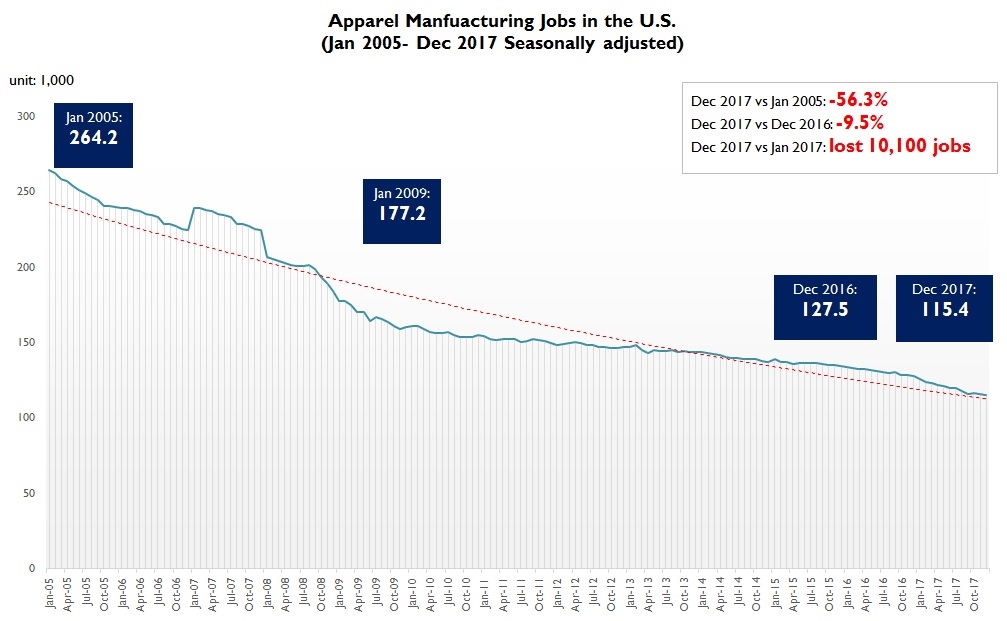

It may disappoint those who are hoping a return of textile and apparel manufacturing jobs in the United States. But according to latest statistics from the Bureau of Labor Statistics (BLS), the U.S. textile industry (NAICS 313 and 314) and apparel industry (NAICS 315) respectively lost another 4,100 and 10,100 jobs in 2017. Between January 2005 and December 2017, 44.2% and 56.3% of jobs in the U.S. textile and apparel sectors were gone.

From the academic perspective, a sizable return of textile and apparel manufacturing job in the United States seems to be extremely unlikely given the nature of the U.S. and the global economy in the 21st century.

Notably, the rising import is found NOT a significant factor leading to the decline in employment in the U.S. textile industry (NAICS 313). As estimated by a US International Trade Commission study in 2016, imports were found only contributed 0.4 percent of the total 7.6 percent annual employment decline in the U.S. textile industry between 1998 and 2014. Instead, more job losses in the sector were caused by: 1) the improved productivity as a result of capitalization and automation (around 4.6 percent annually); and (2) the shrinkage of domestic demand for the U.S. made textiles (around 3.5 percent annually).

And consistent with the prediction of classic trade theories, as capital and technology abundant developed country, the United States, not surprisingly, continues to lose its comparative advantage in making labor-intensive apparel. Hypothetically, apparel “Made in the USA” may come back if apparel manufacturing can be substantially automated like textile manufacturing. However, net job creation in the sector as a result of automation is hard to tell. Additionally, most U.S. apparel companies heavily rely on global sourcing and non-manufacturing activities such as branding, marketing, and design today. Few companies still regard “manufacturing” a key competitive advantage or an area of strategic importance to invest in the future.

Related reading: Creating High-Quality Jobs in the U.S. Textile and Apparel Industry (UD Biden Institute)