Key findings:

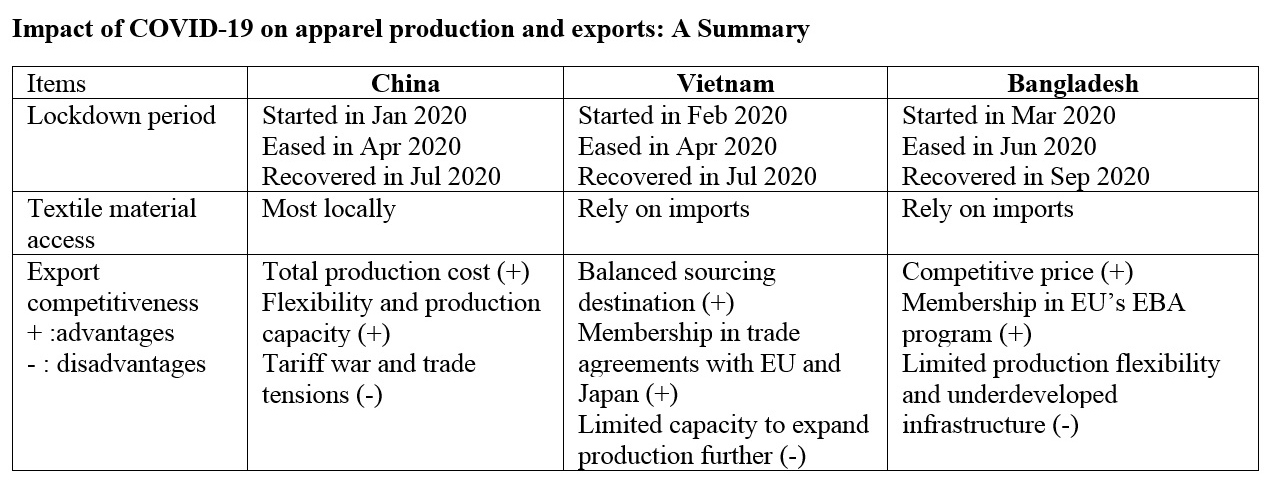

During the pandemic, three factors are most relevant to a country’s apparel export performance: government lockdown measures, textile raw material access, and comprehensive export competitiveness. Against these three factors, apparel producers and exporters in China, Vietnam, and Bangladesh face common but differentiated business challenges and opportunities during the pandemic (see the table above).

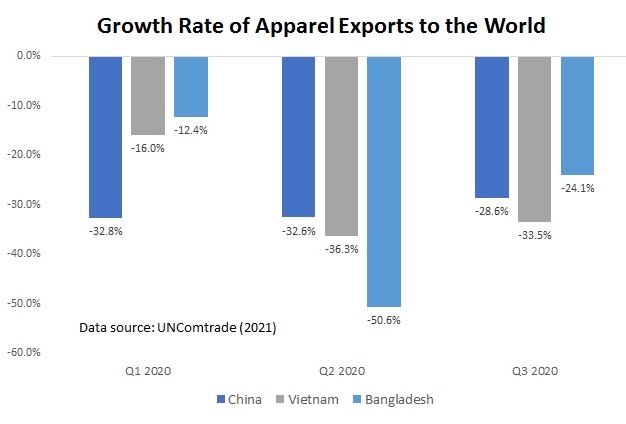

China, Vietnam, and Bangladesh all suffered an unprecedented (nearly 30% year over year) drop in their apparel exports to the world in 2020 (Q1-Q3) due to COVID-19. This result mirrored the reduced import demand in the world’s major apparel consumer markets, where the local economies were also hit hard by the pandemic, including the US (down 2.3%), the EU (down 4.3%), and Japan (down 4.8%).

However, the three countries’ export performance is most different in the US market—China’s apparel exports dropped by 31.6%, much steeper than Vietnam (down 6.9%) and Bangladesh (down 12.6%). It seems that even though COVID-19 may favor China as an apparel sourcing base from an economic perspective, US fashion companies have given more weight to non-economic factors, such as the outlook of the trade war, in their sourcing decisions involving China.

