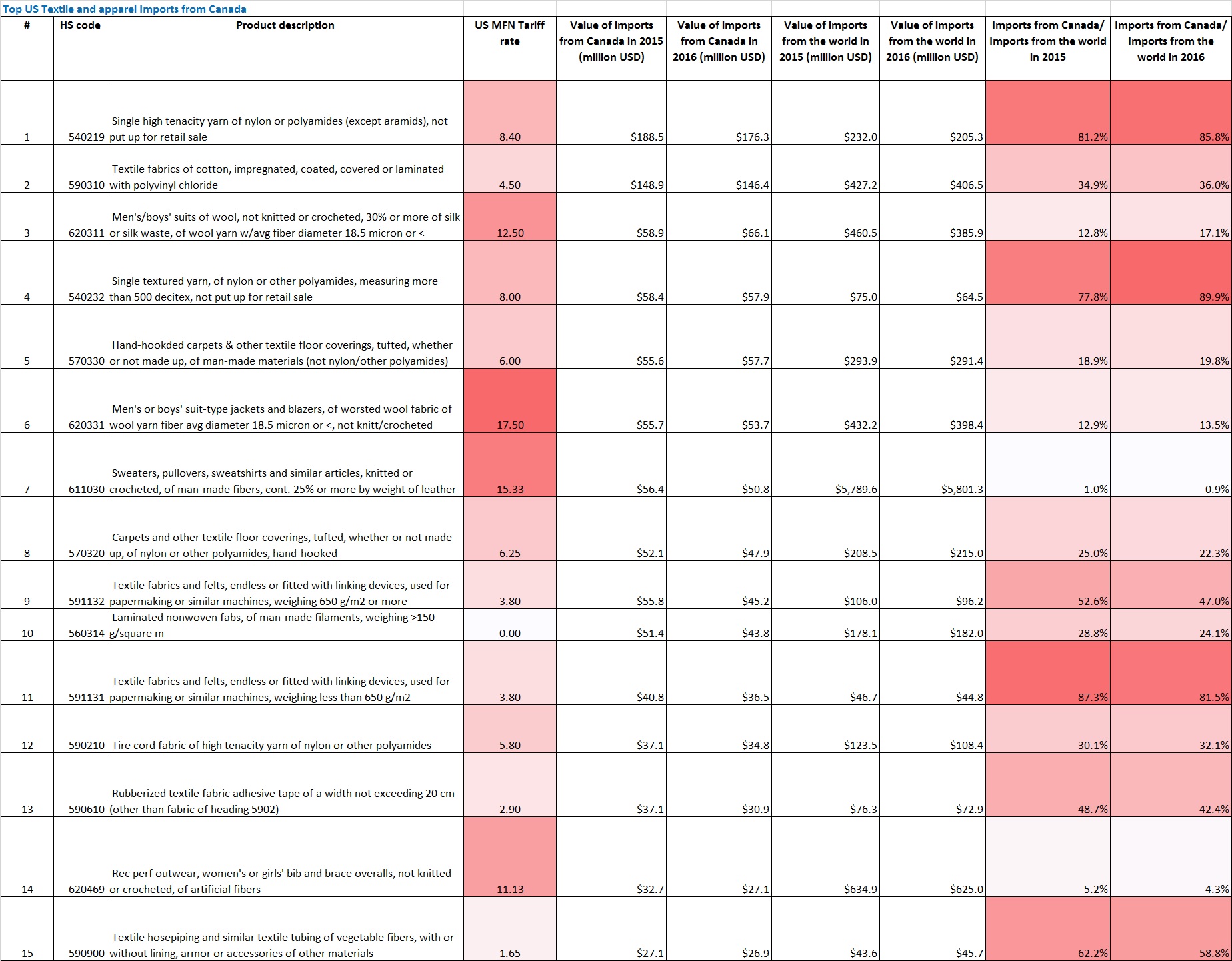

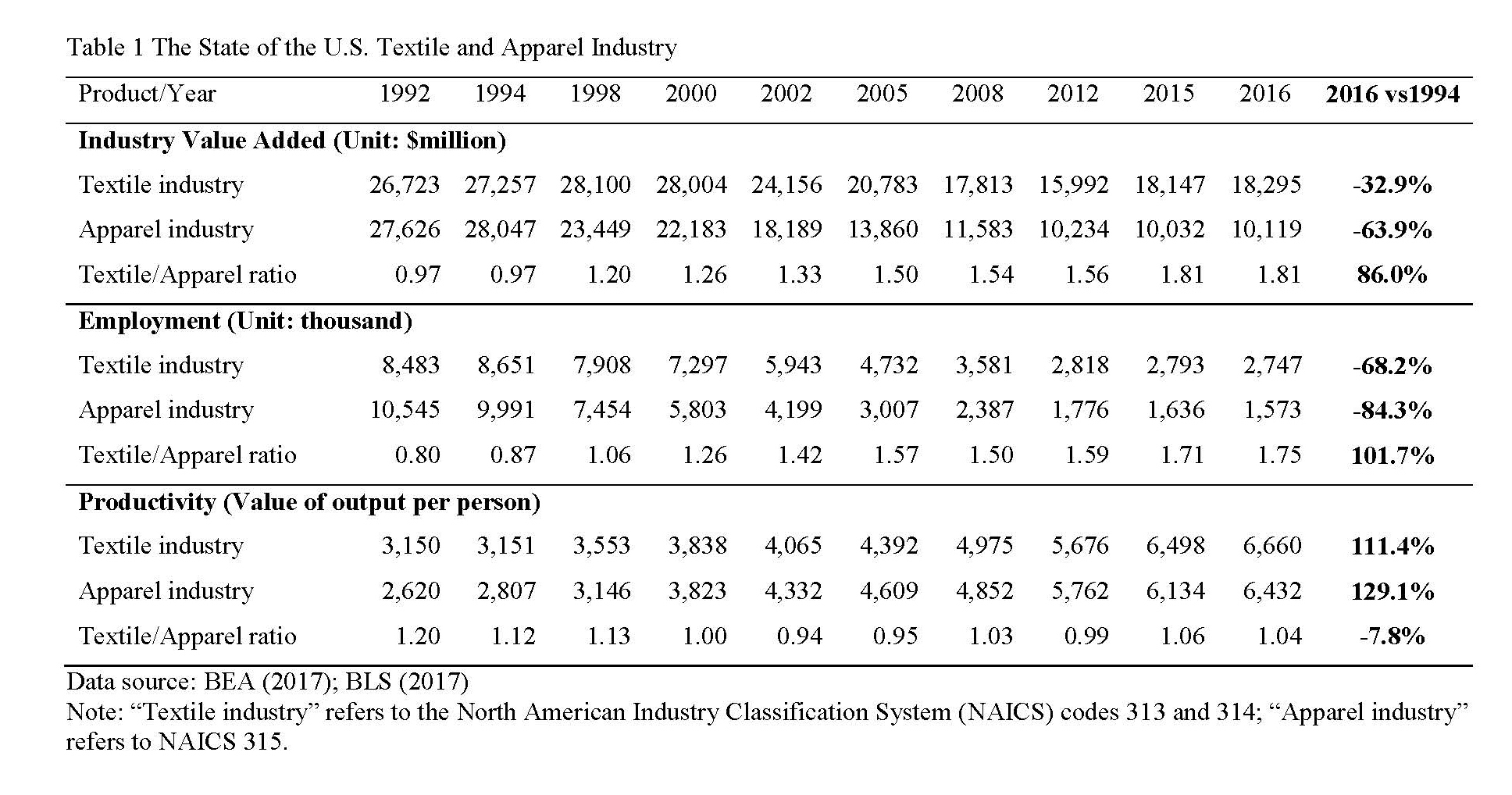

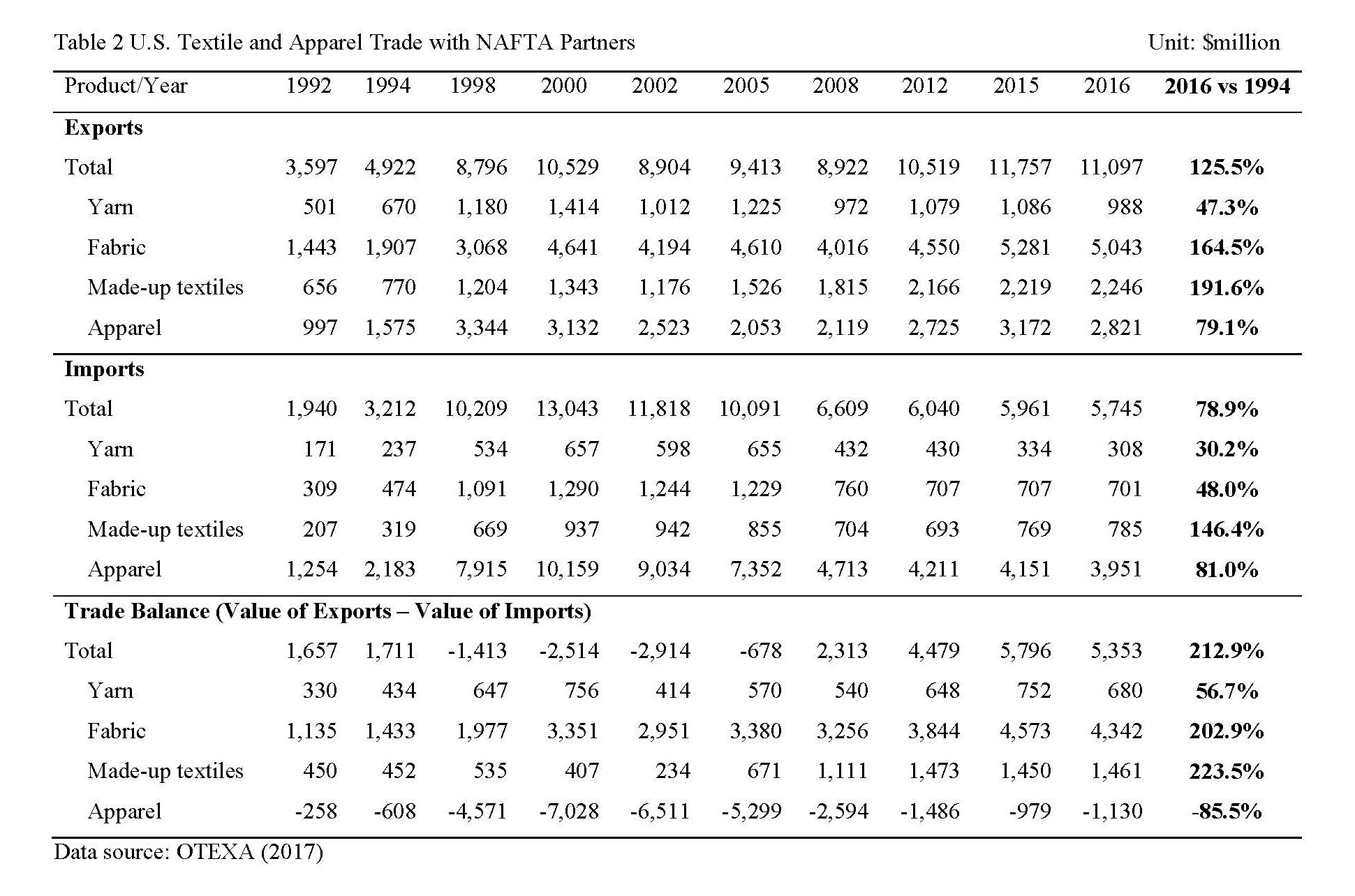

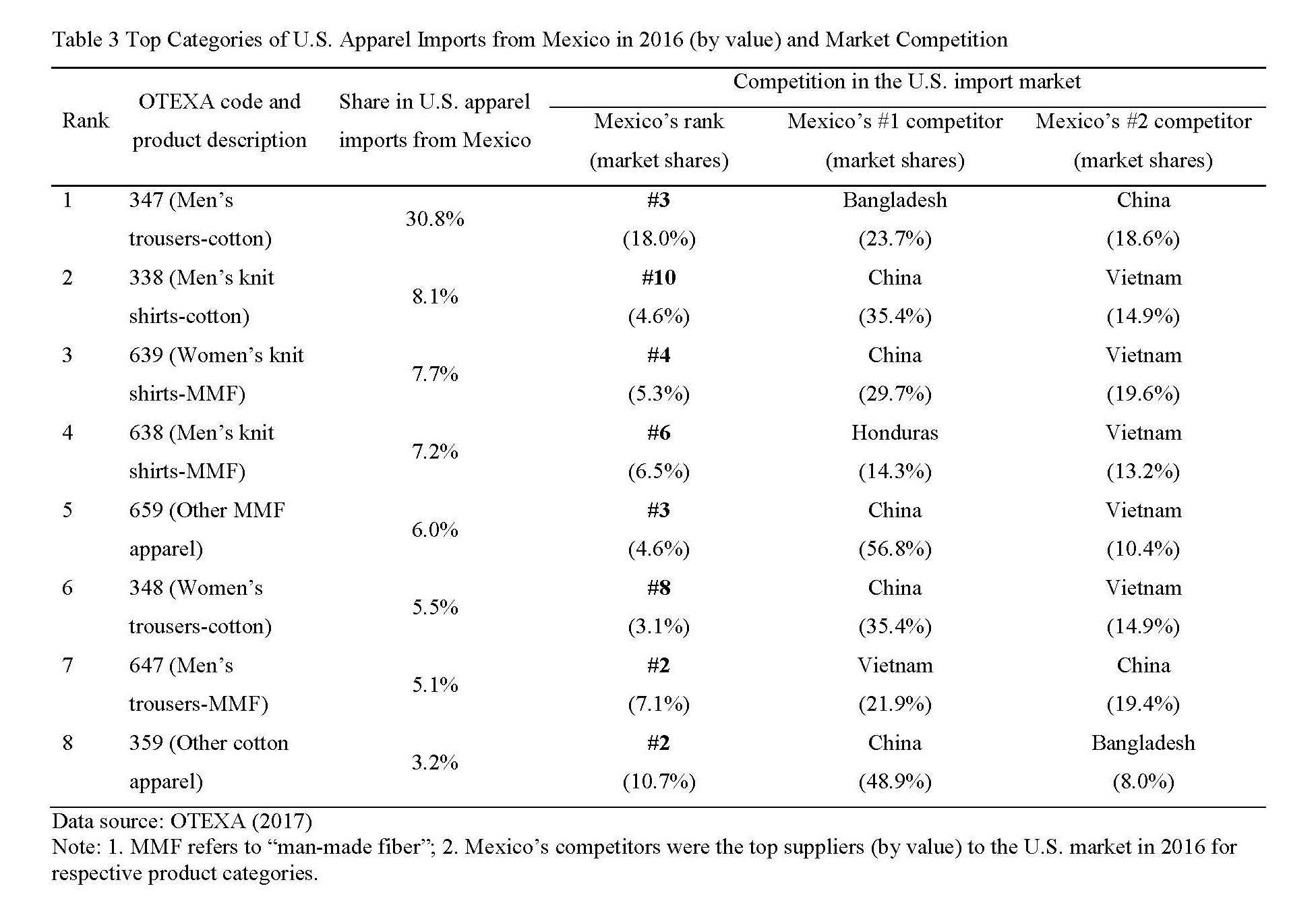

The factsheet is available in PDF

Background

On December 10, 2019, the United States, Mexico and Canada reached an updated U.S.-Mexico-Canada Free Trade Agreement (USMCA). USMCA officially enters into force on 1 July 2020. Compared with the version signed in September 2018, the new USMCA includes even higher labor and environmental standards and stronger enforcement mechanisms for these rules. According to the released protocol of amendment, no change has been made to the Textiles Chapter, however.

