On September 2, 2022, the Office of the US Trade Representative (USTR) announced it would continue the billions of dollars of Section 301 punitive tariffs against Chinese products. USTR said it made the decision based on requests from domestic businesses benefiting from the tariff action. As a legal requirement, USTR will launch a full review of Section 301 tariff action in the coming months.

In her remarks at the Carnegie Endowment for International Peace on Sep 7, 2022, US Trade Representative Katharine Tai further said that the Section 301 punitive tariffs on Chinese imports “will not come down until Beijing adopts more market-oriented trade and economic principles.” In other words, the US-China tariff war, which broke out four years ago, is not ending anytime soon.

A Brief History of the US Section 301 tariff action against China

The US-China tariff war broke out as both unexpected and not too surprising. For decades, the US government had been criticizing China for its unfair trade practices, such as providing controversial subsidies to state-owned enterprises (SMEs), insufficient protection of intellectual property rights, and forcing foreign companies to transfer critical technologies to their Chinese competitors. The US side had also tried various ways to address the problems, from holding bilateral trade negotiations with China and imposing import restrictions on specific Chinese goods to suing China at the World Trade Organization (WTO). However, despite these efforts, most US concerns about China’s “unfair” trade practices remain unsolved.

When former US President Donald Trump took office, he was particularly upset about the massive and growing US trade deficits with China, which hit a record high of $383 billion in 2017. In alignment with the mercantilism view on trade, President Trump believed that the vast trade deficit with China hurt the US economy and undermined his political base, particularly with the working class.

On August 14, 2017, President Trump directed the Office of the US Trade Representative (USTR) to probe into China’s trade practices and see if they warranted retaliatory actions under the US trade law. While the investigation was ongoing, the Trump administration also held several trade negotiations with China, pushing the Chinese side to purchase more US goods and reduce the bilateral trade imbalances. However, the talks resulted in little progress.

President Trump lost his patience with China in the summer of 2018. In the following months, citing the USTR Section 301 investigation findings, the Trump administration announced imposing a series of punitive tariffs on nearly half of US imports from China, or approximately $250 billion in total. As a result, for more than 1,000 types of products, US companies importing them from China would have to pay the regular import duties plus a 10%-25% additional import tax. However, the Trump administration’s trade team purposefully excluded consumer products such as clothing and shoes from the tariff actions. The last thing President Trump wanted was US consumers, especially his political base, complaining about the rising price tag when shopping for necessities. The timing was also a sensitive factor—the 2018 congressional mid-term election was only a few months away.

President Trump hoped his unprecedented large-scale punitive tariffs would change China’s behaviors on trade. It partially worked. As the trade frictions threatened economic growth, the Chinese government returned to the negotiation table. Specifically, the US side wanted China to purchase more US goods, reduce the bilateral trade imbalances and alter its “unfair” trade practices. In contrast, the Chinese asked the US to hold the Section 301 tariff action immediately.

However, the trade talks didn’t progress as fast as Trump had hoped. Even worse, having to please domestic forces that demanded a more assertive stance toward the US, the Chinese government decided to impose retaliatory tariffs against approximately $250 billion US products. President Trump felt he had to do something in response to China’s new action. In August 2019, he suddenly announced imposing Section 301 tariffs on a new batch of Chinese products, totaling nearly $300 billion. As almost everything from China was targeted, apparel products were no longer immune to the tariff war. With the new tariff announcement coming at short notice, US fashion brands and retailers were unprepared for the abrupt escalation since they typically placed their sourcing orders 3-6 months before the selling season.

Nevertheless, Trump’s new Section 301 actions somehow accelerated the trade negotiation. The two sides finally reached a so-called “phase one” trade agreement in about two months. As part of the deal, China agreed to increase its purchase of US goods and services by at least $200 billion over two years, or almost double the 2017 baseline levels. Also, China promised to address US concerns about intellectual property rights protection, illegal subsidies, and forced technology transfers. Meanwhile, the US side somewhat agreed to trim the Section 301 tariff action but rejected removing them. For example, the punitive Section 301 tariffs on apparel products were cut from 15% to 7.5% since implementing the “phase one” trade deal.

Trump lost the 2020 presidential election, and Joe Biden was sworn in as the new US president on January 20, 2021. However, the Section 301 tariff actions and the US-China “phase one” trade deal stayed in force.

