The EU Commission released its negotiating positions for the textile and apparel sector in the Trans-Atlantic Trade and Investment Partnership (T-TIP) on May 14, 2014. The position paper outlines a few areas that the EU Commission says it would include in the T-TIP negotiation with the United States:

- Labeling requirements for textile & apparel and footwear products

- convergence and/or harmonization of approaches to guarantee product safety and consumer protection

- standards approximation

Earlier this year, USTR also released its negotiating objectives for the T-TIP. Specifically for the textile and apparel sector, USTR will “seek to obtain fully reciprocal access to the EU market for U.S. textile and apparel products, supported by effective and efficient customs cooperation and other rules to facilitate U.S.-EU trade in textiles and apparel.” USTR holds the positive view that “eliminating the remaining duties on our exports will create new opportunities for integration into European supply chains and to sell high-quality “made-in-USA” garments to European consumers. Enhanced U.S.-EU customs cooperation will also help ensure that non-qualifying textiles and apparel from third countries are not being imported into the United States under T-TIP.

However, T-TIP negotiation somehow is under the shadow of the Trans-Pacific Partnership (TPP), another free trade agreement currently under negotiation among the United States and other eleven countries in the Asia Pacific region. As reported by the Inside US Trade, the National Council of Textile Organizations (NCTO) holds the view that TTP and T-TIP negotiation should be dealt with “sequentially”. NCTO would like to avoid a situation where the US makes a concession on textiles and apparel to the EU in T-TIP that goes beyond the US offer to Vietnam in TPP, causing Vietnam to demand the same concession in the TPP talks.

One of the most difficult issues on textiles and apparel in T-TIP will be the rule of origin, given that the U.S. and EU have taken vastly different approaches on this issue in their existing preferential trade agreements. The EU rule of origin for apparel essentially consists of two different rules — one that applies generally and one that can be used as an exception. Under the general rule, an apparel item qualifies as originating if it has undergone at least two “substantial processes” in the EU. In general, weaving the yarn into fabric and finishing the fabric are considered substantial operations. Under this scheme, EU manufacturers can use non-originating yarn to make qualifying apparel as long as that yarn is woven into fabric in the EU and also finished there. As a result, this part of the EU rule is sometimes referred to in the United States as the equivalent of a “fabric-forward” rule, since it usually requires all components of the item, starting with the fabric, to be made in the region.

The second part of the EU rule — which functions as an exception — essentially applies a more liberal rule for certain apparel and textile items. These items can qualify for tariff benefits even if only the printing or other downstream operations occur in the EU. Specifically, under this exception, a textile or apparel item that is made from non-originating fabric but for which the printing occurs in the EU can qualify for tariff benefits if the non-originating part of the item is no more than 47.5 percent of the value of the final product. EU manufacturers of printed bed sheets often take advantage of this printing exception (Inside US Trade).

