- What is the biggest hurdle to “speed to market”?

- What’s more important these days? Dollars or days?

- Is mass customization a nice to have or a need to have?

- How are companies fostering better partnerships with vendors?

- How much has your company been impacted by the “Trump effect”?

- Industry buzzwords: Amazon, sustainability, digitalization, transparency, on-demand manufacturing, data analytics.

- How well are companies executing on their data?

- 2017 is the year of _________? And What will 2018 be known for?

Month: December 2017

Tariff Remains a Critical Trade Barrier for the Textile and Apparel Sector (Updated December 2017)

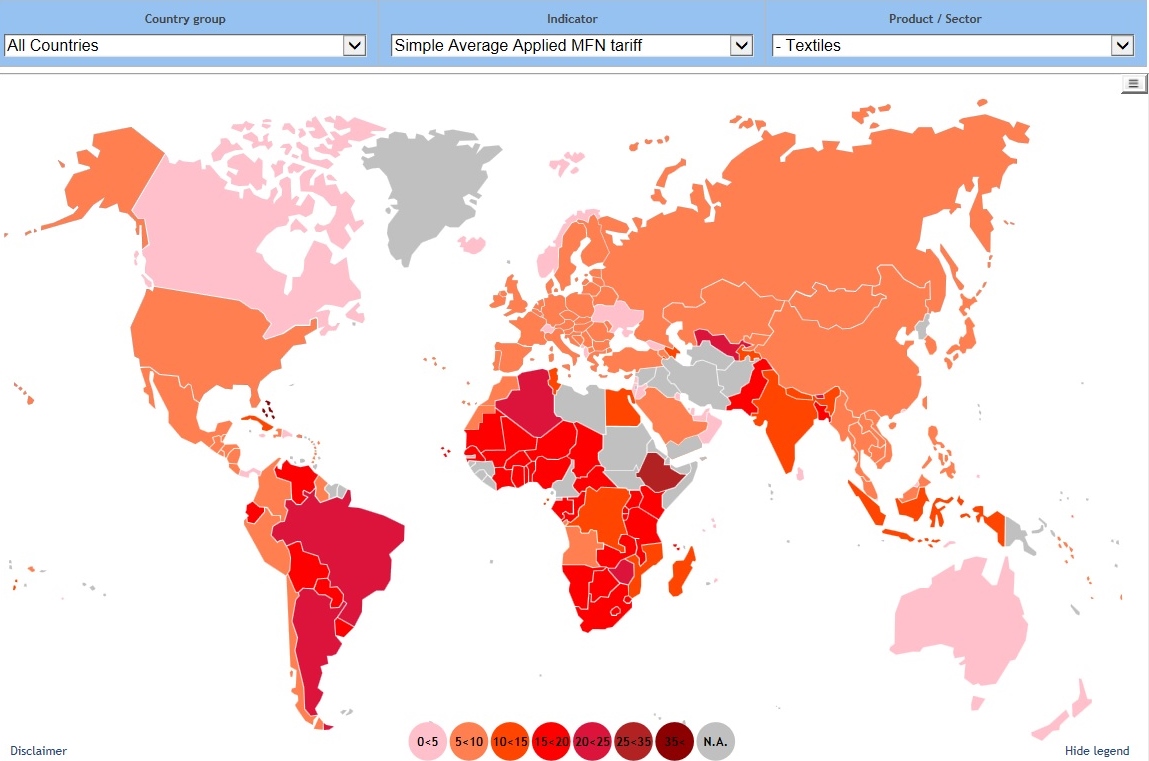

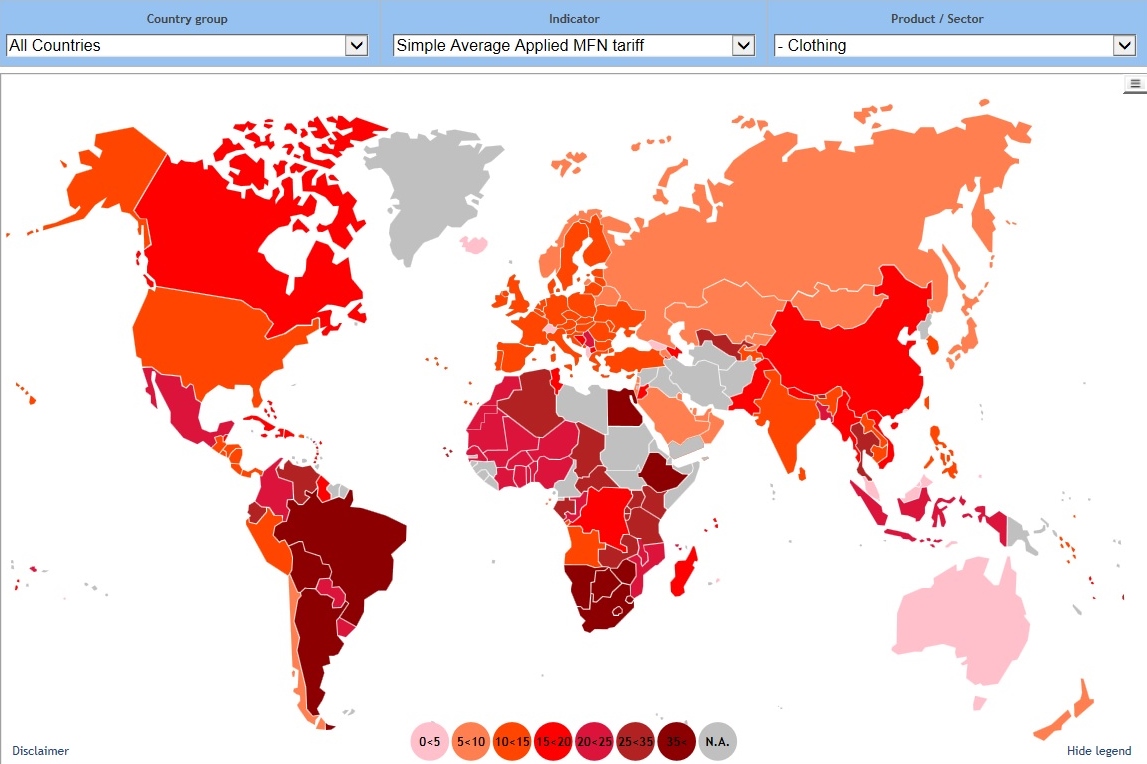

According to latest statistics from the World Trade Organization (WTO), in 2016, the average applied tariff rate remained at 10.5% for textiles and 17.5% for apparel worldwide. Compared with the average tariff rate for all sectors, the tariff rate for textile and apparel is 1.4 percentage points and 8.4 percentage points higher respectively. The result suggests that while tariff may no longer be a critical trade barrier for some sectors, it still significantly matters for the textile and apparel industry.

Least developed countries (LDC) overall set a higher tariff rate for textiles and apparel than other more advanced economies. For many poorest countries in the world, tariff remains the single largest source of tax revenue for the local government. However, it is also true that should these LDCs lower their tariff rate for textile inputs such as yarns and fabrics, it may help apparel manufacturers in these countries lower production cost and improve the price competitiveness of their finished apparel products in the world marketplace.

At the country level, countries with the highest tariff rate for textiles include Bahamas (37.1%), Ethiopia (28.0%), Uzbekistan (24.5%), Algeria (24.0%), Argentina (23.3%), and Brazil (23.3%). Whereas countries with the highest tariff rate for apparel include South Africa (41.0%), Namibia (41.0%), Swaziland (41.0%), Botswana (41.0%), Lesotho (41.0%), Bolivia (40.0%), Egypt (38.4%), Argentina (35.0%), Ethiopia (35.0%) and Brazil (35.0%).

Data also shows that the import tariff rates of the US, EU(28) and Japan, the top three largest textile and apparel importers in the world, stay unchanged over the past three years.