Debate on the impact of the US-China tariff war

Like many other trade policies, the US Section 301 tariff actions against China raised heated debate among stakeholders with competing interests. This was the case even among different US textile and apparel industry segments.

On the one hand, US fashion brands and retailers strongly oppose the punitive tariffs against Chinese products for several reasons:

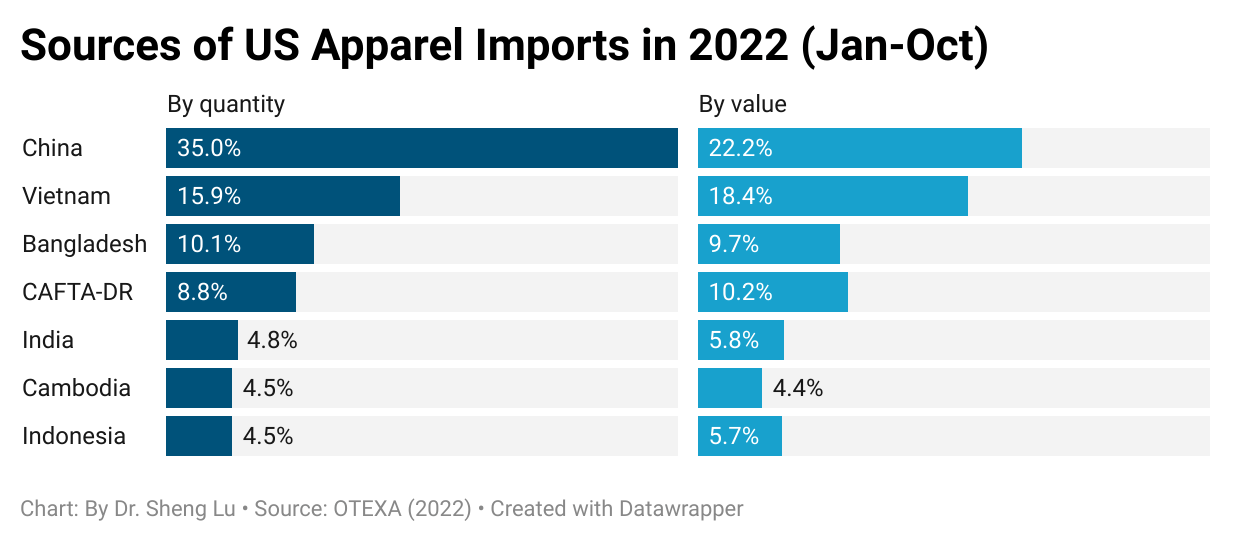

First, despite the Section 301 tariff action, China remained a critical apparel sourcing base for many US fashion companies with no practical alternative. Trade statistics show that four years into the tariff war, China still accounted for nearly 40 percent of US apparel imports in quantity and about one-third in value as of 2021. According to the latest data, in the first ten months of 2022, China remained the top apparel supplier, accounting for 35% of US apparel imports in quantity and 22.2% in value. Studies also consistently find that US fashion companies rely on China to fulfill orders requiring a small minimum order quantity, flexibility, and a great variety of product assortment.

Second, having to import from China, fashion companies argued that the Section 301 punitive tariffs increased their sourcing costs and cut profit margins. For example, for a clothing item with an original wholesale price of around $7, imposing a 7.5% Section 301 punitive tariff would increase the sourcing cost by about 5.8%. Should fashion companies not pass the cost increase to consumers, their retail gross margin would be cut by 1.5 percentage points. Notably, according to the US Fashion Industry Association’s 2021 benchmarking survey, nearly 90 percent of respondents explicitly say the tariff war directly increased their company’s sourcing costs. Another 74 percent say the tariff war hurt their company’s financials.

Third, as companies began to move their sourcing orders from China to other Asian countries like Vietnam, Bangladesh, and Cambodia to avoid paying punitive tariffs, these countries’ production costs all went up because of the limited production capacity. In other words, sourcing from everywhere became more expensive because of the Section 301 action against China.

