USITC adopted two methods to estimate Section 301 tariffs’ economic impacts:

Econometric model estimates using monthly trade data (10-digit HS code) from January 2017 to December 2021.

A set of partial equilibrium models that linked section 301 tariffs to domestic prices and production at the four-digit NAICS code level. USITC used data from 2018 to 2021 as the base year.

USITC only considered Section 301 tariffs’ direct impacts, i.e., “how tariffs impacted prices, production, and trade for products subject to section 301 tariffs and domestic sectors that compete directly with those imports.”

Regarding the overall impact of Section 301 actions, USITC found that the tariffs imposed on Chinese goods resulted in a price rise paid by US importers, but the exporter prices received by Chinese firms were mostly unchanged. As a result, “imports from China decreased in quantity, leading to a substantial decline in their import value. These changes, in turn, caused an increase in production and prices in US domestic industries that were competing with Chinese imports.”

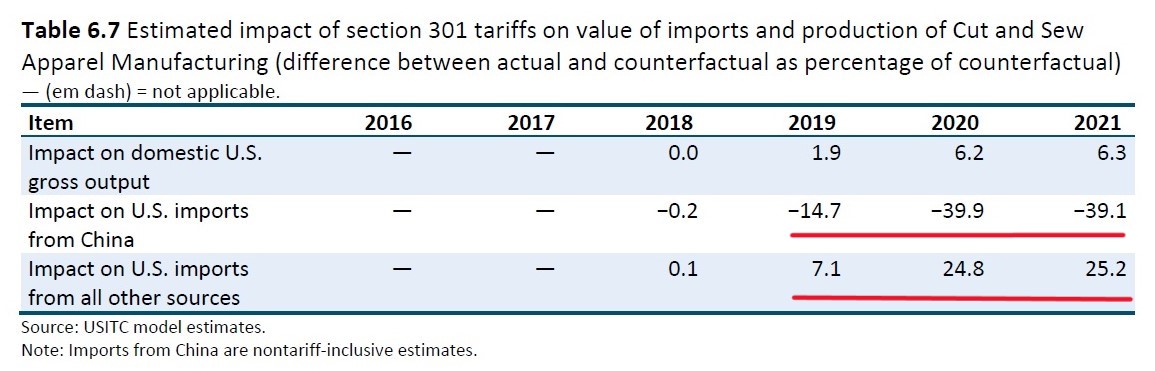

USITC also evaluated the specific impacts of Section 301 tariffs on the Cut and Sew apparel (NAICS 3152) sector. According to USITC:

“nontariff-inclusive value” refers to the change in the value of imports from China excluding the value of the section 301 duties themselves, which provide an indication of the change in import quantities because export prices are mostly unchanged.

First, Section 301 tariffs hurt US apparel imports from China. USITC estimated that US woven apparel (NAICS 3152) imports from China decreased by 14.7% in 2019 but fell nearly 40% in 2020 and 2021 due to Section 301 tariffs. However, USITC didn’t explain why imports from China suddenly worsened, nor if other factors, such as the Uyghur Forced Labor Prevention Act (UFLPA), played a role.

Second, Section 301 tariffs mostly replaced US woven apparel (NAICS3152) imports from China with other sources. However, the direct benefits of Section 301 tariffs to US domestic cut and sew manufacturing seemed limited. Specifically, USITC estimated that US woven apparel imports from sources other than China increased by 7.1% in 2019, 24.8% in 2020, and 25.2% in 2021 due to Section 301 tariffs. In comparison, Section 301 tariffs resulted in modest growth of US domestic woven apparel (NAICS3152) production (up to 6.3%) over the same period.

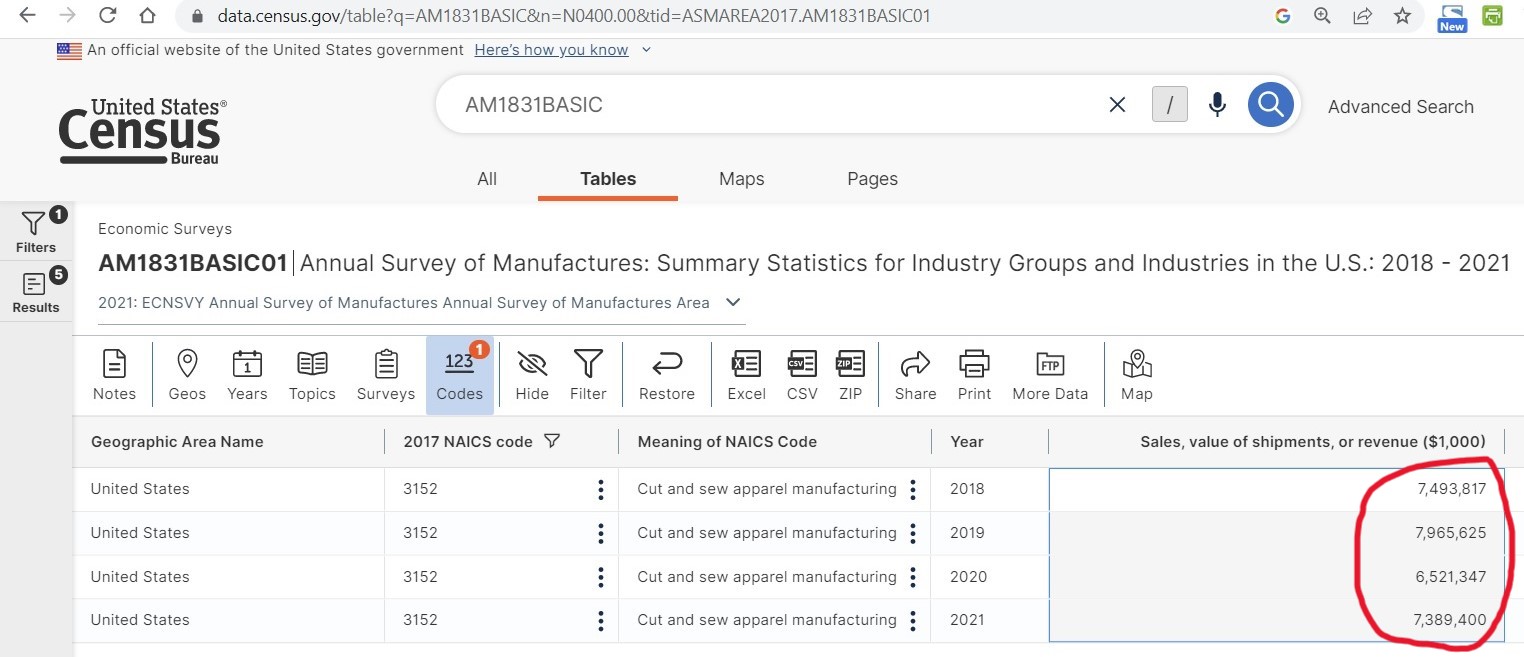

Actual trade and production data further showed that US woven apparel (NAICS 3152) imports from sources other than China increased from $55.3 billion in 2018 to $61.2 billion in 2021 (or up 10.7%). Over the same period, US domestic woven apparel (NAICS 3152) sales & value of shipments declined from $7.49 billion to $7.38 billion (or down 1.4%) (Data source: Census). In other words, no clear evidence suggests that Section 301 tariffs boosted US domestic woven apparel production.

Third, Section 301 tariffs made US woven apparel (NAICS 3152) imports from EVERYWHERE more expensive. On the one hand, USITC found that the price of US woven apparel (NAICS 3152) imports from China increased by 4.4% in 2019, 14.7% in 2020, and 14.5% in 2021 due to the Section 301 tariffs. However, similar to the case of trade volume, USITC didn’t explain why Section 301 tariffs’ price impact suddenly became more significant in 2020 and 2021. (Note: In fact, the Tranche 4A tariffs were 15% since September 1, 2019, but were reduced to 7.5% effective February 14, 2020, because of the US-China Phase One deal.)

Meanwhile, due to limited production capacity outside of China, the Section 301 tariffs caused an increase in the cost of US woven apparel imports from all other countries. Specifically, USITC found that the price of US woven apparel (NACIS 3152) imports from sources other than China increased by 3.2% from 2018 to 2021. (Note: given the hiking sourcing costs in 2022, the price increase could be more significant should USITC include updated 2022 trade data in the estimation.)

Additionally, USITC acknowledged that its estimation may “likely captures the most significant impacts of these tariffs in the short run.” However, some effects of section 301 tariffs would likely be delayed. For example, USITC said, “if importers and domestic producers anticipated the tariffs remaining in place long enough,” they may consider more costly changes, such as adjusting their supply chains and investing in domestic production.

Discussion questions:

Based on USITC’s assessment, should President Biden keep or remove the Section 301 tariffs on imports from China? Why or why not?

Regarding the impact of Section 301, any questions remain unanswered or can be studied further?

Any findings in the USITC report surprised you and why?

In March 2023, the Office of the United States Trade Representative (USTR) released its 2024 Fiscal Year Budget report, outlining six major goals and objectives for FY2024. USTR’s FY2024 goals and objectives for textile and apparel are similar to FY2023, but keywords such as “near-shoring” are newly emphasized.

Goal 1: Open Foreign Markets and Combat Unfair Trade

Provide policy guidance and support for international negotiations or initiatives affecting the textile and apparel sector to ensure that the interests of U.S. industry and workers are taken into account and, where possible, to provide new or enhanced export opportunities for U.S. industry. (Note: no change from FY2023)

Conduct reviews of commercial availability petitions regarding textile and apparel products and negotiate corresponding FTA rules of origin changes, where appropriate, in a manner that takes into account market conditions while preserving export opportunities for U.S. producers and employment opportunities for U.S. workers. (Note: no change from FY2023)

Engage relevant trade partners to address regulatory issues potentially affecting the U.S. textile and apparel industry’s market access opportunities. (Note: no change from FY2023)

Continue to engage with CAFTA-DR partner countries to address trade-related issues to optimize inclusive economic opportunities; strengthen trade rules and transparency and address non-tariff trade impediments; provide capacity building in areas such as textile and apparel trade-related regulation and practice on customs, border and market access issues, including agricultural and sanitary and phytosanitary regulations, to avoid barriers to trade. (note: newly mentioned “transparency”)

Continue to engage CAFTA-DR partners and stakeholders to identify and develop means to increase two-way trade in textiles and apparel and strengthen the North American supply chain and near-shoring to enhance formal job creation. (note: newly emphasized “Near-shoring”)

Provide policy guidance and support for international negotiations or initiatives affecting the textile and apparel sector to ensure that the interests of U.S. industry and workers are taken into account and, where possible, to provide new or enhanced export opportunities for U.S. industry. (Note: no change from FY2023)

Conduct reviews of commercial availability petitions regarding textile and apparel products and negotiate corresponding FTA rules of origin changes, where appropriate, in a manner that takes into account market conditions while preserving export opportunities for U.S. producers and employment opportunities for U.S. workers (note: no change from FY2023)

Engage relevant trade partners to address regulatory issues potentially affecting the U.S. textile and apparel industry’s market access opportunities. (note: no change from FY2023)

Goal 2: Fully Enforce U.S. Trade Laws, Monitor Compliance with Agreements, and Use All Available Tools to Hold Other Countries Accountable

Closely collaborate with industry and other offices and Departments to monitor trade actions taken by partner countries on textiles and apparel to ensure that such actions are consistent with trade agreement obligations and do not impede U.S. export opportunities. (note: no change from FY2023)

Research and monitor policy support measures for the textile sector, in particular in the PRC, India, and other large textile producing and exporting countries, to ensure compliance with international agreements. (note: no change from FY2023)

Continue to work with the U.S. textile and apparel industry to promote exports and other opportunities under our free trade agreements and preference programs, by actively engaging with stakeholders and industry associations and participating, as appropriate, in industry trade shows. (note: no change from FY2023)

Goal 4: Develop Equitable Trade Policy Through Inclusive Processes

Take the lead in providing policy advice and assistance in support of any Congressional initiatives to reform or re-examine preference programs that have an impact on the textile and apparel sector. (note: no change from FY2023)

Other Priorities for USTR in FY2024:

#1 “Advancing a Worker-Centered Trade Policy.” For example, given “communities of color and lower socio-economic backgrounds were more negatively affected by free trade policies that have reduced tariffs and distributed supply chains across the globe,” USTR will develop “a new strategic approach to trade relationships that is not built on traditional free trade agreements…USTR is embarking on trade engagements with allies and like-minded economies, like Taiwan and Kenya and [through] multinational economic frameworks that focus on clean energy and supply chains rather than tariffs.”

