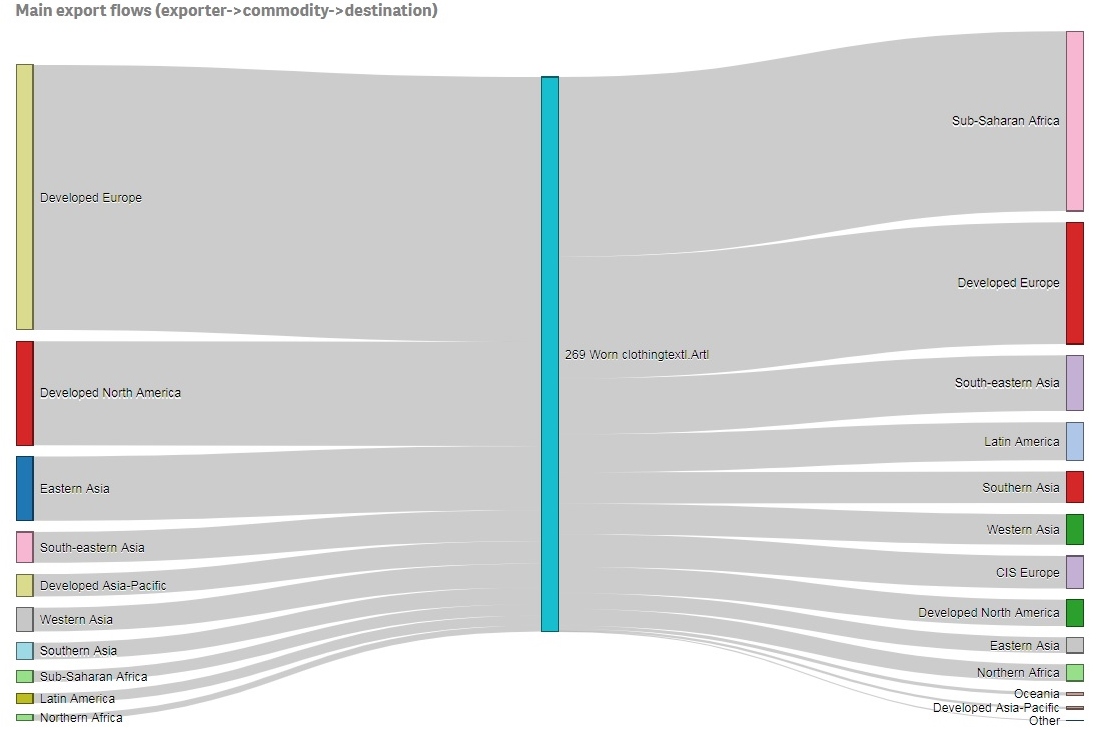

This study intends to explore the key factors that affect the volume of a country’s used clothing exports. Notably, the world’s used clothing exports (defined as the Harmonized System code 6309) substantially increased from only $2.5 billion in 2009 to over $4.2 billion in 2019, or up 63.4% (UNComtrade, 2021). While numerous studies have explored the patterns of used clothing imports and their social-economic impacts on the importing countries, what drives a country’s used clothing exports remains largely unknown.

In the study, we conducted a regression analysis of 37 countries’ used clothing exports in 2019 (or over 90% of the value of the world’s used clothing exports that year) (UNComtrade, 2021). The explanatory factors we considered include new clothing sales (2018-2019), new clothing retail price (2018-2019), population (2019), and country classification (developed or developing in 2019). The results show that:

- First, there is a strong positive relationship between a country’s new clothing sales and its used clothing exports. On average, a 1% increase in new clothing sales would result in a 0.85% increase in used clothing exports when holding other factors constant.

- Second, as new clothing gets cheaper in the retail market, a country would export more used clothing and vice versa. Specifically, when the retail price for new clothing decreases by 1%, the value of used clothing export could increase by 1.2% on average when holding other factors constant.

- Third, when holding other factors constant, used clothing exports from developed countries were 56% higher than in developing economies. Lower-income levels and various other social-economic factors (such as the awareness of sustainability and used clothing collection mechanism) could be the factors behind the phenomenon.

- Fourth, the size of the population has NO significant impact on a country’s used clothing exports. This explains why a developed economy with a relatively small population (such as the Netherlands and Canada) exported far more used clothing than a populous developing one (such as India and Indonesia) in 2019 (Uncomtrade, 2021).

The study’s findings create new knowledge about the primary factors affecting the patterns of used clothing exports and have several important implications. First, the results suggest that we can do more on the supply side to curb the surge of used clothing exports, given the rising concerns about its controversial impacts on the developing world and the environment. Particularly, encouraging consumers to purchase fewer new clothing and shop more “slowly” can be among the most effective ways to reduce the supply of used clothing. Second, echoing the finding of existing studies, the results confirm the significant price impact on the generation of used clothing exports. Notably, the result reminds us about the enormous social-economic and environmental “cost” of selling new clothing too cheaply. Additionally, the findings suggest that developed countries have a crucial role in addressing the used clothing export problem, even those with a relatively small population.

By Aline Gomes Siqueira and Dr. Sheng Lu

Note: The study will be presented at the 2021 International Textile and Apparel Association (ITAA) Annual Conference in November.