The global textile and apparel industry is becoming increasingly complex, shaped not only by conventional economic factors like production costs but also by trade policy, geopolitical uncertainty, and rapidly evolving sustainability regulations. While much of our course has focused on the U.S. market and the perspective of U.S. brands and retailers, it is equally important to understand how these forces are unfolding in other regions of the world, particularly in Europe.

The EU plays a distinctive role in the global textile and apparel system. It is one of the world’s largest apparel consumer markets, home to many leading luxury fashion brands, and a global leader in setting sustainability and regulatory standards for textiles and apparel. Therefore, developments in the EU have far-reaching implications for textile and apparel production, sourcing, and trade patterns worldwide.

We are fortunate to have Dirk Vantyghem, Director General of the European Apparel and Textile Confederation (EURATEX), join us for this interview. Dirk shared valuable insights into how the EU textile and apparel industry is navigating this rapidly changing landscape, including:

The current state of the EU textile and apparel industry, its competitive strengths in innovation, sustainability, and high-end design, and the challenges posed by rising costs and shifting consumer demand

Key sourcing and supply chain trends among EU fashion brands, including diversification, increased transparency, and nearshoring to neighboring regions

The impacts of rising trade tensions and geopolitical uncertainty on EU textile and apparel companies, and how these factors affect business strategies and consumer confidence

The EU textile and apparel industry’s approach to trade policy, balancing open markets with “fair trade” through stronger sustainability and compliance requirements, and expanding trade partnerships globally

The industry response and practical implications of the EU Strategy for Sustainable and Circular Textiles, launched in 2022, and the prospects and opportunities of textile-to-textile recycling in Europe

Potential areas for stronger U.S.-EU cooperation on textile and apparel trade, supply chains, and sustainability standards

About Dirk Vantyghem

Dirk Vantyghem is the Director General of the European Apparel and Textile Confederation (EURATEX), representing the interests of the European textile and apparel companies. Appointed in 2019, he leads the organization’s engagement with European institutions, focusing on promoting a competitive, innovative, and sustainable textile and apparel industry. Mr. Vantyghem brings over 20 years of experience in European business representation and policy advocacy, having previously served as a director at the European Chambers of Commerce and Industry (EUROCHAMBRES) in Brussels. He has extensive expertise in international trade, SME development, EU programs, and economic diplomacy, and holds a master’s degree in economics from the College of Europe.

AboutEmilie Delaye (moderator)

Emilie Delaye is a master’s student & graduate instructor in Fashion and Apparel Studies at the University of Delaware, with a specific interest in supply chain, global sourcing, and sustainability. Emilie is also a member of the Fair Labor Association (FLA) 2025-2026 Student Committee and the University of Delaware President’s Student Advisory Council.

The EU region as a whole remains one of the world’s leading producers of textile and apparel (T&A). The value of EU’s T&A production totaled EUR137.3 bn in 2019, down around 2% from a year ago (Note: Statistical Classification of Economic Activities or NACE, sectors C13, and C14). The value of EU’s T&A output was divided almost equally between textile manufacturing (EUR68.7bn) and apparel manufacturing (EUR68.6bn).