Further, it is important to recognize that fashion companies supported the US government’s efforts to address China’s “unfair” trade practices, such as subsidies, intellectual property rights violations, and forced technology transfers. Many US fashion companies were the victims of such practices. However, fashion companies did not think the punitive tariff was the right tool to address these problems effectively. Instead, fashion brands and retailers were concerned that the tariff war unnecessarily created an uncertain and volatile market environment harmful to their business operations.

On the other hand, the National Council of Textile Organizations (NCTO), representing manufacturers of fibers, yarns, and fabrics in the United States, strongly supported the Section 301 tariff actions against Chinese products. As most US apparel production had moved overseas, exporting to the Western Hemisphere became critical to the survival of the US textile industry. Thus, for years, NCTO pushed US policymakers to support the so-called Western Hemisphere textile and apparel supply chain, i.e., Mexico and Central American countries import textiles from the US and then export the finished garments for consumption. Similarly, NCTO argued that Section 301 tariff action would make apparel “Made in China” less price competitive, resulting in more near sourcing from the Western Hemisphere.

However, interestingly enough, while supporting the Section 301 action against finished garments “Made in China,” NCTO asked the US government NOT to impose punitive tariffs on Chinese intermediaries. As NCTO’s president testified at a public hearing about the Section 301 tariff action in 2019,

“While NCTO members support the inclusion of finished products in Section 301, we are seriously concerned that…adding tariffs on imports of manufacturing inputs that are not made in the US such as certain chemicals, dyes, machinery, and rayon staple fiber in effect raises the cost for American companies and makes them less competitive with China.”

Mitigate the impact of the tariff war: Fashion Companies’ Strategies

Almost four years into the trade war, US fashion companies attempted to mitigate the negative impacts of the Section 301 tariff action. Notably, US apparel retailers were cautious about raising the retail price because of the intense market competition. Instead, most US fashion companies chose to absorb or control the rising sourcing cost; however, no strategy alone has proven remarkably successful and sufficient.

