(The following comments are from students in FASH455 based on the readings)

Yes, US fashion companies should continue to diversify their apparel sourcing bases in 2022 because…

“It is said that you never keep all your eggs in one basket. If something happens in one of the countries that brands are sourcing from, whether it’s economically or politically, their business could be in jeopardy because they have no other sourcing bases anywhere else. As we see now with the Russian and Ukraine War, anything can happen at any time, and huge businesses like Mcdonalds and Starbucks have shut down their stores in Russia. Having connections in the business world is what takes a company further and makes them wealthier.

“The demand for sustainability and transparencyis only rising from consumers and this is causing brands to need to take accountability and action for more ethical sourcing. In order for brands to find factories that will work with the stricter regulations and policies, it may require them to find different and new locations and countries to work with.”

“The pandemic proved to be detrimental to brands only sourcing from a few countries. Pandemic lockdowns and government restrictions were harmful to companies that did not have a diverse sourcing base… A diverse sourcing base will allow companies to have the ability to continue to source new products in case of government lockdowns in other sourcing nations.”

“I think that US fashion companies should continue to diversify their sourcing base in 2022 to benefit other developing countries who are looking to build their economy. The majority of apparel sourcing is done out of China and Vietnam. A diverse apparel sourcing base would be a great way to take the heat off of these countries and benefit others.”

“I think fashion companies should continue to diversify their sourcing bases because it can help them remain competitive while stillkeeping costs down. Keeping costs down can also help prevent giant unpredictable spikes. Lastly, the company will have more flexibility if they are diverse because they won’t be relying on a single source and won’t run into issues if that single source fails.”

“I understand the argument that it is easier for smaller companies to produce solely in China seeing as it can be seen as a one-stop-shop. I also understand why some companies are looking to bring their sourcing closer together and closer to home to mitigate some of the sourcing costs. However, I find this view to be short-sighted and will be detrimental to companies in the long run. As we saw with the pandemic, diversification is helpful in the wake of disaster. If one country is suffering from a natural, economic, or political disaster it would be helpful to have production capabilities in other countries. This way if production is shut down in one country, it is not as detrimental to obtaining products because you can lean on the factories in other countries. I personally would rather wait out the incredibly high costs, which will hopefully go down soon, and keep my sourcing base diversified to be better prepared for unforeseen challenges in the future.”

No, US fashion companies should consolidate their apparel sourcing bases in 2022 because…

“US companies need to work on reducing the number of factories to increase sustainability and labor efforts. It would not be beneficial for the industry to continue to expand their sourcing bases, as that allows for less transparency with consumers. By diversifying their sourcing base they are proving to their consumers they only care about costs and how their clothing is affecting the environment.”

“I do not think US fashion companies should continue to diversify their sourcing base in 2022. These fashion companies should rather focus on nearshoring and local-to-local supply chain. Many retailers are interested in nearshoring as it helps eliminate the need to order months ahead, as the merchandise will have a shorter distance to travel. On top of this, many consumers want transparency and fast delivery. By sourcing more locally, fashion companies will be able to provide shorter shipping times as well as be more aware of sustainability in the supply chain and will then be able to relay the information to the consumers.”

“The very diverse sourcing base is exactly why some fashion companies struggled with supply chain disruptions and shipping delays. As the business environment remains highly uncertain, why not cut ties with some high-risk countries and only source products from the most secure and stable sourcing bases?”

“The present sourcing techniques used by US fashion corporations need to be refined and improved. The number of factories used for sourcing has to be reduced in order to improve sustainability and labor efforts. Increasing the number of sourcing bases does not benefit the industry since it reduces customer trust in the supply chain.”

“From trade data, it seems the top apparel suppliers to the US market barely changed—China, Vietnam, Bangladesh, Cambodia, Indonesia, or India. So, realistically, if a company intends to diversify sourcing, where else can they go?”

“During the pandemic, many US companies focused on strengthening their relationships with key vendors to gain a competitive advantage to achieve more flexibility in sourcing. It worked, then why companies should give up this strategy in 2022? Also, I think it would be wise for fashion companies to give MORE rewards to business partners that helped them survive the difficult times, rather than give sourcing orders to “new vendors”…further, using long-term loyalty and fiscal leverage with strategic business partners as an advantage could prove to be a good option for companies looking to obtain high production capacity, low prices, flexibility, and speed to market from their suppliers.”

Discussion questions:

Which side do you agree with or disagree with and why? What is your recommendation for US fashion companies regarding their apparel sourcing diversification strategies in 2022? Please join our online discussion and leave your comments.

