According to the video, how has the supply chain for apparel and footwear changed over the past decade?

What are the pros and cons of moving from a global supply chain to a regional one for fashion companies?

For fashion companies interested in “near-shoring” and “re-shoring”, what factors should they consider? Why?

Anything else you find interesting/intriguing/thought-provoking/debatable in the video? Why?

Note: Everyone is welcome to join our online discussion. For students in FASH455, please address at least two questions. Please mention the question number # (no need to repeat the question) in your comment.

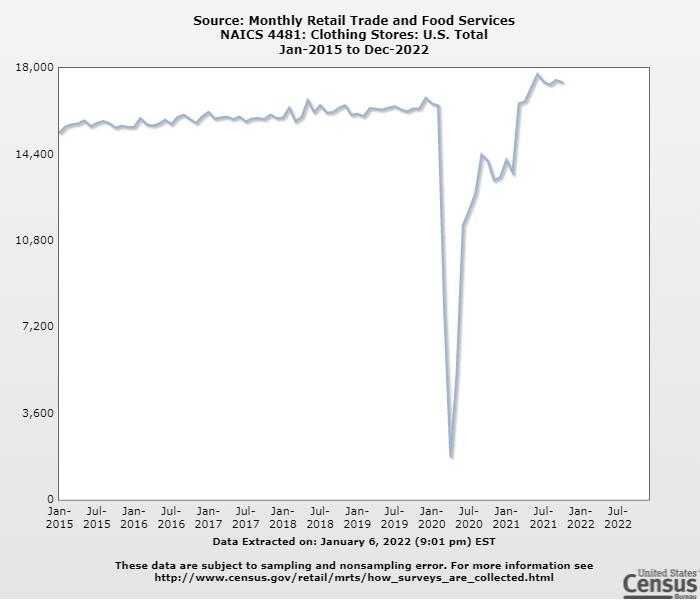

First, US apparel imports continue to rebound in November 2021 as companies build the inventory for the holiday season. Thanks to US consumers’ strong demand and the upcoming holidays, the value of US apparel imports went up by 15.7% in November 2021 from a month ago (seasonally adjusted) and increased by as much as 39.7% from 2020. However, before the pandemic, the value of US apparel imports always peaked in October and then gradually slipped in November and December. The unusual surge of imports in November 2021 could be the combined effects of price inflation and the late arrival of goods due to the shipping crisis.

Meanwhile, US apparel imports so far in 2021 have been far more volatile than in the past few years because of uncertainties and disruptions caused by COVID-19 and the shipping crisis. For example, the year-over-year (YoY) growth rate ranged from 131% in May to 17.6% in July, causing fashion companies additional inventory planning and supply chain management challenges. Unfortunately, the new omicron variant could worsen the market uncertainty and volatility.

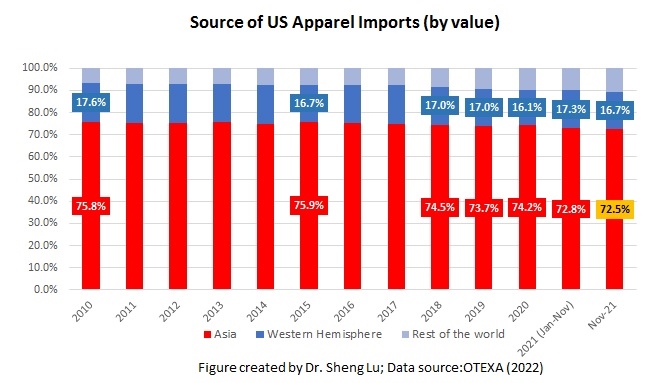

Second, Asian countries remain the dominant sourcing base for US fashion companies as the production capacity elsewhere is limited. Asian countries’ market shares fell from 74.2% in 2020 to 71.3% in July 2021, primarily because of the COVID lockdowns in Vietnam and Bangladesh. US apparel imports came from Asian countries rebounded to 74.8% and 72.5% in October and November 2021, respectively. This result suggests a lack of alternative sourcing destinations outside Asia, especially for large volume items. Meanwhile, the worsening shipping crisis affecting the route from Asia to North America could explain why Asian suppliers’ market shares in November were somewhat lower than a month ago.