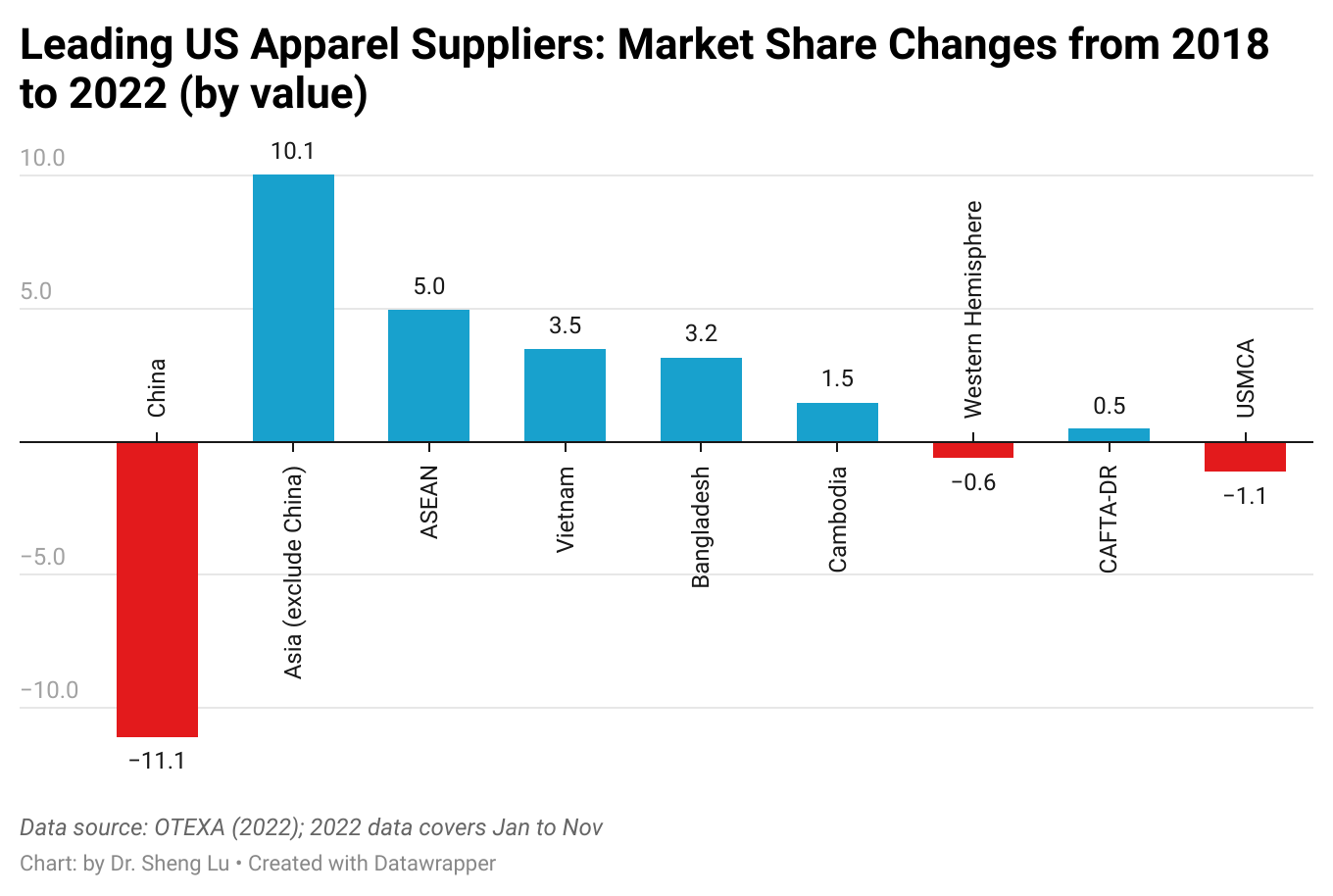

The first approach was to switch to China’s alternatives. Trade statistics suggest that Asian countries such as Vietnam and Bangladesh picked up most of China’s lost market shares in the US apparel import market. For example, in 2022 (Jan-Nov), Asian countries excluding China accounted for 51.2% of US apparel imports, a substantial increase from 41.2% in 2018 before the tariff war. In comparison, about 16.4% of U.S. apparel imports came from the Western Hemisphere in 2021 (Jan-Nov), lower than 17.0% in 2018. In other words, no evidence shows that Section 301 tariffs have expanded U.S. apparel sourcing from the Western Hemisphere.

