The EU region as a whole remains one of the world’s leading producers of textile and apparel (T&A). The EU’s T&A production value totaled EUR135.6 bn in 2019, down around 6% from a year ago (Note: Statistical Classification of Economic Activities or NACE, sectors C13, and C14). The EU’s T&A output value was divided almost equally between textile manufacturing (EUR69.4bn) and apparel manufacturing (EUR66.2bn).

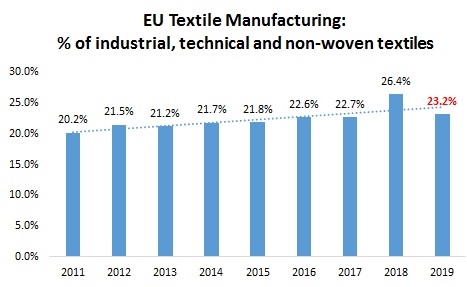

Regarding textile production, Southern and Western EU, where most developed EU members are located, such as Germany, France, and Italy, accounted for nearly 60% of EU’s textile manufacturing in 2020. Further, of EU countries’ total textile output, the share of non-woven and other technical textile products (NACE sectors C1395 and C1396) has increased from 20.2% in 2011 to 23.2% in 2019, which reflects the ongoing structural change of the sector.

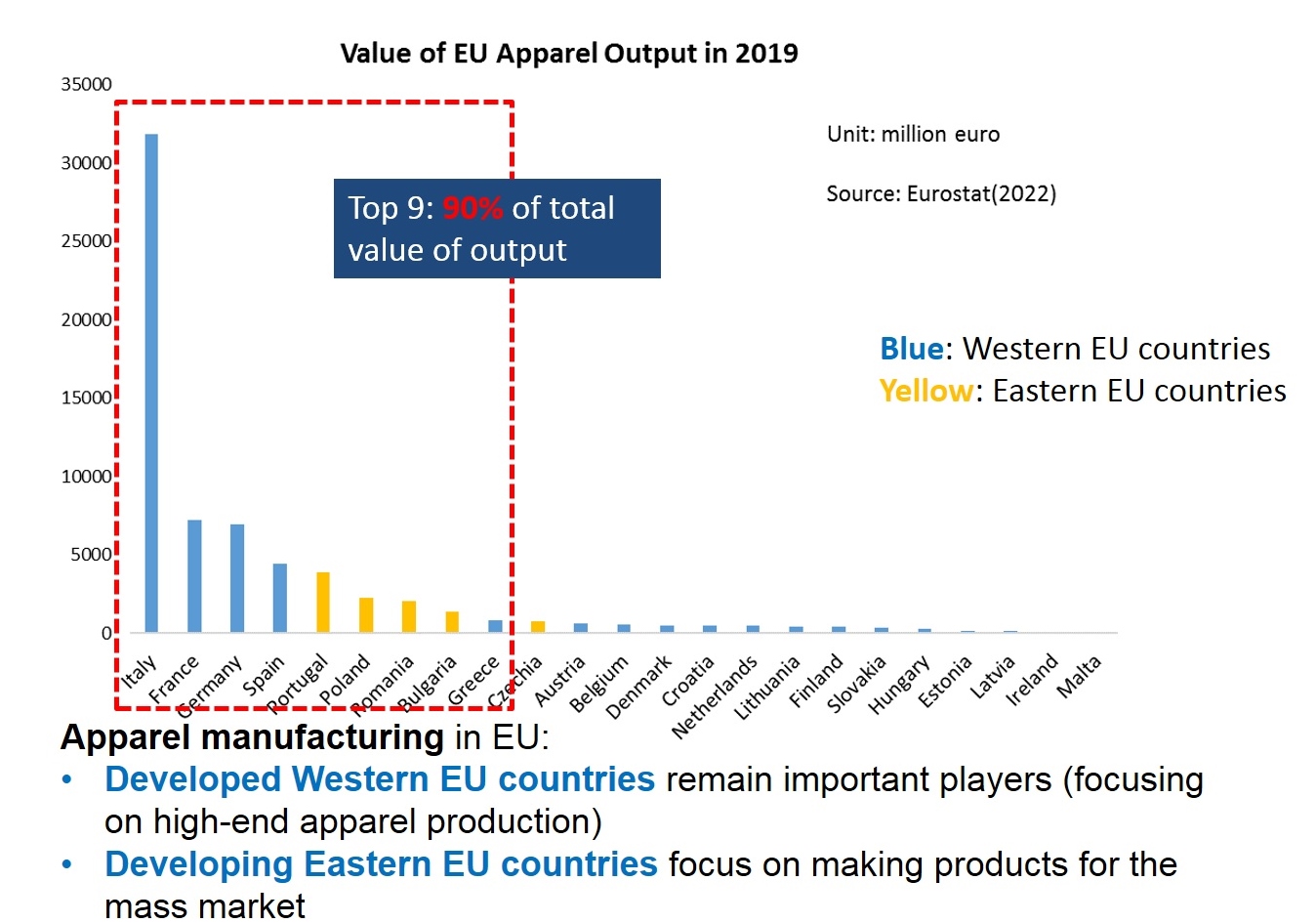

Apparel manufacturing in the EU includes two primary segments: one is the medium-priced products for consumption in the mass market, which are produced primarily by developing countries in Eastern and Southern Europe, such as Poland, Hungary, and Romania, where cheap labor is relatively abundant. The other category is the high-end luxury apparel produced by developed Western EU countries, such as Italy, UK, France, and Germany.

It is also interesting to note that in Western EU countries, labor only accounted for 20.3% of the total apparel production cost in 2019, which was substantially lower than 30.1% back in 2006. This change suggests that apparel manufacturing is becoming capital and technology-intensive in some developed Western EU countries—as companies are actively adopting automation technology in garment production.