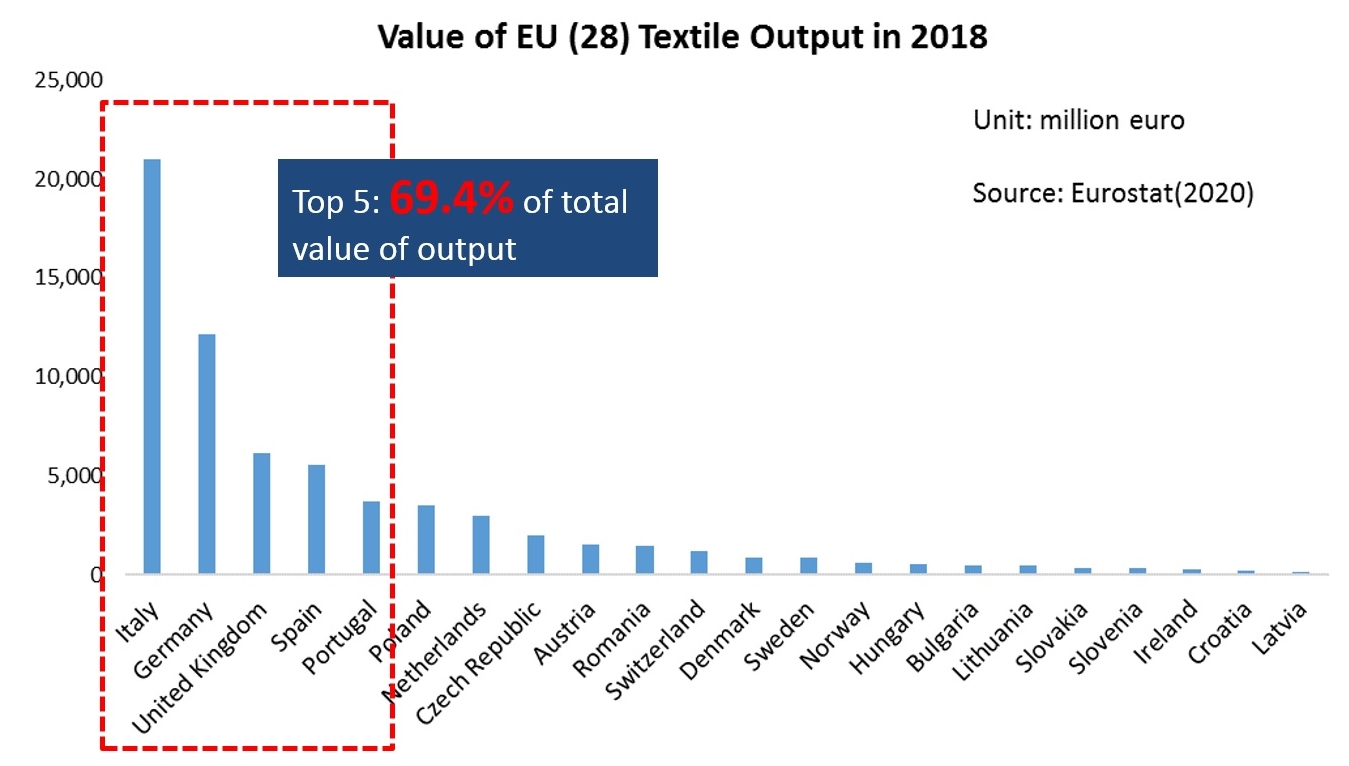

Regarding textile production, Southern and Western EU, where most developed EU members are located such as Germany, France, and Italy, accounted for nearly 75% of EU’s textile manufacturing in 2019. Further, of EU countries’ total textile output, the share of non-woven and other technical textile products (NACE sectors C1395 and C1396) has increased from 19.2% in 2011 to 23.0% in 2017, which reflects the on-going structural change of the sector.

Apparel manufacturing in the EU includes two primary categories: one is the medium-priced products for consumption in the mass market, which are produced primarily by developing countries in Eastern and Southern Europe, such as Poland, Hungary, and Romania, where cheap labor is relatively abundant. The other category is the high-end luxury apparel produced by developed Western EU countries, such as Italy, UK, France, and Germany.

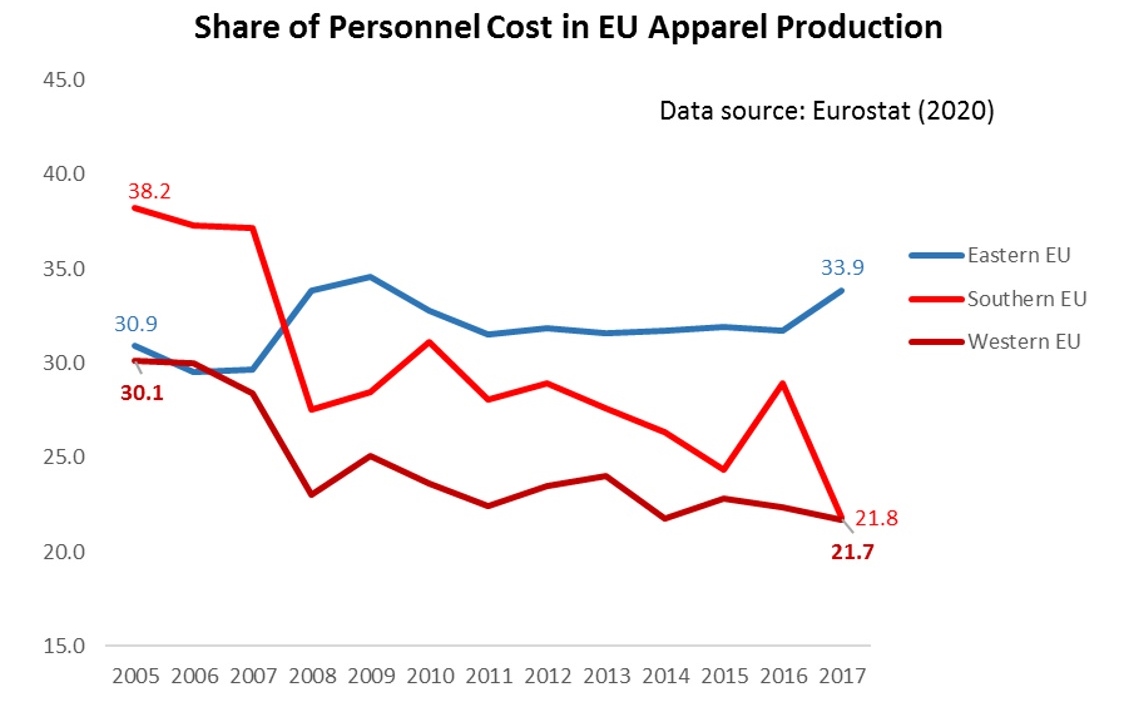

It is also interesting to note that in Western EU countries, labor only accounted for 21.7% of the total apparel production cost in 2017, which was substantially lower than 30.1% back in 2006. This change suggests that apparel manufacturing is becoming capital and technology-intensive in some developed Western EU countries—as companies are actively adopting automation technology in garment production.

