The China National Textile and Apparel Council (CNTAC), the governing body of China’s textile and apparel industry, recently released its 14th five-year plan, detailing the development objectives, growth strategies, and priority tasks for China’s textile and apparel sector from 2021 to 2025. Unlike most market economies, the “five-year plan” serves as China’s top economic development guidelines. Therefore, companies at the micro-level study and follow the “five-year” plan closely to ensure their corporate business strategies align with the tones and visions set out by policymakers.

Based on the plan, several trends are worth watching regarding the future of China’s textile and apparel industry:

#1 Complicated by both economic and non-economic factors, the growth prospect for China’s textile and apparel industry is facing more uncertainties over the next five years.

#2 “Growing bigger” will no longer be a priority for China’s textile and apparel sector over the next five years. However, China has no intention to cut textile and apparel production capacity or shrink its size substantially either.

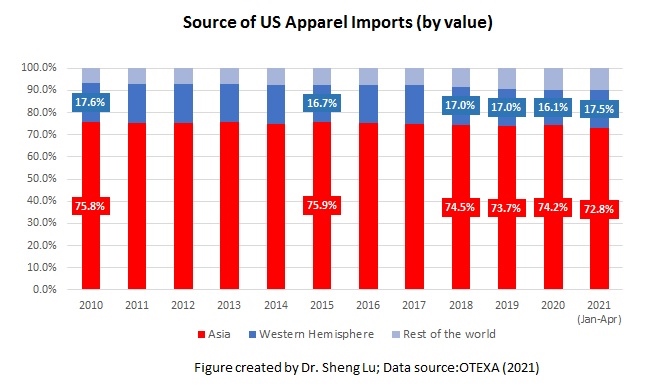

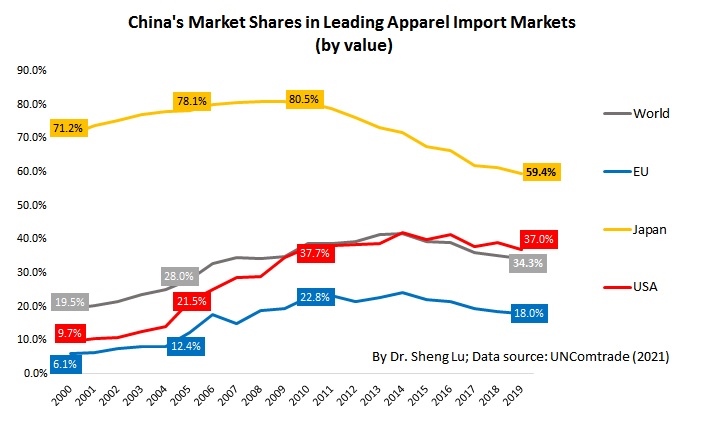

#3 China intends to develop a more sophisticated and high-tech-driven textile and apparel industry and engage in more value-added functions in the supply chain. Notably, in recent years, while China’s shares in the total world apparel exports declined, China is playing a more significant role as a textile supplier for many apparel exporting countries, especially in Asia.

#4 As the export market deteriorated, China plans to rely more heavily on its domestic market to support the textile and apparel industry’s growth. Industry sources predict that China’s annual clothing retail sales could exceed $415 billion by 2025 (vs. $347 billion in the U.S.).

#5 China will continue its efforts in “going global,” i.e., investing in textile and apparel factories overseas, mainly through the “Belt and Road Initiative.” According to CNTAC, China’s outbound foreign investments in the textile and apparel sector exceeded $6.7 billion from 2015 to 2020. Nearly $1.8 billion (or 26.6%) went to neighboring southeast Asian countries, including Vietnam, Cambodia, Thailand, Lao, and Myanmar.

