What is RCEP?

The Regional Comprehensive Economic Partnership (RCEP) is a free trade agreement between ten member states of the Association of Southeast Asian Nations (ASEAN)* and five other large economies in the Asia-Pacific region (China, Japan, South Korea, New Zealand, and Australia). RCEP was reached on November 15, 2020, after nearly eight years of tough negotiation. (Note: ASEAN members include Brunei, Cambodia, Indonesia, Laos, Malaysia, Myanmar, the Philippines, Singapore, Thailand, and Vietnam. India was an original RCEP member but decided to quit in late 2019 due to concerns about competing with Chinese products, including textiles and apparel.)

So far, RCEP is the world’s largest trading bloc. As of 2019, RCEP members accounted for nearly 26.2% of world GDP, 29.5% of world merchandise exports, and 25.9% of world merchandise imports.

As of November 1, 2021, Lao, Burnei, Cambodia, Singapore and Thailand (ASEAN members), as well as China, Japan, New Zealand and Australia have ratified the agreement. This has met the minimum criteria for RCEP to enter into force (i.e., six members, including at least three ASEAN members and three non-ASEAN members).

As announced by Australia on November 2, 2021, RCEP will enter into force on January 1, 2022

Why RCEP matters to the textile and apparel industry?

RCEP matters significantly for the textile and apparel (T&A) sector. According to statistics from the United Nations, in 2019, the fifteen RCEP members altogether exported US$374 billion worth of T&A (or 50% of the world share) and imported US$139 billion (or 20% of the world share).

In particular, RCEP members serve as critical apparel-sourcing bases for many US and EU fashion brands. For example, in 2019, close to 60% of US apparel imports came from RCEP members, up from 45% in 2005. Likewise, in 2019, 32% of EU apparel imports also came from RCEP members, up from 28.1% in 2005.

Notably, RCEP members have been developing and forming a regional textile and apparel supply chain. More economically advanced RCEP members (such as Japan, South Korea, and China) supply textile raw materials to the less economically developed countries in the region within this regional supply chain. Based on relatively lower wages, the less developed countries typically undertake the most labor-intensive processes of apparel manufacturing and then export finished apparel to major consumption markets worldwide.

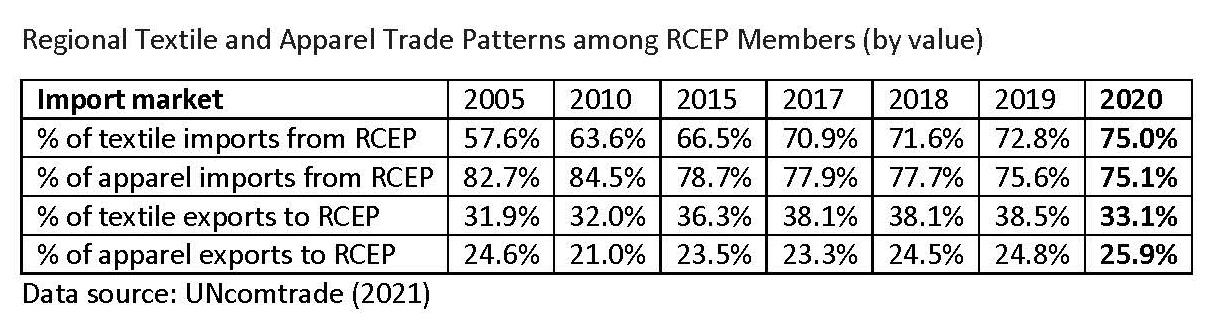

As a reflection of an ever more integrated regional supply chain, in 2019, as much as 72.8% of RCEP members’ textile imports came from other RCEP members, a substantial increase from only 57.6% in 2005. Nearly 40% of RCEP members’ textile exports also went to other RCEP members in 2019, up from 31.9% in 2005.

What are the key provisions in RCEP related to textiles and apparel?

