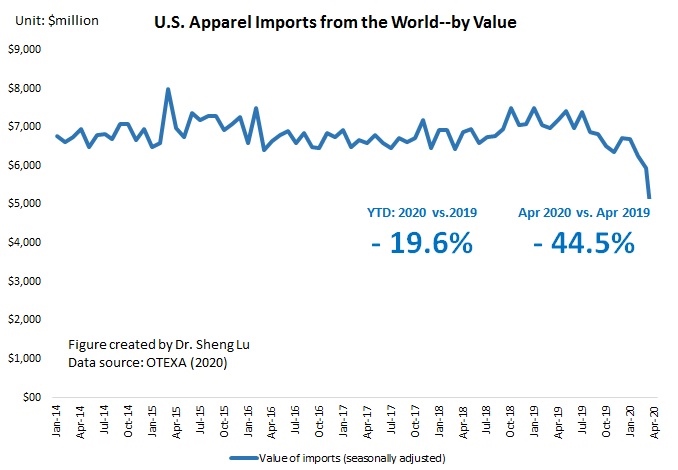

The latest statistics from the Office of Textiles and Apparel (OTEXA) show that the negative impact of COVID-19 on U.S. apparel imports deepened further in April 2020. Specifically:

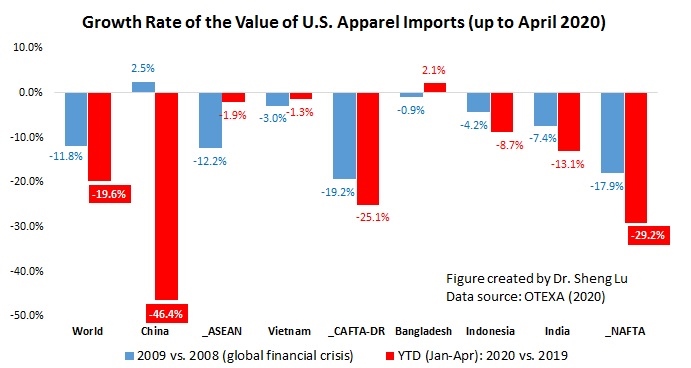

- Unusually but not surprisingly, the value of U.S. apparel imports sharply decreased by 44.5% in April 2020 from a year ago. Between January and April 2020, the value of U.S. apparel imports decreased by 19.6% year over year, which has been much worse than the performance during the 2008-2009 global financial crisis (down 11.8%).

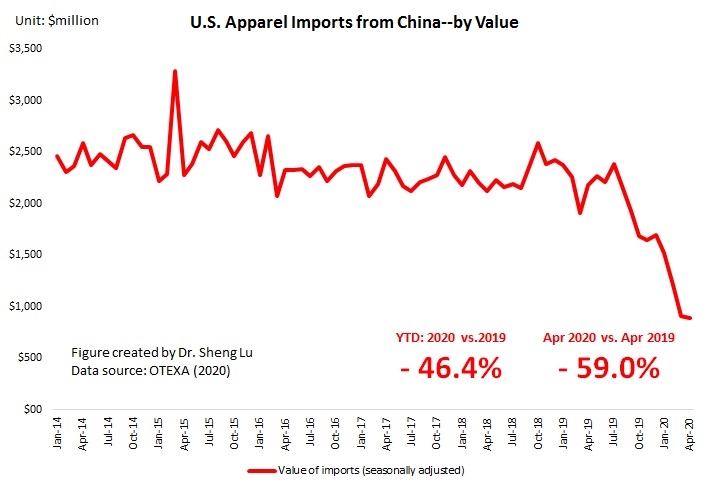

2. As the first country took a hit by COVID-19, China’s apparel exports to the United States continue to deteriorate—its value decreased by a new record of 59.0% in April 2020 compared with a year ago (and -46.4% drop year to date). This result is also worse than the official Chinese statistics, which reported an overall 22% drop in China’s apparel exports in the first four months of 2020).