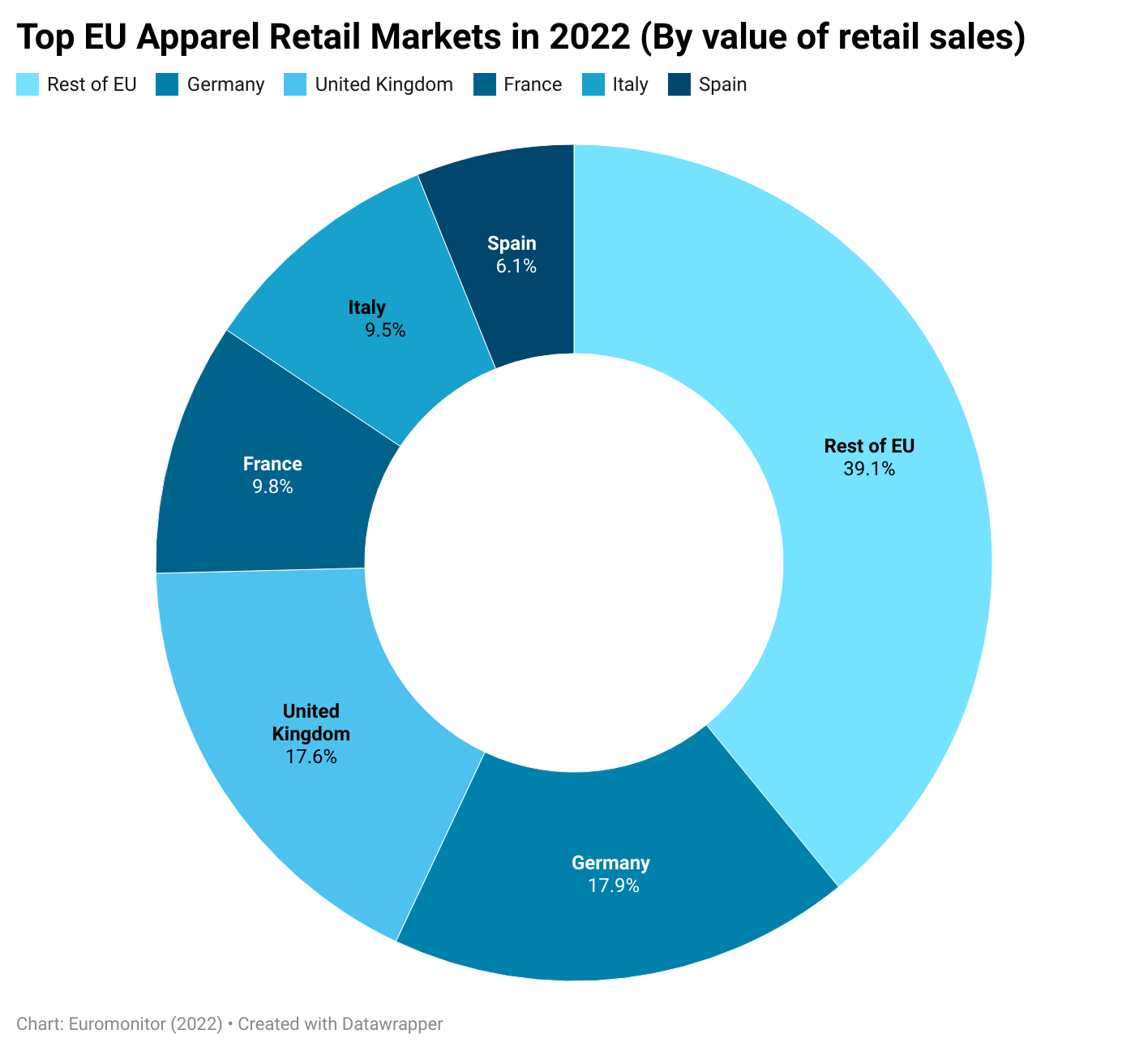

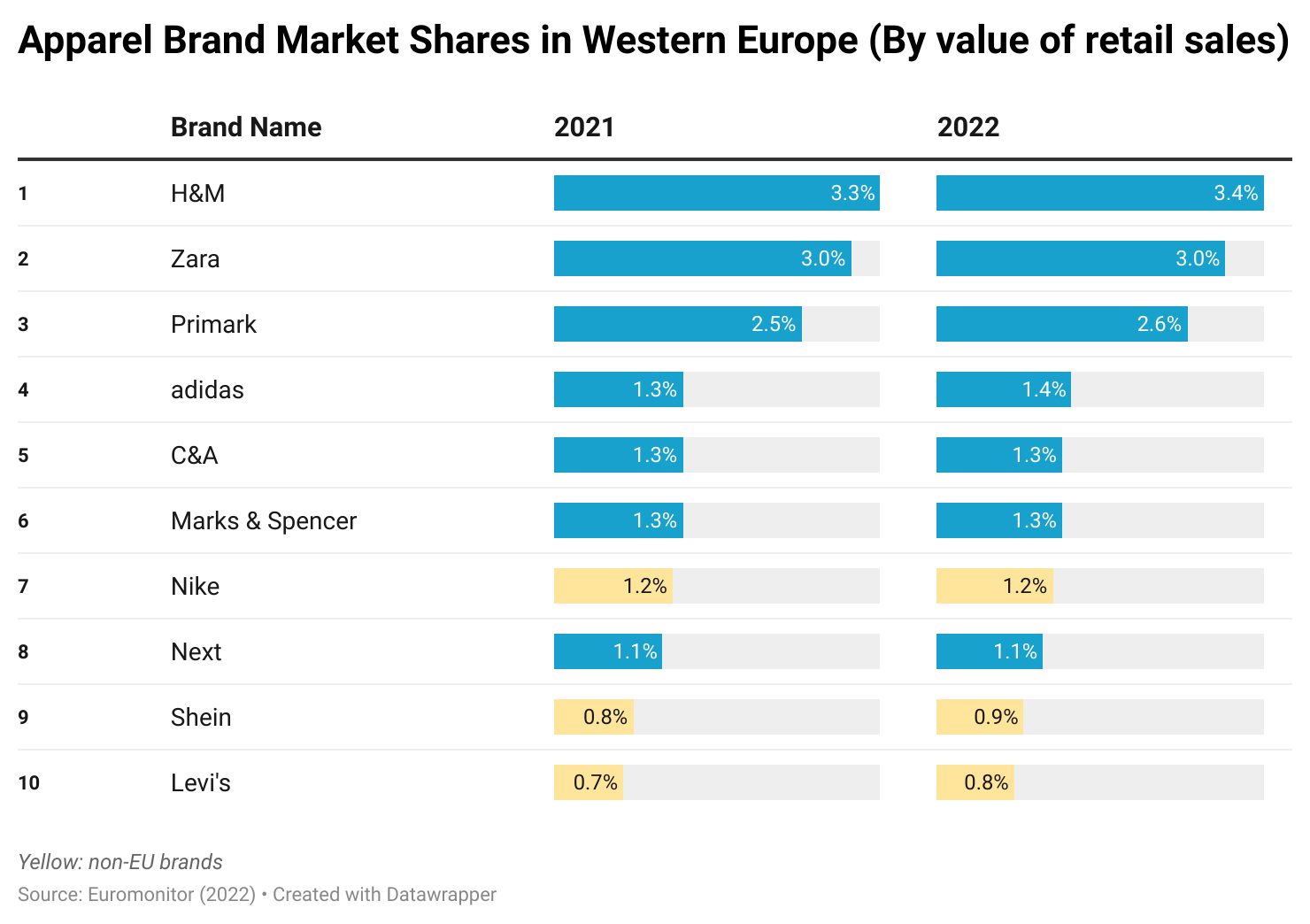

Because of their relatively high GDP per capita and the size of the population, Germany, Italy, the UK, France, and Spain accounted for nearly 60% of total apparel retail sales in the EU in 2021. Such a market structure has stayed stable over the past decade. Also, reflecting local consumers’ preference, EU apparel brands overall outperform non-EU brands in the EU retail market.

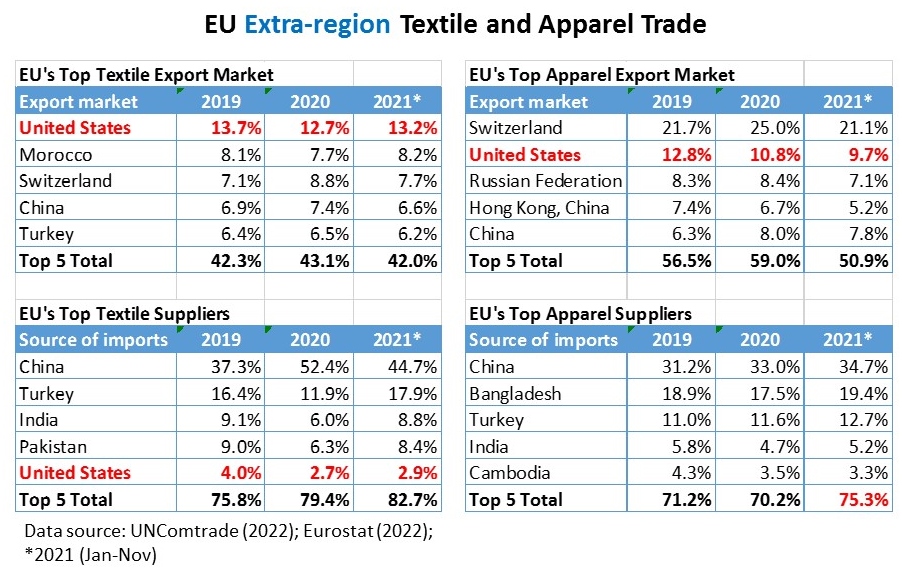

Intra-region trade is an essential feature of the EU’s textile and apparel industry. Despite the increasing pressure from cost-competitive Asian suppliers, statistics from UNComtrade show that of the EU region’s total textile imports in 2019, as much as 53.8% were in the category of intra-region trade. However, it could result from increased PPE imports from Asia, EU countries’ Intra-region trade% for textiles dropped to 40% in 2020.

Meanwhile, about one-third of EU countries’ apparel imports came from other EU members during 2019-2020. In comparison, close to 98% of apparel consumed in the United States was imported over the same period, of which more than 75% came from Asia (Eurostat, 2022; UNComtrade, 2022).

Regarding EU countries’ textile and apparel trade with non-EU members (i.e., extra-region trade), the United States remained one of the EU’s top export markets and a vital textile supplier (mainly for technical and industrial textiles). Meanwhile, Asian countries, led by China, and Bangladesh, served as the dominant apparel sourcing base outside the EU region for EU fashion brands and retailers. Turkey was another important apparel sourcing base for EU fashion companies. There is no sign that COVID-19 has shifted the trade pattern.

Additionally, Vietnam was EU’s sixth-largest extra-region apparel supplier in 2020 (after China, Bangladesh, Turkey, India, and Cambodia), accounting for 4% in value. The EU-Vietnam Free Trade Agreement which took effect in August 2020, could encourage more EU apparel sourcing from the country in the long run.