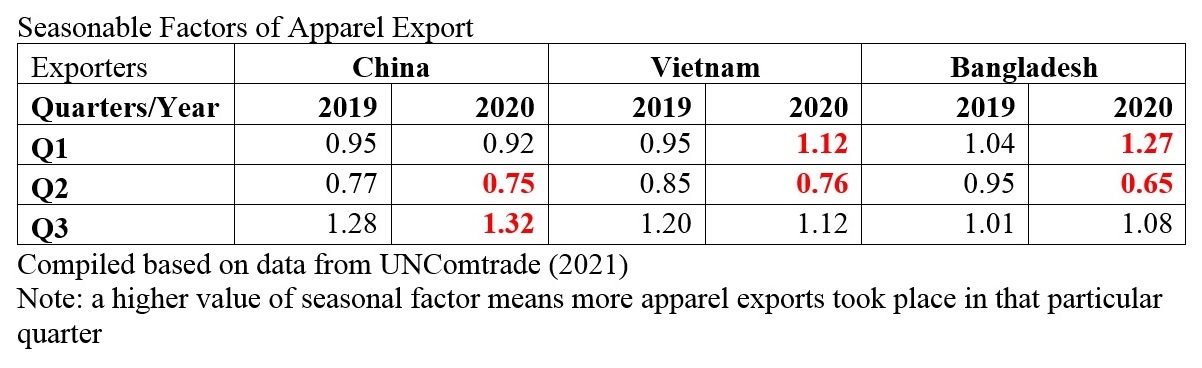

COVID-19 had disrupted apparel exporters’ regular production and export schedule in 2020. The lockdown measures in these three countries seem to affect their export seasonal pattern most significantly. For example, as the first country hit by COVID-19, China’s apparel exports were at the bottom from February to April 2020; however, China’s apparel exports recovered quickly since May 2020 when factories resumed production. In comparison, apparel exports from Vietnam and Bangladesh were at their lowest level from April to May and May to June 2020, respectively, when their factories had to close.

Additionally, Bangladesh’s apparel export seasonality had experienced a more dramatic change in 2020 than in China and Vietnam. A possible reason behind the phenomenon is the export product structure. Notably, China and Vietnam export a more diverse range of products, whereas apparel exports from Bangladesh concentrate on basic fashion items.

Industry sources also indicate that between February 2020 and February 2021, US apparel imports from China and Vietnam see a significant structural change—they include more COVID-popular items such as sweaters, smock dresses, and sweatpants, and fewer dresses, shirts, and suits. However, over the same period, the product structure of US apparel imports from Bangladesh barely changed, and they also included few COVID-popular categories mentioned above. In other words, despite order cancellations, garment factories in China and Vietnam seem more likely to receive new sourcing orders than their counterparts in Bangladesh because of advantages in production flexibility and agility.

Further, China, Vietnam, and Bangladesh all turned less diversified in their apparel export market during the pandemic. Notably, the US, EU, and Japan have become more critical export markets ever. Compared with fashion companies’ efforts in sourcing diversification, it could be more challenging for garment-producing countries to diversify their export market during the pandemic.

Further reading: Victoria Langro and Sheng Lu (2021). Sourcing’s new order – Covid’s impact on world’s top three apparel exporters. Just-Style.

[for FASH455 in spring 2022: If you comment on this blog post, please respond to this question: as we are 2 years into the pandemic, why or why not do you think the study’s findings are still valid?]

From the data, given, what struck me was the huge drop in exports in apparel (31%) from China. While the trade war may have caused demand pressure, the Chinese response to COVID-19 (strict shutdowns) and the worldwide impact the virus is having is heavily impacting the industry to the point, where many think it’s better to move out of China right now. In the short run, it doesn’t seem to make sense for companies to maintain large operations when the demand is so small at the moment. Currently, the only fabric goods that have not lost significant demand are athleisure goods aside from PPE. Many are predicting that such trends will stay as more people plan to work from home, as companies relax their dress code (or people just hide it), not go out as much, and going out to conventions and meetings are not going to be as prevalent as once was. It seems like the world has shifted even more online. For the men at least, it may not be that basic goods will be dress shirts, pants, shorts, and the things we typically wear to work for a while. It might be that basic goods may be sweatpants, hoodies, t-shirts, and pajamas, which do not change much every season and if man-made, can be easily transformed.