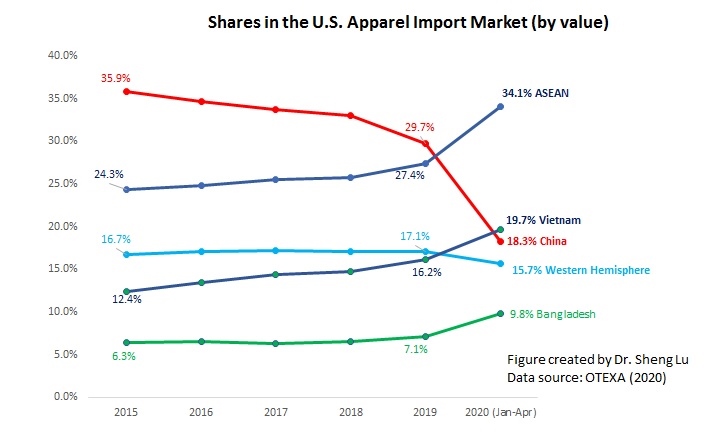

3. For the second month in a row, Vietnam surpassed China and ranked the top apparel supplier to the U.S. market in April 2020. China’s market shares in the U.S. apparel import market remained as low as 18.2% in April 2020 (was 30% in 2019), although it slightly recovered from only 11% in March 2020. With U.S.-China relations at a new low, there have been more intensified discussions on how to move the entire textile and apparel supply chain out of China and diversify apparel sourcing from the Asia region as a whole. However, as China itself has grown into one of the world’s largest apparel consumption markets, there is little doubt that China will remain a critical player for apparel sourcing, especially for the “China for China” business model.

4. Continuing the trend emerged in recent years, China’s lost market shares have been picked up mostly by other Asian suppliers, particularly Vietnam (19.7% YTD in 2020 vs. 16.2% in 2019) and Bangladesh (9.8% YTD in 2020 vs.7.1% in 2019). However, no clear evidence has suggested that U.S. fashion brands and retailers are giving more apparel sourcing orders to suppliers from the Western Hemisphere. In the first four months of 2020, still only 9.4% of U.S. apparel imports came from CAFTA-DR members (down from 10.3% in 2019) and 4.1% from NAFTA members (down from 4.5% in 2019).

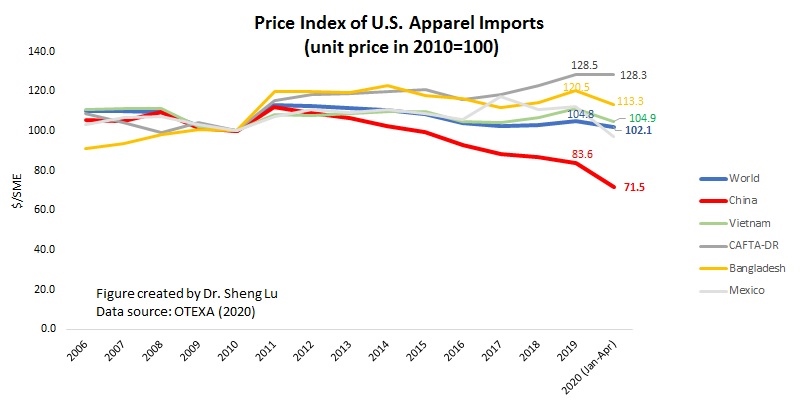

5. As a reflection of weak demand, the unit price of U.S. apparel imports was lower in the first four months of 2020 (price index =102.1) compared with 2019 (price index =104.7). Imports from China have seen the most notable price decrease so far (price index =71.5 YTD in 2020 vs. 83.5 in 2019).

by Dr. Sheng Lu

Due to the decrease in U.S. imports from China in recent months, do you foresee U.S. companies sourcing elsewhere in the future from regions such as Kenya, the Western Hemisphere, or other Asian countries? Or do you think this decrease is only temporary as sourcing demand will increase again after the pandemic?

Good question! A few observations:

1) As mentioned in the article, China’s lost market shares have been picked up mostly by other Asian suppliers, particularly Vietnam, other ASEAN members and Bangladesh. Several factors are behind this phenomenon—an already highly integrated textile and apparel supply chain among Asian countries; China’s foreign investments in these countries, driven by the belt and road initiative; and unparalleled export capacity in the Asia region & overall price advantages.