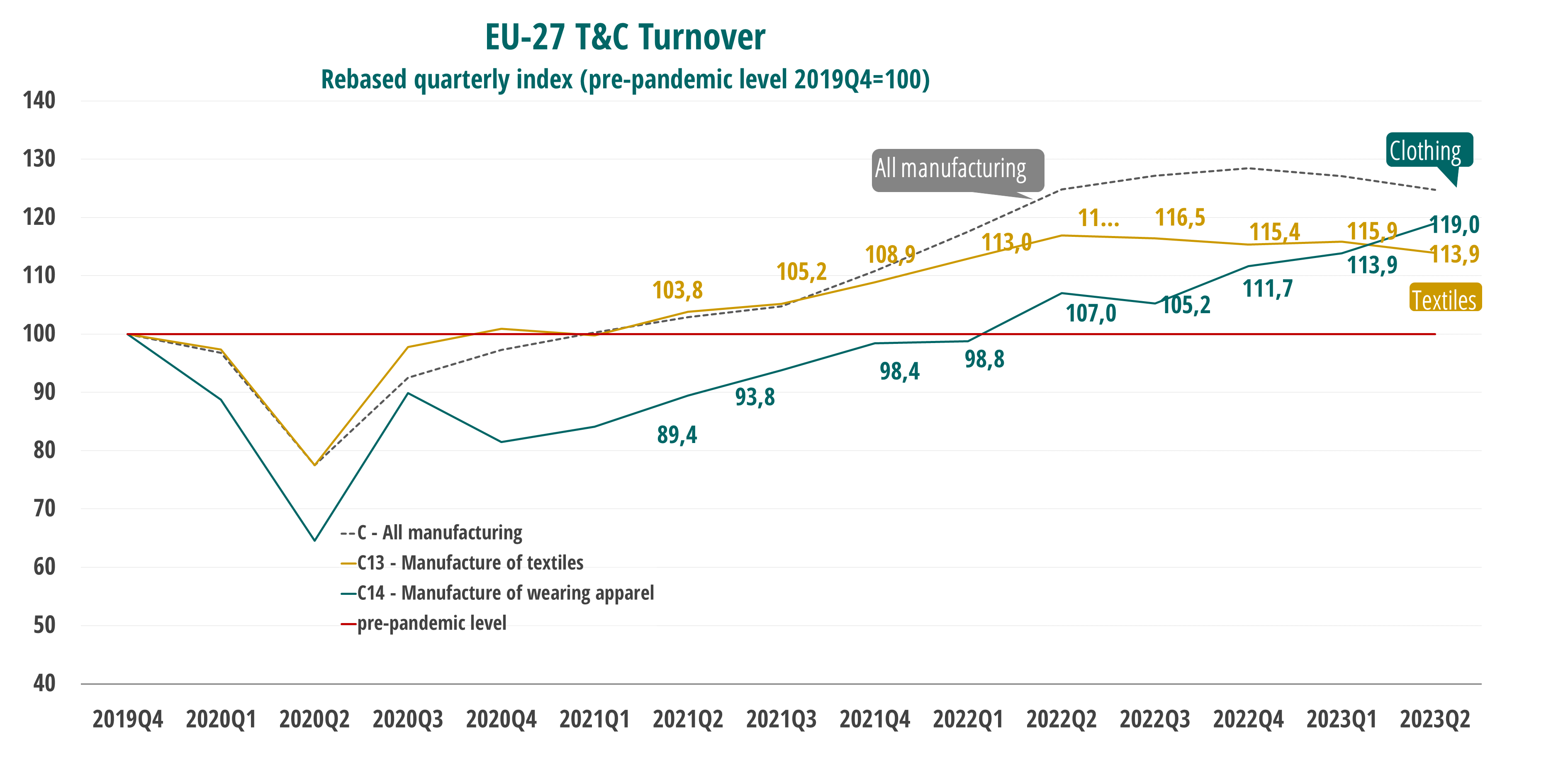

According to the European Apparel and Textile Federation (Euratex), the EU textile and apparel industry continued to recover from COVID-19. For example, the value of textile and apparel output has already reached its pre-pandemic level by the end of 2022. However, Euratex warns that the EU textile and apparel industry still faces significant challenges from a slowed economy, hiking energy costs as a result of the Russia-Ukraine war, and high inflation.