#2 Address forced labor. For example, USTR developed the first-ever focused trade strategy to combat forced labor. Paired with the implementation of the Uyghur Forced Labor Prevention Act, and the Memorandum of Cooperation (MOC) launching of a Task Force on the Promotion of Human Rights and International Labor Standards in Supply Chains under the U.S.-Japan Partnership on Trade. And USTR will “use every tool available to block the importation of goods made partially or entirely with forced labor.”

#3 Re-Aligning the U.S. – Beijing Trade Relationship. “USTR continues to keep the door open to conversations with the PRC, including on its Phase One commitments. However, USTR acknowledges the Agreement’s limitations. USTR’s strategy is expand beyond only pressing Beijing for change and includes vigorously defending our values and economic interests from the negative impacts of the PRC’s unfair economic policies and practices.”

#4 Strengthen enforcement of US trade policy. For example, USTR sees enforcement “a key component of our worker-centered trade policy.” USTR is “upholding the eligibility requirements in preference programs,” such as the African Growth and Opportunity Act (AGOA). As many enforcement tools were “were crafted decades ago,” USTR will be “reviewing our existing trade tools and working with Congress to develop new tools as needed.”

The program is split into two half-day sessions. Public sector trade-related careers will be examined on Friday, March 10, and private sector opportunities will be the focus on Monday, March 13. Both sessions will be held from 8:45 a.m. to 12:30 p.m. on Zoom.

Sarah Clarke, former Chief Supply Chain Officer, PVH Corp.

Hun Quach, Director of Policy and Advocacy, Levi Strauss & Co.

Stephanie Lester, Vice President, Head of Government Affairs, Gap Inc.; former Professional Staff, House Ways and Means Committee, Subcommittee on Trade

Patty Lopez, Sr. Director- Vendor Management, Gap Inc.; former Sr Director-Global Production, Gap Inc.

Julia Hughes, President, U.S. Fashion Industry Association

Natalie Hanson, Deputy Assistant USTR for Textiles, Office of the U.S. Trade Representative

Jon Gold, Vice President of Supply Chain and Customs Policy, National Retail Federation

Nate Herman, Senior Vice President, American Apparel and Footwear Association (AAFA)

Bill McRaith, former Chief Supply Chain Officer, PVH Corp.

Heidi Colby-Oizumi, Chief Chemicals and Textiles Division, US International Trade Commission

Linda Martinich, Senior International Trade Specialist, Office of Textiles and Apparel, US Department of Commerce

Thomas Newberg, International Trade Specialist, Office of Textiles and Apparel, US Department of Commerce

Blake Harden, Vice President, International Trade at Retail Industry Leaders Association (RILA); former Trade Counsel, U.S. House of Representatives, Committee on Ways and Means, Subcommittee on Trade

Eric Biel, Senior Advisor, Fair Labor Association; Adjunct Professor, Georgetown University Law Center; former Associate Deputy Undersecretary, U.S. Department of Labor, Bureau of International Labor Affairs

Nicole Bivens Collinson, President, International Trade and Government Relations, Sandler, Travis & Rosenberg, P.A.; former Assistant Textile Negotiator, Office of the United States Trade Representative

Amanda Blunt, Counsel, Legal Affairs & Trade, General Motors; former Associate General Counsel, Office of the U.S. Trade Representative

Lisa Schroeter, Global Director of Trade and Investment Policy, Dow; former Executive Director, TransAtlantic Business Dialogue

Maria Luisa Boyce, Vice President, UPS Global Public Affairs; former Executive Director Office of Trade Relations/Senior Advisor for Trade Engagement, U.S. Customs and Border Protectionformer President, Border Trade Alliance

Brenda Smith, Global Director of Government Outreach, Expeditors; former Executive Assistant Commissioner, U.S. Customs & Border Protection

Nikole Burroughs, Deputy Chief of Staff for Management and Resources, USAID; former Staff Director, Subcommittee on Asia, the Pacific the Nonproliferation, United States House Committee on Foreign Affairs

Catherine DeFilippo, Director of Operations, United States International Trade Commission; former Economist, US International Trade Commission

Paul H. DeLaney, III, Partner, Kyle House Group; former Vice President for Trade and International at Business Roundtable, former International Trade Counsel to Chairman Orrin G. Hatch for the U.S. Senate Committee on Finance

Erin Ennis, Senior Director, Global Public Policy, Dell Technologies; former Assistant to the Deputy US Trade Representative, Office of the US Trade Representative

Naomi Freeman, Consultant, Sandler, Travis & Rosenberg; former Director for the Generalized System of Preferences at the Office of the U.S. Trade Representative

Nasim Fussell, Partner, Holland & Knight LLP; former Chief International Trade Counsel, U.S. Senate Committee on Finance

Ed Gresser, Vice President and Director, Trade and Global Markets at PPI; former Assistant U.S. Trade Representative for Trade Policy and Economics at the Office of the United States Trade Representative

Jodi Herman, Assistant Administrator for Legislative and Public Affairs, USAID; former Vice President for Government Relations and Public Affairs, National Endowment for Democracy (NED)

Charlotte Mcclure, Logistics Supervisor, Cap America; former Overseas Specialist, Cap America; former Logistics Specialist, Cap America

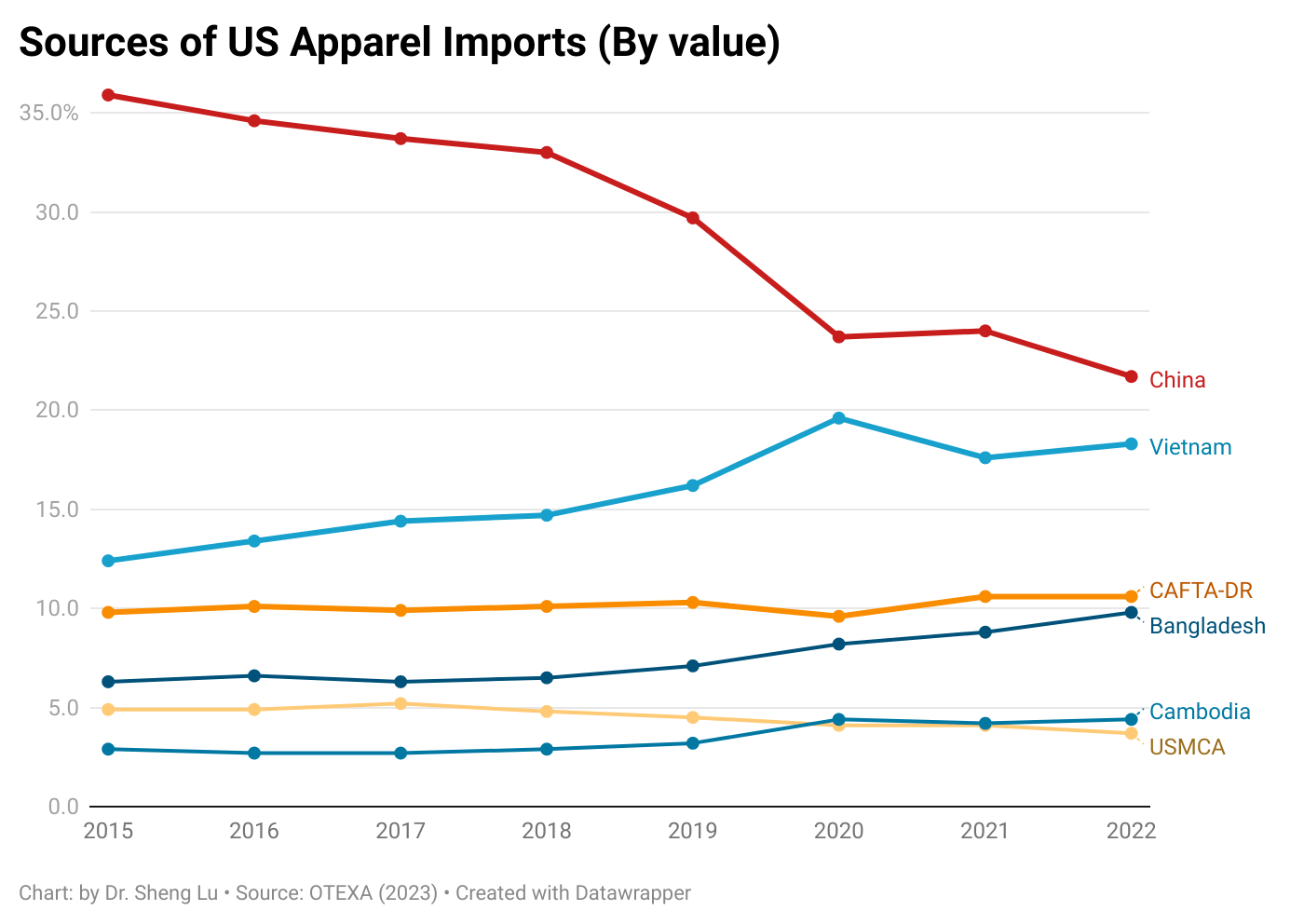

Trend 1: US fashion companies continue to diversify their sourcing base in 2022

Numerous studies suggest that US fashion companies leverage sourcing diversification and sourcing from countries with large-scale production capacity in response to the shifting business environment. For example, according to the 2022 fashion industry benchmarking study from the US Fashion Industry Association (USFIA), more than half of surveyed US fashion brands and retailers (53%) reported sourcing apparel from over ten countries in 2022, compared with only 37% in 2021. Nearly 40% of respondents plan to source from even more countries and work with more suppliers over the next two years, up from only 17% in 2021.

