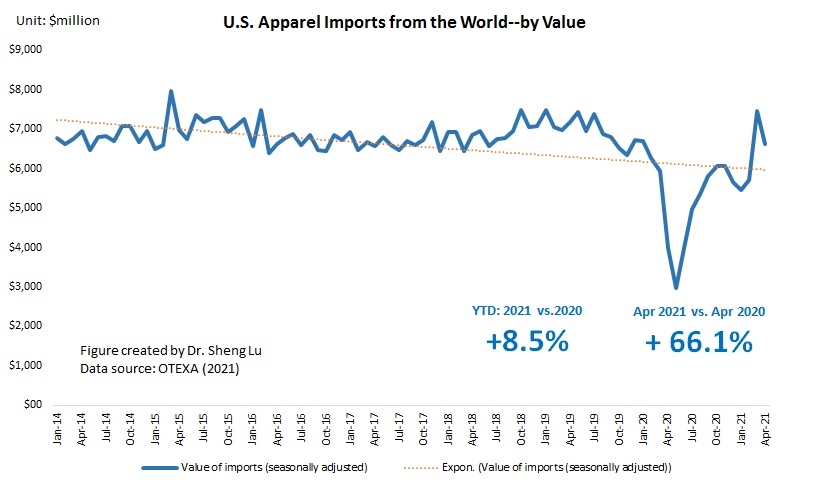

First, thanks to consumers’ resumed demand and a more optimistic outlook for the U.S. economy, U.S. apparel imports continue to rebound. However, uncertainties remain. On the one hand, mirroring retail sales patterns, the value of U.S. apparel imports in April 2021 went up by 66% from a year ago, a new record high since the pandemic. The absolute value of U.S. apparel imports so far in 2021 (January –April) also recovered to around 88% of the pre-Covid level (i.e., January to April 2019). However, the value of U.S. apparel imports in April 2021 was 11.2% lower than in March 2021 (seasonally adjusted), suggesting that the market environment is far from stable yet as the COVID situation in the U.S. and other parts of the world continue to evolve.

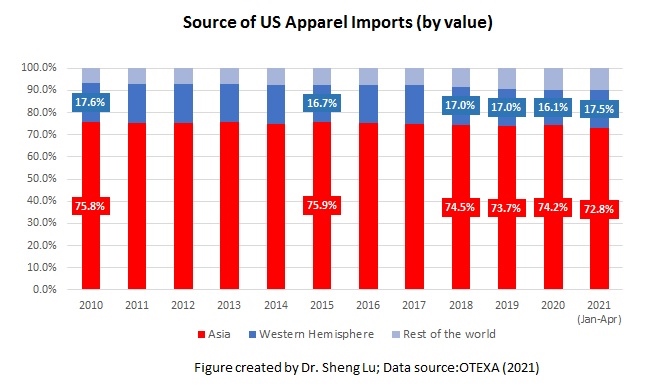

Second, data indicates that Asia as a whole remains the single largest sourcing base for U.S. fashion companies, stably accounting for around 72-75% of the import value. Studies show that two factors, in particular, contribute to Asia’s competitiveness as a preferred apparel sourcing base—price and flexibility & agility. Asia’s highly integrated regional supply chains and its vast production capacity shape its competitiveness in these two aspects.

However, the recent surge of COVID cases in India and its neighboring Southeast Asian countries has raised new worries about the potential sourcing risks and supply chain disruptions for U.S. fashion companies currently sourcing from there.

