The full article is available HERE

Key findings:

First, mirroring the trend of aggregate market demand, the value of UK’s apparel imports has only grown marginally over the past decade. Specifically, between 2010 and 2018, the compound annual growth rate of UK’s apparel imports was close to zero, which was notably lower than 1.4% of the world average, the United States (1.9%), Japan (1.5%) and even the European Union as a whole (1.1%).

Second, UK’s fashion brands and retailers are gradually reducing imports from China and diversifying their sourcing base. Similar to other leading apparel import markets in the world, China was the largest apparel-sourcing destination for UK fashion companies, followed by Bangladesh, which enjoys duty-free access to the UK under EU’s Everything But Arms (EBA) program. Because of geographic proximity and the duty-free benefits under the Customs Union with the EU, Turkey was the third-largest apparel supplier to the UK.

Affected by a mix of factors ranging from the increasing cost pressures, intensified competition to serve the needs of speed-to-market better, the market shares of “Made in China” in the UK apparel import market had dropped significantly from its peak of 37.2% in 2010 to a record low of 21.4% in 2018. However, no single country has emerged to become the “next China” in the UK market. Notably, while China’s market shares decreased by 6.3 percentage points between 2015 and 2018, the next top 4 suppliers altogether were only able to gain 0.7 percentage points of additional market shares over the same period.

Third, despite Brexit, the trade and business ties between the UK and the rest of the EU for textile and apparel products are strengthening. Thanks to the regional supply chain, EU countries as a whole remain a critical source of apparel imports for UK fashion brands and apparel retailers. More than 33% of the UK’s apparel imports came from the EU region in 2018, a record high since 2010. On the other hand, the EU region also is the single largest export market for UK fashion companies.

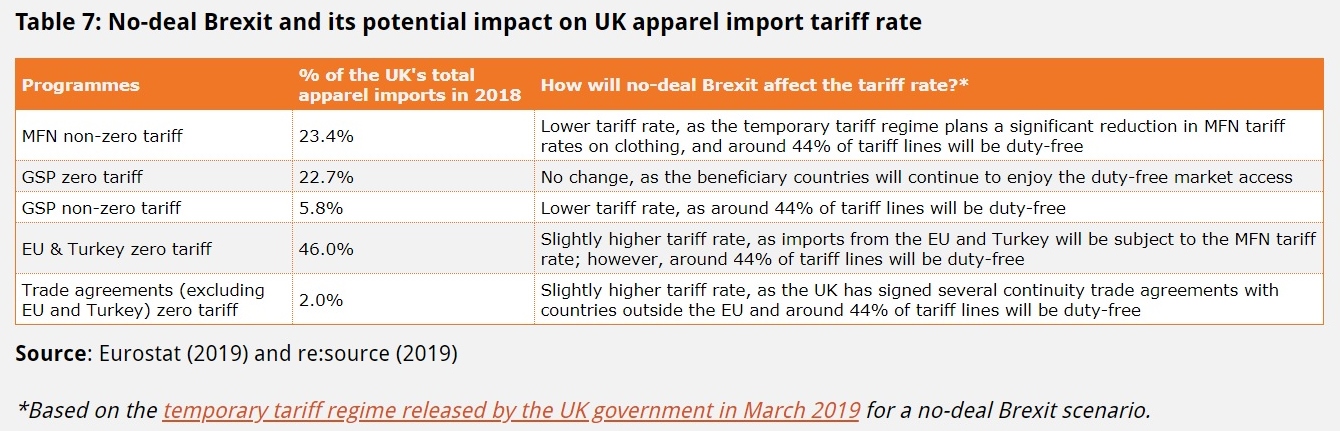

Fourth, the potential impacts of no-deal Brexit on UK fashion companies’ sourcing cost seem to be modest:

- For products currently sourced from countries without a free trade agreement with the EU (such as China) and those Generalized System of Preferences (GSP) beneficiaries that enjoy non-zero preferential duty rates, the tariff rate in the no-deal Brexit scenario will be lower than the current level, as round 44% of tariff lines will be duty-free.

- For products currently sourced from countries that enjoy duty-free benefits under the GSP program (such as EBA beneficiary countries), their duty-free market access to the UK will remain unchanged according to the temporary tariff regime.

- Products currently sourced from EU countries and Turkey will lose the duty-free benefits and be subject to the MFN tariff rate. However, because around 44% of tariff lines will be duty-free, the magnitude of tariff increase should be modest.

- Likewise, products currently sourced from countries that enjoy duty-free benefits under an EU free trade agreement could lose the duty-free treatment and be subject to the MFN tariff rate. However, as around 44% of tariff lines will be duty-free and the UK has signed several continuity trade agreements with some of these countries, the magnitude of tariff increase should be modest overall too. Additionally, these countries are minor sourcing bases for UK fashion companies.

About the authors: Victoria Langro is an Honors student at the University of Delaware; and Dr. Sheng Lu is an Associate Professor in Fashion and Apparel Studies at the University of Delaware.