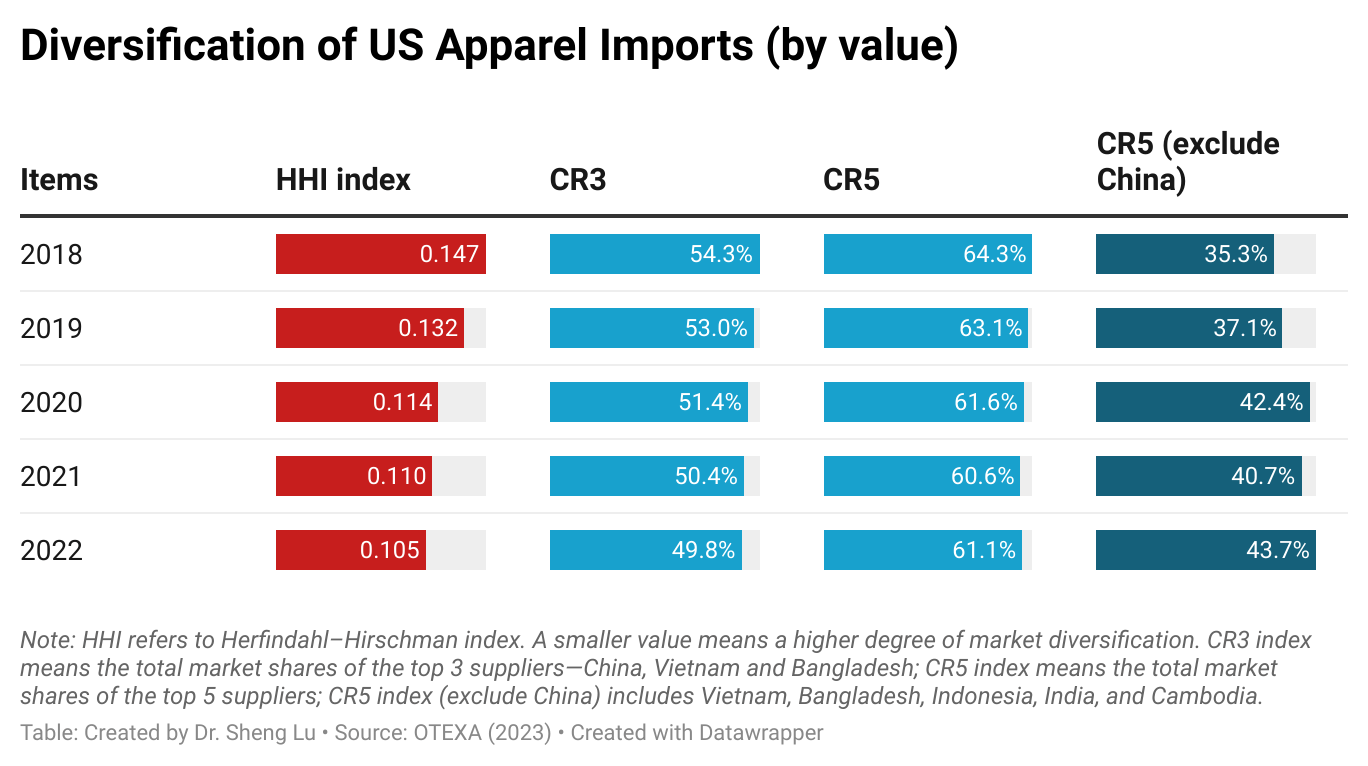

Trade data confirms the trend. For example, the Herfindahl–Hirschman index (HHI), a commonly-used measurement of market concentration, went down from 0.110 in 2021 to 0.105 in 2022, suggesting that US apparel imports came from even more diverse sources.

Trend 2: Asia as a whole will remain the dominant source of imports

Measured in value, about 73.5% of US apparel imports came from Asia in 2022, up from 72.8% in 2021. Likewise, the CR5 index, measuring the total market shares of the top five suppliers—all Asia-based, i.e., China, Vietnam, Bangladesh, Indonesia, and India, went up from 60.6% in 2021 to 61.1% in 2022. Notably, the CR5 index without China (i.e., the total market shares of Vietnam, Bangladesh, Indonesia, India, and Cambodia) enjoyed even faster growth, from 40.7% in 2021 to 43.7% in 2022.

Additionally, facing growing market uncertainties and weakened consumer demand amid high inflation pressure, US fashion companies may continue to prioritize costs and flexibility in their vendor selection. Studies consistently show that Asia countries still enjoy notable advantages in both areas thanks to their highly integrated regional supply chain, production scale, and efficiency. Thus, US fashion companies are unlikely to reduce their exposure to Asia in the short to medium term despite some worries about the rising geopolitical risks.

Trend 3: US fashion companies’ China sourcing strategy continues to evolve

Several factors affected US apparel sourcing from China negatively in 2022:

One was China’s stringent zero-COVID policy, which led to severe supply chain disruptions, particularly during the fall. As a result, China’s market shares from September to November 2022 declined by 7-9 percentage points compared to the previous year over the same period.

The second factor was the implementation of the Uyghur Forced Labor Prevention Act (UFLPA) in June 2022, which discouraged US fashion companies from sourcing cotton products from China. For example, only about 10% of US cotton apparel came from China in the fourth quarter of 2022, down from 17% at the beginning of the year and much lower than nearly 27% back in 2018.

The third contributing factor was the US-China trade tensions, including the continuation of Section 301 punitive tariffs. Industry sources indicate that US fashion companies increasingly source from China for relatively higher-value-added items targeting the premium or luxury market segments to offset the additional sourcing costs.

Further, three trends are worth watching regarding China’s future as an apparel sourcing base for US fashion companies:

One is the emergence of the “Made in China for China” strategy, particularly for those companies that view China as a lucrative sales market. Recent studies show that many US fashion companies aim to tailor their product offerings further to meet Chinese consumers’ needs and preferences.

Second is Chinese textile and apparel companies’ growing efforts to invest and build factories overseas. As a result, more and more clothing labeled “Made in Bangladesh” and “Made in Vietnam” could be produced by factories owned by Chinese investors.

Third, China could accelerate its transition from exporting apparel to providing more textile raw materials to other apparel-exporting countries in Asia. Notably, over the past decade, most Asian apparel-exporting countries have become increasingly dependent on China’s textile raw material supply, from yarns and fabrics to various accessories. Moreover, recent regional trade agreements, particularly the Regional Comprehensive Economic Partnership (RCEP), provide new opportunities for supply chain integration in Asia.

Trend 4: US fashion companies demonstrate a new interest in expanding sourcing from the Western Hemisphere, but key bottlenecks need to be solved

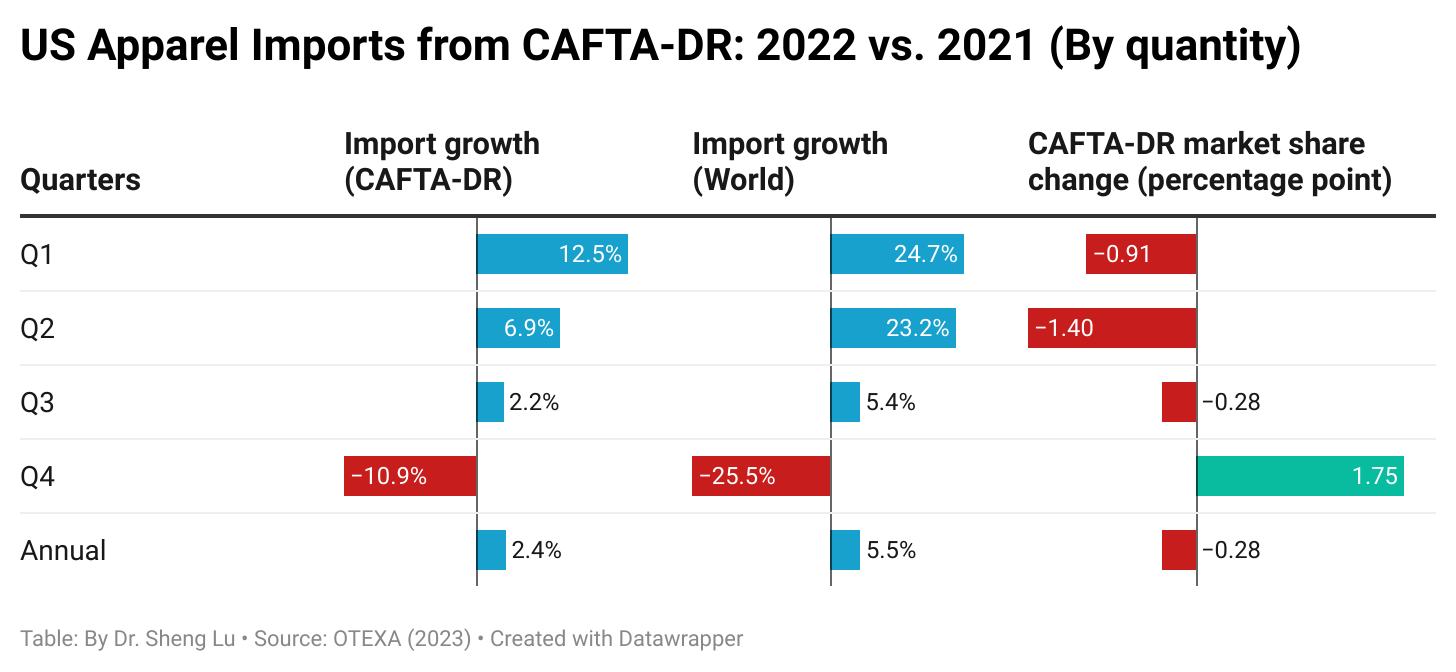

Trade data suggests a mixed picture of near-shoring in 2022. For example, members of the Dominican Republic-Central America Free Trade Agreement (CAFTA-DR) and US-Mexico-Canada Trade Agreement (USMCA) accounted for a declining share of US apparel imports in 2022, measured in quantity and value. While CAFTA-DR and USMCA members showed an increase in their market share of US apparel imports in the fourth quarter of 2022, reaching 10.7% and 3.1%, respectively, this growth was not accompanied by an increase in trade volume. Instead, US apparel imports from these countries decreased by 11% and 15%, respectively, compared to the previous year. CAFTA-DR and USMCA members’ gain in market share was mainly due to a sharper decline in US apparel imports from the rest of the world (i.e., decreased by over 25% in the fourth quarter of 2022).