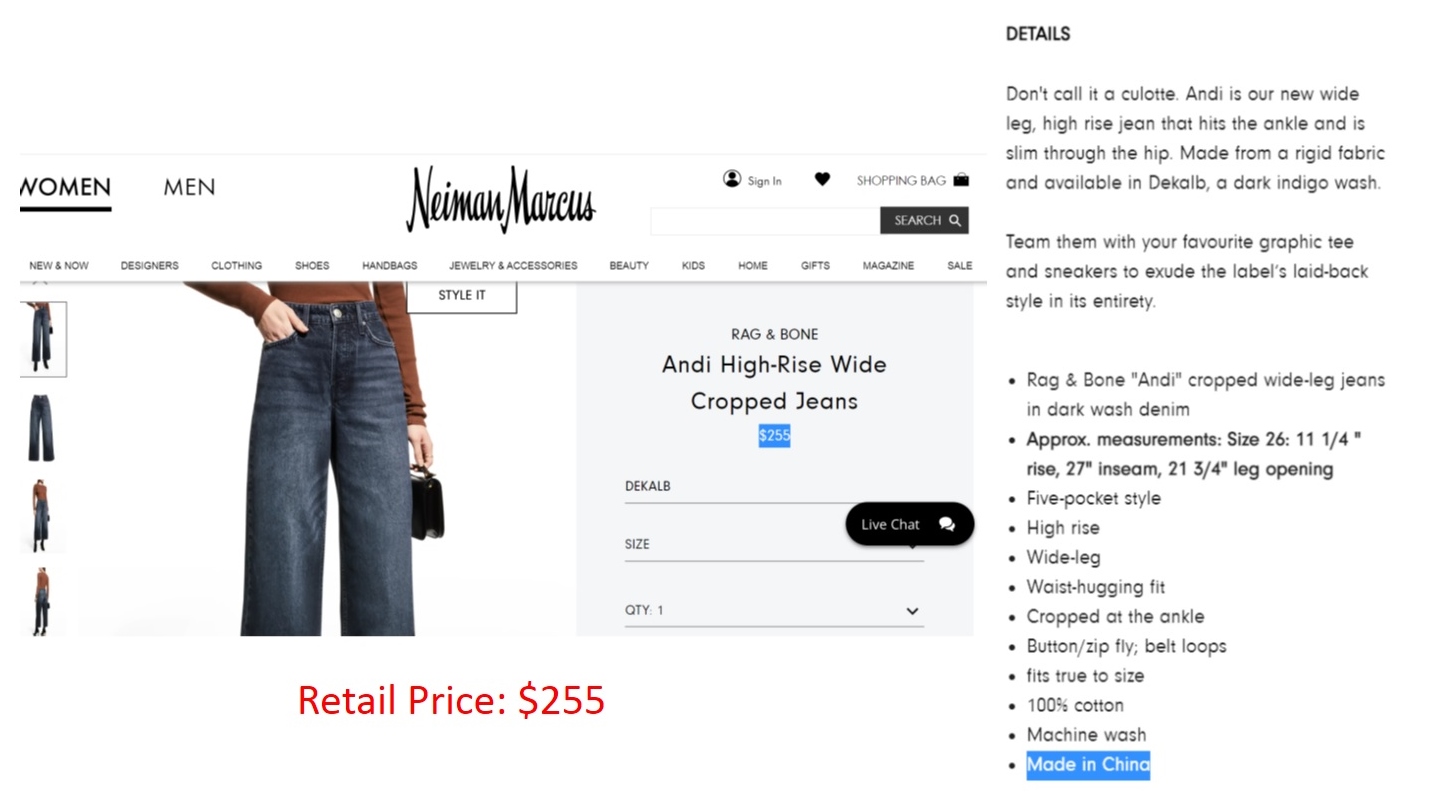

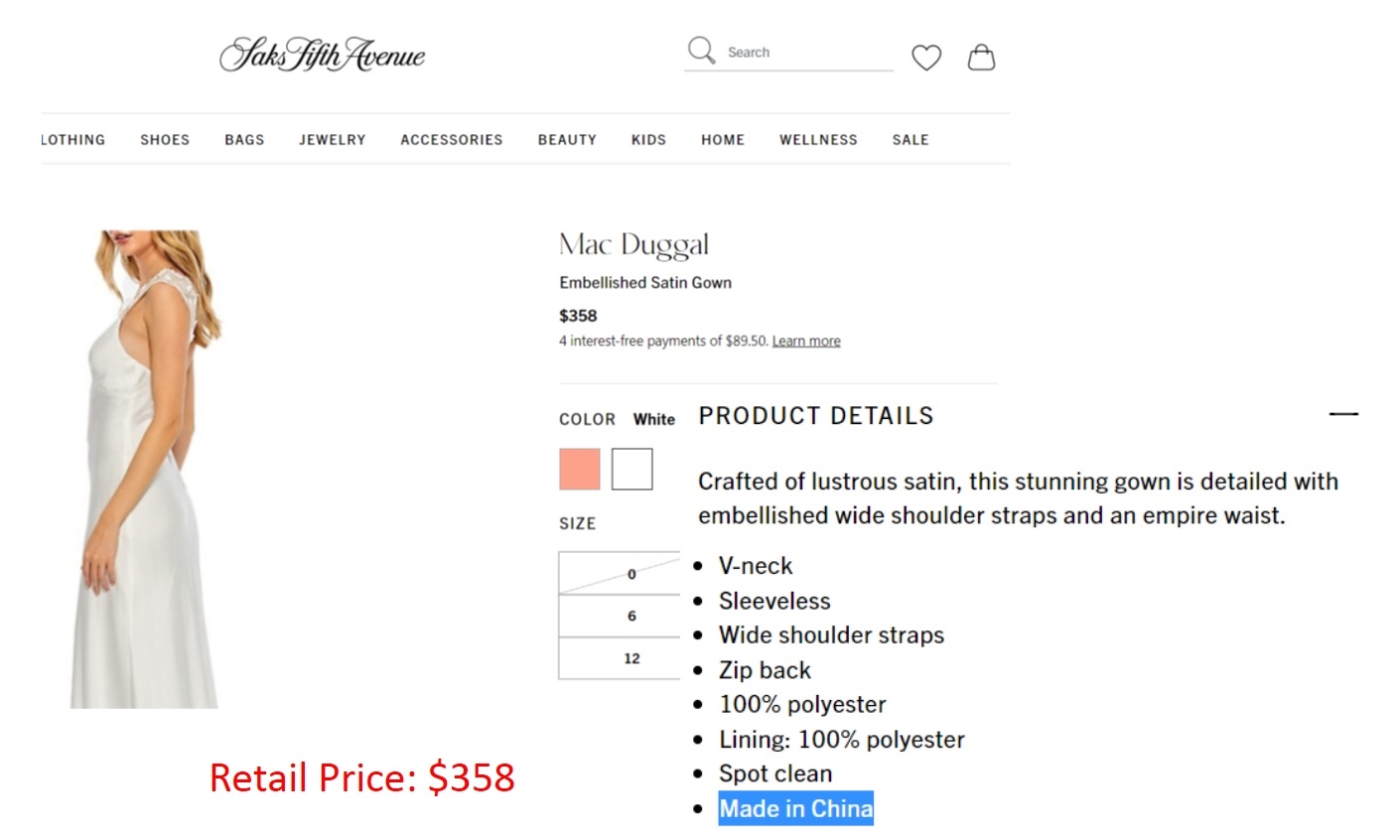

The second approach was to adjust what to source from China by leveraging the country’s production capacity and flexibility. For example, market data from industry sources showed that since the Section 301 tariff action, US fashion companies had imported more “Made in China” apparel in the luxury and premium segments and less for the value and mass markets. Such a practice made sense as consumers shopping for premium-priced apparel items typically were less price-sensitive, allowing fashion companies to raise the selling price more easily to mitigate the increasing sourcing costs. Studies also found that US companies sourced fewer lower value-added basic fashion items (such as tops and underwear), but more sophisticated and higher value-added apparel categories (such as dresses and outerwear) from China since the tariff war.

Related, US fashion companies such as Columbia Sportswear leveraged the so-called “tariff engineering” in response to the tariff war. Tariff engineering refers to designing clothing to be classified at a lower tariff rate. For example, “women’s or girls’ blouses, shirts, and shirt-blouses of man-made fibers” imported from China can tax as high as 26.9%. However, the same blouse added a pocket or two below the waist would instead be classified as a different product and subject to only a 16.0% tariff rate. Nevertheless, using tariff engineering requires substantial financial and human resources, which often were beyond the affordability of small and medium-sized fashion companies.

Third, recognizing the negative impacts of Section 301 on US businesses and consumers, the Office of the US Trade Representative (USTR) created a so-called “Section 301 exclusion process.” Under this mechanism, companies could request that a particular product be excluded from the Section 301 tariffs, subject to specific criteria determined at the discretion of USTR. The petition for the product exclusion required substantial paperwork, however. Even companies with an in-house legal team typically hire a DC-based law firm experienced with international trade litigation to assist the petition, given the professional knowledge and a strong government relation needed. Also of concern to fashion companies was the low success rate of the petition. The record showed