Textiles and Apparel and USMCA

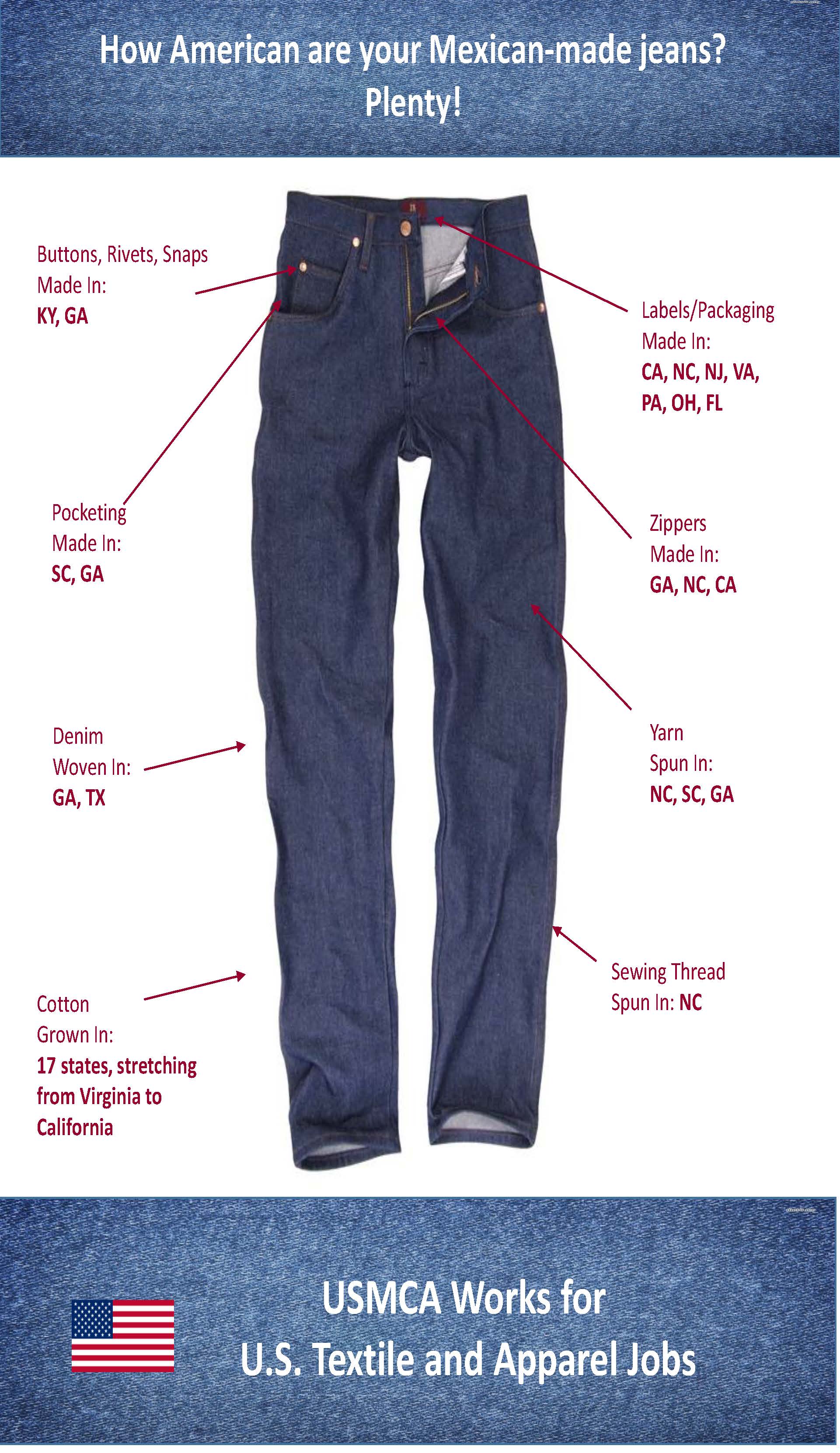

First, in general, USMCA still adopts the so-called “yarn-forward” rules of origin. This means that fibers may be produced anywhere, but each component starting with the yarn used to make the garments must be formed within the free trade area – that is, by USMCA members.

Second, other than the source of yarns and fabrics, USMCA now requires that some specific parts of an apparel item (such as pocket bag fabric) need to use inputs made in the USMCA region so that the finished apparel item can qualify for the import duty-free treatment.

Third, USMCA allows a relatively more generous De minimis than NAFTA 1.0.

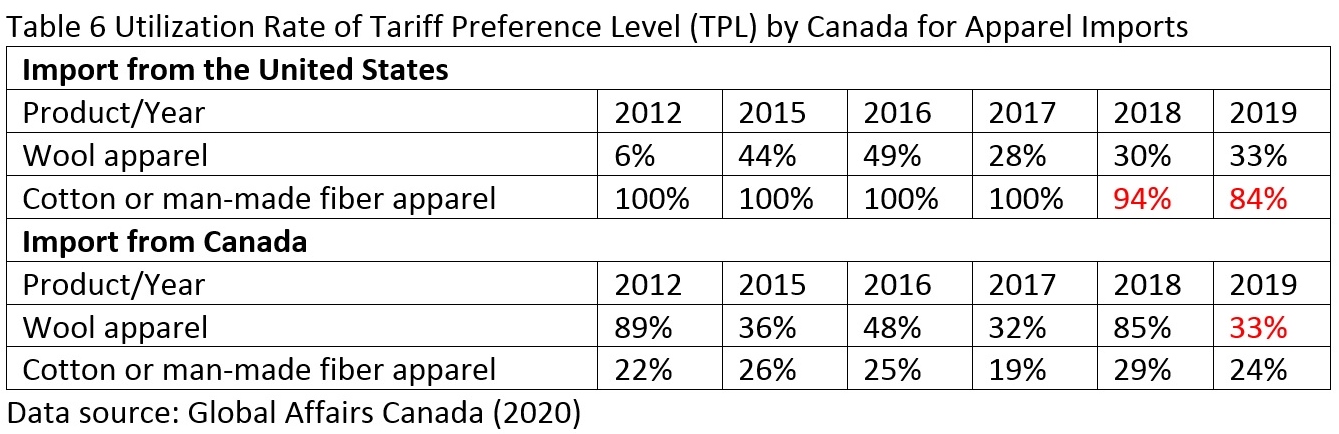

Fourth, USMCA seems to be a “balanced deal” that has accommodated the arguments from all sides regarding the tariff preference level (TPL) mechanism:

- Compared with NAFTA, USMCA will cut the TPL level, but only to those product categories with a low TPL utilization rate;

- Compared with NAFTA, USMCA will expand the TPL level for a few product categories with a high TPL utilization rate.

Fifth, USMCA will make no change to the Commercial availability/short supply list mechanism in NAFTA 1.0.

Sixth, it remains to be seen whether USMCA will boost “Made in the USA” fibers, yarns and fabrics by limiting the use of non-USMCA textile inputs. For example, while the new agreement expands the TPL level for U.S. cotton/man-made fiber apparel exports to Canada (currently with a 100 percent utilization rate), these apparel products are NOT required to use U.S.-made yarns and fabrics. The utilization rate of USMCA will also be important to watch in the future.

(Additional reading: Apparel-specific rules of origin in USMCA)