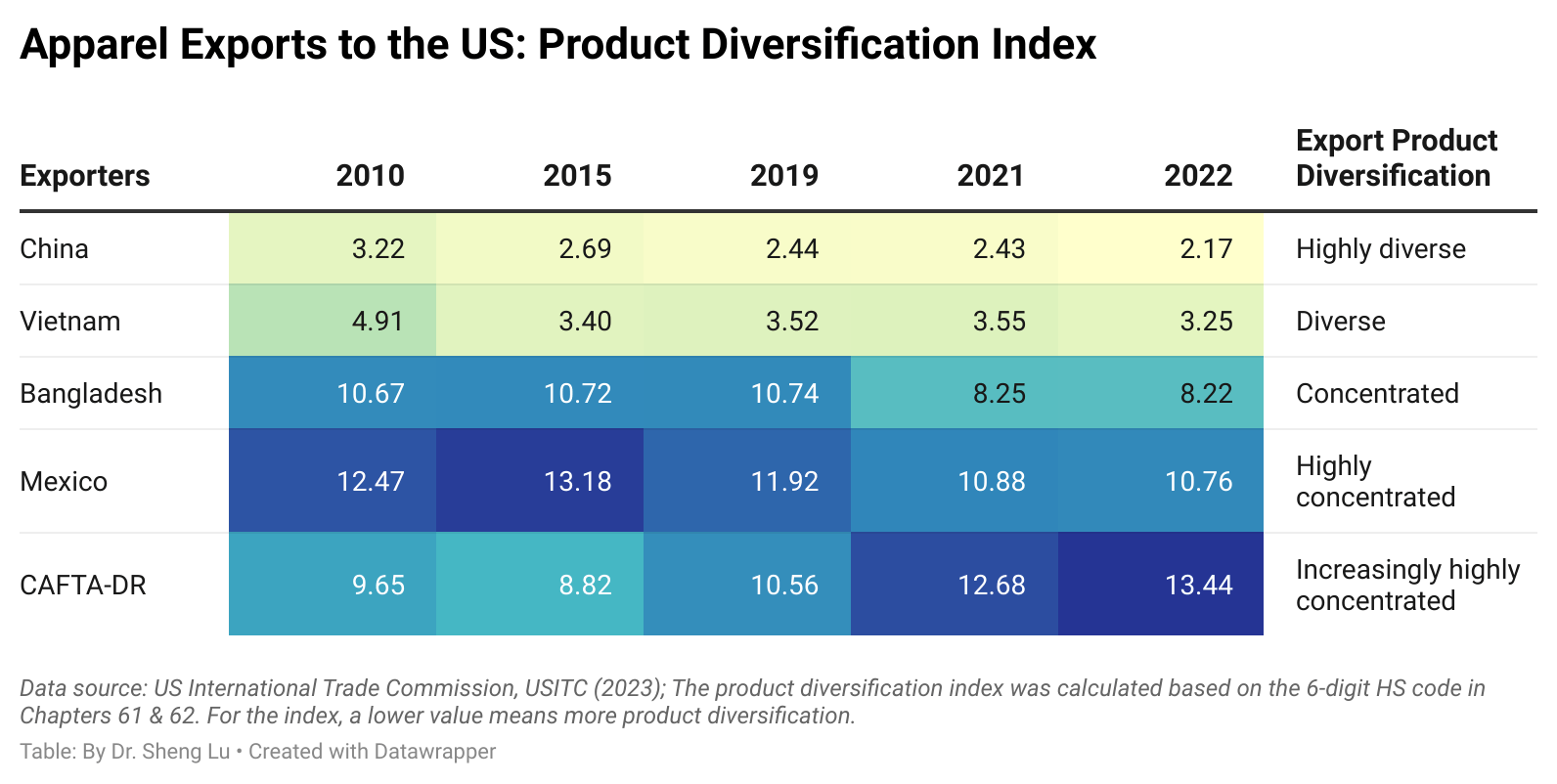

Trade data also suggests two other bottlenecks preventing more US apparel sourcing from CAFTA-DR and USMCA members. One is the lack of product diversity. For example, the product diversification index consistently shows that US apparel imports from CAFTA-DR members and Mexico concentrated on only a limited category of products, and the problem worsened in 2022. The result explained why US fashion companies often couldn’t move souring orders from Asia to CAFTA-DR and USMCA members.

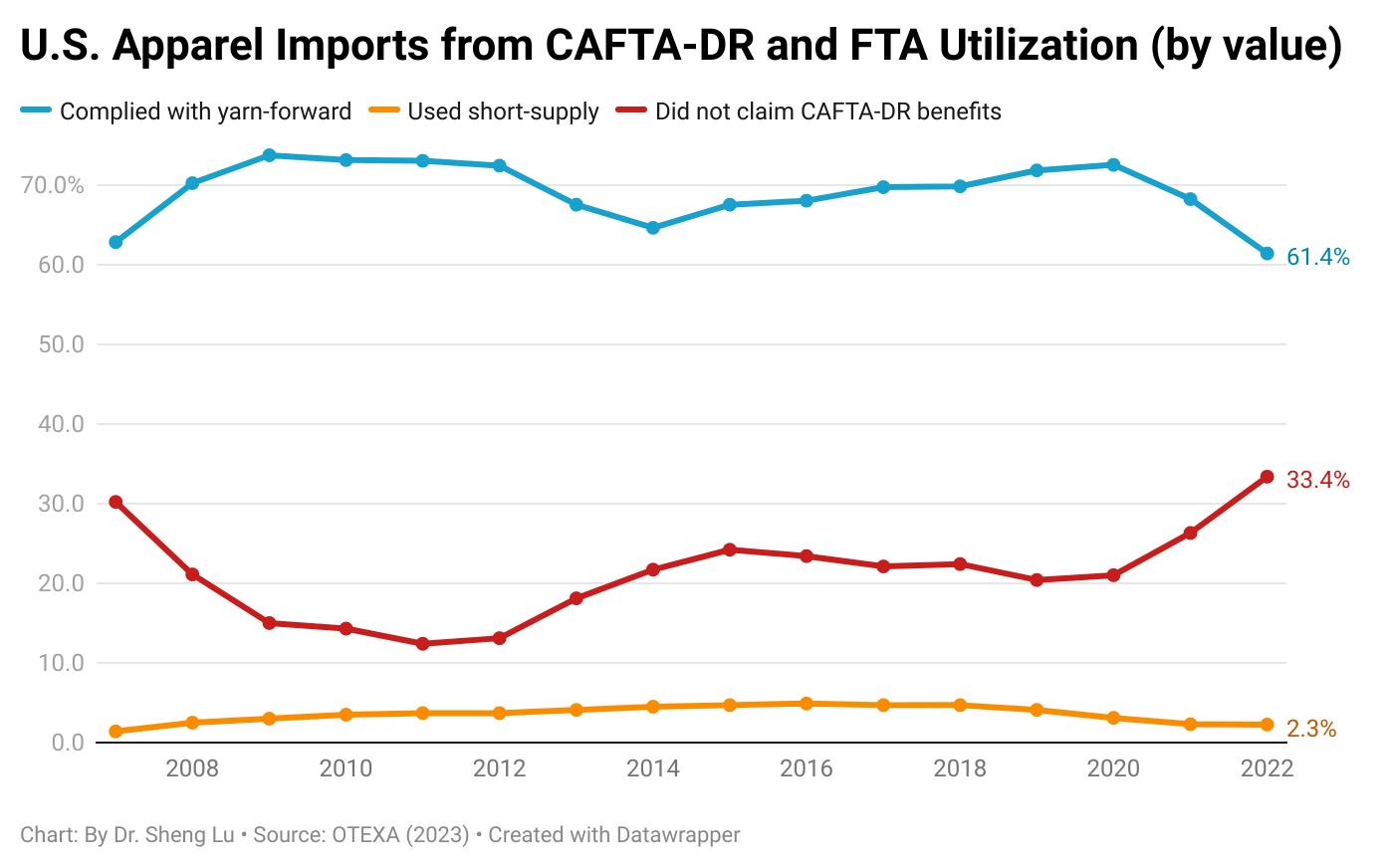

Another problem is the underutilization of the trade agreement. For example, CAFTA-DR’s utilization rate for US apparel imports consistently went down from its peak of 87% in 2011 to only 74% in 2021. The utilization rate fell to 66.6% in 2022, the lowest since CAFTA-DR fully came into force in 2007. This means that as much as one-third of US apparel imports from CAFTA-DR did NOT claim the agreement’s preferential duty benefits. Thus, regarding how to practically grow US fashion companies’ near-shoring, we could expect more public discussions and debates in the new year.

The session intends to facilitate constructive dialogue regarding the latest progress, challenges, and opportunities for achieving more sustainable and socially responsible apparel sourcing in the Post-COVID world. The session will offer a unique opportunity to hear directly from leading fashion brands and retailers regarding 1) fashion companies’ latest sourcing practices against the evolving business environment and their impacts on due diligence; 2) fashion companies’ new efforts and innovative projects to achieve more sustainable and socially responsible apparel sourcing; 3) opportunities and challenges to further improve sustainability and social responsibility in apparel sourcing in the post-COVID world. In addition, the session will be highly relevant and informative to all stakeholders in the fashion apparel business community, civil society, international organizations, academia, and policymakers.

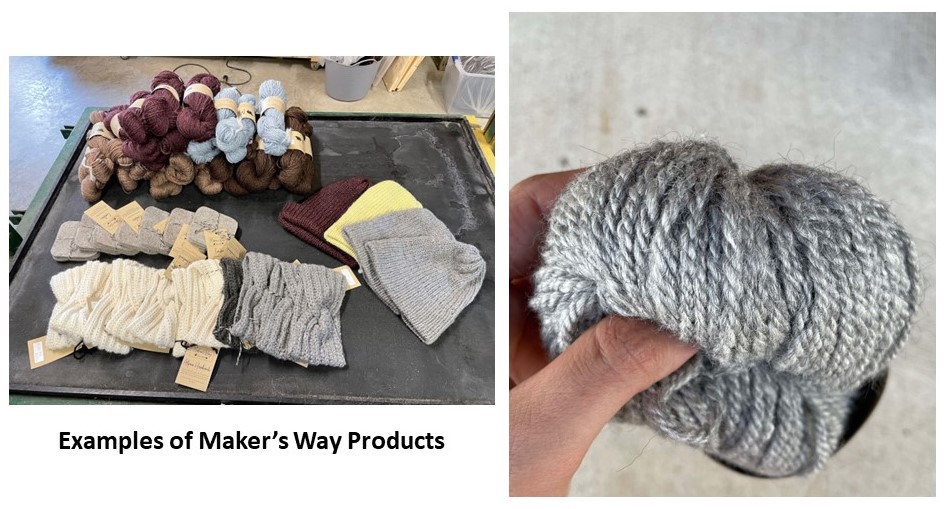

Elizabeth Davelaar is a Co-Owner of Maker’s Way Fiber Mill in Brandon, SD, which opened in October 2021. The mill is a family-run business, with Elizabeth’s sister, Erin, and her mother, Kari, as other co-owners. Elizabeth began her career in the fashion industry at the University of Minnesota, where she graduated with a BS in Apparel Design from the College of Design. She then went to the University of Delaware, where she graduated with an MS in Fashion and Apparel Studies and a Graduate Certificate in Sustainable Apparel Business.