Like many other sectors, the apparel industry is NOT immune to the Russia-Ukraine military conflict. According to data from Euromonitor, as one of the world’s largest apparel consumption markets, apparel retail sales in Russia exceeded USD 28 billion in 2021.

Notably, many well-known global fashion brands, such as H&M, Zara, Uniqlo, Adidas, Hugo Boss, Nike, and the emerging ultra-fast fashion retailer Shein, are top players with the largest market shares in Russia’s apparel retail market.

Russia was a lucrative and growing market for luxury apparel brands. Industry sources indicate that of apparel items launched to the Russian retail market from Jan 2021 to Feb 2022, more than 19% were in the luxury segment, much higher than 10% in the US and 8.7% in Italy, France, German, the UK, and Spain combined.

That being said, store closure, the EU, and US’s export ban of luxury goods to Russia would modestly impact most luxury apparel brands. Notably, Russia remains a relatively small market for luxury apparel brands. For example, less than 2% of LVMH’s annual sales came from Russia and 3% for the Kering Group. In comparison, Western EU and North America combined typically account for half of a luxury apparel band’s annual sales.

Given the fast deterioration of the situation, a growing number of international fashion brands and retailers have decided to suspend their operations in Russia, including Nike, H&M, Puma, Zara, Levi’s, Hermes, Chanel, and Gucci. Japan’s Fast Retailing Group (Uniqlo) initially chose to stay, but later reversed its decision. According to Yale University, as of March 18, 2022, over 400 global companies have withdrawn from Russia, but some remain.

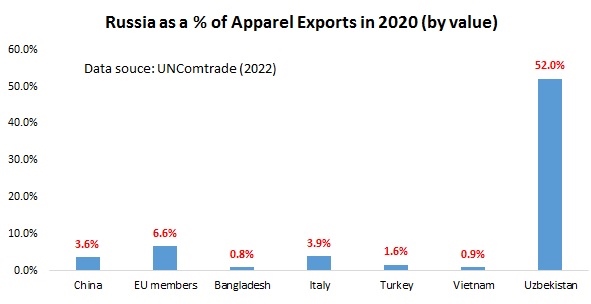

Further, the World Trade Organization data shows that Russia ranked as the world’s No.10 largest apparel importer in 2020 (by value). According to UNComtrade, China served as Russia’s single largest source of apparel in 2020 (40.3%), followed by EU members (12.3%), Bangladesh (10.5%), Turkey (6.2%), and Vietnam (5.1%). However, Russia accounted for a relatively small proportion of these countries’ apparel exports, implying a modest trade impact.

Nevertheless, a few Eastern EU countries rely more heavily on Russia as their top apparel export market, including Uzbekistan (52%), Moldova (40.4%), and Lithuania (18.8%). Apparel producers in these countries could be vulnerable to trade disruption.

On the other hand, the fashion industry faces growing price pressure because of the Russia-Ukraine war. As the immediate result of the escalated tension, the world oil price jumped substantially. This means textile fibers derived from oil, such as polyester, could face tremendous price pressure. As man-made fiber becomes more expensive, the demand for natural fiber could also increase, eventually extending the price inflation to natural fiber.

US Producer Price Index: Textile Products and Apparel: Polyester Fibers

Global Price of Cotton

Further, the vast uncertainty and risk caused by the war for the world economy and geopolitics could be a more significant concern. For example, a fluctuating financial market and a slower world economy would complicate the post-covid recovery. Also, Turkey, one of Ukraine’s close neighbors, serves as a leading apparel supplier for the EU market. Apparel companies that rely on sourcing from Turkey may need to prepare for a contingency plan. Media reports that the Turkish textile and apparel industry suffers as customers in Ukraine and Russia cancel orders.

Question #2: Primark sources from 28 countries work with around 928 contracted factories. What are the pros and cons of using such a diverse sourcing base?

Question #3: Near-shoring, meaning bringing manufacturing closer to home, is growing in popularity. Does it mean globalization is “in retreat”? What is your view?

Question #4: In the current state of the fashion industry, ethical labor laws are really important, especially to consumers. For example, activists are protesting Pretty Little Thing in London to protest the low wages paid to garment workers at the factories that Pretty Little Thing sources from. With this in mind, do you think that it would be wise for Primark to look for sourcing opportunities outside of Asia? Or do you believe Primark’s Ethical Trade and Environmental Sustainability team is sufficient to ensure ethical and sustainable sourcing?

