Regarding Levi’s “new normal” for apparel sourcing and supply chain management, what is Harmit Singh’s vision? Why or why not do you agree with him?

How could Levi’s digital transformation plans affect its sourcing practices?

What is your evaluation of Levi’s “tailor shop” program?

What is the rationale behind Levi’s “buy better and wear better” initiative?

What is a chief financial officer (CFO)’s role in helping Levi’s achieve its sustainability goals?

Anything else you find interesting/intriguing/new/inspiring from the video and why?

About Levi’s

Levi’s supplier map (source: Open Apparel Registry)

Levi Strauss & Co is a global apparel company rooted in the jeans category. Its brand portfolio consists of Levi’s brand, Levi’s Signature, Dockers, and Denizen. In 2020, Levi’s global sales exceeded $7.1 billion. The United States is Levi’s largest market, accounting for about 41% of its sales in 2020, followed by Mexico. As of June 2021, Levi’s sources its apparel products from around 350 factories located in about 30 countries.

Years before the pandemic, Levi Strauss has begun to reduce its reliance on wholesalers and instead expand its direct-to-consumer (DTC) business. In response to COVID-19, Levi Strauss has increased flexibility and resilience through diversification across geographies, categories, genders, and distribution channels. Levi’s is also well-known as a leader in sustainability, particularly reducing chemical and water use in products.

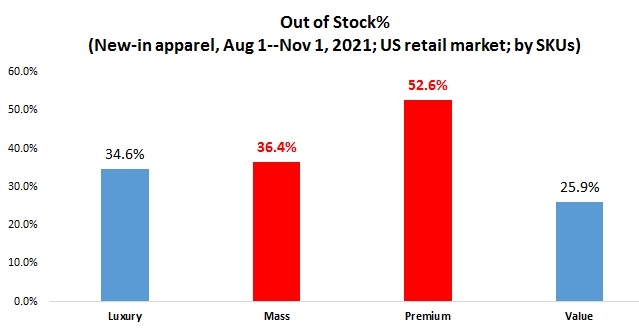

US fashion brands and apparel retailers face the challenge of running out of inventory amid the holiday season and the ongoing shipping crisis. Based on consultation with industry insiders and resources, we take a detailed look at which apparel products are more likely to be out of stock in the US retail market. Several patterns are noteworthy:

First, clothing products targeting the premium and mass market face more significant shortages than luxury or value apparel items in the US. Take clothing items in the premium market, for example. Of those apparel products newly launched to the US retail market from August 1 to November 1, 2021, nearly half of them were already out of stock as of November 10, 2021 (note: measured by SKUs). The increased demand from middle-class US consumers could be among the primary contributing factors.

Second, seasonal products and stable fashion items are more likely to be out of stock. For example, as we are already in the winter season, it is not surprising to see many swimwear products run out of stock. Meanwhile, it is interesting to see stable fashion products like hosiery and underwear also report a relatively high percentage of inventory shortage. The result could be the combined effects of consumers’ robust demand and the shipping delay.

Third, apparel products locally sourced from the US seem to have the lowest out-of-stock rate. Reflecting the shipping crisis, clothing items sourced from Bangladesh and India report a much higher out-of-stock rate. However, a substantial percentage of “made in the USA” apparel was in the category of “T-shirt”, implying switching to domestic sourcing often is not a viable option for US fashion brands and retailers.

Additionally, fast fashion retailers overall report a much lower out-of-stock rate than department stores and specialty clothing stores. This result showcases fast fashion retailers’ competitive advantages in supply chain management, which payoffs in the current challenging business environment.