Third, US companies continue to treat China as one of their essential sourcing bases in the current business environment. However, companies are NOT reversing their long-term strategy of reducing “China exposure.” China stays the largest supplier for the US market in November 2021, accounting for 41.5% of total US apparel imports in quantity and 25.8% in value. Due to the seasonal factor, China’s market shares typically peak from June to September and then drop from October until March-April.

Both industry sources and the export product diversification index also consistently show that China supplied the most variety of products to the US market with no near competitors. In comparison, US apparel imports from Bangladesh, Mexico, and CAFTA-DR members concentrate more on specific product categories.

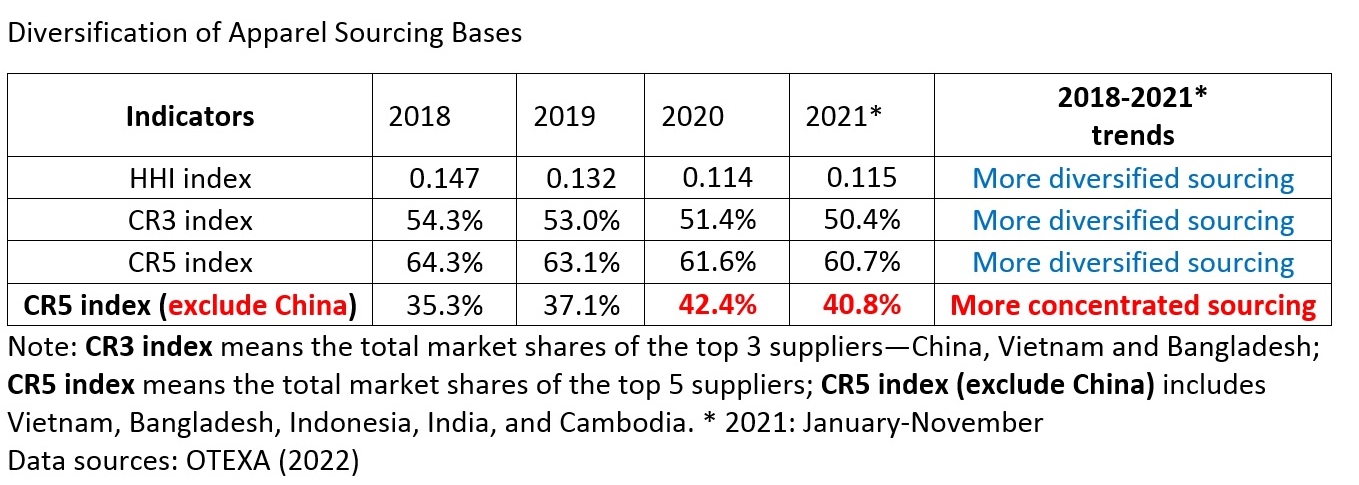

Nevertheless, the HHI index and market concentration ratios (CR3 and CR5) calculated based on the latest data suggest that US fashion companies continue to move their apparel sourcing orders from China to other Asian countries overall. For example, only around 15% of US cotton apparel comes from China, compared with about 27% in 2018. My latest studies also indicate that it has become ever more common to see a fashion company places only around 10% of its total sourcing value or volume from China compared to over 30% in the past. Furthermore, with the growing tensions of the US-China relations and the newly enacted Uyghur Forced Labor Prevention Act, fashion companies could take another look at their China sourcing strategy to avoid potential high-impact disruptions.

Fourth, near sourcing from the Western Hemisphere, especially CAFTA-DR members, continue to gain popularity. Specifically, 17.3% of US apparel imports came from the Western Hemisphere year-to-date (YTD) in 2021 (January-November), higher than 16.1% in 2020. Notably, CAFTA-DR members’ market shares increased to 10.6% in 2021 (January to November) from 9.6% in 2020. The value of US apparel imports from CAFTA-DR also enjoyed a 41.7% growth in 2021 (January—November) from a year ago, one of the highest among all sourcing destinations. The imports from El Salvador (up 42.6%), Honduras (up 47.1%), and Guatemala (36.6%) had grown particularly fast so far in 2021. However, the political instability in some Central American countries could make fashion companies feel hesitant to permanently switch their sourcing orders to the region or make long-term investments.

Additionally, the latest trade data suggests a notable increase in the price of US apparel imports. Notably, the unit price of US apparel imports from almost all leading sources went up by more than 10% from January 2021 to November 2021. As worldwide inflation continues, the rising sourcing cost pressure won’t ease anytime soon.