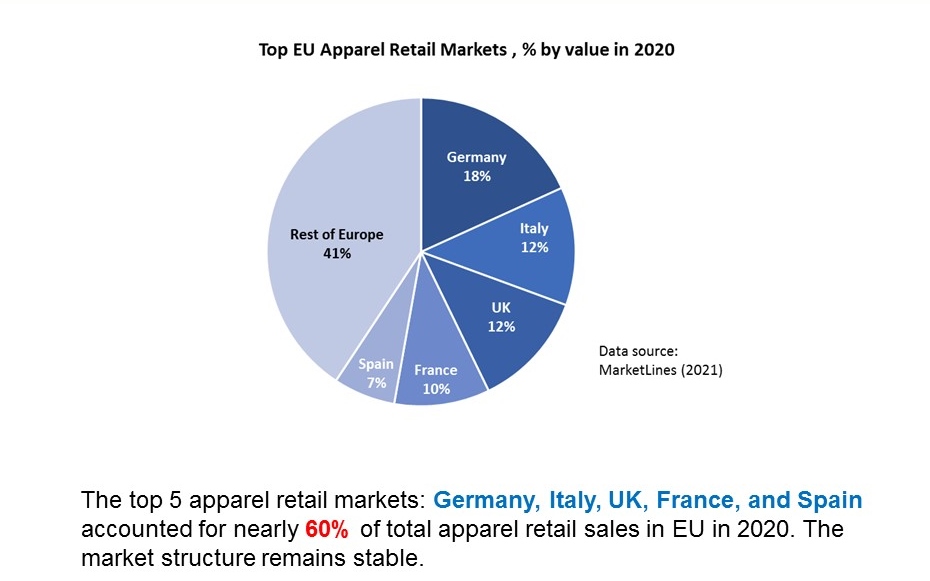

Because of their relatively high GDP per capita and size of the population, Germany, Italy, UK, France, and Spain accounted for nearly 60% of total apparel retail sales in the EU in 2020. Such a market structure has stayed stable over the past decade.

Data source: UNcomtrade (2021)

Intra-region trade is an important feature of the EU’s textile and apparel industry. Despite the increasing pressure from cost-competitive Asian suppliers, statistics from UNComtrade show that of the EU region’s total US$73.8bn textile imports in 2019, as much as 54.6% were in the category of intra-region trade. Similarly, of EU countries’ total US$204.0bn apparel imports in 2019, as much as 37.4% also came from other EU members. In comparison, close to 98% of apparel consumed in the United States are imported in 2019, of which more than 75% came from Asia (Eurostat, 2021; UNComtrade, 2021).

Regarding EU countries’ textile and apparel trade with non-EU members (i.e., extra-region trade), the United States remained one of the EU’s top export markets and a vital textile supplier (mainly for technical and industrial textiles). Meanwhile, Asian countries served as the dominant apparel sourcing base outside the EU region for EU fashion brands and retailers.

