(See updated analysis: Patterns of US Apparel Imports in the First Half of 2022 and Key Sourcing Trends)

The latest trade data shows that in the first four months of 2022, US apparel imports increased by 40.6% in value and 25.9% in quantity from a year ago. However, the seemingly robust import expansion is shadowed by the rising market uncertainties.

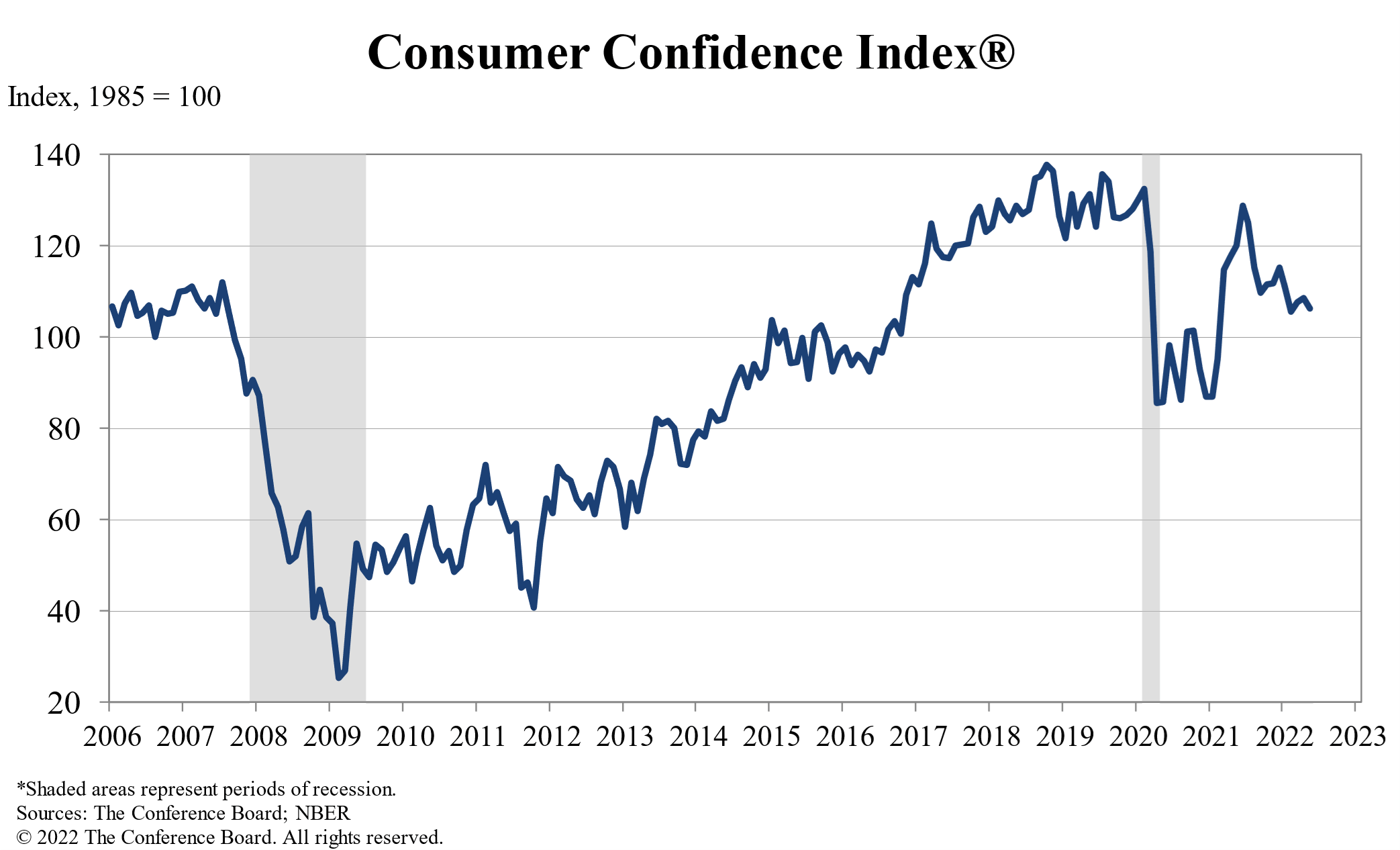

Uncertainty 1: US economy. As the US economic growth slows down, consumers have turned more cautious about discretionary spending on clothing to prioritize other necessities. Notably, in the first quarter of 2022, clothing accounted for only 3.9% of US consumers’ total expenditure, down from 4.3% in 2019 before the pandemic. Likewise, according to the Conference Board, US consumers’ confidence index (CCI) dropped to 106.4 (1985=100) in May 2022 from 113.8 in January 2022, confirming consumers’ increasing anxiety about their household’s financial outlook.

