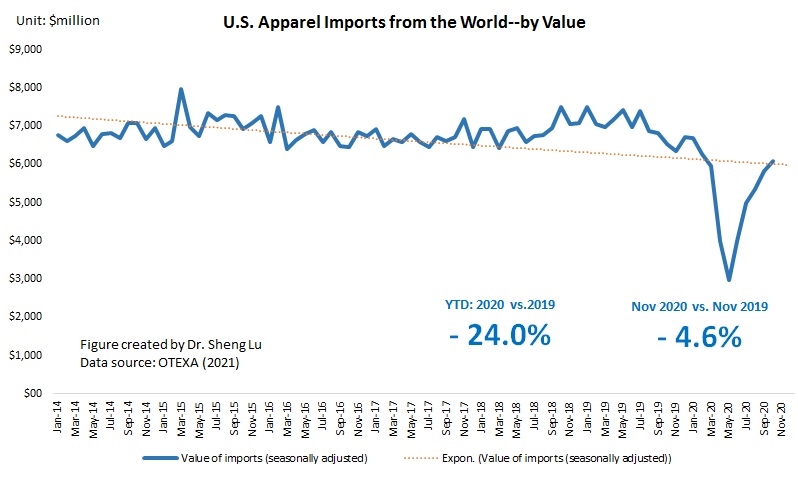

First, U.S. apparel imports continue to rebound thanks to consumers’ robust demand. However, the speed of recovery slowed. Specifically, The value of U.S. apparel imports in November 2020 marginally went down by 0.3% from October 2020 (seasonally adjusted), compared with an 8.8% growth from Aug to September and a 4.6% growth from September to October (seasonally adjusted).

As of November 2020, the volume of U.S. apparel imports has recovered to around 85-90% of the pre-coronavirus level. This result echoes the trend of U.S. apparel retail sales (NAICS 4481), which also indicates a “V-shape” rebound since May 2020.

Data further shows that compared with the 2008 world financial crisis, Covid-19 has caused a more significant drop in the value of U.S. apparel imports. However, it seems the post-Covid recovery process has been more robust than the 2009 financial crisis. The Auto Regressive Integrated Moving Average (ARIMA) model forecasts that at the current speed of recovery, the value of U.S. apparel imports (seasonally adjusted) could start to enjoy a positive year over year (YoY) growth by February 2021 (or around 11 months after the outbreak of Covid-19 in March 2020). In comparison, when recovering from the 2008 world financial crisis, it took almost 15 months to turn the YoY growth rate from negative to positive).

With the new lockdown measures taken in response to the resurgence of the Covid cases, the outlook of US apparel imports remains uncertain. It should also be noted that the period from December to April usually is the light season for apparel imports.

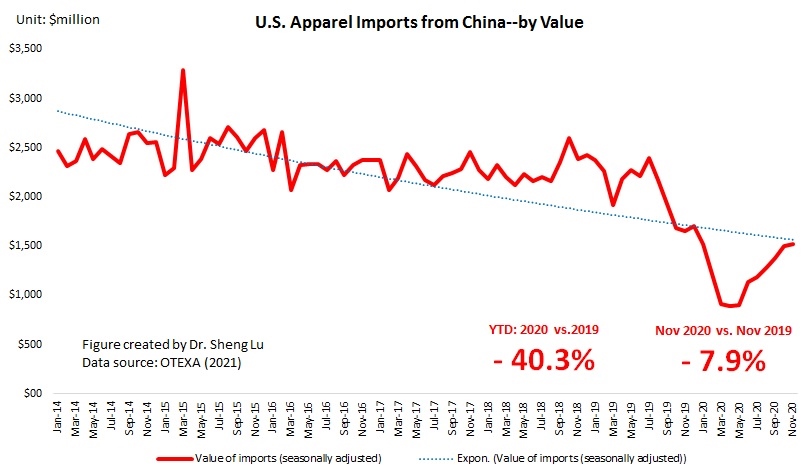

Second, supporting the findings of some recent studies, data suggests that U.S. fashion brands and retailers continue to reduce their “China exposure” in 2020. For example, both the HHI index and market concentration ratios (CR3 and CR5) suggest that apparel sourcing orders are gradually moving from China to other Asian countries. Related, since August 2020, China’s market shares in total U.S. apparel imports have been sliding both in quantity and in value.