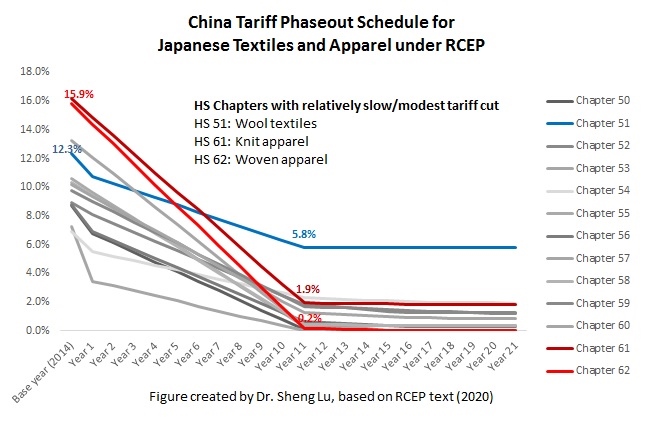

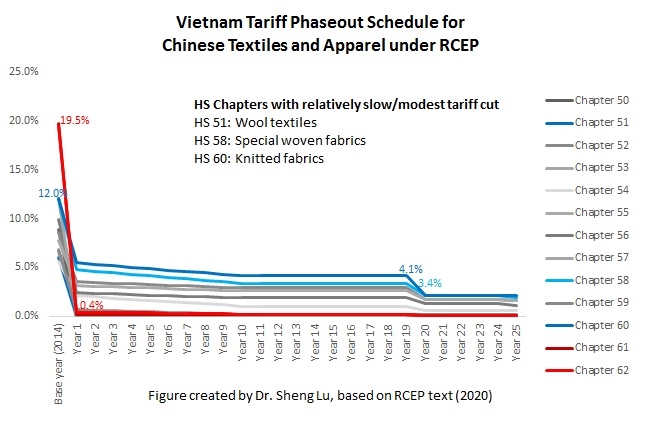

First, RCEP members have committed to reducing the tariff rates to zero for most textile and apparel traded between RCEP members on day one after the agreement enters into force. That being said, the detailed tariff phaseout schedule for textile and apparel products under RCEP is very complicated. Each RCEP member sets their own tariff phaseout schedule, which can last more than 20 years (for example, 34 years for South Korea and 21 years for Japan.) Also, different from U.S. or EU-based free trade agreements, the RCEP phaseout schedule is country-specific. For example, South Korea sets different tariff phaseout schedules for textile and apparel products from ASEAN, China, Australia, Japan, and New Zealand. Japan’s tariff cut for apparel products is more generous toward ASEAN members and less so for China and South Korea (see the graph above). Companies interested in taking advantage of the duty-free benefits under RCEP need to study the “rules of the game” in detail.

Second, in general, RCEP adopts very liberal rules of origin for apparel products. It only requires that all non-originating materials used in the production of the good have undergone a tariff shift at the 2-digit HS code level (say a change from any chapters from chapters 50-60 to chapter 61). In other words, RCEP members are allowed to source yarns and fabrics from anywhere in the world, and the finished garments will still qualify for duty-free benefits. Most garment factories in RCEP member countries can immediately enjoy the RCEP benefits without adjusting their current supply chains.

What are the potential economic impacts of RCEP on the textile and apparel sector?

On the one hand, the implementation of RCEP is likely to further strengthen the regional textile and apparel supply chain among RCEP members. Particularly, RCEP will likely strengthen Japan, South Korea, and China as the primary textile suppliers for the regional T&A supply chain. Meanwhile, RCEP will also enlarge the role of ASEAN as the leading apparel producer in the region.

On the other hand, as a trading bloc, RCEP could make it even harder for non-RCEP members to get involved in the regional textile and apparel supply chain formed by RCEP members. Because an entire regional textile and apparel supply chain already exists among RCEP members, plus the factor of speed to market, few incentives are out there for RCEP members to partner with suppliers from outside the region in textile and apparel production. The tariff elimination under the RCEP will put textile and apparel producers that are not members of the agreement at a more significant disadvantage in the competition. Not surprisingly, according to a recent study, measured by value, only around 21.5% of RCEP members’ textile imports will come from outside the area after the implementation of the agreement, down from the base-year level of 29.9% in 2015.

Further, the reaching of RCEP could accelerate the negotiation of other trade agreements in the Asia-Pacific region, such as the China-South Korea-Japan Free Trade Agreement. We might also see growing pressures on the Biden administration to join the Comprehensive and Progressive Agreement of the Trans-Pacific Partnership (CPTPP) to strengthen the US economic ties with countries in the Asia-Pacific region. The economic competition between the United States and China in the area could also intensify as the combined effects of RCEP and CPTPP begin to shape new supply chains and test the impacts of the two countries on the regional trade patterns.

By Sheng Lu

Further reading

- Regional Comprehensive Economic Partnership (RCEP): What Does it Mean for US Apparel Sourcing from Asia? (2021 TexworldUSA webinar)

- Lu, S. (2021). Why Why does the Regional Comprehensive Economic Partnership matter to apparel?. Just-Style

- Lu, S. (2019). Regional Comprehensive Economic Partnership (RCEP): Impact on the integration of textile and apparel supply chain in the Asia-Pacific region. In Shen, B., Gu, QL., Yang, YX (Eds), Fashion Supply Chain Management in Asia: Concepts, Models and Cases. Springer.