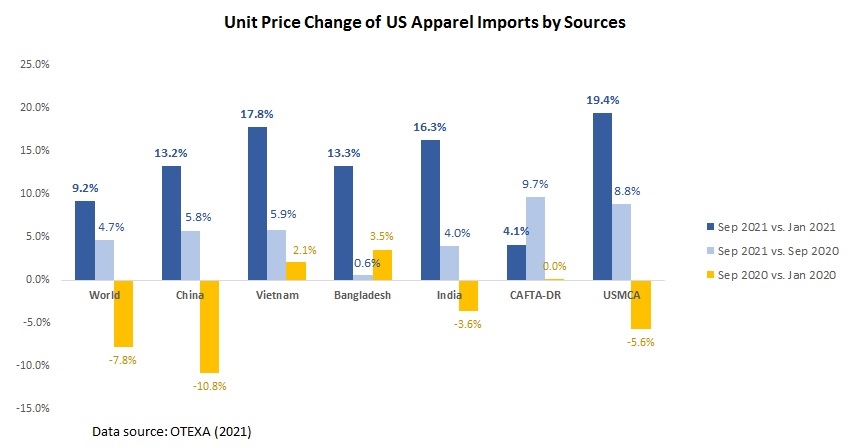

On the other hand, the latest trade data suggests a notable increase in the price of US apparel imports. Notably, the unit price of US apparel imports from almost all leading sources went up by more than 10% from January 2021 to September 2021.

Today, fashion companies consider a long list of factors when deciding where to source their apparel products, ranging from cost, speed to market, flexibility to the risk of social and environmental compliance. While existing studies have identified these major sourcing factors, whether they are treated equally in companies’ apparel sourcing decisions remains mostly unknown. Neither is it clear how fashion companies make a trade-off among these sourcing factors, given no sourcing destination is perfect.

This study aims to quantitatively evaluate the influence of primary sourcing factors on fashion companies’ determination of apparel sourcing destinations. For the study, we collected a detailed evaluation of the world’s 27 largest sourcing destinations in 2019 against 15 specific performance indicators from GlobalData, one of the most popular sourcing analytics tools. The evaluation uses a 5-point rating scale for each performance indicator.

Because some of these 15 performance indicators measure similar items, we first conducted an exploratory factor analysis, which reduced these indicators to five principal sourcing factors based on their correlation matrix scores. These five principal sourcing factors cover the following themes:

Capacity: It covers seven performance indicators that measure a sourcing destination’s capabilities (including flexibility and lead time) of providing apparel products and other value-added services.

Price & Tariff: It covers two performance indicators that measure the financial implications of sourcing from a particular destination, including eligibility for preferential import duties.

Stability: It covers two performance indicators that measure a sourcing destination’s macro-business environment, specifically sourcing-related political and economic climates.

Sustainability: It encompasses all social and environmental compliance issues related to apparel production and sourcing.

Quality: It covers two performance indicators that measure whether a sourcing destination obtains skilled workers and the overall quality of its products.

Next, we calculated the 27 apparel exporting countries’ average scores of these five principal sourcing factors. Based on the results, we further conducted a multiple regression analysis to evaluate the impact of the five principal sourcing factors on the value of these 27 countries’ apparel exports to the U.S., EU, and Asia in 2019, respectively. These three regions combined accounted for more than 80% of world apparel imports that year; however, fashion companies in each area are suggested to have unique sourcing preferences.

First, the result suggests that improving the performance in Stability and Quality can help a country enhance its attractiveness as an apparel sourcing base in the U.S. and Asia markets, but not so much in the EU market.

Second, a higher score for the factor Sustainability does not result in more sourcing orders at the country level in all three markets examined. It seems fashion companies’ current sourcing model does not provide substantial financial rewards encouraging better performance in sustainability. It is also likely that sustainability and compliance are treated more as pre-requisite criteria instead of determining the volume of the sourcing orders.

Third, the impact of Price & Tariff and Capacity on the value of apparel imports is not statistically significant in any of the three markets examined. This result does NOT necessarily mean price and production capacity is irrelevant. Instead, the result implies that fashion companies’ sourcing decision today is not merely about “chasing the lowest price.” Meanwhile, due to concerns about supply chain risks, even the most “economically competitive” sourcing destination won’t receive all the sourcing orders.

The findings of the study suggest that fashion companies’ sourcing decisions today appear to be more complicated and subtle than what is revealed by the existing literature and the public perception. Notably, the findings present different views from previous studies regarding how sourcing cost and sustainability affect fashion companies’ selection of sourcing destinations.

The findings also call our attention to the significant impact of non-economic factors on companies’ sourcing decisions, particularly the perceived political risks. This result explained why fashion companies had quickly reacted to the recent forced labor concerns in Xinjiang, China, and the military coup in Myanmar and halted sourcing from the regions.