by Sheng Lu

Great article! The data presented did well to supplement your main points. When it comes to trade, specifically textile and apparel trade, many minds automatically think of the U.S., China, India, Bangladesh, etc. I feel like many individuals fail to analyze the unique role and state of the textile and apparel industry in Europe. Similar to other regions of the world, labor in apparel production typically resides in less developed countries. This is best exemplified by the significant decrease in labor cost between 2006 and 2009 in Western Europe, which indicates a shift towards more capital-intensive industries. Furthermore, the EU has a system called the Intra-region trade to reduce trade barriers amongst EU, which has a complete supply chain. Despite the convenience and benefits created by this network, I found it puzzling that the region’s trade % for textiles decreased 40% in 2020 given that we were in peak pandemic when PPE textiles were in high demand. Lastly, I found your description of the EU textile and apparel industry’s effect on other areas of the world important as the intra-trade system results in their main competitors being located in other places. Once again, this article was a satisfactory supplement to the information presented in the lecture as it demonstrated real world implications of the state of the EU textile and apparel industry.

You made some excellent points! The fact that the EU remains one of the world’s largest textile and apparel producers and exporters is often overlooked. Notably, many high-wage western EU countries continue to manufacture apparel products and they do not necessarily rely on fancy new technologies (you may think about the video in our lectures). However, the industry’s lack of labor force (especially the young generation) could be a long-term challenge.

After reading this article, I feel that the EU is often overlooked as one of the leading producers in the world for the textile and apparel industry. While Europe is home to many fashion capitals of the world, often European countries are overlooked for their production. There are two major categories; medium priced products produced in countries like Poland, Hungary and Romania, and high end luxury apparel produced in Germany, Italy, the UK and France. I also find the EU’s intra-region trade agreement interesting. Pre-pandemic, more than 50% of imports were between the EU, but due to increased PPE imports from Asia during the pandemic, this number dropped to 40%. I believe it is in the best interest of the EU to try to get these numbers back up in the next few years to stimulate their own economies.

This article does a great job explaining EU textile and apparel trade patterns. Apparel manufacturing in the EU is so large that it includes two primary segments. One segment is the medium-priced products for consumption in the mass market which are produced primarily by developing countries in Eastern and Southern Europe such as Poland, Hungary, and Romania, where cheap labor is relatively abundant. The other segment is the high-end luxury apparel produced by developed Western EU countries, such as Italy, UK, France, and Germany. In this article, we also see that there is a change of labor for the total apparel production cost in the EU region which is interesting. In 2019, labor only accounted for 20.3% of the total apparel production cost which was much lower than it was in 2006, as it was 30.1%. This change means that apparel manufacturing is becoming capital and technology-intensive in some developed Western EU countries as companies are actively adopting automation technology in garment production.

As stated in the article there has been a decreased labor costs, specifically labor accounted for 30% of total apparel production cost, while in recent years it only accounts for 20%. This is due to developed Western EU countries becoming capital and technology-intensive. As Italy, UK, France, and Germany continue to adopt automation technology in garment production, I am interested to see how it is incorporated into and/or affects the luxury market in this region. The luxury market thrives off of their reputation and craftsmanship, will technology tarnish that?

This is a great article and many great points are made supported by data. The garment industry all over the world, especially since the start of COVID-19 has been transforming drastically. The EU region still holds a very important role in the industry. It is vital to keep a steady relationship and connection between the United States and Europe to ensure more stability and certainty in apparel manufacturing. I really like how the article acknowledges the two primary segments necessary to keep Europe and the US at such high altitudes in comparison to many other places around the world.

The factors that support the EU-intra reign trade textiles are that the EU’s single market strategy has given members with important financial incentives to source textiles and garments from inside the zone. It provides for free movement of goods between EU nations, but EU-based businesses must pay an average tariff rate of 6.5 percent for textiles and 11.8 percent for garments imported from outside the EU. There are two types of apparel production in the EU. One is mass-market medium-priced items made mostly in emerging nations in Eastern and Southern Europe, such as Poland, Hungary, and Romania, where low-wage labor is relatively plentiful. The high-end luxury clothes manufactured by developed Western EU nations such as Italy, the United Kingdom, France, and Germany are the second group. I was also unaware that they were a major producer of T&A. Asian countries have traditionally dominated manufacturing in my mind.

