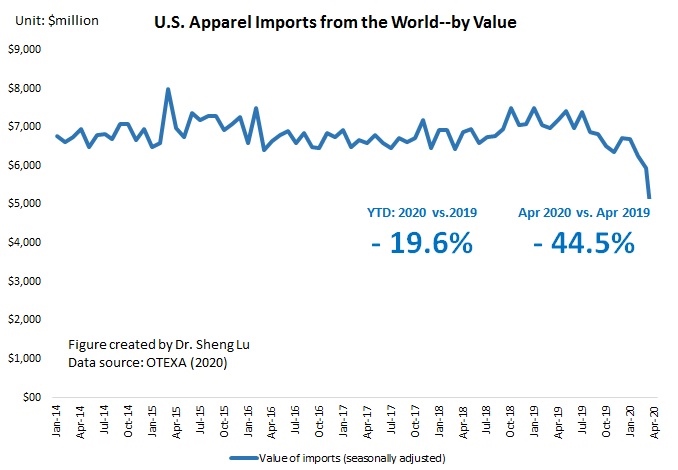

The latest statistics from the Office of Textiles and Apparel (OTEXA) show that the negative impact of COVID-19 on U.S. apparel imports deepened further in April 2020. Specifically:

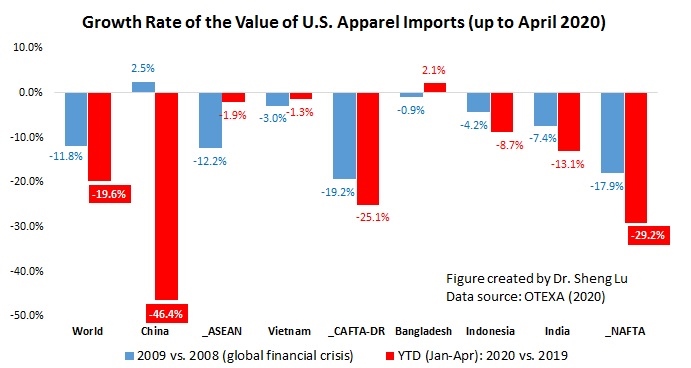

- Unusually but not surprisingly, the value of U.S. apparel imports sharply decreased by 44.5% in April 2020 from a year ago. Between January and April 2020, the value of U.S. apparel imports decreased by 19.6% year over year, which has been much worse than the performance during the 2008-2009 global financial crisis (down 11.8%).

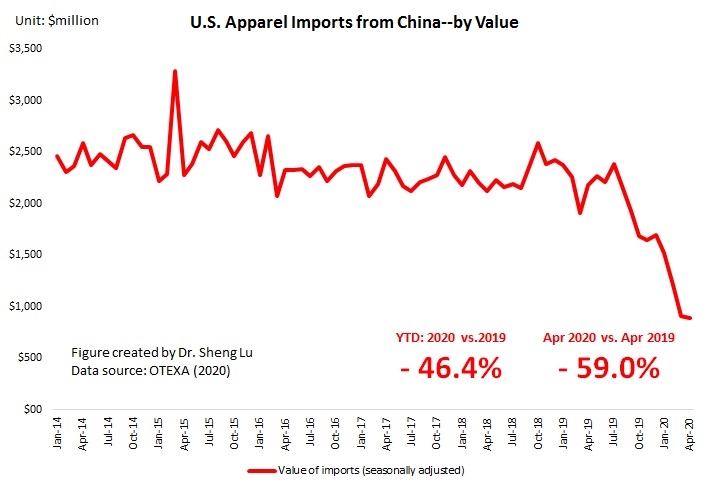

2. As the first country took a hit by COVID-19, China’s apparel exports to the United States continue to deteriorate—its value decreased by a new record of 59.0% in April 2020 compared with a year ago (and -46.4% drop year to date). This result is also worse than the official Chinese statistics, which reported an overall 22% drop in China’s apparel exports in the first four months of 2020).

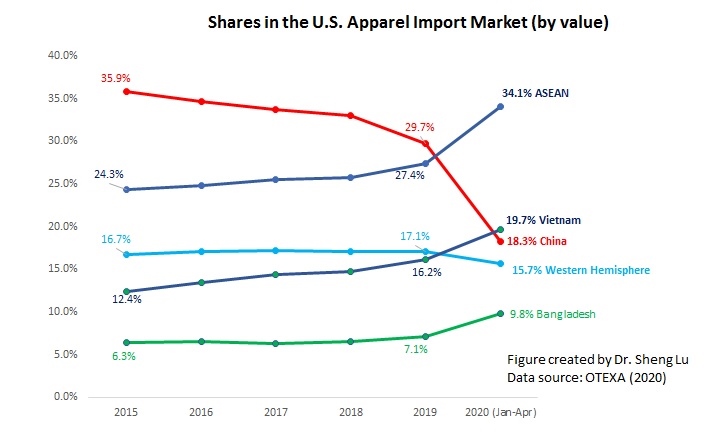

3. For the second month in a row, Vietnam surpassed China and ranked the top apparel supplier to the U.S. market in April 2020. China’s market shares in the U.S. apparel import market remained as low as 18.2% in April 2020 (was 30% in 2019), although it slightly recovered from only 11% in March 2020. With U.S.-China relations at a new low, there have been more intensified discussions on how to move the entire textile and apparel supply chain out of China and diversify apparel sourcing from the Asia region as a whole. However, as China itself has grown into one of the world’s largest apparel consumption markets, there is little doubt that China will remain a critical player for apparel sourcing, especially for the “China for China” business model.

4. Continuing the trend emerged in recent years, China’s lost market shares have been picked up mostly by other Asian suppliers, particularly Vietnam (19.7% YTD in 2020 vs. 16.2% in 2019) and Bangladesh (9.8% YTD in 2020 vs.7.1% in 2019). However, no clear evidence has suggested that U.S. fashion brands and retailers are giving more apparel sourcing orders to suppliers from the Western Hemisphere. In the first four months of 2020, still only 9.4% of U.S. apparel imports came from CAFTA-DR members (down from 10.3% in 2019) and 4.1% from NAFTA members (down from 4.5% in 2019).

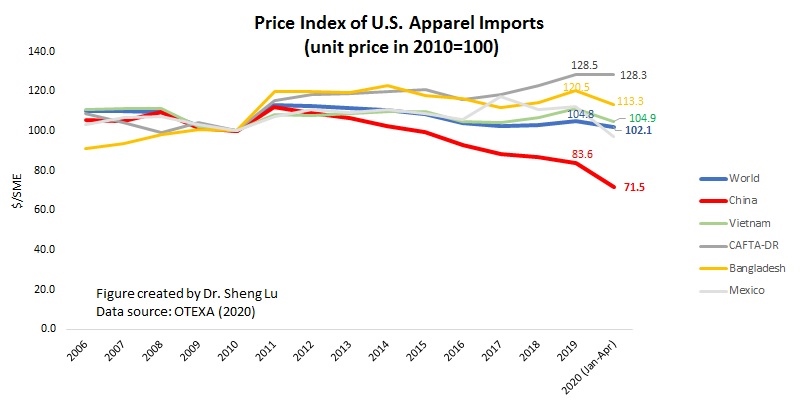

5. As a reflection of weak demand, the unit price of U.S. apparel imports was lower in the first four months of 2020 (price index =102.1) compared with 2019 (price index =104.7). Imports from China have seen the most notable price decrease so far (price index =71.5 YTD in 2020 vs. 83.5 in 2019).

by Dr. Sheng Lu