In January 2021, Just-Style consulted a panel of industry leaders and scholars in its Outlook 2021–Key Issues to Shape Apparel Sourcing Management Briefing. Below is my contribution to the report. All comments and suggestions are more than welcome!

What do you see as the biggest challenges – and opportunities – facing the apparel industry in 2021?

I see COVID-19 and market uncertainties caused by the contentious US-China relations as the two most significant challenges facing the apparel industry in 2021.

The difficulties imposed by COVID-19 on fashion businesses are twofold. First, with the resurgence of COVID cases worldwide, when and how quickly apparel consumption can rebound to the pre-COVID level remain hard to tell, particularly in leading consumption markets, including the United States and Europe. As the apparel business is buyer-driven, the industry’s full recovery is impossible without a strong return of consumers’ demand. Numerous studies also show that switching to making and selling PPE won’t be sufficient to make up for losses from regular businesses for most fashion companies.

Second, COVID-19 will also continue to post tremendous pressures on the supply side. In the 2020 Fashion Industry Benchmarking Study, which I conducted in collaboration with the US Fashion Industry Association (USFIA), the surveyed sourcing executives reported severe supply chain disruption during the pandemic. These disruptions come from multiple aspects, ranging from a labor shortage, a lack of textile raw materials, and a substantial cost increase in shipping and logistics. Even more concerning, many small and medium-sized (SME) vendors, particularly in the developing countries, are near the tipping point of bankruptcy after months of struggle with the order cancellation, mandatory lockdown measures, and a lack of financial support. The post-covid recovery of the apparel business relies on a capable, stable, and efficient textile and apparel supply chain, in which these SME vendors play a critical role.

In 2021, fashion companies also have to continue to deal with the ramifications of contentious US-China relations. On the one hand, the chance is slim that the punitive tariffs imposed on Chinese products, which affect most textiles and apparel, will soon go away. On the other hand, we cannot rule out the possibility that the US-China commercial relationship will deteriorate further in 2021, as more sensitive, complicated, and structural issues began to get involved, such as national security, forced labor, and human rights. Compared with President Trump’s unilateral trade actions, the new Biden administration may adopt a multilateral approach to pressure China. However, it also means more countries could be “dragged into” the US-China trade tensions, making it even more challenging for fashion companies to mitigate the trade war’s supply chain impacts.

Meanwhile, I see digitalization as a big opportunity for the apparel industry, not only in 2021 but also in the years to come. Fashion brands and retailers will increasingly find digitalization ubiquitous to their businesses—like air and electricity. In 2021, I expect fashion companies will make more efforts to creatively use digital technologies to interact with consumers, make transactions, develop products, and improve consumers’ online shopping experiences. Thanks to the adoption of digital tools, apparel companies may also find new opportunities to improve sustainability, better understand their customers through leveraging data science, and develop a more agile and nimble supply chain.

What’s happening with supply chains? How is the sourcing landscape likely to shift in 2021, and what can apparel firms and their suppliers do to stay ahead, remain competitive and build resilience for the future?

Apparel companies’ sourcing and supply chain strategies will continue to evolve in response to consumers’ shifting demand, COVID-19, and the new policy environment. Several trends are worth watching in 2021:

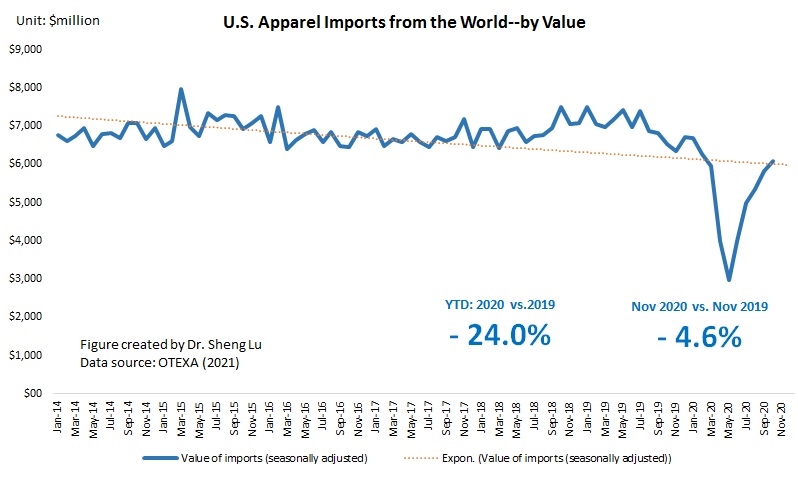

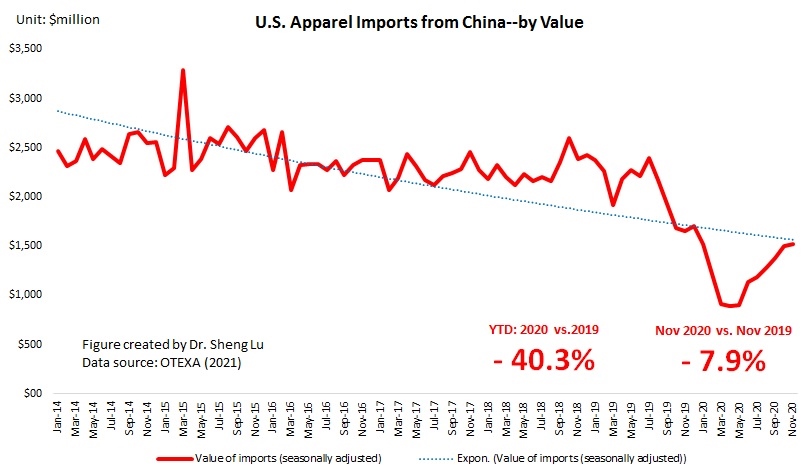

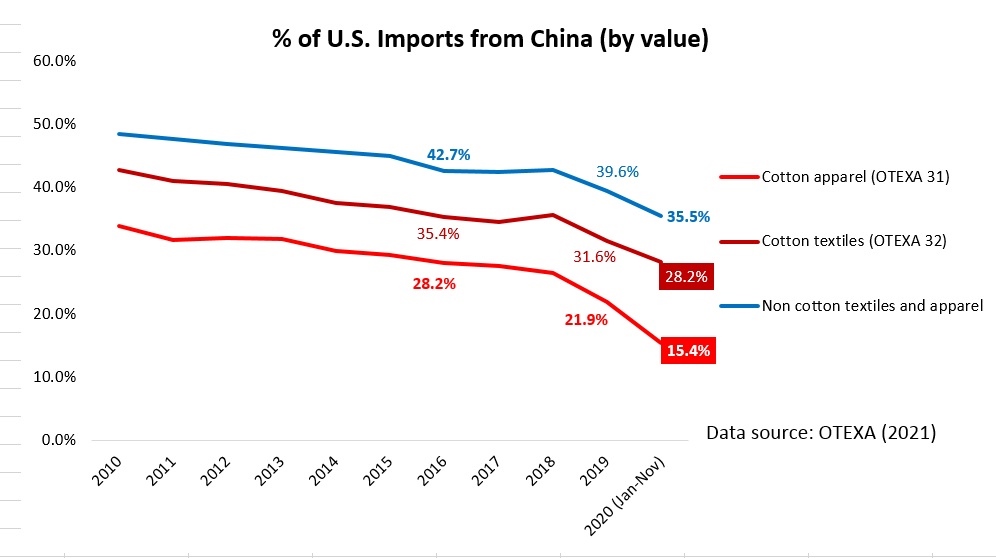

First, fashion companies’ sourcing bases at the country level will stay relatively stable in 2021 overall. For example, although it sounds a little contradictory, fashion companies will continue to treat China as an essential sourcing base and reduce their “China exposure” further, a process that has started years before the tariff war. Most apparel sourcing orders left China will go to China’s competitors in Asia, such as Vietnam, Bangladesh, and Cambodia. This also means that Asia, as a whole, will remain the single largest source of apparel imports, particularly for US and Asia-based fashion companies. In comparison, still, “near-sourcing” is NOT likely to happen on a large scale, mainly because “near-sourcing” requires enormous new investments to rebuild the supply chain, and most fashion companies do not have the resources to do so during the pandemic.

Second, sourcing diversification is slowing down at the firm level, and more apparel companies are switching to consolidate their existing sourcing base. For example, as the 2020 USFIA benchmarking study found, close to half of the respondents say they plan to “source from the same number of countries, but work with fewer vendors” through 2022. Another 20 percent of respondents say they would “source from fewer countries and work with fewer vendors.” The results are understandable– competition in the apparel industry is becoming supply chain-based. Building a strategic partnership with high-quality vendors will play an ever more critical role in supporting fashion brands and retailers’ efforts to achieve speed to market, flexibility and agility, sourcing cost control, and low compliance risk. Thus, apparel companies find it more urgent and rewarding to consolidate the existing sourcing base and resources and strengthen their key vendors’ relations.

Third, apparel sourcing executives still need to keep a close watch on trade policy in 2021. However, we may see fewer news headlines about trade and more “behind the door” advocacy and diplomacy. Specifically:

- US Section 301 actions: While the punitive tariffs on Chinese goods may not go away anytime soon, there could be a fight over whether the new Biden administration should continue granting certain companies exclusions from those tariffs. Further, in October 2020, the Trump Administration launched two new Section 301 investigations on Vietnam regarding its import and use of timber and reported “undervaluation currency.” The case is pending, but the stakes are high for fashion companies —Vietnam is often treated as the best alternative to sourcing from China and already accounting for nearly 20% of total US apparel imports.

- The US-China relationship: We all know the relationship is at its low-point, but the fact is many US fashion companies still treat China as one of their most promising markets to explore. China continues to expand its role in the Asia-based textile and apparel supply chain also. In a nutshell, more than ever, apparel executives need to care about what is going on in geopolitics. Hopefully, “tough times can breed positive outcomes.”

- CPTPP and RCEP: With the reaching of the Regional Comprehensive Economic Partnership (RCEP) in November 2020, there are growing calls for the new Biden administration to consider rejoining the Trans-Pacific Partnership (TPP) in some format to showcase the US presence in the Asia-Pacific region. To make the situation even more complicated, China has openly expressed its interest in joining the Comprehensive Progressive Agreement of the Trans-Pacific Partnership (CPTPP), commonly known as “the TPP without the US.” 2021 will be a critical time window for all stakeholders, including the apparel sector, to debate various trade policy options that could shape the future trade architecture in the Asia-Pacific region.

- Brexit: Brexit will enter a new phase in 2021 as the transition period ends on 31 December 2020. On the positive side, we have a playbook to follow—the UK has announced its new tariff schedules for various scenarios, which provide critical market predictability. We might also see the reaching of a new US-UK free trade agreement in the first half of the year, which will be exciting news for the apparel sector, particularly those in the luxury segment. However, as the US Trade Promotion Authority (TPA) is set to expire in July 2021, when and how soon such an agreement will enter into force will be another story. By no means trade policy in 2021 will go boring.

by Sheng Lu