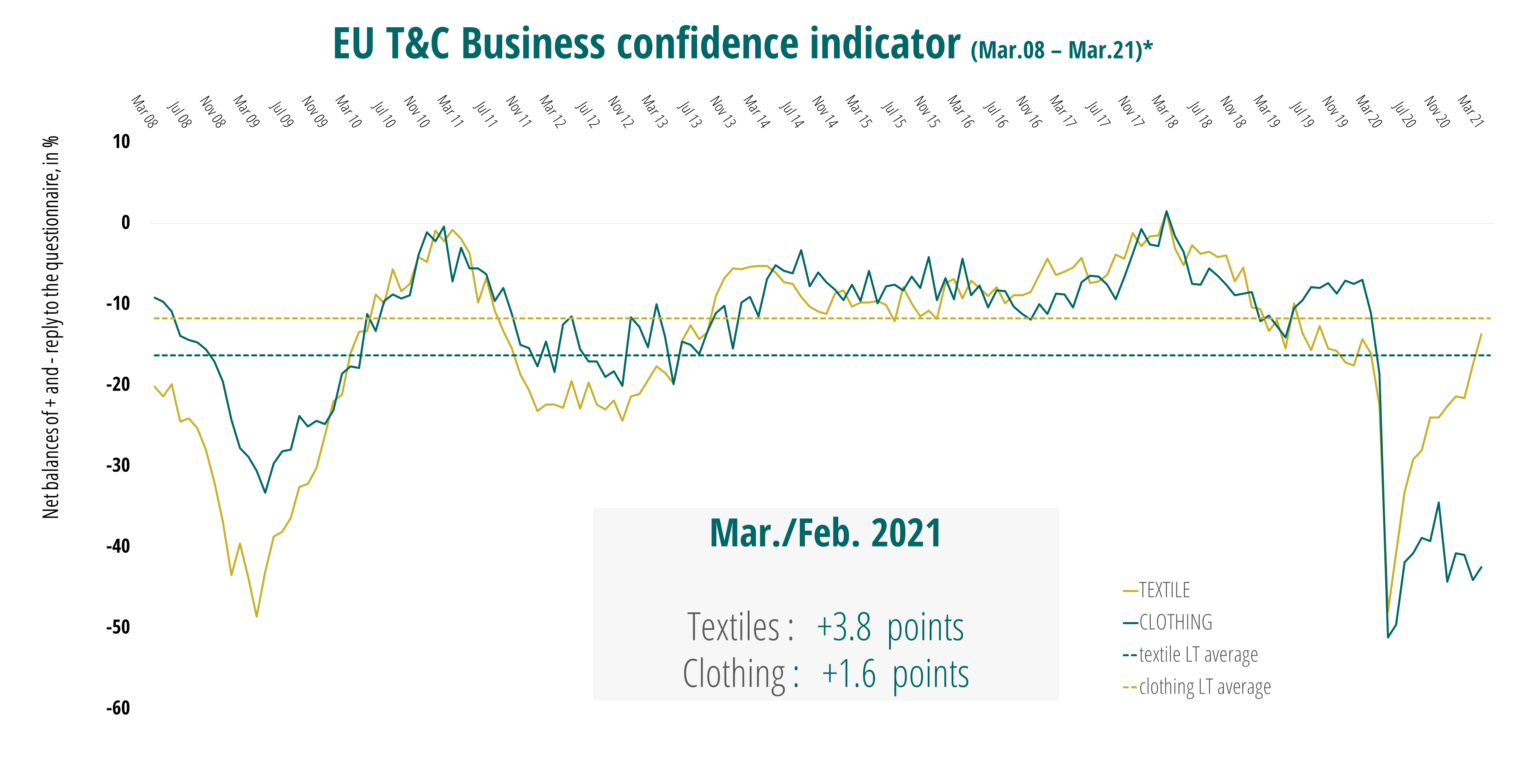

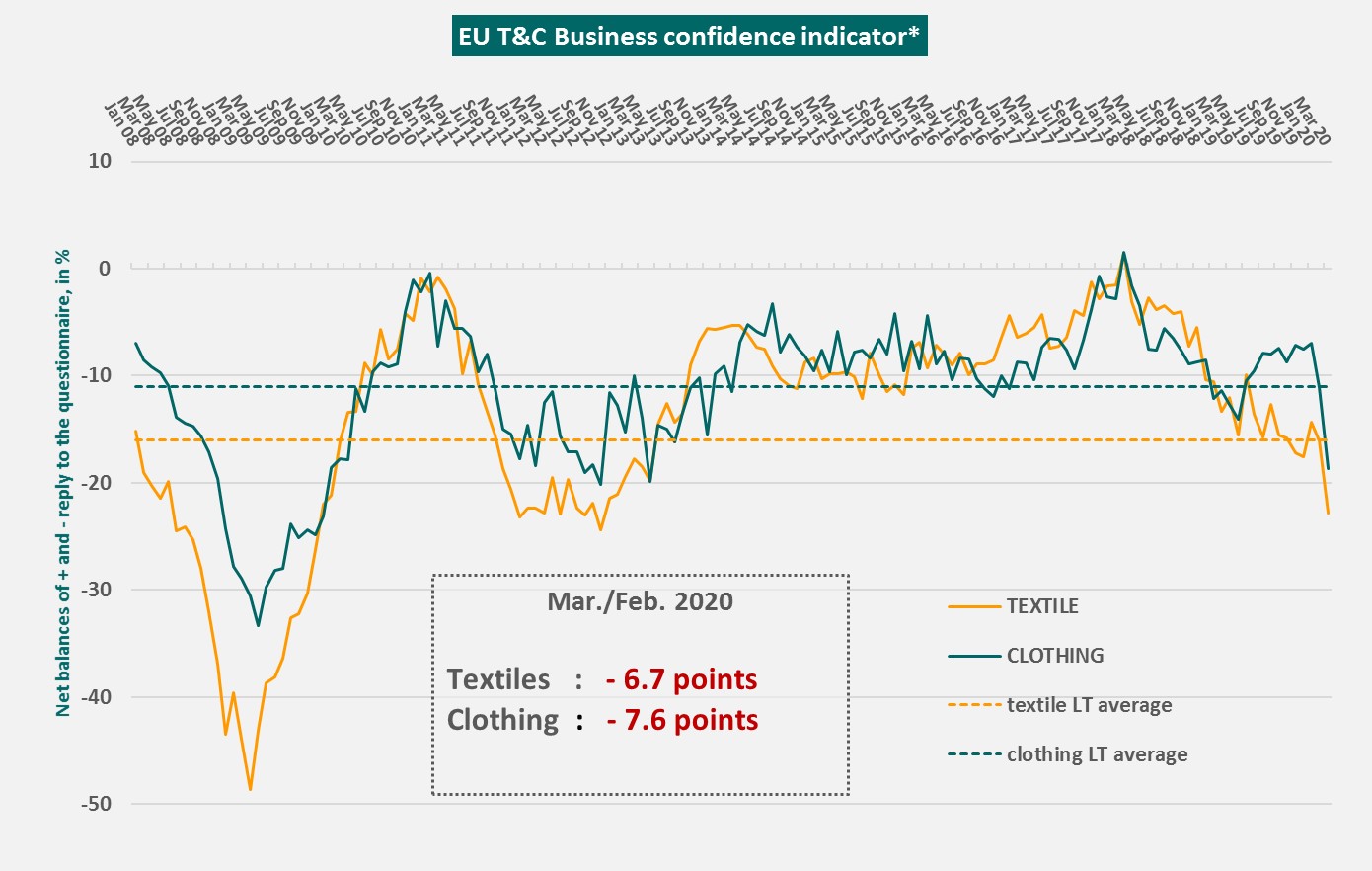

2021 hopefully will be a year of recovery and growthfor the EU textile and apparel industry. According to Euratex, the EU Business Confidence indicator of March 2021 gained momentum, with a confirmed upward trend in the textile industry (+3.8 points), and a modest recovery in the clothing industry (+1.6 points). However, Euratex also noted that EU textile and apparel companies still face daunting challenges and uncertainties in 2021, ranging from the rising raw material price, increasing transportation cost, to political instability in some key sourcing destinations (such as China and Myanmar).

While textile and apparel is well-known as a global sector, the latest statistics show that world textile and apparel trade patterns remain largely regional-based. Three particular regional textile and apparel trade flows are critical to watch:

First, Asian countries are increasingly sourcing textile raw material from within the region. As much as 85% of Asian countries’ textile imports came from other Asian countries in 2019, a substantial increase from only 70% in the 2000s. This result reflects the formation of an ever more integrated regional textile and apparel supply chain in Asia. However, as Asian countries become more economically integrated, textile and apparel producers in other parts of the world could find it more challenging to get involved in the region. With the recent reaching of several mega free trade agreements among countries in the Asia-Pacific region, such as the Regional Comprehensive Economic Partnership (RCEP), the pattern of “Made in Asia for Asia” is likely to strengthen further.