You made some great points. I am not surprised China’s exports have dropped because throughout the year people were consuming less which we know because demand for certain products was not as high. I think once the pandemic hit a lot of companies did not need the exports they would normally need from China. Another trend I think we could see is companies wanting to operate more domestically or closer to home, because if something similar to the pandemic were to happen in the future, businesses may not suffer as much if operations are domestic.

great discussion here. Just to add a point–there is a seasonal pattern of US apparel imports from different sources. For example, to fulfill consumers’ last-minute holiday orders, which require faster speed to market, U.S. fashion companies typically do relatively more near-sourcing from September to December. In comparison, U.S. fashion companies place more sourcing orders with Asian suppliers from June to late September/early October.

And when i compare China’s market shares from Dec 2018 to Dec 2020, the result suggests a more significant negative impact of the trade war on China’s market shares in the US apparel import market.

Echoing the comments above, COVID has made it challenging to adjust sourcing base simply because companies don’t have the sources to do so. And covid somehow “favors” China as it has one the most complete textile and apparel supply chain in the world.

Although China recovered quickly since factories resumed production in May 2020, I was surprised to read that China’s apparel exports were at the very bottom due to the COVID-19 pandemic. I figured they would bounce back due t their wide variety of products that are being exported. It make senses that they would start to focus producing products that were popular items during COVID-19. Since they are gearing their products based off of the consumers desires, they are guaranteed to receive more orders and export more items to different sectors because of the high use of online shopping during the pandemic. Diversifying sourcing methods to obtain a mix of products that consumers desire and demand is the key to a successful export schedule.

I was not surprised to hear that China’s apparel exports dropped by 31.6% just because of the strict shutdowns that were in place. I was also not surprised to see that Vietnam was only down 6.9% and Bangladesh was down 12.6%. As I discussed in another blog post, I think the U.S. as well as other countries are going to start sourcing more from Vietnam and Bangladesh and less from China, which is represented in the data. U.S. fashion companies are starting to take into account the outlook of the trade war and other non-economic factors. It was also understandable that the type of apparel imports for the U.S. has changed significantly. Apparel imports are including more COVID-popular items such as sweaters, smock dresses, and sweatpants, and fewer dresses, shirts, and suits, which is not a shock given that a lot of people even still today are working from home.

Everything seems so predictable and understandable, then why would fashion companies still feel very uncertain about the sourcing outlook this year? How to explain companies’ concerns about market uncertainties?

I definitely expected to see a drop in in exports apparel in countries due to COVID-19, but 31.6% was really shocking. This gave me a really good perspective on how much COVID-19 has really affected apparel exports from countries. These three countries, China, Bangladesh and Vietnam all experienced this, especially China. Along with this, it is not surprising that US imports from China are going down, because the US is starting to source more from Bangladesh and Vietnam. I also expected to read about the types of clothing that were more in demand when the pandemic started. A lot of comfy clothing (sweatshirts, sweatpants, etc.) became much more in demand, and I think this trend is going to continue. COVID-19 has made a tremendous impact on apparel exports, many of these impacts that may be permanent.

it is not surprising that US imports from China are going down, because the US is starting to source more from Bangladesh and Vietnam. But why?

There has been tension between the US administrations and that tension has pushed businesses to turn to other sources in the case of higher tariffs and such. I also believe trade agreements and sustainable methods have also increased change and encouraged discussion about how the US can become more self-sufficient.

I think that one reason US imports from China are decreasing has to do with the fact that China is become more mature country in terms of the 6 stages of T&A we spoke about in class. The trend of this graph showed that as a country becomes more mature, their capital also grows which slows down apparel productions and shifts more toward textile manufacturing, and innovation. I wonder if this has anything to do with the change of sourcing. I remember seeing a blog post about fashion students from China’s opinions on this topic and I found that discussion fascinating. Although this is certainly not the only reason for the decrease in number, as it is clear that it is more unpredictable!

After reading this article, I can say that I feel like companies will want to work more closer to where they originate from. I say that because if something unexpected and tragic were to happen again, their company may not have to adjust as much if they were closer to home rather than operating form further away. I do have a question though, as these companies are well adjusted to the way they operate now, why are there drops in export apparels in countries if they are getting back on their feet?

