Key findings:

1. The garment industry matters significantly to Cambodia, both economically, and socially. As of 2019, as much as 70% of Cambodia’s merchandise exports were apparel items. Likewise, around one-third of Cambodia’s manufacturing output currently comes from the garment sector alone. Further, as of 2016, the garment industry in Cambodia employed nearly 928,600 workers (almost 79% were female), an increase of 239% from 2007.

2. Cambodia’s apparel exports have enjoyed steady growth in recent decades, reaching US$7.83 billion in 2018 – a jump of 256% from US$2.2 billion in 2005. Yet, it faces several major challenges:

- Due to limited production techniques and capital availability, apparel producers in Cambodia are still mostly engaged in cut-make-trim (CMT) activities, meaning they rely heavily on imported textile raw material and are only able to make a marginal profit based on low-value-added sewing work.

- Cambodia’s apparel exports are highly concentrated on the EU and the US markets, which together accounted for 73.4% of the country’s total garment exports in 2019.

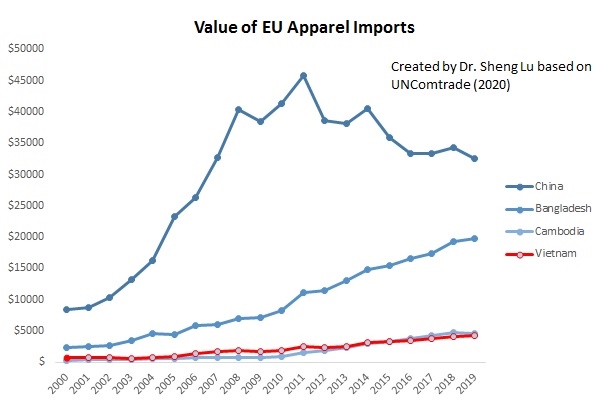

- Cambodia is facing intense competition in its main apparel export markets—there has been little growth in Cambodia’s share of EU and US apparel imports over the past two decades, remaining as low as 3% as of 2019.

3. Cambodia has benefited significantly from the EU Everything But Arms (EBA) program. Established in 2001, the EBA trade initiative provides least developed countries (LDCs), such as Cambodia, with duty-free and quota-free access to the vast EU market for all products except weapons and ammunition. Like other EBA beneficiary countries, the majority (around 95%) of Cambodia’s apparel exports to the EU currently claim the duty- and quota-free EBA benefits.

4. Out of concerns over Cambodia’s “serious and systematic violations of the human rights principles enshrined in the International Covenant on Civil and Political Rights,” the European Commission on 12 February 2020 formally announced the withdrawal of part of the tariff preferences granted to Cambodia under the EBA program. Starting from 12 August 2020, a select group of Cambodia’s apparel exports to the EU, together with all travel goods, sugar, and some footwear will be subject to the EU’s Most-Favored-Nation (MFN) tariff rat, which were at the rate of 11.5% on average for apparel items in 2019.

5. Even the partial suspension of Cambodia’s EBA eligibility could result in significant and lasting negative impacts on its apparel exports to the EU:

- The apparel items directly affected by the EBA suspension accounted for around 15% of the value of Cambodia’s total apparel exports to the EU in 2019. For those apparel categories directly targeted by the EBA suspension, EU fashion brands and retailers may quickly shift sourcing orders from Cambodia to other supplying countries to avoid paying the additional tariffs.

- Social responsibility is being given more weight in fashion companies’ sourcing decisions. This means even those apparel items not directly targeted by the EU EBA suspension could face widespread order cancellations as sourcing from Cambodia is deemed to involve higher social compliance risks. In a worse but possible scenario, Cambodia’s apparel exports to the whole world could be under threat as many EU fashion brands and retailers operate globally and adopt a unified ethical standard and code of conduct for apparel sourcing across different markets.

- Additionally, the timing cannot be worse: Due to the devastating hit by Covid-19, as of April 2020, Cambodia had reported nearly 130 garment factory closures and more than 100,000 workers laid off. These numbers may increase further as the effect of the pandemic continue to unfold.

Further reading: Abby Edge and Sheng Lu (2020). How will EU trade curb affect Cambodia’s apparel industry? Just-Style.

Discussion questions:

- What you would suggest to the Cambodian government or garment factories there to mitigate the negative impacts of the EU EBA suspension?

- Why or why not the EU should reconsider its decision to partially suspend Cambodia’s EBA eligibility because of Covid-19?

- If you were fashion brands and retailers that source from Cambodia, what would you do?