2) No evidence has suggested a significant boost of “near-sourcing” because of COVID-19. On the contrary, US apparel sourcing from the Western Hemisphere dropped to 15.7% YTD in 2020 compared with 17% in 2019. Industry reports suggest that many apparel producing countries in the Western Hemisphere are struggling hard with COVID-19, which could be a factor (https://www.just-style.com/analysis/guatemala-garment-workers-on-the-frontline-of-the-pandemic_id138887.aspx)

3) US apparel imports from Kenya and the AGOA region have been increasing in relative terms. However, it is important to recognize that they remain relatively small players (for example, only 0.7% of US apparel imports came from Kenya YTD in 2020, even though it was an increase from 0.5% in 2019). My other concern is due to a very tight budget, fashion brands and retailers will be even less likely to commit to expanding apparel sourcing from the region. Not like the Asian or Western Hemisphere, sourcing from AGOA members requires extra investments and companies simply don’t have the resources…

Welcome for any follow-up comments.

The graph showing the growth rate of the value of U.S. apparel imports was very shocking to me. Seeing how the value of U.S. apparel imports decreased by 19.6% from 2019 and 2020, which has been much worse than the performance during the 2008-2009 global financial crisis (down 11.8%). This makes me wonder if the decrease is going to continue, and how the apparel industry can impact if the economy is going to be worse or better then during the financial crisis in 2008-2009?

I think that it is very interesting that Vietnam has surpassed China for two months now as the US top apparel supplier. If the textile and apparel supply chain moves out of Asia altogether, as the blog mentions, where will it go? I also wonder what effects the move will have on other industries. If the industry stays in Asia, the findings seem promising for Vietnam to continue as the biggest supplier, I wonder if this will change in the future.

I don’t think textile and apparel supply chain will move out of Asia altogether. Just like the question you asked–where will it go (or where we could source from?) In terms of sourcing value, about 80% of US apparel imports came from Asia.

very soon, we will specifically look at the western hemisphere supply chain and factory Asia. I am sure you will have a fresh understanding /view about the issue after our class.

I see that in point #1 apparel imports have decreased almost 20% from January 1st, 2020 through April 2020. This sharp decline is on track with the WTO’s 13-32% decrease in global trade this year alone. Do you think that apparel imports will continue to decrease over the course of the year, even dropping below the WTO estimate? Or do you think the T&A industry will be able to get back on track and minimize some of the decrease in trade?

Good thought and observation! Apparel is a buyer-driven industry. Studies consistently show that the growth of the national economy will have huge impacts on the import demand for clothing. As the U.S. economy suffers a notable negative growth in the first quarter of 2020, the value of apparel imports decreased correspondingly. My estimate shows that every 1% decline in the US and EU Gross Domestic Product (GDP) in 2020 could lead to at least a 2-3% drop in the value of their apparel imports (https://shenglufashion.com/2020/03/25/how-might-covid-19-affect-apparel-sourcing-and-trade/).

As COVID-19 continues to evolve, there remain lots of unknowns about the U.S. and the world economy down the road. The most recent forecast from the World Bank suggests the U.S. GDP will decline 6.1% in 2020 (https://www.worldbank.org/en/publication/global-economic-prospects).

It is also interesting to keep a close watch on the ongoing structural change in the market—for example, many industry professors say the increasing awareness of sustainability and the necessity for WFH/social distancing will affect what consumers want and how they shop. Ultimately, fashion brands and retailers need to adjust their sourcing strategies (including where to source) to meet consumers’ changing demands.

Welcome for any follow-up thoughts and comments.

I agree with the industry professors in the need for more sustainability within brands. I think social distancing and working from home has led consumers to change the way they think about everything in their life. Ordering from online sites with little to no information on their sourcing, production and shipping definitely has led to consumers questioning about all stages of the products they buy. People are now more aware than ever of the many channels their goods go through and want the assurance they are supporting a socially and sustainably aware brand.