Removing the seasonal factor, US apparel imports in April 2022 went up 2.8% in quantity and 3.0% in value from March 2022, much lower than 9.3% and 11.9% a month ago (i.e., March 2022 vs. February 2022). The notable slowed import growth reflects the negative impact of inflation on US consumers’ clothing spending. According to the Census, the value of US clothing store sales marginally went up by 0.8% in April 2022 from a month ago, also the lowest so far in 2022.

Uncertainty 2: Worldwide inflation. Data from the Bureau of Economic Analysis shows that the price index of US apparel imports reached 103.1 in May 2022 (May 2020=100), up from 100.3 one year ago (i.e., a 2.8% price increase). At the product level (i.e., 6-digit HS Code, HS Chapters 61-62), over 60% of US apparel imports from leading sources such as China, Vietnam, Bangladesh, and CAFTA-DR experienced a price increase in the first quarter of 2022 compared with a year ago. The price surge of nearly 40% of products exceeded 10 percent. As almost everything, from shipping, textile raw materials, and labor to energy, continues to soar, the rising sourcing costs facing US fashion companies are not likely to ease anytime soon.

The deteriorating inflation also heats up the debate on whether to continue the US Section 301 tariff action against imports from China. Since implementing the punitive tariffs, US fashion companies have to pay around $1 billion in extra import duties every year, resulting in the average applied import tariff rate for dutiable apparel items reaching almost 19%. Although some e-commerce businesses took advantage of the so-called “de minimis” rule (i.e., imports valued at $800 or less by one person on a day are not required to pay tariffs), over 99.8% of dutiable US apparel imports still pay duties.