that nearly 90 percent of petitions were denied for failure to demonstrate “severe economic harm.” Eventually, since the launch of the exclusion process, fewer than 1% of apparel items subject to the Section 301 punitive tariff were exempted. Understandably, the extra financial burden and the long shot discouraged fashion companies, especially small and medium-sized, from taking advantage of the exclusion process.

In conclusion, with USTR’s latest announcement, the debate on Section 301 and the outlook of China as a textile and apparel sourcing base will continue. Notably, while economic factors matter, we shall not ignore the impact of non-economic factors on the fate of the Section 301 tariff action against China. For example, with the implementation of the Uyghur Forced Labor Prevention Act (UFLPA), only about 10% of US cotton apparel imports came from China in the first ten months of 2022 (latest data available), the lowest in a decade. As the overall US-China bilateral trade relationship significantly deteriorated in recent years and the friction between the two countries expanded into highly politically sensitive areas, the Biden administration could “willfully” choose to keep the Section 301 tariff as negotiation leverage. Domestically, President Biden also didn’t want to look “weak” on his China policy, given the bipartisan support for taking on China’s rise.

by Sheng Lu

Suggested citation: Lu, S. (2022). US-China Tariff War and Apparel Sourcing: A Four-Year Review. FASH455 global apparel and textile trade and sourcing. https://shenglufashion.com/2022/09/10/us-china-tariff-war-and-apparel-sourcing-a-four-year-review/

Dr. Lu, wanting that most apparel be made outside the USA because of price is what started the “race to the bottom” and it has not stopped! Once you start feeding a tiger you must continue other wise he will eat you. Tariffs are just an aspirin. Reality check demands price increases as in a free market environment. But politics rule otherwise. Why is our industry “overregulated”? Because it is a “social industry”….it requires less capital investment AND requires abundant hand labor. In other words, very well suited for developing countries. So why bother trying to regulate it? IF a developed country wants cheap imports, it must be prepared to pay and and all tariffs, duties, etc. I welcome your thoughts on this mess.