The COVID-19 pandemic began in Eastern Asia at the start of January 2020, where many countries including China, Vietnam, and Bangladesh were forced to shut down, eventually the virus spreading to other parts of the world later on. While many Asian countries were able to recover mostly by September 2020, places like the U.S., Canada, Europe, etc. were still struggling to contain the pandemic in the beginning of 2021. Although exporters in Asia dealt a shorter time with the pandemic, it still halted production significantly and financially burdened them. While China is the biggest exporter compared to Vietnam and Bangladesh, it struggled the most because of non-economic factors such as tensions in the trade war and even unfair stereotypes about where exactly the virus started. People strongly blamed China for “starting” the pandemic because it was already easy to blame them during the trade war. This definitely hurt China in the short-term in terms of exporting, but with a new presidency, these tensions have been a lot more eased.

This article help me to see things a bit more clear. Initially, I hypothesized that because China had such a large population, they wouldn’t be affected as badly as Vietnam and Bangladesh. In reality, China suffered the most. The recovery time for each depended on what was being exported for example, recovery came quickly for countries that exported COVID related products (gloves, hats, masks etc.).

I knew that the COVID-19 pandemic has obviously affected apparel imports, but I was stunned to see that China, Bangladesh, and Vietnam all had a 30% drop in apparel exports over the course of 2020. Especially after taking this class, I see just how much many countries’ economies depend on the apparel industry, so clearly this data shows how troublesome this was for these countries.

This article really brought to light the importance of location when it comes to sourcing. COVID-19 truly demonstrated the impacts of globalization on supply chains with delayed shipments and even order cancellations. This particular article makes it evident that for Asian countries, sourcing is more competitive than ever. Especially now with 30% drops, ethical business practices come back into question. Many of these factories may resort back to cutting corners in order to save money and time which will lead to decreased salaries and longer working hours. With countries’ economies so heavily reliant on the fashion industry, this type of hit is major. Even China is not untouchable when it comes to the effects of the pandemic on supply chain operations. This is a time for countries to reevaluate their global partnerships as well as their main industrial sectors.

In this article, I found it interesting how much China, Vietnam, and Bangladesh lost in apparel exports due to the pandemic, however, I was not surprised by this information. I also remember hearing in the news how all production processes were disrupted during the beginning of the pandemic and the article confirmed this. I expected all of these major changes in the industry but it still is a concerning issue within the fashion industry. The part I found most surprising was how imports were lower from other countries, online websites were still up and running, so I believed more people would be buying clothes, even if just loungewear.

The outbreak of the epidemic has led to three problems of apparel export, customs export, textile import, and finished apparel export. For China, Vietnam, and Bangladesh, three of the biggest apparel exporters, the outbreak has reduced exports. China has seen the sharpest decline. COVID-19 breaks the world’s normal pattern of clothing trade. China and Vietnam are diversified in their exports. But in Bangladesh, which makes it’s living mainly from garment exports, the drop is devastating.

The COVID-19 pandemic has greatly affected fashion brands and retailers around the world. It was very interesting read more about how the pandemic has affected major textile and apparel producers and exporters including China, Bangladesh and Vietnam. US apparel imports and exports coming from these various locations have also been greatly affected, as we still see many bans on imports and exports today. The three major factors that were ultimately put into effect would be government lockdown measures, textile raw material access, and comprehensive export competitiveness, as stated in the blog. It is important that fashion brands and retailers continue to look towards a more successful future, as the fashion industry is ever so changing.

The speed of China’s response to the pandemic caused China to quickly restore the supply chain, but the United States in response to the pandemic no quick response measures, U.S. citizens to realize the importance of imported products in Asia, China, as has a good production supply chain, able to respond to a pandemic, but the American manufacturing industry faces huge challenges, how to effectively help us manufacturing progress?

COVID-19 impacted supply chains all around the world with disrupted export schedules, shipment delays, and changing production processes. Specifically, China saw an apparel export drop in 31% due to the shutdowns that were put into place. On the other hand, Vietnam was was only down 6.9% and Bangladesh by 12.6%. I believe that China was effected more than the other two previously mentioned countries because of the U.S. Due to the tariff war and the pandemic, the US started to source more from Vietnam and Bangladesh rather than China.