Second, the EU intra-region trade pattern for textile and apparel stays relatively strong and stable. Intra-region trade refers to trade flows between EU members. Statistics show that 54.6% of EU(27) members’ textile imports and 37.4% of their apparel imports came from within the EU(27) region in 2019. This pattern only slightly changed over the past decade. In other words, despite the reported increasing competition from Asian suppliers, many of which even enjoy duty-free market access to the EU market (such as through the EU Everything But Arms program), a substantial share of apparel sold in the EU markets are still locally made.

EU consumers’ preferences for “slow fashion” (i.e., purchasing less but for more durable products with higher quality) may contribute to the stable EU intra-region trade pattern. Many EU consumers also see textile and apparel as cultural products and do NOT shop simply for the price. This explains why Western EU countries such as Italy, Germany, and France rank the top apparel producers and exporters in the EU region despite their high wage and production costs.

Third, the Western Hemisphere (WH) supply chain faces significant challenges despite the seemingly growing popularity of “near-sourcing.” On the one hand, textile and apparel exporters in the Western-Hemisphere still rely heavily on the regional market. In 2019, respectively, as much as 79% of textiles and 86% of apparel exports from countries in the Western Hemisphere went to the same region.

However, on the other hand, the Western-Hemisphere supply chain is facing increasing competition from Asian suppliers. For example, in 2019, only 22% of North, South, and Central American countries’ textile imports and 15% of their apparel imports came from within the Western Hemisphere, a new record low in ten years. Similarly, in the first eleven months of 2020, only 15.7% of US apparel imports came from the Western Hemisphere, down from 17.1% in 2019 before the pandemic. The limited local textile production capacity and the high production cost are the two notable factors that discourage US fashion brands and retailers from committing to more “near-sourcing” from the Western Hemisphere.

In comparison, Asian countries supplied a new record high of 62.2% of textiles and 75% apparel to countries in the Western Hemisphere in 2019, up from 49.1% and 71.1% ten years ago. This trend suggests that as the competitiveness of “Factory Asia” continues to improve, even regional trade agreements (such as USMCA and CAFTA-DR) and their restrictive “yarn-forward” rules of origin have limits to protect the Western Hemisphere supply chain.

In comparison, Asian countries supplied a new record high of 62.2% of textiles and 75% apparel to countries in the Western Hemisphere in 2019, up from 49.1% and 71.1% ten years ago. This trend suggests that as the competitiveness of “Factory Asia” continues to improve, even regional trade agreements (such as USMCA and CAFTA-DR) and their restrictive “yarn-forward” rules of origin have limits to protect the Western Hemisphere supply chain.

Additionally, many say that the reaching of RCEP creates new pressure for the new Biden administration to consider joining the CPTPP and strengthening economic ties with countries in the Asia-Pacific region. Notably, several USMCA and CAFTA-DR members, such as Mexico, also have RCEP or CPTPP membership. Apparel producers in these Western Hemisphere countries may find it more rewarding to access the cheaper textile raw material from Asia through CPTPP or RCEP rather than claiming the duty-saving benefits for finished garments under USMCA or CAFTA-DR. Like it or not, the Biden administration’s inaction will also have consequences.