The second approach of fashion retailers and businesses to mitigate the negative impacts of the Section 301 tariff action on the industry was really interesting to me. The textile and apparel industry sourced more high-end apparel “Made in China” because of the fact that consumers who shop for high-end apparel would be less likely to notice or care about an increase in prices due to their spending habits. In my opinion, this is a great way to mitigate the negative impacts of the Section 301 tariff action because increasing the price for those who are less price sensitive can benefit those who shop for mass-market goods because the increase in the price of high-end goods lessens the impact of tariffs and taxes on mass-market goods, making them still affordable to consumers who wish to save money or that are price-sensitive. The tariff war’s impact on what US fashion companies are sourcing is a very interesting phenomenon and I personally think it is a good remedy to practice considering the 7.5% punitive Section 301 tariffs on apparel products. Although this practice will not solve the tariff war’s impacts on the industry completely, it is a step in the right direction. It does not negatively affect consumers too much and shows strategic ideas to get around Section 301 tariff action’s negative impact. My policy recommendation would be to focus more deeply on this second approach regarding apparel products sourced from China because this strategy causes US fashion brands and retailers to source less mass-market goods which allow for more sustainability. Since mass-market goods are oftentimes overproduced and, consequently go to waste, it can help not only the negative effects of the tariff war but provide a more sustainable approach to the textile and apparel industry. There could be positive changes due to this approach including less textile and apparel waste, a strengthened relationship between the US and Asia industries, and a more sustainable industry.

Very interesting point! I agree that the price impact of the section 301 tariff action is a critical debate. Trade policymakers currently rely mostly on macro-trade statistics for their analysis. This prevents them from fully understanding how retailers actually react to the tariff actions. My observation (as mentioned in the post) is that retailers no longer treat China as a sourcing base for cheap products. Thus, I am not very positive that retailers will immediately adjust their retail price once the Section 301 tariffs are removed.

Global supply chains are a critical component of apparel and textiles. Fashion companies have reported the negative impacts and tensions in their businesses. US fashion brands and retailers oppose this tariff because there’s no other alternative or backup plans to this. The trade statistics show that 40% of apparel imports in the US come from China. I think it’s also interesting to see the breakdown math of how the increased price in tariffs reduces profit margins. I don’t think it was a good idea for China to move their sourcing orders to other Asian countries just to avoid having to pay larger tariffs.

By fashion businesses and retailers using another approach, they can reduce the negative impacts that are associated with the section 301 tariff. China is known for their unfair trading practices. Due to the impact of the tariff war on fashion companies, this article shows that sourcing is best for apparel products. To create a more sustainable fashion industry, there has to be less apparel & textile waste and a better relationship between brands and suppliers. Now that the Uyghur Forced Labor Prevention Act is enforced cotton apparel imports have been reduced now to 10%.

I think Section 301 action, for the most part, did not accomplish its goals. China agreed to purchase more goods and services from the U.S and address concerns, while the U.S agreed to reduce the tariffs rather than remove them all. The purpose of Section 301 was to give the Office of the United States Trade Representative (USTR) the ability to take action against unfair trade practices that violate the trade agreement and that can harm U.S businesses. However, the outcome of this negotiation has done more harm than good to the U.S and China. In my opinion, this does not accomplish the goal since instead of making trade easier, it’s driving businesses away. This was not the intention and proves that the U.S and China need to reevaluate the terms of the Section 301 actions. However, there are some good outcomes such as the benefits it has had on the National Council of Textile Organizations’ (NCTO). To make sure Section 301 is successful when accomplishing its goals in the future, there are many things for Biden to consider when reviewing this tariff agreement that can eliminate the negative impacts.