The Regional Comprehensive Economic Partnership (RCEP)is a free trade agreement between ten member states of the Association of Southeast Asian Nations (ASEAN)* and five other large economies in the Asia-Pacific region (China, Japan, South Korea, New Zealand, and Australia). RCEP was reached on November 15, 2020, after nearly eight years of tough negotiation. (Note: ASEAN members include Brunei, Cambodia, Indonesia, Laos, Malaysia, Myanmar, the Philippines, Singapore, Thailand, and Vietnam. India was an original RCEP member but decided to quit in late 2019 due to concerns about competing with Chinese products, including textiles and apparel.)

So far, RCEP is the world’s largest trading bloc. As of 2019, RCEP members accounted for nearly 26.2% of world GDP, 29.5% of world merchandise exports, and 25.9% of world merchandise imports.

As of November 1, 2021, Lao, Burnei, Cambodia, Singapore and Thailand (ASEAN members), as well as China, Japan, New Zealand and Australia have ratified the agreement. This has met the minimum criteria for RCEP to enter into force (i.e., six members, including at least three ASEAN members and three non-ASEAN members).

Why RCEP matters to the textile and apparel industry?

RCEP matters significantly for the textile and apparel (T&A) sector. According to statistics from the United Nations, in 2019, the fifteen RCEP members altogether exported US$374 billion worth of T&A (or 50% of the world share) and imported US$139 billion (or 20% of the world share).

In particular, RCEP members serve as critical apparel-sourcing bases for many US and EU fashion brands. For example, in 2019, close to 60% of US apparel imports came from RCEP members, up from 45% in 2005. Likewise, in 2019, 32% of EU apparel imports also came from RCEP members, up from 28.1% in 2005.

Notably, RCEP members have been developing and forming a regional textile and apparel supply chain. More economically advanced RCEP members (such as Japan, South Korea, and China) supply textile raw materials to the less economically developed countries in the region within this regional supply chain. Based on relatively lower wages, the less developed countries typically undertake the most labor-intensive processes of apparel manufacturing and then export finished apparel to major consumption markets worldwide.

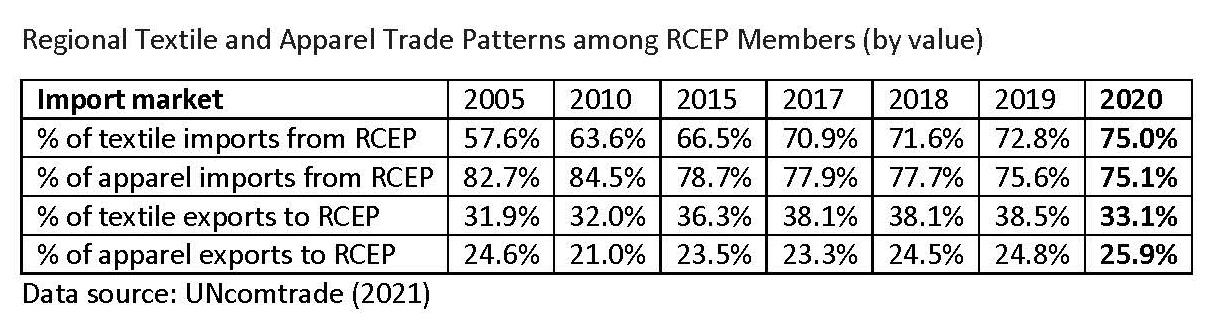

As a reflection of an ever more integrated regional supply chain, in 2019, as much as 72.8% of RCEP members’ textile imports came from other RCEP members, a substantial increase from only 57.6% in 2005. Nearly 40% of RCEP members’ textile exports also went to other RCEP members in 2019, up from 31.9% in 2005.

What are the key provisions in RCEP related to textiles and apparel?