Elizabeth served as a project manager for a non-profit fashion brand in St. Louis and taught sewing to immigrant women in St. Louis and women in Ethiopia. She then moved to Vi Bella Jewelry in Sioux Center, IA, working her way from Shipping Manager to VP of Operations, Sustainability and Design. She then opened Maker’s Way Fiber Mill in 2021 with her family and has been working with local fiber producers to grow the yarn industry in South Dakota and surrounding areas.

Interview Part

Sheng: What inspired you to start your fiber mill business? What makes it special and exciting?

Elizabeth: The mill was born out of the need to solve a problem. I became interested in natural dye at the University of Delaware under Professor Cobb. Once I moved back to the area where I grew up, COVID hit, and I was able to dive deeper into the natural dye and use local plants as a dye source. This also led to being curious about local natural fibers. South Dakota isn’t a state that grows cotton, and the hemp industry is currently small, but it has an abundance of sheep. According to statistics from the US Department of Agriculture, South Dakota has 235,000 sheep and is home to one of the nation’s largest wool co-ops. However, there are only 2 working fiber mills in the area that provide custom processing, which makes yarn made from local fiber very hard to find.

This led to the opening of Maker’s Way Fiber Mill. We are a full-service, custom fiber mill and make yarn, felt, roving, and home goods products from primarily wool and alpaca fiber. Approximately 90% of our time is spent processing for clients who own the animals and use the yarn themselves or sell it, with the other 10% processing yarn that we sell online via our website and in-person at events. The vast majority of our customers are local (within 4-5 hrs) and sell locally to crafters. We take pride in knowing where the fiber we use comes from, sourcing from local farms or using fiber from vintage or second-hand sources.

Hats made from 80% alpaca/20% Wool (both sourced from SD) with a small amount of recycled sari silk blended in. Photo courtesy of Elizabeth Davelaar

(Photo courtesy of Elizabeth Davelaar)

Photo courtesy of Elizabeth Davelaar

Sheng: According to Maker’s Way Fiber Mill’s website, sustainability is a critical feature of your products. Why is that, and how do you make your products sustainable?

Elizabeth: We believe that we are stewards of the earth and should be conscious of how the products we make are grown, created, and then how they can be disposed of. The fashion industry, from creating the product to end life, is a huge polluter. The current market for wool is not great for producers, and there isn’t a good avenue for alpaca producers. We work very hard to ensure that our products are sourced from people that we know and trust or are from vintage or second-hand sources. We also work to ensure our products are made from natural fibers, thus they are biodegradable.

We also work to limit the waste in our mill. Although we try our absolute best to reduce loss in the process, each step produces some loss in fiber. This fiber is swept up and either rewashed and added to our Millie line or added to our bird nest starters. The Millie line is yarn spun up from the scraps, and we end up running about four batches of this a year. Each batch is unique because of the different blends of fiber we run. The bird nest starters use fiber that either falls out of our carder or is swept off the floor. These are then put outside in the spring for birds to use for nesting. The fibers are short enough that the baby birds don’t get tangled in them as they would with yarn and because they are natural animal fibers, the nests will biodegrade, unlike acrylic yarns that are sometimes used.

Photo courtesy of Elizabeth Davelaar

Sheng: Maker’s Way Fiber Mill’s products are 100% locally made in South Dakota. From your perspective, what are the opportunities and challenges for manufacturing textiles in the US today?

Elizabeth: I see two big challenges in the natural animal fiber side of the U.S. textile industry: Lack of consumer knowledge of where clothing comes from and lack of infrastructure. But both also present big opportunities!

First, we have found with our mill that people don’t have a good understanding of how many steps there are in creating yarn in general, let alone clothing. We have people who question our pricing because they don’t understand what it means to make yarn in the United States. From start to finish, it takes eight different steps to get raw fiber from producers to yarn ready to sell. Our consultations for new clients tend to be very educational because even fiber producers don’t necessarily know all the steps. As we open the mill for tours and talk to people at events, they start to understand and respect how much work is behind the yarn we create, and that is when we see buy-in – when people start to see the whole process, as well as the people.

The second challenge I see is the overall lack of infrastructure. We are one of approximately 200 small-scale / artisan-style mills in the country (this number is approximate – there is not a good database) and do not run near the quantity compared to the larger manufacturers. As of 2018, there aren’t any small-scale fiber mill equipment manufacturers in the US, so all of the equipment available to us is either used or has to be imported from Canada or Italy. Wait time for most small producers to get their fiber made into yarn is approximately 8-12 months at many mills, some run up to 18 months out. Our mill currently runs about 6 months out and we have been open for just over a year.

For producers who want to sell their wool to larger manufacturers and not have it custom processed, as far as our research has shown, there is one large-scale scouring (wool washing) facility in the states and most of the large-scale spinners use fiber from this facility to spin into yarn and then send the fiber off to other finishing companies for knitting. Otherwise, all of the wool is shipped overseas, and producers are earning approximately $1.66/lb of wool (in 2020). We have heard of many producers that have stockpiles of wool because they are waiting for higher wool prices. Coops also won’t accept wool that isn’t white, so all dark colors of wool get thrown away as there isn’t a market for it.

We also see this as an opportunity. We have noticed the “buying local” trend extending past food also to include yarn. People also see value in making their own clothing and being intentional through knitting/crocheting. There is a growing market for it. We have also seen some demand for the addition of another large-scale scouring facility that could meet the needs for wool insulation and other home applications.

Sheng: Like other fashion programs in the US, most of our FASH students take job opportunities from fashion brands and retailers, not necessarily textile mills. How to raise the young generation’s interest in pursuing a career in textile and apparel factories? Do you have any suggestions?

Elizabeth: I definitely never intended to start a fiber mill when I was in school. I only took one textile class and am pretty sure only one of my design projects used wool. UD was really what fed the sustainability bug in me and I started to realize that sustainability starts at the very beginning of the lifecycle of clothing. Whether or not something can be biodegradable, recyclable, or repurposed starts with what fiber makes up the clothing. UD also showed me how global apparel is and how much carbon footprint it makes.

Working in a fiber mill is not an easy job. It is dirty, we tend to put in long days, and we are constantly learning new things. I am a very hands-on person, and I love being able to create things from nothing, so this job is a great fit for me. The part I loved most about being in design school was being able to create things, and my current job is that all day, every day. We split the mill into “zones” and between myself, Erin and our mom, we all specialized in a specific part of the process. I am in charge of skirting and cleaning fleeces, which means cleaning off all of the hay and visibly dirty areas (aka manure) and then washing the fiber in 140-180 degree water to get the dirt and lanolin out of the fleece. I then pick and card the fiber, which opens up and organizes the fiber into a long tube that is then drafted, spun, plied, and put into skeins. While most days tend to include the same things, each day is never the same as the last. Each animal fleece we run acts differently, so we are always learning new and better ways to run the equipment we have. It is challenging but also a labor of love. Because we work directly with producers, we know the names of most of the animals and love knowing that their fleeces are being used instead of being discarded! We also love connecting with local people who love purchasing from local producers and makers.

Photo courtesy of Elizabeth Davelaar

One of the biggest things I believe fashion programs can do to help open up students to different options in the fashion industry is to expose them to different opportunities and allow them to follow whatever passion they have and emphasize that there isn’t a “right” path in the industry. My classes opened me up to labor issues around the world and that then led me to Delaware. And the opportunities I was given at UD to follow my passions are a huge reason I am doing what I am doing now. One of the things I think UD does right is having many different professors with varying backgrounds in the FASH department and I think other universities would do well to implement that too.

Sheng: Any other key issues or industry trends you will watch in 2023?

Elizabeth: One of the key trends we are watching is the local craft movements and knowing where your clothing comes from. We saw a crafting resurgence happen during COVID and people are still pickup up their knitting needles and crochet hooks to create items to wear and love. We also see some carryover of the local food scene into the local fiber scene. We believe that this will continue to grow!

This study aims to understand western fashion brands and retailers’ latest China apparel sourcing strategies against the evolving business environment. We conducted a content analysis of about 30 leading fashion companies’ public corporate filings (i.e., annual or quarterly financial reports and earnings call transcripts) submitted from June 1, 2022 to December 31, 2022.

The results suggest several themes:

First, China remains one of the most frequently used apparel sourcing destinations. For example:

Express says, “The top five countries from which we sourced our merchandise in 2021 were Vietnam, China, Indonesia, Bangladesh and the Philippines, based on total cost of merchandise purchased.”

According to TJX, “a significant amount of merchandise we offer for sale is made in China.”

Children’s Place says, “We source from a diversified network of vendors, purchasing primarily from Vietnam, Cambodia, Indonesia, Ethiopia, Bangladesh, and China.“

Ralph Lauren adds, “In Fiscal 2022, approximately 97% of our products (by dollar value) were produced outside of the US, primarily in Asia, Europe, and Latin America, with approximately 19% of our products sourced from China and another 19% from Vietnam.

However, many fashion companies have significantly cut their apparel sourcing volume from China. More often, China is no longer the No.1 apparel sourcing destination, overtaken by China’s competitors in Asia, such as Vietnam.

According to Lululemon, “During 2021, approximately 40% of our products were manufactured in Vietnam, 17% in Cambodia, 11% in Sri Lanka, 7% in China (PRC), including 2% in Taiwan, and the remainder in other regions… From a sourcing perspective, when looking at finished goods for the upcoming 2022 fall season, Mainland China represents only 4% to 6% of our total unit volume.”

Levi’s says, “The good thing about our supply chain is we’ve got truly a global footprint. We don’t manufacture a whole lot in China anymore. We’ve been slowly divesting manufacturing out of China, if you will, and kind of playing our chips elsewhere on the global map… Less than 1% of what we’re bringing into this country, into the US, less than 1% of it is coming from China.”

Adidas says, “In 2021, we sourced 91% of the total apparel volume from Asia (2020: 93%). Cambodia is the largest sourcing country, representing 21% of the produced volume (2020: 22%), followed by China with 20% (2020: 20%) and Vietnam with 15% (2020: 21%).”

Victoria’s Secret says, “On China, China is a single-digit percentage of our total inflow of merchandise. We’re not particularly dependent on China at all.”

Nike: “As of May 31, 2022, we were supplied by 279 finished goods apparel contract factories located in 33 countries. For fiscal 2022, contract factories in Vietnam, China and Cambodia manufactured approximately 26%, 20% and 16% of total NIKE Brand apparel, respectively“

Meanwhile, fashion companies still heavily use China as a sourcing base for textile raw materials (such as fabrics). For example:

Columbia Sportswear says it sources most of its finished products from Vietnam, but “a large portion of the raw materials used in our products is sourced by our contract manufacturers in China.”

Likewise, Puma says, “90% of our recycled polyester comes from Vietnam, China, Taiwan (China) and Korea.”

Guess says, “During fiscal 2022, we sourced most of our finished products with partners and suppliers outside the U.S. and we continued to design and purchase fabrics globally, with most coming from China.”

Lulumemon says, “Approximately 48% of the fabric used in our products originated from Taiwan, 19% from China Mainland, 11% from Sri Lanka, and the remainder from other regions.”