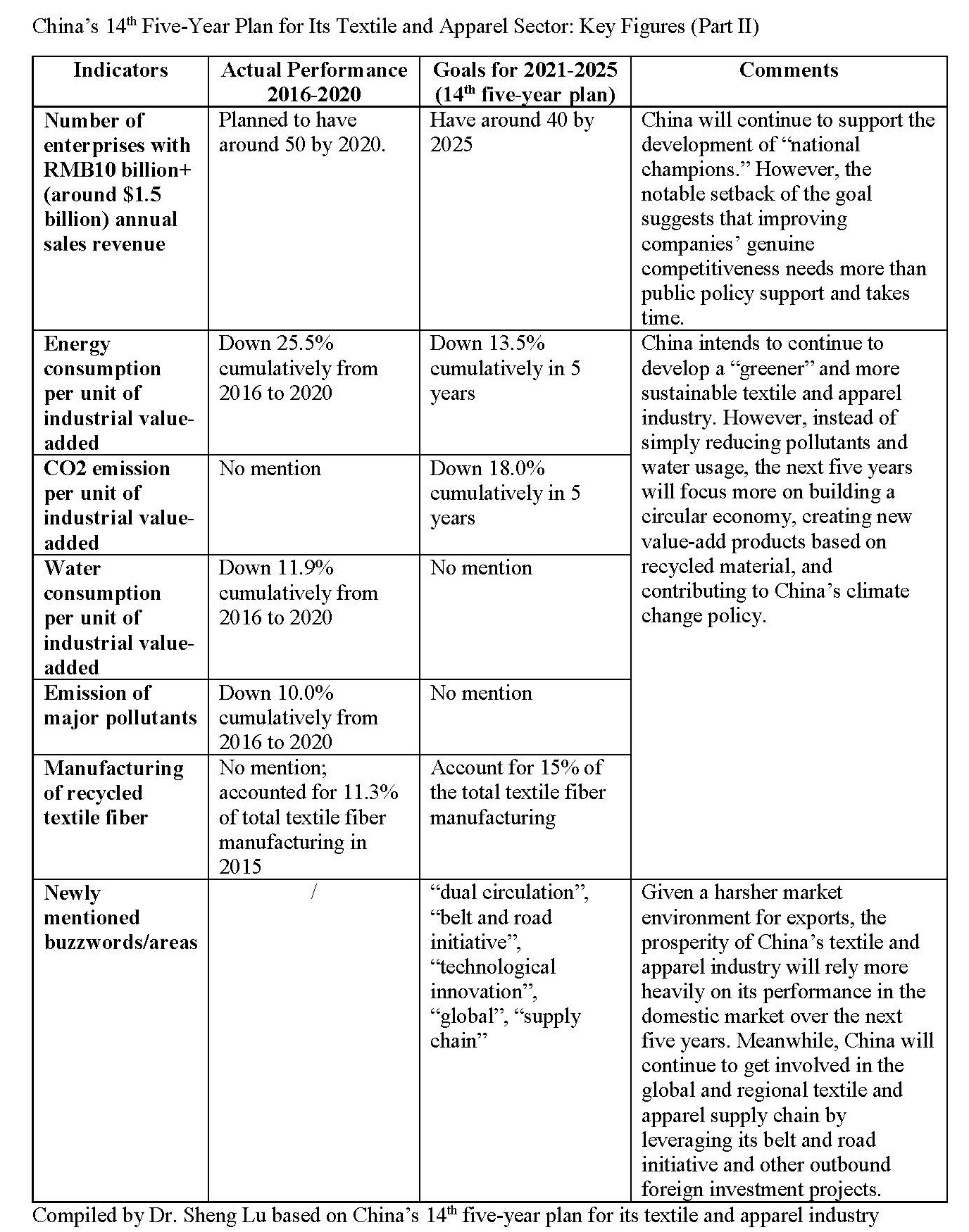

#6 China intends to develop a “greener” and more sustainable textile and apparel industry. However, instead of simply reducing pollutants and water usage, China plans to develop a sustainability-led growth model, emphasizing areas including circular economy and creating new value-added products based on recycled material.

By Sheng Lu

Further reading: Lu,Sheng (2021). The plan for China textiles and apparel over the next 5 years. Just-Style.