Founded in Sweden in 1947, H&M is widely regarded as a leading fast-fashion retailer, known for offering a high volume of trend-driven products at competitive prices. To better understand H&M’s fast fashion business model and its implications for the company’s sourcing practices, this study analyzed H&M’s detailed factory list published in February 2026, which includes 1,455 entries.

The factories on the list were classified using information from the “Product Type” and “Factory Type” columns. Specifically, Apparel suppliers are factories that produce finished garments (e.g., denim, knitwear, woven apparel) and are listed as “Manufacturing unit”. Factories that did not provide product information were excluded from the analysis.

Key findings:

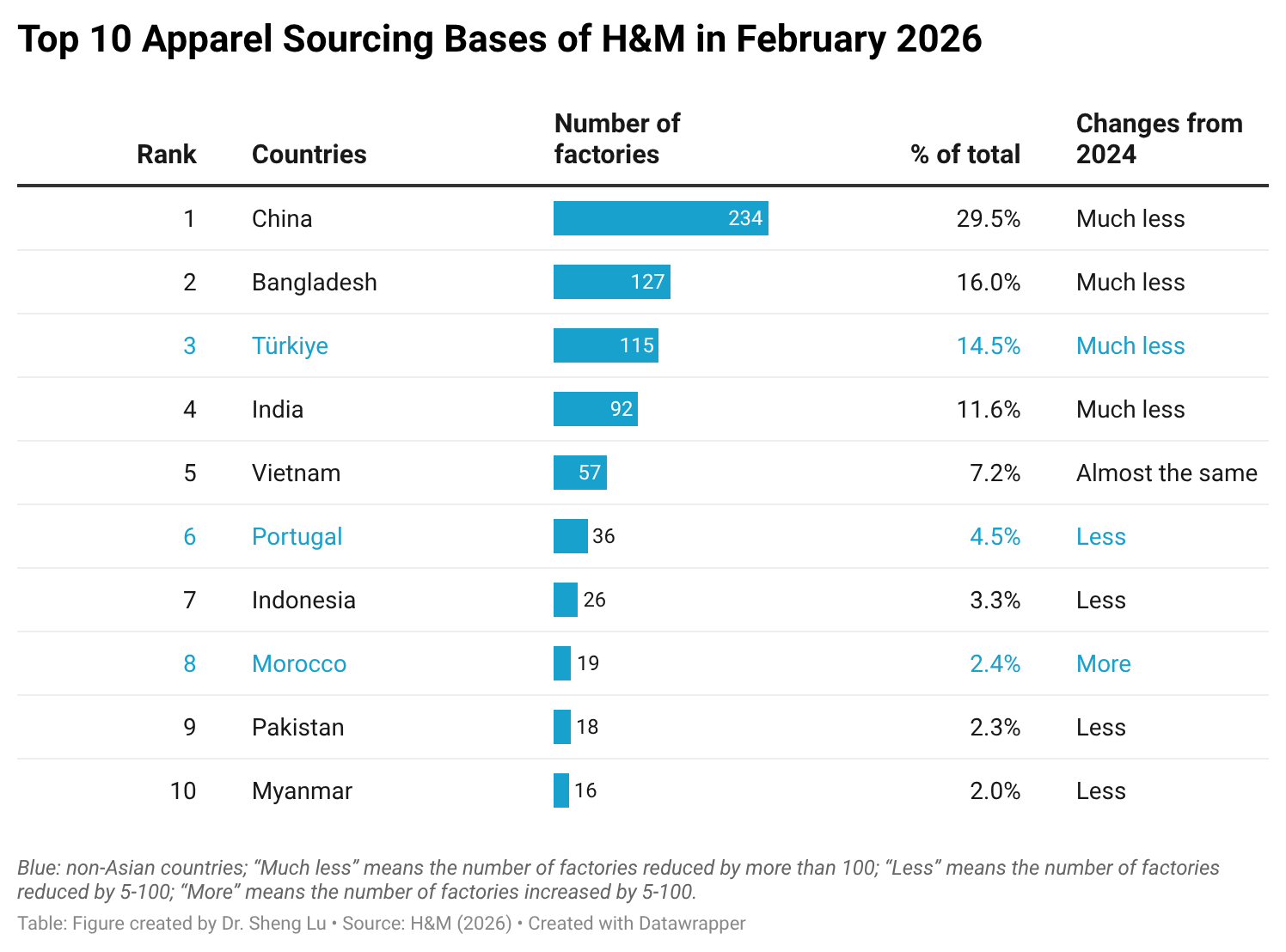

First, like most other leading apparel brands and retailers, H&M utilized a geographically diverse sourcing base. Specifically, as of February 2026, H&M sourced apparel from nearly 800 factories across 23 countries and about 550 factories producing textile raw materials in 15 countries.

However, compared to its 2024 sourcing base, H&M seemed to have consolidated the number of factories it sourced from.

Notably, H&M appears to maintain long-term relationships with its suppliers. Among the nearly 800 contracted apparel factories, 314 (nearly 40%) have worked with H&M for more than 10 years, and another 126 for 6–10 years. Only 261 factories (about 33%) have fewer than 3 years of relationship. According to H&M’s website, it “onboard new suppliers or factories and, occasionally, phase them out according to our business needs.”

Second, while Asia remains H&M’s largest apparel sourcing base, other regions, particularly Europe and Africa, also play a critical role. As of February 2026, seven of the top ten countries with the most contracted factories for H&M were located in Asia. However, Türkiye, Portugal, and Morocco also ranked among the top ten. Compared to U.S. fashion companies, which tend to rely more heavily on Asian sourcing, these countries generally play a more limited role in their sourcing portfolios, highlighting H&M’s relatively greater emphasis on regional diversification and proximity sourcing. In particular, sourcing from Europe and Africa can provide H&M with shorter lead times and greater responsiveness to EU market demand, which aligns well with the speed-to-market requirements of its fast fashion business model.