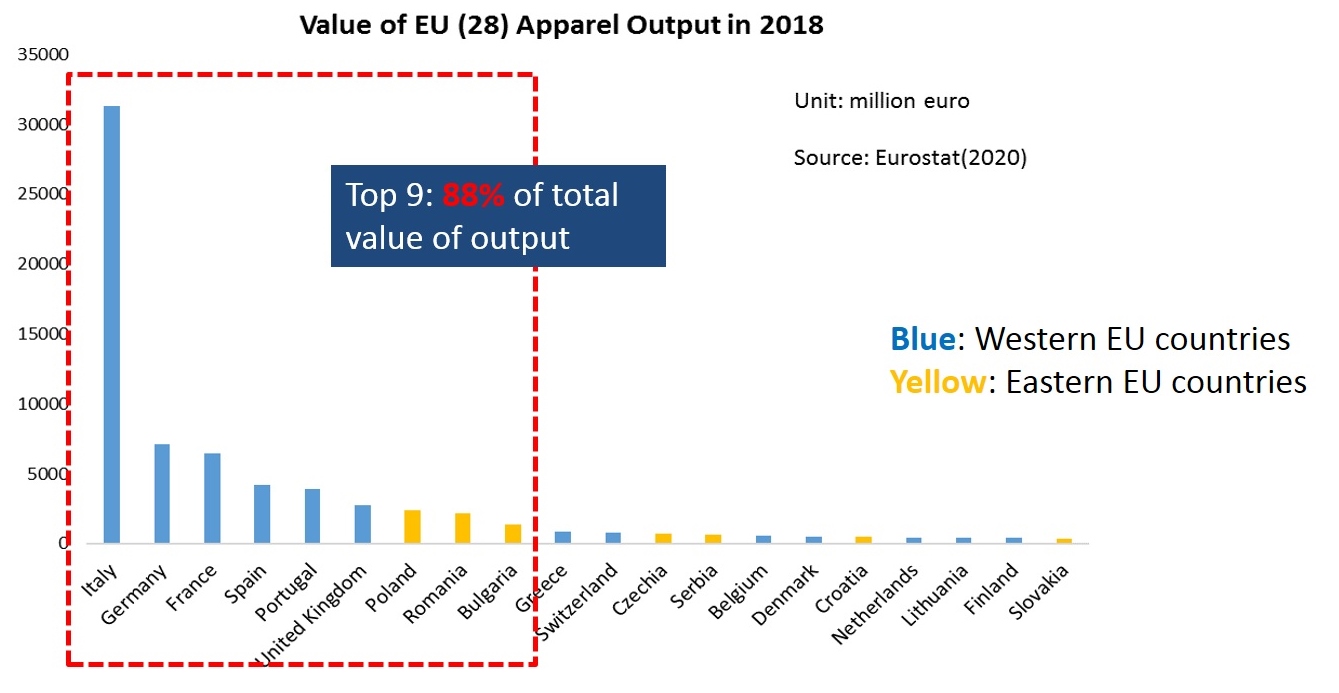

The EU region as a whole remains one of the world’s leading producers of textile and apparel (T&A). The value of EU’s T&A production totaled EUR146.2bn in 2018, marginally up 2% from a year ago (Note: Statistical Classification of Economic Activities or NACE, sectors C13, and C14). The value of EU’s T&A output was divided almost equally between textile manufacturing (EUR77.4bn) and apparel manufacturing (EUR70.0bn).

Regarding textile production, Southern and Western EU, where most developed EU members are located such as Germany, France, and Italy, accounted for nearly 73.7% of EU’s textile manufacturing in 2018. Further, of EU countries’ total textile output, the share of non-woven and other technical textile products (NACE sectors C1395 and C1396) has increased from 19.2% in 2011 to 23.0% in 2017, which reflects the on-going structural change of the sector.

Apparel manufacturing in the EU includes two primary categories: one is the medium-priced products for consumption in the mass market, which are produced primarily by developing countries in Eastern and Southern Europe, such as Poland, Hungary, and Romania, where cheap labor is relatively abundant. The other category is the high-end luxury apparel produced by developed Western EU countries, such as Italy, UK, France, and Germany.

It is also interesting to note that in Western EU countries, labor only accounted for 21.7% of the total apparel production cost in 2017, which was substantially lower than 30.1% back in 2006. This change suggests that apparel manufacturing is becoming capital and technology-intensive in some developed Western EU countries—as companies are actively adopting automation technology in garment production.

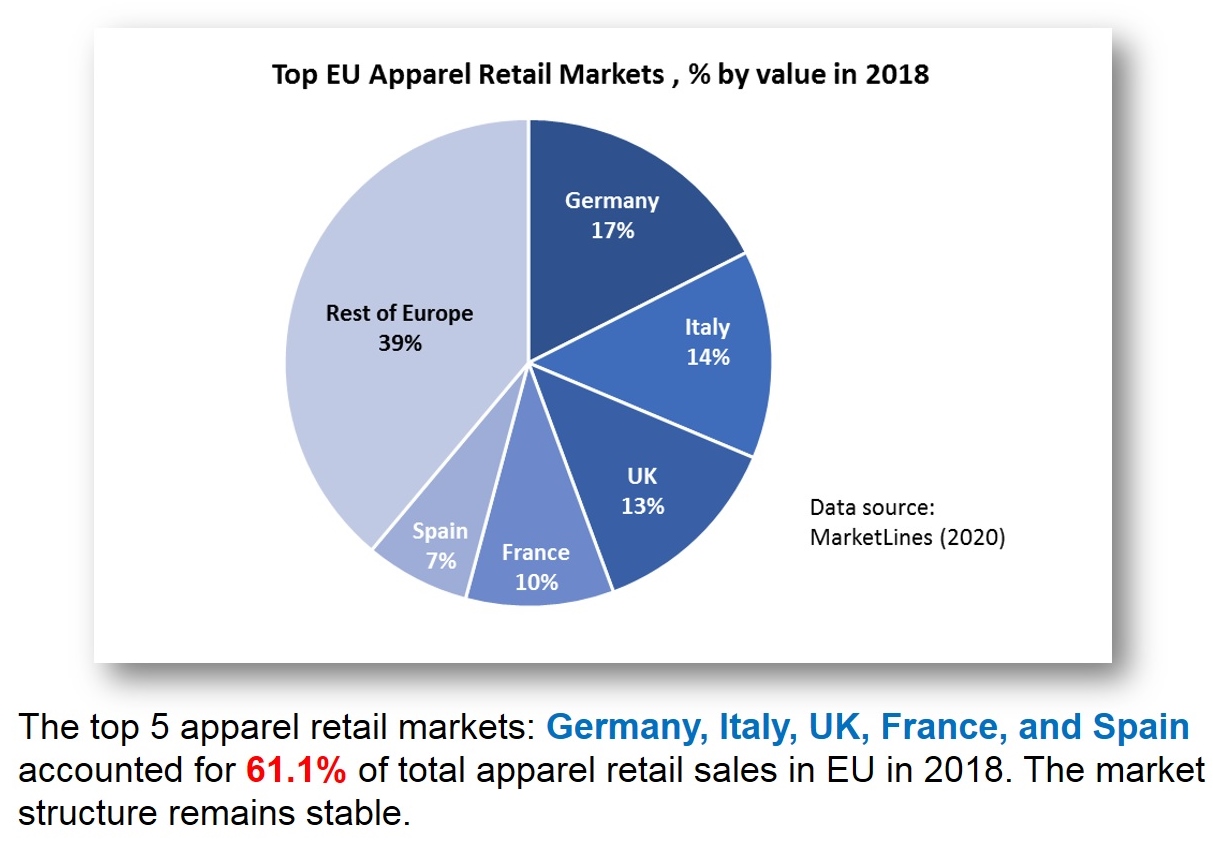

Because of their relatively high GDP per capita and size of the population, Germany, Italy, UK, France, and Spain accounted for 61.1% of total apparel retail sales in the EU in 2018. Such a market structure has stayed stable over the past decade.