Question #5: As of May 2021, Primark has the most workers in its Asian factories. Should we still call Primark an EU company? Does a company’s national identity still matter in today’s globalized world?

(Welcome to our online discussion. For students in FASH455, please address at least two questions and mention the question number (#) in your reply)

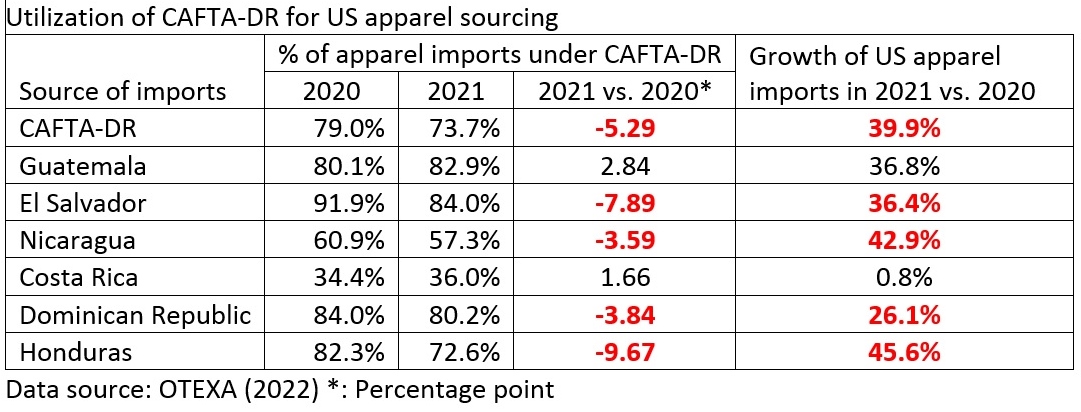

As US fashion companies diversify their sourcing from Asia, near-sourcing from the Western Hemisphere, particularly members of the Dominican Republic-Central America Free Trade Agreement (CAFTA-DR) seems to benefit. According to the latest trade data from the Office of Textiles and Apparel (OTEXA), US apparel companies placed relatively more sourcing orders with suppliers in the Western Hemisphere in 2021. For example, CAFTA-DR members’ market shares increased by 0.31 percentage points in quantity and nearly one percentage point in value compared with a year ago.

However, it is concerning to see the utilization rate of CAFTA-DR for apparel sourcing fall to a new record low of only 73.7% in 2021. This means that as much as 26.3% of US apparel imports from CAFTA-DR members did NOT claim the duty-free benefits.

The lower free trade agreement (FTA) utilization rate became a problem, particularly among CAFTA-DR members with fast export growth to the US market in 2021. For example, whereas US apparel imports from Honduras enjoyed an impressive 45.6% growth in 2021, only 72.6% of these imports claimed the CAFTA-DR duty benefits, down from 82.3% a year ago. We can observe a similar pattern in El Salvador, Nicaragua, and the Dominican Republic.

The phenomenon is far from surprising, however. For years, US fashion companies have expressed concerns about the limited textile supply within CAFTA-DR, especially fabrics and textile accessories. The lack of textile supply plus the restrictive “yarn-forward” rules of origin in the agreement often creates a dilemma for US fashion companies: either source from Asia entirely or source from CAFTA-DR but forgo the duty-saving benefits.

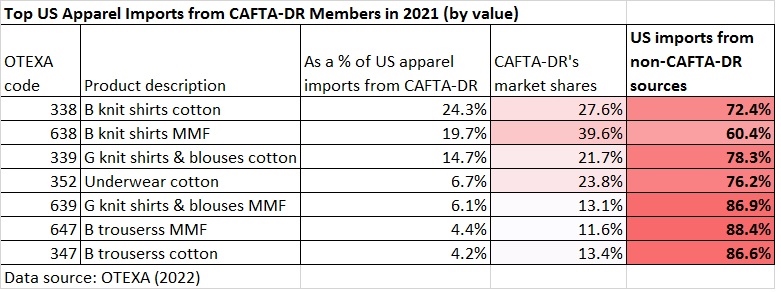

Likewise, because of a lack of sufficient textile supply within the region, US apparel imports from CAFTA-DR members become increasingly concentrated on basic fashion items, typically facing intense competition with many alternative sourcing destinations. For example, measured in value, over 80% of US apparel imports from CAFTA-DR members in 2021 were shirts, trousers, and underwear. However, US companies import the vast majority (70%-88%) from non-CAFTA-DR sources for these product categories.