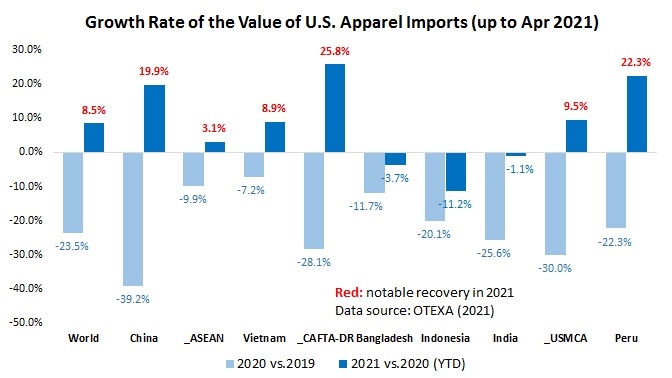

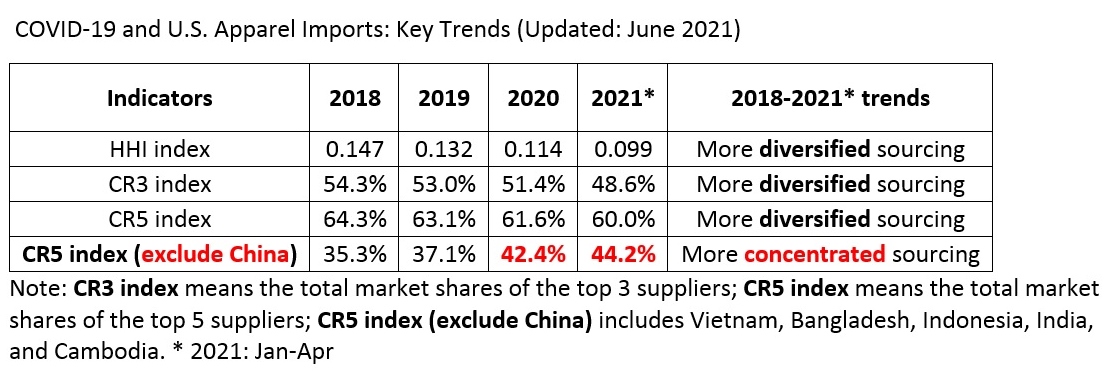

Third, as the direction of the US-China relations becomes ever more concerning, U.S. fashion companies seem to accelerate diversifying sourcing from China. Even China remains the top apparel supplier for the U.S. market, from January to April 2021, China’s market shares fell to 32.1% in quantity (was 36.6% in 2020) and 20.2% in value (was 23.7% in 2020). Also, the HHI index and market concentration ratios (CR3 and CR5) suggest that US fashion companies are increasingly moving their apparel sourcing orders from China to other Asian countries. For example, according to a leading U.S. fashion corporation in its latest annual report, “in response to the recent tariffs imposed by the current US administration, the Company has reduced the amount of goods being produced in China.”

Further, the latest data suggests that the concerns about the alleged forced labor in Xinjiang hurt China’s prospect as an apparel sourcing destination, BOTH for cotton and non-cotton items. Measured by value, only 11.9% of U.S. cotton apparel came from China in April 2021, a new record low since implementing the CBP WROs, which impose a regional ban on any cotton and cotton apparel made in the Xinjiang region. The latest data also suggests that China is quickly losing market shares for non-cotton textile and apparel items.