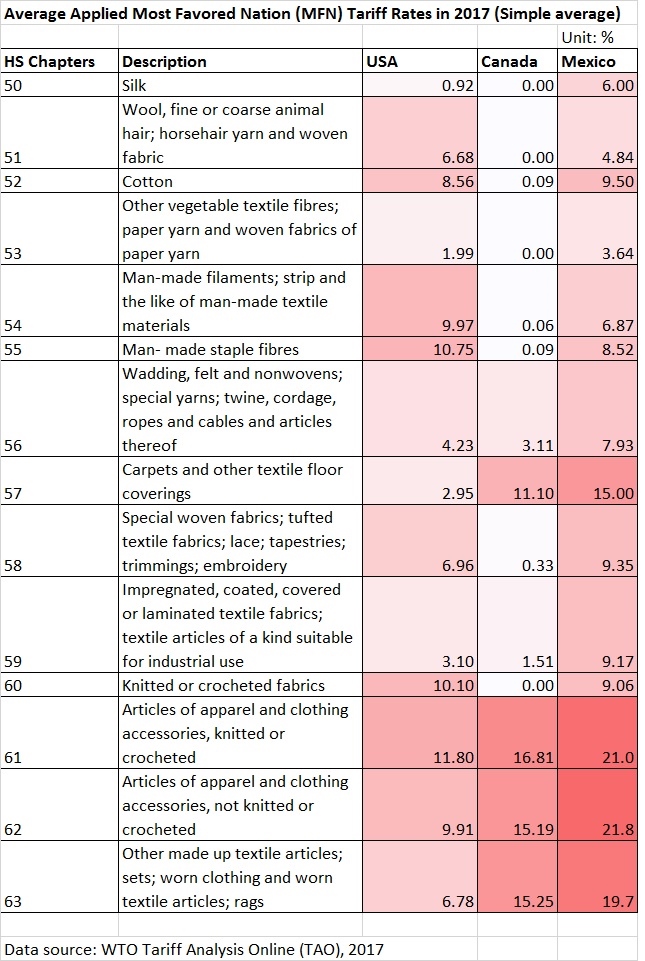

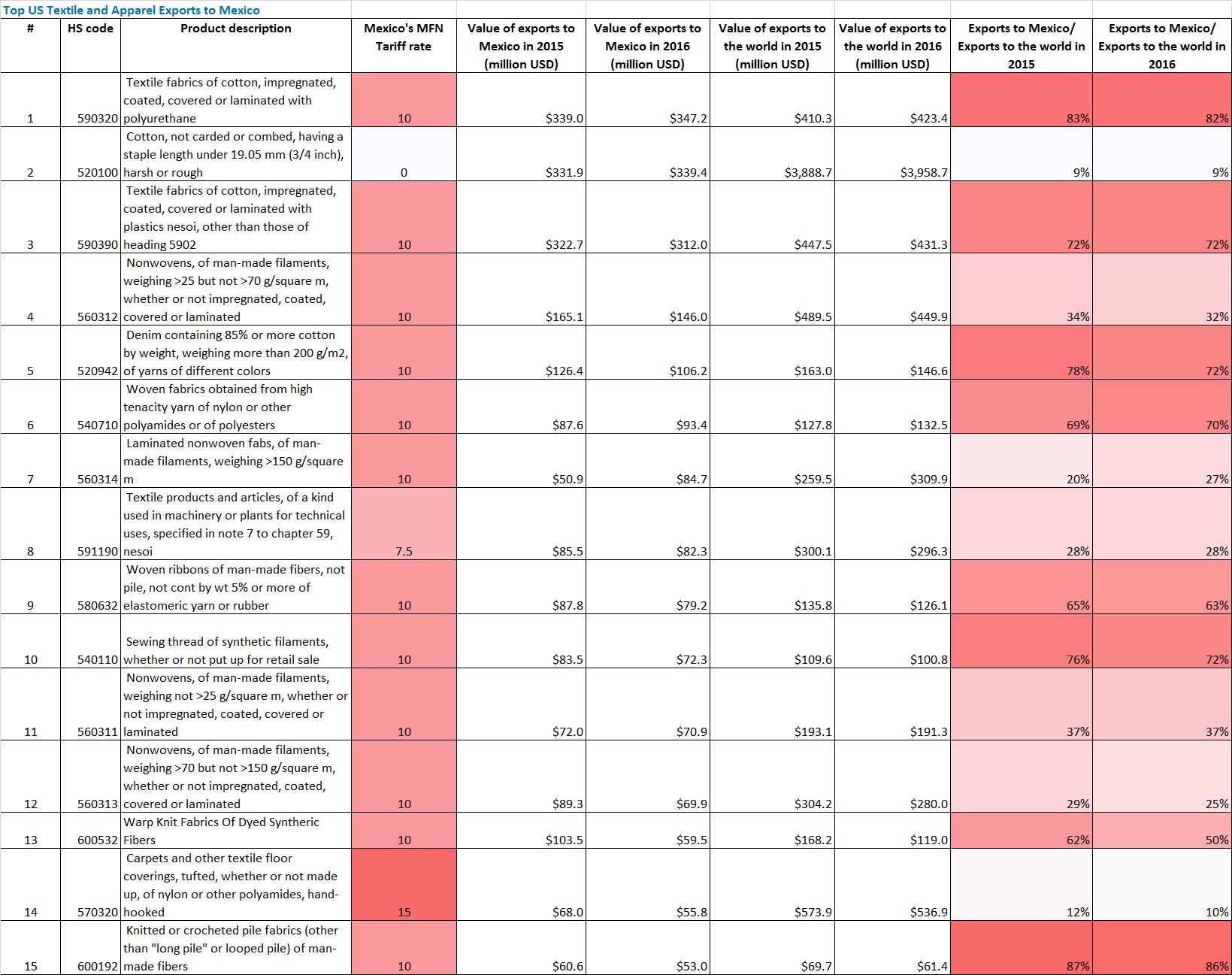

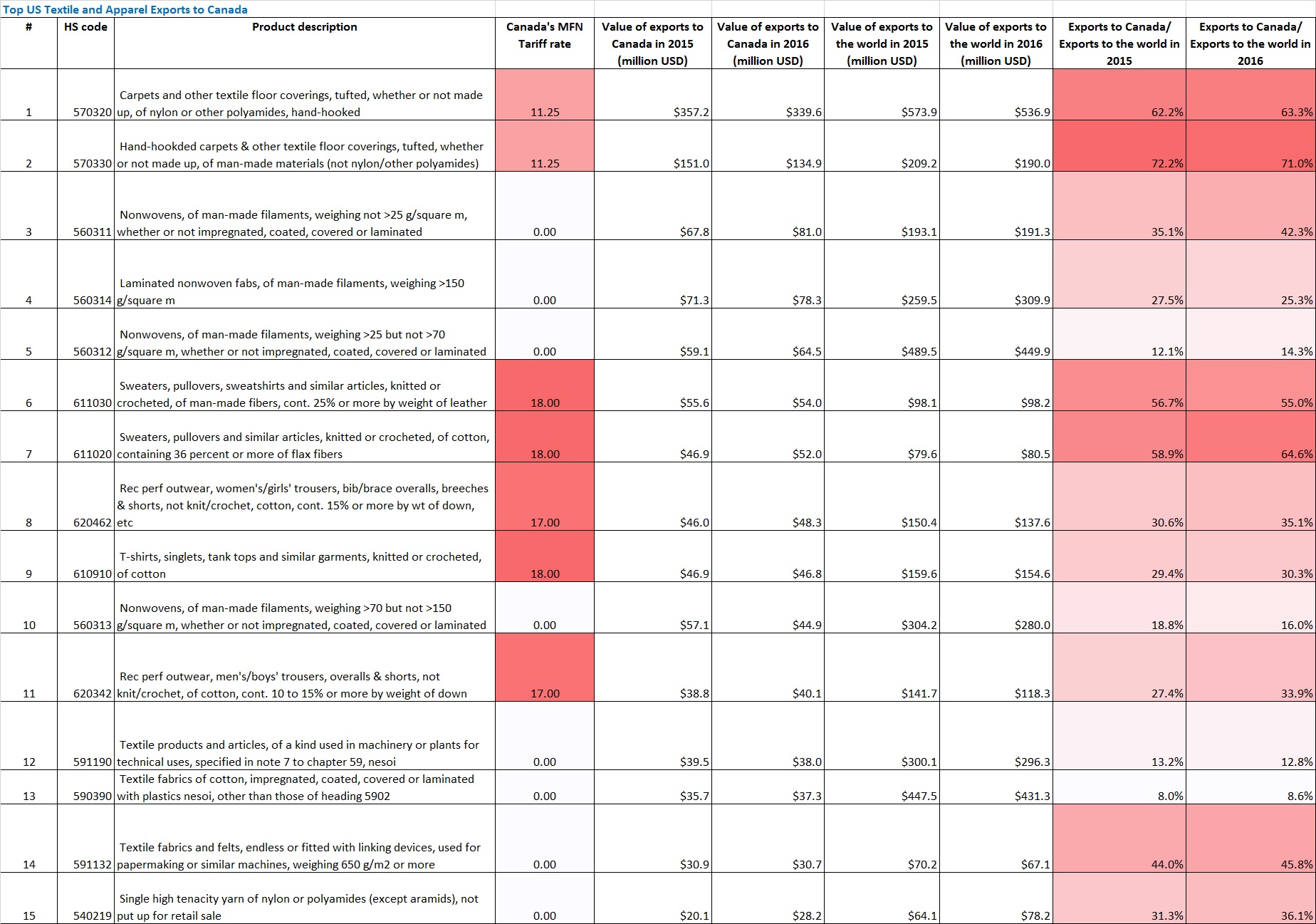

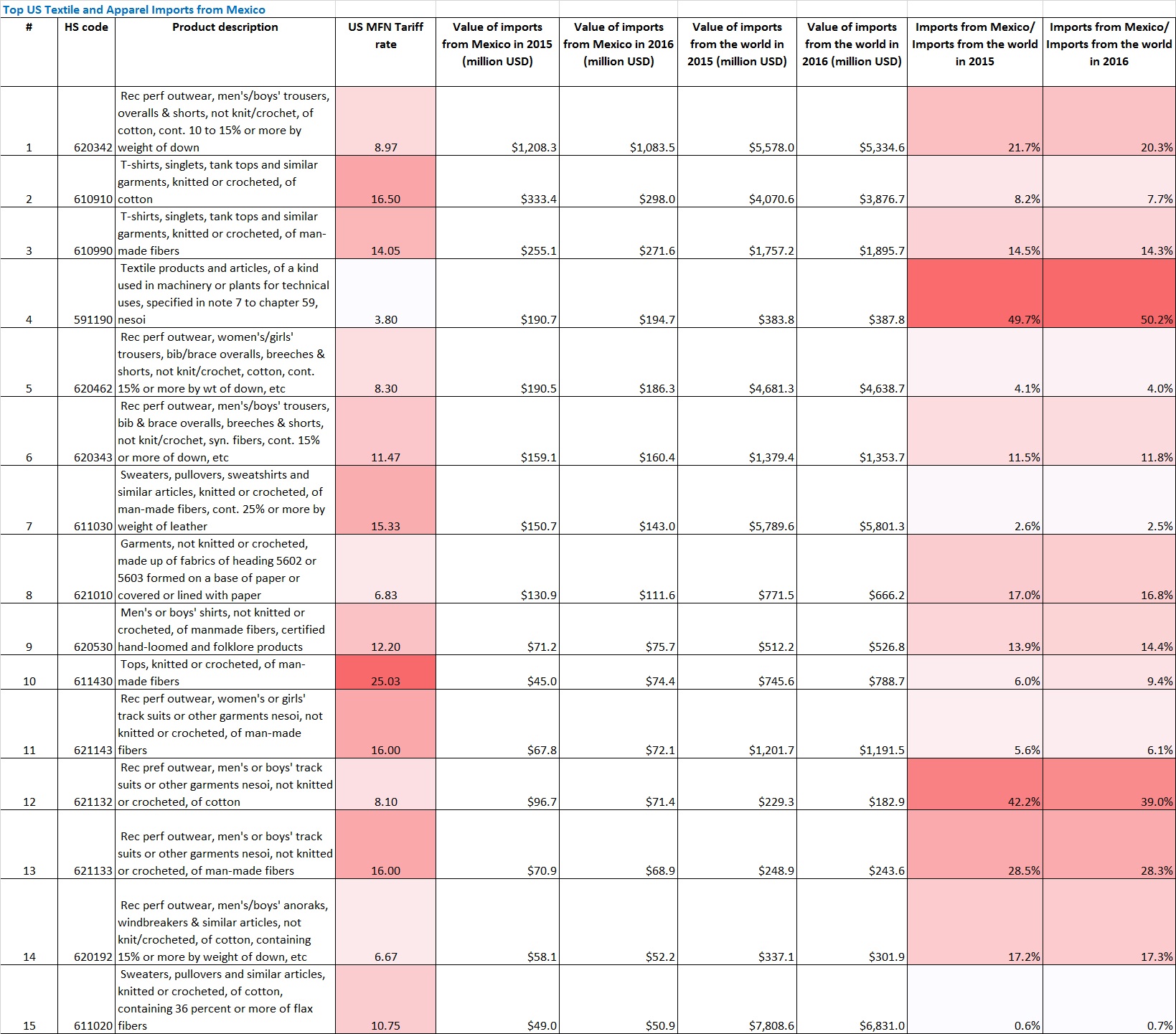

Economic Impacts of USMCA on the Textile and Apparel Sector

According to an independent assessment by the U.S. International Trade Commission (USITC) released on April 19, 2019:

First, USMCA overall is a balanced deal for the textile and apparel sector, particularly regarding the rules of origin (RoO) debate. As USITC noted, USMCA eases the requirements for duty-free treatment for certain textile and apparel products, but tighten the requirements for other products.

Second, the USMCA changes to the Tariff Preference Level (TPLs) would not have much effect on related trade flows. As USITC noted in its report, where USMCA would cut the TPL level on particular U.S. imports from Canada or Mexico, the quantitative limit for these product categories was not fully utilized in the past. Meanwhile, the TPL level for product categories typically fully used would remain unchanged under USMCA. The only trade flow that might enjoy a notable increase is the U.S. cotton and man-made fiber (MMF) apparel exports to Canada—the TPL is increased to 20million SME annually under USMCA from 9 million under NAFTA.

Third, USITC suggested that in aggregate, the changes under USMCA for the textile and apparel sector will more or less balance each other out and USMCA would NOT affect the overall utilization of USMCA’s duty-free provisions significantly. Notably, the under-utilization of free trade agreements (FTAs) by U.S. companies in apparel sourcing has been a long-time issue. Data from the Office of Textiles and Apparel (OTEXA) shows that of the total $4,163 million U.S. apparel imports from the NAFTA region in 2019, around $3,742 million (or 89.9%) claimed the preferential duty benefits under the agreement. As noted in the U.S. Fashion Industry Benchmarking Study, some U.S. fashion companies do not claim the duty savings largely because of the restrictive RoO and the onerous documentation requirements.