Understandably, it will be unlikely to substantially expand US apparel sourcing from CAFTA-DR members without solving the textile supply shortage problem facing the region.

According to the video, how has the supply chain for apparel and footwear changed over the past decade?

What are the pros and cons of moving from a global supply chain to a regional one for fashion companies?

For fashion companies interested in “near-shoring” and “re-shoring”, what factors should they consider? Why?

Anything else you find interesting/intriguing/thought-provoking/debatable in the video? Why?

Note: Everyone is welcome to join our online discussion. For students in FASH455, please address at least two questions. Please mention the question number # (no need to repeat the question) in your comment.

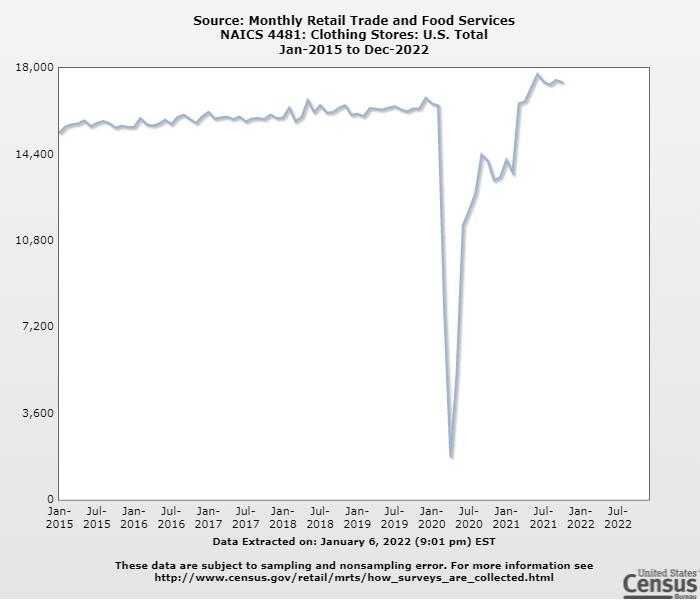

First, US apparel imports continue to rebound in November 2021 as companies build the inventory for the holiday season. Thanks to US consumers’ strong demand and the upcoming holidays, the value of US apparel imports went up by 15.7% in November 2021 from a month ago (seasonally adjusted) and increased by as much as 39.7% from 2020. However, before the pandemic, the value of US apparel imports always peaked in October and then gradually slipped in November and December. The unusual surge of imports in November 2021 could be the combined effects of price inflation and the late arrival of goods due to the shipping crisis.

Meanwhile, US apparel imports so far in 2021 have been far more volatile than in the past few years because of uncertainties and disruptions caused by COVID-19 and the shipping crisis. For example, the year-over-year (YoY) growth rate ranged from 131% in May to 17.6% in July, causing fashion companies additional inventory planning and supply chain management challenges. Unfortunately, the new omicron variant could worsen the market uncertainty and volatility.

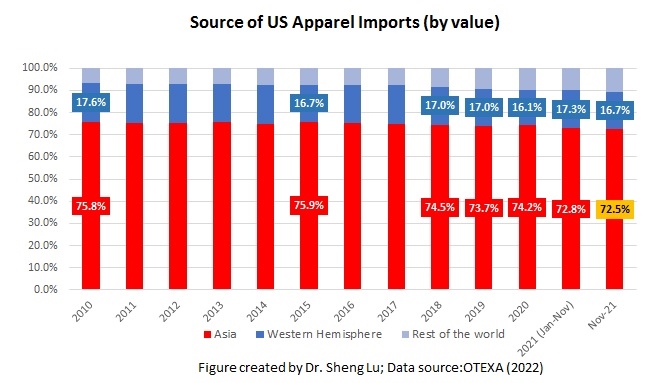

Second, Asian countries remain the dominant sourcing base for US fashion companies as the production capacity elsewhere is limited. Asian countries’ market shares fell from 74.2% in 2020 to 71.3% in July 2021, primarily because of the COVID lockdowns in Vietnam and Bangladesh. US apparel imports came from Asian countries rebounded to 74.8% and 72.5% in October and November 2021, respectively. This result suggests a lack of alternative sourcing destinations outside Asia, especially for large volume items. Meanwhile, the worsening shipping crisis affecting the route from Asia to North America could explain why Asian suppliers’ market shares in November were somewhat lower than a month ago.

