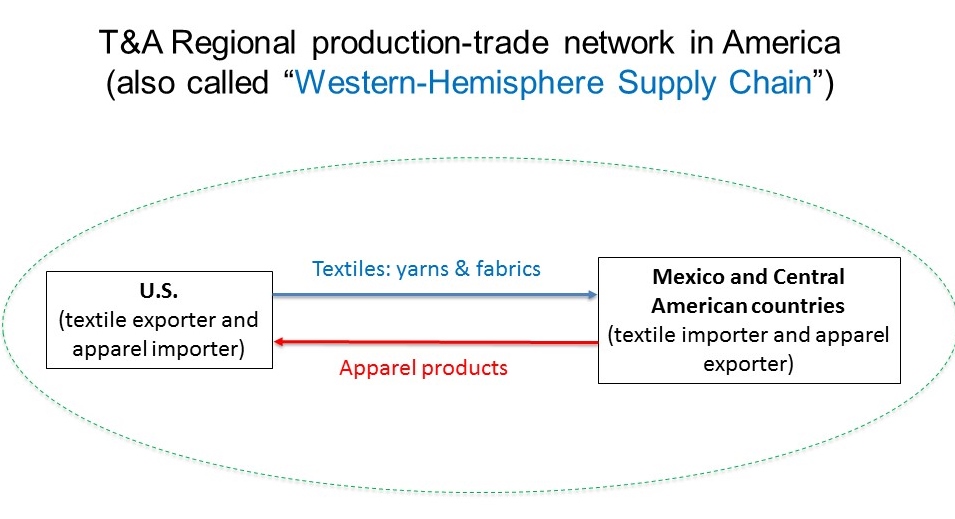

Within the Western-Hemisphere (WH) textile and apparel supply chain, the United States serves as the leading textile supplier, whereas developing countries in North, Central, and South America (such as Mexico and countries in the Caribbean region) assemble imported textiles from the United States or elsewhere into apparel. The majority of clothing produced in the area is eventually exported to the United States or Canada.

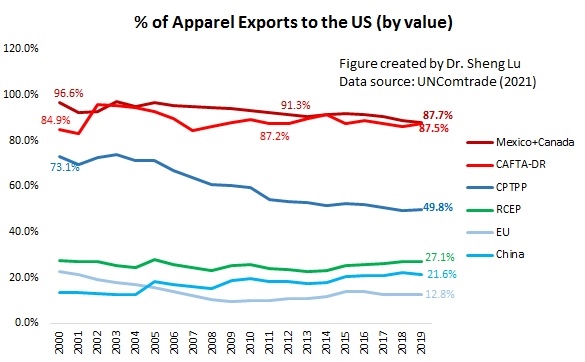

WH countries still form a close supply chain partnership in textile and apparel production. For example, close to 70% of US textile exports went to WH members in 2020, a pattern that has stayed stable over the past decades (OTEXA, 2021). Meanwhile, the United States serves as the single largest export market for most apparel exporting countries in the WH For example, in 2019, close to 89% of apparel exports from CAFTA-DR and USMCA (NAFTA) members went to the US.

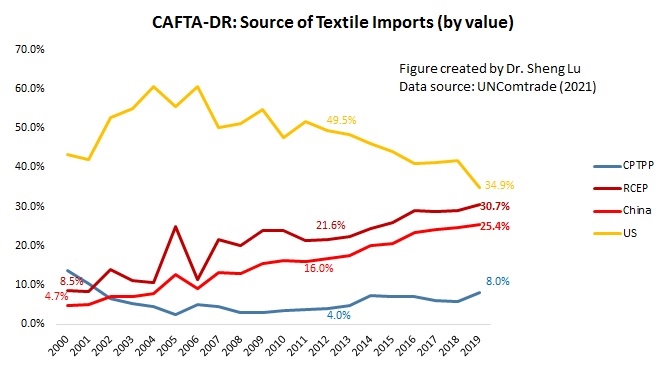

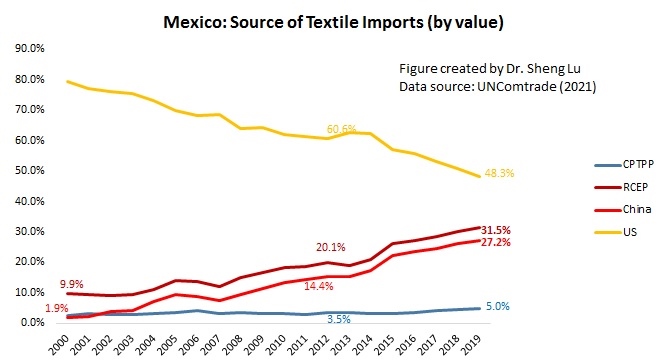

However, the WH textile and apparel supply chain is not without significant challenges. For example, CAFTA-DR and Mexico are increasingly using textiles inputs from outside the WH region, which weakens the US role as a dominant textile supplier. Notably, most of the market shares lost by US textile suppliers are fulfilled by Asian countries, including China and other members of the RCEP (Regional Comprehensive Economic Partnership). Theoretically, using cheaper textile inputs from Asia may help apparel producing countries in the WH improve the price competitiveness of their finished garments and diversify their export markets beyond the US.

Meanwhile, despite the apparent popularity of “near-sourcing”, no evidence suggests that US fashion brands and retailers are sourcing more from WH countries, including CAFTA-DR and USMCA (NAFTA) members. Neither the US-China trade war nor COVID-19 seems to have shifted the trends. Instead, close to 75%-80% of US apparel imports still come from Asian countries (OTEXA, 2021). Studies further show that a vast majority of US apparel imports from WH concentrate on a limited category of products, such as tops and bottoms, which is far from sufficient to meet retailers’ sourcing needs.

On the other hand, technical textiles and industrial textiles account for a growing share in the total US textile exports, and Asia is a particularly fast-growing market. However, there is few US free trade agreement with Asian countries, making it a disadvantage to promote “Made in the USA” products in these markets. It is debatable what should be the priority for the US textile and apparel trade policy: to continue to protect the exports of yarn and fabrics to the WH or open new export markets for technical and industrial textiles outside the WH region?

by Sheng Lu

Relate readings:

- Keough, K., & Lu, S. (2020). Explore the export performance of textiles and apparel “Made in the USA”: A firm-level analysis. Journal of the Textile Institute.

- Lu, S. (2018). What will happen to the U.S. textile and apparel industry if the NAFTA goes? Margin: The Journal of Applied Economic Research, 12(2), 113-137.

- Lu, S. (2021).Regional supply chains still shape textile and apparel trade. Just-Style.