upgrading, i.e. moving from simply “manufacturing” products to “serving” the market needs.

Sheng Lu

Recommended reading: China’s 13th five-year plan for its textile and apparel industry: Key numbers

Is there any thing that China can do to increase the growth rate of the T&A industry? Increasing this growth rather than decreasing it will really help China’s economy, so how can they go about fixing this?

I found this post to be very interesting. In another class I am taking, we discussed the many repercussions china seems to be facing due to its decreased annual GDP. As time progresses, China seems to be losing in the battle of cheap labor. Many companies are moving their labor out of China, to areas like Bangladesh and Vietnam, who are able to offer cheaper labor costs than China’s. Even Chinese companies are moving their own production from their own organic grounds to other international locations where the cost of manufacturing and textiles are less expensive. China has been a leader in this industry for the past few decades, and seems to be losing speed at a rapid pace. What can China’s textile and apparel industry do to regain its footing as the leader in this industry, before it is too late? How willing are companies that have outsourced their production to China be willing to give up the comfort of supply chain efficiency, regulation, and trustworthiness as well as relationships developed over time, in order to seek out cheaper labor costs?

really great comment! two quick follow-up comments: first, like the case in the US, T&A companies in China are also restructuring themselves, especially moving from low-end manufacturing to more value added functions. My personal observation is companies’ performance is getting more polarized: those transformed their business models can do really well and those rely on the old growth model are facing tremendous challenges. Second, I think Chinese T&A companies are embracing the concept of “supply chain” as well. the question is not what will happen to “made in China”. but what role China will play in “factory Asia”… welcome for any further thoughts!

Although China is facing some serious decline in growth in the T&A industry, I do not see this situation as entirely negative. While China is working on rebuilding its strength and lowering labor costs, apparel companies are looking to source their products elsewhere where they can keep margins low. This is a HUGE opportunity for less developed countries to step up to the plate. If these countries can keep wages low yet maintain good quality and quick lead time, it is likely they will bring in more and more business. This will not only help their economy but it will help the economy on a global scale. While I do hope China is able to restructure their T&A industry and see growth again, I am happy to watch other countries become big players in the industry as well so the market is not so much saturated by China.

agree!! Actually, there has been some studies exploring how China can become an apparel export market for least developed countries. For example, this is a research project I get involved: http://www.intracen.org/uploadedFiles/intracenorg/Content/Exporters/Sectors/Food_and_agri_business/Cotton/AssetPDF/China%20final%20technical%20document%20for%20print1.pdf

With the increasing, rapid rate of China’s T&A production, is it a concern that they could be developing faster than they can handle? If production costs in China increase, is it possible that other countries will look elsewhere? If so, what will happen to China’s T&A industry. As technology advances it will be interesting to see if China remains as the leader of the T&A. It will also be interesting to see how China’s rapid development effects its competitors and pushes them to develop as well!

It seems other less developed countries are very happy to see “Made in China” is becoming more expensive, such as Bangladesh. They are also encouraging Chinese factories to move there. Nevertheless, textile and apparel is a very dynamic industry. we have to keep an eye on those constant changes…

I think this article was very interesting as it took a look at why China is both still a world leader in the T&A industry but at the same time may be taking a few steps back. China is currently accounting more than 54% of the worlds textiles and fiber production but the industry is slowing a bit. The Chinese production definitely has not started to decrease but it has slowed quiet a bit. From 2009 to 2010 the output increase 10% but from 2013-2014 it was only a 7% increase. I think this has to do to the fact that China is slowly outgrowing the T&A industry much like the United States. They are trying to expand into much more technologically advanced production with higher skilled workers. This will increasingly help the economy as a whole but their T&A production will hurt from this. We also learned that China is having a little bit of a worker shortage compared to previously. There is not an as much of unskilled workers available to work for these factories. Because China is much more technologically advance and have more educated workers available in the country, they will follow the US in a lot of ways and start to have an advantage in more advanced production.

Great comment! One update: China’s textile and apparel exports declined in 2016, a very interesting but not too surprising signal: http://asia.nikkei.com/Business/Trends/China-textile-exports-fall-for-first-time-in-6-years

It’s interesting to read that although China remains as a manufacturing powerhouse that is has grown to be, their GDP is increasingly decreasing. I commend China for their efforts and all their initiatives to make their work force more respected and paid fairly. Their shift in focuses, however, seems that they are not content with just being a labor powerhouse. They are in essence “under construction” as they are trying out new developmental tactics to continue to be an important factor in the T&A industry. This structural shift China is going through is a time of risk and adaptation. There will always be a loss before a gain, that’s just how business functions. This is why I feel that although China has seen some decreasing rates and statistics recently, it is not all bad, The government needs to have proper surveillance over their annual GDP and effect on the economy, but as for the current market I believe that it is time for China to move on as they have started to. There are many other developing countries that can take China’s former work while China continues to advance.

agree. indeed! I assume the pattern of global t&A trade will be very different 10 years from now…

The article above explains the current status of China’s production industry. China is slowly going downhill in terms of stability within their manufacturing and production. One reason for this occurrence is because China’s production costs are increasing which is influencing companies to look elsewhere for sourcing and manufacturing. In addition, the industry has a very slow growth rate. From 2009-2010, China had a growth rate of 10.3%. From 2013-2014, China had a 7% growth rate. This statistic shows how China is slowly decreasing their growth annually. Also, traditional manufacturing companies are losing profits due to their manufacturing methods. I believe that China can improve their overall textile and apparel industry by investing in newer technology and adjusting their production processes to be more efficient. In doing so, these production plants could work towards increasing their growth and improving the economy as a whole.

good reading of these numbers!! Agree with your observation. China is indeed investing heavily in strengthening its research and development in the textile industry. the new battlefield could be the high-end industrial and technical textile market.

Do you see any relocation of Chinese textile and apparel manufacturing to Pakistan in context of expected better connectivity resulting out of under construction China- Pakistan Economic corridor?

I found this article very interesting. Do you think if China continues to raise production costs companies will look to other countries to manufacture those goods? Will smaller, less developed countries be able to generate the same quality and quick lead time as well as China? I am very interested to see what happens down the line.

That’s a good question. First, from my observation, China is following the same path as many developed countries: use robots to replace expensive workers: https://shenglufashion.wordpress.com/2015/11/29/the-future-of-made-in-china-robots-are-taking-over-chinas-factory-floors/ Second, Chinese textile and apparel factories are also actively seeking foreign investment opportunities. Very interesting, just recently, a Chinese apparel factory announced to open a new factory in the US: https://www.businessoffashion.com/articles/news-analysis/chinese-manufacturer-to-open-20-million-factory-in-us Third, I think your concerns are valid. It seems no other country can fully replace China, even not in the near future. However, it is also true that manufacturing is becoming more supply-chain based. Apparel imports from Asia probably will always contain Chinese elements and value created in China.