Third, US companies continue to treat China as one of their essential sourcing bases in the current business environment. However, companies are NOT reversing their long-term strategy of reducing “China exposure.” China stays the largest supplier for the US market in November 2021, accounting for 41.5% of total US apparel imports in quantity and 25.8% in value. Due to the seasonal factor, China’s market shares typically peak from June to September and then drop from October until March-April.

Both industry sources and the export product diversification index also consistently show that China supplied the most variety of products to the US market with no near competitors. In comparison, US apparel imports from Bangladesh, Mexico, and CAFTA-DR members concentrate more on specific product categories.

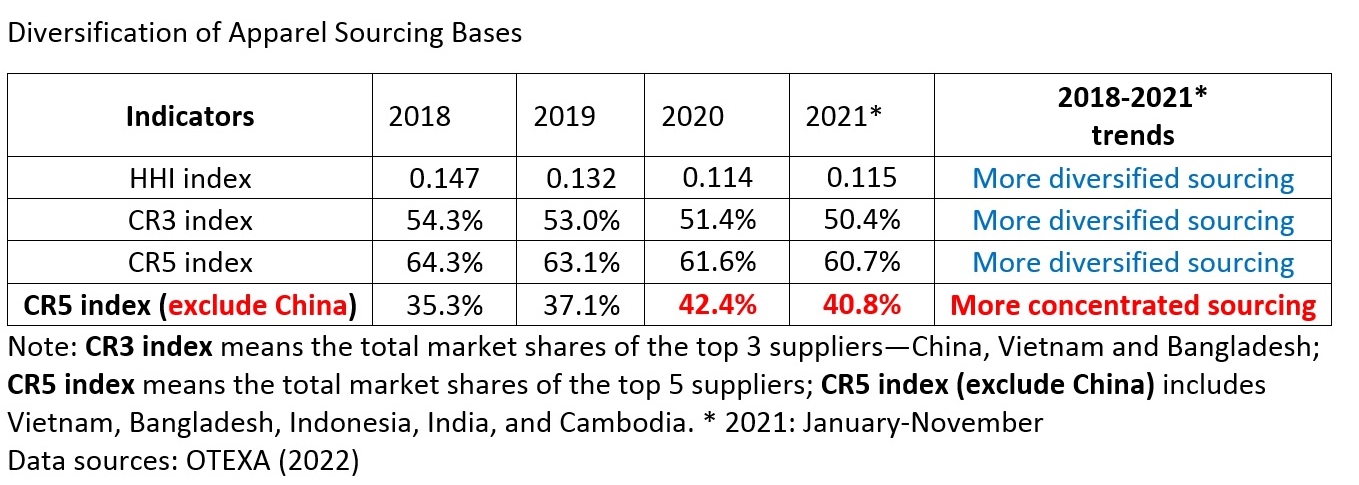

Nevertheless, the HHI index and market concentration ratios (CR3 and CR5) calculated based on the latest data suggest that US fashion companies continue to move their apparel sourcing orders from China to other Asian countries overall. For example, only around 15% of US cotton apparel comes from China, compared with about 27% in 2018. My latest studies also indicate that it has become ever more common to see a fashion company places only around 10% of its total sourcing value or volume from China compared to over 30% in the past. Furthermore, with the growing tensions of the US-China relations and the newly enacted Uyghur Forced Labor Prevention Act, fashion companies could take another look at their China sourcing strategy to avoid potential high-impact disruptions.

Fourth, near sourcing from the Western Hemisphere, especially CAFTA-DR members, continue to gain popularity. Specifically, 17.3% of US apparel imports came from the Western Hemisphere year-to-date (YTD) in 2021 (January-November), higher than 16.1% in 2020. Notably, CAFTA-DR members’ market shares increased to 10.6% in 2021 (January to November) from 9.6% in 2020. The value of US apparel imports from CAFTA-DR also enjoyed a 41.7% growth in 2021 (January—November) from a year ago, one of the highest among all sourcing destinations. The imports from El Salvador (up 42.6%), Honduras (up 47.1%), and Guatemala (36.6%) had grown particularly fast so far in 2021. However, the political instability in some Central American countries could make fashion companies feel hesitant to permanently switch their sourcing orders to the region or make long-term investments.

Additionally, the latest trade data suggests a notable increase in the price of US apparel imports. Notably, the unit price of US apparel imports from almost all leading sources went up by more than 10% from January 2021 to November 2021. As worldwide inflation continues, the rising sourcing cost pressure won’t ease anytime soon.

{kind=link}