Second, Western fashion companies unanimously ranked the COVID situation as one of their top concerns for China. Many companies reported significant sales revenue and profits loss due to China’s draconian “zero-COVID” policy and lockdown measures. For example,

Tapestry says, “For Greater China, sales declined 11% due to lockdowns and business disruption… as a result, we have tempered our fiscal year 2023 outlook based on the expectation for a delayed recovery in China.”

Adidas says, “With Great China… we continue to see several market-specific challenges that are affecting our entire industry. The strict zero COVID-19 policy with nationwide restrictions remains in place amid more than 2000 daily new COVID-19 cases in November. As a consequence, offline traffic is subdued due to the imminent risk of new lockdowns.

Under Armour says, “Ongoing impacts of the COVID-19 pandemic and related preventative and protective actions in China…have negatively impacted consumer traffic and demand and may continue to negatively impact our financial results.”

VF Corporation says, “The performance in Greater China…continues to be impacted by widespread rolling COVID lockdowns and restrictions as well as lower consumer spending.”

Puma says, “COVID-19-related restrictions are still impacting business in Greater China, and higher freight rates and raw material prices continue to put pressure on margins.”

Notably, despite China’s most recent COVID policy U-turn, most fashion companies expect market uncertainties to stay in China, at least in the short run, given the surging COVID cases and policy unpredictability. For example:

PVH says, “While we remain optimistic about our business in China, it continues to be a challenging environment as restrictions have once again intensified in the fourth quarter of 2022.”

Nike says, “So we’ve taken a very cautious approach in our guidance to China, given the short-term uncertainties that are there.”

Abercrombie & Fitch also listed China’s COVID situation as one of their top risk factors, “risks and uncertainty related to the ongoing COVID-19 pandemic, including lockdowns in China, and any other adverse public health developments.”

Third, fashion companies report the negative impacts of US-China trade tensions on their businesses. Also, as the US-China relationship sours, fashion bands and retailers have been actively watching the potential effect of geopolitics. For example,

Express says, “recent geopolitical conditions, including impacts from the ongoing conflict between Russia and Ukraine and increased tensions between China and Taiwan, have all contributed to disruptions and rising costs to global supply chains.”

When assessing the market risk factors, Chico’s FAS says, “our reliance on sourcing from foreign suppliers and significant adverse economic, labor, political or other shifts (including adverse changes in tariffs, taxes or other import regulations, particularly with respect to China, or legislation prohibiting certain imports from China)”

Adidas holds the same view, “In addition, the challenging market environment in China had an adverse impact on the company’s business activities… Additional challenges included the geopolitical situation in China and extended lockdown measures.”

Macy’s adds, “At this time, it is unknown how long US tariffs on Chinese goods will remain in effect or whether additional tariffs will be imposed. Depending upon their duration and implementation, as well as our ability to mitigate their impact, these changes in foreign trade policy and any recently enacted, proposed and future tariffs on products imported by us from China could negatively impact our business, results of operations and liquidity if they seriously disrupt the movement of products through our supply chain or increase their cost.”

Gap Inc. says, “Trade matters may disrupt our supply chain. For example, the current political landscape, including with respect to U.S.-China relations, and recent tariffs and bans imposed by the United States and other countries (such as the Uyghur Forced Labor Prevention Act) has introduced greater uncertainty with respect to future tax and trade regulations.”

QVC says, “The imposition of any new US tariffs or other restrictions on Chinese imports or the taking of other actions against China in the future, and any responses by China, could impair our ability to meet customer demand and could result in lost sales or an increase in our cost of merchandise, which would have a material adverse impact on our business and results of operations.”

Additionally,NO evidence shows that fashion companies are decoupling with China. Instead, Western fashion companies, especially those with a global presence, still hold an optimistic view of China as a long-term business opportunity. For example:

Inditex, which owns Zara, says, “we remain absolutely confident about our opportunities there (in China) in the medium to long term. Fashion demand continues to be strong in China. For sure it will remain a core market for us for Inditex.”

Ralph Lauren says, “China provides not only the successful blueprint for our elevated ecosystem strategy globally, it also represents one of several geographic long-term opportunities for our brand…We continue to see near and long term brand opportunities in China.”

Lululemon says, “On China, we remain very excited…we remain very, very excited about the potential and the role that will play in quadrupling our international business with Mainland China.”

Nike says, “We have remained committed to investing in Greater China for the long term.”

Adidas says, “On China, clearly, we believe in as a midterm opportunity in China… And then when the market opens up (from COVID), we believe, the western brand is well-positioned in China again, and we can start growing significant in China again.”

Meanwhile, Western fashion companies plan to make more efforts to localize their product offer and cater to the specific needs of Chinese consumers, especially the young generation. The “Made in China for China” strategy could become more popular among Western fashion companies. For example,

PVH says, “So, I think in general, our production in China is heavily oriented to China for China production. I think for us generally speaking, the biggest impact of the shutdowns that we’ve seen across Shanghai and Beijing has really been focused on the impact to our China market.”

Likewise, Levi’s says, “We’re manufacturing somewhere in the neighborhood of 5% of our global production is in China, and most of it staying in China.“

Hanesbrands says, “we’re committed to opening new stores, and that’s continues to go well, despite, the challenges that are there. Looking specifically at Champion, we continued our expansion in China adding new stores in the quarter through our partners.”

H&M says, “we still see China as an important market for us.”

According to Hugo Boss, “Thanks to overall robust local demand, revenues in China in 2021 grew 24% as compared to 2019.”

VF Corporation adds, “China is a significant opportunity…(We are) really pushing decision-making into the regions and providing more and more latitude for local-for-local decision-makings around product, around storytelling, certainly staying within the confines or the framework of the brand strategy, but really giving more freedom and more empowerment to the regions.”

Julianne Bartolotta is the founder and CEO of the apparel brand Julianne Bartolotta (JB).

Grew up in Huntington, New York, Julianne began her fashion career by double majoring in Apparel Design and Fashion Merchandising at the University of Delaware. After graduating in Spring 2018, Julianne joined Saks Fifth Avenue’s Private Label Brands as a Product Development Assistant Manager. Julianne was involved in designing for the men’s brands, Saks Fifth Avenue Collection and Saks Fifth Avenue Modern. Although a relatively small team, the experience allowed Julianne to “wear many hats” and control the entire design process from start to finish. Julianne and her team also designed for many product categories, including sportswear, tailored clothing, dress shirts, swim, and personal furnishings, to name a few.

After two years on the men’s team, Julianne moved over to help rebrand and relaunch Saks Fifth Avenue’s women collections. Her designs were adopted for Fall 21 collection and the experience allowed her to get familiar with the whole design process. This project also gave Julianne the knowledge and courage to move to the next career level.

In January 2022, Julianne left her dream job at Saks and started to build her own apparel brand. Officially launched in November 2022, Julianne Bartolotta has become a rising star in the luxury fashion world.

Sheng: Thank you so much for speaking with us,Julianne! What inspired you to start your apparel company? What makes it special and exciting?

Julianne: When Covid-19 hit New York in March 2020, I was furloughed from my job at Saks like many peers. I remember being at home when the house phone rang, and it was my dad calling to tell my mom and me that his nursing home ran out of masks and he needed us to sew 200 cloth masks for the nurses and staff. My mom and I ran to the only store open, Walmart, to buy fabric. We then set up a folding table in my kitchen and got to sewing. So we decided to choose a fabric with bright, colorful designs because we thought it would make people happy.

My dad got so many responses from the residents and the staff, saying that they loved the masks. They made the residents feel more comfortable and at ease when seeing their nurse, because it was as if wearing the mask was like wearing a smile.

After seeing the positive impact of my masks on the residents and staff, I decided to begin offering other mask designs on an Etsy Shop. My Etsy took off, and I started experimenting with scrunchies, headbands, swimsuits, and dresses, all sewn by me.

When I returned to Saks, I found myself craving the lifestyle of an entrepreneur. I enjoyed being my own boss and making creative decisions. Seeing people wear my designs and having a 5-star average on Etsy pushed me to take a leap of faith and pursue starting my own business. I officially gave my resignation in December of 2021 and began January 2022 with my focus solely on my brand.

Today, Julianne Bartolotta (JB) is a women’s Ready-to-Wear brand, offering a mini capsule collection each season. We offer sweaters, dresses, skirts, shorts, blouses, and even catsuits. My target audience is women ages 25-45, who live in urban and suburban areas that value fashion and look forward to dressing up on the weekends. She does not mind spending a bit more on a dress because she is excited to wear something unique, trendy, and well-made. We are a woman-owned, women-run, family business, where my mom is my Chief Operating Officer (COO), and my sister is one of my fit and marketing models.

Every item in the collection is designed by me and made in Italy, using the same manufacturers as other household luxury brands. Each style is meant to act as a “statement piece,” meaning there is something statement-worthy about the design, color, fabrication, or buttons. During my time at Saks, I learned from studying selling reports that the styles with “statement-worthy” details had the highest sell-throughs across most brands. I learned that women want to show off their cool clothes! They would rather spend $250 on a dress that stands out than $250 on a dress that probably won’t get her much attention.

My intention with this collection is to make women feel like a light in a dark room, just as my masks did during such a scary and unpredictable time. Clothing is how we portray ourselves to the world. My brand prides itself on making quality clothing, with statement-worthy designs, to show the world a woman’s femininity and confidence. With JB, the clothing speaks for itself, so you don’t have to!

Sheng: All your companies’ products are “Made in Italy.” Why is that?

Julianne: While at Saks, we used factories in Italy, China, Spain, and other countries worldwide. When President Trump imposed higher tariffs on China, it pushed us to revisit our supplier base. We eventually decided to move almost everything to Italy because the tariff duties were lower and the “Made in Italy” label is very desirable. People love clothing made in Europe, especially Italy. Italian factories pride themselves on their craft. They are very artisanal and view fashion as art. The factories are also smaller, with about 25-50 people working on the main floor. Because of this, the garments are being handled by fewer people, so the workers will spend a lot of time taking care of each garment. So if you were to compare this to factories in Asia, for example, there would typically be hundreds of workers on the main floor, and each worker would have a particular job, sewing a specific part of the garment and passing it on to the next worker (i.e., productin line).

When branching off to start my own business, I took this sourcing knowledge with me and chose to work with Made in Italy factories. Because the factories in Italy are smaller, they are also able to offer lower minimums. Being a starting-out designer, it’s important not to over-buy. You don’t want to end up in a situation where you are sitting on inventory and can’t move it.

The “Made in Italy” label is also an homage to my Italian heritage. I am actually a dual citizen, so I have American citizenship as well as Italian citizenship. I have family in Italy that I have visited in recent years and communicate with regularly. Having my garments made in Italy is a way for me to give recognition to my family’s roots and uphold a standard of luxury at the same time.

When sourcing fabric for my garments, it would be typical to attend fabric shows in Milan and Florence to pick the best fabrics for my designs. Because of Covid, I could not travel to attend these shows, so I had yarn books and color cards sent to me instead. I was able to get pricing and pick the best suitable fabrics that way, but in the future, I plan to go and network with the mills as well.