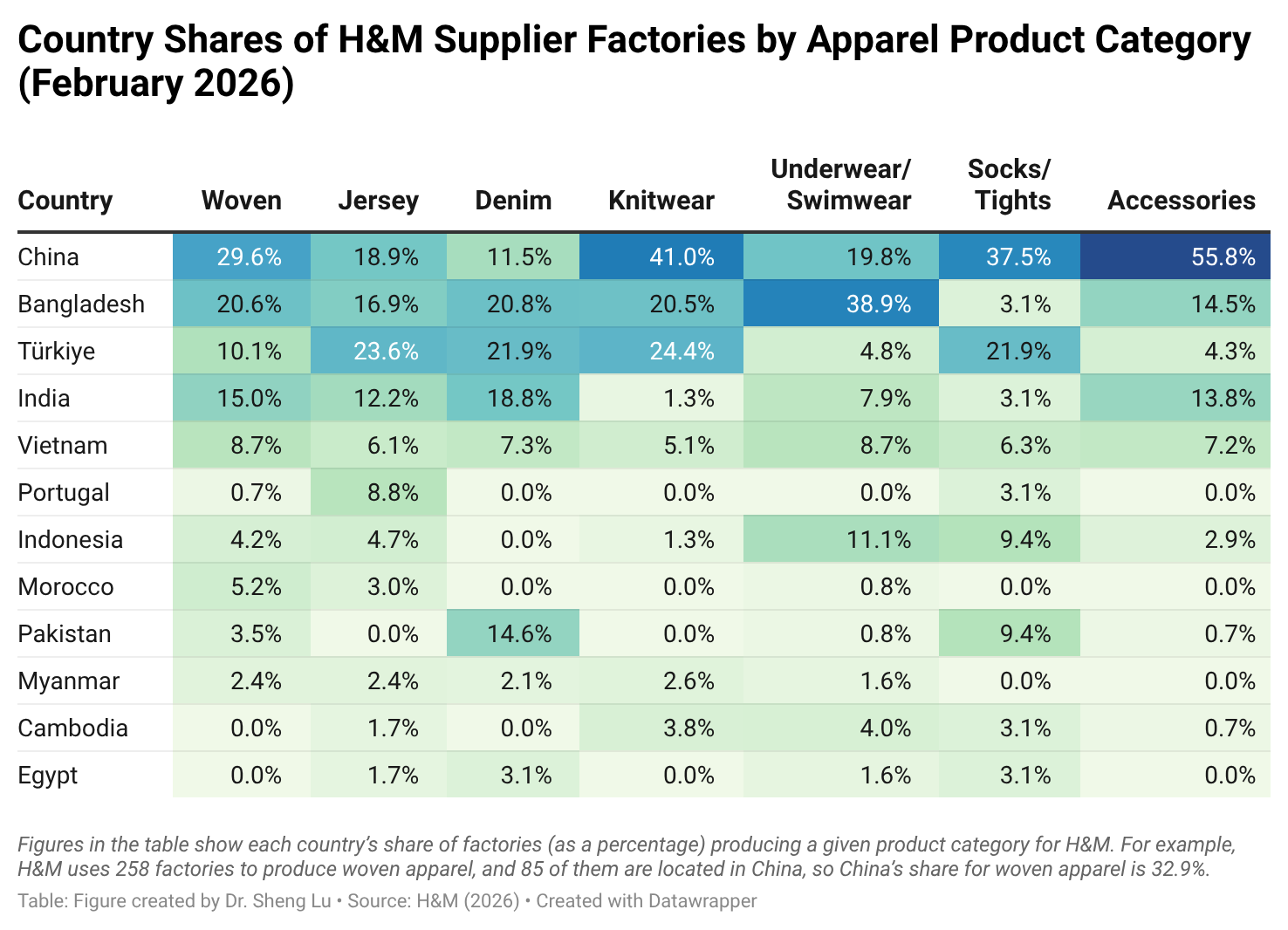

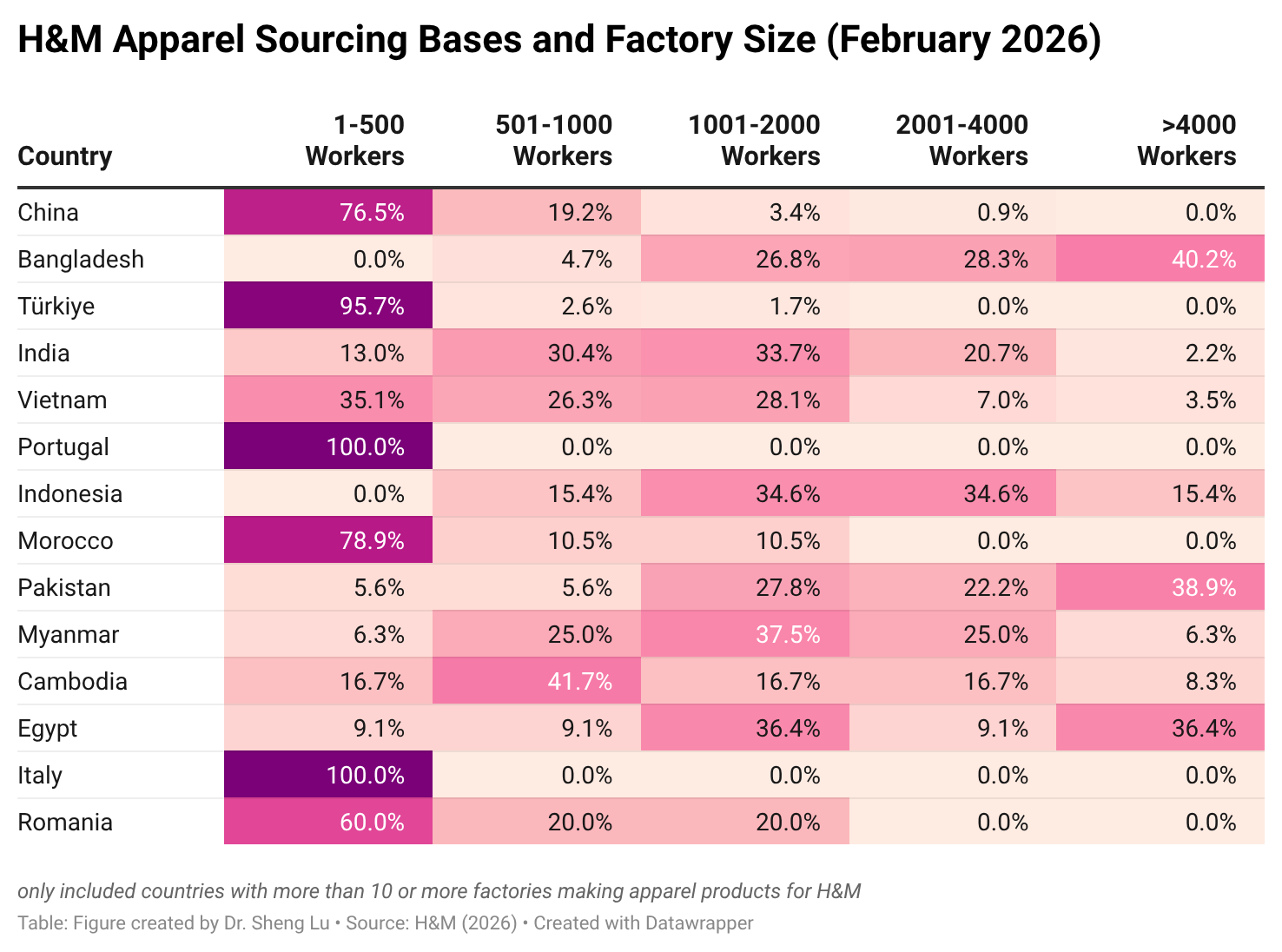

Third, at the country level, in terms of the number of contracted factories, China remains H&M’s single largest apparel sourcing destination (over 230 factories, or 29.5%) as of February 2026. H&M also sourced the widest range of apparel product categories from its China-based factories, covering woven apparel (85 factories), jersey (56 factories), knitwear (32 factories), and denim (11 factories). In other words, China is one of the few countries that can make almost all types of products for H&M. In comparison, H&M was inclined to source more narrow product categories from other top-supplying countries, such as Türkiye for jersey, denim and knitwear; India for denim, Indonesia for underwear/swimwear; and Pakistan for denim and socks. This finding aligns with recent studies indicating that Western fashion companies commonly regard China as highly competitive for its product variety, which is difficult for other countries to match.

It is also noteworthy that most of H&M’s contracted factories in China are relatively small, with over 76% employing fewer than 500 workers. This pattern is consistent with China’s role in supplying more variety-driven orders with small- to medium-sized minimum order quantities (MOQs). In contrast, H&M’s contracted factories in other major Asian sourcing countries, such as Bangladesh, Pakistan, and Indonesia, are more concentrated in large-scale production, typically employing over 1,000 workers. Notably, 41% of H&M’s contracted factories in Bangladesh and nearly 40% in Pakistan have more than 4,000 workers, indicating their role in producing high-volume orders for the company.