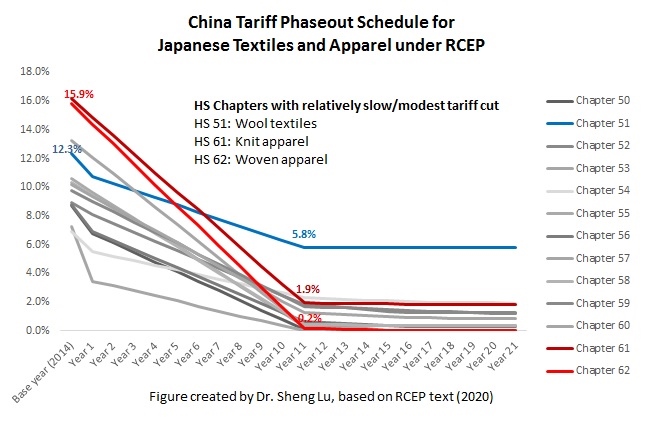

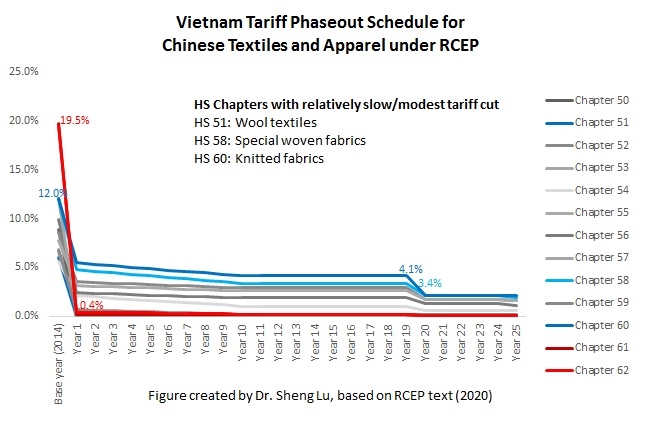

First, RCEP members have committed to reducing the tariff rates to zero for most textile and apparel traded between RCEP members on day one after the agreement enters into force. That being said, the detailed tariff phaseout schedule for textile and apparel products under RCEP is very complicated. Each RCEP member sets their own tariff phaseout schedule, which can last more than 20 years (for example, 34 years for South Korea and 21 years for Japan.) Also, different from U.S. or EU-based free trade agreements, the RCEP phaseout schedule is country-specific. For example, South Korea sets different tariff phaseout schedules for textile and apparel products from ASEAN, China, Australia, Japan, and New Zealand. Japan’s tariff cut for apparel products is more generous toward ASEAN members and less so for China and South Korea (see the graph above). Companies interested in taking advantage of the duty-free benefits under RCEP need to study the “rules of the game” in detail.

Second, in general, RCEP adopts very liberal rules of origin for apparel products. It only requires that all non-originating materials used in the production of the good have undergone a tariff shift at the 2-digit HS code level (say a change from any chapters from chapters 50-60 to chapter 61). In other words, RCEP members are allowed to source yarns and fabrics from anywhere in the world, and the finished garments will still qualify for duty-free benefits. Most garment factories in RCEP member countries can immediately enjoy the RCEP benefits without adjusting their current supply chains.

What are the potential economic impacts of RCEP on the textile and apparel sector?

On the one hand, the implementation of RCEP is likely to further strengthen the regional textile and apparel supply chain among RCEP members. Particularly, RCEP will likely strengthen Japan, South Korea, and China as the primary textile suppliers for the regional T&A supply chain. Meanwhile, RCEP will also enlarge the role of ASEAN as the leading apparel producer in the region.

On the other hand, as a trading bloc, RCEP could make it even harder for non-RCEP members to get involved in the regional textile and apparel supply chain formed by RCEP members. Because an entire regional textile and apparel supply chain already exists among RCEP members, plus the factor of speed to market, few incentives are out there for RCEP members to partner with suppliers from outside the region in textile and apparel production. The tariff elimination under the RCEP will put textile and apparel producers that are not members of the agreement at a more significant disadvantage in the competition. Not surprisingly, according to a recent study, measured by value, only around 21.5% of RCEP members’ textile imports will come from outside the area after the implementation of the agreement, down from the base-year level of 29.9% in 2015.

Further, the reaching of RCEP could accelerate the negotiation of other trade agreements in the Asia-Pacific region, such as the China-South Korea-Japan Free Trade Agreement. We might also see growing pressures on the Biden administration to join the Comprehensive and Progressive Agreement of the Trans-Pacific Partnership (CPTPP) to strengthen the US economic ties with countries in the Asia-Pacific region. The economic competition between the United States and China in the area could also intensify as the combined effects of RCEP and CPTPP begin to shape new supply chains and test the impacts of the two countries on the regional trade patterns.