Latest statistics released by the American Apparel and Footwear Association (AAFA) indicate several trends in the U.S. apparel industry:

- First, the retail market is gradually recovering. According to AAFA, on average, every American spent $907 on clothing (or purchased 64 garments) in 2013. Although this figure is still less than the one before the 2008 financial crisis, it is the highest level since 2012.

- Second, “Made in USA” is growing but US consumers still rely on imports. Data from AAFA shows that US apparel production increased 6.2 percent from 2012 to 2013, accounting for 2.55% share of U.S. apparel market. However, nearly 98% of apparel consumed in the US were still imports in 2013.

- Third, China remains the top apparel supplier to the United States. Despite the concerns about the rising production cost in China, latest data from OTEXA shows that, in 2014 (January to November) China still accounted for 42.5% of US apparel imports in terms of quantity and 39.1% in terms of value–almost the highest level in history. These two numbers were 41.7% and 39.9% a year earlier. On the other hand, Vietnam’s market share has reached 9.3% (by value) and 10.7% (by quantity) in 2014 (January to November), about ¼ of China’s exports to the United States.

- Fourth, job market reflects continuous shift of the apparel industry. According to AAFA, among the total 2.8 million workers directly employed by the US apparel industry in 2013, only 5% were in the manufacturing sector, 5% were in the wholesaling sector and as many as 90% were working for retailers. However, within the apparel retail sector, total employment by the department stores is quickly shrinking—dropped 7.6 percent from 2012 to 2013 and cumulatively 21.3 percent from 1998 to 2013. At the same time, specialty clothing stores and sporting goods stores are hiring more people: 13.8% and 64.5% increase of employment from 1998 to 2013 respectively. The contrasting employment trend reflects the changing nature of the U.S. apparel retail market and the channels through which U.S. consumers purchase clothing.

- Fifth, US consumers are paying higher taxes on imported clothing. Calculated by AAFA, while the overall U.S. imports were only charged by a 1.4% tariff rate, the effective duty rate on all apparel imports rose to 13.6% in 2013. The higher effective duty rate may be caused by the fact that less apparel were imported utilizing free trade agreement or trade preference programs.

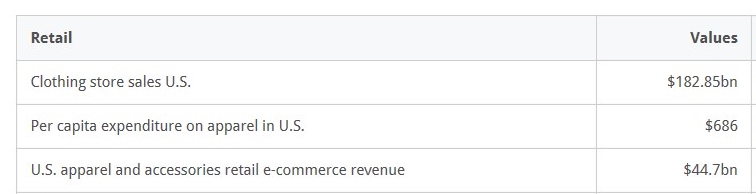

Appendix: Facts on the US Apparel Market in 2012

Data Source: http://www.statista.com/