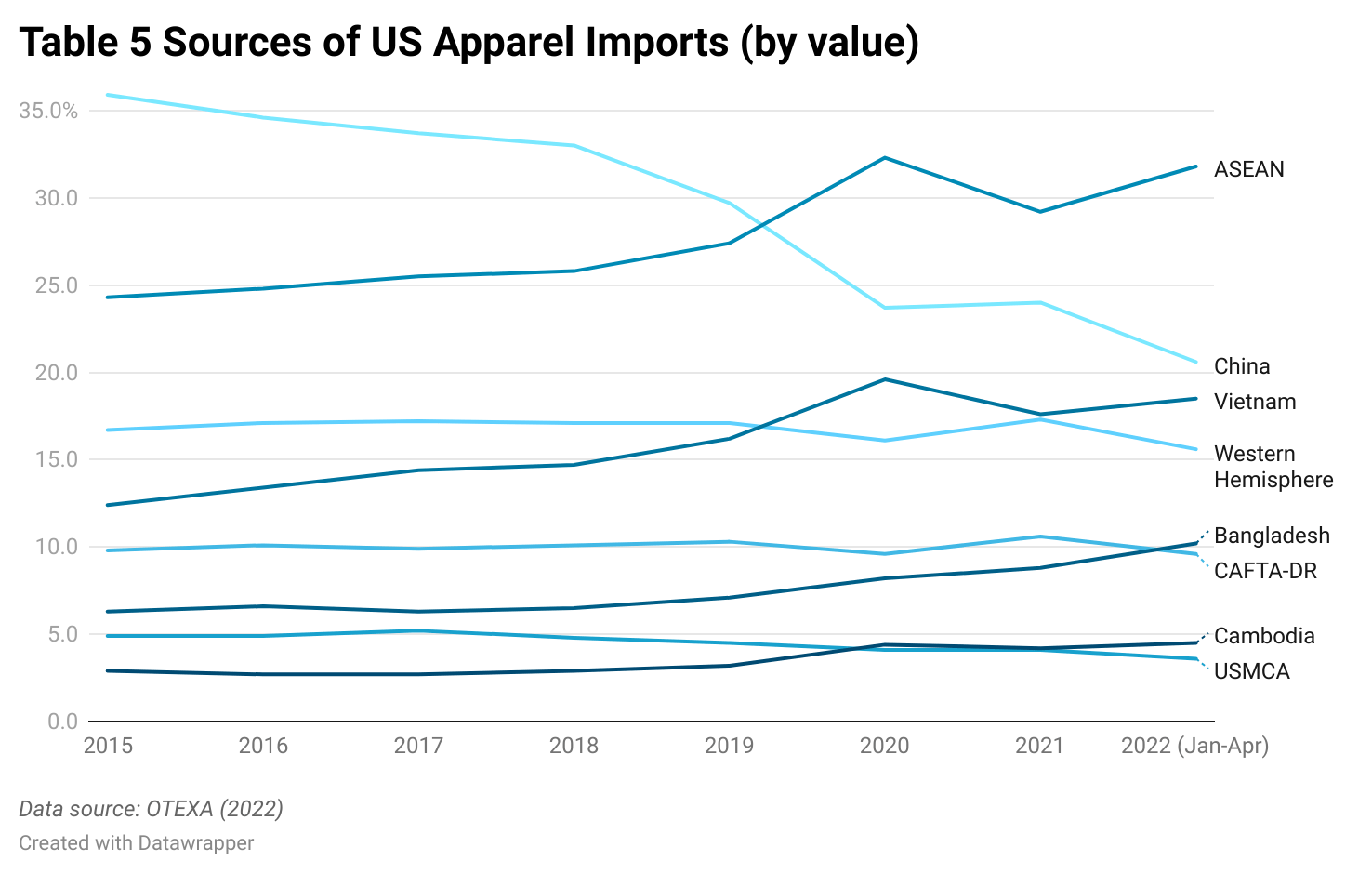

Uncertainty 3: “Made in China.” US apparel imports from China in April 2022 significantly dropped by 26.7% in quantity and 24.6% in value from March 2022 (seasonally adjusted). China’s market shares also fell to a new record low of 26.3% in quantity and 16.8% in value in April 2022. The zero-COVID policy and new lockdown undoubtedly was a critical factor contributing to the decline. Fashion companies’ concerns about the trajectory of the US-China relations and the upcoming implementation of the new Uyghur Forced Labor Prevention Act (UFLPA) are also relevant factors. For example, only 10.5% of US cotton apparel imports came from China in April 2022, a further decline from about 15% at the beginning of the year. Given the expected challenges of meeting the rebuttable presumption requirements in UFLPA and the high compliance costs, it is not unlikely that US fashion companies may continue to reduce their China exposure.

As US fashion companies source less from China, they primarily move their sourcing orders to China’s competitors in Asia. Measured in value, about 74.8% of US apparel imports came from Asia so far in 2022 (January-April), up from 72.8% a year ago. In comparison, there is no clear sign that more sourcing orders have been permanently moved to the Western Hemisphere. For example, in April 2022, CAFTA-DR members accounted for 9.3% of US apparel imports in quantity (was 10.8% in April 2021) and 10.2% in value (was 11.4% in April 2021).

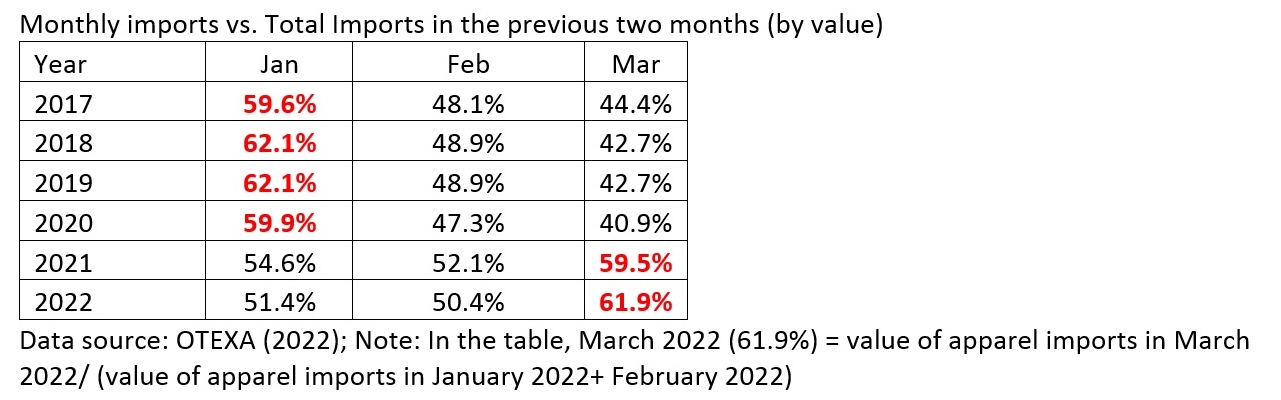

Uncertainty 4: Shipping delays. Data suggests we are not out of the woods yet for shipping delays and supply chain disruptions. For example, as Table 2 shows, the seasonable pattern of US apparel imports in March 2022 is similar to January before the pandemic (2017-2020). In other words, many US fashion companies still face about 1.5-2 months of shipping delays. Additionally, several of China’s major ports were under strict COVID lockdowns starting in late March, including Shanghai, the world’s largest. Thus, the worsened supply chain disruptions could negatively affect the US apparel import volumes in the coming months.

by Sheng Lu

Further reading: Lu, S. (2022). Myanmar loses appeal for US apparel imports. Just-Style.