The following findings were based on an analysis of trade volume and tariff data at the 6-digit HTS code level.

#1 Amid COVID-19, shipping crisis, and US-China tariff war, US fashion brands and retailers demonstrate a new round of interest in expanding “near-sourcing” from member countries of the US-Mexico-Canada Trade Agreement (USMCA, previously NAFTA) and Dominican Republic-Central America Free Trade Agreement (CAFTA-DR).

Data shows that 15.2% of US apparel imports came from USMCA and CAFTA-DR members YTD in 2021 (January-August), higher than 13.7% in 2020 and about 14.7% before the pandemic (2018-2019). Notably, CAFTA-DR members’ market shares increased to 11% in 2021 (January to Aug) from 9.6% in 2020. The value of US apparel imports from CAFTA-DR also enjoyed a 54% growth in 2021 (January—Aug) from a year ago, faster than 25% of the world’s average.

#2 Sourcing apparel from USCMA and CAFTA-DR members helps US fashion brands and retailers save around $1.6-1.7 billion tariff duties annually. (note: the estimation considers the value of US apparel imports from USMCA and CAFTA-DR members at the 6-digit HTS code level and the applied MFN tariff rates for these products; we didn’t consider the additional Section 301 tariffs US companies paid for imports from China). Official trade statistics also show that measured by value, about 73% of US apparel imports under free trade agreements came through USMCA (25%) and CAFTA-DR (48%) from 2019 to 2020.

#3 US apparel imports from USMCA and CAFTA-DR members do NOT necessarily focus on items subject to a high tariff rate. Measured at the 6-digit HS code level, apparel items subject to a high tariff rate (i.e., applied MFN tariff rate >17%) only accounted for about 8-9% of US apparel imports from USMCA members and 7-8% imports from CAFTA-DR members. In comparison, even having to pay a significant amount of import duties, around 17% of US apparel imports from Vietnam and 10% of imports from China were subject to a high tariff rate (see table below).

The phenomenon suggests that USCMA and CAFTA-DR members still have limited production capacity for many man-made fibers (MMF) clothing categories (such as jackets, swimwear, dresses, and suits), typically facing a higher tariff rate. This result also implies that expanding production capacity and diversifying the export product structure could make USMCA and CAFTA-DR more attractive sourcing destinations.

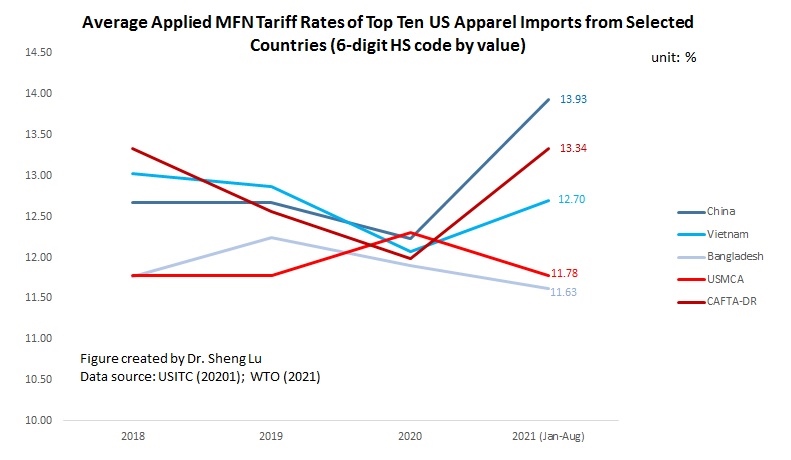

#4 US apparel imports from USMCA and CAFTA-DR members tend to focus on large-volume items subject to a medium tariff rate. Specifically, from 2017 to 2021 (Jan-Aug), ten products (at the 6-digit HTS code level) typically contributed around half of the US tariff revenues collected from apparel items (HS chapters 61-62). However, the average applied MFN tariff rates for these items were only about 13%. Meanwhile, these top tariff-revenue-contributing apparel items accounted for about 50% of US apparel imports from USMCA members and nearly 64%-69% of imports from CAFTA-DR members.

Likewise, the top ten products (at the 6-digit HTS code level) typically accounted for 65%-68% of US apparel imports from USMCA members and nearly 73-75% of US apparel imports from CAFTA-DR members. These products also had a medium average applied MFN rate at 11-12% for USMCA and 12-13% in the case of CAFTA-DR.

Given the duty-saving incentives, expanding “near-sourcing” from USMCA and CAFTA-DR members could prioritize these large-volume apparel items with a medium tariff rate in short to medium terms. However, in the long run, a shortcoming of this strategy is that many such items are basic fashion clothing that primarily competes on price (such as T-shirts and trousers) and cannot leverage the unique competitive edge of near-sourcing (such as speed to market). When the US reaches new free trade agreements, particularly those involving leading apparel-producing countries in Asia, it could offset the tariff advantages enjoyed by USMCA and CAFTA-DR members and quickly result in trade diversion.

by Sheng Lu

More reading:

- Sheng Lu (2021). US apparel sourcing: Understanding import duty savings. Just-Style.

- USTR Roundtable Highlights the United States-Central America Supply Chain for Textiles and Apparel (October 2021)

This article was eye-opening in that it brought light to trade volume and tariff data. The pandemic, the shipping crisis, and the US-China tariff war, have increased US fashion brands and retailers’ interest in near-sourcing from member countries of trade agreements. I learned from this article and from this course that near-sourcing is when a business moves its operations closer to where its end products are sold. This process is trending in the supply chain industry today. For example, data has shown that a good amount of US apparel imports came from USMCA and CAFTA-DR members in 2021, and the percentage was notably higher than in 2020 and before the pandemic. The value of US apparel imports from CAFTA-DR has also grew from the year before. Sourcing apparel from USCMA and CAFTA-DR members helps US fashion brands and retailers save around $1.6-1.7 billion tariff duties annually…. a huge amount so trade agreements seem to be extremely beneficial.

After reading through this article, I am not surprised by the increase in imports from USMCA and CAFTA-DR members. USMCA and CAFTA-DR are set up to make trade easier between these countries and have many benefits. My question is why the percentage of imports went down during the year 2020. Imports were at about 14.7% before the pandemic (2018-2019) and then decreased to 13.7% in 2020. Only now is it starting to increase again in the year 2021. I wonder, with all of the benefits of these agreements, why would the US go out of their way to pay high tariffs to other countries during the pandemic? My only guess is through what we learned in class about the ease of trade with China during the pandemic due to their flexibility and speed. However, I still think not paying tariffs would be more frugal. I am curious to see if the imports from these regions continue to rise as we continue towards the new normal.

I am intrigued by the amount of trade that goes on in the CAFTA-DR region and the way that the region takes advantage of duty free trade opportunities. I was especially shocked when I read that Sourcing apparel from USCMA and CAFTA-DR members helps US fashion brands and retailers save around $1.6-1.7 billion tariff duties annually. This shows the success of the trade agreement within the Western Hemisphere supply chain. Do you think that this trend will continue? With RCEP coming into play, I do not know for sure. Due to the current political climate and health crisis due to COVID-19 the concept of near-shoring has grown in popularity and has become a real possibility for future sourcing decisions. Although this is a goal for fashion brands and suppliers, is it possible with Asia having such a cheap and efficient supply chain?I can only wonder how Asia will evolve and pose as a major competitor to the United States and other members of CAFTA-DR.