Data source: UNcomtrade (2020)

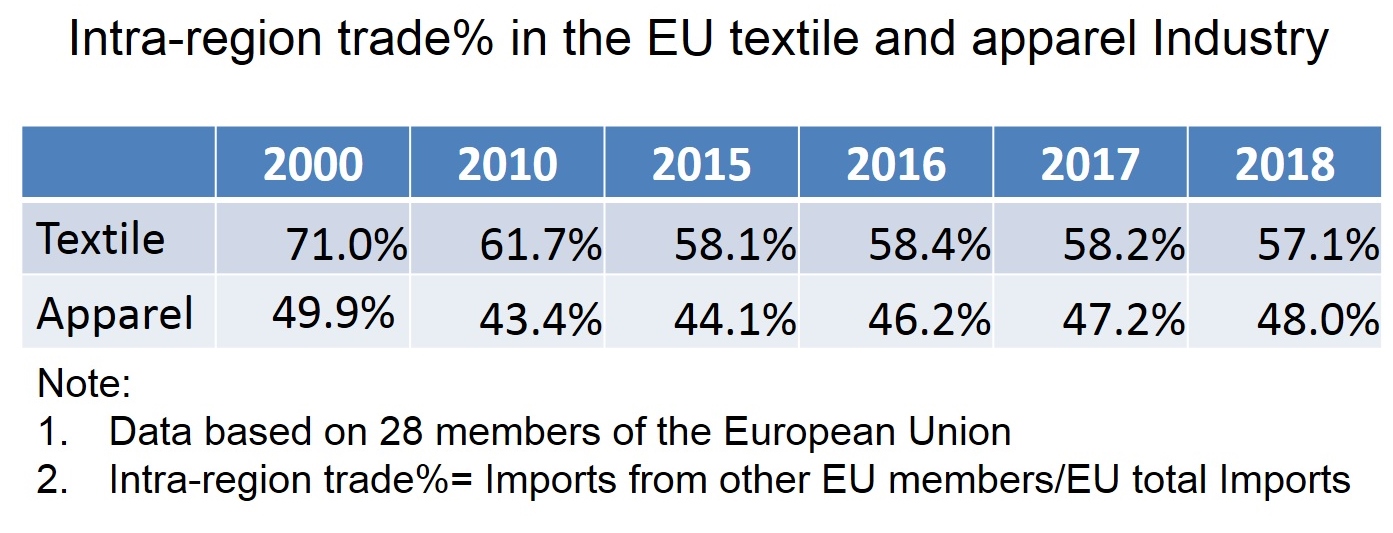

Intra-region trade is an important feature of the EU’s textile and apparel industry. Despite the increasing pressure from cost-competitive Asian suppliers, statistics from the World Trade Organization (WTO) show that of the EU region’s total US$73.7bn textile imports in 2018, as much as 57.1% were in the category of intra-region trade. Similarly, of EU countries’ total US$205.0bn apparel imports in 2018, as much as 48.0% also came from other EU members. In comparison, close to 97% of apparel consumed in the United States are imported in 2018, of which more than 80% came from Asia (Eurostat, 2020; WTO, 2020).

The EU textile and apparel industry is not immune to COVID-19. According to the European Apparel and Textile Federation (Euratex), the outbreak of COVID-19 may cause a 50% drop in sales and production for the EU textile and apparel sector in 2020. A recent survey of EU-based T&A companies shows that almost 9 out of 10 respondents reported facing serious constraints on their financial situation and 80% of companies had temporarily laid-off workers. Around 25% of surveyed companies were considering closing down their businesses. Further, EU T&A companies were concerned about EU’s tightened border controls, which have “increased sharply, leading to delays in supplies but also cancelling of orders, thus aggravating the economic impact.”

On

October 16, 2018, the Trump

Administration notified U.S. Congress its intention to negotiate the

U.S.-EU Free Trade Agreement. Between

2013 and 2016, the United States and EU were also engaged in the negotiation of

a comprehensive free trade agreement– Trans-Atlantic Trade and Investment Partnership

(T-TIP) with the goal to unlock market access opportunities for

businesses on both sides of the Atlantic through the ambitious elimination of

trade and investment barriers as well as enhanced regulatory coherence. The T-TIP

negotiation was stalled since 2017, although

the Trump Administration has never officially announced to withdraw from the

agreement.

II. Negotiating Objectives

On

January 11, 2019, the Office of the U.S. Trade Representative (USTR) released

thenegotiating

objectives of the proposed U.S.-EU Free Trade Agreement after

seeking inputs from the public. Overall, the proposed agreement aims to address

both tariff and non-tariff barriers and to “achieve fairer, more balanced trade”

between the two sides.

Regarding textiles and apparel, USTR says it will secure duty-free access for U.S. textile and

apparel products and seek to improve competitive opportunities for exports of

U.S. textile and apparel products while taking into account U.S. import

sensitivities” during the negotiation. The proposed U.S.-EU free trade

agreement also will “establish origin procedures for the certification and

verification of rules of origin that promote strong enforcement, including with respect to textiles.” T-TIP

had adopted similar negotiating objectives for the textile and apparel sector.