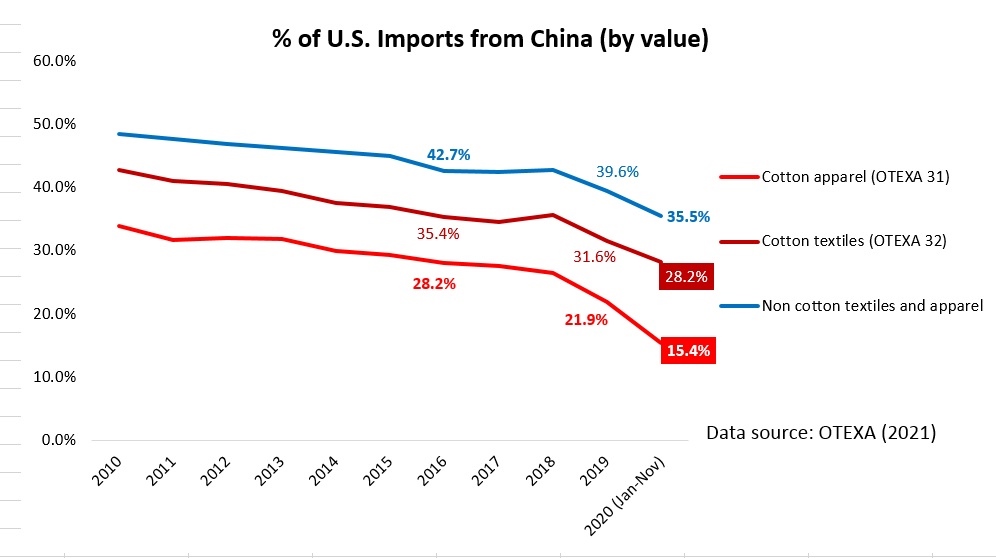

We should NOT ignore the impact of non-economic factors on China’s prospect as an apparel sourcing destination. For example, the reported forced labor issue related to Xinjiang, China, and a series of actions taken by the U.S. government (such as the CBP withhold release orders) have significantly affected U.S. cotton apparel imports from China. Measured by value, from January to November 2020, only 15.4% of U.S. cotton apparel came from China, compared with 22.2% in 2019 and 28% back in 2017. While China’s total textile and apparel exports to the US dropped by 32% in 2020 (Jan to Nov), China’s cotton textiles and cotton apparel exports to the US went down more sharply by 41.1% and 47.2%, respectively.

Third, despite Covid-19, Asia as a whole remains the single largest source of apparel for the U.S. market. Other than China, Vietnam (19.8% YTD in 2020 vs. 16.2% in 2019), ASEAN (32.6% YTD in 2020 and vs. 27.4% in 2019), Bangladesh (8.2% YTD in 2020 vs.7.1% in 2019), and Cambodia (4.4% YTD in 2020 vs. 3.2% in 2019) all gain additional market shares in 2020 (Jan to Nov) from a year ago.

Fourth, still, no clear evidence suggests that U.S. fashion brands and retailers have been giving more apparel sourcing orders to suppliers from the Western Hemisphere because of COVID-19 and the U.S.-China tariff war. In the first eleven months of 2020, 9.4% of U.S. apparel imports came from CAFTA-DR members (down from 10.3% in 2019) and 4.4% from USMCA members (down from 4.5% in 2019). The limited local textile production capacity and the high production cost are the two notable disadvantages of sourcing from the region.

by Sheng Lu