It comes with no surprise that the fashion apparel industry has changed drastically in light of the novel coronavirus (COVID-19).

- According to the latest statistics released by the U.S. Census Bureau, hit by COVID-19, the value of U.S. clothing and clothing accessories sales went down by 50.5% in March 2020, compared with a year earlier.

- According to a recent NPR news report, in Bangladesh, the world’s second-largest garment exporter, about one million garment workers have lost their jobs as a direct result of sourcing changes. An online survey of Bangladesh employers, administered between March 21 and March 25, 2020, indicates that 72.4% of furloughed workers have been sent home without pay, and 80.4% of dismissed workers have not received severance pay.

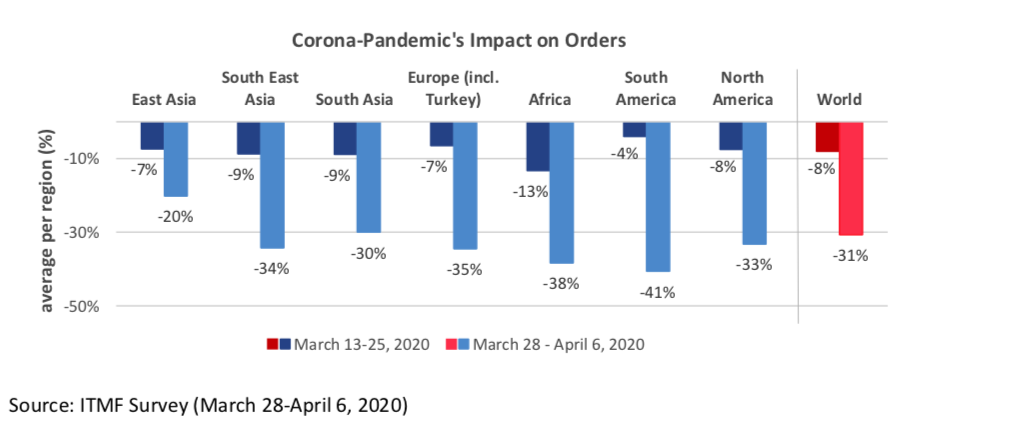

- A survey of 700 companies conducted by the International Textile Manufacturers Federation (ITMF) between 28 March and 6 April 2020 shows that companies in all regions of the world suffered significant numbers of cancellations and/or postponements of orders. Globally, current orders dropped by 31% on average. The severity of the decrease ranges from 20.0% in East Asia to 41% in South America.

- According to a newly created COVID-19 Tracker developed by the Worker Rights Consortium, it is concerning that many large-scale fashion brands and retailers are not paying their overseas manufacturers back for the materials the manufacturers have already paid for to start making garments.

Additionally, here is a list of well-known fashion brands that have announced to cut or cancel sourcing orders as of April 13, 2020:

- Primark has closed all its stores across Europe and the U.S. and asked all of its suppliers to stop production. However, the company has set up a fund to pay the wages of factory employees who worked on clothing orders that were canceled.

- Ross Stores has announced to cancel all merchandise orders through mid-June, 2020.

- Gap Inc. has decided to halt the shipments of their summer orders and the production of the fall products

- H&M has also canceled orders but told its suppliers it would honor the orders it already placed before the COVID-19.

Additional reading:

- COVID-19 and the textiles, clothing, leather and footwear industries (ILO, April 2020)

- Clothing makers in Asia give stark coronavirus warning (BBC news)

Compiled by Meera Kripalu (Honors student, Marketing and Fashion Merchandising double majors) and Dr. Sheng Lu

The discussion is closed for this post.