III. Industry viewpoints on the agreement

As of

January 2019, leading trade associations

representing the U.S. apparel industry and the EU textile and apparel industries

have expressed support for the proposed U.S.-EU Free Trade Agreement. In general,

these industry associations recommend the agreement to achieve the following

goals:

First, eliminate import duties. For example:

American

Apparel and Footwear Association (AAFA): “We

support the immediate and reciprocal elimination of the high duties that both

countries maintain on textiles, travel goods, footwear, and apparel.”…” We also

support the immediate elimination of any retaliatory duties imposed by the

E.U., as well as any duties imposed by the U.S. (that led to that retaliation).

The duties impose costs on activities, including manufacturing activities in

the U.S., and undermine markets for U.S. exporters in Europe.”

European

Apparel and Textile Confederation (Euratex):“The

European Textile and Clothing sector faces high tariffs while exporting to the

US market from 11% to up to 32% for some products, namely sewing thread of

man-made filaments, suits, woven fabrics of cotton, trousers and t-shirts. Zero

customs duties while ensuring modern rules of origin will allow EU companies to

boost exports and offer more choice to American consumers and professional

buyers.”

Second, promote regulatory coherence (Harmonization). For example:

AAFA: “The E.U. and the

United States both maintain an extensive array of product safety, chemical management,

and labeling requirements regarding apparel (including legwear), footwear,

textiles, and travel goods.”…” Yet they often contain different requirements,

such as testing or certification, that greatly add compliance costs.”…” We

believe the U.S.‐E.U. trade agreement presents an important opportunity to achieve

harmonization or alignment for these regulations.”

Euratex: “Maintaining high

level of standards while eliminating unnecessary burdens, removing additional

requirements and facilitating customs procedures that impede business are top

priorities. Mutual recognition of the EU and US standards will preserve high

level of consumer protection on both sides of the Atlantic. Convergence on labelling (fibre

names, care symbols and wool labelling),

consumer safety on children products and flammability standards is key for the

T&C sector.” “EURATEX believes the EU and US standardization bodies should

cooperate on setting standards for Smart Textiles taking into account the

industry views for facilitating development and trade of such products of the

future.”

Third, adopt flexible/modern rules of origin. For example:

AAFA: “We should also support higher usage of the agreement by making sure the rules of origin reflect the realities of the industry today…”the yarn forward” rules, although theoretically promote usage of trade partner inputs, in practice they operate as significant barriers that restrict the ability of companies to use a trade agreement in many cases”…” We need to incorporate sufficient flexibilities into the rules of origin so that different supply chains –and the U.S. jobs they support – can take advantage of the agreement.”

Euratex: “Zero customs

duties while ensuring modern rules of

origin will allow EU companies to boost exports and offer more choice to

American consumers and professional buyers.”

The National Council of Textile Organizations (NCTO), which represents the U.S. textile industry, hasn’t publically stated its position on the proposed U.S.-EU Free Trade Agreement. However, NCTO had strongly urged U.S. trade negotiators to adopt a yarn-forward rule of origin in T-TIP. NCTO also opposed opening the U.S. government procurement market protected by the Berry Amendment to EU companies.

IV. Patterns of U.S.-EU textile and apparel trade

The

United States and the EU are mutually important textile and apparel (T&A)

trading partners. For example, the United States is EU’s largest extra-region

export market for textiles, and EU’s fifth largest extra-region supplier of

textiles in 2017 (Euratex, 2018).

Meanwhile,

the EU is one of the leading export markets for U.S.-made technical textiles as

well as an important source of high-end apparel products for U.S. consumers (OTEXA,

2018). Specifically, in 2017, U.S. T&A exports to the European Union

totaled $2,572 million, of which 73.2% were textile products, such as specialty

& industrial fabrics, felts & other non-woven fabrics and filament

yarns. In comparison, EU’s T&A exports to the United States totaled $4,163

million in 2017, among which textiles and apparel evenly accounted for 48.7%

and 51.3% respectively.

V. Potential economic impact of the agreement

By adopting the Global Trade Analysis Project (GTAP) model, Lu (2017) quantitatively evaluated the potential impact of a free trade agreement between the U.S. and EU on the textile and apparel sector. According to the study:

First,

the trade creation effect of the agreement will expand the EU-U.S.

intra-industry trade for textiles. Meanwhile, the agreement is likely to

significantly expand EU’s apparel exports to the United States.

Second,

the trade diversion effect of the U.S.-EU Free Trade Agreement will affect other

T&A exporters negatively, including Asia’s T&A exports to the U.S. market

and EU and Turkey’s T&A exports to the EU market.

Third, the U.S.-EU Textile and Apparel Trade might affect the intra-region T&A trade in the EU region negatively but in a limited way.

Overall, the study suggests that the EU T&A industry will benefit from the additional market access opportunities created by the U.S.-EU Free Trade Agreement.One important factor is that the U.S. and EU T&A industries do not constitute a major competing relationship. For example, the United States is no longer a major apparel producer, and EU’s apparel exports to the United States fulfill U.S. consumers’ demand for high-end luxury products. The U.S.-EU Free Trade Agreement is also likely to create additional export opportunities for EU textile companies in the U.S. market, especially in the technical textiles area, which accounted for approximately 40% of EU’s total textile exports to the United States in 2017 measured in value. Compared with traditional yarns and fabrics for apparel making purposes, technical textiles are with a greater variety in usage, which allows EU companies to be able to differentiate products and find their niche in the U.S. market.

Further, the study suggests that we shall pay more attention to the details of non-tariff barrier removal under the U.S.-EU Free Trade Agreement, which could result in bigger economic impacts than tariff elimination.