The EU focusing on both high-end textile and apparel manufacturing seems to be a beneficial practice for its supply chain when comparing these manufacturing processes with those of the Western Hemispheres. The Western Hemisphere has shown struggles when it comes to sourcing and/or manufacturing high-end textile and apparel products because none of the countries a part of the CAFTA-DR free trade agreement have the ability to produce such goods. This creates a roadblock for opportunities in the textile and apparel industry in the US, whereas the EU does not have to worry so much about this. Having regional access to these materials and apparel products is a huge help to its supply chain and allows a more diverse variety of apparel products for consumers. The EU shows great advancements in technology for the textile and apparel industry, such as 3D printing software and France and high-tech machinery for manufacturing fashion products. On the other hand, about 80% of apparel imports from the CAFTA-DR region are basic apparel pieces, leaving little room for a diversity of goods and fewer options for consumers, which can be bad for business. In my opinion, I believe that the US should focus more on creating high-tech machinery and solutions to their lack of product variety. If the US began to focus more on this, their textile and apparel industry could improve greatly and allow for better and more business. It would be able to export a wider selection of goods, including high-end apparel, if there was the ability to produce them efficiently, leading to possible interest from other regional supply chains to get involved more heavily with the Western Hemisphere supply chain. One last thought – US fashion brands and retailers would benefit greatly because if the US began implementing high-tech machinery in their production processes and therefore offering more goods then those brands would be able to source from within their region, taking advantage of duty-free imports. Retailers and brands would then see an increase in profit because they would be spending less on imports with no tariffs or taxes and they could attract more consumers with a wider variety of goods.

In the European Union’s Apparel and Textile Industry, the trade patterns show that it’s one of the world’s leading producers of clothes. Having reasonably priced products for consumption and a stable market is what has made the apparel and textile industry in the EU so successful today. The intra-region trade system helps to reduce the trade barriers in the European Union. In the Western European Union countries labor decreased from 30.1% to 20.3%. The European Union is focused on capital & technology intensive apparel manufacturing to produce these garments. In the Western European Union countries labor decreased from 30.1% to 20.3%. The bar graphs at the top of this article show from 2019 the decrease in labor and value output in the fashion industry whereas the employment and number of enterprises in textiles and apparel have increased.

One statistic that stuck out to me is in Western EU countries; labor only accounted for 20.3% of the total apparel production cost in 2019, which was substantially lower than 30.1% back in 2006. This is obviously due to advancements in technology and the rising number of smart factories. I am interested to see how this percentage lowers in the future and would not be surprised if it is cut in half in the next 5 years.

The combination of developing countries like Poland, Hungary, and Romania producing medium-priced, labor-intensive products while higher end products are made by Italy, France, Germany, and the UK supports the EU intra-region trade. By utilizing the resources they have within Europe, the EU trade region reaps the benefits it has within itself and has no real need to invest sourcing and production elsewhere. The high amount of apparel sales of 60% throughout Europe’s developed countries, like France, the UK, Germany, Spain, and Italy, also supports the EU-intra region for textiles and apparel. Seeing such a high number of sales in these countries further emphasizes Europe’s ability to supply themselves with the resources they need to be a successful T&A sector, without any outside help from other countries.

The whole process of intra-region trade is very intriguing to me. It takes ideas we have learned and focuses them on a smaller scale. As with all trade, economic development plays the biggest role. Developed Western EU countries focus on high-end apparel production while medium-priced products for the mass-market are manufactured in developing countries in eastern and southern Europe. This is because those developing countries (i.e. Poland, Hungary, etc) have cheaper, more abundant labor that can produce garments at a cheaper cost. These countries also have less access to capital and technology, meaning their textiles are not of the highest of quality, giving them the cheaper price to the mass market. The developed countries (i.e. Italy, France, etc) have the means (capital and technology) to produce products of higher quality, leading to higher costs, creating a high-end market. Overall, the European Union is comparatively independent when it comes to their apparel industry. Nearly half of apparel consumed in Europe are made in Europe, creating the reliance on intra-regional trade we see. I greatly admire this kind of interdependence and true ability to manufacture and finish apparel closer to home.