Sheng: Can you share with us your sourcing practice? For example, what are your vendor selection criteria? What does the importing process look like?

Julianne: Currently I work with three factories in Italy, all specializing in different realms. One specializes in knitting sweaters, one works with woven fabrics, and the other works with jersey knits and stretch materials. I selected these factories because they were able to offer me low minimums. I was also given net payment terms, so I don’t have to pay my factories upfront for my clothes, which allows me to use selling time to help pay for the invoices.

When selecting my factories, I also made sure to know what other brands they work with. Big retailers like Saks have special ethics codes in place that the brand’s factories must comply with to sell to their stores. This includes ensuring that the factories don’t overwork their staff, the work environment conditions are safe, and the workers are compensated appropriately for their work. I made sure to use only reputable factories that produce for other luxury brands so that I comply with the same standards.

When I am working on costing for my styles, I have to contact my broker for each item’s landing factor to get my landed cost. A landing factor is a number that includes the exchange rate and duties on a specific style based on the type of article of clothing it is (blouse, jacket, pants, etc.), whether it is woven or knit, what the fabrication is, and where it is coming from. The landing factor for an Italian wool sweater could be different from the landing factor on an Italian wool coat. Landing factors usually range from .5 to 1.9. For example, if an item has a first cost of 30 euros and a landing factor of 1.5, the landed cost would come to $45. Landing factors can change over time, so it’s important that I check in with my broker every season to make sure I know what to expect when it comes time to ship.

My landing factors do not include the shipping cost. Because my orders are so small, and my production timeline is shorter than other big brands, it is in my best interest to air my goods. This isn’t the case for most brands, as airing goods can become quite costly. Usually, goods would be shipped by boat, but when Covid hit, there were fewer workers to unload the cargo ships in New York, which caused many retail orders to become very delayed. I wanted to avoid this altogether, and since my boxes are small, I chose to air my shipments instead. As I work on my production timeline and grow my business, I will probably have to move towards shipping my goods by boat.

Sheng: Regarding the apparel business environment in 2023, what are the opportunities and challenges? What trends shall we watch closely?

Julianne: The apparel industry right now is tough, butthere are still opportunities for fashion businesses. Inflation has caused many people to rethink how much they are willing to spend on clothing. People want to feel like they will get their money’s worth on their purchases across the board. This is where social media marketing comes into play. If you can create a strong social media presence, and gain credibility through the right PR tactics, people will be more inclined to shop for your brand. Influencers are becoming modern world celebrities. If you see Danielle Bernstein wearing a dress from a small named brand, you suddenly give the brand credibility and want to check out their Instagram. With more people joining Tiktok, Instagram’s algorithm shifting towards reels, and influencers gaining more popularity, there are plenty of opportunities to spread the word; brands need to take advantage of these social media tools in the most compelling way.

It is becoming more common for people to start a side hustle in today’s world. Many people work from home and have the extra time and effort to put towards their small business. This means that the market for fashion startups is becoming saturated, but if you can create a brand that stands out from the rest, and put out engaging social media content, your audience can really grow and take off.

I would pay attention to how big and small brands are trying to take advantage of Tiktok and Instagram. Big brands are joining the Tiktok and Reels bandwagon and putting out more relatable content. They are using influencers, giving them discount codes to share, and sending them PR packages to show off on social media. It’s also interesting to see how small startup brands can utilize the same influencers and tactics to bring awareness to themselves. Social media creates a stage where small and big brands can coexist and compete for the same customers. Through social media, small brands can become more relevant, and big brands can try to stay relevant.

Sheng: Any reflections on your experiences at UD and FASH? What advice do you have for our current students who are preparing for their careers after graduation?

Julianne: Looking back on my college experience at UD and in the Fashion and Apparel Department(FASH), it feels like it was just yesterday! I double majored in Apparel Design and Fashion Merchandising, so I took a majority of the fashion classes offered, but if I could give any advice, I would say to be involved as much as you can. Utilize the amazing learning and career development opportunities that UD FASH offers you! Also, interning as much as possible– whether you get paid or not, it could be a valuable experience. I would suggest interning in a few different fields in fashion (if you can) to see what you like best before applying to jobs. For example, I had market week internships, product development internships, and fashion design internships, and I worked in retail. These experiences helped me decide what I liked and didn’t like.

Also, it is competitive out there, so don’t get discouraged! For example, the interview with Saks was a long process but I am so grateful that it worked out the way it did.

If you are a designer and want to start your own business, I would HIGHLY recommend working for someone else first. When you work for someone else, whether a big brand or a small startup, you learn the business’s ins and outs and network. It is much easier to start a business when you have connections then trying to start a business having to cold call vendors. Starting a business is also much easier when you understand the production calendar. Knowing what needs to be done and in what order will avoid a lot of mistakes! Put your time in, learn and grow, and you will be able to achieve great things!

Mango is a fashion company based in Barcelona, Spain that was founded in 1984 by brothers Isak Andic and Nahman Andic. The company has grown significantly since its inception and now has over 2,700 stores in 109 countries worldwide. Mango is known for its trendy and high-quality clothing, which is targeted toward young women.

One of the critical factors in Mango’s success has been its ability to stay current and relevant in the fast-paced fashion world. The company regularly collaborates with top designers and influencers to create unique and fashionable collections that appeal to its target audience. Mango also closely monitors emerging trends and adapts its collections accordingly.

Besides clothing, Mango also offers accessories, such as bags, shoes, jewelry, and a home collection. The company has a solid online presence, with an e-commerce website that allows customers to shop from anywhere in the world.

In December 2022, Mango announced the Sustainable 2030 strategy, which “aims to move towards the full traceability and transparency of its value chain, in order to continue with the process of auditing its suppliers and ensuring that appropriate working conditions are being fulfilled for the workers in the factories the company works with around the world.” As part of the strategy, Mango will “focus its efforts on moving towards a more sustainable collection, prioritizing materials with a lower environmental impact and incorporating circular design criteria, so that by 2030 these will predominate in the design of its products and all its fibers will be of sustainable origin or recycled.”

Mango’s Apparel Sourcing Strategies (as of December 2022)