I am not surprised that China, Vietnam, and Bangladesh all suffered drop in apparel exports in 2020 due to the COVID-19 pandemic. As China was the first country to be hit by COVID-19, I am not surprised they experienced a steeper drop at 31.6%. I am also not surprised that China was able to recover from this drop as quickly as they did as they were able to manufacture COVID-popular items such as sweatpants and leisure wear. China adapted to the current demands of the supply chain which gave them the ability to recover from this drop at the beginning of the pandemic. They were also the first country to be hit, so they had enough time to recover as well.

It is understandable to hear that China, Vietnam, and Bangladesh have all experienced a decline in apparel exports in 2020 as a result of the pandemic. The entire supply chain was hit with decreased demands in exports, but China was one of the first to experience this because the virus’ outbreak originated there. The 31.6% drop in exports was a result of slowed shopping and overall industry breaks. These decreased exports have hurt the countries that patriciate because apparel manufacturing and exporting is a huge part of their economy and is also one of the main ways that their citizens make money. Millions of garments workers were without a job due to the pandemic.

It’s important to note that Bangladesh’s apparel export seasonality had experienced a more dramatic change in 2020 than in China and Vietnam because of the lack of diversity in products they manufacture. I really feel for Bangladesh’s manufacturing industry and the employees who make it what it is because they’re trapped in an endless cycle of unfair work with nothing but more pressure from the government. Additionally, the government is under pressure because they want to keep their title as the 2nd largest garment exporter but to do that they have to keep ultra-low costs which in the end, keeps them stuck in a box with no room for growth or opportunity. They have no stability which makes it unsurprising that their weaknesses really showed though once the pandemic hit.

After the global pandemic in 2020, China, Vietnam, and Bangladesh all experienced a decline in apparel exports. Due to the decrease of demands in exports, the whole supply chain was impacted negatively. Although China was one of the first countries to deal with the lasting issues of the pandemic, I personally feel that Bangladesh got hit the hardest. Less developed countries did not have the means to recover as well as other, more developed countries after the pandemic. Bangladesh garment workers already dealt with poor working conditions, and the pandemic only made it even worse. Apparel manufacturing and exporting is such a large portion of Bangladesh’s economy, and with the negative impact on the supply chain, they were only left with more problems to deal with.

I thought this article was very insightful and found it interesting how things have progressed since this piece was posted. For instance, I found it very interesting that China faced a much steeper decrease than Bangladesh or Vietnam regarding exports to the US. This was likely due to COVID as well as trade disputes. Over time these issues may have actually worsened as the US has now implemented the UFLPA and strict Chinese COVID policies have backed up supply chains. As a result of this, many fashion brands are decreasing Chinese exposure in the T&A industry. However, based on a hostile trade environment between the US and China though and a botched TPP (as well as other factors), the RCEP FTA was since in 2022 giving China and other Asian nations a leg up in T&A production which could help revitalize their regional supply chains.

I also enjoyed reading about how COVID affected Bangladesh. Due to their limited production capacity, the seasonality of their garments did not fare well with the versatility needed during the pandemic. I wonder the best way a developing nation should handle this crisis.

After viewing the bar graph and statistical references, I was not shocked to see the steep decline in Chinese exports due to Covid-19. It just goes to show how much the U.S. depended on its exports prior to the pandemic. In the table, it is interesting to see how much Covid-19 impacted the three countries and the advantages and disadvantages they faced. For China specifically, the tariff war did not help their economy, as prices were very high, leading the U.S. to look for products elsewhere. I would assume this controversy, along with the lockdown would have caused such a significant decrease in export trade. While the U.S. has looked to source products elsewhere, such as Vietnam and Bangladesh, I am surprised their numbers were as low as they were considering their lack of resources and expansion during Covid-19. Because this industry is very labor-intensive for underdeveloped countries, like Bangladesh, I would have predicted a larger decrease in overall apparel exports with the lack of employment during the lockdown.

This summary shows how COVID-19 did not hit all “top three” suppliers in the same way. The similar 30% global drop hides the sharp fall in China’s share of U.S. imports compared with Vietnam and Bangladesh, which reflects trade war concerns layered on top of the pandemic.

The timing and product mix story feels especially important. China and Vietnam shifted faster into “COVID-friendly” items like sweats and knitwear, while Bangladesh stayed locked into basics and saw more disruption to its seasonal pattern. The final point on export concentration is sobering, as producers talk about diversification but grow even more dependent on the U.S., EU, and Japan during a crisis.