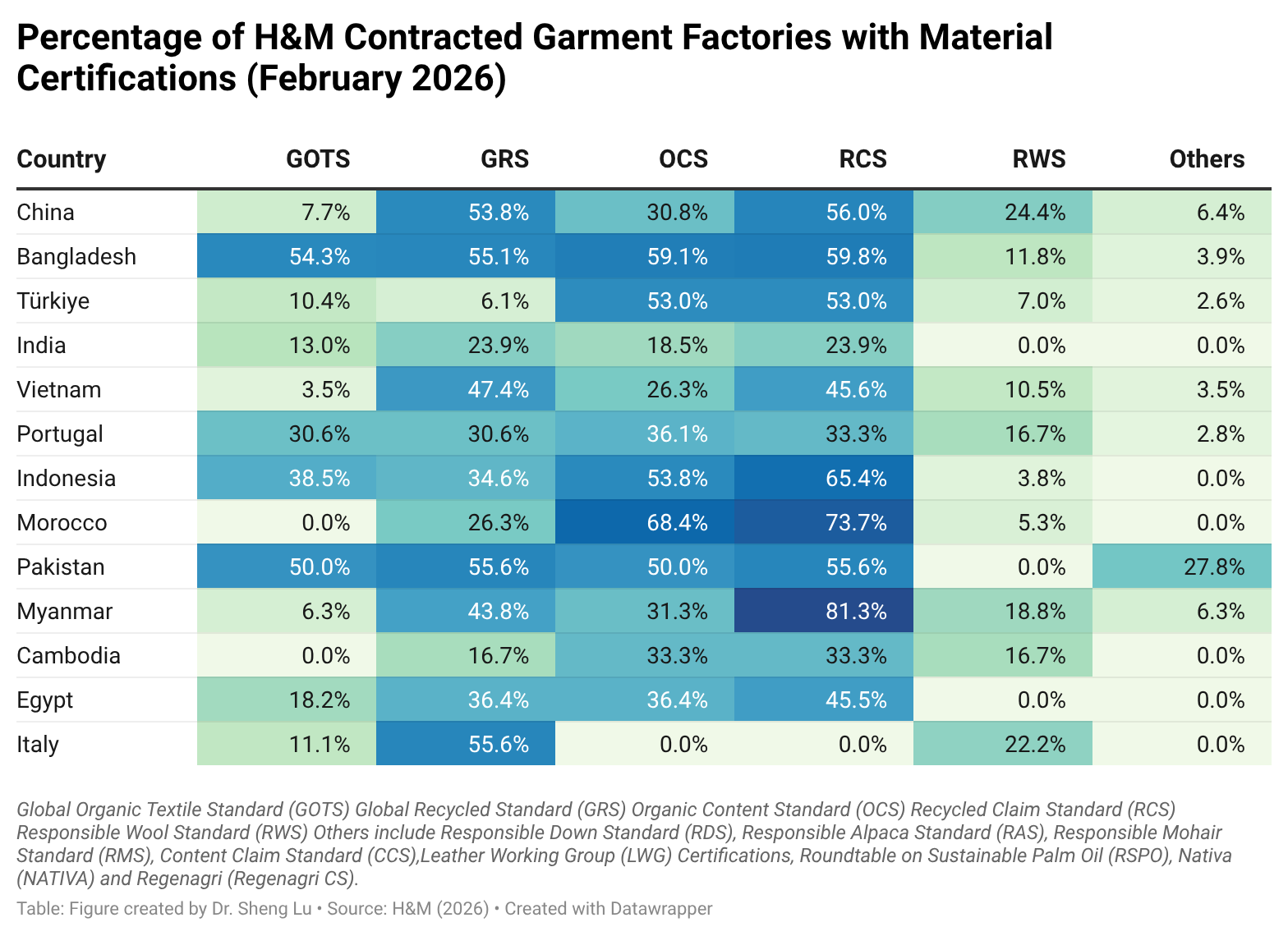

Additionally, H&M contracted garment factories have commonly received material certification, led by those related to organic and recycled content. For example, as of February 2026, among H&M’s contracted apparel factories, 49.6% held the Recycled Claim Standard (RCS), followed by Global Recycled Standard, GRS (39%) and Organic Content Standard, OCS (38.5%). The results align with H&M’s stated material goals of increasing the use of recycled or sustainably sourced materials in commercial products to 100% by 2030, including reaching 50% recycled materials. Most of H&M’s top apparel-supplying countries already have 50–70% of factories holding at least one type of material-related certification. The ability to obtain such certifications is increasingly becoming a baseline expectation for H&M suppliers.

by Sheng Lu

Additional reading: H&M’s Evolving Sourcing Map Speaks to Global Supply Chain Shifts (Sourcing Journal, April 2026)