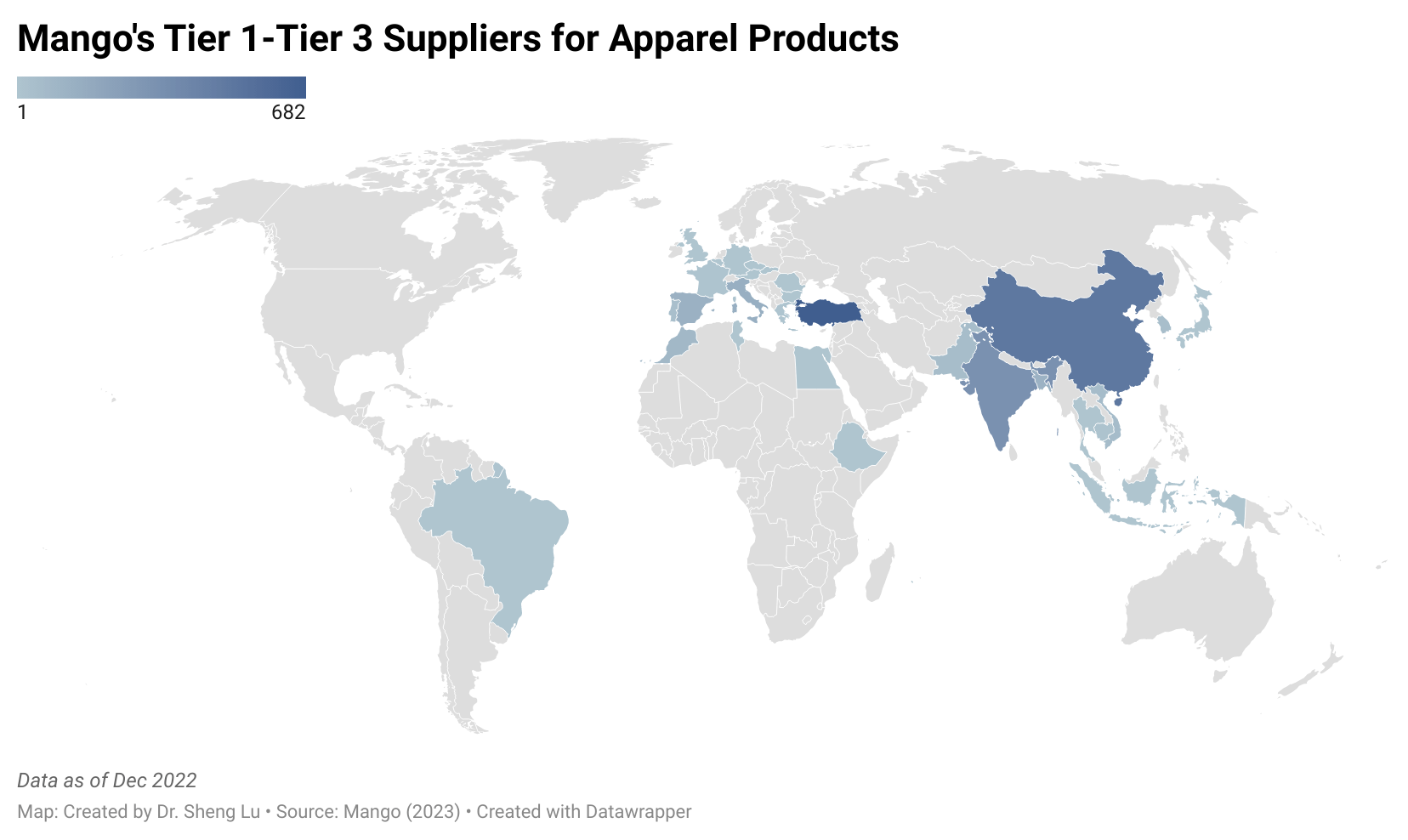

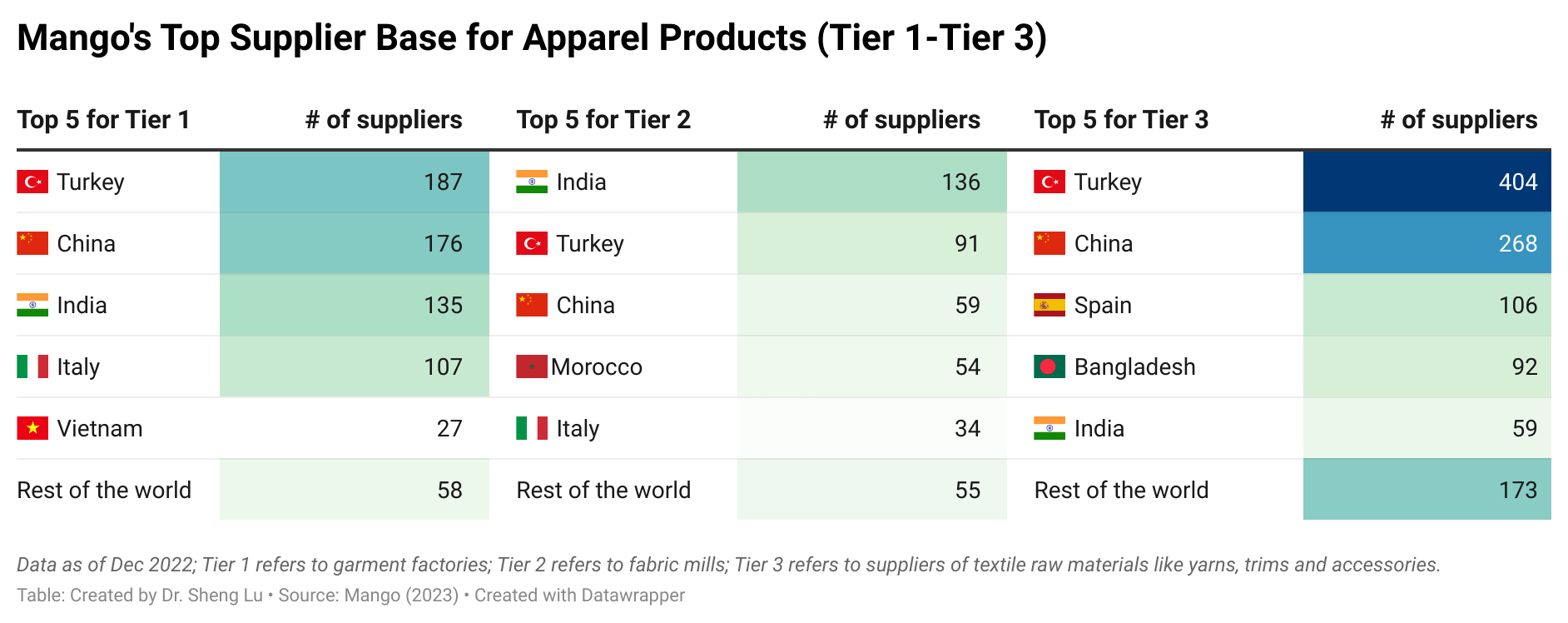

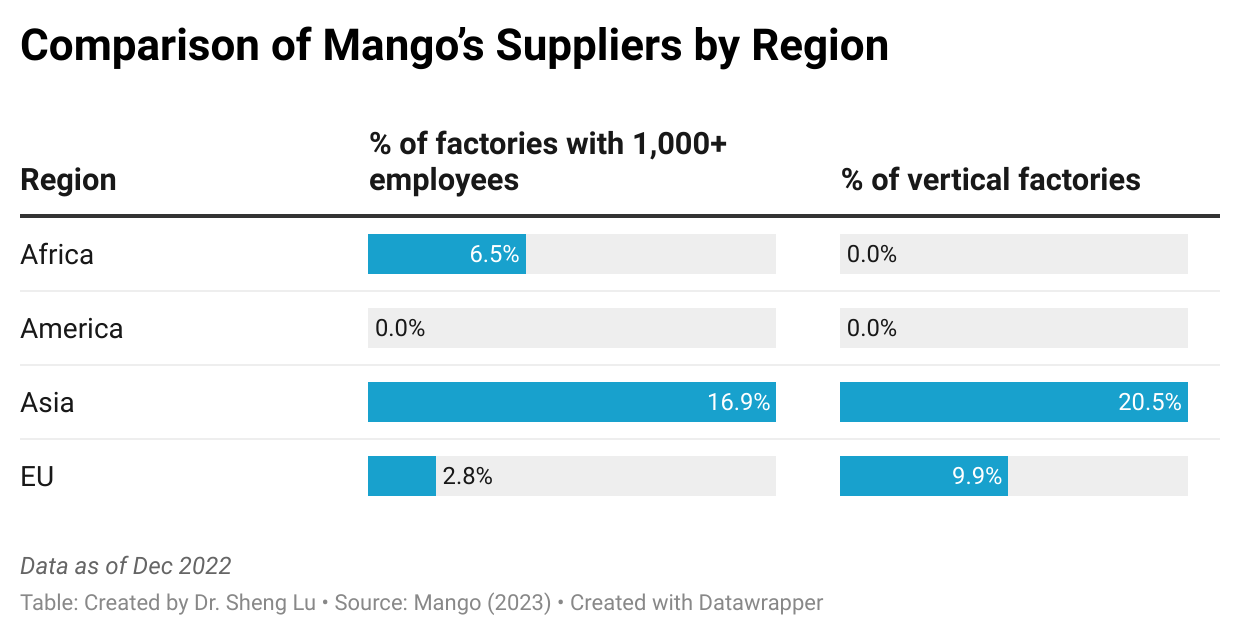

First, Mango adopted a sophisticated global sourcing network for its apparel products. Specifically, Mango’s apparel supply chain involves 1,878 Tier 1, Tier 2, and Tier 3 factories in 29 countries worldwide. About 31% of these factories produce garments (Tier 1), 19% supply fabrics (Tier 2), and 49% provide textile raw materials like yarns and accessories (Tier 3). Further, about 407 factories (or 21%) have vertical production capability (e.g., making both finished garments and textile inputs).

Second, like many EU fashion companies, near-shoring from the EU and Turkey is a critical feature of Mango’s apparel sourcing strategy. For example, about 44.8% of Mango’s Tier 1 garment suppliers were EU based (including Turkey), whereas Asia suppliers only accounted for 54%. Likewise, about 34% of Mango’s Tier 2 fabric suppliers and nearly half of its Tier 3 yarn and accessories suppliers were also EU based. The result reflects the EU’s intra-region textile and apparel trade patterns, supported by the region’s relatively complete textile and apparel supply chain. In comparison, US fashion companies typically source more than 80% of finished garments from Asia, and most of these garments also use Asia-based textile raw materials.

Third, measured by the number of suppliers, Mango’s top Tier 1 apparel production bases include Turkey (187 factories), China (176 factories), India (135 factories), and Italy (107 factories). Industry sources further indicated that between 2021 and 2022, Mango primarily sourced from Turkey and India for Tops (69% and 78%, respectively). Mango’s imports from China and Italy were more diverse in product categories (e.g., dresses, outwear, bottoms, and swimwear). On the other hand, Mango’s apparel imports from Italy were much higher priced ($107 retail price on average) than those from the other three countries ($38-41 retail price on average).

Fourth, the factory size and vertical production capabilities of Mango’s suppliers seem to vary by region. Notably, Mango’s Asia-based suppliers are more likely to be large-sized (with 1,000+ employees) and offer vertical production (e.g., making both finished garments and textile input). Mango’s Africa and America-based suppliers were relatively small-sized or lacked vertical integration.

This study explored the survival strategies of apparel manufacturing in a high-wage developed economy using “Made in Ireland” as a case study. Based on a statistical analysis of 4,000 apparel items for sale in the retail market from January 2018 to December 2021, the study found that:

First, unlike the conventional views like the factor proportion trade theory and the global value chain theory, the study’s results showed that garment manufacturing did NOT disappear in Ireland as a high-wage developed country. Notably, garments “Made in Ireland” demonstrated many unique attributes, such as:

statistically more likely to target luxury and high-end markets than foreign-made apparel imported into Ireland;

statistically more likely to highlight their Irish cultural heritage and mention keywords such as “traditional,” “centuries-old,” “craftsmanship,” and “historical” in the product description;

statistically more likely to focus on manufacturing specific product categories with a world reputation, including jumpers and kilts;

statistically less likely to be seen in categories with an abundant supply from lower-cost imports, such as bottoms;

In other words, economic theories need to incorporate non-price competition factors and better explain the development patterns of a country’s garment sector, particularly in developed economies.

Second, the findings called for a rethink of the strategies supporting the garment-manufacturing sector in a high-wage developed country. Current industry practices and government policies aiming to promote garment manufacturing in a developed country primarily focus on implementing protectionist trade measures (i.e., restricting imports) or investing in modern technologies like automation. However, the study’s findings suggested new approaches. For example, using disaggregated product data at the Stock Keeping Unit (SKU) level, the study indicated that a substantial portion of garments “Made in Ireland” was sold overseas. Thus, promoting exports instead of curbing imports could be a more effective way of expanding garment production in a high-wage developed country.

On the other hand, the popularity of “Made in Ireland” jumpers and kilts in the world marketplace suggested that garment manufacturers in a high-wage developed country could survive their business by leveraging cultural heritage, history, and traditional craftsmanship instead of fancy new technologies. Likewise, to a certain extent, the value of maintaining garment manufacturing in a high-wage developed country in the 21st Century may not necessarily be about replacing imports, improving “speed to market,” or creating jobs but preserving a country’s unique cultural heritage and history.

Third, the study’s findings revealed the challenges facing garment manufacturers in a high-wage developed country like Ireland. For example, garments “Made in Ireland” were more likely to be sold with a discount, implying their price competition with foreign-made imports might not be entirely avoidable despite all the efforts from targeting the niche markets to differentiating product assortments.

On the other hand, garments “Made in Ireland” often targeted the high-end market, requiring the workforce to obtain demanding skills such as advanced sewing, craftsmanship, and a deep understanding of the Irish culture. However, the aging workforce and the shortage of skilled labor, a common problem facing developed countries, could also prevent the expansion of apparel manufacturing in Ireland in the long run. Thus, prompting the traditional Irish culture and apparel production craftsmanship, especially to attract the young generation to garment factories and be willing to pursue a career there, would be critical for sustaining the garment manufacturing sector in Ireland and other high-wage developed countries.

Background

Ireland has a long history of making garments, and specific categories of apparel “Made in Ireland” are famous worldwide, such as jumpers and kilts. As of 2020 (i.e., the latest data available), about 340 garment factories still operate in Ireland, a notable increase from 293 in 2010 (Eurostat, 2022). Meanwhile, the output of Ireland’s apparel manufacturing sector totaled $68 million in 2020 (measured in value-added), a substantial drop from $142 million ten years ago (Eurostat, 2022).

Meanwhile, export was critical in supporting apparel “Made in Ireland” today. Statistics show that Ireland’s apparel exports totaled $270 million in 2019 before the pandemic, down about 19% from 2005 (UNComtrade). However, over that period, Ireland’s apparel exports to most developed countries enjoyed positive growth, such as Spain (up 151%), the Netherlands (up 4.5%), Germany (up 14.5%), France (up 61.6%), and Japan (up 20.2%). Further, Ireland’s top four largest apparel export markets were all developed Western EU countries (UNComtrade, 2022). Geographic proximity and the specific product structure of Ireland’s apparel exports could be important factors behind these distinct export patterns.

by Miriam Keegan (FASH MS student, Fulbright-EPA scholar) and Sheng Lu

Full paper: Keegan, M. & Lu, S. (2023). Can garment production survive in a developed economy in the 21st century? A study of “Made in Ireland”. Research Journal of Textile and Apparel. (ahead of print) https://doi.org/10.1108/RJTA-09-2022-0113