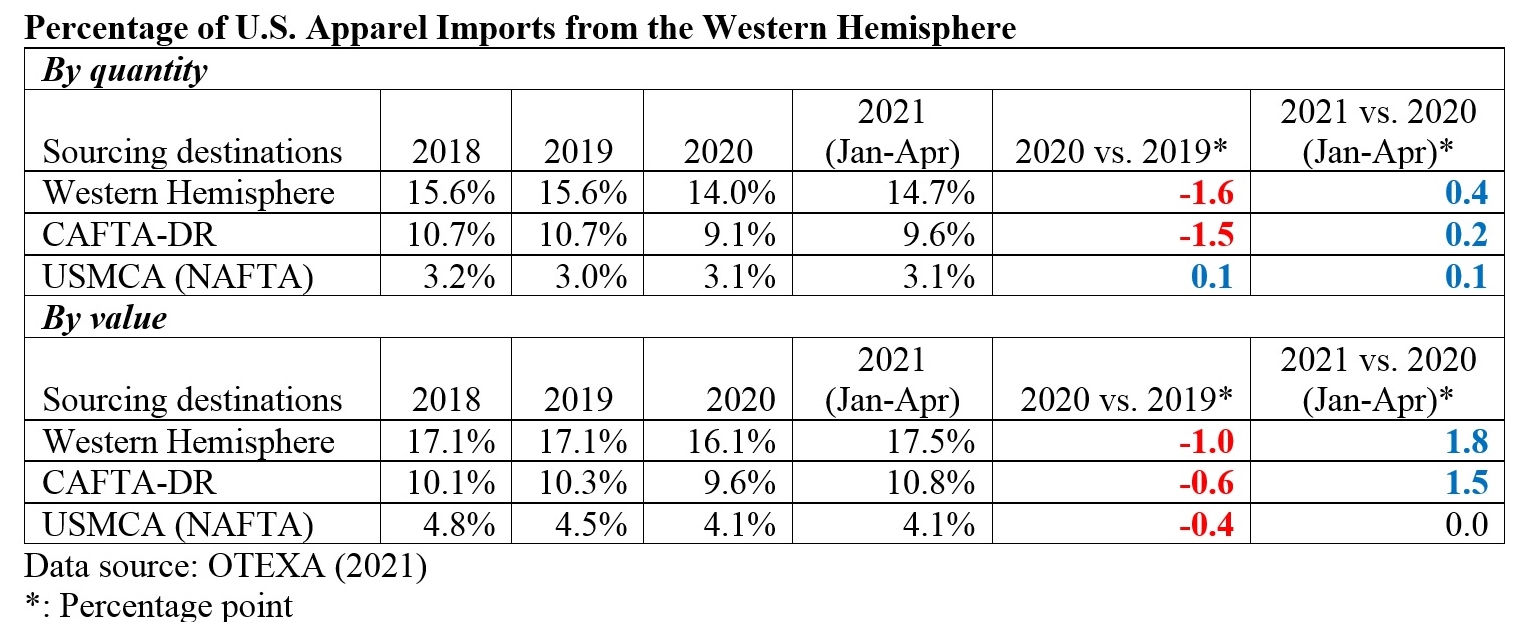

Fourth, U.S. apparel sourcing from CAFTA-DR members gains new momentum, reflecting the strong interest in sourcing more from the region from the business community and policymakers. For example, 17.5% of U.S. apparel imports came from the Western Hemisphere in 2021 (Jan-Apr), higher than 16.1% in 2020 and 17.1% before the pandemic. Notably, CAFTA-DR members’ market shares increased to 10.8% in 2021 (Jan-Apr) from 9.6% in 2020. The value of U.S. apparel imports from CAFTA-DR also enjoyed a 25.8% growth in 2021 (Jan-Apr) from a year ago, one of the highest among all sourcing destinations. The imports from El Salvador (up 29.2%), Honduras (up 28.0%), and Guatemala (27.0%) had grown particularly fast in 2021.

Meanwhile, U.S. apparel imports from USMCA members stayed stable overall. CAFTA-DR and USMCA members currently account for around 60% and 25% of U.S. apparel imports from the Western Hemisphere. They are also the single largest export market for U.S. textile products (around 70%). The Biden administration has signaled its strong interest in strengthening the western hemisphere textile and apparel supply chain by leveraging CAFTA-DR along with other trade policy tools.

by Sheng Lu

The apparel industry has made a great recovery, and the April 2021 numbers had recovered almost fully to match the April 2019 numbers, the industry post-covid still remains unstable. Even though we are seeing the light at the end of the tunnel regarding the pandemic, I can’t see the apparel industry remaining completely stable for a while longer. As the article stated, the April 2021 value of US apparel imports dropped 11.2% from March 2021 which shows some instability. I believe as countries and economies continue to recover from the pandemic, we will not be able to expect a completely stable industry.

Trends of apparel and textile sourcing are moving from China to other Asian countries in an effort to diversify. This could be also because China wasn’t a reliable supplier for a product and the buyer had to go to another Asian country to supply their needs. With shortages following COVID-19, it has caused a negative impact on some suppliers because the product is’t able to be bought, or certain material couldn’t be collected to make the product consumers are demanding. To meet demand, buyers have had to shift focus to other countries that could meet the demand they need to supply. The fashion industry will most likely remain on an unstable trend as long as increased shortages in the supply chain continue to happen.

Based on the figures given, it appears that the value of U.S. apparel imports is roughly back to normal. Although it is slightly below previous levels, this is still a good indicator that the worst of COVID-19’s impact is over. Xinjiang has been in and out of the news lately for reports of slave labor used in production of cotton in the region. It is nice to see public outrage about something like this happening because it will push companies to change their sourcing habits so that they do not receive backlash.

There’s no doubt that Asia will remain the top supplier for the U.S. but the instability comes when discussing which Asian countries we continue doing business with, whether it be China or other Asian countries. Because of COVID-19 regulations and other factors caused by the pandemic such as shortages and delays, shifts in reliability are occurring and causing the instability in the textile and apparel industry.

you mentioned “instability” and “shifts in reliability” great words, but What do they mean?

It’s refreshing to see some good news about the apparel industry after such a long and detrimental period. We are seeing an increase of 66% in the value of U.S. apparel imports since the beginning of the pandemic. Although this sounds promising, it’s not guaranteed that it will remain steady. For example, the value of U.S. imports actually decreased by 11.2% in just one month (March-April). I’m interested to see just how long it will take to get back on track and maintain a steady slope. Another topic that was mentioned in this post was the increase in apparel imports from the western hemisphere. Obviously, the pandemic had a huge effect on imported goods, which led the United States to begin sourcing their materials from other countries within the western hemisphere. Whereas China was a main source of imports to the U.S. prior to COVID19, we are now starting to stray away from China and move apparel sourcing orders to other Asian countries.