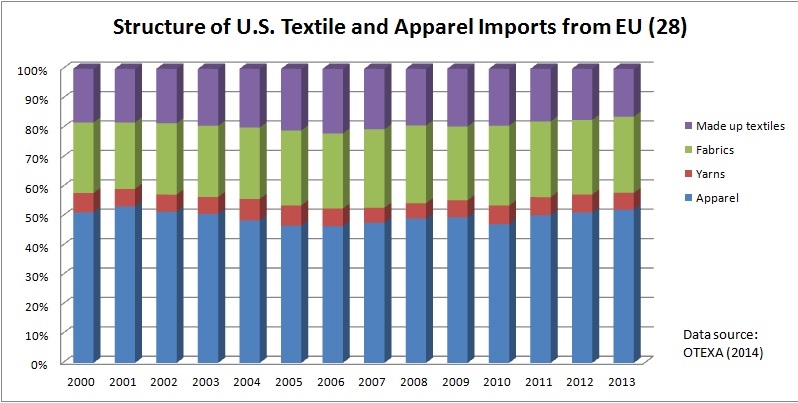

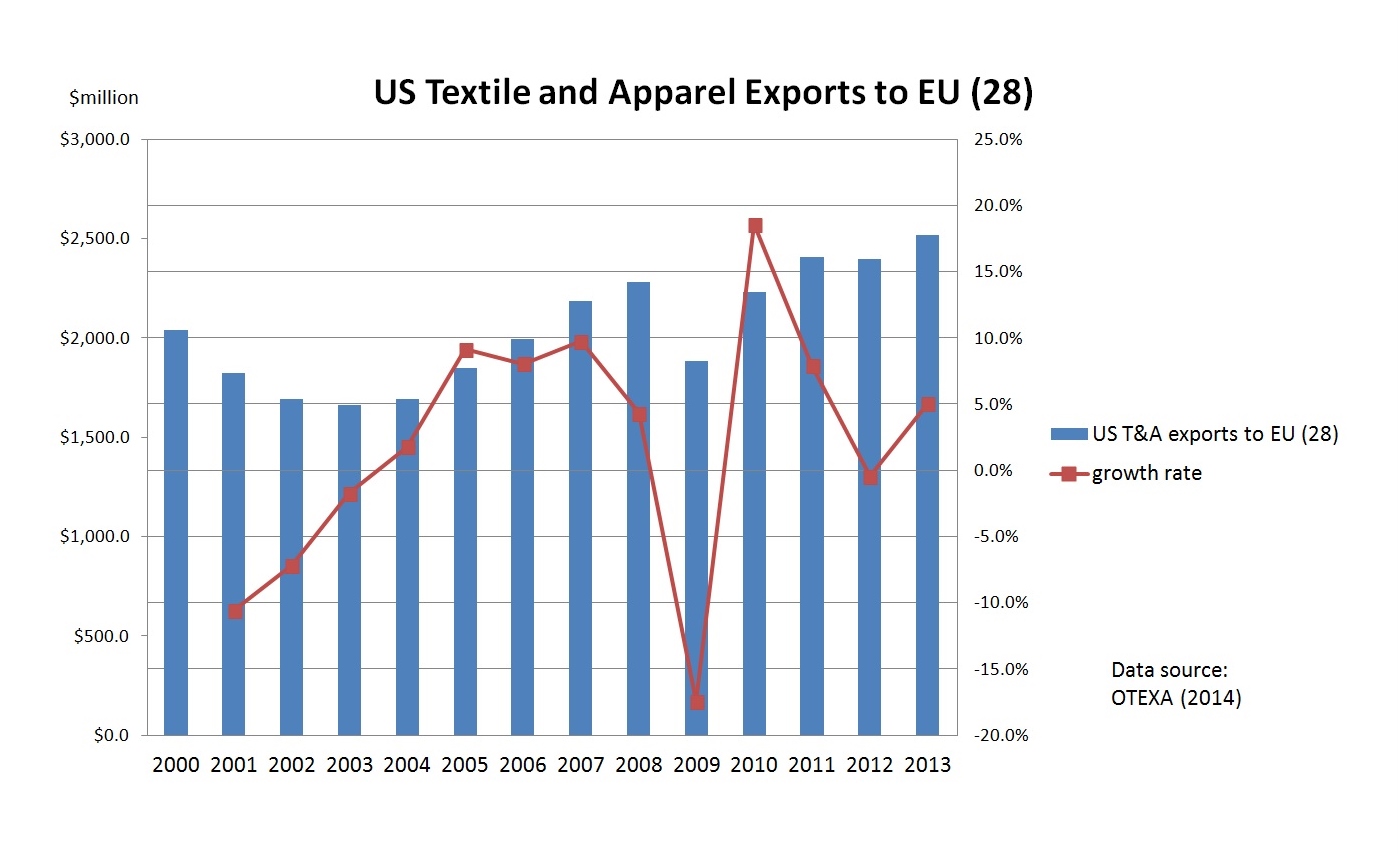

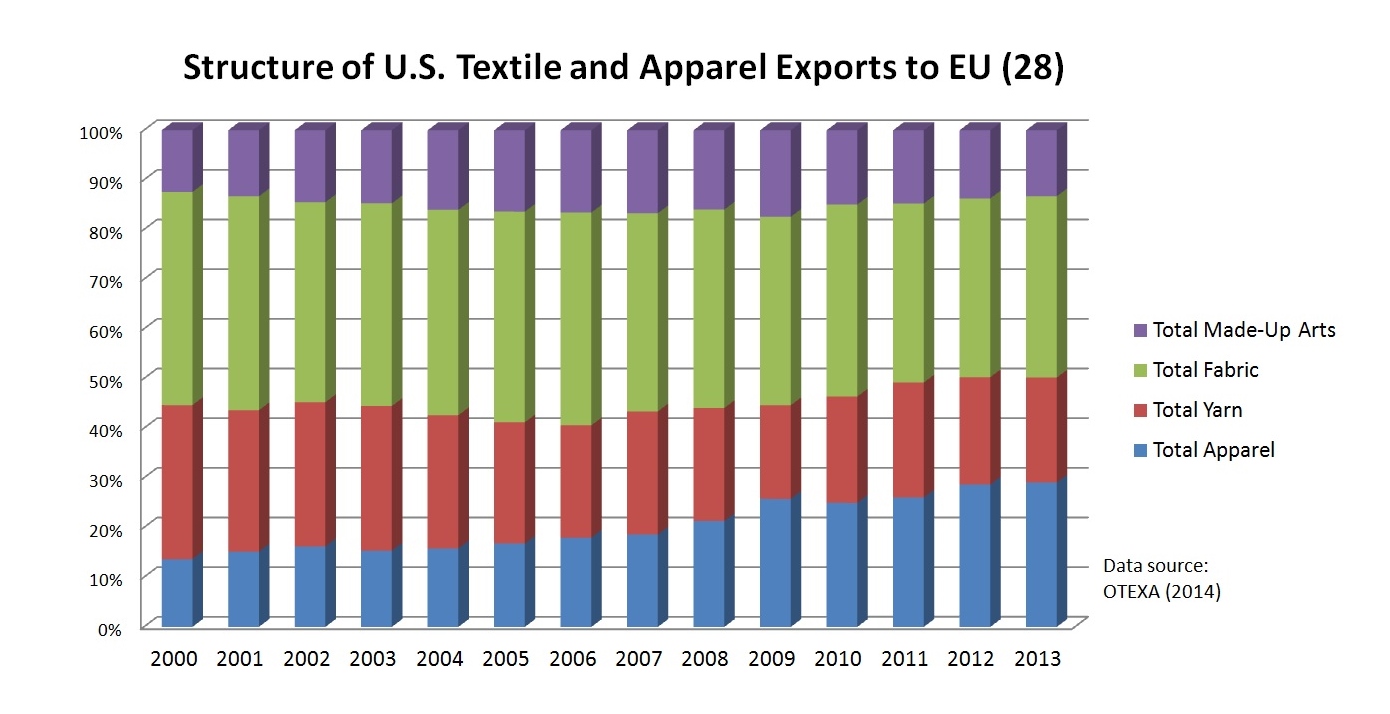

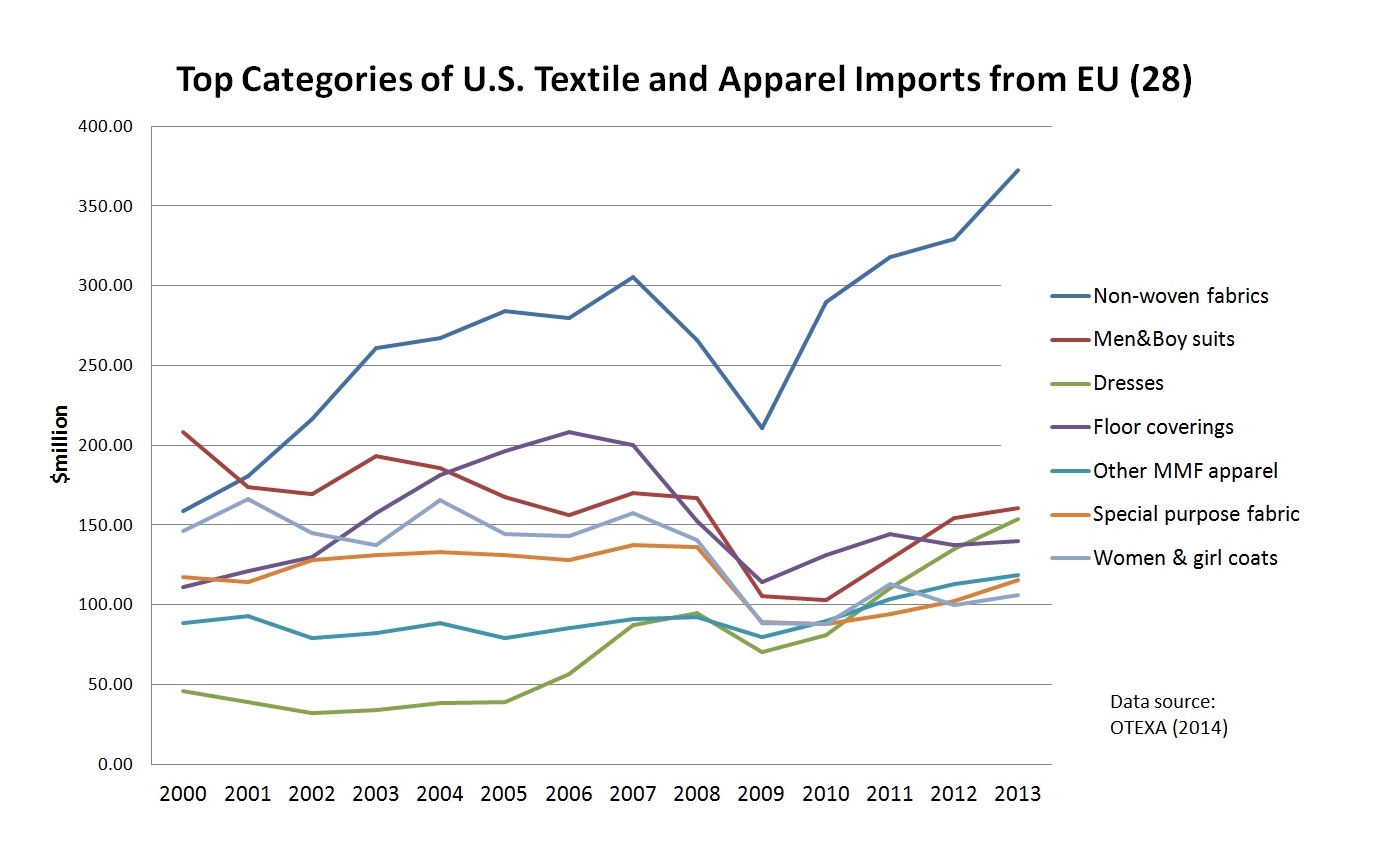

Latest data from OTEXA shows that in 2013, U.S. textile and apparel imports from EU(28) totaled $4 billion, among which 52% were apparel products and 48% were textiles. Top product categories of U.S. textile and apparel imports from EU include non-woven fabrics, men&boys’ suits, dresses, floor coverings, other man-made fiber apparel, special purpose fabrics and women & girls’ coats. In comparison, U.S. textile and apparel exports to EU(28) reached $2.5 billion in 2013, among which only 29% were apparel products and 71% were textiles. Top product categories of U.S. textile and apparel exports to EU include specialty & industrial fabrics, felts & other non-woven fabrics, filament yarns, other made-up textile articles, waste & tow staples, women & girls slacks, shorts and pants as well as spun yarns & thread.