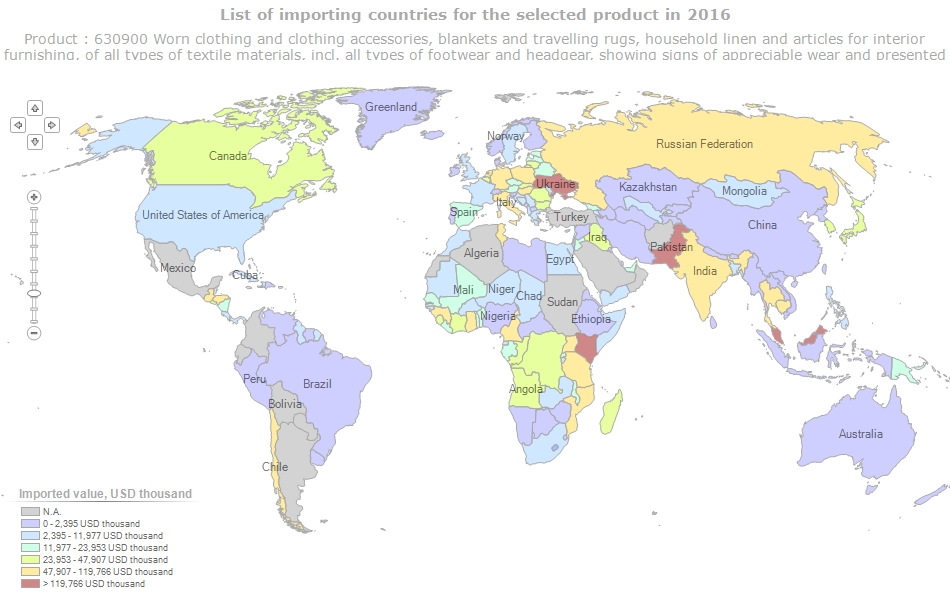

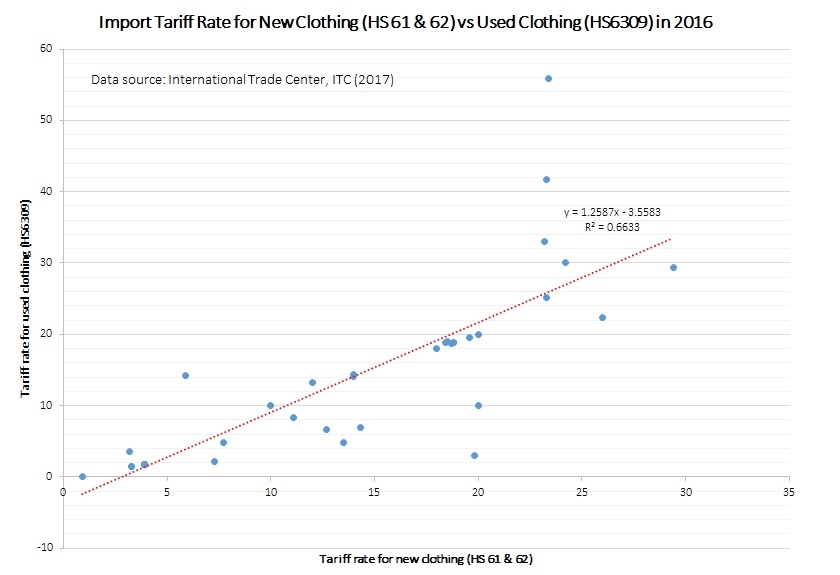

Additionally, there seems to be a positive relationship between a country’s import tariff rate for new clothing (HS 61 & 62) and used clothing (HS 6309). Of the total 180 countries covered by the International Trade Center (ITC) database, about 62.7% set an equal or higher tariff rate for new clothing than used clothing. Some African nations place a particularly high tariff rate for used clothing, including Zimbabwe (167%), South Africa (149%), Rwanda (117%), Namibia (80%), Tanzania (56%), and Uganda (41%).

Detailed tariff rates in Excel can be downloaded from HERE